20

Ingersoll Rand Michael W. Lamach Chairman and CEO 2014 J.P. Morgan Aviation, Transportation & Industrials Conference March 11, 2014

Ingersoll Rand

Michael W. Lamach

Chairman and CEO

2014 J.P. Morgan Aviation, Transportation & Industrials Conference

March 11, 2014

2

Safe Harbor

This presentation includes “forward-looking statements,” which are statements that are not

historical facts, including statements that relate to the mix of and demand for our products,

performance of the markets in which we operate, our share repurchase program including

the amount of shares to be repurchased and timing of such repurchases, our projected

2014 first quarter and full-year financial performance and assumptions regarding our

effective tax rate. These forward-looking statements are based on our current expectations

and are subject to risks and uncertainties, which may cause actual results to differ

materially from our current expectations. Such factors include, but are not limited to, our

ability to fully realize the expected benefits of the completed spinoff and restructuring; global

economic conditions; demand for our products and services; and tax law changes.

Additional factors that could cause such differences can be found in our Form 10-K for the

year ended December 31, 2013 and in our other SEC filings. We assume no obligation to

update these forward-looking statements.

This presentation also includes adjusted non-GAAP financial information which should be

considered supplemental to, not a substitute for, or superior to, the financial measure

calculated in accordance with GAAP. Further information about the adjusted non-GAAP

financial information, including why management believes the information is useful, the

purposes for which management uses the information and reconciliation to the nearest

GAAP measure, is included in financial tables attached to the earnings news release that

can be found at www.ingersollrand.com.

All data for beyond the fourth quarter of 2013 are estimates.

3

Positioning Ingersoll Rand to Deliver

Shareholder Value

Operational

Excellence

Balanced

Capital Allocation

Accelerating

Revenue Growth

Strong, recognized brandsWell positioned in both

geographic and end markets

Sustainable, Profitable Growth and Shareholder Value

Leading market shares

4

• Building capabilities and integrating

business models

• Enhanced innovation capabilities to

deliver growth

• Sustainable operating margin improvement

– operational and functional excellence

• Divested underperforming operations

• Spinout of security businesses to

realize full value

• Significant cash flow generation

• Capital allocation focused on creating

shareholder value – dividend increase and

ongoing share repurchase program

Well positioned to drive future growth and margin expansion

Significant Progress 2009 to 2013

5

Adjusted Operating and EBITDA Margins

2011 2012 2013

Climate 8.8% 9.3% 10.4%

Industrial 14.9% 15.8% 16.0%

Operations 10.2% 10.9% 11.7%

Total 8.7% 9.2% 9.6%

2011 2012 2013

Operating Income EBITDA

8.7% 9.2%

12.0%11.6%

12.3%

9.6%

Steady improvements in operating performance

Adjusted Operating Margins

6

• Leading global brands and market positions

• Strong long-term growth drivers

– Macro drivers are energy efficiency and

sustainability

– Large installed base drives replacement

business and parts and service growth

– Global footprint and exposure to attractive

growing markets

– Organic growth enhanced by innovation

– Market recoveries

• Product/service offering underpinned by shared

technologies, materials, manufacturing,

processes and supply chain

• Continued margin and cash flow improvement

opportunity from operational/functional

excellence

“New” Ingersoll Rand: Foundational Strengths

A world leader in creating comfortable, sustainable and

efficient environments

7

29%

18%15%

19%

14%

5%

Golf

Non-Res

Building,

N. America

Non-Res

Building,

OverseasResidential

Building, Americas

Industrial/

Process

Transport

Refrigeration

End Markets

Climate

76%

Industrial

24%

By Segment

2013 Revenue Profile for New Ingersoll Rand

By Geography

North America

63%

Eur/ME15%

Asia16%

LatinAmerica

2013 Revenue: ~$12.4B

68% New equipment

32% Aftermarket

37% of revenues outside of North America

6%

8

Capitalizing on Market Drivers and Trends

Urbanization

Efficiency and

SustainabilityFood and water

scarcity

Existing Building

Solutions

Food Cost

and Safety

Integrated

Building

Solutions

Regulation

Refrigerant

Market drivers for continued long term growth

Global

Industrialization

9

Core Technical Capabilities Shared Across Businesses

CompressionMaterials and

Chemistry

Thermal

Management

Smart, Wireless

Devices

Remote Services

and Analytics

Vibration/Acoustics

Engineering

Precision

Machining

Modeling and

Simulation

10

Growing Aftermarket Systems & Services

Leveraging large installed base to grow aftermarket

Total Revenues

Commercial HVAC

Industrial

New

Equipment

32%

2005 2013

7% CAGR

2005 2013

5% CAGR

Aftermarket: 32% of

2013 revenues;

$3.9 billion in 2013

~40% aftermarket

revenues

~40% aftermarket

revenues in air

compressors

Tools to improve

technical

mobility and

productivity

11

Delivering Growth Through Innovation

Thermo King™ Precedent

Temperature

Control System

C800 Oil-Free Centrifugal

CompressorSeries™ S CenTraVac

Variable Speed 20 SEER

Residential HVAC system

Intellectual Property

2011 2012 2013

InventionDisclosures

PatentApplications

Grow Technology Leadership: Air Equipment

New products delivering share gain and margin expansion

R-Series Oil-Flooded Rotary Compressors: Platform Completion

R90-110 R132-160 R55-75 R37-45 R15-37

Centac Oil-Free Centrifugal Compressors: Platform Expansion

12

C800

2007 2010

C1000 C2000

Certification of

all platforms

2011 2012 2013

13

Manufacturing Facilities94

6749

2009 2013 2013 PostSpin

Operational Excellence

• Restructuring of manufacturing

footprint largely completed in 2013

• Improved pricing processes: price

exceeded material inflation for 11

consecutive quarters

• Material productivity

– Global procurement

– Centralize spend

• Lean transformation – Operations

– Strong improvement in key

metrics

– Covers 40% of conversion costs

in 2013, 60% by 2014

• Lean transformation – Functional

– Program to reduce back office

costs

Past Due

DaysCycle

Time

Employee

Engagement

Cost

Leverage

Building capabilities: increasing margins and working capital efficiency

Value Streams

14

Lean Transformation Improvements

Lynn HavenHastings

Metrics % Reduction

# of Stations 85%

Assembly Space 64%

Capital 35%

Labor Hrs Per Unit 25%

Metrics % Reduction

# of Stations 43%

Total Sq. Footage 36%

Capital 23%

Labor Hrs Per Unit 26%

Metrics % Improved

Cost / Margin 23%

Past Due Days 43%

Metrics % Change

Cycle Time Reduction 48%

Past Due Deliveries 69%

On-time Deliveries 36%

AreciboClarksville / Monterrey

15

Value Stream Expansion

“OPEX”Growth Excellence

Market

AnalyticsProduct

Management

Technology &

Innovation

Sales Force

CapabilityPricing

• Rigorous analytics, market segmentation, customer insights

• Generating, developing and launching offerings

• Reduce cycle times and increase speed to market

• Monetize reliability and energy efficiency through customized solutions

LaunchIdea

Significant opportunity to grow and expand margins

using value stream discipline

CustomerCustomer

Value

Quote

to Cash

16

Capital Allocation

Shareholder

Value

Balance Sheet

• BBB Rating

• No maturities until 2015

M & A

• Focused on core businesses

• Value accretive on a risk

adjusted basis

Share Repurchase

• Complete current $2B

authorization in 1Q 14

• New $1.5B authorization

in 2014

Organic Investment

• Innovation and Growth

• Opex

Dividend

• Peer group metrics

Balancing capital allocation alternatives to create shareholder value

17

Capital Allocation

Annual Dividend Per Share Share Repurchase, $M

2011 2012 2013 2014 F

840

1,160

800

1,200

1,375-1,475

$~5.5 billion returned to shareholders from 2011 to 2014F

• $1.00 per share dividend for 2014

• 2014 dividend increased by 19%

from 2013

36.3M 18.4M 21.0M # of shares

• 2013 authorization of $2B targeted for

Q1 2014 completion

• New authorization in 2014 of $1.5B

• Total repurchase spend target for full

year 2014 of $1,375M to $1,475M

$0.50

$0.28

$0.43

$0.64

$0.84

$1.00

2009 2010 2011 2012 2013 2014F

1Q

18

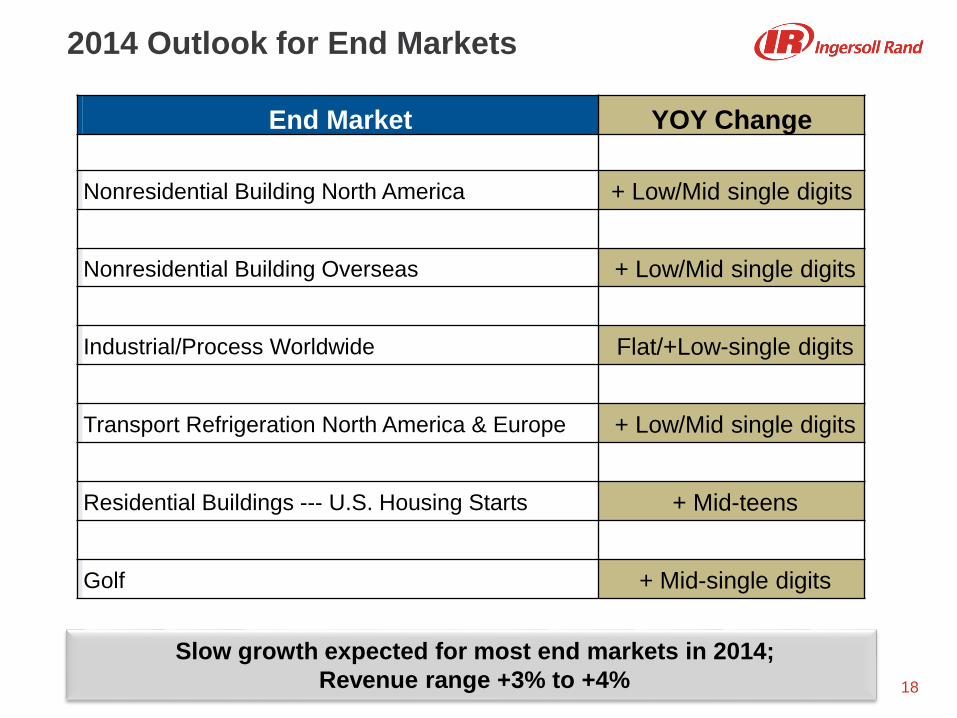

2014 Outlook for End Markets

End Market YOY Change

Nonresidential Building North America + Low/Mid single digits

Nonresidential Building Overseas + Low/Mid single digits

Industrial/Process Worldwide Flat/+Low-single digits

Transport Refrigeration North America & Europe + Low/Mid single digits

Residential Buildings --- U.S. Housing Starts + Mid-teens

Golf + Mid-single digits

Slow growth expected for most end markets in 2014;

Revenue range +3% to +4%

19

Summary

• Well positioned for the future – with strong

momentum and further upside

‒ Attractive end markets

‒ Leading brands and growth from innovation

‒ Strong penetration and positioning in developing

markets with significant potential

• Integration of businesses delivering sustainable

results

• OPEX will generate improved efficiencies, margins

and speed to market

• Increased focus on delivering organic growth

– Extending OPEX principles to generating ideas

and developing and launching products

• Strong cash generation and disciplined capital

allocation to deliver returns to shareholders

Much progress…Much more opportunity ahead

20