36

MICRO ASSESSMENT REPORT SANTA CATARINA TEACHING AND ENGINEERING FOUNDATION (FEESC) DATE: 23 AUGUST 2019 PARTNER: MARTIN DANIEL, [email protected] COMMISSIONED BY: UNDP Brazil

MICRO ASSESSMENT REPORT SANTA CATARINA TEACHING AND ENGINEERING FOUNDATION (FEESC) DATE: 23 AUGUST 2019 PARTNER: MARTIN DANIEL, [email protected] COMMISSIONED BY: UNDP Brazil

HACT Framework Micro Assessment

CONTENTS

MICRO ASSESSMENT FINDINGS ..................................... 3

1.1. BACKGROUND, SCOPE AND METHODOLOGY ................................... 3

1.2. SUMMARY OF RISK ASSESSMENT RESULTS ...................................... 5

1.3. DETAILED INTERNAL CONTROL FINDINGS AND RECOMMENDATIONS ............. 7

ANNEXES ............................................................. 12

ANNEX I: IMPLEMENTING PARTNER AND PROGRAMME INFORMATION ................... 13

ANNEX II: IMPLEMENTING PARTNER ORGANISATIONAL CHART .......................... 14

ANNEX III: LIST OF PERSONS MET ..................................................... 15

ANNEX IV: MICRO ASSESSMENT QUESTIONNAIRE ....................................... 15

HACT Framework Micro Assessment

MICRO ASSESSMENT FINDINGS

1.1. BACKGROUND, SCOPE AND METHODOLOGY

Background

The micro assessment is part of the requirements under the Harmonized Approach to Cash Transfers (HACT) Framework. The HACT framework represents a common operational framework for UN agencies’ transfer of cash to government and non-governmental implementing partners.

The micro assessment assesses the implementing partner’s control framework. It results in a risk rating (low, moderate, significant or high). The overall risk rating is used by the UN agencies, along with other available information (e.g. history of engagement with the agency and previous assurance results), to determine the type and frequency of assurance activities as per each agency’s guideline and can be taken into consideration when selecting the appropriate cash transfer modality for an implementing partner.

Scope

The micro assessment provides an overall assessment of the implementing partner’s programme, financial and operations management policies, procedures, systems and internal controls. It includes:

A review of the implementing partner legal status, governance structures and financial viability; programme management, organizational structure and staffing, accounting policies and procedures, fixed assets and inventory, financial reporting and monitoring, and procurement;

A focus on compliance with policies, procedures, regulations and institutional arrangements that are issued both by the Government and the implementing partner.

It takes into account results of any previous micro assessments conducted of the implementing partner.

Methodology

We performed the micro assessment at the locations and on the dates set out in Annex I.

Through discussion with management, observation and walk-through tests of transactions, we have assessed the implementing partner’s internal control system with emphasis on:

The effectiveness of the systems in providing the implementing partner’s management with accurate and timely information for management of funds and assets in accordance with work plans and agreements with the United Nations agencies;

The general effectiveness of the internal control system in protecting the assets and resources of the implementing partner.

We discussed the results of the micro assessment with applicable UN agency personnel and the implementing partner prior to finalization of the report. The list of persons met and interviewed during the micro assessment is set out in Annex III.

HACT Framework Micro Assessment

Results

The results of our micro assessment are set out in section 1.2 below, and our detailed internal control findings and recommendations in section 1.3.

Martin Daniel Partner For, and on behalf of, BDO LLP 23 August 2019

HACT Framework Micro Assessment

1.2. SUMMARY OF RISK ASSESSMENT RESULTS

The table below summarizes the results and main internal control gaps found during application of the micro assessment questionnaire (in Annex IV). Detailed findings and recommendations are set out in section 1.3 below.

Tested subject area

Risk assessment* Comments

1. Implementing partner

The Santa Catarina Teaching and Engineering Foundation (FEESC) is a private non-profit legal entity that was established in 1966. The FEESC is only responsible for the financial administration of the projects.

The partner is a party to two civil lawsuits; however, the possibility of the FEESC having to pay out compensation is low and the maximum compensation has been calculated at R$ 120,334.60 and has been provided for in full.

2. Programme management

The partner has its own project management system (SIFEESC) and several manuals that assist in carrying out operational activities. Each project follows the guidelines provided by the donor. In addition to these guidelines, the partner also uses various tools for monitoring and evaluation such as financial reports, monthly meetings, monthly and annual planning, among others. It should be noted that the partner is only responsible for administrative and financial management of the project, and not the technical implementation of the project.

3. Organisational structure and staffing

The partner has sufficient and detailed written policies and procedures related to recruitment, employment and personnel practices, and also has clearly defined and detailed job descriptions on an individual level. The organisational structure of the finance and project departments is well designed, and the finance department is staffed adequately to ensure sufficient controls to manage UNDP funds.

4. Accounting policies and procedures

The partner uses a computerised accounting system which allows for proper recording of the project transactions by budget line. The partner has sufficient staff to allow for appropriate segregation of duties. Each project has a separate bank account and the reconciliations are carried out on a monthly basis; however, although the reconciliations are reviewed there is no physical evidence of this review. Additionally, the petty cash counts are not reviewed by a separate member of staff to those carrying out the count.

The partner does not have an internal audit function.

Low

Low

Low

Low

HACT Framework Micro Assessment

Tested subject area

Risk assessment* Comments

5. Fixed assets and inventory

The fixed assets register is reconciled with the subsidiary ledger on a monthly basis and physical fixed asset verifications are carried out on an annual basis. All assets have a barcode on their asset number tag, these are scanned (by location) using a handheld machine. The partner has car and buildings insurance.

As the value of inventory held by the partner is completely immaterial, they do not maintain inventory records in the accounting system or carry out physical verifications as the cost of doing so would be greater than the value of the inventory.

6. Financial reporting and monitoring

The partner prepares annual financial statements in accordance with Brazilian legislation. They also prepare monthly management accounts. For each project, the reports are prepared in accordance with the project agreement, with regards to content and frequency. The partner uses a computerised financial management system, the accounting software they use is WK Sistema, which can produce all the necessary reports.

7. Procurement

The FEESC has a separate structured procurement unit, and all staff are well qualified with relevant training. The partner also has a computerised procurement system. However, the partner's contract templates do not specifically include references to ethical procurement practices, or supplier ineligibility criteria. They also do not specifically maintain a database of past supplier performance.

Overall risk assessment

* High, Significant, Moderate, Low

Low

Low

Low

Low

HACT Framework Micro Assessment

1.3. DETAILED INTERNAL CONTROL FINDINGS AND RECOMMENDATIONS

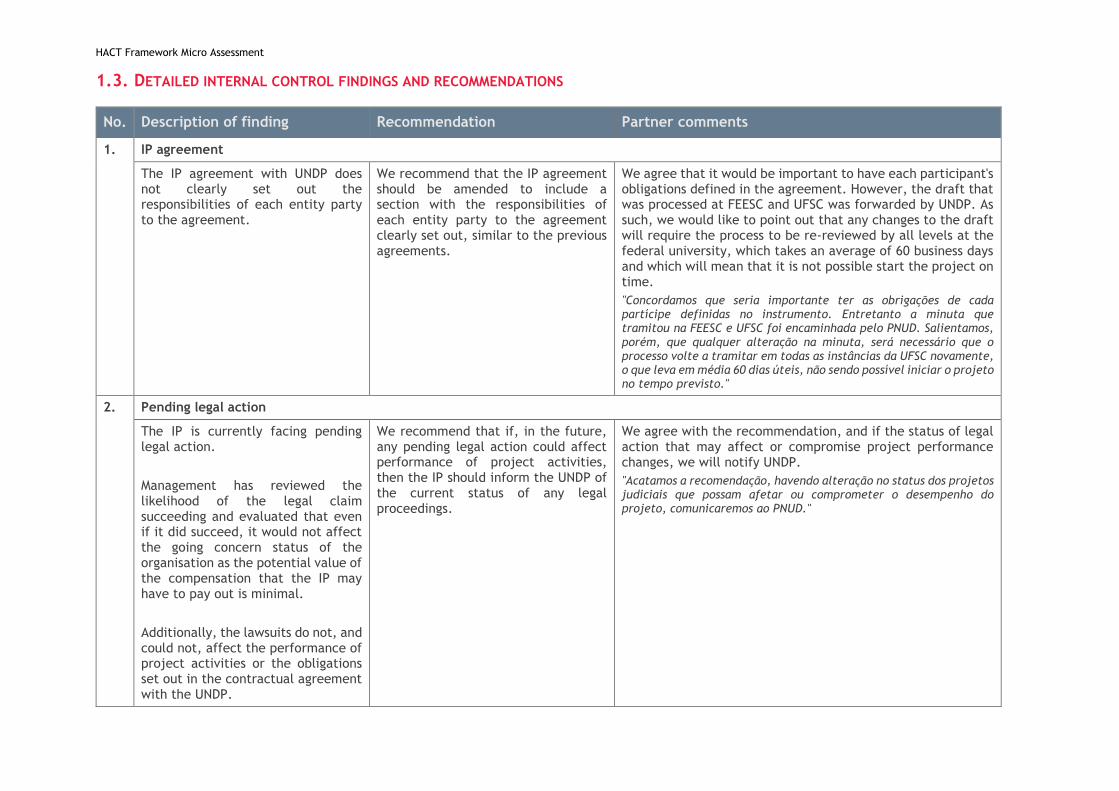

No. Description of finding Recommendation Partner comments

1. IP agreement

The IP agreement with UNDP does not clearly set out the responsibilities of each entity party to the agreement.

We recommend that the IP agreement should be amended to include a section with the responsibilities of each entity party to the agreement clearly set out, similar to the previous agreements.

We agree that it would be important to have each participant's obligations defined in the agreement. However, the draft that was processed at FEESC and UFSC was forwarded by UNDP. As such, we would like to point out that any changes to the draft will require the process to be re-reviewed by all levels at the federal university, which takes an average of 60 business days and which will mean that it is not possible start the project on time.

"Concordamos que seria importante ter as obrigações de cada partícipe definidas no instrumento. Entretanto a minuta que tramitou na FEESC e UFSC foi encaminhada pelo PNUD. Salientamos, porém, que qualquer alteração na minuta, será necessário que o processo volte a tramitar em todas as instâncias da UFSC novamente, o que leva em média 60 dias úteis, não sendo possível iniciar o projeto no tempo previsto."

2. Pending legal action

The IP is currently facing pending legal action.

Management has reviewed the likelihood of the legal claim succeeding and evaluated that even if it did succeed, it would not affect the going concern status of the organisation as the potential value of the compensation that the IP may have to pay out is minimal.

Additionally, the lawsuits do not, and could not, affect the performance of project activities or the obligations set out in the contractual agreement with the UNDP.

We recommend that if, in the future, any pending legal action could affect performance of project activities, then the IP should inform the UNDP of the current status of any legal proceedings.

We agree with the recommendation, and if the status of legal action that may affect or compromise project performance changes, we will notify UNDP.

"Acatamos a recomendação, havendo alteração no status dos projetos judiciais que possam afetar ou comprometer o desempenho do projeto, comunicaremos ao PNUD."

HACT Framework Micro Assessment

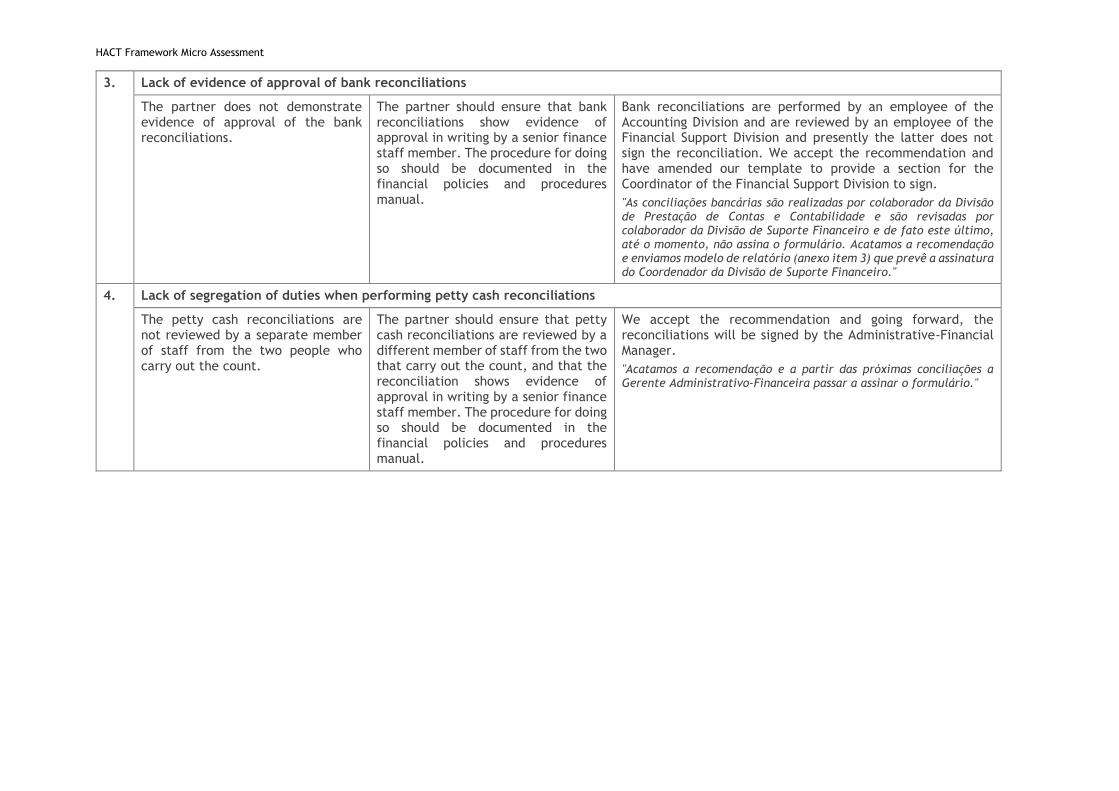

3. Lack of evidence of approval of bank reconciliations

The partner does not demonstrate evidence of approval of the bank reconciliations.

The partner should ensure that bank reconciliations show evidence of approval in writing by a senior finance staff member. The procedure for doing so should be documented in the financial policies and procedures manual.

Bank reconciliations are performed by an employee of the Accounting Division and are reviewed by an employee of the Financial Support Division and presently the latter does not sign the reconciliation. We accept the recommendation and have amended our template to provide a section for the Coordinator of the Financial Support Division to sign.

"As conciliações bancárias são realizadas por colaborador da Divisão de Prestação de Contas e Contabilidade e são revisadas por colaborador da Divisão de Suporte Financeiro e de fato este último, até o momento, não assina o formulário. Acatamos a recomendação e enviamos modelo de relatório (anexo item 3) que prevê a assinatura do Coordenador da Divisão de Suporte Financeiro."

4. Lack of segregation of duties when performing petty cash reconciliations

The petty cash reconciliations are not reviewed by a separate member of staff from the two people who carry out the count.

The partner should ensure that petty cash reconciliations are reviewed by a different member of staff from the two that carry out the count, and that the reconciliation shows evidence of approval in writing by a senior finance staff member. The procedure for doing so should be documented in the financial policies and procedures manual.

We accept the recommendation and going forward, the reconciliations will be signed by the Administrative-Financial Manager.

"Acatamos a recomendação e a partir das próximas conciliações a Gerente Administrativo-Financeira passar a assinar o formulário."

HACT Framework Micro Assessment

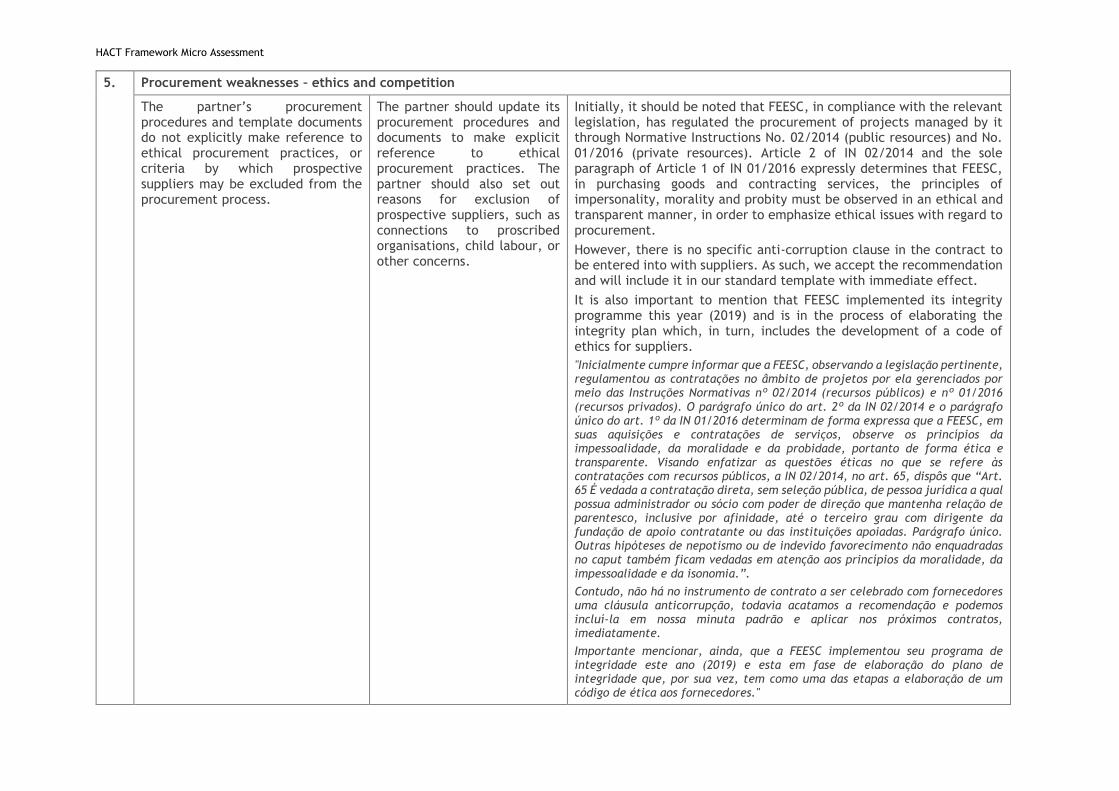

5. Procurement weaknesses – ethics and competition

The partner’s procurement procedures and template documents do not explicitly make reference to ethical procurement practices, or criteria by which prospective suppliers may be excluded from the procurement process.

The partner should update its procurement procedures and documents to make explicit reference to ethical procurement practices. The partner should also set out reasons for exclusion of prospective suppliers, such as connections to proscribed organisations, child labour, or other concerns.

Initially, it should be noted that FEESC, in compliance with the relevant legislation, has regulated the procurement of projects managed by it through Normative Instructions No. 02/2014 (public resources) and No. 01/2016 (private resources). Article 2 of IN 02/2014 and the sole paragraph of Article 1 of IN 01/2016 expressly determines that FEESC, in purchasing goods and contracting services, the principles of impersonality, morality and probity must be observed in an ethical and transparent manner, in order to emphasize ethical issues with regard to procurement.

However, there is no specific anti-corruption clause in the contract to be entered into with suppliers. As such, we accept the recommendation and will include it in our standard template with immediate effect.

It is also important to mention that FEESC implemented its integrity programme this year (2019) and is in the process of elaborating the integrity plan which, in turn, includes the development of a code of ethics for suppliers.

"Inicialmente cumpre informar que a FEESC, observando a legislação pertinente, regulamentou as contratações no âmbito de projetos por ela gerenciados por meio das Instruções Normativas nº 02/2014 (recursos públicos) e nº 01/2016 (recursos privados). O parágrafo único do art. 2º da IN 02/2014 e o parágrafo único do art. 1º da IN 01/2016 determinam de forma expressa que a FEESC, em suas aquisições e contratações de serviços, observe os princípios da impessoalidade, da moralidade e da probidade, portanto de forma ética e transparente. Visando enfatizar as questões éticas no que se refere às contratações com recursos públicos, a IN 02/2014, no art. 65, dispôs que “Art. 65 É vedada a contratação direta, sem seleção pública, de pessoa jurídica a qual possua administrador ou sócio com poder de direção que mantenha relação de parentesco, inclusive por afinidade, até o terceiro grau com dirigente da fundação de apoio contratante ou das instituições apoiadas. Parágrafo único. Outras hipóteses de nepotismo ou de indevido favorecimento não enquadradas no caput também ficam vedadas em atenção aos princípios da moralidade, da impessoalidade e da isonomia.”.

Contudo, não há no instrumento de contrato a ser celebrado com fornecedores uma cláusula anticorrupção, todavia acatamos a recomendação e podemos incluí-la em nossa minuta padrão e aplicar nos próximos contratos, imediatamente.

Importante mencionar, ainda, que a FEESC implementou seu programa de integridade este ano (2019) e esta em fase de elaboração do plano de integridade que, por sua vez, tem como uma das etapas a elaboração de um código de ética aos fornecedores."

HACT Framework Micro Assessment

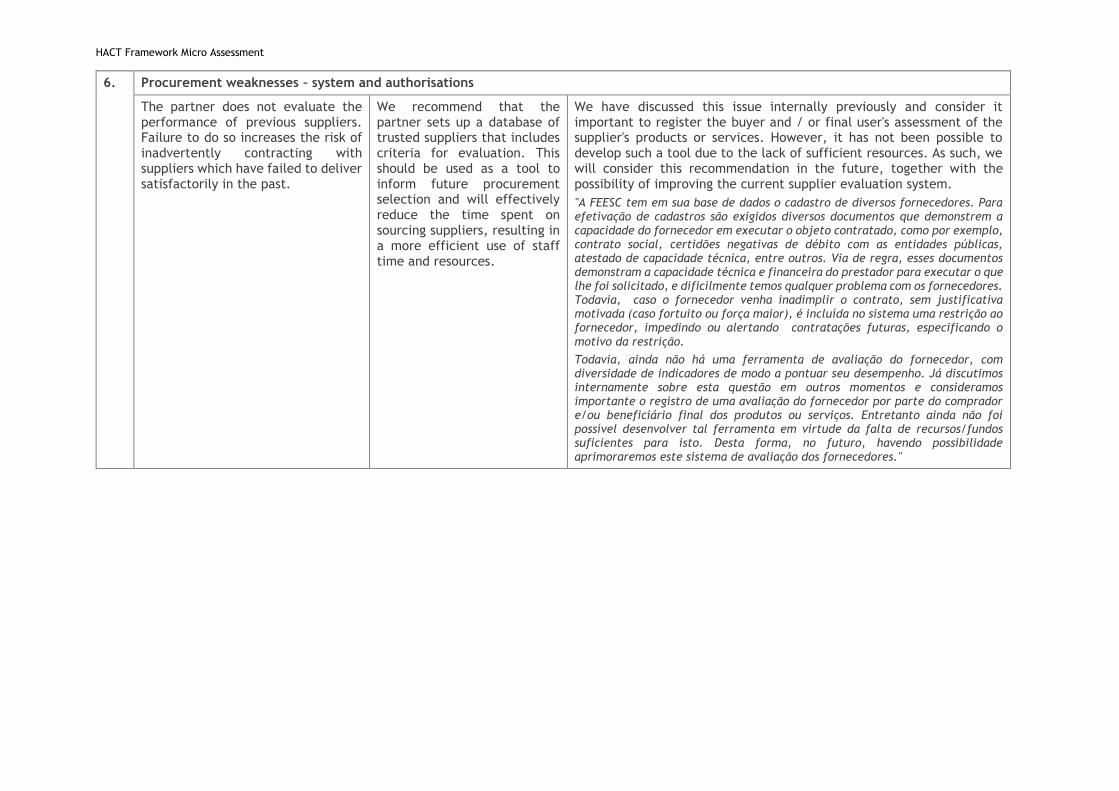

6. Procurement weaknesses – system and authorisations

The partner does not evaluate the performance of previous suppliers. Failure to do so increases the risk of inadvertently contracting with suppliers which have failed to deliver satisfactorily in the past.

We recommend that the partner sets up a database of trusted suppliers that includes criteria for evaluation. This should be used as a tool to inform future procurement selection and will effectively reduce the time spent on sourcing suppliers, resulting in a more efficient use of staff time and resources.

We have discussed this issue internally previously and consider it important to register the buyer and / or final user's assessment of the supplier's products or services. However, it has not been possible to develop such a tool due to the lack of sufficient resources. As such, we will consider this recommendation in the future, together with the possibility of improving the current supplier evaluation system.

"A FEESC tem em sua base de dados o cadastro de diversos fornecedores. Para efetivação de cadastros são exigidos diversos documentos que demonstrem a capacidade do fornecedor em executar o objeto contratado, como por exemplo, contrato social, certidões negativas de débito com as entidades públicas, atestado de capacidade técnica, entre outros. Via de regra, esses documentos demonstram a capacidade técnica e financeira do prestador para executar o que lhe foi solicitado, e dificilmente temos qualquer problema com os fornecedores. Todavia, caso o fornecedor venha inadimplir o contrato, sem justificativa motivada (caso fortuito ou força maior), é incluída no sistema uma restrição ao fornecedor, impedindo ou alertando contratações futuras, especificando o motivo da restrição.

Todavia, ainda não há uma ferramenta de avaliação do fornecedor, com diversidade de indicadores de modo a pontuar seu desempenho. Já discutimos internamente sobre esta questão em outros momentos e consideramos importante o registro de uma avaliação do fornecedor por parte do comprador e/ou beneficiário final dos produtos ou serviços. Entretanto ainda não foi possível desenvolver tal ferramenta em virtude da falta de recursos/fundos suficientes para isto. Desta forma, no futuro, havendo possibilidade aprimoraremos este sistema de avaliação dos fornecedores."

HACT Framework Micro Assessment

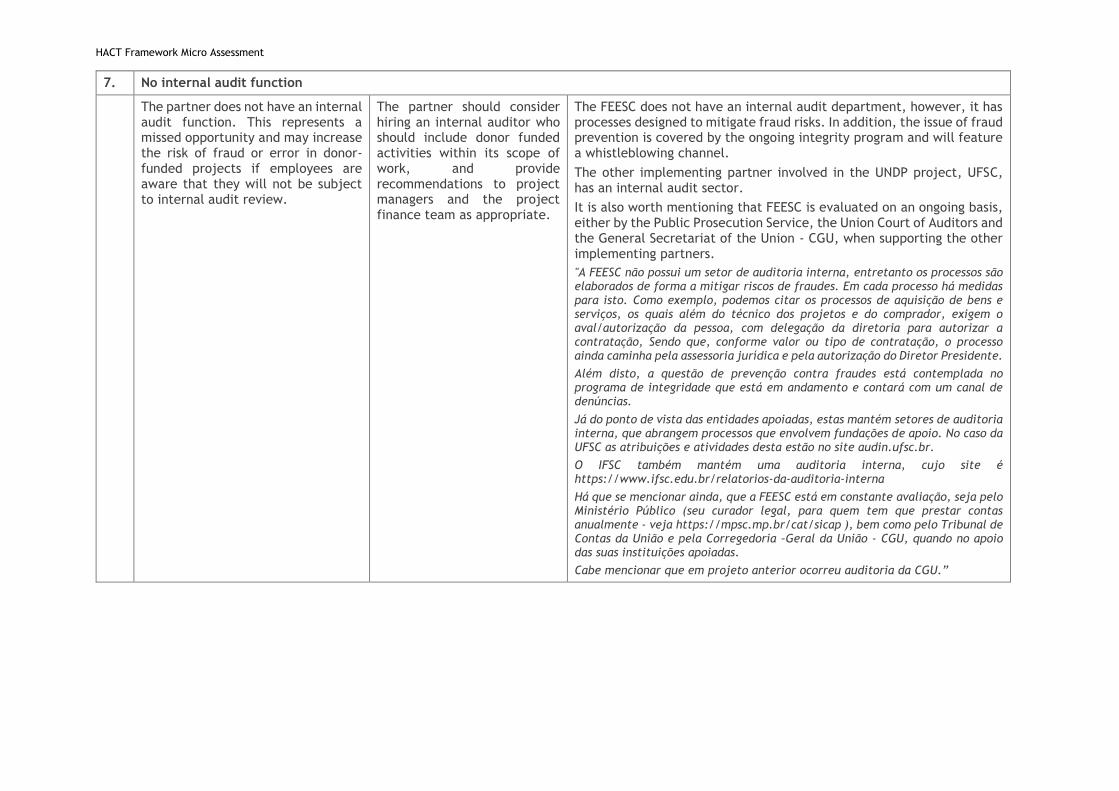

7. No internal audit function

The partner does not have an internal audit function. This represents a missed opportunity and may increase the risk of fraud or error in donor-funded projects if employees are aware that they will not be subject to internal audit review.

The partner should consider hiring an internal auditor who should include donor funded activities within its scope of work, and provide recommendations to project managers and the project finance team as appropriate.

The FEESC does not have an internal audit department, however, it has processes designed to mitigate fraud risks. In addition, the issue of fraud prevention is covered by the ongoing integrity program and will feature a whistleblowing channel.

The other implementing partner involved in the UNDP project, UFSC, has an internal audit sector.

It is also worth mentioning that FEESC is evaluated on an ongoing basis, either by the Public Prosecution Service, the Union Court of Auditors and the General Secretariat of the Union - CGU, when supporting the other implementing partners.

"A FEESC não possui um setor de auditoria interna, entretanto os processos são elaborados de forma a mitigar riscos de fraudes. Em cada processo há medidas para isto. Como exemplo, podemos citar os processos de aquisição de bens e serviços, os quais além do técnico dos projetos e do comprador, exigem o aval/autorização da pessoa, com delegação da diretoria para autorizar a contratação, Sendo que, conforme valor ou tipo de contratação, o processo ainda caminha pela assessoria jurídica e pela autorização do Diretor Presidente.

Além disto, a questão de prevenção contra fraudes está contemplada no programa de integridade que está em andamento e contará com um canal de denúncias.

Já do ponto de vista das entidades apoiadas, estas mantém setores de auditoria interna, que abrangem processos que envolvem fundações de apoio. No caso da UFSC as atribuições e atividades desta estão no site audin.ufsc.br.

O IFSC também mantém uma auditoria interna, cujo site é https://www.ifsc.edu.br/relatorios-da-auditoria-interna

Há que se mencionar ainda, que a FEESC está em constante avaliação, seja pelo Ministério Público (seu curador legal, para quem tem que prestar contas anualmente - veja https://mpsc.mp.br/cat/sicap ), bem como pelo Tribunal de Contas da União e pela Corregedoria –Geral da União - CGU, quando no apoio das suas instituições apoiadas.

Cabe mencionar que em projeto anterior ocorreu auditoria da CGU.”

HACT Framework Micro Assessment

ANNEXES

HACT Framework Micro Assessment

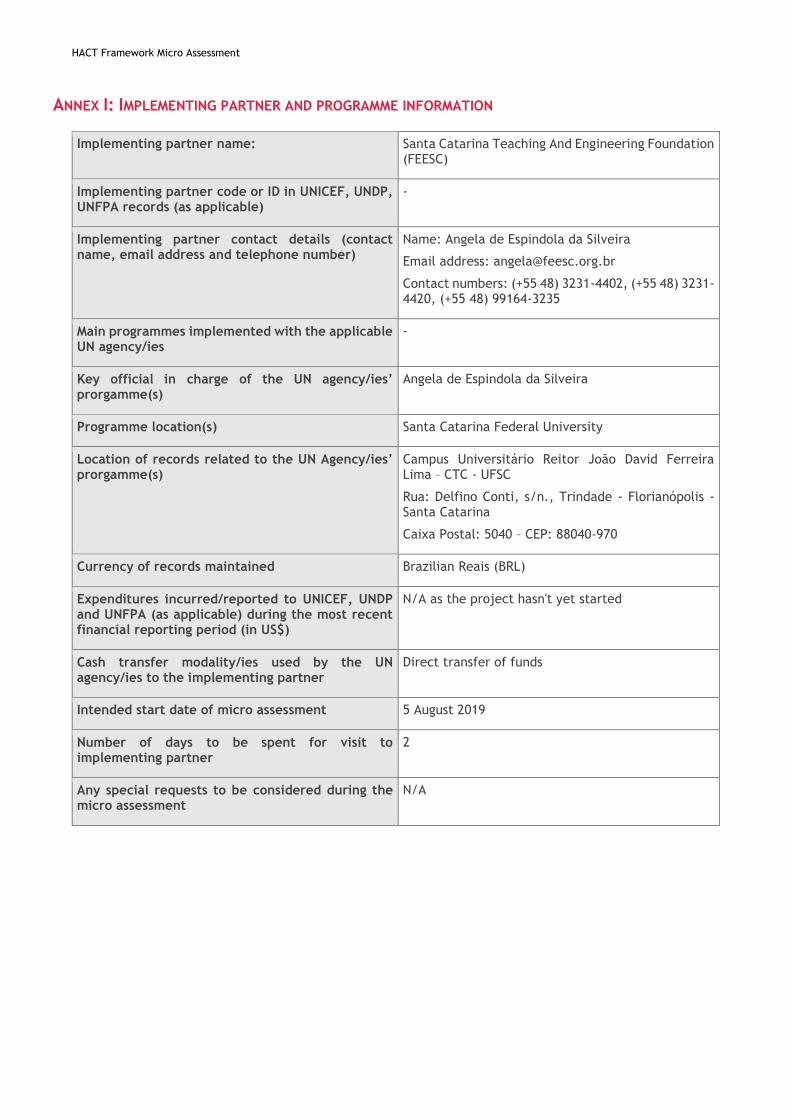

ANNEX I: IMPLEMENTING PARTNER AND PROGRAMME INFORMATION

Implementing partner name: Santa Catarina Teaching And Engineering Foundation (FEESC)

Implementing partner code or ID in UNICEF, UNDP, UNFPA records (as applicable)

-

Implementing partner contact details (contact name, email address and telephone number)

Name: Angela de Espindola da Silveira

Email address: [email protected]

Contact numbers: (+55 48) 3231-4402, (+55 48) 3231-4420, (+55 48) 99164-3235

Main programmes implemented with the applicable UN agency/ies

-

Key official in charge of the UN agency/ies’ prorgamme(s)

Angela de Espindola da Silveira

Programme location(s) Santa Catarina Federal University

Location of records related to the UN Agency/ies’ prorgamme(s)

Campus Universitário Reitor João David Ferreira Lima – CTC - UFSC

Rua: Delfino Conti, s/n., Trindade - Florianópolis - Santa Catarina

Caixa Postal: 5040 – CEP: 88040-970

Currency of records maintained Brazilian Reais (BRL)

Expenditures incurred/reported to UNICEF, UNDP and UNFPA (as applicable) during the most recent financial reporting period (in US$)

N/A as the project hasn't yet started

Cash transfer modality/ies used by the UN agency/ies to the implementing partner

Direct transfer of funds

Intended start date of micro assessment 5 August 2019

Number of days to be spent for visit to implementing partner

2

Any special requests to be considered during the micro assessment

N/A

HACT Framework Micro Assessment

ANNEX II: IMPLEMENTING PARTNER ORGANISATIONAL CHART

HACT Framework Micro Assessment

ANNEX III: LIST OF PERSONS MET

Name Unit / organisation Position

Angela de Espindola da Silveira Management, FEESC Executive Manager

João Hélio Martins Project dept., FEESC Project Manager

Graziela Régis Montenegro Finance dept., FEESC Finance Manager

Fabiane Eusebina Silveira HR dept., FEESC Human Resources Manager

André Luis da Trinidade Finance dept., FEESC Accounting Coordinator

Larissa Miguel da Silveira Purchasing dept., FEESC Purchasing Manager

HACT Framework Micro Assessment

ANNEX IV: MICRO ASSESSMENT QUESTIONNAIRE

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

1. Implementing partner

1.1 Is the IP legally registered? If so, is it in compliance with registration requirements? Please note the legal status and date of registration of the entity.

Yes Low 1 The Santa Catarina Teaching and Engineering Foundation - FEESC is a private non-profit legal entity established by the Santa Catarina Electric Power Station - CELESC, by public deed issued at the 4th Notary Office of the District of Florianopolis, on pages 143/144 of Book No. 5, May 18, 1966, and recorded at pages 264 of book A-11, under no. 0733, on March 14, 1975, at the Registry Office of the Securities, Documents and Legal Entities of Comarca Capital.

1.2 If the IP received United Nations resources in the past, were significant issues reported in managing the resources, including from previous assurance activities.

No Moderate 4 The only issues noted in managing project resource was due to lack of clarity on how expenditure is to be executed (selection process procedures, etc.), as well as acceptance of technical reports submitted for release of subsequent instalments. It should be noted that FEESC is not responsible for the technical reports.

Refer to internal control finding 1.

1.3 Does the IP have statutory reporting requirements? If so, are they in compliance with such requirements in the prior three fiscal years?

Yes Low 1 The partner produces annual financial reports which are submitted for approval by the board of directors, statutorily audited, and must be presented to the State Public Ministry of Santa Catarina (SICAP) by 30/06 of each year. Furthermore, the partner provides Management Report to the federal university of Santa Catarina (UFSC) and the federal institute of Santa Catarina (IFSC). In addition to these, as provided in the Bylaws, it is mandatory to submit these reports to the Fiscal Council and the Curator Council. The partner has been in compliance with the requirements for the past three years.

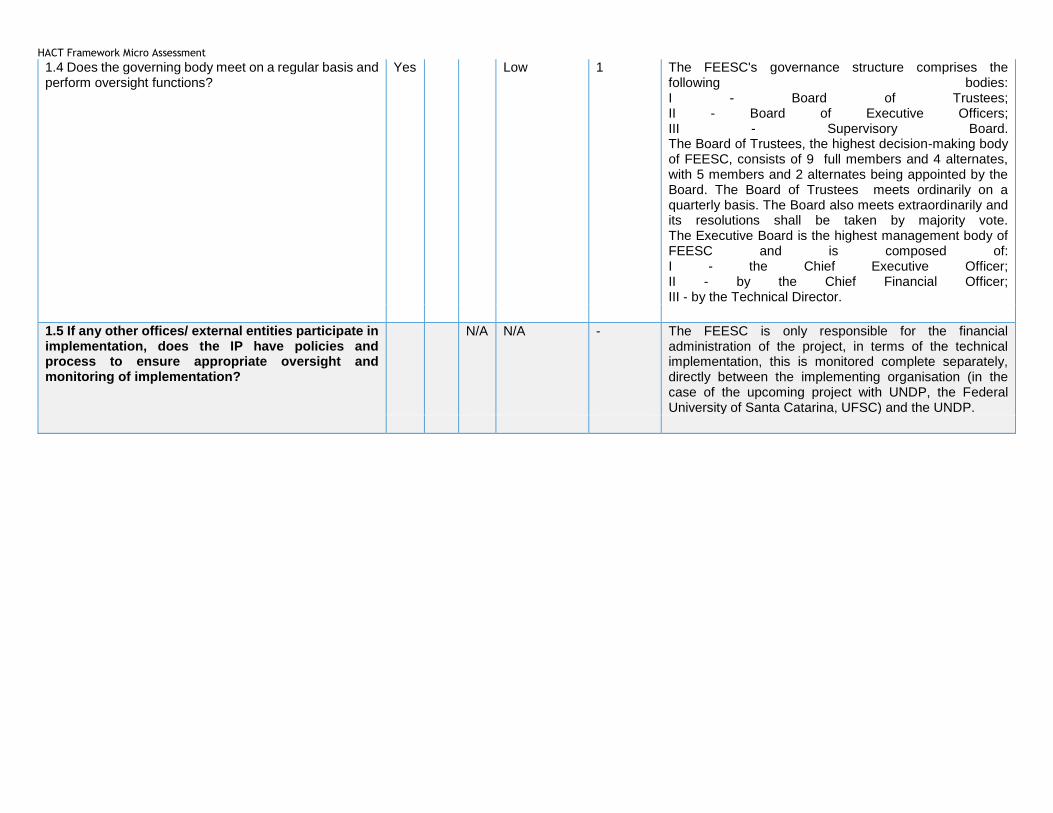

HACT Framework Micro Assessment 1.4 Does the governing body meet on a regular basis and perform oversight functions?

Yes Low 1 The FEESC's governance structure comprises the following bodies: I - Board of Trustees; II - Board of Executive Officers; III - Supervisory Board. The Board of Trustees, the highest decision-making body of FEESC, consists of 9 full members and 4 alternates, with 5 members and 2 alternates being appointed by the Board. The Board of Trustees meets ordinarily on a quarterly basis. The Board also meets extraordinarily and its resolutions shall be taken by majority vote. The Executive Board is the highest management body of FEESC and is composed of: I - the Chief Executive Officer; II - by the Chief Financial Officer; III - by the Technical Director.

1.5 If any other offices/ external entities participate in implementation, does the IP have policies and process to ensure appropriate oversight and monitoring of implementation?

N/A N/A - The FEESC is only responsible for the financial administration of the project, in terms of the technical implementation, this is monitored complete separately, directly between the implementing organisation (in the case of the upcoming project with UNDP, the Federal University of Santa Catarina, UFSC) and the UNDP.

HACT Framework Micro Assessment 1.6 Does the IP show basic financial stability in-country (core resources; funding trend) Provide the amount of total assets, total liabilities, income and expenditure for the current and prior three fiscal years.

Yes Moderate 4 2018 Assets/liabilities: 57.866.394,04 Revenue: 73.086.360,28 Expenses: 73.080.898,07 Surplus: 5.462,21 2017 Assets/liabilities: 52.740.219,72 Revenue: 77.340.895,64 Expenses: 76.251.034,73 Surplus: 1.089.860,91 2016 Assets/liabilities: 63.256.352,97 Revenue: 5.482.024,24 Expenses: 5.692.633,78 Deficit: -210.609,54 2015 Assets/liabilities: 75.929.150,28 Revenue: 6.019.822,29 Expenses: 5.402.207,26 Surplus: 617.615,03 In 2017, due to a change in Brazilian law project income was reclassified from third party income to partner income. Additionally, in the same year, the partner received a 90% discount on fines and a 70% discount on interest expenses which considerably increased the surplus. Both of these cases were reviewed in the external audit report.

1.7 Can the IP easily receive funds? Have there been any major problems in the past in the receipt of funds, particularly where the funds flow from government ministries?

Yes Low 1 The funds are received through the specific bank account for the project. The only problems noted have been regarding the delay in receiving funds, particularly with respect to reimbursements.

1.8 Does the IP have any pending legal actions against it or outstanding material/significant disputes with vendors/contractors? If so, provide details and actions taken by the IP to resolve the legal action.

Yes Significant 3 The partner is party to two civil lawsuits; however, the possibility of the FEESC having to pay out compensation is low and the maximum compensation has been calculated at R$ 120,334.60 and has been provided for in full.

Refer to internal control finding 2.

HACT Framework Micro Assessment 1.9 Does the IP have an anti-fraud and corruption policy? Yes Moderate 2 The partners procedures and policies manual includes

sections on fraud and the code of ethics.

1.10 Has the IP advised employees, beneficiaries and other recipients to whom they should report if they suspect fraud, waste or misuse of agency resources or property? If so, does the IP have a policy against retaliation relating to such reporting?

Yes Moderate 2 The FEESC is in the process of establishing the Integrity Programme, with the objectives of: I - adopting the best practices to maintain, in a process of constant improvement and strengthening, an institutional environment based on ethics and probity; II - stimulate the integrity behaviour within the scope of FEESC; and III - promote the adoption of institutional measures and actions aimed at the prevention, detection, punishment and remediation of ethical deviations, administrative offenses, acts of fraud and corruption. Among the planned outcomes is to create of a complaints channel, together with an investigation procedure.

1.11 Does the IP have any key financial or operational risks that are not covered by this questionnaire? If so, please describe. Examples: foreign exchange risk; cash receipts.

No Low 1 No other financial risks were identified.

Total number of questions in subject area: 11

Total number of applicable questions in subject area: 10

Total number of applicable key questions in subject area:

4

Total number of risk points: 20

Risk score 2.00

Area risk rating Low

HACT Framework Micro Assessment

Subject area (key questions in bold) Yes No N/A Risk Assessment

Risk points

Remarks/comments

2. Programme management

2.1. Does the IP have and use sufficiently detailed written policies, procedures and other tools (e.g. project development checklist, work planning templates, work planning schedule) to develop programmes and plans?

Yes Low 1 The partner has its own project management system (SIFEESC) and several manuals that assist in carrying out operational activities. It should be noted that the partner is only responsible for administrative and financial management of the project, and not the technical implementation of the project.

2.2. Do work plans specify expected results and the activities to be carried out to achieve results, with a time frame and budget for the activities?

Yes Low 1 Work plans specify expected outputs and time frames. Results are measured against time and costs. All the plans are made to ensure time and costs are appropriately accounted for.

2.3 Does the IP identify the potential risks for programme delivery and mechanisms to mitigate them?

Yes Low 1 The partner management meets to identify possible risks to programme implementation prior to the start of any new project, and periodically during the implementation phase. In the evaluation, possible actions to mitigate these risks are raised and taken to the Board who deliberate the actions to be taken, as well as on going monitoring of the risks.

2.4 Does the IP have and use sufficiently detailed policies, procedures, guidelines and other tools (checklists, templates) for monitoring and evaluation?

Yes Low 1 Each project follows the guidelines provided by the donor. In addition to these guidelines, the partner also uses various tools for monitoring and evaluation such as financial reports, monthly meetings, monthly and annual planning, among others.

2.5 Does the IP have M&E frameworks for its programmes, with indicators, baselines, and targets to

monitor achievement of programme results?

Yes Low 1 The partner is only responsible for the financial management of the project. The federal university of Santa Catarina is responsible for project implementation and providing technical monitoring reports directly to the UNDP regarding the project progress. However, the partner monitors and evaluates the project progress from a financial standpoint.

HACT Framework Micro Assessment 2.6 Does the IP carry out and document regular monitoring activities such as review meetings, on-site project visits, etc.

Yes N/A - The partner is only responsible for the financial management of the project. The federal university of Santa Catarina is responsible for project implementation and providing technical monitoring reports directly to the UNDP regarding the project progress. However, the partner monitors and evaluates the project progress from a financial standpoint.

2.7 Does the IP systematically collect, monitor and evaluate data on the achievement of project results?

Yes Low 1 The federal university of Santa Catarina is responsible for project implementation and providing technical monitoring reports directly to the UNDP regarding the project progress. However, the partner monitors and evaluates the project progress from a financial standpoint.

2.8 Is it evident that the IP followed up on independent

evaluation recommendations?

Yes Low 1 The partner is audited annually by external auditors, who carry out an internal controls audit part way through the year in addition to the financial audit at year-end. The auditor recommendations are presented at the board of directors meeting, and an implementation plan is prepared to monitor the implementation progress.

Total number of questions in subject area: 8

Total number of applicable questions in subject area: 7

Total number of applicable key questions in subject area:

1

Total number of risk points: 7

Risk score 1.00

Area risk rating Low

HACT Framework Micro Assessment

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

3. Organizational structure and staffing

3.1 Are the IP’s recruitment, employment and personnel practices clearly defined and followed, and do they embrace transparency and competition?

Yes Low 1 The partner has sufficient and detailed written policies and procedures related to recruitment, employment and personnel practices. When hiring staff, the partner uses recruitment and selection companies or publishes the job posting on recruitment websites. After all the resumes have been submitted, they're screened and then the selected candidates are invited for interviews. The project coordinator is responsible for screening the hiring of any contractors involved in the project.

3.2 Does the IP have clearly defined job descriptions? Yes Low 1 The partner has clearly defined and detailed job descriptions on an individual level. During the micro assessment we reviewed the job description for key management positions. The description included the overall remit of the position alongside the specific responsibilities of the role, and the requirements in terms of previous experience, education, and skills. For projects, the coordinator provides a description of the activities in the project agreement.

HACT Framework Micro Assessment 3.3 Is the organizational structure of the finance and programme management departments, and competency of staff, appropriate for the complexity of the IP and the scale of activities? Identify the key staff, including job titles, responsibilities, educational backgrounds and professional experience.

Yes Low 1 The organisational structure of the finance and project departments is well designed. The finance department is lead by the finance manager (Graziela Régis Montenegro) with the other members of staff split into two departments: accounting and finance. The qualifications, experiences and responsibility of each individual member of staff is described in the individual job descriptions. Executive Manager: Degree in Computer Science (post-grad in quality and productivity) Activities: Plan and control the activities developed by FEESC, in compliance with the statutory objectives and guidelines established by the Board of Directors and the Board of Trustees. Project Manager: Degree in Accounting Sciences Activities: Plan, coordinate and monitor projects. Purchasing Manager: Degree in Law Activities: Plan, coordinate and monitor purchases in compliance with current legislation. Administrative and Finance Manager: Degree in Economic Sciences Activities: To plan, coordinate and control, financial operations. HR Manager: Degree in Accounting Sciences Activities: Coordinate, supervise and guide personnel management processes.

3.4 Is the IP’s accounting/finance function staffed adequately to ensure sufficient controls are in place to manage agency funds?

Yes Low 1 The partner's finance department is staffed adequately to ensure sufficient controls to manage UNDP funds.

3.5 Does the IP have training policies for accounting/finance/ programme management staff? Are necessary training activities undertaken?

Yes Low 1 The partner has a manual that details the Training Incentive Programme for its employees. Any employee can put in a request to their manager to attend an external training course. The requests are reviewed, and where possible the partner pays either part of or the full cost of the course. Certificates of all courses attended are maintained in the employees file.

HACT Framework Micro Assessment 3.6 Does the IP perform background verification/checks on all new accounting/finance and management positions?

Yes Moderate 2 For prospective staff in management positions, the partner verifies their technical qualifications and employment history via background checks (including social media) and contact with the previous employers where deemed necessary.

3.7 Has there been significant turnover in key finance positions the past five years? If so, has the rate improved or worsened and appears to be a problem?

No Low 1 There has been no significant turnover in the past 5 years.

3.8 Does the IP have a documented internal control framework? Is this framework distributed and made available to staff and updated periodically? If so, please describe.

Yes Low 1 The partner's internal control framework is included in their code of conduct. The manual are distributed to all staff on joining the company and is updated periodically.

Total number of questions in subject area: 8

Total number of applicable questions in subject area: 8

Total number of applicable key questions in subject area:

3

Total number of risk points: 9

Risk score 1.13

Area risk rating Low

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

4. Accounting policies and procedures

4a. General

4.1 Does the IP have an accounting system that allows for proper recording of financial transactions from United Nations agencies, including allocation of expenditures in accordance with the respective components, disbursement categories and sources of funds?

Yes Low 1 All processes are integrated in the partner's accounting system with a separate code for each project ensuring that at the time of accounting the transaction is allocated properly. Additionally, each project has an individual bank account to be able to fully monitor receipt of funds and project expenditure.

4.2 Does the IP have an appropriate cost allocation methodology that ensures accurate cost allocations to the various funding sources in accordance with established agreements?

Yes Low 1 The partner has established project codes for funds received from different donors in the software for easy identification and tracking of the programme's financial information in the financial system, in line with the funding agreements. All project related expenses and receipt of funds are allocated, according to budget line, to the relevant project directly in the system.

HACT Framework Micro Assessment 4.3 Are all accounting and supporting documents retained in an organized system that allows authorized users easy access?

Yes Low 1 Reports and supporting documents are kept both in electronic format and paper copies. The paper copies are maintained in a storage room in an organised manner for easy access.

4.4 Are the general ledger and subsidiary ledgers reconciled at least monthly? Are explanations provided for significant reconciling items?

N/A N/A - The accounting system does not have separate sub-ledgers.

4b. Segregation of duties

4.5 Are the following functional responsibilities performed by different units or individuals: (a) authorization to execute a transaction; (b) recording of the transaction; and (c) custody of assets involved in the transaction?

Yes Low 1 Transactions are authorised different members of staff depending on the transaction type and value. (a) Project transactions requested by the implementing partner, e.g. the university, will be approved by the project technician in accordance with the budget. They will then be passed to the purchasing department, and once the transaction has been authorised by two managers, the payment will need to be approved by the finance department. (b) Transactions are recorded by accounting department. (c) The reception will receive the assets, and in the case of project assets they will be forwarded to the implementing partner who will sign receipt of the goods. If the goods are for the FEESC, then they will go directly to the user after they have been received.

4.6 Are the functions of ordering, receiving, accounting for and paying for goods and services appropriately segregated?

Yes Low 1 All purchase orders are processed and approved by the purchasing department. The finance department approves and makes the payments, while the accounting team are responsible for recording the transaction. All goods are received by the reception staff.

4.7 Are bank reconciliations prepared by individuals other than those who make or approve payments?

Yes Low 1 Each project has a separate bank account and the reconciliations are carried out on a monthly basis. The reconciliations are prepared by the assistant accountant who is not involved in making or approving payments. The finance department is divided into two separate teams, the accounting team and the finance team. The finance team make and approve the payments while the accounting team is responsible for recording transactions.

HACT Framework Micro Assessment 4c. Budgeting system

4.8 Are budgets prepared for all activities in sufficient detail to provide a meaningful tool for monitoring subsequent performance?

Yes Low 1 Project budgets are detailed enough to monitor financial performance; technical project progress is monitored by the implementing party of the agreement.

4.9 Are actual expenditures compared to the budget with reasonable frequency? Are explanations required for significant variations from the budget?

Yes Low 1 The finance department performs a monthly comparison of the budget vs. actual expenditure in order to avoid variations in the overall limits approved by the board of directors. Additionally, each time a purchase request is received, it is compared to the agreed budgeted expenditure. Project expenditure is monitored on a daily for budget and financial control. Variations in expenses are evaluated before the approval of the expense, through a review with the project coordinator. After the expenses have been incurred, a reconciliation of budget vs actual expenses is carried out at regular intervals.

4.10 Is prior approval sought for budget amendments in a timely way?

Yes Low 1 Budget amendments for the FEESC can only be made with the authorization of the fiscal council. Project technicians can propose project budget amendments to the donors when the implementing partner raises a request that is either not included in the budget or is above the budget limit.

4.11 Are IP budgets approved formally at an appropriate level?

Yes Low 1 FEESC management prepares the budget, which is submitted to the Board of Directors and the Board of Trustees for approval . The fiscal council is the last body to review and approve the budget. All project budgets are approved by the donor.

4d. Payments

4.12 Do invoice processing procedures provide for: · Copies of purchase orders and receiving reports to be obtained directly from issuing departments? · Comparison of invoice quantities, prices and terms with those indicated on the purchase order and with records of goods/services actually received? · Checking the accuracy of calculations?

Yes Low 1 When an invoice is received, a three-way match is performed by the purchasing department. Once the checks have been carried out, the payment is processed.

HACT Framework Micro Assessment 4.13 Are payments authorized at an appropriate level? Does the IP have a table of payment approval thresholds?

Yes Low 1 All transactions must be approved by a minimum of two managers, regardless of the value.

4.14 Are all invoices stamped ‘PAID’, approved, and marked with the project code and account code?

Yes Low 1 All invoices are emitted electronically with the donor agreement details included in the "additional details" section and the purchase order number. Each invoice is stamped as received by the partner. In order to pay an invoice, the partner's accounting software requires it to be linked to the correct purchase order, and does not allow for duplicate payments to be made to the same invoice number.

4.15 Do controls exist for preparation and approval of payroll expenditures? Are payroll changes properly authorized?

Yes Low 1 Payroll is prepared by the HR officer and is approved by two managers. The payment is made by the finance department and recorded by the accounting team. Salary increases, which occur in March, are made in accordance with the law. The project technician is responsible for other changes regarding salaries and positions, provided they are within the budget. The board must authorize any changes regarding FEESC staff.

4.16 Do controls exist to ensure that direct staff salary costs reflects the actual amount of staff time spent on a project?

Yes Low 1 FEESC staff costs are paid from the management percentage paid to the partner from each project and are not related to the amount of time spent on any individual project. For staff contracted for projects, the contractor are accompanied by the project coordinator who will oversee their work and maintain records of their hours worked. This monitoring is carried out by the implementing partner and then communicated to FEESC.

4.17 Do controls exist for expense categories that do not originate from invoice payments, such as DSAs, travel, and internal cost allocations?

Yes Low 1 All payments not related to invoices are linked to an own process, such as, per diem payments that go through an approval process, which is managed by a computerized operating system and there is a reconciliation of the physical documents with due requests for expenses.

HACT Framework Micro Assessment 4e. Policies and procedures

4.18 Does the IP have a stated basis of accounting (i.e. cash or accrual) and does it allow for compliance with the agency's requirement?

Yes Low 1 The partner uses the accruals basis of accounting, which is in line with Brazilian legislation. However, for project accounting, the cash basis is used. The projects are accounted for on a separate system and the year end project positions are included in the partners annual financial statements, in accordance with the third party income sector of the manual.

4.19 Does the IP have an adequate policies and procedures manual and is it distributed to relevant staff?

Yes Low 1 The institution has a procedures and policies manual which is available to all employees.

4f. Cash and bank

4.20 Does the IP require dual signatories / authorization for bank transactions? Are new signatories approved at an appropriate level and timely updates made when signatories depart?

Yes Low 1 Two signatories are required in order to approve bank transactions. The signatories are the directors and the managers. The directors can approve changes to the signatories.

4.21 Does the IP maintain an adequate, up-to-date

cashbook, recording receipts and payments?

Yes Low 1 The partner maintains the cash book for each project on electronically on their accounting system. All receipts and payments are recorded in the system to ensure the cash book and other system generated reports are up to date.

4.22 If the partner is participating in micro-finance advances, do controls exist for the collection, timely deposit and recording of receipts at each collection location?

N/A N/A - The IP doesn't participate in micro-financing advances.

4.23 Are bank balances and cash ledger reconciled monthly and properly approved? Are explanations provided for significant, unusual and aged reconciling items?

Yes Significant 6 Each project has a separate bank account and the reconciliations are carried out on a monthly basis. They are prepared by the assistant accountant and although they are reviewed by a senior member of staff, there is no signature to evidence this review.

Refer to internal control finding 3.

4.24 Is substantial expenditure paid in cash? If so, does the IP have adequate controls over cash payments?

N/A N/A - No significant expenditure is paid in cash.

4.25 Does the IP carry out a regular petty cash reconciliation?

Yes Significant 3 The partner carries out a petty cash reconciliation on a monthly basis. The reconciliation and count are performed by the Accounting Coordinator and the Financial Sector Technician together; however, they are not reviewed and approved by another member of staff.

Refer to internal control finding 4.

HACT Framework Micro Assessment 4.26 Are cash and cheques maintained in a secure location with restricted access? Are bank accounts protected with appropriate remote access controls?

Yes Low 1 Cash and cheques are kept in the partner's safe which is kept in the Financial Division. The safe requires both a key and code to open it; only the Area Coordinator and the Financial Sector Technician have a copy of the key and know the code. The safe is also sufficiently large enough that it would not be possible for someone to steal it easily.

4.27 Are there adequate controls over submission of electronic payment files that ensure no unauthorized amendments once payments are approved and files are transmitted over secure / encrypted networks?

Yes Low 1 Only staff in the finance department have access to the bank accounts online and can approve electronic payments via a security token provided by the bank.

4g. Other offices or entities

4.28 Does the IP have a process to ensure expenditures of subsidiary offices/ external entities are in compliance with the work plan and/or contractual agreement?

N/A N/A - The partner controls of the financial transactions for the projects and only approves expenses that are in line with the project budget. Expenses not detailed in the budget or above the budget limit must be approved by the donor prior to sending the request to the purchasing department.

4h. Internal audit

4.29 Is the internal auditor sufficiently independent to make critical assessments? To whom does the internal auditor report?

No Significant 3 N/A as the partner does not have an internal audit department.

Refer to internal control finding 7.

4.30 Does the IP have stated qualifications and experience requirements for internal audit department staff?

N/A N/A - N/A as the partner does not have an internal audit department.

4.31 Are the activities financed by the agencies included in the internal audit department’s work programme?

N/A N/A - N/A as the partner does not have an internal audit department.

4.32 Does the IP act on the internal auditor's recommendations?

N/A N/A - N/A as the partner does not have an internal audit department.

Total number of questions in subject area: 32

Total number of applicable questions in subject area: 25

Total number of applicable key questions in subject area:

17

Total number of risk points: 34

Risk score 1.36

Area risk rating Low

HACT Framework Micro Assessment

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

5. Fixed assets and inventory

5a. Safeguards over assets

5.1 Is there a system of adequate safeguards to protect assets from fraud, waste and abuse?

Yes Low 1 At the operational level there are controls such as: approval approvals of purchase and disposal; purchasing regulations; annual physical inventory, sequential numbering of fixed asset labels; evaluation of impairment; assessment of useful life; reconciliations; auditing, among others.

5.2 Are subsidiary records of fixed assets and inventory kept up to date and reconciled with control accounts?

Yes Low 1 The fixed assets register is reconciled with the subsidiary ledger on a monthly basis.

5.3 Are there periodic physical verification and/or count of fixed assets and inventory? If so, please describe?

Yes Low 1 Physical fixed asset verifications are carried out on an annual basis. Only the fixed assets owned by the partner are included in these verifications, and not project assets. All assets have a barcode on their asset number tag, these are scanned (by location) using a handheld machine and then a report is printed which shows all the items scanned in that location. This is then compared to the print out of assets from the system (also by location) . The system is then updated if there are any differences. Two people from fixed assets team are involved in the scanning, and then the finance department are responsible for updating the system. Physical copies of the printed reports are also kept.

5.4 Are fixed assets and inventory adequately covered by insurance policies?

Yes Moderate 2 The partner has car and building insurance. The fixed assets are not insured as the cost of insuring them is greater than the value of the assets.

5b. Warehousing and inventory management

5.5 Do warehouse facilities have adequate physical security?

Yes Low 1 Inventory is stored in a locked cupboard in the administration. The building has an alarm system and security cameras. The key is maintained by the two members of reception staff.

5.6 Is inventory stored so that it is identifiable, protected from damage, and countable?

Yes Moderate 2 The partner maintains very low volumes of inventory. It is stored on shelving units and separated by item type, e.g. printer paper.

HACT Framework Micro Assessment 5.7 Does the IP have an inventory management system that enables monitoring of supply distribution?

Yes Moderate 4 The reception staff keep track of all the items consumed. This is a manual process which records the name, department, item, quantity and date. This record is maintained in order to identify the rationale for any significant changes in consumption of such items.

5.8 Is responsibility for receiving and issuing inventory segregated from that for updating the inventory records?

N/A N/A - As the value of inventory held by the partner is completely immaterial, they do not maintain inventory records in the accounting system as the cost of doing so would be greater than the value of the inventory.

5.9 Are regular physical counts of inventory carried out? N/A N/A - The value of the inventory is so low that the cost / benefit is not worth carrying out physical counts. The partner only has small quantities of office stationery (pens, paper, printer ink) and cleaning materials.

Total number of questions in subject area: 9

Total number of applicable questions in subject area: 7

Total number of applicable key questions in subject area:

2

Total number of risk points: 12

Risk score 1.71

Area risk rating Low

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

6. Financial reporting and monitoring

6.1 Does the IP have established financial reporting procedures that specify what reports are to be prepared, the source system for key reports, the frequency of preparation, what they are to contain and how they are to be used?

Yes Low 1 The partner prepares annual financial statements in accordance with Brazilian legislation. The also prepare monthly management accounts. For each project, the reports are prepared in accordance with the project agreement, with regards to content and frequency.

6.2 Does the IP prepare overall financial statements? Yes Low 1 The partner prepares annual financial statements, in addition to their other reporting requirements for donors. The annual financial statements include the Balance Sheet, Income Statement (deficit or surplus), Cash Flow Statement, Statement of Changes in Equity, and annual management report.

HACT Framework Micro Assessment 6.3 Are the IP’s overall financial statements audited regularly by an independent auditor in accordance with appropriate national or international auditing standards? If so, please describe the auditor.

Yes Low 1 The partner undergoes external audit annually. The external auditor is currently AudiBanco, but the foundation partner the external auditor every 3 years, with the approval of the board of directors, in accordance with Brazilian law.

6.4 Were there any major issues related to ineligible expenditure involving donor funds reported in the audit reports of the IP over the past three years?

No Low 1 There have not been any major issues related to ineligible expenditure involving donor funds in the past three years.

6.5 Have any significant recommendations made by auditors in the prior five audit reports and/or management letters over the past five years and have not yet been implemented?

No Low 1 There are no major recommendations that have not been implemented for the past five years.

6.6 Is the financial management system computerized?

Yes Low 1 The partner uses a computerised financial management system, the accounting software the use is WK Sistema.

6.7 Can the computerized financial management system produce the necessary financial reports?

Yes Low 1 The accounting software produces the necessary reports.

6.8 Does the IP have appropriate safeguards to ensure the confidentiality, integrity and availability of the financial data? E.g. password access controls; regular data back-up.

Yes Low 1 The financial management system has access control, segregation of function, auditing (when applicable), individualized password control, and daily backup of information.

Total number of questions in subject area: 8

Total number of applicable questions in subject area: 8

Total number of applicable key questions in subject area:

3

Total number of risk points: 8

Risk score 1.00

Area risk rating Low

HACT Framework Micro Assessment

Subject area (key questions in bold)

Yes No N/A Risk Assessment

Risk points

Remarks/comments

7. Procurement and contract administration

7a. Procurement

7.1 Does the IP have written procurement policies and procedures?

Yes Low 1 FEESC follows the government decree no. 8.241 from the 21st of May 2014, purchasing law no. 8.666 from 21st June 1993, purchasing law no. 10.520 from 17th June 2002, in addition to their own internal purchasing policy (which is predominantly based on the government decree). The partner will follow the appropriate guidelines based firstly on whether the purchase is being made with government or private funds and the policies of each donor. The head of the purchasing sector will identify the policy to be followed for each purchase. The partner's computerised procurement system also provides guidance on which policy should be followed.

7.2 Are exceptions to procurement procedures approved by management and documented ?

Yes Low 1 Exceptions will be dealt with by the board, and legal advice sought if necessary. With regards to project expenditure, in case of exception the project technician will contact the donor for approval.

7.3 Does the IP have a computerized procurement system with adequate access controls and segregation of duties between entering purchase orders, approval and receipting of goods? Provide a description of the procurement system.

Yes Low 1 FEESC has a computerised procurement system. For project expenditure, the project technician will submit requests to the purchasing department if they are within the budget. The purchasing technician will then obtain quotes, which then need to be approved by the project technician and purchasing manager. The purchase order can then be raised by the purchasing technician and forward on to the finance department for payment approval. Goods are received by the reception staff and registered in the system by the accounting team.

7.4 Are procurement reports generated and reviewed regularly? Describe reports generated, frequency and review & approvers.

Yes Low 1 The purchasing department sends a daily report to each member of the department and the Executive Management, reporting all procurement processes for which have been delivered by the suppliers. Another report is also emailed on a daily basis which identifies duplicates purchases for projects. There is also a report of any procurement processes that have been at the same stage for more than one day.

HACT Framework Micro Assessment 7.5 Does the IP have a structured procurement unit with defined reporting lines that foster efficiency and accountability?

Yes Low 1 The IP has a separate structured procurement unit which is split into the following sections: - contracts - imports - direct purchases

7.6 Is the IP’s procurement unit resourced with qualified staff who are trained and certified and considered experts in procurement and conversant with UN / World Bank / European Union procurement requirements in addition to the a IP's procurement rules and regulations?

Yes Moderate 2 All procurement staff are well qualified with relevant training. All staff are familiar with external agency procurement requirements. The head of the purchasing sector will always identify the purchasing regulations to be followed for each purchase.

7.7 Have any significant recommendations related to procurement made by auditors in the prior five audit reports and/or management letters over the past five years and have not yet been implemented?

No Low 1 No significant recommendations related to procurement have been made.

7.8 Does the IP require written or system authorizations for purchases? If so, evaluate if the authorization thresholds are appropriate?

Yes Low 1 All transactions must be approved by a minimum of two managers, regardless of the value.

7.9 Do the procurement procedures and templates of contracts integrate references to ethical procurement principles and exclusion and ineligibility criteria?

No Significant 3 The partner's contract templates do not specifically include references to ethical procurement practices, or supplier ineligibility criteria.

Refer to internal control finding 5.

7.10 Does the IP obtain sufficient approvals before signing a contract?

Yes Low 1 All transactions must be approved by a minimum of two managers, regardless of the value.

7.11 Does the IP have and apply formal guidelines and procedures to assist in identifying, monitoring and dealing with potential conflicts of interest with potential suppliers/procurement agents? If so, how does the IP proceed in cases of conflict of interest?

Yes Low 1 The partner's procurement procedures includes guidelines for dealing with cases of possible conflicts of interest, and the FEESC aims to use preventative measures wherever possible, e.g. reviewing the partners of potential suppliers.

HACT Framework Micro Assessment 7.12 Does the IP follow a well-defined process for sourcing suppliers? Do formal procurement methods include wide broadcasting of procurement opportunities?

Yes Low 1 When sourcing suppliers, the purchasing department will conduct market research, perform a search on their own register and / or on the internet, and in some cases, they will also publish the procurement opportunity on the partner website or in the main newspaper depending on the item/service to be purchased. The partner also requests the company's legal entity certificate, financial details to check company's liquidity, and a referral from one of the suppliers previous customers.

7.13 Does the IP keep track of past performance of suppliers? E.g. database of trusted suppliers.

Yes Moderate 2 Where the partner has experienced difficulties with a supplier, a restriction can be added to the supplier account in order to prevent any future purchases being made with that supplier. However, aside from the restriction the partner does not specifically maintain a database of past supplier performance, although this was something that the partner previously planned to implement.

Refer to internal control finding 6.

7.14 Does the IP follow a well-defined process to ensure a secure and transparent bid and evaluation process? If so, describe the process.

Yes Low 1 The supplier selection process and the related procurement procedures are documented in the purchasing regulation followed by the partner. The process is transparent. Please see 7.10 and 7.12 for further details.

7.15 When a formal invitation to bid has been issued, does the IP award the contract on a pre-defined basis set out in the solicitation documentation taking into account technical responsiveness and price?

Yes Low 1 The supplier is selected based on the lowest price who has also complied with the technical requirements

7.16 If the IP is managing major contracts, does the IP have a policy on contracts management / administration?

Yes Low 1 The partner has a specific contract department, within the purchasing department, which specifically deals with contracts.

7b. Contract Management - To be completed only for the IPs managing contracts as part of programme implementation. Otherwise select N/A for risk assessment

7.17 Are there personnel specifically designated to manage contracts or monitor contract expirations?

Yes Low 1 The partner has a specific contract department, within the purchasing department, which specifically deals with contracts. Additionally, where required they will contract an external expert (engineer, technician) to monitor the contract implementation.

HACT Framework Micro Assessment 7.18 Are there staff designated to monitor expiration of performance securities, warranties, liquidated damages and other risk management instruments?

N/A N/A - N/A

7.19 Does the IP have a policy on post-facto actions on contracts?

Yes Low 1 This is covered in the partners procurement manual.

7.20 How frequent do post-facto contract actions occur? Yes Low 1 They rarely occur and predominantly relate to extensions to the contract period.

Total number of questions in subject area: 20

Total number of applicable questions in subject area: 19

Total number of applicable key questions in subject area:

5

Total number of risk points: 23

Risk score 1.21

Area risk rating Low

Totals

Total number of questions: 96

Total number of applicable questions: 84

Total number of applicable key questions: 35

Total number of risk points: 113

Total risk score 1.35

Overall risk rating Low