25

Regional Fleet Developments & Impact On MRO Demand: MRO Middle East Brian Kough Director – Forecasts & Analysis Aviation Week Washington, DC

| Date post: | 19-Jul-2015 |

| Category: |

Business |

| Upload: | reyyan-demir |

| View: | 618 times |

| Download: | 4 times |

Confidential and Proprietary. Copyright © 2013, Aviation Week

Regional Fleet Developments & Impact On MRO Demand:

MRO Middle East

Brian Kough Director – Forecasts & Analysis Aviation Week Washington, DC

Copyright © 2014 Penton 2

Regional Fleet Developments & Impact On MRO Demand

Fleet Trends & Outlook

• Middle East fleet changes

• Shorter Service Lives

• “Upgauging” cabin sizes

• The Duopoly continues

• Outlook for deliveries

• Patterns in fleet retirement

Copyright © 2014 Penton 3

Regional Fleet Developments & Impact On MRO Demand

MRO Implications

• Changes in aircraft economic life

• Other factors: Scrappers

• Middle East regional MRO forecast

• Strong CAGR relative to other regions

• Ten-Year MRO market of some $53 billion

• Things to think about “right now”

Copyright © 2014 Penton 4

Regional Fleet Developments & Impact On MRO Demand

Regional Fleet Trends & Outlook

Copyright © 2014 Penton 5

Upgauging: A New ‘Fact Of Life’

…for the largest in class

Increasingly, airlines are opting…

B737-800

B777-300

A330-300

Copyright © 2014 Penton 6

The Duopoly: Airbus & Boeing

Forecast Top Five New Aircraft Deliveries Middle East

777-300 ER & Airbus families dominate the decade’s deliveries

Copyright © 2014 Penton 7

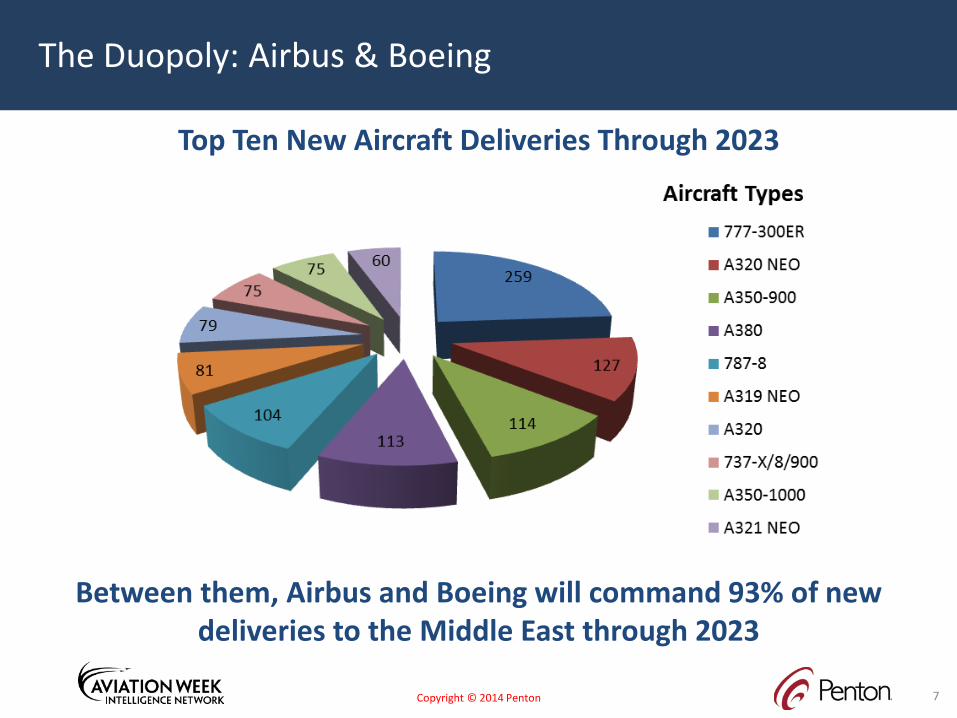

Between them, Airbus and Boeing will command 93% of new deliveries to the Middle East through 2023

The Duopoly: Airbus & Boeing

Top Ten New Aircraft Deliveries Through 2023

Copyright © 2014 Penton 8

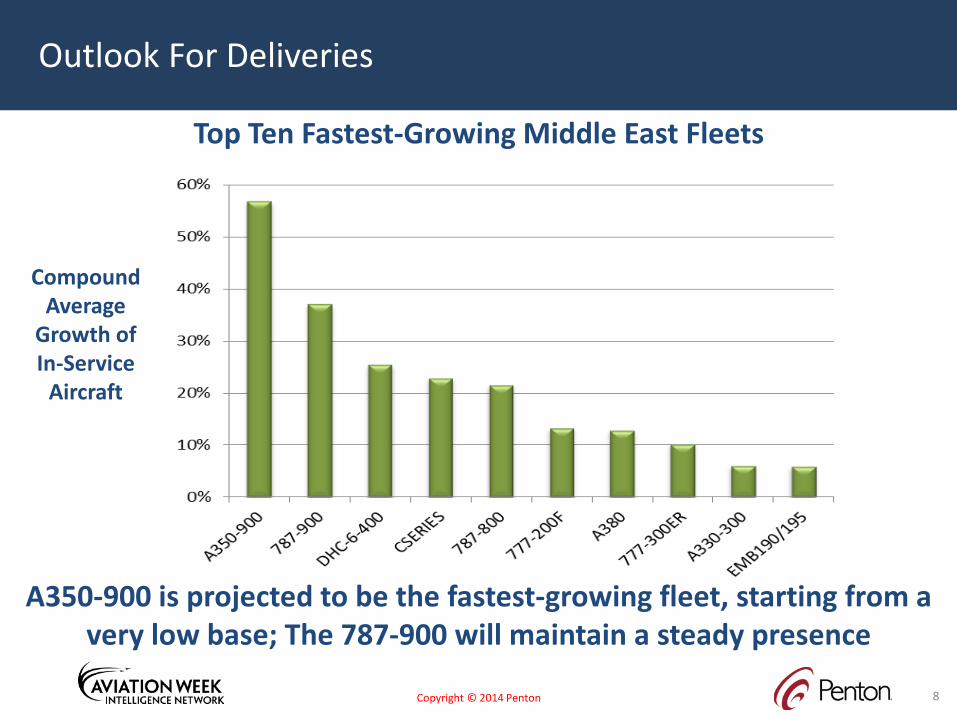

A350-900 is projected to be the fastest-growing fleet, starting from a very low base; The 787-900 will maintain a steady presence

Outlook For Deliveries

Top Ten Fastest-Growing Middle East Fleets

Compound Average

Growth of In-Service

Aircraft

Copyright © 2014 Penton 9

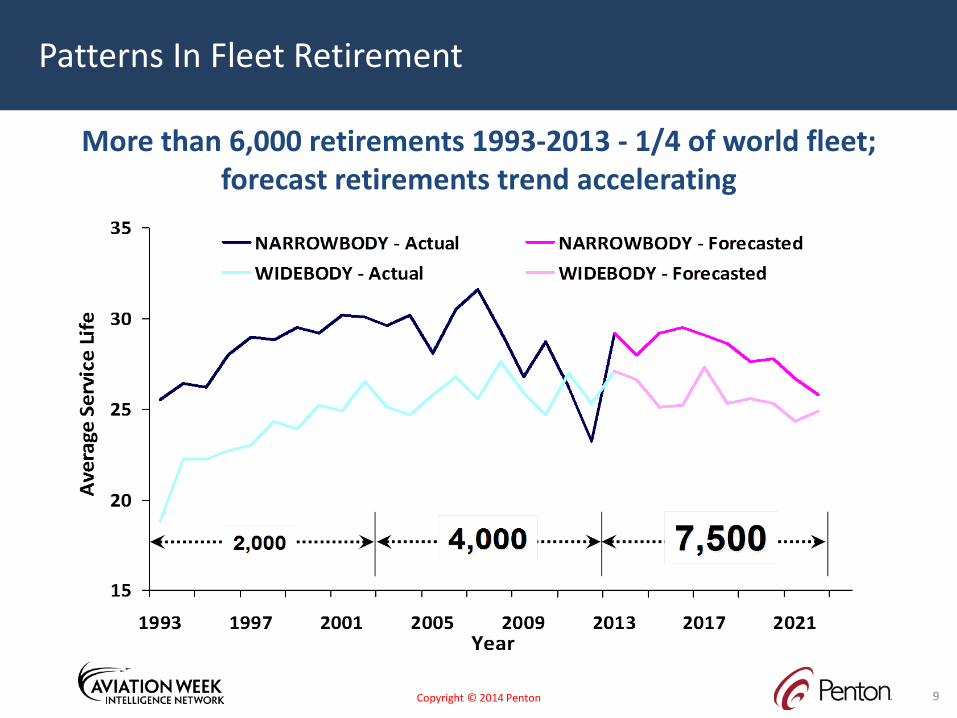

More than 6,000 retirements 1993-2013 - 1/4 of world fleet; forecast retirements trend accelerating

Patterns In Fleet Retirement

Copyright © 2014 Penton

Patterns In Fleet Retirement

Types Seen Retiring in Middle East Fokker 100: most not out until 2021

MD80: most not out until 2020

Airbus 320: the overall fleet grows,

but older aircraft retire at rate of

about 3 per year

A300-600: out by 2017

A310: most out by 2016

747-400

10

A320

B747

Copyright © 2014 Penton

Patterns In Fleet Retirement

11

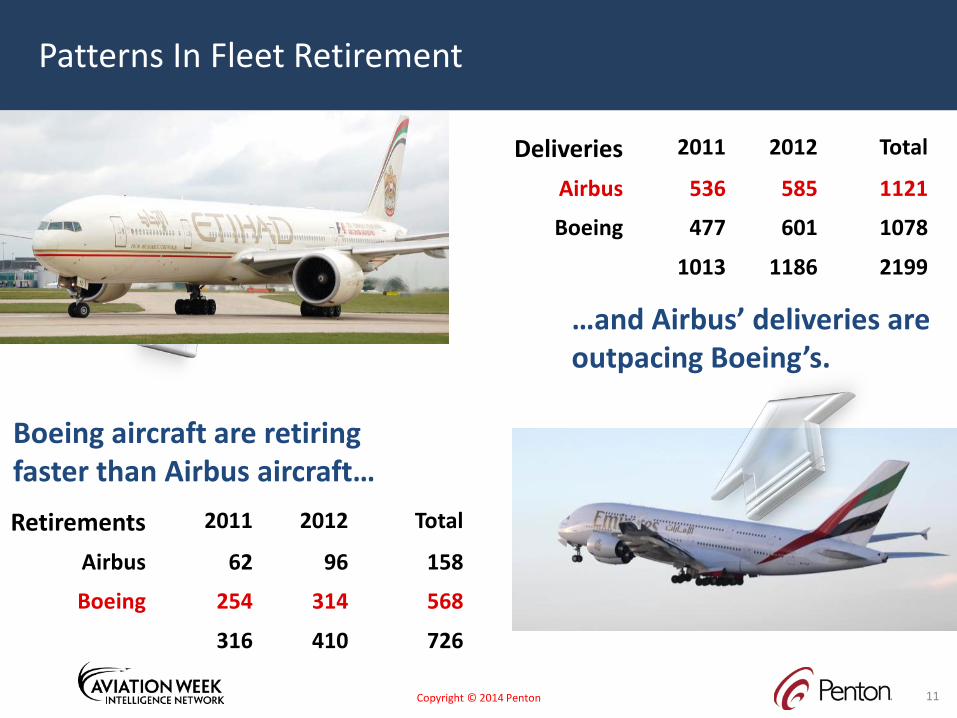

Boeing aircraft are retiring faster than Airbus aircraft…

…and Airbus’ deliveries are outpacing Boeing’s.

Retirements 2011 2012 Total

Airbus 62 96 158

Boeing 254 314 568

316 410 726

Deliveries 2011 2012 Total

Airbus 536 585 1121

Boeing 477 601 1078

1013 1186 2199

Copyright © 2014 Penton

Patterns In Fleet Retirement

12

Net 2012-2013 Airbus fleet growth: 1,014 aircraft Net 2012-2013 Boeing fleet growth: 610 aircraft

Continuously growing worldwide fleet should more than compensate for somewhat younger retirements

Copyright © 2014 Penton

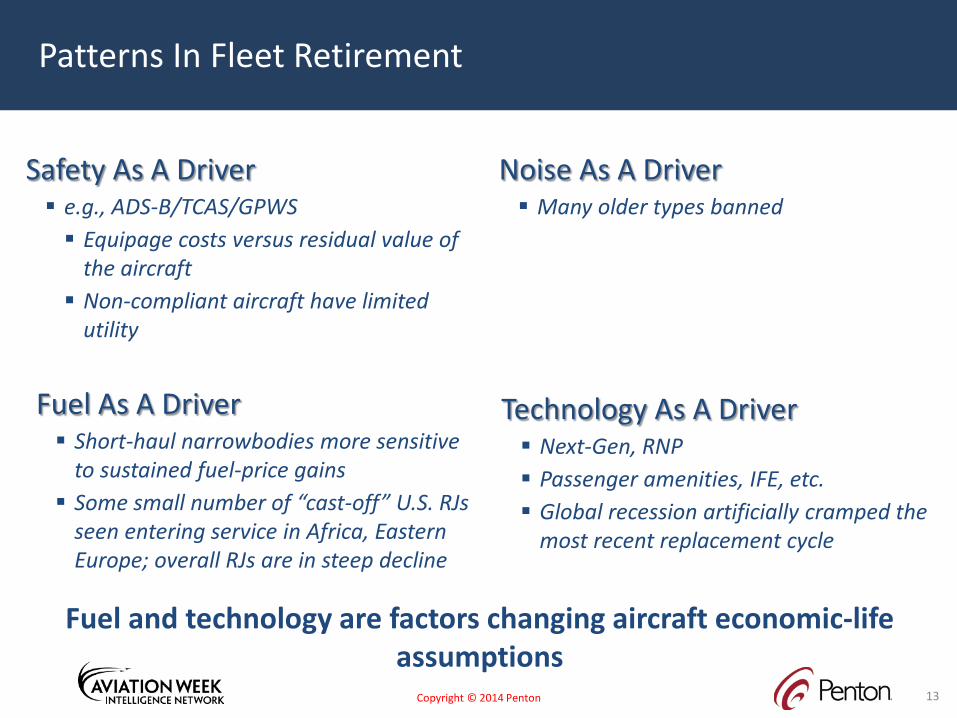

Patterns In Fleet Retirement

Safety As A Driver e.g., ADS-B/TCAS/GPWS Equipage costs versus residual value of

the aircraft Non-compliant aircraft have limited

utility

13

Fuel As A Driver Short-haul narrowbodies more sensitive

to sustained fuel-price gains Some small number of “cast-off” U.S. RJs

seen entering service in Africa, Eastern Europe; overall RJs are in steep decline

Noise As A Driver Many older types banned

Technology As A Driver Next-Gen, RNP Passenger amenities, IFE, etc. Global recession artificially cramped the

most recent replacement cycle

Fuel and technology are factors changing aircraft economic-life assumptions

Copyright © 2014 Penton

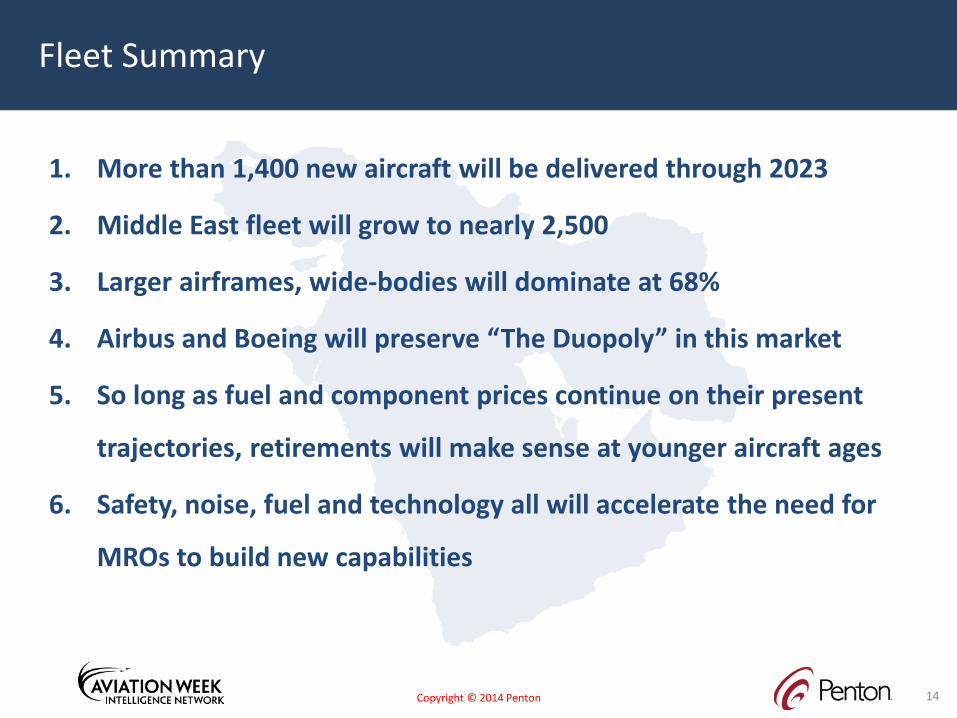

1. More than 1,400 new aircraft will be delivered through 2023

2. Middle East fleet will grow to nearly 2,500

3. Larger airframes, wide-bodies will dominate at 68%

4. Airbus and Boeing will preserve “The Duopoly” in this market

5. So long as fuel and component prices continue on their present

trajectories, retirements will make sense at younger aircraft ages

6. Safety, noise, fuel and technology all will accelerate the need for

MROs to build new capabilities

14

Fleet Summary

Copyright © 2014 Penton 15

MRO Implications

Regional Fleet Developments & Impact On MRO Demand

Copyright © 2014 Penton 16

Changes In Aircraft Economic Life

Increasingly, younger aircraft are going straight to part-out…

This aircraft was less than 13 years old

upon retirement

Copyright © 2014 Penton 17

15

2025

3035

40

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

NB+WB PASSENGER NB+WB FREIGHTER

15

20

25

30

35

40NARROWBODY JETS * WIDEBODY JETS *

2,0002,000retirementsretirements

4,0004,000retirementsretirements

Changes In Aircraft Economic Life

Jet aircraft economic service life may have peaked

Copyright © 2014 Penton 18

Changes In Aircraft Economic Life

Increasingly, younger aircraft are going straight to part-out…

CFM56 components are valuable and sought-after

Airbus A320s are also popular, driven by component needs

Copyright © 2014 Penton 19

Survivor Disappearing Corporation Merged FleetUnited Air Lines Continental Airlines 346Delta Air Lines Northwest Airlines 316Expressjet Airlines Atlantic Southeast Airlines 169US Airways America West Airlines 132Air India Indian Airlines 85Japan Airlines International Japan Air Systems 75China Southern Airlines Zhongyuan Airlines, China Northern, China Xinjiang 72China Eastern Airlines Shanghai Airlines 54Olympic Air Aegean Airlines 53Air China China Southwest Airlines 49SN Brussels Airlines Virgin Express 48Tuifly Hapag-Llyod Express, Hapag-Lloyd Flug 43Kingfisher Airlines Air Deccan 41Flybe Finnair 38Piedmont Airlines Allegheny Airlines 33

Next:American Airlines US Airways 337

Top 15 mergers in the past 10 years affected over 3,400 aircraft

Consolidation Creates Bargaining Power

Copyright © 2014 Penton 20

Average Fleet Size

185201

225

115126

146

0

50

100

150

200

250

2000 2006 2012

Top 50 OperatorsTop 100 Operators

Number of Operators

63

75

98

30

4248

0

20

40

60

80

100

120

2000 2006 2012

50 or More Aircraft in Fleet100 or More Aircraft in Fleet

Consolidation Creates Bargaining Power

Operators worldwide have grown larger, with better bargaining power over MRO costs

Copyright © 2014 Penton 21

On-Airplane MRO Cost

$0.00

$0.50

$1.00

$1.50

$2.00

1960 1970 1980 1990 2000 2010 2020

Technology Year

Cost

$ /

FH

/ 1

000

LB M

TOW Narrowbody

Widebody

Technology, Too, Has Chipped Away At MRO Oppty

Technology has brought down aircraft life-cycle MRO costs

Copyright © 2014 Penton 22

MRO Forecast: Middle East

Aviation Week forecasts a $3.7 billion MRO market in 2014

Engine Maintenance & Component categories are the largest share of the market

Copyright © 2014 Penton 23

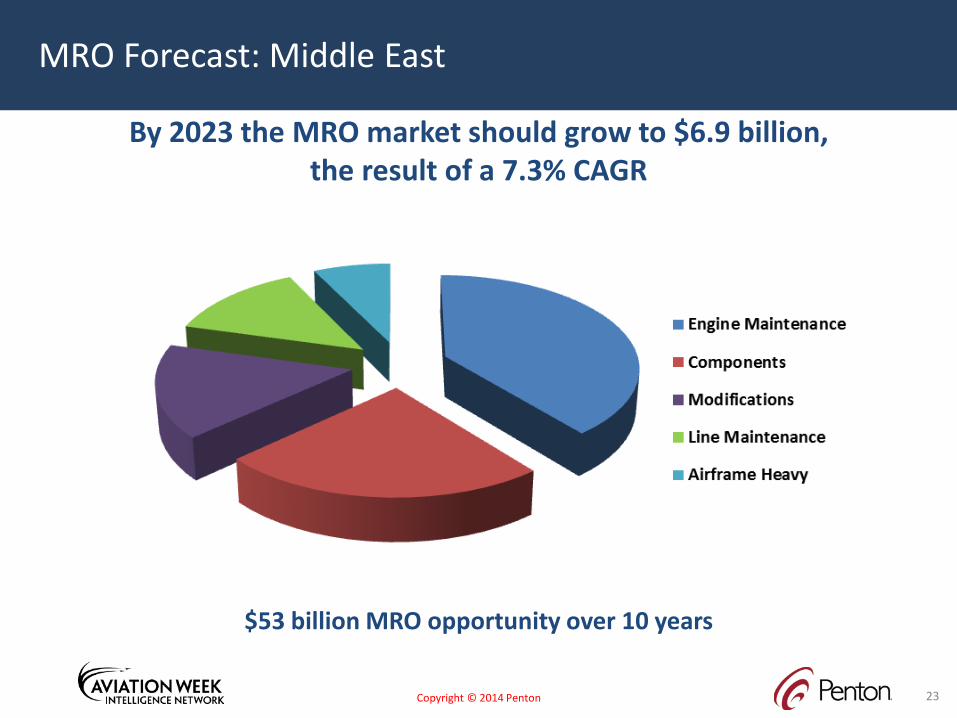

MRO Forecast: Middle East

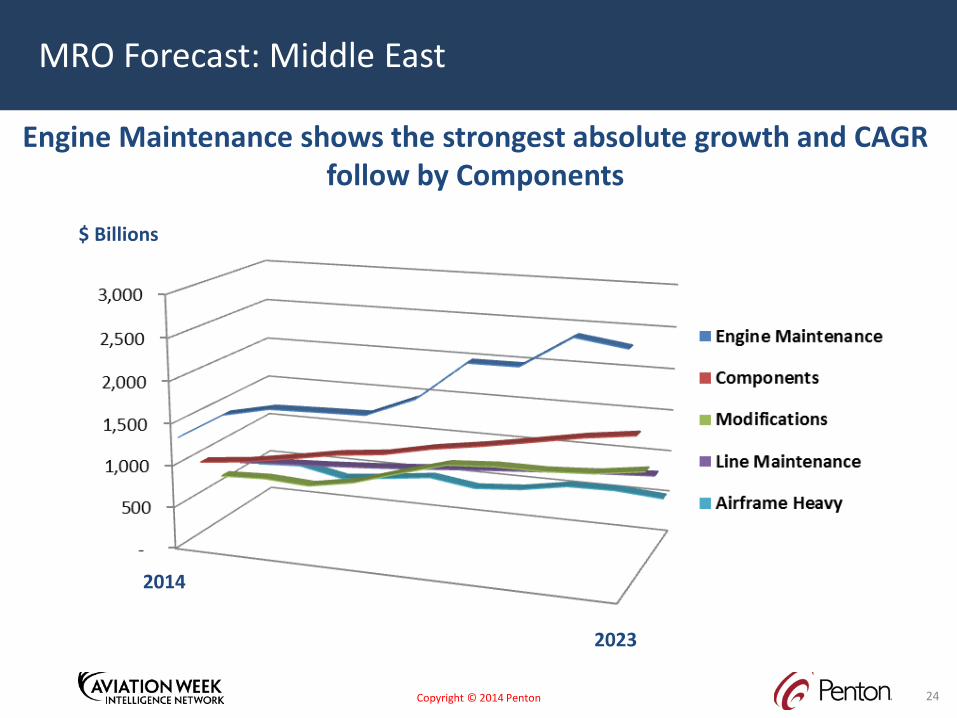

By 2023 the MRO market should grow to $6.9 billion, the result of a 7.3% CAGR

$53 billion MRO opportunity over 10 years

Copyright © 2014 Penton 24

MRO Forecast: Middle East

Engine Maintenance shows the strongest absolute growth and CAGR follow by Components

$ Billions

2014

2023

Copyright © 2014 Penton 25

Take-Aways: Reshaped Fleet, New Imperatives

1. Younger fleet suggests creative service offerings or packages may be inevitable to balance revenue stream

2. Higher number of larger twins. Implications for MROs? Hangar space/shop space/tooling needs?

3. Growth of leasing companies’ share of the overall aircraft portfolio

will lead to more emphasis on margins; parting-out will accelerate unless OEMs adjust

4. Newer, less diverse fleets will boost importance of competence on Airbus and Boeing

5. Engine maintenance is largest share of MRO spending & expands more by 2023