Mining and infrastructure: reflecting on the experiences of Tanzania and Mozambique Drawing on research conducted for the Making the Most of Commodities Project: UCT & Open University http://www.commodities.open.ac.uk/di scussionpapers and Robbins and Perkins (forthcoming 2012) Journal of International Development TIPS Seminar 1 June 2012 Glen Robbins & Dave Perkins

Transcript

Mining and infrastructure: reflecting on the

experiences of Tanzania and Mozambique

Drawing on research conducted for the Making the Most of Commodities Project: UCT & Open

apers and Robbins and Perkins (forthcoming 2012) Journal of International Development

TIPS Seminar

1 June 2012

Glen Robbins & Dave Perkins

2

Infrastructure and Mining Investment

• How infrastructure influences investment choices (in the mining activity)– Impact on scale of pre-production set-up costs and

thus delay profitability point (potentially raising costs of borrowing or risk profile of project). Note – transport less of an issue

– Feasibilities will also look closely at supply chain risks & logistics costs as these cannot be ignored – higher levels of uncertainty in predicting delivery times and costs are a concern.

– In some cases are a prerequisite

3

Infrastructure and Mining Investment• How infrastructure issues in mining influences investment choices by states

– Governments with stressed expenditure systems generally struggle to provide up-front commitments at scale

– Donor funds and World Bank/ADB loans are key but limited when scale of projects is considered (base of systems in place, topography, distance, user classes)

– Other options include deals with Chinese companies/state or some form of PPP arrangement

– Maintenance budgets tend to be limited or non-existent (a washed away bridge or a blown sub-station might take a year or more to get fixed) – although in Tanzania, with donor and loan support, the past five years have seen steady improvement

– Mining activity can be seen as a revenue source for infrastructure provision via fiscal allocations enabled because of tax/royal flows or through users charges

– Revenue flows attached with mining consumers can be used to raise funds by states or to use in PPP deals of one sort or another (limited track record of success and politically uncomfortable, unattractive terms due to risk perceptions)

– Often a reliance on investors in mining projects to fund infrastructure connections (access roads, rail-heads, connections to grid, water pipes) in full at no consumption charge discount (attractive to states as it adds to next coverage of infrastructure and might allow previously un-served communities access to some services with no significant diversion of state resources)

44

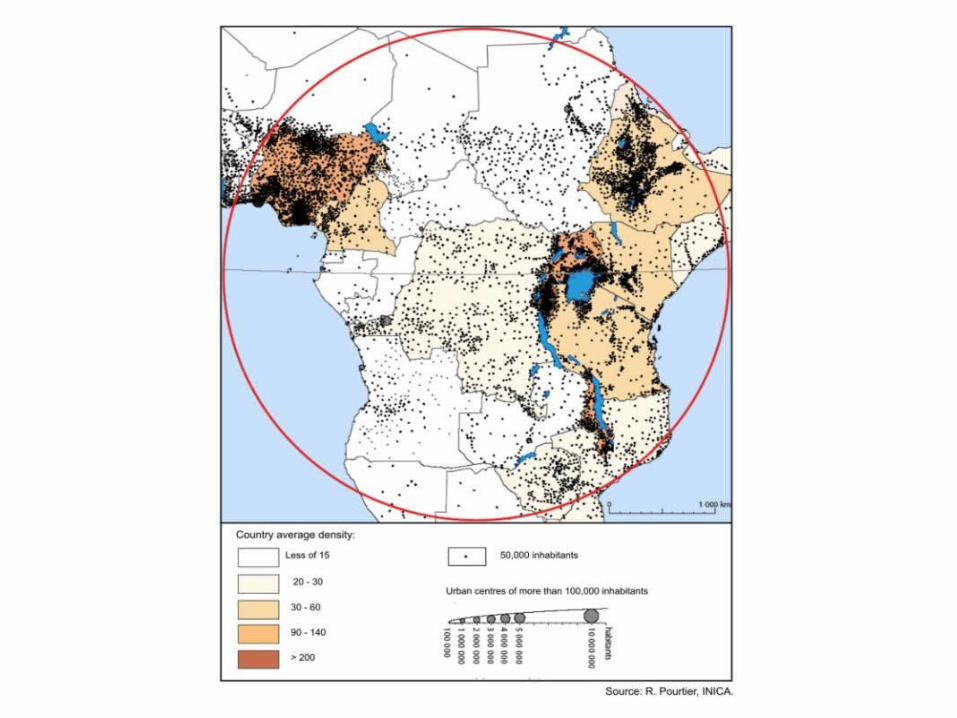

Tanzania and Mozambique

• Tanzania and Mozambique are in the upper-middle ranking of African countries in terms of FDI, with its FDI stock doubling in the first half of the 2000s and again in the second half.– Both have been among the best African FDI performers outside

countries with oil and gas (with exception of RSA)– These countries have overtaken traditional stronger performers in FDI

growth (Kenya, Botswana etc)– Two thirds of growth in FDI stock since 2000 is accounted for by mining

Tanzania’s infrastructure• “Despite its geographic advantages as a potential entrepôt to its landlocked

neighbors Burundi, Rwanda, Uganda and Zambia, as well as the D.R. Congo, there is clear evidence to suggest that Tanzania’s lack of infrastructure is acting as a constraint on the expansion of trade and economic activity in both the country and the region.” (Ter-Minassian et al, 2008: 8)

• The World Bank’s Logistics Performance Index (World Bank 2007a) ranked Tanzania’s transport infrastructure well below the average of other sub-Saharan African and low-income countries.

• In the power sector losses from power failure amount to 10 percent of sales for the median Tanzanian firm compared to only 1 percent for the median Chinese firm. (Eifert, Gelb & Ramachandran, 2005)

• Pedersen quotes Mwase as saying that the passability of Tranzania roads declined from 70 pecent in 1970 to 30 percent in 1991 (Mwase in Pedersen, 2001: 12).

• These empirical findings are corroborated by evidence from business surveys:

– Global Competitiveness Report (2007-08)– UNCTAD WIR (various)– Enterprise survey (WB) and Investment climate survey (WB)

• There have been some improvements but quite limited in terms of scale of backlog/needs

The growing gap between mining investment and infrastructure spend

• Historic synergies between developing infrastructure platforms and enabling mining extraction that also yielded a measure of linkages (synergies not just in terms of supply and demand but also in terms of capabilities)

• Slight recovery (in historical terms) of infrastructure spend in SSA (excl RSA) largely driven by donor commitment post SAPs but growing gap as no country fiscal capability, limited ODA and lack of private take up in PPPs. (not including mobile telecommunications)

1940s 1960s 1980s 2000s

Capital invest-ment

Mining investment

Infrastructure investment

Tanzania conceptual image & timeline

1967 Arusha Declaration: 60% of all production in hands of state