42

Midterm Exam Review Microeconomics Econ EB122 Summer 2012 Inst. Shan A . Garib Mohawk College

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | jeffery-todd |

| View: | 235 times |

| Download: | 1 times |

Midterm Exam ReviewMicroeconomics

Econ EB122 Summer 2012

Inst. Shan A . GaribMohawk College

Opportunity Cost• Opportunity cost: the value of the highest-

valued alternative that must be forgone when a choice is made. It is the evaluation of a trade-off.

• Marginal benefits and costs: the benefits and opportunity costs associated with one additional unit of the good.

Positive and Normative Analysis

• positive economics– Uses science and numbers to describe things– Eg. It is 23 degrees Celsius outside

• normative economics– relies on value judgments to evaluate or

recommend alternative policies

Scarcity the Fundamental Economic Problem

• Scarcity: wants > production • Production is any activity converting resources

in to goods and services

Microeconomics vs. Macroeconomics

• Microeconomics - the study of individual economic agents and individual markets

• Macroeconomics - the study of economic aggregates, the big picture

Simplifying assumptions

• ceteris paribus –all else being equal

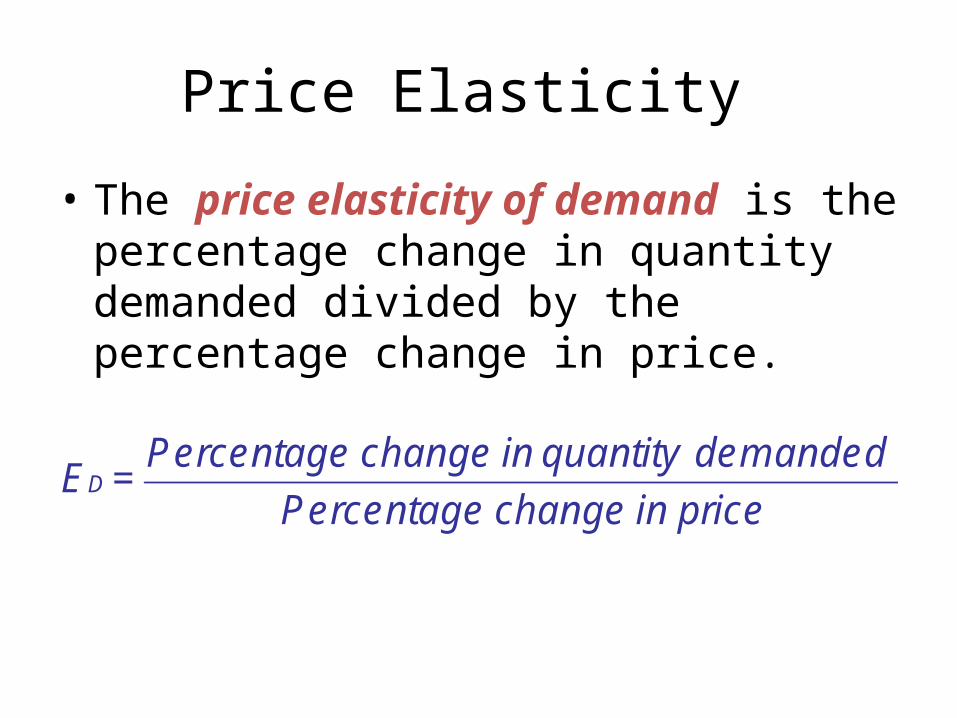

Price Elasticity

• The price elasticity of demand is the percentage change in quantity demanded divided by the percentage change in price.

price in change Percentage

demanded quantity in change Percentage=ED

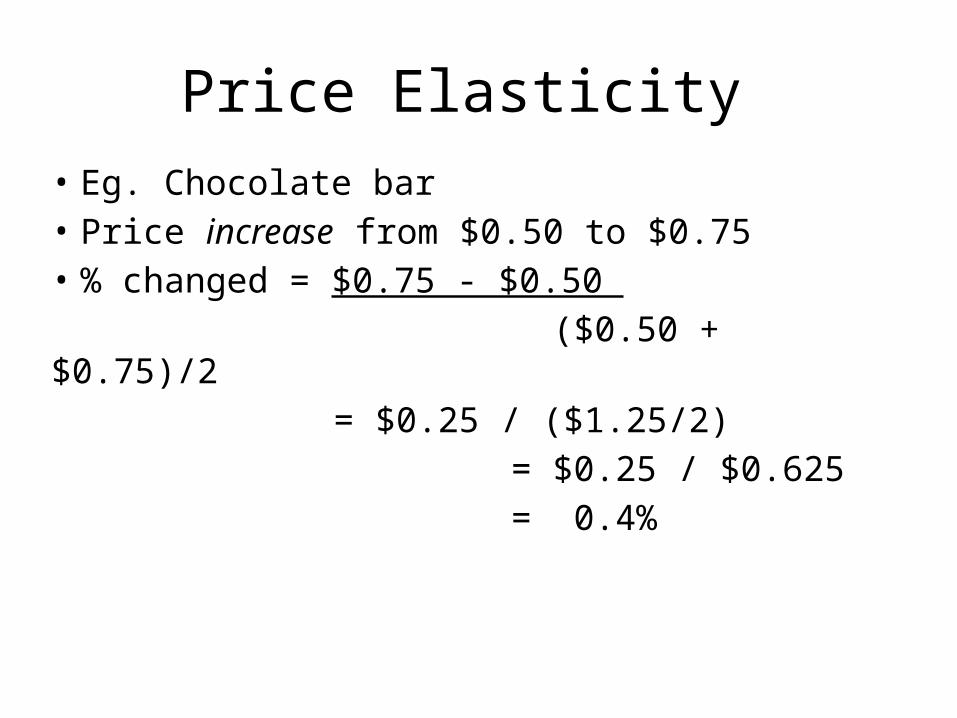

Price Elasticity • Eg. Chocolate bar • Price increase from $0.50 to $0.75• % changed = $0.75 - $0.50 ($0.50 + $0.75)/2

= $0.25 / ($1.25/2) = $0.25 / $0.625 = 0.4%

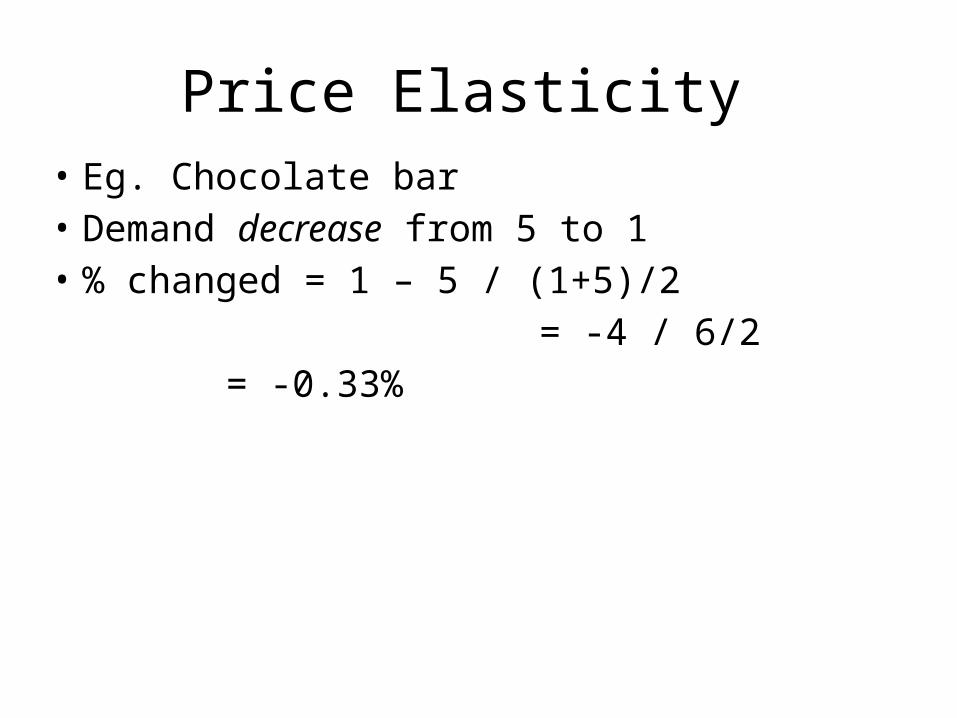

Price Elasticity • Eg. Chocolate bar • Demand decrease from 5 to 1• % changed = 1 – 5 / (1+5)/2 = -4 / 6/2

= -0.33%

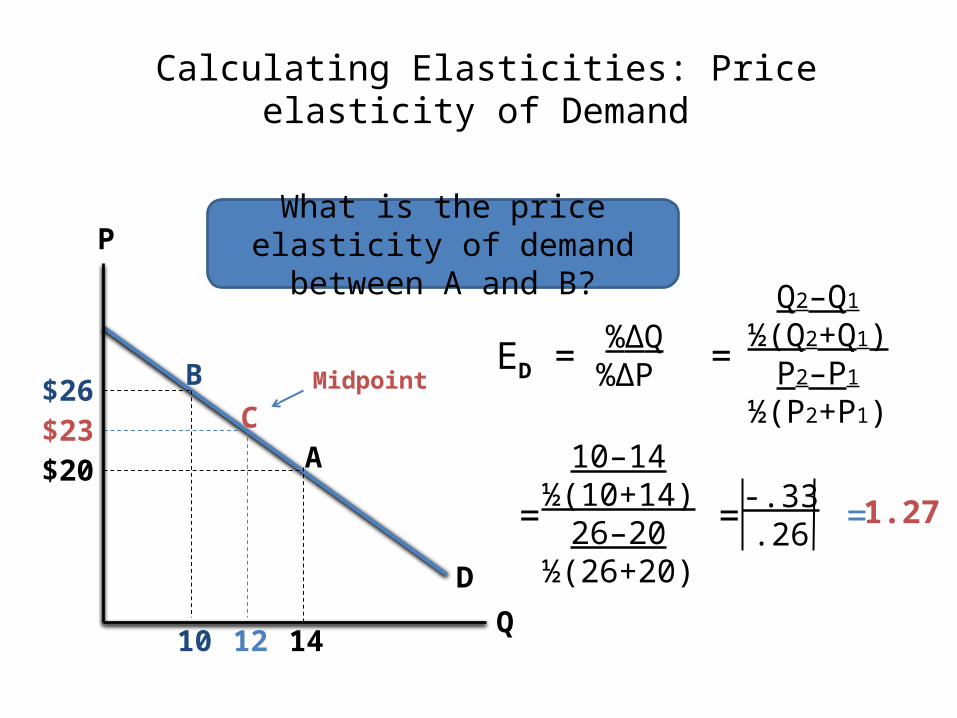

Calculating Elasticities: Price elasticity of Demand

D

P

Q

What is the price elasticity of demand between A and B?

$20

10

$26

14

MidpointB

A

ED = %ΔQ%ΔP

Q2–Q1

½(Q2+Q1)P2–P1

½(P2+P1)

=

C

12

$23

=

10–14½(10+14)

26–20½(26+20)

-.33.26 = 1.27 =

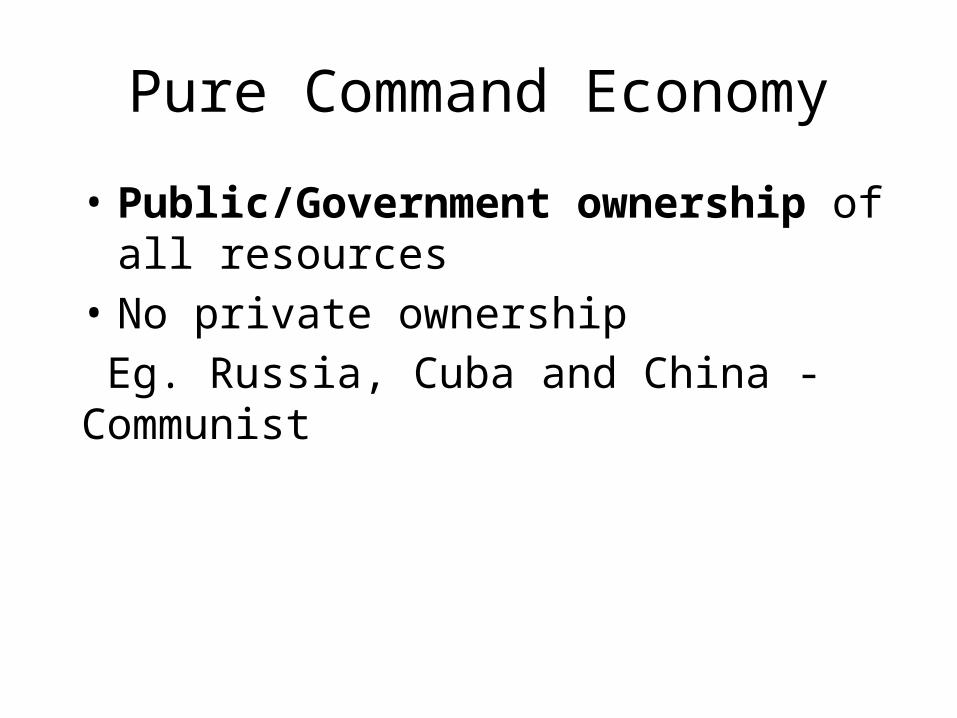

Pure Command Economy

• Public/Government ownership of all resources

• No private ownership Eg. Russia, Cuba and China - Communist

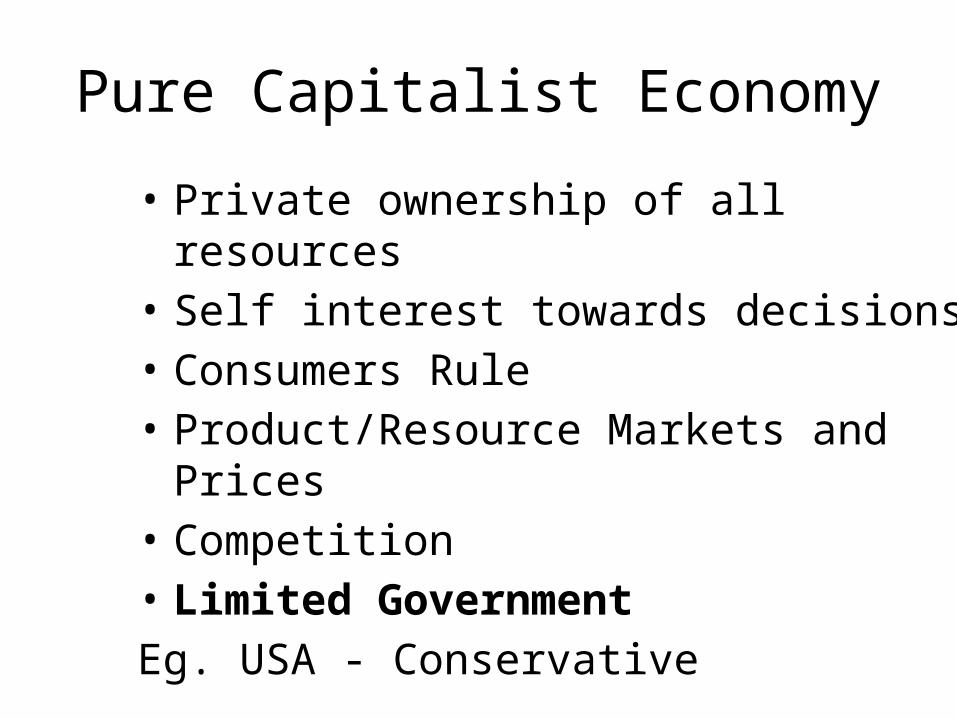

Pure Capitalist Economy

• Private ownership of all resources• Self interest towards decisions • Consumers Rule• Product/Resource Markets and Prices• Competition• Limited Government Eg. USA - Conservative

Mixed Economic System• Public and Private ownership of all resources Eg. Canada - Liberal

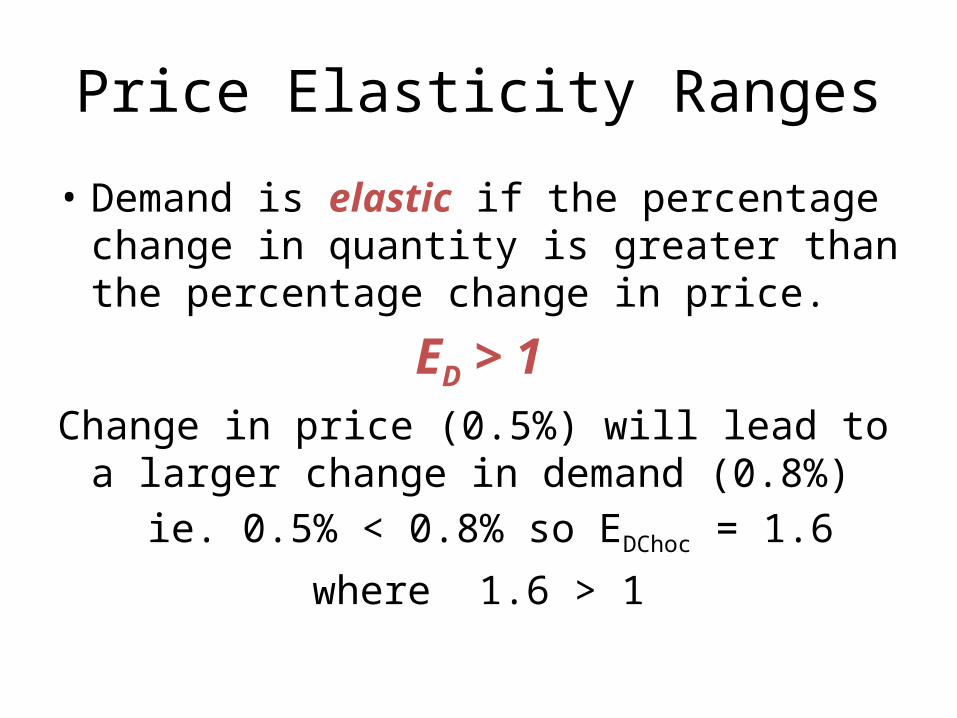

Price Elasticity Ranges

• Demand is elastic if the percentage change in quantity is greater than the percentage change in price.

ED > 1Change in price (0.5%) will lead to a larger

change in demand (0.8%) ie. 0.5% < 0.8% so EDChoc = 1.6

where 1.6 > 1

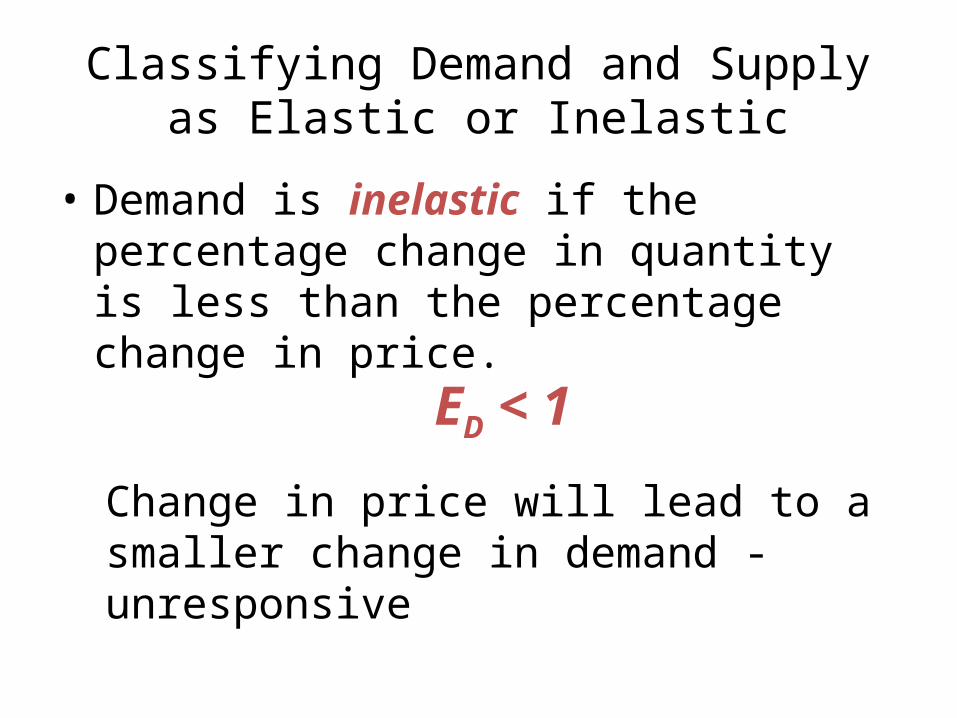

Classifying Demand and Supply as Elastic or Inelastic

• Demand is inelastic if the percentage change in quantity is less than the percentage change in price.

ED < 1

Change in price will lead to a smaller change in demand - unresponsive

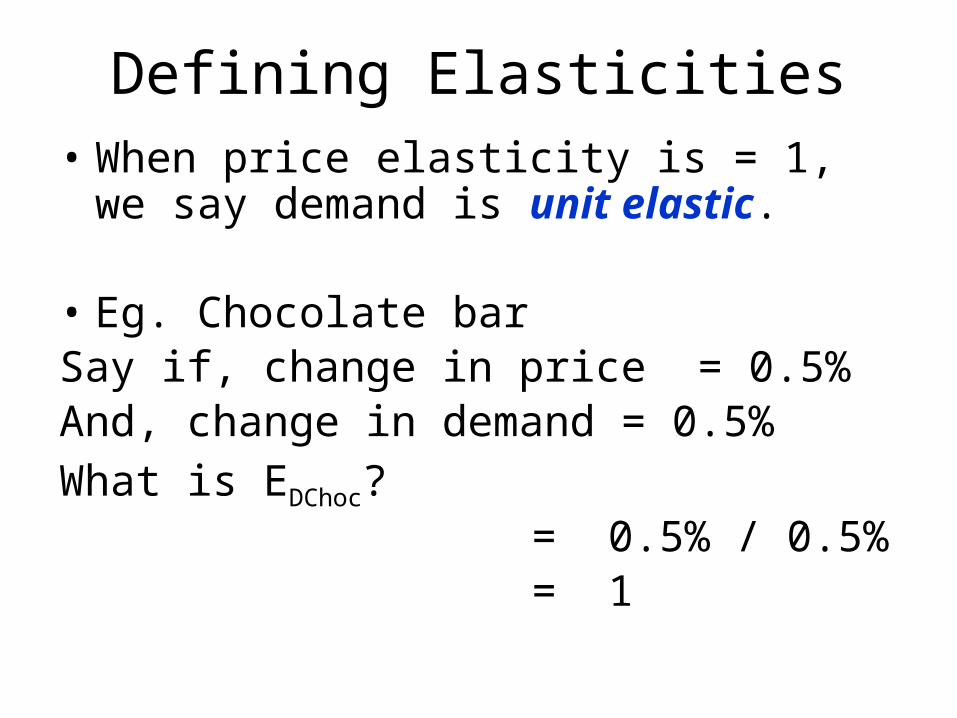

Defining Elasticities• When price elasticity is = 1, we say demand is

unit elastic.

• Eg. Chocolate bar Say if, change in price = 0.5%And, change in demand = 0.5%What is EDChoc?

= 0.5% / 0.5% = 1

Production Possibilities Curve• The production possibilities curve shows the

maximum quantity of goods and services that can be produced when the existing resources are used fully and efficiently.

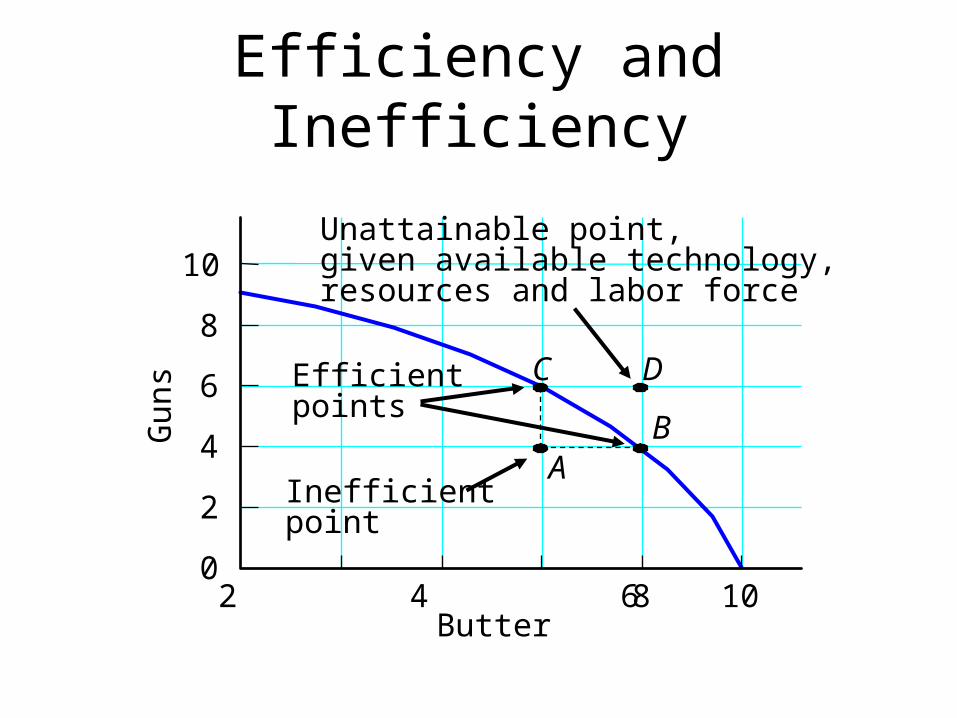

Efficiency and InefficiencyG

uns

10

8

6

4

2

0 2 4 6 8 10

Butter

C D

A

B

Efficientpoints

Inefficientpoint

Unattainable point, given available technology, resources and labor force

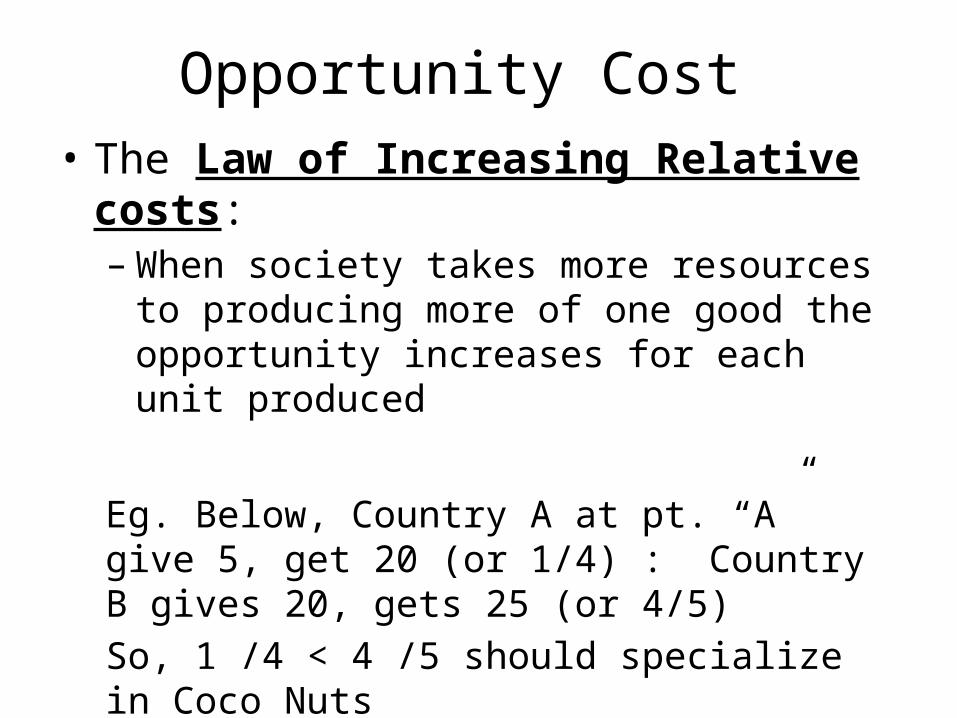

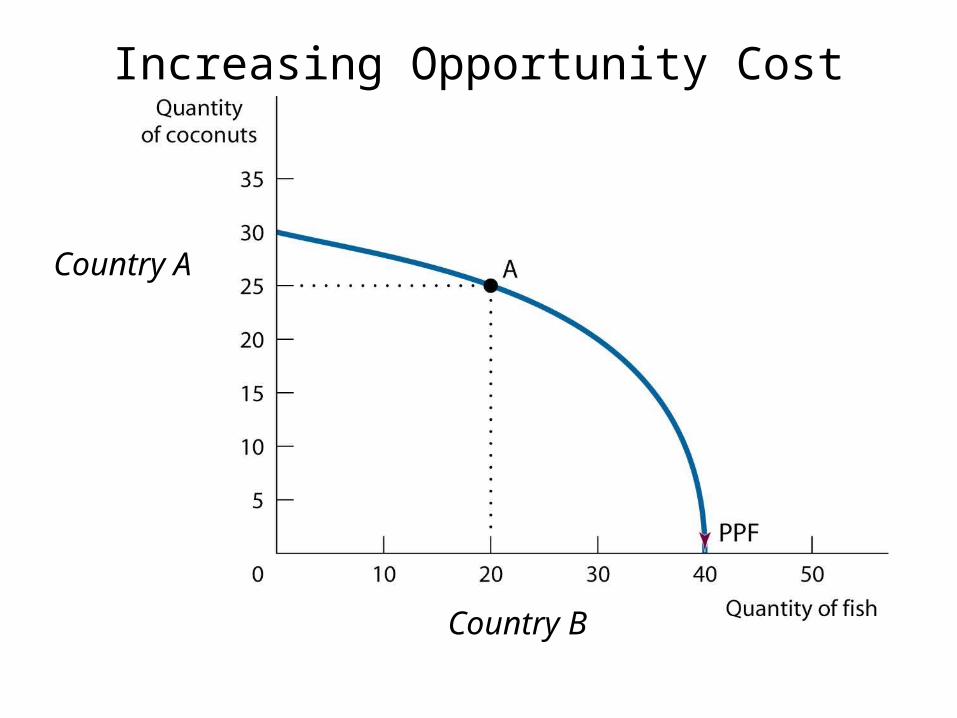

Opportunity Cost • The Law of Increasing Relative costs:

– When society takes more resources to producing more of one good the opportunity increases for each unit produced

Eg. Below, Country A at pt. “A” give 5, get 20 (or 1/4) : Country B gives 20, gets 25 (or 4/5)So, 1 /4 < 4 /5 should specialize in Coco NutsAs move further down curve Country A gives up more then gets ie. Higher OppCost

Increasing Opportunity Cost

Country A

Country B

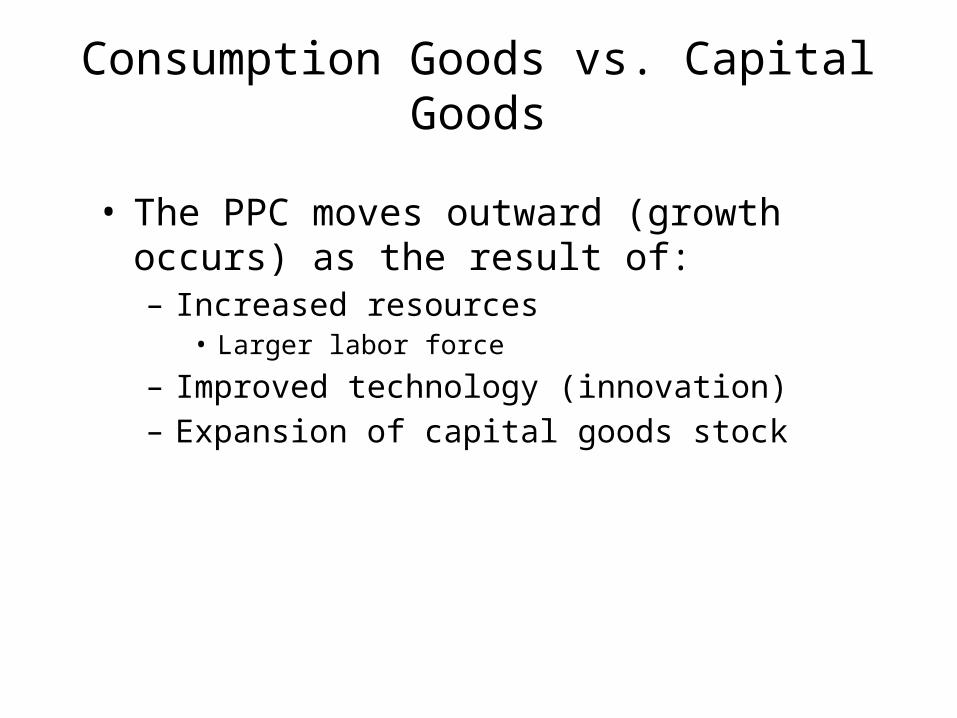

Consumption Goods vs. Capital Goods

• The PPC moves outward (growth occurs) as the result of:– Increased resources

• Larger labor force

– Improved technology (innovation)– Expansion of capital goods stock

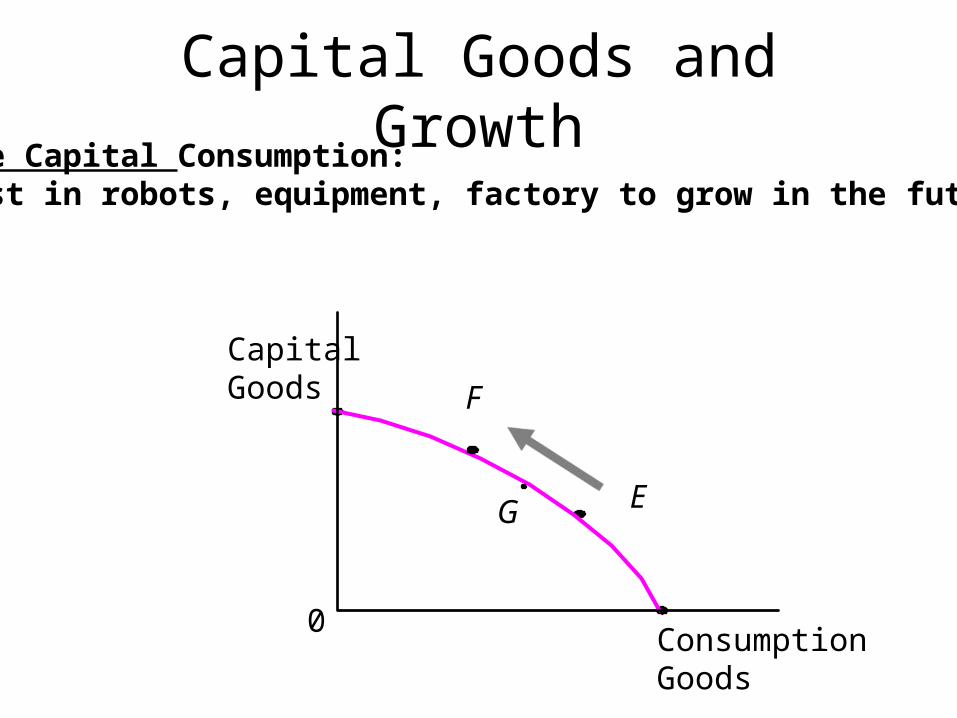

Choose Capital Consumption:-invest in robots, equipment, factory to grow in the future

CapitalGoods

Consumption Goods

0

Capital Goods and Growth

E

F

G

Shifts in the Production Possibility Curve

• More output is represented by an outward shift in the production possibility curve.

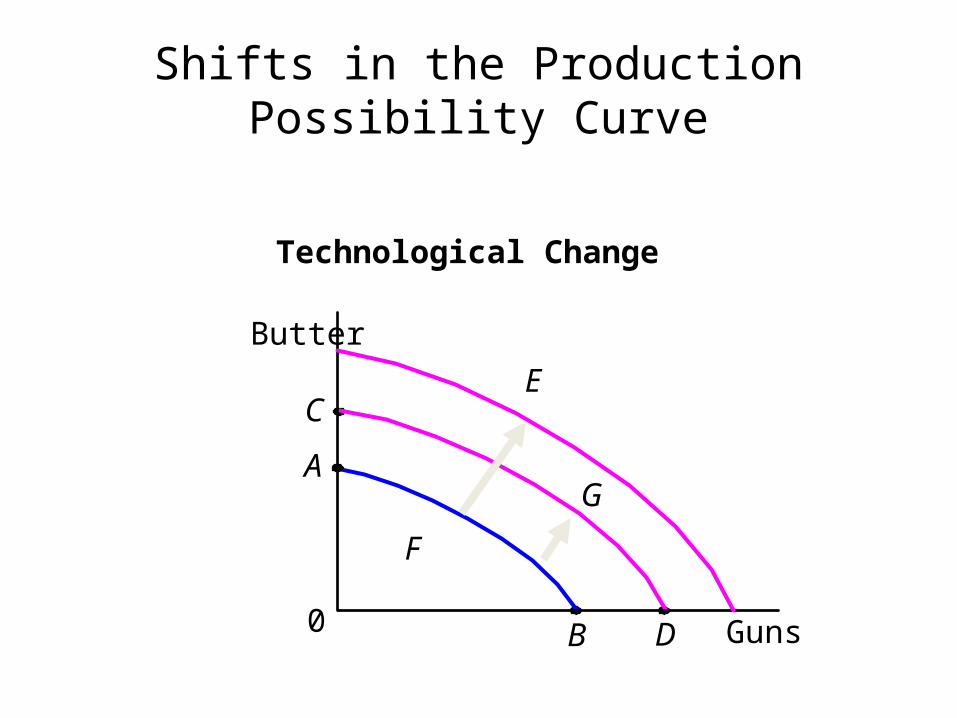

Technological Change

Butter

A

B Guns0

Shifts in the Production Possibility Curve

C

D

E

F

G

Individual versus Market Demand Curves

• A market demand curve is the (horizontal) sum of all individual demand curves.– This is determined by adding the individual

demand curves of all the demanders. Eg everyone’s demand for chocolate bars

The Demand Curve

• The demand curve is the graphic representation of the law of demand.

• The demand curve slopes downward and to the right.

• As the price goes up, the quantity demanded goes down. Inverse relationship between price and quantity demanded

Shifts in Demand through 5 things

TastesTastes

IncomeInferior and Normal Goods

IncomeInferior and Normal Goods

Number of buyers Number of buyers

ExpectationsExpectationsPrices of related goodsSubstitutes and Compliments

Prices of related goodsSubstitutes and Compliments

Price Elasticity

• Elasticity is a measure of the responsiveness of one variable to another.

• Eg. Chocolate bar is $0.50 how many will you buy? 5? If price changes to $1.00, how many will you now demand? 1?– Elasticity measures how your demand will change

if the price changes

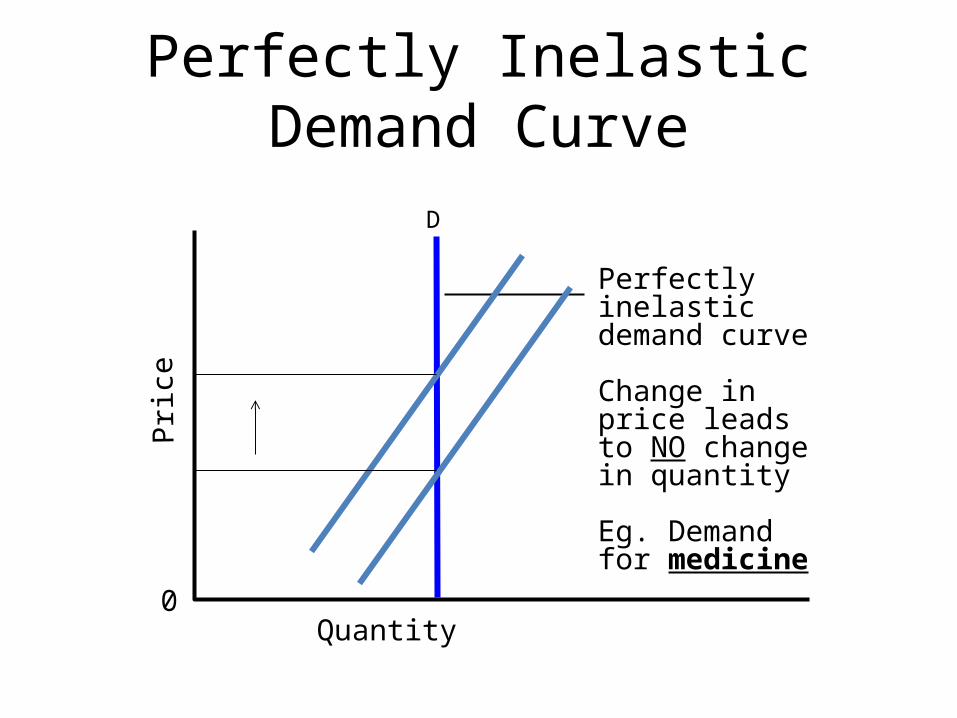

Perfectly inelastic demand curve

Change in price leads to NO change in quantity

Eg. Demand for medicine

Pric

e

0Quantity

Perfectly Inelastic Demand Curve

D

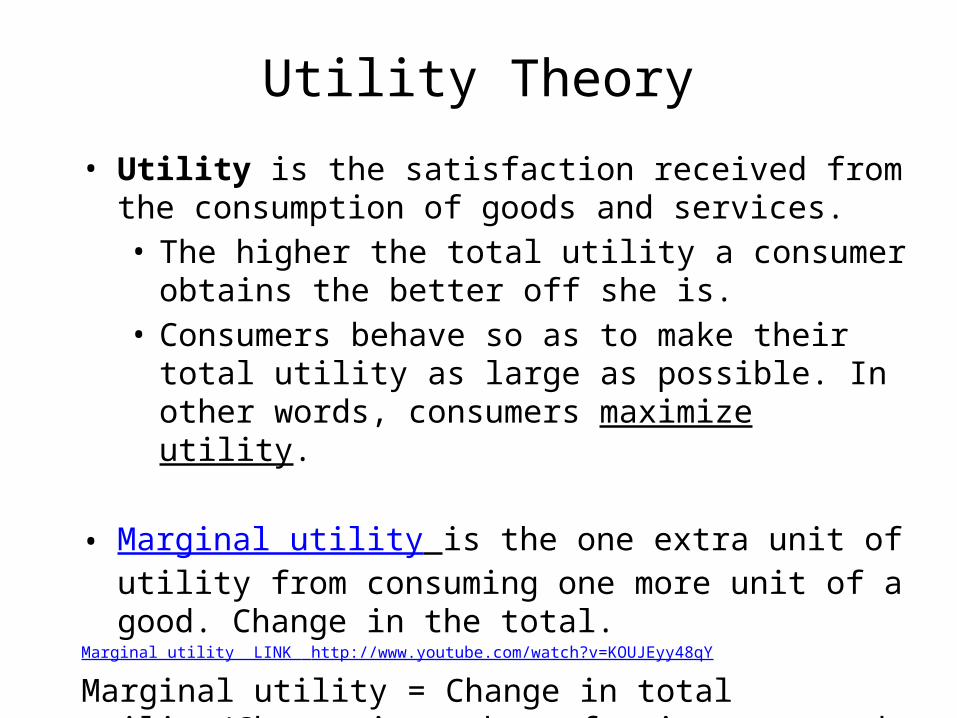

Utility Theory• Utility is the satisfaction received from the consumption of

goods and services. • The higher the total utility a consumer obtains the better

off she is. • Consumers behave so as to make their total utility as large

as possible. In other words, consumers maximize utility.

• Marginal utility is the one extra unit of utility from consuming one more unit of a good. Change in the total.

Marginal utility LINK http://www.youtube.com/watch?v=KOUJEyy48qY

Marginal utility = Change in total utility/Change in number of units consumed

Optimizing Consumption Choices

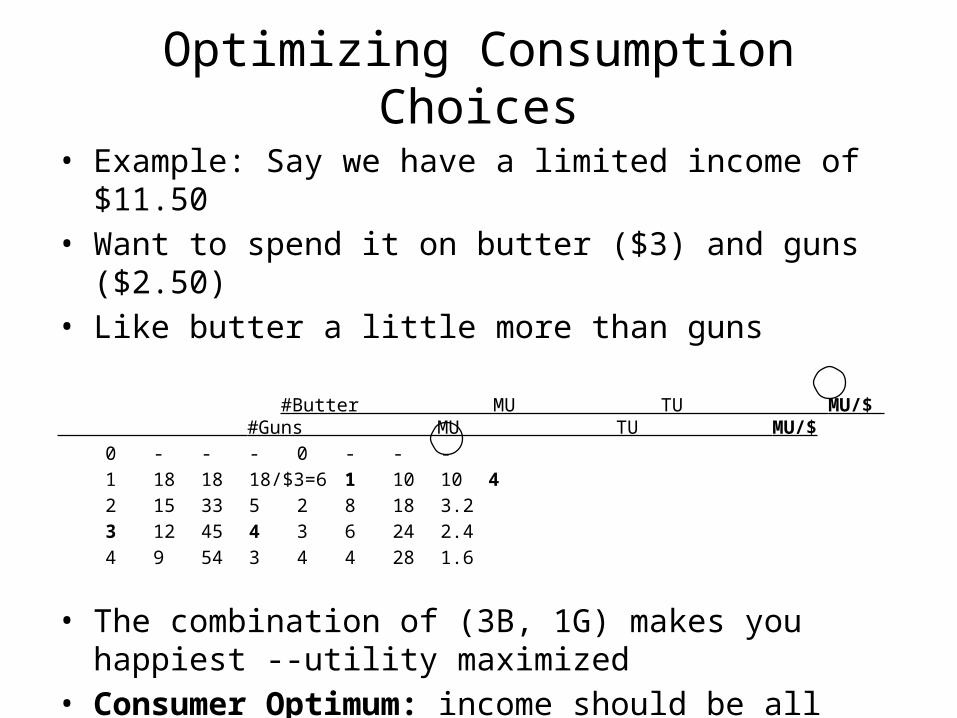

• Example: Say we have a limited income of $11.50• Want to spend it on butter ($3) and guns ($2.50)• Like butter a little more than guns

#Butter MU TU MU/$ #Guns MU TU MU/$0 - - - 0 - - - 1 18 18 18/$3=6 1 10 10 42 15 33 5 2 8 18 3.23 12 45 4 3 6 24 2.44 9 54 3 4 4 28 1.6

• The combination of (3B, 1G) makes you happiest --utility maximized

• Consumer Optimum: income should be all spent so that the last dollar on each gets the same MU

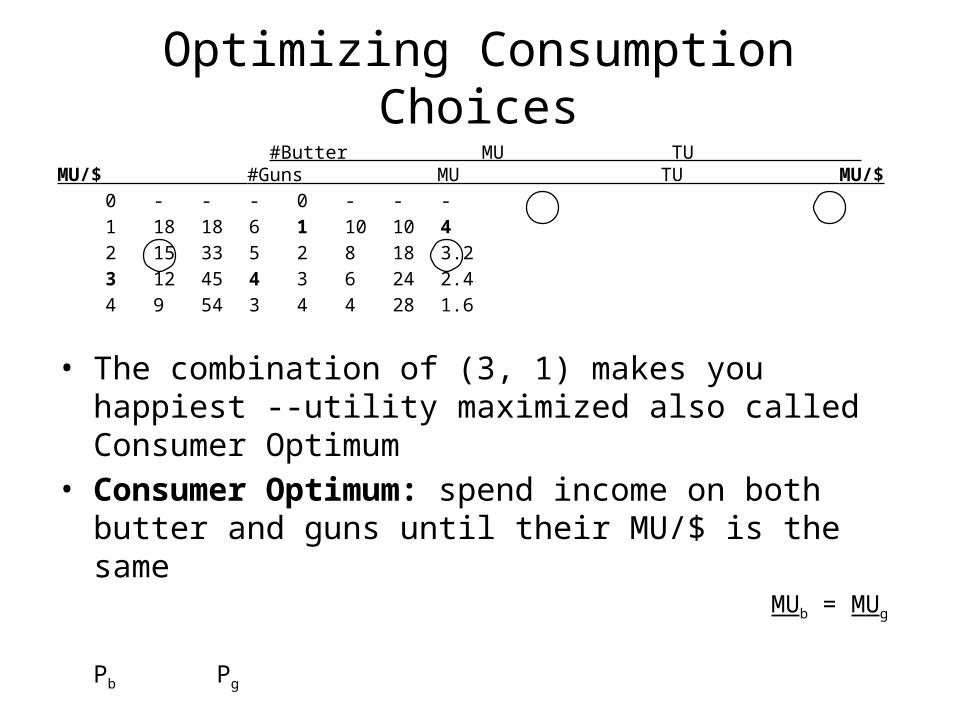

Optimizing Consumption Choices #Butter MU TU MU/$ #Guns MU TU MU/$

0 - - - 0 - - - 1 18 18 6 1 10 10 42 15 33 5 2 8 18 3.23 12 45 4 3 6 24 2.44 9 54 3 4 4 28 1.6

• The combination of (3, 1) makes you happiest --utility maximized also called Consumer Optimum

• Consumer Optimum: spend income on both butter and guns until their MU/$ is the same

MUb = MUg

Pb Pg

or, 12/$3 = 10/$2.50

or, 4 = 4

Complements and Substitutes

• Substitutes are goods that can be used in place of another. Eg. Butter and margarine!

• Substitutes have positive cross-price elasticities.

• As margarine price goes up, demand for butter goes up too!!!

Complements and Substitutes

• Complements are goods that are used in conjunction with other goods.

• Complements have negative cross-price elasticities.

• Eg. Peanut butter and jelly...when the price of up, demand for jelly goes down.

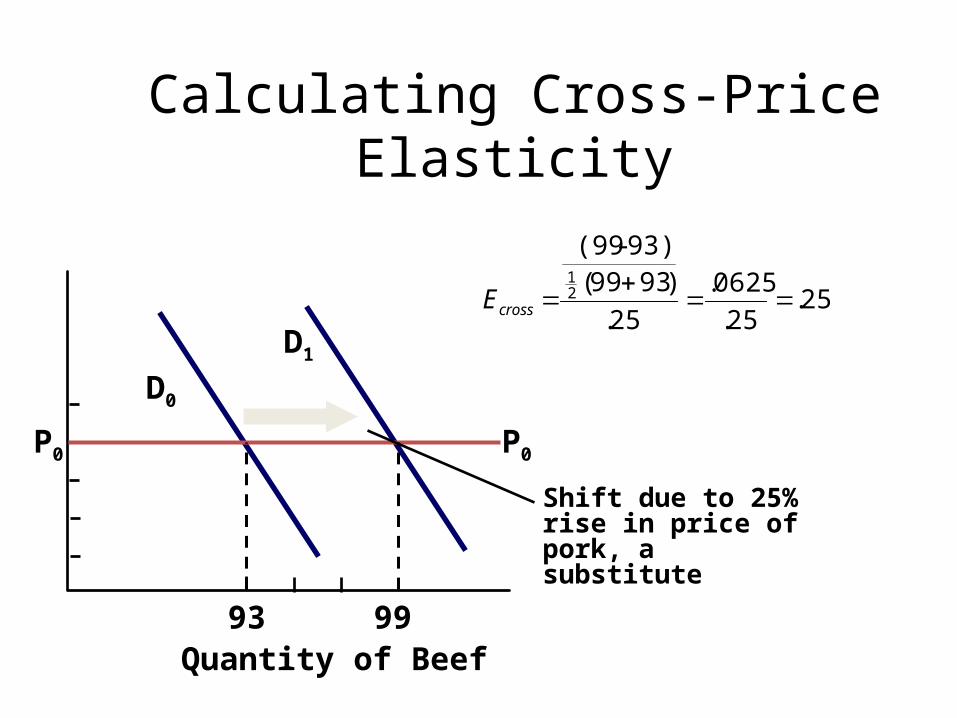

Calculating Cross-Price Elasticity

D0

P0

D1

P0

93Quantity of Beef

99

Shift due to 25% rise in price of pork, a substitute

25.25.

0625.

25.

)9399(93)-(99

21

crossE

Income Elasticity of Demand

• An increase in income generally increases one’s consumption of almost all goods.

• The increase may be greater for some goods than for others.

Income Elasticity of Demand

• Normal goods are those whose consumption increases with an increase in income.

• They have income elasticities greater than zero or positive

Income Elasticity of Demand

• Inferior goods are those whose consumption decreases when income increases.

• Inferior goods have income elasticities less than zero.

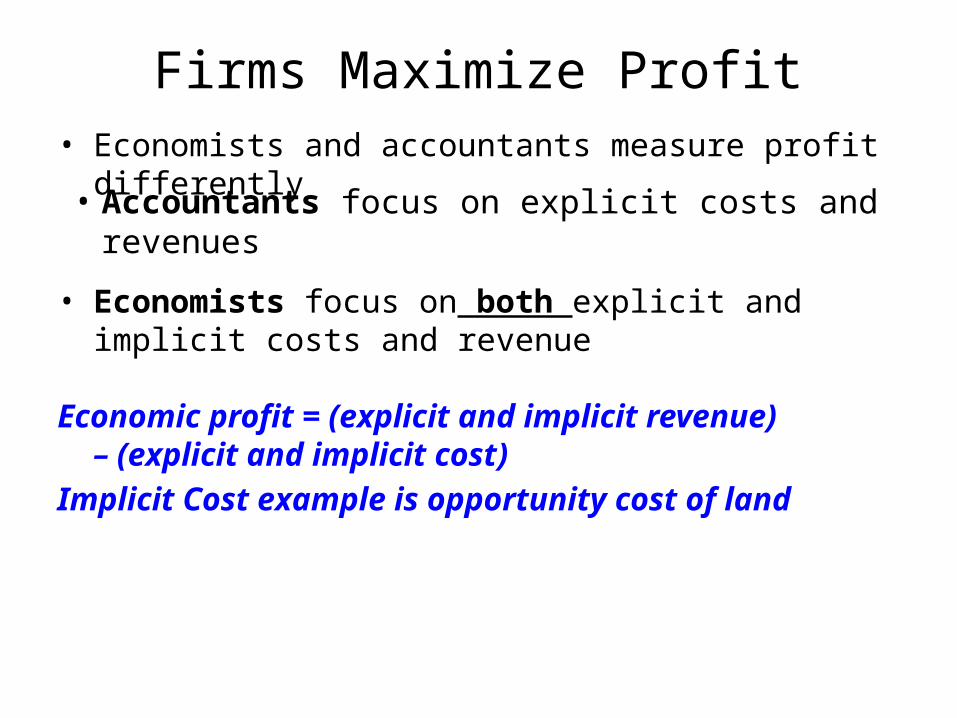

Firms Maximize Profit

• Accountants focus on explicit costs and revenues

• Economists and accountants measure profit differently

• Economists focus on both explicit and implicit costs and revenue

Economic profit = (explicit and implicit revenue) – (explicit and implicit cost)

Implicit Cost example is opportunity cost of land

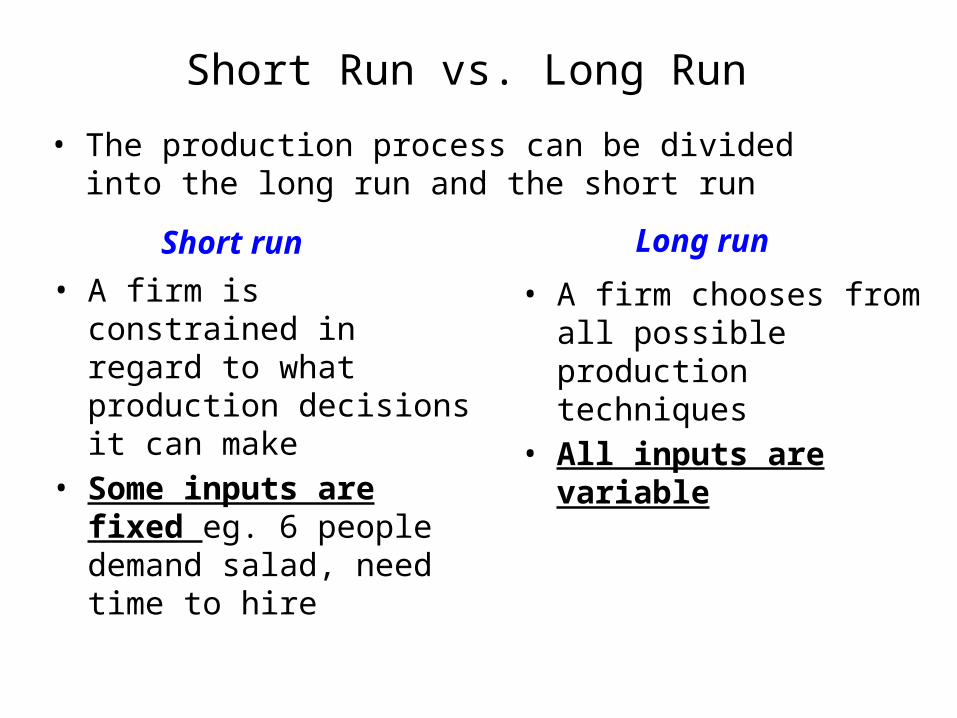

Short Run vs. Long Run

• A firm chooses from all possible production techniques

• All inputs are variable

• The production process can be divided into the long run and the short run

Short run Long run

• A firm is constrained in regard to what production decisions it can make

• Some inputs are fixed eg. 6 people demand salad, need time to hire

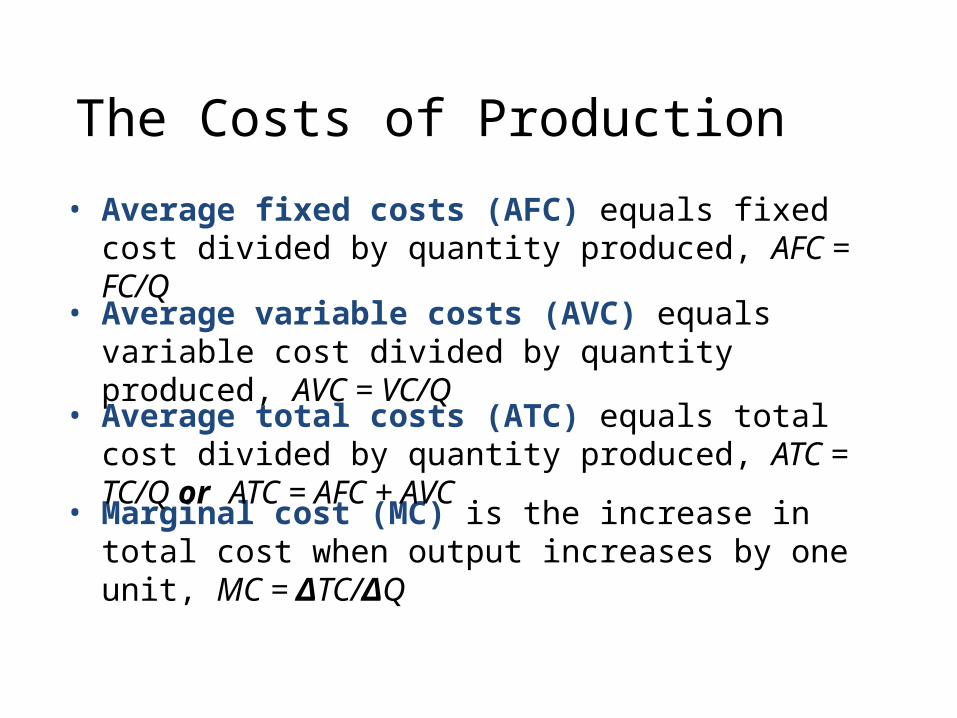

The Costs of Production• Average fixed costs (AFC) equals fixed cost divided

by quantity produced, AFC = FC/Q

• Marginal cost (MC) is the increase in total cost when output increases by one unit, MC = ΔTC/ΔQ

• Average variable costs (AVC) equals variable cost divided by quantity produced, AVC = VC/Q

• Average total costs (ATC) equals total cost divided by quantity produced, ATC = TC/Q or ATC = AFC + AVC

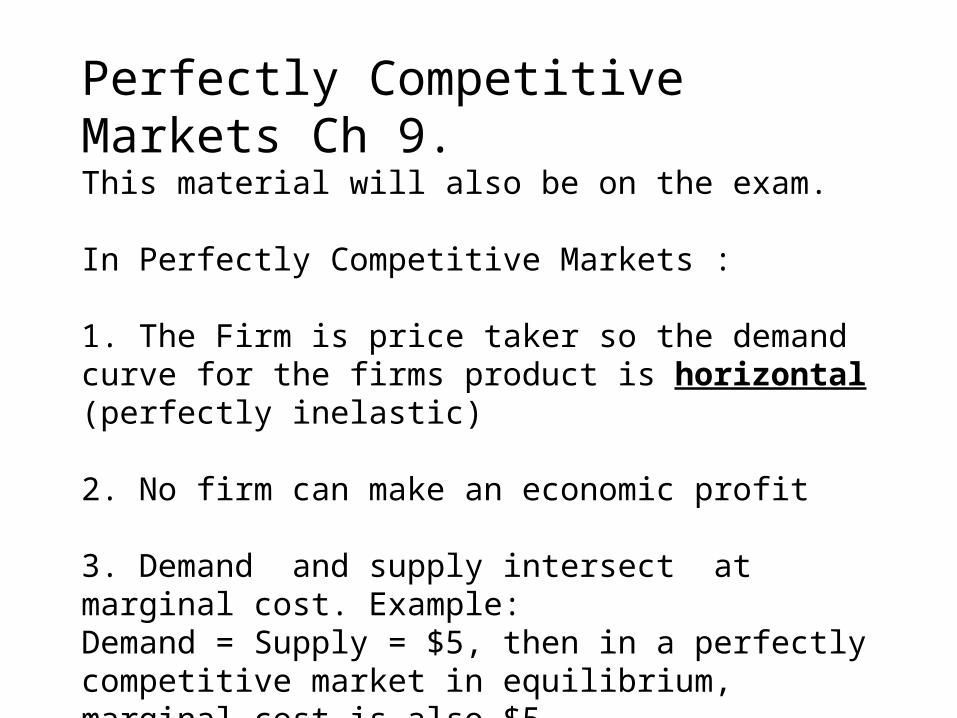

Perfectly Competitive Markets Ch 9.This material will also be on the exam.

In Perfectly Competitive Markets :

1. The Firm is price taker so the demand curve for the firms product is horizontal (perfectly inelastic)

2. No firm can make an economic profit

3. Demand and supply intersect at marginal cost. Example:Demand = Supply = $5, then in a perfectly competitive market in equilibrium, marginal cost is also $5.

In other words, in equilibrium: Demand = Supply = Marginal Cost = $5