FISCAL POLICY INSTITUTE PROJECT REPORT Migration to GST: Preparedness and level of Knowledge, Understanding, Application and Skills of Human Resources in the Government and the Industry Submitted as part of summer internship by Shiva Raman S Indian Institute of Management Lucknow June 2010

Transcript

FISCAL POLICY INSTITUTE

PROJECT REPORT

Migration to GST: Preparedness and

level of Knowledge, Understanding,

Application and Skills of Human

Resources in the Government and the

Industry

Submitted as part of summer internship

by

Shiva Raman S

Indian Institute of Management Lucknow

June 2010

i

Letter of Transmittal

June 12, 2010

Shri P. R. Devi Prasad,

Director,

Fiscal Policy Institute,

Finance Department,

Government of Karnataka,

Bangalore.

Dear Sir,

I am pleased to submit the report, “Migration to GST: Preparedness and level of Knowledge,

Understanding, Application and Skills of Human Resources in the Government and the

Industry” in partial fulfillment of the requirements for the degree of Post Graduate Diploma

in Management. I hereby declare that this is an original work done by me and the findings of

this work have not been previously submitted for any publication.

Please feel free to revert to me with any questions and/or comments regarding this report.

Sincerely

(Shiva Raman S)

Summer Intern

Indian Institute of Management

Enclosure: Final Report

ii

Certificate

This is to certify that the project titled ‘Migration to GST: Preparedness and level of

Knowledge, Understanding, Application and Skills of Human Resources in the

Government and the Industry’ submitted by Shri Shiva Raman S as a part of summer

internship is the result of the work done by him at Fiscal Policy Institute Bangalore, Finance

Department, Government of Karnataka, from April to June 2010 under our guidance.

Place: Bangalore

Date:

Shri P.R. Devi Prasad IES

Director

Fiscal Policy Institute

Finance Department

Government of Karnataka

Place: Bangalore

Date:

Smt Anita V. Nazare

Special Officer

Fiscal Policy Institute

Finance Department

Government of Karnataka

iii

Acknowledgements

I am deeply indebted to Shri P.R. Devi Prasad, Director, Fiscal Policy Institute, Bangalore,

under whose guidance the present study was conducted. He has been giving valuable

suggestions, generous help and corrections during all the phases of the project, without which

the efforts could not have been completed successfully.

I would like to extend my indebtedness and gratitude to Smt. Anita V. Nazare, Special

Officer, FPI, for the invaluable guidance and feedback provided by her at every stage of the

project. She could always find time from her busy schedule to help in this study.

I am indebted to Shri Sameer Hassan MBA, Kum. Munawwara Shakila MBA, and Kum.

Veena N. H MBA, all Consultants at FPI, for their guidance and support from time to time.

I am indebted to Shri J Crasta, President, FKCCI, Shri B T Manohar, Chairman, State Taxes

Committee 2009-10, FKCCI, Shri Subramanyam, Head of Business Research Cell, FKCCI,

and Kum. Lillu Aswataiah, Deputy Secretary, FKCCI for their guidance and invaluable help

in getting responses from Trade and Industry.

I am indebted to the following officials for their guidance and invaluable help in getting

responses.

1. Shri Ajay Seth IAS, Secretary (B&R), FD, GoK

2. Shri Balamurugan K IRS, Additional Commissioner, Large Taxpayers Unit,

Bangalore

3. Shri H D Arun Kumar, J.C.C.T, GoK

4. Shri Pradeep Singh Kharola IAS, C.C.T, GoK

5. Shri Sriram IRS, Additional Director, National Academy of Central Excise and

I am deeply thankful to my fellow interns, Shri Samar Sinh and Shri Laxmikant Jhawar for

their enormous support, guidance and help at every juncture through exchange of ideas and

views on the study.

I am thankful to Officers and Staff at FPI and FPAC who have shown tremendous

cooperation and support throughout the course of study.

iv

I would also like to thank Shri B K Bhattacharya ex-IAS, Chairman, Expenditure Reforms

Commission, Government of Karnataka for his support and encouragement.

I would also like to thank Government of Karnataka for giving me an opportunity to work on

this project at FPI.

I would also like to thank all the respondents for giving their time and invaluable responses

for this study.

I would like to thank Dr. D. Tripati Rao, Professor, IIM Lucknow, for his support and

encouragement.

The author alone is responsible for any errors and omissions.

Shiva Raman S

Summer Intern

Indian Institute of Management

v

Table of Contents

Letter of Transmittal ................................................................................................................................ i

Certificate ................................................................................................................................................ ii

Acknowledgements ................................................................................................................................ iii

Table of Contents .................................................................................................................................... v

List of Figures ....................................................................................................................................... vii

List of Tables ....................................................................................................................................... viii

Abbreviations ......................................................................................................................................... ix

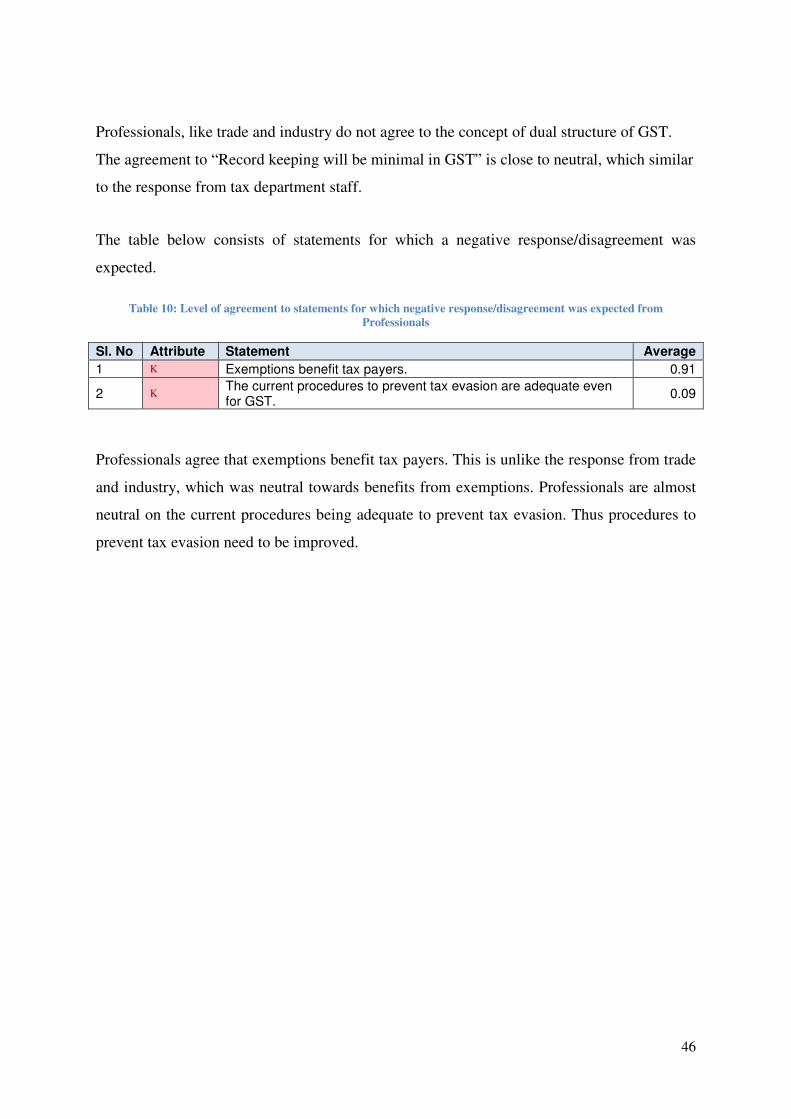

Table 10: Level of agreement to statements for which negative response/disagreement was expected

from Professionals .............................................................................................................. 46

Table 11: Level of agreement to statements for which positive response/agreement was expected from

general public ...................................................................................................................... 50

Table 12: T-Test results for Hypothesis 1 ............................................................................................. 53

Table 13: T-Test results for Hypothesis 2 ............................................................................................. 54

Table 14: Data gathered from general public on awareness and understanding of VAT and GST ...... 85

ix

Abbreviations

ACCT Assistant Commissioner of Commercial Taxes

Addl. CCT Additional Commissioner of Commercial Taxes

ATO Australia Taxation Office

BAS Business Activity Statement

CBDT Central Board of Direct Taxes

CBEC Central Board of Excise and Customs

CBIT Central Board of Indirect Taxes

CCT Commissioner of Commercial Taxes

CENVAT Central Value Added Tax

CGST Central Goods and Services Tax

CRA Canada Revenue Agency

CST Central Sales Tax

CTD Commercial Taxes Department

CTO Commercial Taxes Officer

DCCT Deputy Commissioner of Commercial Taxes

EC Empowered Committee

GoI Government of India

GoK Government of Karnataka

GST Goods and Services Tax

GSTSAO GST Start-Up Assistance Office

HST Harmonised Sales Tax

IGST Integrated Goods and Services Tax

ITD Income Tax Department

JCCT Joint Commissioner of Commercial Taxes

KUAS Knowledge, Understanding, Application and Skills

LTU Large Taxpayers Unit

MODVAT Modified Value Added Tax

PAYG Pay-As-You-Go

PST Provincial Sales Tax

QST Quebec Sales Tax

RQ Revenue Quebec

SGST State Goods and Services Tax

TINXSYS Tax Information Exchange System

TRPS Tax Return Preparers Scheme

VAT Value Added Tax

1

1 Introduction

In the Union budget 2007-08, the then finance minister proposed that India should move

towards a national level GST, with the Centre and the States sharing revenue. He had further

proposed to set April 1, 2010 as the date for introducing GST1. There was much

disappointment for everyone who expected Budget 2010 to lay out the plan for goods and

services tax (GST) rollout. GST was postponed to April 1, 2010. The earlier deadline of April

1, 2010 was missed because of disagreement between the Centre and the states on many areas

of GST. Some of the areas of differences include threshold limit, exemption list, revenue-

neutral rate and constitutional amendments. In his budget speech (2010), the Union Finance

Minister said that the indirect tax administrations at the Centre and the States needed to

revamp their internal work processes based on the use of Information Technology.

The existing VAT system was implemented by the States beginning April 1, 2003 replacing

the State Sales Tax system. The VAT system removed the problem on “tax on tax” and the

burden of cascading effect. Since set-offs benefits can be availed only if tax is paid on the

inputs and previous purchase, this created a built-in check in the VAT system which resulted

in transparency and reduction in tax evasion. VAT reduced the heterogeneity in the tax

structure across States which other-wise resulted in distortion and shifting of trade from one

State to another.

Still the VAT structure at the Centre and the State had deficiencies2. The CENVAT does not

include several central taxes such as surcharges, additional excise duty, etc. It also does not

capture the value-additions in the distributive trade below the manufacturing level. The State

level VAT does not include several taxes such as luxury tax, entertainment tax, etc. Further

the load on CENVAT is included in the value of goods to be taxed under State VAT.

1.1 Objectives of GST

GST will be an improvement over the existing Value Added Tax (VAT) system. Introduction

of GST will remove the cascading effect on CENVAT and also subsume several taxes. GST

will provide more support to trade and industry through wider coverage of input tax credit,

subsuming of several taxes and phasing out of CST. Though increase is revenue is not an

1 First Discussion Paper on GST, section 1.2 2 The primary deficiencies can be found in “GST Reforms and Intergovernmental Considerations in India” section 2

2

objective, GST can increase revenue for both Centre and State through widening of tax base

and increase in tax compliance. Both the industry and the government can benefit from GST.

The objectives of GST3 are given below:

• The incidence of tax should fall only on domestic consumption

• To optimize efficiency and equity of the system

• There should be no export of taxes across taxing jurisdictions

• The Indian market should be integrated into a common market

• To enhance the cause of cooperative federalism

1.2 Recent progress in implementation of GST

In January 2010, the discussion on GST between the Centre and the States was inconclusive

on compensation. The States have been insisting for compensation from GoI to offset any

loss in revenue during the initial stages. Though the States will gain from levy of service

taxes, they will lose revenue mainly because of removal of the cascading effect, payment of

input tax credit and phasing out of CST4. States also fear that the proposed constitutional

amendments to create a common market across India in GST may take away their fiscal

autonomy. Even with revenue neutral rates, it will be difficult to estimate the exact gain or

loss in revenue for each and every state because of GST. The introduction of GST will

require constitutional amendments because both the Centre and the State will have a common

tax base without any demarcation that currently exists. For this an absolute consensus has to

be reached between the Centre and the States. States also fear that the proposed constitutional

amendments to create a common market across India in GST may take away their fiscal

autonomy.

On May 12, 2010, finance minister Mr. Pranab Mukherjee reached out to states to restart

negotiations on GST. On May 21, 2010, the Empowered Committee met the finance ministry

officials. This was the first meeting after the Budget was presented in February. All relevant

matters for the implementation of GST were discussed. Mr. Mukherjee assured the States that

he was prepared to go beyond the Rs.50,000 crore compensation package over the next five

years recommended by the 13th Finance Commission to incentivise States to migrate to GST.

Mr. Asim Dasgupta, West Bengal finance minister and chairman of the empowered

3 Objectives given in 13th Finance Commission Task Force Report (section 2.1) 4 The CST, imposed on inter-state movement of goods, was reduced from 4 percent to 3 percent in 2007-08 and later to 2 percent in 2008-09.

3

committee said, “April 1, 2011 is our target and we will make all efforts to meet it. We are

confident.” Mr. Dasgupta also said that the draft of the proposed constitutional amendments

required for GST implementation would be sent to state finance ministers over the fortnight

by the law ministry. However, no such amendments are available in public domain.

The empowered committee, in its first discussion paper on GST, had suggested that

businesses below a gross annual turnover of Rs 1.5 crore will be subjected to GST only by

the state and not by the Centre. The Centre, however, is strongly opposed to the idea as it

would result in a substantial revenue loss, and said there should be a common threshold of Rs

10 lakh. The Centre has also said that it wants a common exemption list for both the Centre

and the State, and an acceptable level of GST rate, against the States’ demand of 18-20

percent.

The activities and their duration mentioned in the timeline5 for implementation of GST

suggested in 13th Finance Commission Task Force report show that still lot more is required

to be done before introduction of GST. With less than ten months left to meet the revised

target date of April 1, 2011 one will have to wait and see if the country can prepare enough to

migrate to GST within the time available.

1.2.1 IT Infrastructure

IT infrastructure for GST rollout is being looked into by a Committee, comprising the Unique

Identification Authority Chairman Mr. Nandan Nilekani. On June 1, 2010, Mr. Nilekani after

his interaction with officials of the CBEC has said that the Central and the State governments

could not work in isolation on IT infrastructure for GST and that the system must be

taxpayer-friendly to increase compliance6. He said there should be a platform where the

states’ IT team and the Centre’s IT team interact with each other and meet on a regular basis

to share their views.

IT infrastructure will play a major role in implementation of GST. The dependable IT

systems have to be developed simultaneously and uniformly in all the states, unlike in the

case of IT structure for value-added tax. The Centre has a broad IT infrastructure in place, but

it is a major issue with states which have varying capacity. The Centre’s online tax payment

5 The timeline (suggested introduction date: 1st October 2010) suggested by the empowered committee along with activities relating to implementation of GST is available in Appendix. Accountability and responsibility of activites to be carried by the Centre, the State and the Empowered Committee are also given. 6 Source of news: http://www.business-standard.com/india/storypage.php?autono=396671

4

application ACES7 (Automation of Central Excise and Service Tax) will be suitably upgraded to

take care of the GST but computerization of states is the biggest concern. Maharashtra,

Gujarat and Tamil Nadu are even ahead of the Centre, but a large number of states do not

have the infrastructure.

1.3 Problem Statement

For a smooth transition, the difficulties related to implementation of GST have to be

realistically considered. Some of the key factors that need to be considered are given below:

• Infrastructure for tax administration

o Up-gradation of the current system

o Data transition from the old system to the new system

o Processing of tax payments, audits and appeals

o Seamless integration of the tax system of the Centre and the States

• Changes in the Legal framework

o Constitutional amendments that will be required

o Dispute resolution processes

o Disposal of pending cases related to the old system

• Design of the tax structure

o Clear definitions of taxable events and classification of taxes

o Tax rates

o Revenue sharing between the Centre and the States

• Road map for migration to the new system

• Training of staff of the tax departments of both the Centre and the States

o Awareness about the Acts, Rules and provisions

o Awareness of administration of service tax in states

• Promoting awareness and understanding of GST among the public and professionals

o Collaborating with various professionals like accountants, tax consultants, etc

o Change in business processes, pricing by companies

o Integration with other future projects like the Unique Identification Number

o Educating the residents and citizens about the benefits of the new system

7 E-governance portal of CBEC for Central Excise & Service Tax Assesees: http://www.aces.gov.in/. Details about ACES can be seen at http://www.centralexciseaurangabad.gov.in/htmldocs/ACES.pdf

5

All stakeholders which would include Central government, State governments, tax

administration, trade and industry, professionals who act as facilitators and consumers who

are tax payers have to be well prepared. Understanding the concerns of the stakeholders will

help in better implementation of GST. A hasty implementation of GST without adequate and

timely preparation will hamper the progress of the tax structure and could lead to confusion

among tax department staff and taxpayers, which would have adverse impact on revenue

collection.

1.4 Purpose of the Study

The purpose of the study is given below:

• To quickly asses the current preparation level of the government and the industry for

rollout of GST on following aspects

o Infrastructure for tax administration

o Knowledge, Understanding, Application and Skills (KUAS) of man power in

the Government and the Industry required for implementation of GST

• To identify problems that can hinder the smooth transition to GST.

• To propose some measures to be taken to enable a smooth transition from the current

tax system to the GST system

• To Compare the proposed GST system in India with international best practises

1.5 Significance of the Study

This study gives an understanding of some issues of GST from the perspective of various

stakeholders. A important factor is the process of implementation both in allowing effective

prior consultation to identify possible problems and improvements as well as preparing the

taxpaying public for change8. Incorporating the views of the trade and industry will be

helpful for laying a clear roadmap and better implementation of GST. This will help the State

in identifying critical areas to be considered during the transition phase.

8 Successful tax reform: the experience of value added tax in the United Kingdom and goods and services tax in New Zealand by James, Simon and Alley, Clinton of University of Exeter Business School, July 2008

6

1.6 Definitions

Knowledge

Knowledge is information about a subject which has been obtained by experience or study,

and which is either in a person's mind or possessed by people generally9. In this report,

Knowledge refers to information about GST. Questions pertaining to what of GST were

classified as knowledge related questions.

Understanding

Understanding is to know why or how something happens or works. In this report, refers to

the implications and purpose of GST. Questions pertaining to why GST were classified as

Understanding related questions.

Application

Application is to make use of something or use it for a practical purpose. In this report,

Application refers to the activities related to implementation and operationalization of GST.

Questions pertaining to how and when to implement GST were classified as Application

related questions.

Skill

A skill is an ability to do an activity or job well, especially because you have practiced it. In

this report, Skills refers to the practice or training required for knowing, understanding and

applying GST. Questions pertaining to training needs were classified as Skill related

questions.

9 General definitions of Knowledge, Understanding, Application and Skills have been taken from the Cambridge Dictionary

7

2 GST in Other Countries

VAT is a multi-stage tax levied at each stage of the value addition chain, with a provision to

allow input tax credit (ITC) on tax paid at an earlier stage, which can be appropriated against

the VAT liability on subsequent sale10.

Presently VAT is followed in over 160 countries. In some countries this VAT is known as

goods and services tax or GST. The proposed GST structure in India is similar to that of

Canada. Some of the problems that they faced during implementation of GST are discussed

here. Besides, experience of Australia has also been covered.

2.1 GST in Canada

In Canada, a federal level VAT (GST) was introduced in 199111. At the sub-national level,

there are two types of VATs. These are given below:

1 The Quebec Sales Tax (QST), a tax imposed on essentially the same base as Canada’s

federal VAT (GST) but administered by the provincial government, and

2 The Harmonized Sales Tax (HST), essentially a provincial VAT imposed on the same

base as the federal GST and administered by the federal government

In some provinces, Provincial Sales Tax or Retail Sales Tax continues to exist.

The existence of these two different forms of provincial VAT has not resulted in technical or

economic problems for the federal VAT. On the other hand, the existence of a federal VAT

has apparently spared Canada from many of the VAT evasion problems, to which so much

attention is paid in the European Union (EU). In EU, there is no ‘Union-wide’ VAT.

Quebec has its own VAT (QST) on a base that consists of both goods and services and that is

largely harmonized with the federal GST. Both taxes are administered by the revenue

authorities of Quebec. Quebec was compensated by the federal government for the costs it

incurred in implementation of GST. Audit of tax returns is undertaken in close collaboration

between the two governments.

10 A brief on VAT (Value Added Tax), from CTD website 11 Source: SALES TAXES IN CANADA: THE GST-HST-QST-RST “SYSTEM” by Richard M. Bird and Pierre-Pascal Gendron

8

Under the HST model, the provincial VATs are completely harmonized with the federal

VAT. The two taxes are levied at a single composite rate, and administered by the federal

government. Revenue from the tax are redistributed to the participating governments on the

basis of the tax base.

The Canadian experience has demonstrated that a federal VAT can work perfectly well in a

country in which some sub-national units have their own VATs, some have their own retail

sales taxes (RSTs), and some have no sales tax at all.

When GST was introduced, the high visibility of the GST meant that most Canadians thought

of it as a "new" tax. The previous federal sales tax was invisible. The GST law allowed

registered firms to quote either tax exclusive or tax inclusive prices. However, in virtually

every case retailers treated the new GST exactly like the existing RST by adding it onto the

price at the cash register. Now, however, Canadians got the bad news every time they had to

dig into their pockets to pay the highly visible GST. Moreover, they had to pay the GST not

only on goods but also on many services that were exempt from provincial RSTs. Politically,

it was clear that something had to be done to avoid the appearance of increasing taxes on the

poor. This led to many special treatments to different sectors and activities.

The unreasonable delay in passing the legislation and the major last-minute changes made in

some key elements of the tax, before the legislation was passed made it impossible to

implement the educational campaign as planned and intended. While some of the initial

difficulties encountered were overcome with time, almost a decade after the introduction of

the GST the Auditor-General of Canada was still pointing out serious flaws in GST

administration, particularly with respect to audit.

A major ‘risk analysis’ program with respect to GST was launched in 2000 (though not fully

implemented nationally until 2004) was focused, in part, on the possibility of fraudulent

refund claims. For the three fiscal years ending in 2003, about 1,300 GST returns with

fraudulent refund claims (totalling C$9 million) were detected. The estimated “non-

compliance” rate fell from over 9 percent in 1998-99 to less than 4 percent in 2003-04.

The dual GST (CGST-SGST) model proposed in India is similar to the GST-QST model

implemented the province of Quebec. The next section looks into the GST-QST model in

some detail.

9

2.1.1 The Quebec Sales Tax

The QST is a destination-based credit-invoice VAT that subjects most goods and services

consumed in Québec to tax at a statutory rate. But QST is not free of cascading effect. It is

applied on the federal GST inclusive prices of goods and services. Both GST and QST are

collected at the point of sale, and their amounts are shown separately on the invoice. The

QST base is not completely harmonized with the GST base.

Revenue Québec (RQ) administers the GST on behalf of the federal government on Québec’s

territory, in addition to the QST. Under the terms of the agreement, RQ receives and

processes applications for registration under the GST/HST system from all persons carrying

on commercial activities in Québec. (Businesses registered for the GST are automatically

registered for the HST, and GST registration covers the activities of any business in all 10

provinces.) After registration, all taxable persons continue to deal with RQ for all GST/HST-

related matters including returns, remittances, rebate applications, audits, and investigations,

interpretations of laws and regulations, notices of objection, tax collection, and unfilled

returns.

The quality of RQ as a tax administration and its detailed knowledge of its taxpayer

population, when added to the economies of scale from collecting two taxes together rather

than separately, made the package an attractive one. With good information exchange,

combining the QST to the GST may well have helped both governments protect their

revenues. The CRA pays RQ a fee for collecting, administering and remitting the GST to the

federal government.

In addition to exchanging tax information with the CRA for the purposes of administering

both taxes in Québec, RQ maintains an up-to-date, bilingual, and generally user friendly

Internet site to assist with administration, enforcement, and taxpayer education. Many guides

and forms are easily accessible from the site. Forms contain information that allows RQ to

track information and tax across the GST/HST-QST system.

One unusual feature found on the site is a list of QST cheaters, with name, trade name,

address, type of business, and fraud amount revealed for all to see. Businesses in the

restaurant, construction and home renovation, and services sectors consistently get top

billing. While one may question the appropriateness of this practice from a privacy

10

perspective, it appears to be effective. The practice is tied to a public ‘fairness campaign’

conducted by the Québec government under which tax evasion is portrayed as undermining

fairness for all and hence to be discouraged on that basis rather than on the basis of revenue

losses and the accompanying economic inefficiency. RQ has a direct incentive to collect and

enforce the GST since the QST base grows when GST collections grow. This benefits both

parties.

RQ uses a target system to track administrative performance. In that respect, activities in

audit and non-filers yielded higher than expected revenue recoveries, although again we are

unable to break out data for the QST alone.

One of the reasons that the QST-GST model works out well is because RQ has harmonized

its management systems fully with the new GST management system used by the CRA. This

effort began in 2002 and was completed in April 2007.

The Quebec experience demonstrates that the dual GST model proposed for implementation

of GST in India can be made mutually benefit to both the Centre and the State.

2.2 GST in Australia

In Australia, GST is a broad sales tax of 10 percent on most goods and services transactions.

It is a value added tax, not a sales tax, in that it is refunded to all parties in the chain of

production other than the final consumer.

It was introduced on 1 July 2000, replacing the previous Federal wholesale sales tax system

and designed to phase out a number of various State and Territory Government taxes, duties

and levies such as banking taxes and stamp duty.

In 1999, an agreement was enacted with the state and territory governments of Australia that

their various duties, levies and taxes on consumption would be removed gradually over time,

with the budget shortfall being replaced by GST income from the Commonwealth Grants

Commission. Furthermore, (federally levied) personal income tax and company tax was

reduced to offset the GST.

11

2.2.1 How Australia prepared trade and industry for GST

On 13 August 1999, the GST Start-Up Assistance Office (GSTSAO)12 was established within

the Department of Treasury to administer the $500 million assistance set aside by the

Government to assist Small and Medium Enterprises, the Community sector and Education

(SMECEs) institutions get ready for the GST. The GSTSAO administered these funds in

consultation with The New Tax System Advisory Board, the Business Advisory Panel and

the Community Sector Advisory Panel.

The GST Start-Up Assistance Office delivered programs until 28 February 2001, and closed

on 30 June 2001, one year after implementation of GST.

The assistance funds were used to deliver four programs described below:

1. Organisation Delivered Assistance (ODA) Programme: The objective of the ODA

programme was to deliver GST business skills seminars and material to small and

medium enterprises, the community sector and educational institutions (SMECEs)

through the peak body representing each industry sector. Peak bodies were invited to

submit proposals for funding that described how they would deliver the assistance and

the proposed cost. Contracts were negotiated with peak bodies after an assessment of

the proposals against benchmarks. The GSTSAO arranged contracts with some peak

bodies that were required to coordinate delivery to a number of related peak bodies

under a consortium arrangement. This ensured good coverage and value for money.

2. Advisor Education Programme13: The objective of the programme was to provide

GST education to a large network of geographically accessible informal advisors who

in turn could pass the information to the end target group. Courses were held in over

70 locations Australia-wide on the following topics:

• Introduction to the GST and Registration Options;

• GST and Your Systems and Records; and

• Frequently Asked Questions; and

• How to complete your BAS and PAYG; and

• Combined course of all of the above.

12 http://www.gststartup.gov.au/ 13 Course material can be found at http://www.gststartup.gov.au/index.asp?file=educational/aep/AEO_EDUdown.html

12

3. Business Skills Education Programme: The GST Assist Helpline was launched on

11 October 1999 to provide a complete GST business skills information service

targeting SMECEs. The service was operated under contracts with The Institute of

Chartered Accountants (ICAA) and the Society of Certified Practising Accountants of

Australia (SCPAA) who provided answers to callers from small business, and the

community and education sector respectively. GST Assist operated until 28 February

2001. During the lifespan of the helpline, information was provided to more than 1

million callers.

Publications

The Office arranged for the production and distribution of around 20 million

publications on business skills, the GST, BAS and PAYG (including booklets, videos

and CD ROMs). In addition, electronic versions of the products were available on

GST start-up website: www.gststartup.gov.au.

Websites

Two websites provided information about the GST assistance programmes:

• www.gststartup.gov.au - provided information about the programmes, access to

products online including media releases and other GSTSAO publications.

• www.gstassist.gov.au - provided access to registered supplier applications and

information about registered suppliers.

Assistance for Constituents from a Non English Speaking Background

The programme initially provided GST education to ethnic business and community

leaders and media. This was supported by presentations by GSTSAO and ATO

officers, the distribution of information kits (in 24 languages), containing publications

developed by the GSTSAO.

4. Direct Assistance Programme: The objective of the direct assistance programme

was to deliver a $200 certificate to small business and community groups that

registered for GST by 31 May 2000. The certificate was to be redeemed with a

registered supplier for goods or services that would assist the GST registrant to

prepare for the GST. This included computer hardware, computer software,

stationary, training courses, and financial advice. The certificates were available for

use until 11 November 2000.

13

• Over 19,00,000 certificates were issued.

• Over 14,000 suppliers were registered to supply goods and services under this

programme.

14

3 Methodology

In this chapter, the methodology adopted for this study is outlined. The research design, tools

of the study, sample of the study, statistical techniques and limitations of the study are

discussed.

3.1 Research Design

The following research techniques were used in this study.

3.1.1 Exploratory Research

Exploratory research has the goal of formulating problems more precisely, clarifying

concepts, gathering explanations, gaining insight, eliminating impractical ideas, and forming

hypotheses. It provides insights into and comprehension of an issue or situation14.The initial

phase of the project demanded an exploratory research to capture the knowledge,

understanding, application and skills relating to migration to GST. The problems and risks in

implementation of GST, and suggestions to mitigate the same were also gathered.

3.1.2 Descriptive Research

Descriptive research defines questions and finds answers to these questions using statistical

techniques on the data gathered. The following null hypotheses have been tested using the

collected data.

• Tax department staffs with an experience of more than 20 years do not differ

significantly from staffs with an experience of 20 years or less in their agreement to

use of information technology for greater transparency in administration of GST.

• Trade and Industry agree to the dual structure of GST, i.e. separate GSTs of the

Centre and the State.

3.1.2.1 Variables used in the Study

The following variables were used in the study:

1. Work experience of respondents

2. Group of target audience, i.e. top officials, middle level tax officials, tax department

staff, trade and industry, professionals and general public.

14 Types of research techniques, their objective and application can be seen at http://en.wikipedia.org/wiki/Exploratory_research

15

3.2 Tools of the Study

Interviews were conducted to collect data from top officials. Questionnaires were used to

collect data from middle level tax officials, tax department staff, trade and industry,

professionals and general public.

3.2.1 Interview

Interviews were designed after studying secondary information and in consultation with

experts. The following information was gathered:

• Impact of GST on efficiency and effectiveness of the revenue system

• Opinion on tax rates and tax base of GST

• Current status of KUAS of tax officials of the infrastructure, changes in legal

framework, design of the tax structure and roadmap for implementation of GST

• Man power requirement for implementation of GST

• Training needs

• Modes of Training

• Creation of awareness among the stakeholders

• Co-ordination and information sharing between the Centre and the States

• Risks and Constraints in implementation of GST

• Suggestions to mitigate risks and overcome constraints

3.2.2 Questionnaire

Questionnaires were designed separately for different groups of target audience. To begin

with an exhaustive list of questions were prepared. Then these questions were segregated

under five different questionnaires. The segregation of questions was based on the group of

target audience that would be appropriate to answer a particular question. After consultation

with experts, the questionnaires were refined.

The questionnaire consisted of both open ended and closed ended questions. Open ended

questions were used to gather data on training needs, problems foreseen during transition and

suggestion to mitigate the same. Closed ended questions were used to gather data on sources

for understanding GST and to know whether the respondents have attended any training

programs in GST. The questionnaires also had an opinionnaire section that was used to

capture the degree of agreement on the following aspects.

16

• Objectives of GST

• Impact on processes in tax administration and businesses

• Difficulties in tax administration and compliance

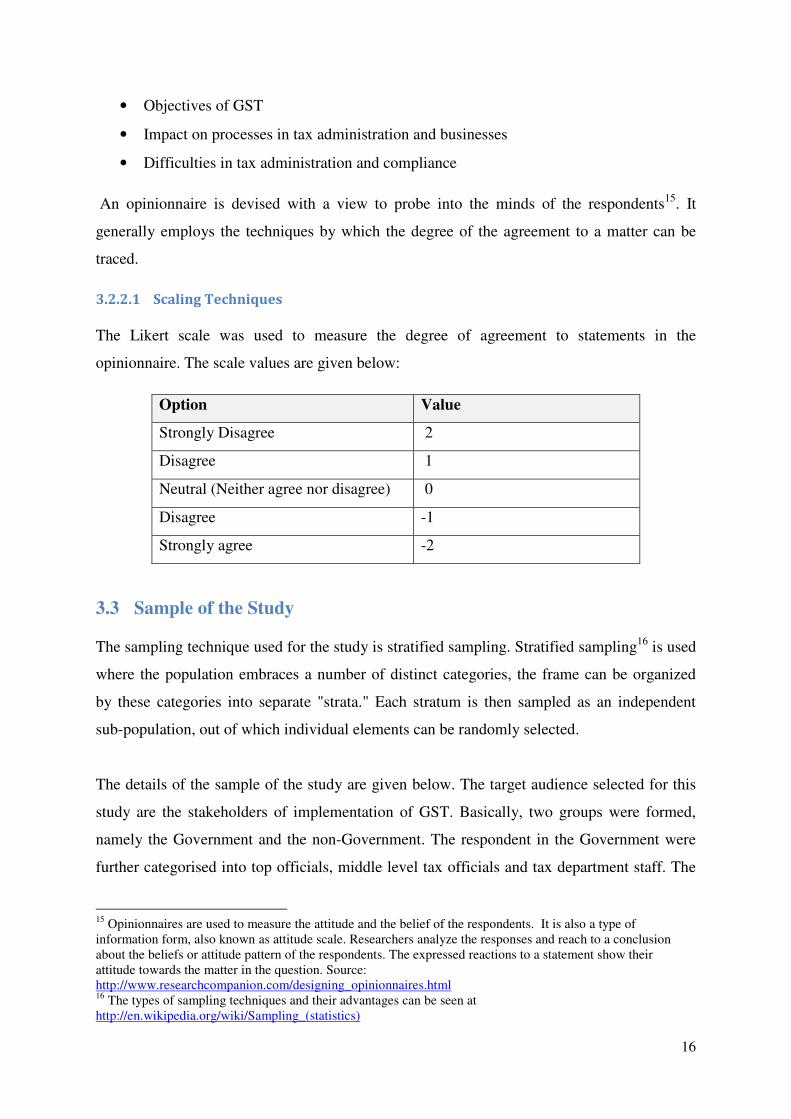

An opinionnaire is devised with a view to probe into the minds of the respondents15. It

generally employs the techniques by which the degree of the agreement to a matter can be

traced.

3.2.2.1 Scaling Techniques

The Likert scale was used to measure the degree of agreement to statements in the

opinionnaire. The scale values are given below:

Option Value

Strongly Disagree 2

Disagree 1

Neutral (Neither agree nor disagree) 0

Disagree -1

Strongly agree -2

3.3 Sample of the Study

The sampling technique used for the study is stratified sampling. Stratified sampling16 is used

where the population embraces a number of distinct categories, the frame can be organized

by these categories into separate "strata." Each stratum is then sampled as an independent

sub-population, out of which individual elements can be randomly selected.

The details of the sample of the study are given below. The target audience selected for this

study are the stakeholders of implementation of GST. Basically, two groups were formed,

namely the Government and the non-Government. The respondent in the Government were

further categorised into top officials, middle level tax officials and tax department staff. The

15 Opinionnaires are used to measure the attitude and the belief of the respondents. It is also a type of information form, also known as attitude scale. Researchers analyze the responses and reach to a conclusion about the beliefs or attitude pattern of the respondents. The expressed reactions to a statement show their attitude towards the matter in the question. Source: http://www.researchcompanion.com/designing_opinionnaires.html 16 The types of sampling techniques and their advantages can be seen at http://en.wikipedia.org/wiki/Sampling_(statistics)

17

non-Government section was categorised into trade and industry, professionals (chartered

accountants and tax professionals) and general public. The responses have been collected

based on the availability of the respondents in the limited time that was available for data

collection.

Categories Details Number of

Respondents

Duration

Top level officials Commissioner,

Additional Commissioners,

And Joint Commissioners of

Commercial Taxes Department and

Large Taxpayers unit.

Secretary and Deputy Secretary of

Finance Department, Government

of Karnataka.

10 (8 State + 2

Centre)

40 minutes

to 120

minutes

Middle level

officials

Deputy Commissioners,

Assistant Commissioners

And Commercial Tax Officers of

Commercial Taxes Department and

Large Taxpayer unit.

5 ( 4 State + 1

Centre)

20 minutes

to 30

minutes

Tax department

staff

Inspectors and Superintendents of

Commercial Taxes Department

Karnataka and Central Excise and

Customs

52 (10 State + 42

Centre)

10 minutes

to 15

minutes

Trade and Industry Representatives of FKCCI, retailers,

wholesalers and manufacturers

24 20 minutes

to 30

minutes

Professionals Chartered Accountants and Tax

Consultants

11 20 minutes

to 30

minutes

General Public Post Graduate Students,

Government Officials and Software

Engineers

15 2 minutes to

5 minutes

Total 117

18

3.4 Collection of Research Data

The interview questions were e-mailed to the respondents with a briefing on the objective of

the study and appointments were taken accordingly. The researcher personally visited the

offices of the respondents to gather their responses. The conditions for administering the

interview were fulfilled.

In some cases online questionnaires were used to gather responses through the internet.

Otherwise, copies of questionnaires were distributed to the respondents in their offices and

data was collected. The respondents were briefed about the objective of the study before

starting to answer the questionnaire.

The qualitative data collected was tabulated and used to perform statistical analysis.

3.5 Statistical Techniques

The data collected were scored on a 5 point scale from 2 to -2. Simple averages were used to

interpret the level of agreement to statements on GST. To test the hypotheses framed, one

sample t-test17 and independent sample t-test were used.

In one-sample t-test, the observed mean (from a single sample) is compared to an expected

(or reference) mean of the population (e.g., some theoretical mean), and the variation in the

population is estimated based on the variation in the observed sample.

The independent sample t-test is the most commonly used method to evaluate the differences

in means between two independent groups. Theoretically, the t-test can be used even if the

sample sizes are very small (e.g., as small as 10; some researchers claim that even smaller

sample sizes are possible), as long as the variables are approximately normally distributed

and the variation of scores in the two groups is not reliably different.

17 Refer to http://www.statsoft.com/textbook/statistics-glossary/t/button/t/ for concepts and usage of t-test

19

3.6 Limitations of the Study

The study has the following limitations:

• The sample sizes of the six groups of target audience were limited because of time

constraints. The maximum possible responses were gathered in the time available for

data collection.

• The first discussion paper on GST from EC and the Finance Commission Task Force

report on GST were used for designing the questionnaires. Since the draft of the

proposed constitutional amendments required for GST is yet to be released, the exact

details of GST may differ from the referred reports/papers.

• The awareness of GST among the tax department staff was poor. Therefore the

training needs mentioned by this group were not specific.

• Data has only been collected in Bangalore. The commercial tax offices in other

districts of Karnataka have not been covered.

• Analysis of the level of agreement to statements on GST has been done separately for

each statement only. Analysis of total of averages was not done because of difficulty

in estimating the weights for individual statements.

20

4 Analysis and Interpretation of Results

In this chapter, the analysis and the interpretation of results are given in detail. The responses

collected through interviews and questionnaires constitute raw data for the study. The data

was further subjected to organisation and tabulation. For methodical presentation, the

analysis of the data and corresponding results are given in two parts.

Part I deals with analysis and interpretation of data pertaining to the following:

1. Opinion on critical aspects of design and implementation of GST. Section 1.2.1 gives

details of the topics discussed with top officials in the interviews.

2. Level of agreement to statements on GST. The statements are analysed in two groups.

The first group consists of statements for which a positive response/agreement was

expected, and the second group consists of statements for which a negative

response/disagreement was expected.

3. Whether the respondents received training or attended seminars/workshops on GST.

4. The main source of understanding GST.

5. Training needs.

6. Risks and constraints in implementation of GST.

7. Suggestions to mitigate risks in implementation of GST.

Part II deals with the testing of the hypotheses given below:

1. Tax department staffs with an experience of more than 20 years do not differ

significantly from staffs with an experience of 20 years or less in their agreement to

use of information technology for greater transparency in administration of GST.

2. Trade and Industry agree to the dual structure of GST, i.e. separate GSTs of the

Centre and the State.

21

4.1 PART - I

The analysis of data and interpretation has been done separately for each group of target

audience. It is presented in the following order (1) top officials, (2) middle level tax officials,

(3) tax department staff, (4) trade and industry, (5) professionals, and (6) general public18.

4.1.1 Top Officials of the Centre and the State governments

The information gathered from 10 officials of CTD, FD, NACEN and LTU on some aspects

of GST are given below:

Impact of GST on effectiveness and efficiency of the revenue system

The general view was that GST will enhance the effectiveness and efficiency of the revenue

system in the long run. Majority of respondents estimated the time required for this change to

be between 3 to 5 years. Some officers think it may take more than 5 years to stabilise the

new system. Information Technology systems will be used extensively to track transactions at

every step of a supply chain which is currently not the case. GST is expected to widen the tax

base. For this tracking of transactions is essential. Any discontinuity in the tracking system

will have a detrimental effect on the effectiveness of the tax system. Taxpayers try to avoid

taxes by taking advantage of the differences in rates in different region, and the exemptions

provided by the government. By developing a uniform tax system across the country and by

tracking every transaction, effectiveness of the system will be enhanced. Also, the Centre and

the State will be administering a common base. This double check is expected to make the

system effective. The efficiency of the system is expected to increase through simplification

of procedures and eliminating unnecessary steps. IT systems will reduce the cost and time

involved in administration. At the same time, compliance costs will come down for the

dealers. This will create a win-win situation for the Government and the Industry.

Implementing faster means for dispute resolution will also enhance the efficiency of the

system.

18 As a result of this arrangement some suggestions appear to be repeated but they are meant for a particular group.

22

Opinion on rates and tax base of GST

• Tax Rates – Dual GST: Centre GST and State GST

Dual GST is the form of GST that is applicable to the federal setup in India with

powers to administer tax given to both the State and the Centre. Other forms of GST

are: Harmonized national GST and only State GSTs. Though a single harmonized

national GST would be the ideal solution to create a nationwide common market, this

kind of system will shake the federal structure and would not be applicable to India.

No clear opinions were given on the tax rates, since the exact revenue neutral rates

have still not been finalized. The combined revenue neutral rate estimated by the

Finance Commission Task Force of 12 percent was not well accepted. The state tax

department is clearly of the view that 100 percent compensation should be provided

for any revenue loss.

• Food items

For the poor, the proportion of expenditure on food to income is far higher than the

average. In 2005, on average, food accounted for one-third of total private consumer

expenditure19. Therefore taxing food will have a major impact on the poor. All

respondents were of the opinion that unprocessed food that is a major component of

food consumed by the poor should be exempted. If not exempted, it should be taxed at

a lower rate.

• Land and Real Property

There was a mixed opinion on land on real property as to whether this has to be

brought under GST or not. Majority of the respondents suggested that land and real

property should be left out of GST for the following reasons.

• Land by its very nature does not fall under good or service as it is immovable.

But in Canada, New Zealand and Australia, housing and construction is

treated just like any other commodity.

19 Section 5.B, GST Reforms and Intergovernmental Consideration in India

23

• It forms a major portion of the revenue for the State government20. Thus

bringing it under GST would be risky, especially considering the loss in

revenue that may occur. Moreover, in India States do not levy income tax

which is not the case in countries like Canada. It can be brought under GST

once the implementation is stabilized and there is more clarity in the system.

• Non-profit Sector and Public Bodies

There was a mixed opinion on whether non-profit sectors like NGOs should be taxed

or not. Majority were of the view that all activities irrespective of the intention should

be taxed. Exemptions and reduced rates of taxes cause distortion and are source to

disputes. Moreover, taxing all activities will ensure transparency in the activities

carried out by these. It will also discourage organization to project themselves as non-

profit organizations to avoid taxes.

A minority felt that tracking these activities will be a difficult task, and only

commercial activities should be taxed.

• Financial Services

Every respondent was of the view that taxing financial services is a difficult task. The

explicit service charges that are charged by the service providers will be taxed, but

taxing the implicit benefits21 that the financial services get cannot be ascertained.

Current status of KUAS of tax officials on the following

• Infrastructure for tax administration

The current infrastructure is not adequate for the implementation of GST. The

database needs to be updated to capture more information. Building the software

applications will not be problem, but meeting the hardware requirements will be a

challenging task. In the Commercial Taxes Department, computers and hardware

backup system like UPS (uninterrupted power supply) need to be upgraded to take

advantage of technological advancements. Due to inadequate backup systems, servers

go down during power cuts.

20 Audit Report (Revenue), Karnataka (2008-09): In 2008-2009, Stamps and Registration fees along with land revenue accounted for Rs. 3182.37 crores. This is 11.5 percent of the total tax revenue of Rs. 27,645.66 crores 21 The excess of interest rate on the loan over the rate of interest or cost of funds to the bank for that loan is the implicit income for the bank.

24

How data will be shared on real time basis between the States and the Centre is an

area that needs investigation.

• Changes in the Legal framework

GST will require changes to the legal framework of the tax system. Amendments will

be required to allow the Centre and the State on a common base.

An understanding of the law is required for every officer from the level of

Commercial Tax Officer (CTO) and above. Superintendent and Inspectors should also

be updated when they are promoted to the post of CTO.

The law should be simple and unambiguous with minimal deviation from flawless

GST. Officials expressed concerns about the amendments being approved in the

parliament with a super majority (two-thirds of the house). Firstly, with different

parties ruling different states, getting to a consensus on the amendments required may

not be all that easy.

Coming up with a draft bill and freezing the law should be of the utmost importance.

This is the first step in preparation for implementation of GST. On June 7, 2010, Mr.

Dasgupta said that the monsoon session is being targeted for bringing the

constitutional amendments bill (for introduction of GST) in India. This should set the

stone rolling for implementation of GST.

• Design of the tax structure

The design suggested by the Finance Commission Task Force was well accepted by

the officials. There were concerns about the combined revenue neutral rates being

estimated at 12 percent (5 percent CGST and 7 percent SGST). The current VAT rate

in Karnataka is 13.5 percent. Even though States will be allowed to levy services tax,

a 7 percent SGST rate was not accepted.

There were concerns raised regarding uniformity in the tax structure. Importance of

certain commodities is more in a particular place. Importance of certain commodities

is more for the poorer sections of the country. The social and economic impact should

be considered before designing a national level uniform tax structure.

25

On compensation of revenue loss for the States, there was demand for 100 percent

compensation. This will give the confidence to the States to move forward with GST

without any worries. Some states are increasing their VAT rates in order to seek a

higher compensation from the Centre. This kind of behavior by the States will hinder

the progress in implementation of GST.

• Road map or a transition plan to move to the new system

A clear roadmap should be developed by the States with a base given by the Centre to

maintain uniformity of milestones and deadlines. The timeline for implementation of

GST22 given by the Thirteenth Finance Commission Task Force should be followed

with a revised schedule. The officers demanded more urgency to be shown by the

Empowered Committee and the Union government to arrive at consensus on the

compensation package. As the first task, the GST legislation should be passed as

earlier as possible leaving enough time for preparation.

Man power requirement for implementation of GST

GST will increase the tax base by increasing the number of points of taxation. The number of

points of taxation itself may not increase the number of assesees. But the number of assesees

is expected to increase because of the inclusion of services under the State GST. This

increase can be taken care by effective use of Information Technology systems. It is expected

that the role of man power should be drastically reduced. There might even be a case of

reducing man power.

• Orientation of man power to the GST system

The change from the State Sales Tax regime to the State Value Added Tax regime

was a bigger change than the current change required from VAT to GST.

Conceptually, GST is based on VAT. So at the State level, there should not be any

difficulty is orienting the staff to the GST system. But the current change will be a

bigger change at the Centre level. Centre might face issues which States faced during

transition to the VAT regime.

22 See Appendix for timeline for implementation of GST

26

Modes of training

The modes of training that can be adopted will depend on the time left to prepare for GST. It

will also depend on training capacity, i.e., the number of officials/staff members that can be

trained per day. With enough time for preparation, of about a year, both formal and “hands

on” training modes can be used. Formal training should be adopted to educate the employees

about the objectives, benefits, expected problems, acts and rules. This should be followed by

a hand on training that would be more specific to the role of the employee within the

department. Different sections of the department should be trained on the procedures, rules

and scope of their job. A realistic environment should be simulated for trainees to have a

practical experience before the actual implementation of GST. This will improve the

confidence of the tax department as well as that of the Industry.

Issues in training programs during transition to VAT

In August 2001, the Government of Karnataka appointed Crown Agents23 (technical

consultants) to provide technical assistance to the CTD at a total cost of Rs. 20.33 crores, to

assist in transition from the then Sales tax regime to the VAT regime. Crown Agents of UK

conducted training of trainers (ToT), developed the application software and supported the

communication processes, basically holding the department’s hands till the VAT program

was up and running. The feedback received from the tax department officials and staff on the

training is not satisfactory. The reasons for dissatisfaction are given below:-

• Time gap between the training programs and introduction of VAT: The department

imparted training to its staff between November 2001 and July 200324 on VAT

implementation and administration covering the modules relating to registration,

returns and payment, refunds, input tax credits, debt management and audit. But VAT

for introduced on April 1, 2005.

• Lack of adequate hands on training: There were differences in actual implementation

and the training imparted to the officials and staff.

23 Crown Agents (Crown Agents for Oversea Governments and Administrations Limited) is an international development company delivering capacity-building and institutional development consultancy services in public sector transformation, particularly in revenue enhancement and expenditure management, banking, public finance, training and procurement. Crown Agents works with the public and private sectors in more than one hundred countries, and for international development agencies and institutions. 24 CAG report 2008-2009 (Section 2.2.7.6)

27

• Lack of synchronization between trainee and trainer: The trainees were not

comfortable with the trainers. There were communication problems between CTD

employees and the trainers.

• Attitude of staff towards training was not positive: Attitude is a major concern cited

by all most all the officials. Aligning the employees to achieve the objectives of GST

is one of the most challenging tasks during the transition. Officials are more

concerned about the attitude of grass root level staffs that are ignorant and reluctant

towards training programs.

Creating awareness among the stakeholders

A major factor for success of VAT/GST in New Zealand is the effective prior consultation to

identify problems and improvements, and preparing the tax payer for the change, as part of

implementation.

In reality, the dealers help the Government in collecting tax from the consumers.

Professionals act as facilitators to help dealers in the process of remitting tax to the

government. Therefore it is imperative to take the dealers and professionals into confidence

for a hassle-free transition.

For the general public, introduction of VAT will make the tax system more transparent.

Under the current VAT regime all that the consumer sees in his bills is a VAT of 12.5+

percent in addition to the value of goods and services purchased. Under GST, both CGST and

SGST will be displayed separately. This will make the Centre component of the tax visible,

which so far was invisible to the consumer25. Though on the whole the consumer will be

paying lesser than what he/she is paying under the current VAT system, the perception of

amount of tax paid might change. This makes it imperative for the general public to be

educated on the changes, benefits and impact on GST.

Coordination between the Centre and the States

Coordination and sharing of information between the States and the Centre is the single most

important factor for the success of GST. Till now the State Taxes departments have worked

in compartments. The market was region based. Now the objective is to make India a

common market with a uniform tax system across the country. Moreover, tracking

25 See section 2.1 for Canadian experience in this regard

28

transactions at every level of supply chain arrangements is absolutely necessary to building

an efficient and effective system. This requires the infrastructure of all states to be upgraded.

It will be challenging task to upgrade IT systems in backward states.

Since both the Centre and the State will be levying tax on the same base, they need to work in

tandem for the advantage of one another. This will be very effective when there is perfect

coordination. For example in case of non-compliance cases, assessment error, penalties, raids,

etc., the procedures and mode of communication should be clearly defined.

The rules and roles regarding sharing of information should be clearly defined without any

ambiguity. IT system and network channels should be built for seamless and real time sharing

of information.

The practice of making revenue estimations just before the presentation of the Budget will

not be possible after implementation of GST. Preparation of the Union Budget and the State

Budget may not be a secret anymore as decision on tax rates cannot be made at a state level

or union level. A single rate of CGST and SGST will require the consensus of the Centre and

the States.

Risks and Challenges

• Preparation of the Government and the trade and industry for GST. A hasty

implementation of GST without much preparation may lead to problems that may in

turn increase administration costs.

• Changes in revenue level for the State as well as the Centre. Though GST is

accepted to be beneficial in the long run, whether these benefits will result in

increase in revenue in the short run is not certain.

• Coordination and Integration of the State tax systems and the Central tax system.

• Monitoring of inter-state transaction should be automated as much as possible. This

is absolutely necessary to track the entire supply chain to have a rich database of

information. By tracking every step the tax base will increase the tax rates will go

down for the end user. If this is not achieved, GST will be defeated.

29

Suggestions

• Tax structure

The deviation from flawless GST should be kept to a minimum.

• Preparation of the Government and the Industry

Sufficient time should be provided to the CTD and the Industry to prepare for GST.

Problems and improvement areas should be identified to make the system successful.

Simulated training programs should be used to train the CTD to build confidence in

the system

The capacity of facilitators like chartered accountants, tax consultants and even

computer assistants should be enhanced. Work load should be transferred from the

CTD and the Industry to these facilitators. The CTD can implement schemes like

“TRPS (Tax Return Preparer Scheme)”26 that was introduced by the Income Tax

Department in partnership with NIIT.

• Computerization

Automate the manual tasks to enhance efficiency and transparency. The CTD staff,

especially staff at grass root level should be trained on computer skills.

• Monitoring Inter-state Transaction

The capacity of Tax Information Exchange System (TINXSYS)27 has to be increased

to ensure that every transaction is tracked. Steps should be taken so that there is a

seamless flow of information in real time.

26 http://www.trpscheme.com: The Government of India Tax Return Preparers Scheme to train unemployed and partially employed persons to assist small and medium taxpayers in preparing their returns of income has now entered its Second Phase. During its launch year, on a pilot basis, close to 5,000 TRPs at 100 centers in around 80 cities across the country were trained. 3737 TRPs were certified by the Income Tax Department to act as Tax Return Preparers, who assisted various people in filing their IT Returns. The Government has now decided to increase their area of operations by including training on TDS returns and Service Tax returns to these TRPs. 27http://www.tinxsys.com/: TINXSYS is a centralized exchange of all interstate dealers spread across the various States and Union territories of India. TINXSYS is an exchange authored by the Empowered Committee of State Finance Ministers (EC) as a repository of interstate transactions taking place among various States and Union Territories. TINXSYS helps the Commercial Tax Departments of various States and Union Territories to effectively monitor the interstate trade.

30

• Transition of current data to new system

The data in the current system should be transferred to the new system so that there is

continuity of records. During the transition from Sales Tax system to VAT system

there were issues in data transition. The continuity of records of taxpayers was lost in

the transition. In some cases, dealers who had to pay arrears in the Sales tax system

were given refunds under the VAT system.

31

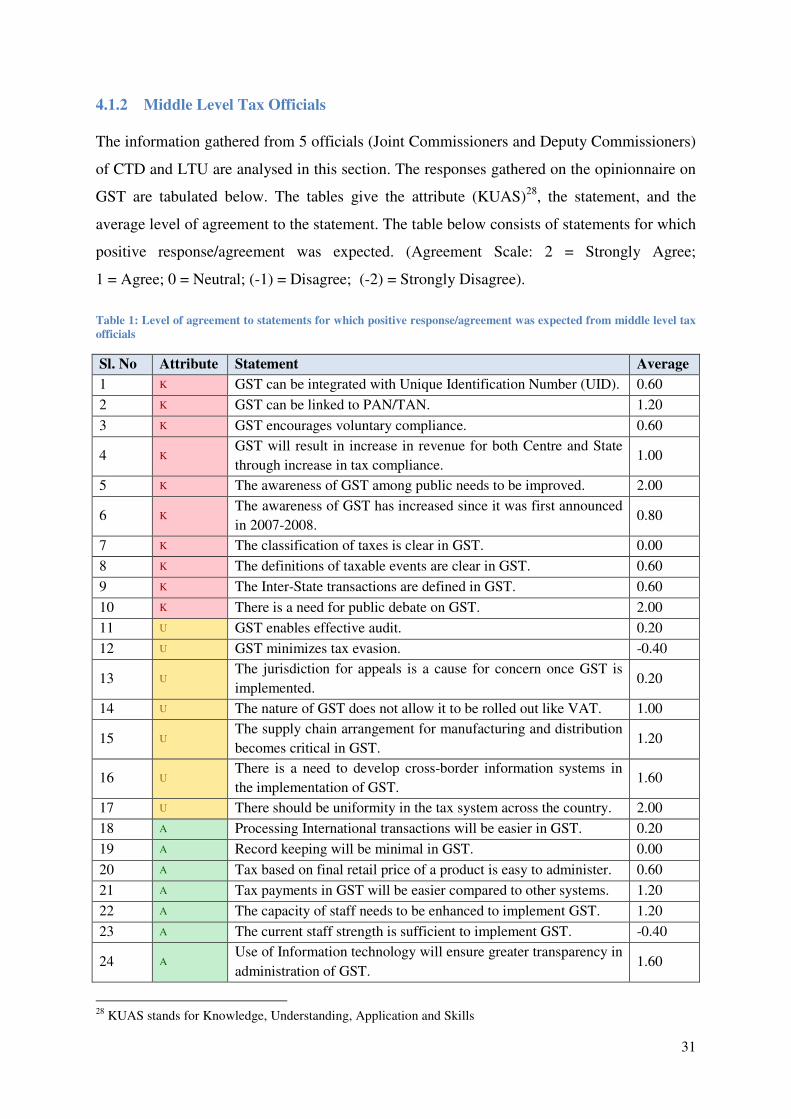

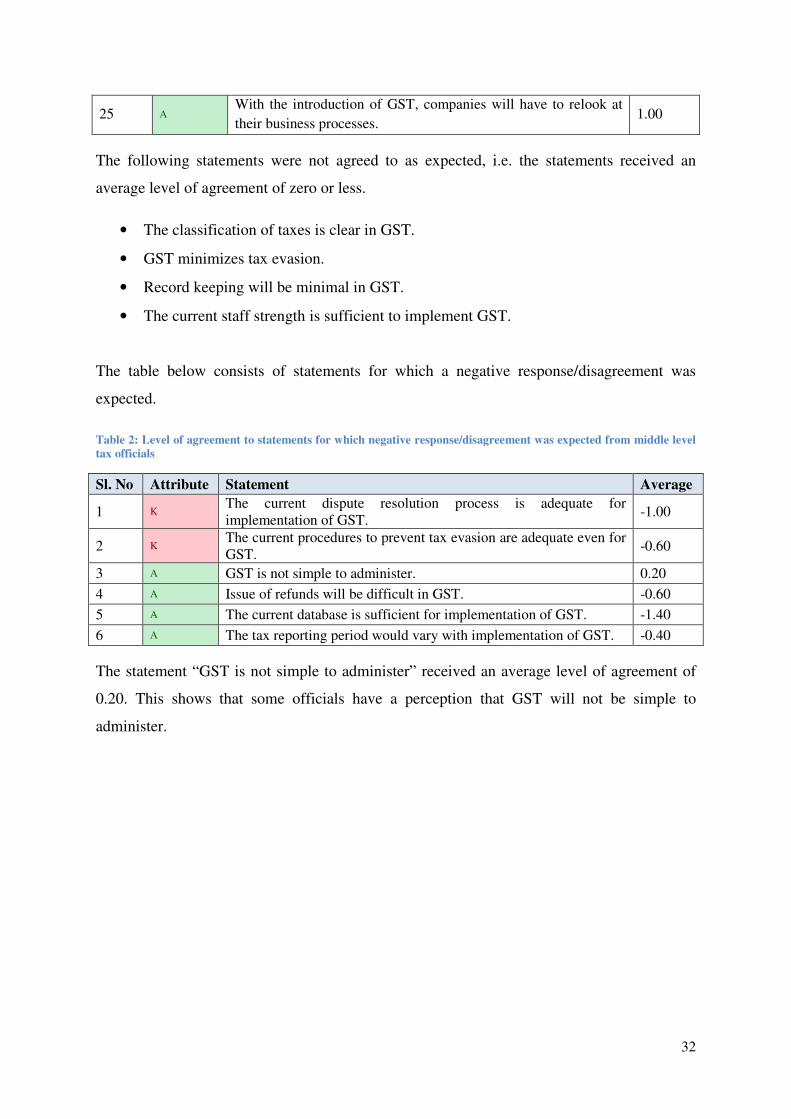

4.1.2 Middle Level Tax Officials

The information gathered from 5 officials (Joint Commissioners and Deputy Commissioners)

of CTD and LTU are analysed in this section. The responses gathered on the opinionnaire on

GST are tabulated below. The tables give the attribute (KUAS)28, the statement, and the

average level of agreement to the statement. The table below consists of statements for which

positive response/agreement was expected. (Agreement Scale: 2 = Strongly Agree;

ists of statements for which positive response/agreement was expected.

ent to statements for which positive response/agreement was expected from general public

Statement

areness of GST has increased since it was first announced 2008.

There is a need for public debate on GST.

The general public on average agrees that awareness on GST has increased very slightly since

2008. And they also see the need for public debate on GST.

Awareness of GST and VAT

The graph below shows the percentage of the respondents from general public

. Seventy three percent claim that they are aware of GST. This

eports and news articles about the progress on GST by media.

: Percentage of respondents from general public who claim to be aware of GST

73%

27%

Awareness of GST

50

The data gathered from 15 people from the general public are analysed in this section.

Responses were collected from post graduate students, government employees and software

T are tabulated below. The tables

KUAS), the statement, and the average level of agreement to the statement.

1) = Disagree; (-2) =

ists of statements for which positive response/agreement was expected.

was expected from general public

Average

areness of GST has increased since it was first announced 0.06

0.71

The general public on average agrees that awareness on GST has increased very slightly since

The graph below shows the percentage of the respondents from general public who claim to

claim that they are aware of GST. This

eports and news articles about the progress on GST by media.

claim to be aware of GST

The graph below shows the percentage of the respondents from general public

be aware/not aware of VAT.

five years of implementation of VAT in the State, this was expected.

Figure 10: Percentage of respondents from gen

The graph below shows the percentage of the respondents from general public

be aware/not aware of the proposed date for implementation of GST (April 1, 2011)

thirteen percent claim to be aware of this. This shows tha

on GST.

Figure 11: Percentage of respondents from gen

Yes

No

Knowledge of proposed date for

implementaton of GST

Yes

No

The graph below shows the percentage of the respondents from general public

. Ninety three percent claim that they are aware of

five years of implementation of VAT in the State, this was expected.

centage of respondents from general public who claim to be aware of VAT

he graph below shows the percentage of the respondents from general public

the proposed date for implementation of GST (April 1, 2011)

thirteen percent claim to be aware of this. This shows that they are not following the progress

centage of respondents from general public who claim to be aware of the proposed date for

implementation of GST

93%

7%

Awareness of VAT

13%

87%

Knowledge of proposed date for

implementaton of GST

51

The graph below shows the percentage of the respondents from general public who claim to

claim that they are aware of VAT. After

aware of VAT

he graph below shows the percentage of the respondents from general public who claim to

the proposed date for implementation of GST (April 1, 2011). Only

t they are not following the progress

aware of the proposed date for

Understanding of the concept of

The graph below shows the percentage of the respondents from general public

understand/not understand the concept of

Figure 12: Percentage of respondents from general public

The graph below shows the percentage of the respondents from general public

understand/not understand the concept of VAT

concept of VAT. And thirty three percent said that they understand the conc

that educating the public on GST will not be difficult.

Figure 13: Percentage of responde

Understanding of the concept of GST

Yes

No

Understanding the concept of VAT

Yes

No

the concept of GST and VAT

elow shows the percentage of the respondents from general public

the concept of GST.

Percentage of respondents from general public who claim to understand the concept of GST

graph below shows the percentage of the respondents from general public

the concept of VAT. Sixty seven percent said that they understand the

concept of VAT. And thirty three percent said that they understand the concept of GST.

that educating the public on GST will not be difficult.

: Percentage of respondents from general public who claim to understand the concept of VAT

33%

67%

Understanding of the concept of GST

67%

33%

Understanding the concept of VAT

52

elow shows the percentage of the respondents from general public who claim to

claim to understand the concept of GST

graph below shows the percentage of the respondents from general public who claim to

Sixty seven percent said that they understand the

ept of GST. This shows

claim to understand the concept of VAT

Understanding of the concept of GST

53

4.2 PART II

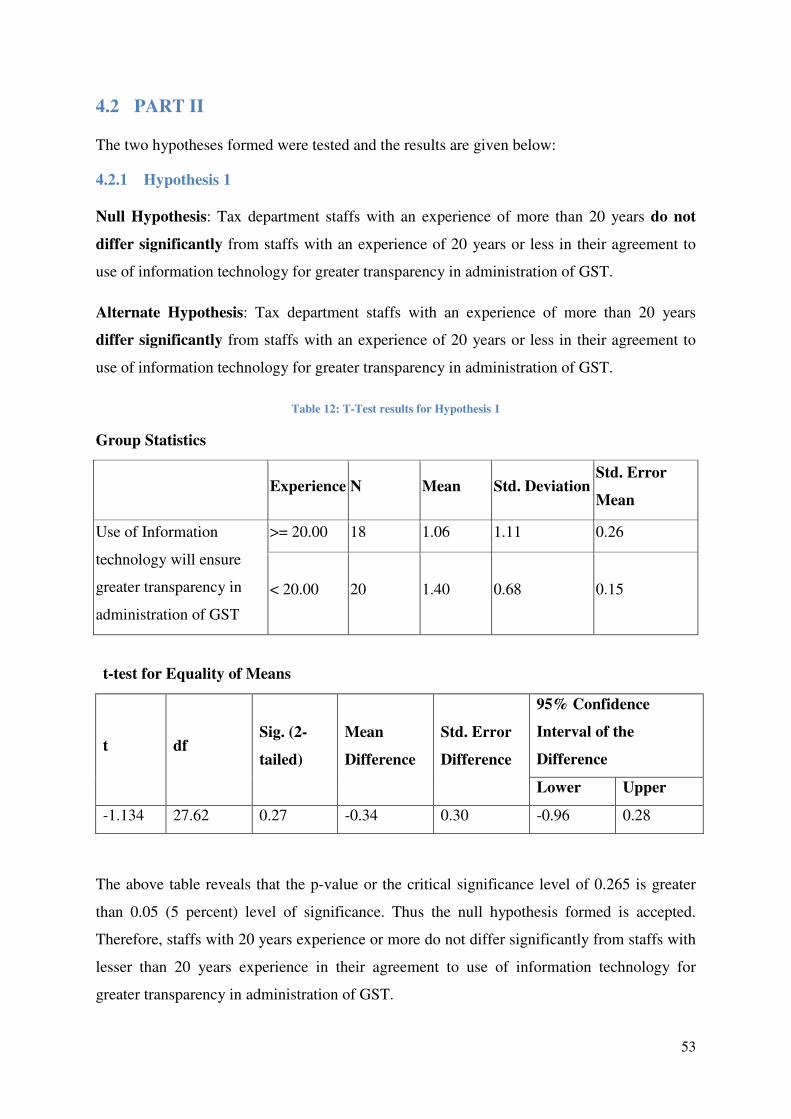

The two hypotheses formed were tested and the results are given below:

4.2.1 Hypothesis 1

Null Hypothesis: Tax department staffs with an experience of more than 20 years do not

differ significantly from staffs with an experience of 20 years or less in their agreement to

use of information technology for greater transparency in administration of GST.

Alternate Hypothesis: Tax department staffs with an experience of more than 20 years

differ significantly from staffs with an experience of 20 years or less in their agreement to

use of information technology for greater transparency in administration of GST.

Table 12: T-Test results for Hypothesis 1

Group Statistics

Experience N Mean Std. Deviation Std. Error

Mean

Use of Information

technology will ensure

greater transparency in

administration of GST

>= 20.00 18 1.06 1.11 0.26

< 20.00 20 1.40 0.68 0.15

t-test for Equality of Means

t df Sig. (2-

tailed)

Mean

Difference

Std. Error

Difference

95% Confidence

Interval of the

Difference

Lower Upper

-1.134 27.62 0.27 -0.34 0.30 -0.96 0.28

The above table reveals that the p-value or the critical significance level of 0.265 is greater

than 0.05 (5 percent) level of significance. Thus the null hypothesis formed is accepted.

Therefore, staffs with 20 years experience or more do not differ significantly from staffs with

lesser than 20 years experience in their agreement to use of information technology for

greater transparency in administration of GST.

54

On the basis of the above test it can be concluded that years of work experience is not an

influencing factor for agreement to use of information technology.

4.2.2 Hypothesis 2

Null Hypothesis: Trade and Industry agree to the dual structure of GST, i.e. separate GSTs

of the Centre and the State.

Alternate Hypothesis: Trade and Industry do not agree to the dual structure of GST, i.e.

separate GSTs of the Centre and the State.

Table 13: T-Test results for Hypothesis 2

One-Sample Statistics

N Mean Std. Deviation Std. Error Mean

The Centre and State must

have separate GST 24 -0.88 .90 .18

One-Sample Test

Test Value = 1

t df

Sig. (2-

tailed)

Mean

Difference

95% Confidence

Interval of the

Difference

Lower Upper

The Centre and State must

have separate GST -10.21 23 .00 -1.86 -2.26 -1.50

The above table reveals that the p-value or the critical significance level of .00 is lesser than

0.05 (5 percent) level of significance. Thus the null hypothesis formed is rejected and the

alternate hypothesis that Trade and Industry do not agree to the dual structure of GST is

accepted.

55

5 Findings and Recommendations

India has been moving towards a GST regime right from introduction of MODVAT in 1986

to the introduction of VAT in states. All these were steps taken to move to a VAT based GST

regime. Now we are at the last step of this big change. GST, basically a value added tax has

been beneficial to all countries that implemented it. Countries like New Zealand and the UK

have derived a lot of benefit from GST. Key factors contributing to the success of GST in