47

Ministerio de Comercio, Industria y Turismo República de Colombia GABRIEL DUQUE MILDENBERG Viceminister for Foreign Trade June 7th, 2010 COLOMBIAN TRADE POLICY AND LOGISTICS

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | janet-whiston |

| View: | 217 times |

| Download: | 0 times |

Ministerio de Comercio, Industria y TurismoRepública de Colombia

GABRIEL DUQUE MILDENBERGViceminister for Foreign Trade

June 7th, 2010

COLOMBIAN TRADE POLICY

AND LOGISTICS

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Content

I. Colombia: A Top Global and Regional Reformer

II. Trade Policy

III. Tariffs versus Logistics Costs

IV. Logistics in Colombia

Ministerio de Comercio, Industria y TurismoRepública de Colombia

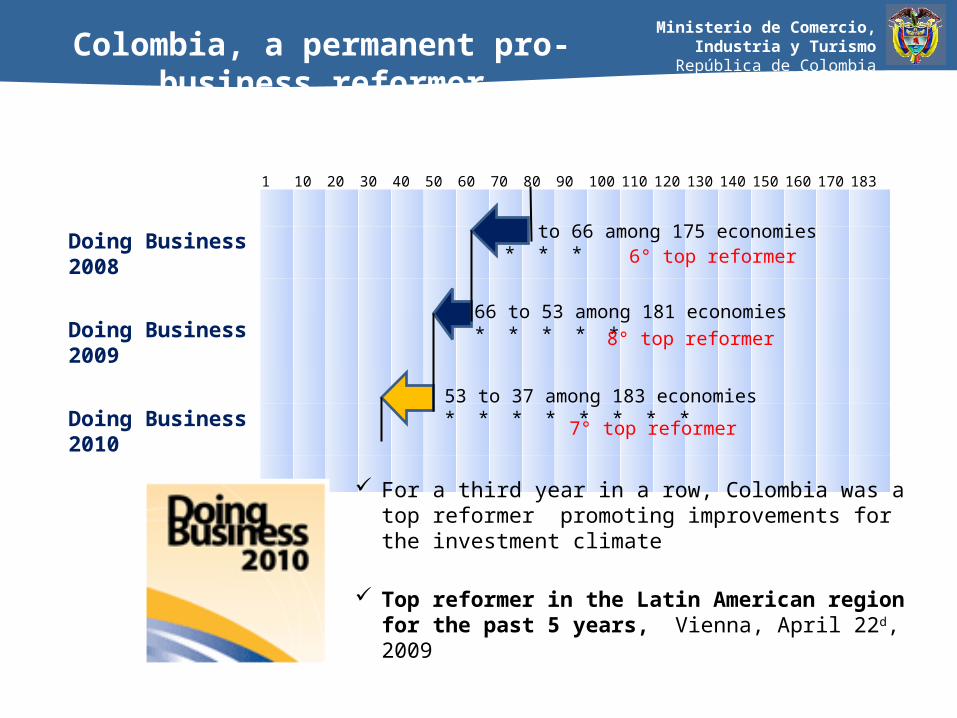

1 10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160 170 183

Doing Business 2008

Doing Business 2009

Doing Business 2010

83 to 66 among 175 economies* * *

66 to 53 among 181 economies* * * * *

53 to 37 among 183 economies* * * * * * * *7° top reformer

8° top reformer

6° top reformer

Colombia, a permanent pro-business reformer

For a third year in a row, Colombia was a top reformer promoting improvements for the investment climate

Top reformer in the Latin American region for the past 5 years, Vienna, April 22d, 2009

Ministerio de Comercio, Industria y TurismoRepública de Colombia

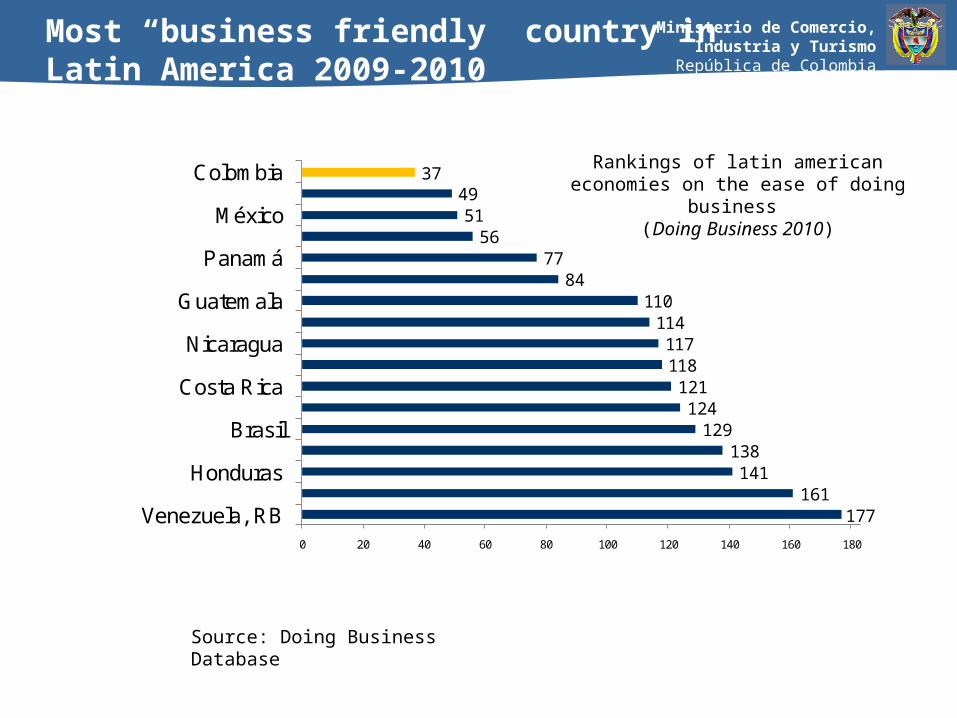

177161

141138

129124

121118117

114110

8477

5651

4937

0 20 40 60 80 100 120 140 160 180

Venezuela, RB

Honduras

Brasil

Costa Rica

Nicaragua

Guatemala

Panamá

México

Colombia

Most “business friendly” country in Latin America 2009-2010

Rankings of latin american economies on the ease of doing business

(Doing Business 2010)

Source: Doing Business Database

Ministerio de Comercio, Industria y TurismoRepública de Colombia

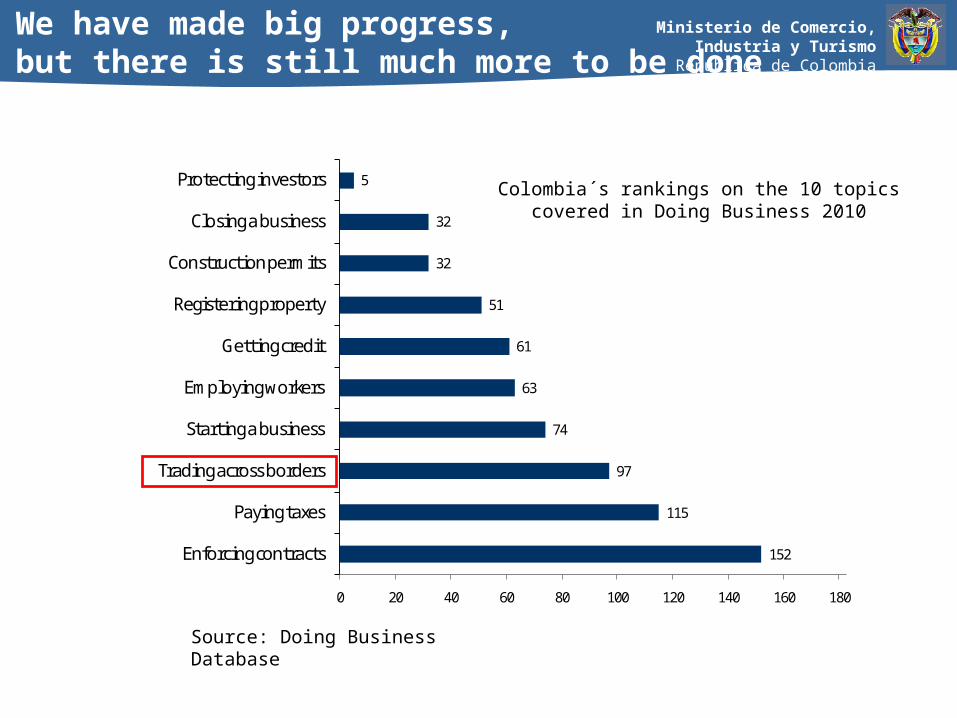

We have made big progress,but there is still much more to be done

152

115

97

74

63

61

51

32

32

5

0 20 40 60 80 100 120 140 160 180

Enforcing contracts

Paying taxes

Trading across borders

Starting a business

Employing workers

Getting credit

Registering property

Construction permits

Closing a business

Protecting investors Colombia´s rankings on the 10 topics covered in Doing Business 2010

Source: Doing Business Database

Ministerio de Comercio, Industria y TurismoRepública de Colombia

• Presidential mandate

• Technical assistance from WB & IFC

• Presidential directive

• Designation of project manager

• Strong convincement of the public institutions and the private sector on the usefulness of facilitating the entrepreneurial activity while strengthening effective regulation.

• Prioritization of key reforms

• Leadership from the Ministry to coordinate and synchronize efforts and tasks at national and local levels to attain improvements on identified Doing Business issues and to comply with set deadlines and goals.

Some of the parties involved: National Planning Department, Ministry of Social Welfare, Ministry of Justice, Finance Ministry, Ministry of Environment, Housing, and Territorial Development, Ministry of Transport, Congress, Judicial Administration, National Tax Administration, Financial Superintendence, Superintendence of Companies, Superintendence of Industry and Commerce, Chambers of Commerce Association (Confecámaras), Chamber of Commerce of Bogotá, the Mayor of Bogotá and his cabinet

What have we done in order to have a better investment climate

Ministerio de Comercio, Industria y TurismoRepública de Colombia

II. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

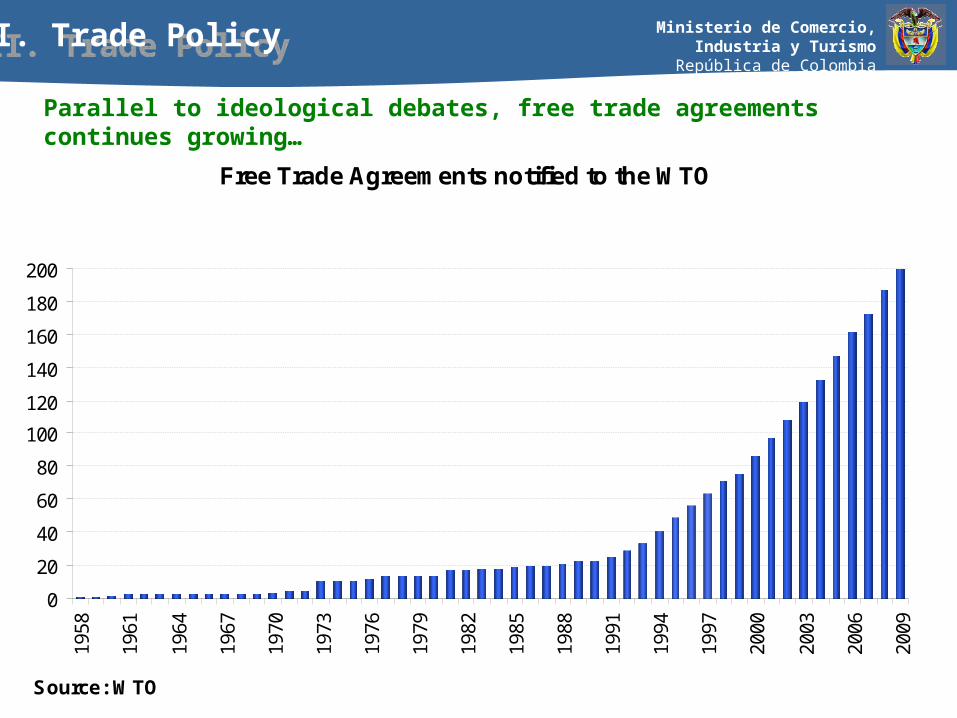

Parallel to ideological debates, free trade agreements continues growing…

Free Trade Agreements notified to the WTO

0

20

40

60

80

100

120

140

160

180

200

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

2006

2009

Source: WTO

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

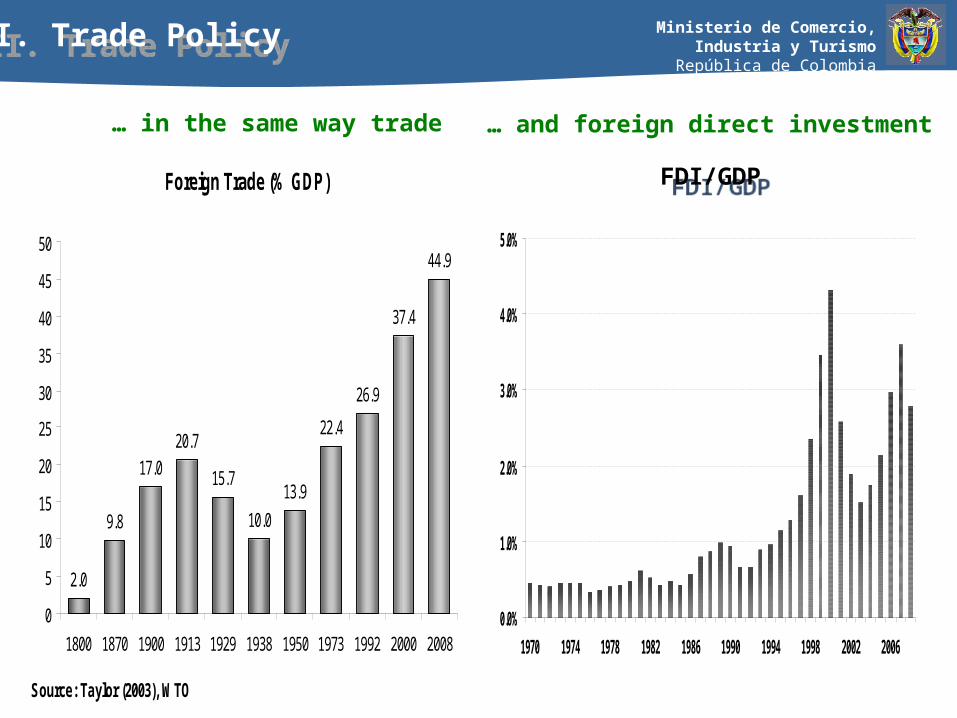

… in the same way trade

Foreign Trade (% GDP)

2.0

9.8

17.020.7

15.7

10.0

13.9

22.4

26.9

37.4

44.9

0

5

10

15

20

25

30

35

40

45

50

1800 1870 1900 1913 1929 1938 1950 1973 1992 2000 2008

Source: Taylor (2003), WTO

II. Trade PolicyII. Trade Policy

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006

… and foreign direct investment

FDI/GDPFDI/GDP

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Source: IMF

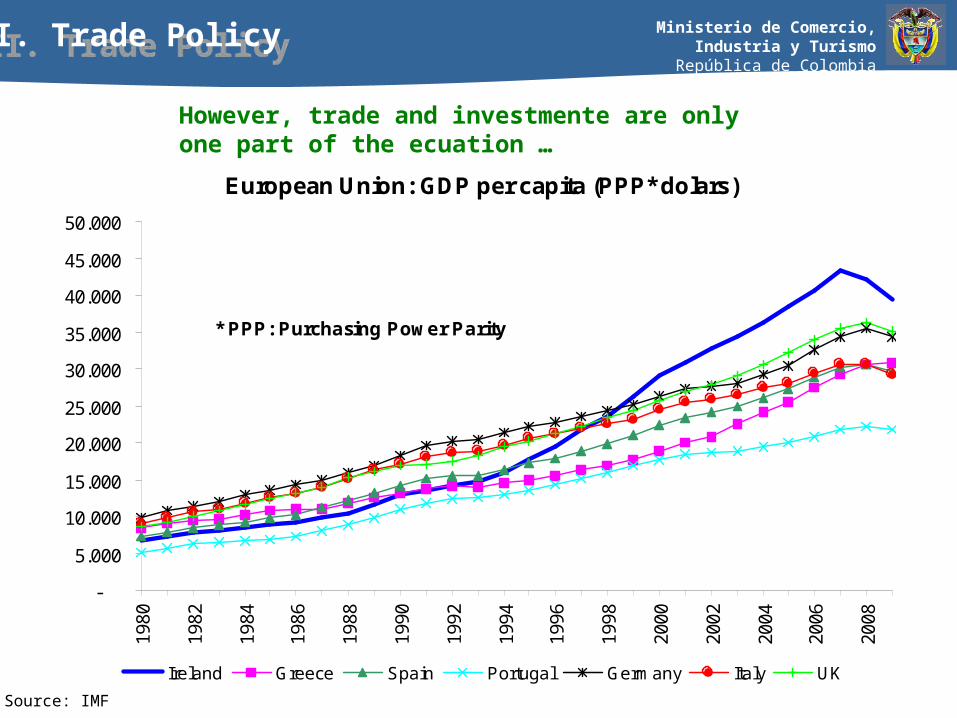

However, trade and investmente are only one part of the ecuation …

II. Trade PolicyII. Trade Policy

European Union: GDP per capita (PPP* dolars)

-

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

50.000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

* PPP: Purchasing Power Parity

Ireland Greece Spain Portugal Germany Italy UK

Ministerio de Comercio, Industria y TurismoRepública de Colombia

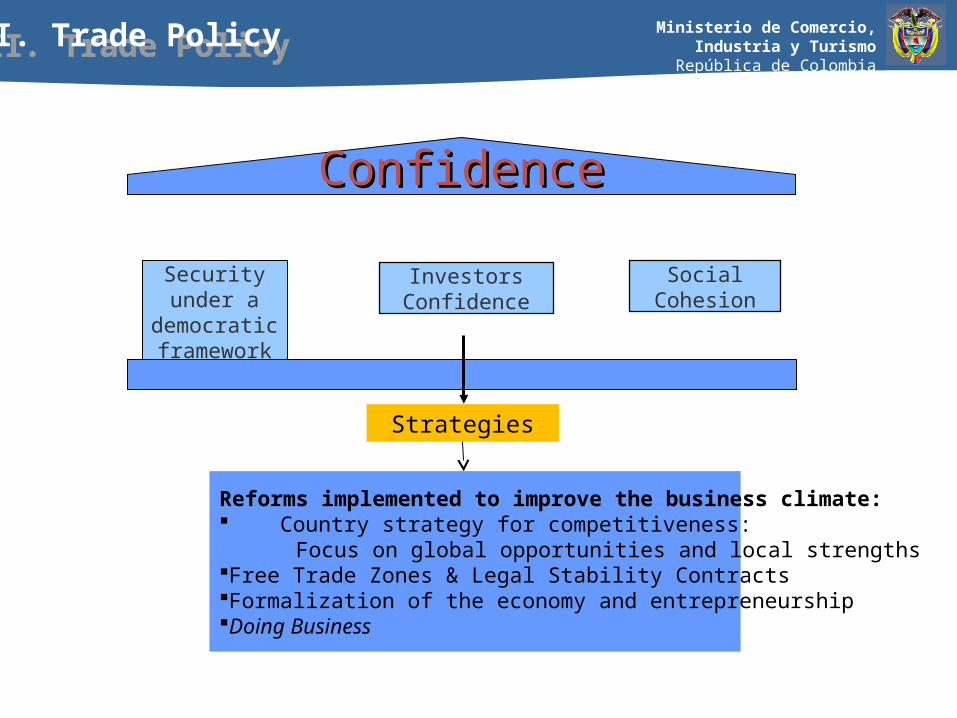

ConfidenceConfidence

Security under a democratic framework

Social CohesionInvestors Confidence

Strategies

Reforms implemented to improve the business climate: Country strategy for competitiveness: Focus on global opportunities and local strengthsFree Trade Zones & Legal Stability Contracts Formalization of the economy and entrepreneurshipDoing Business

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

As an small economy, Colombia needs an insertion estrategy to global economy :

• Maximize benefits from an estable and long run preferential access to foreign markets.

• Attract more investment.

• Diversify colombian exports, by markets and products.

• Exploit comparative advantages and incorporate new tachnologies.

As an small economy, Colombia needs an insertion estrategy to global economy :

• Maximize benefits from an estable and long run preferential access to foreign markets.

• Attract more investment.

• Diversify colombian exports, by markets and products.

• Exploit comparative advantages and incorporate new tachnologies.

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

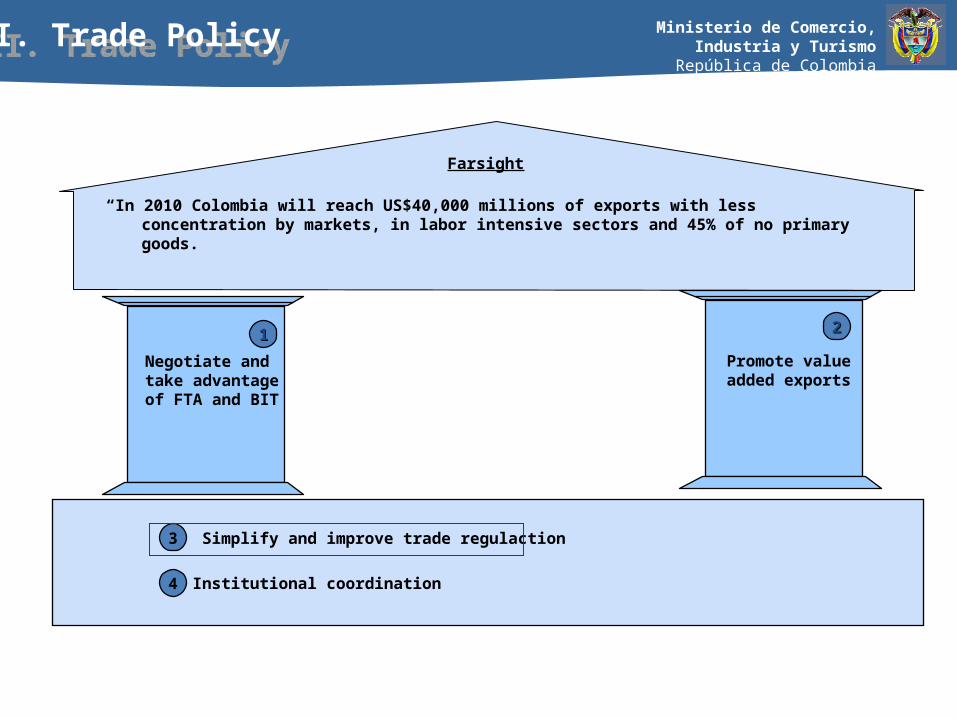

“In 2010 Colombia will reach US$40,000 millions of exports with less concentration by markets, in labor intensive sectors and 45% of no primary goods.

Farsight

11

3 Simplify and improve trade regulaction

4 Institutional coordination

Negotiate and take advantage of FTA and BIT

22

Promote value added exports

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

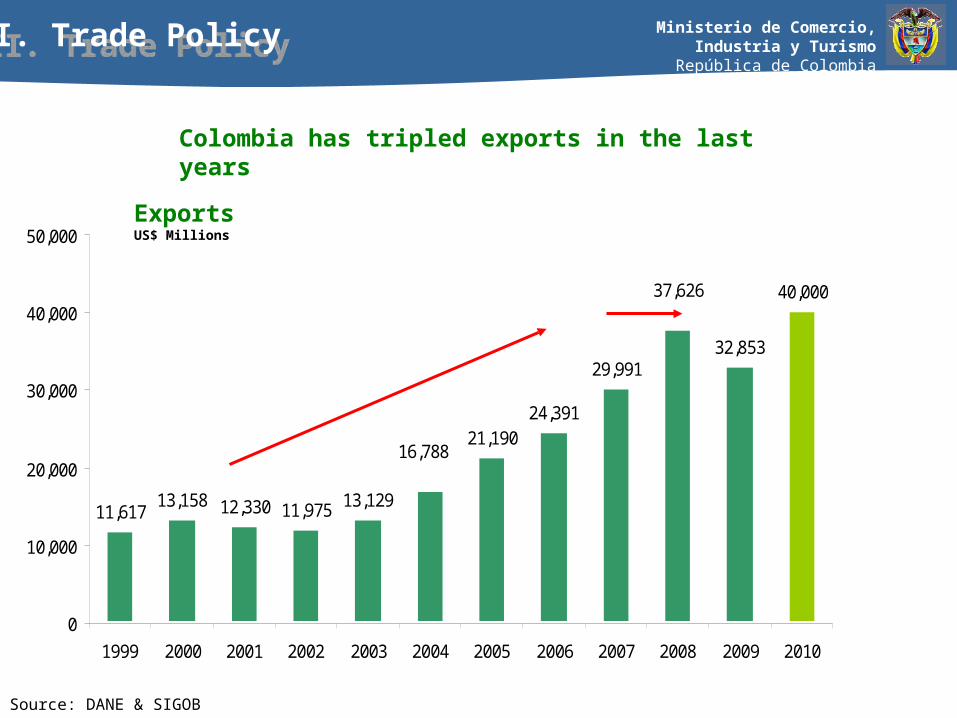

ExportsUS$ Millions

Source: DANE & SIGOB

Colombia has tripled exports in the last years

11,61713,158 12,330 11,975 13,129

21,19024,391

29,99132,853

40,000

16,788

37,626

0

10,000

20,000

30,000

40,000

50,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

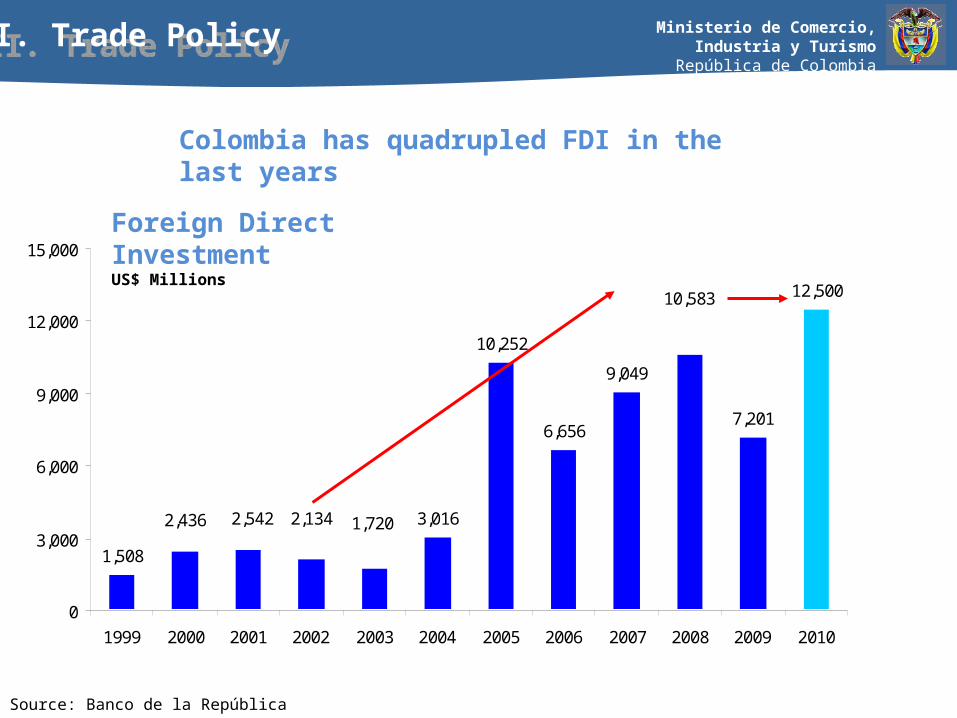

Foreign Direct InvestmentUS$ Millions

Colombia has quadrupled FDI in the last years

1,508

3,016

10,252

6,656

9,049

7,201

12,500

1,7202,1342,5422,436

10,583

0

3,000

6,000

9,000

12,000

15,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Source: BR

Source: Banco de la República

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

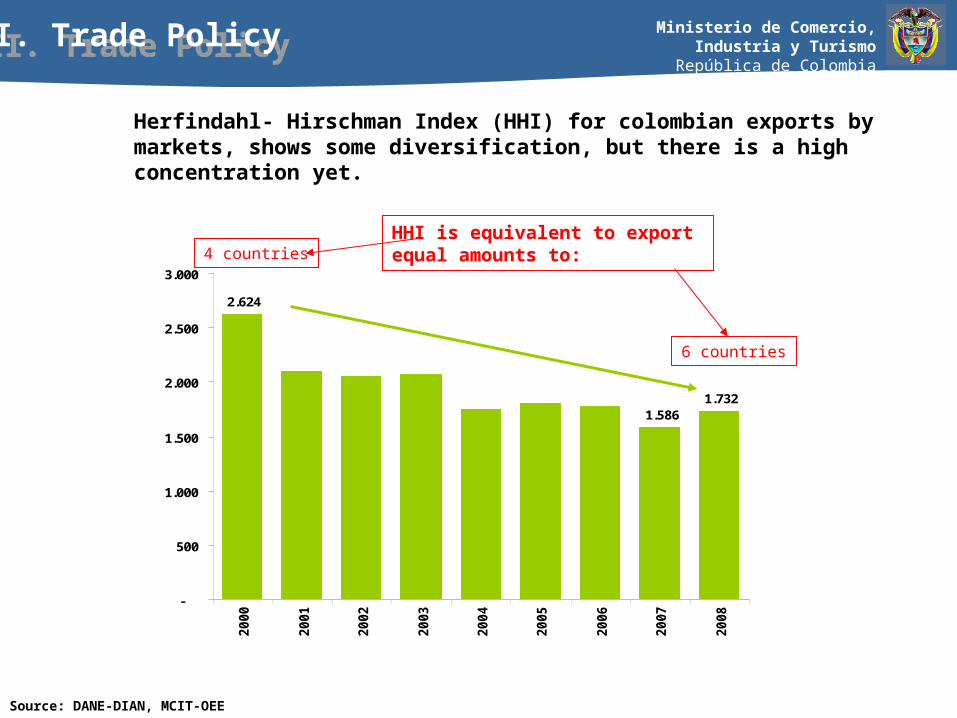

1.5861.732

2.624

-

500

1.000

1.500

2.000

2.500

3.000

2000

2001

2002

2003

2004

2005

2006

2007

2008

IHH

Herfindahl- Hirschman Index (HHI) for colombian exports by markets, shows some diversification, but there is a high concentration yet.

Source: DANE-DIAN, MCIT-OEE

HHI is equivalent to export equal amounts to:4 countries

6 countries

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

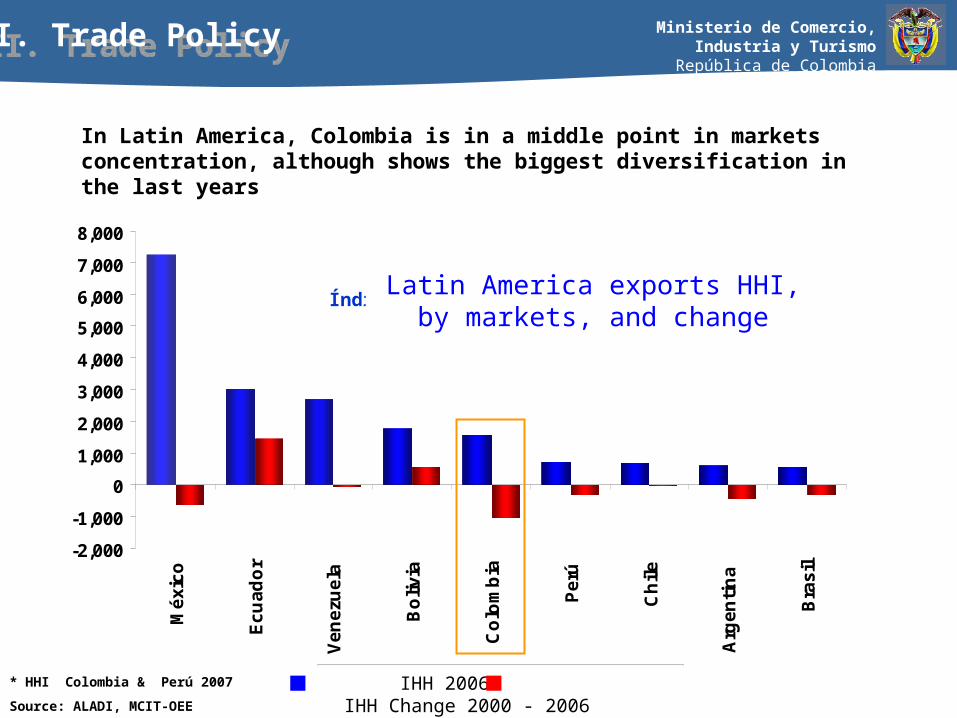

Índice de concentración de las exportaciones y cambio en países de América Latina

* HHI Colombia & Perú 2007

Source: ALADI, MCIT-OEE

In Latin America, Colombia is in a middle point in markets concentration, although shows the biggest diversification in the last years

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Mé

xic

o

Ec

ua

do

r

Ve

ne

zue

la

Bo

liv

ia

Co

lom

bia

Pe

rú

Ch

ile

Arg

en

tin

a

Bra

sil

IHH 2006 Cambio en IHH entre 2000 y 2006 IHH 2006 IHH Change 2000 - 2006

Latin America exports HHI, by markets, and change

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

* HS 4 digits

Source: DANE, DIAN, MCIT-OEE

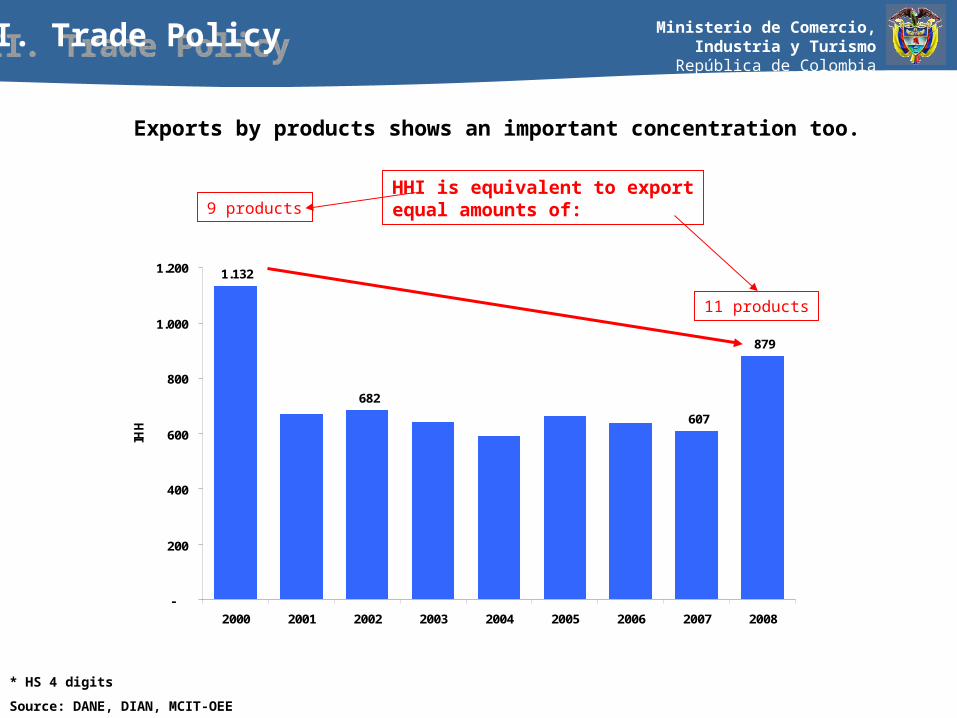

879

607

1.132

682

-

200

400

600

800

1.000

1.200

2000 2001 2002 2003 2004 2005 2006 2007 2008

IHH

Exports by products shows an important concentration too.

HHI is equivalent to exportequal amounts of:9 products

11 products

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

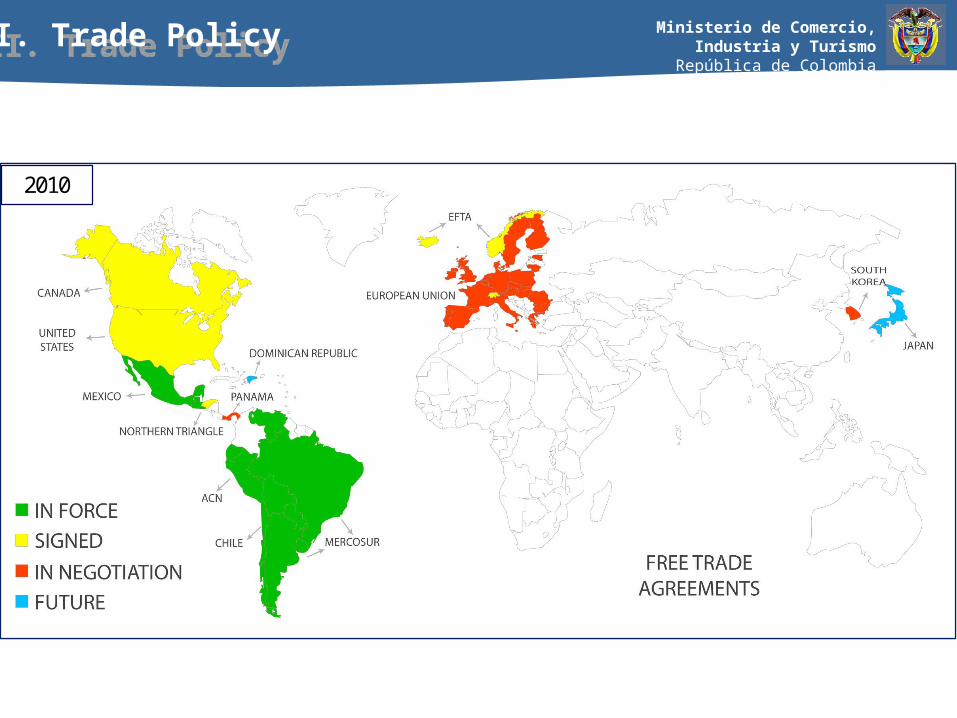

20102010

II. Trade PolicyII. Trade Policy

Ministerio de Comercio, Industria y TurismoRepública de Colombia

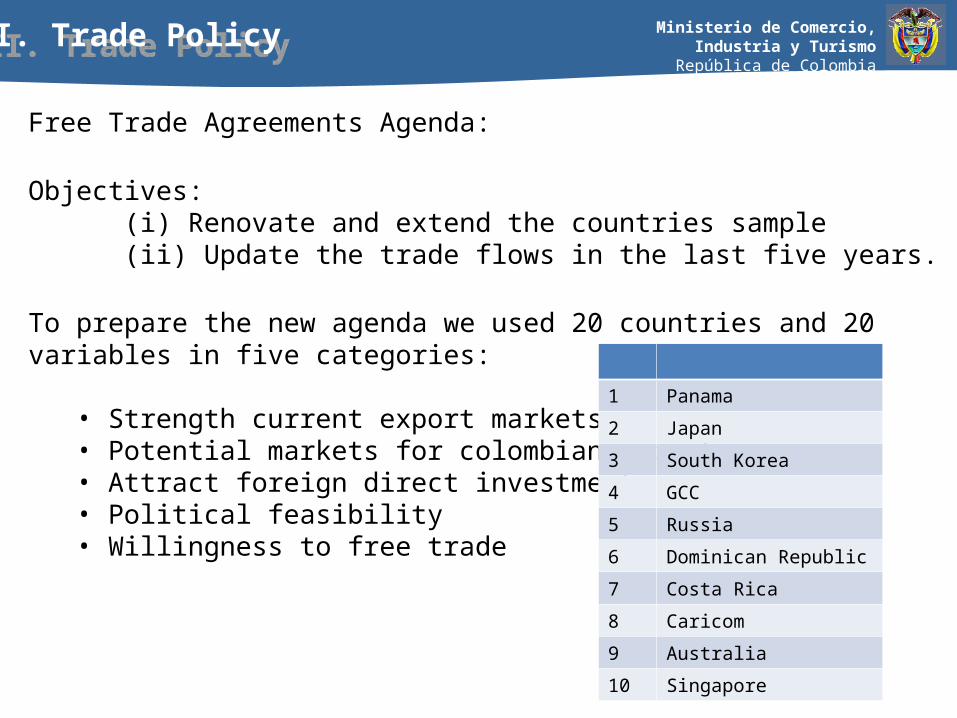

Free Trade Agreements Agenda:

Objectives:(i) Renovate and extend the countries sample (ii) Update the trade flows in the last five years.

To prepare the new agenda we used 20 countries and 20 variables in five categories:

• Strength current export markets• Potential markets for colombian exports• Attract foreign direct investment• Political feasibility• Willingness to free trade

II. Trade PolicyII. Trade Policy

1 Panama

2 Japan

3 South Korea

4 GCC

5 Russia

6 Dominican Republic

7 Costa Rica

8 Caricom

9 Australia

10 Singapore

Ministerio de Comercio, Industria y TurismoRepública de Colombia

III. Tariffs versus Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

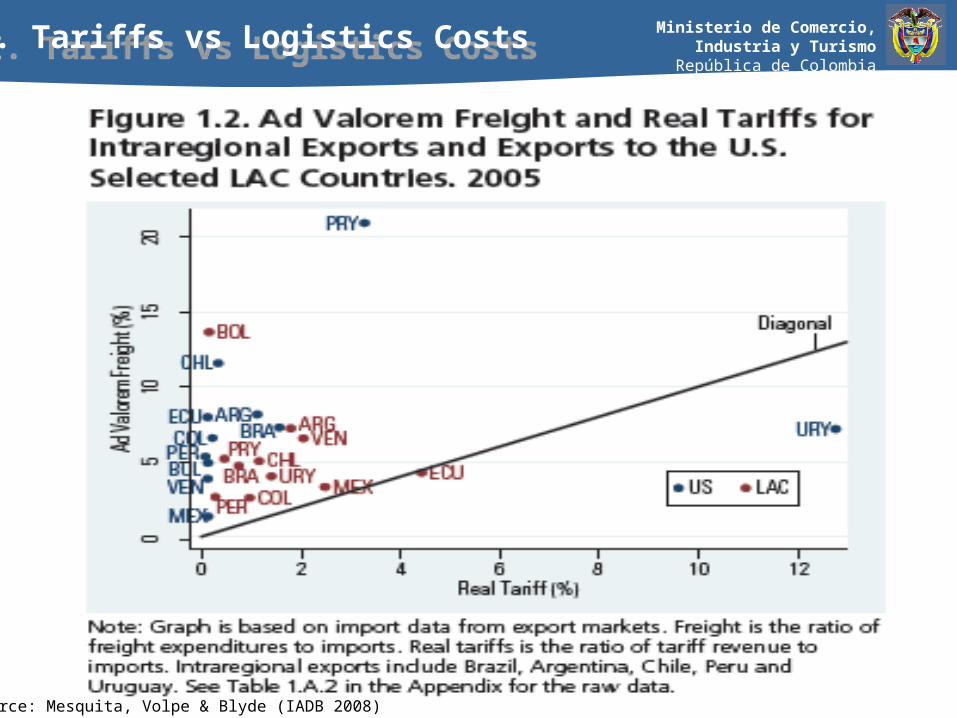

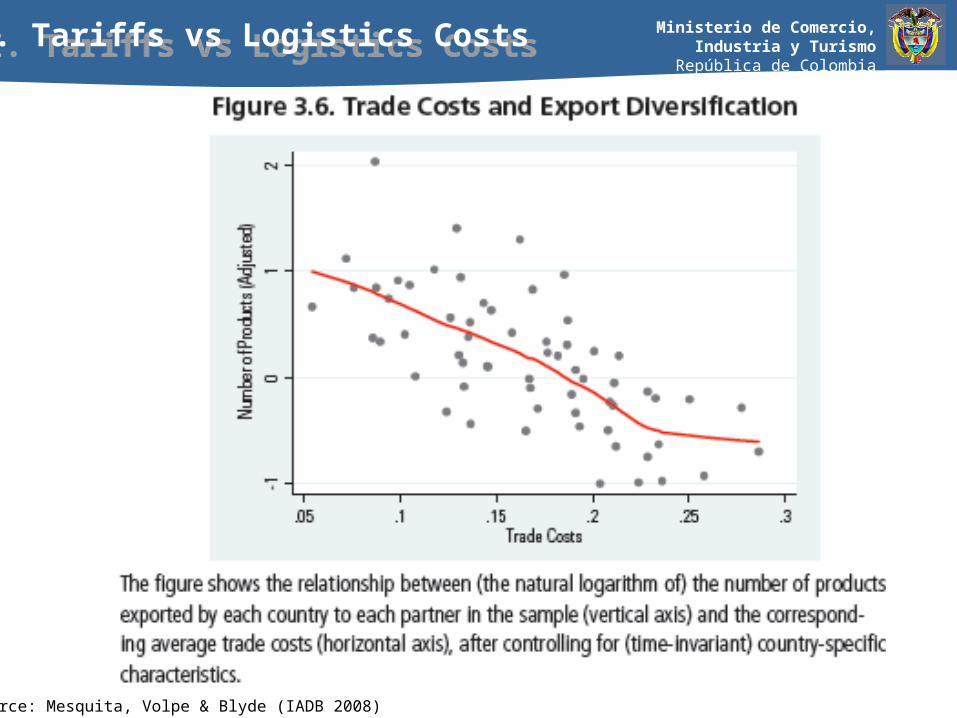

Source: Mesquita, Volpe & Blyde (IADB 2008)

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

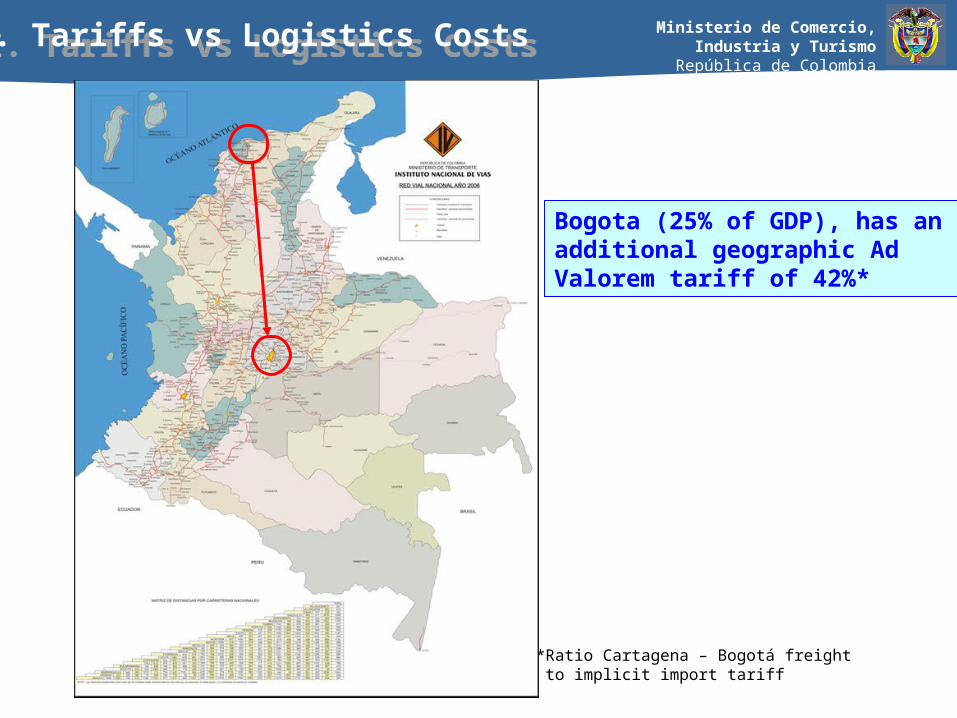

Bogota (25% of GDP), has an additional geographic AdValorem tariff of 42%*

*Ratio Cartagena – Bogotá freight to implicit import tariff

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

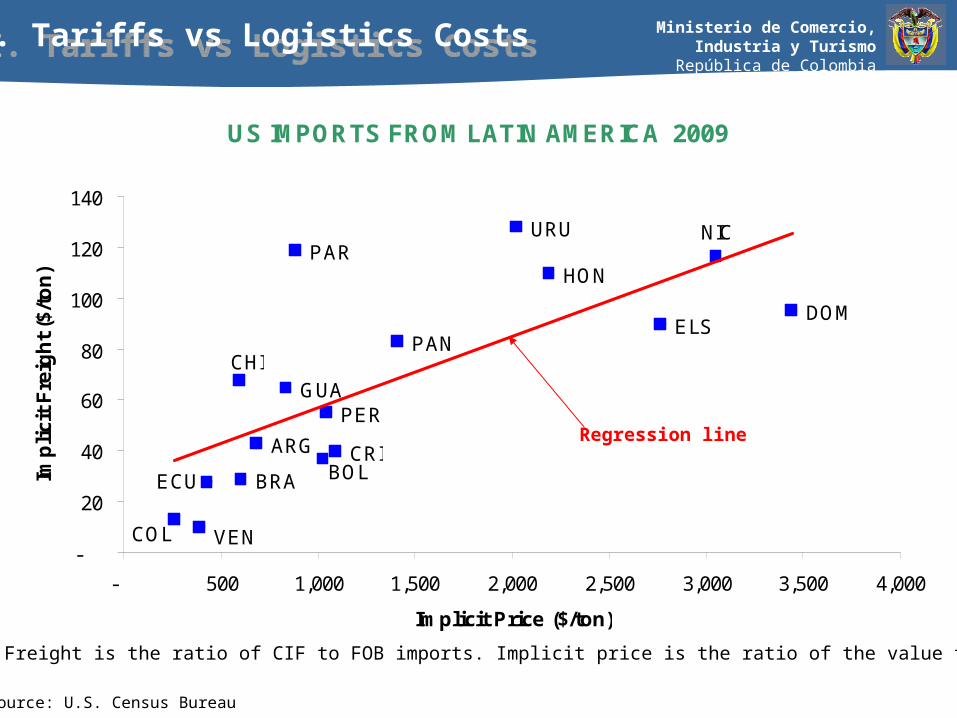

Note: Implicit Freight is the ratio of CIF to FOB imports. Implicit price is the ratio of the value to volume imports

Source: U.S. Census Bureau

US IMPORTS FROM LATIN AMERICA 2009

ARG

BRACRI

DOMELS

GUA

HON

PAN

PAR

PER

URU

BOL

CHI

COL

ECU

NIC

VEN-

20

40

60

80

100

120

140

- 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Implicit Price ($/ton)

Imp

lici

t F

reig

ht

($/t

on

)

Regression line

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Source: Mesquita, Volpe & Blyde (IADB 2008)

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

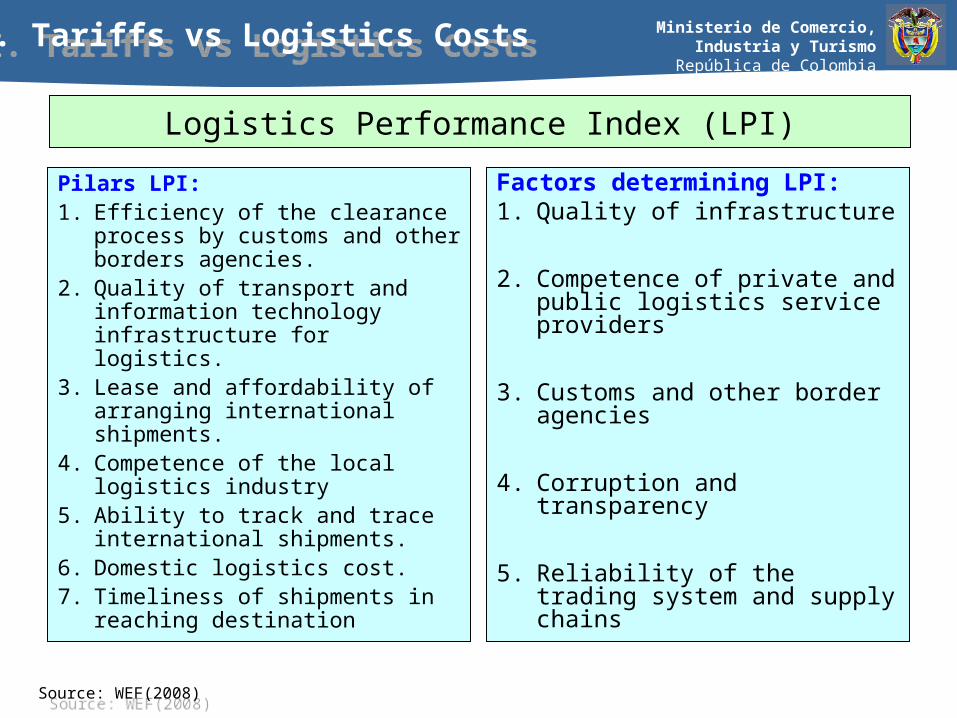

Logistics Performance Index (LPI)

Pilars LPI:1. Efficiency of the clearance

process by customs and other borders agencies.

2. Quality of transport and information technology infrastructure for logistics.

3. Lease and affordability of arranging international shipments.

4. Competence of the local logistics industry

5. Ability to track and trace international shipments.

6. Domestic logistics cost.7. Timeliness of shipments in

reaching destination

Factors determining LPI:1. Quality of infrastructure

2. Competence of private and public logistics service providers

3. Customs and other border agencies

4. Corruption and transparency

5. Reliability of the trading system and supply chains

Source: WEF(2008)Source: WEF(2008)

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

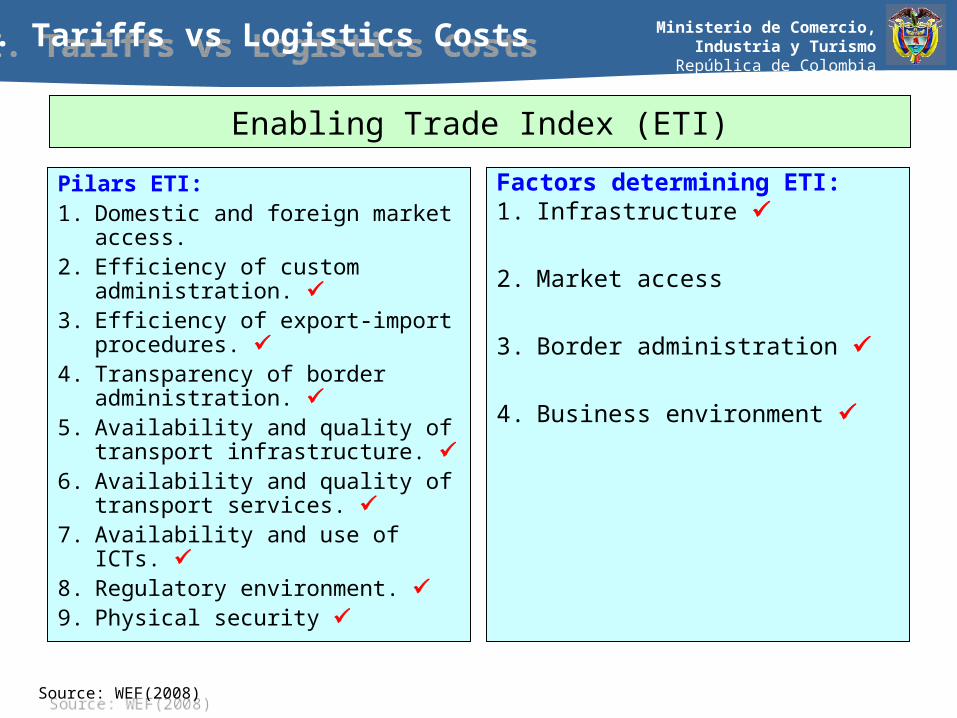

Enabling Trade Index (ETI)

Pilars ETI:1. Domestic and foreign market

access.2. Efficiency of custom

administration. 3. Efficiency of export-import

procedures. 4. Transparency of border

administration. 5. Availability and quality of transport

infrastructure. 6. Availability and quality of transport

services. 7. Availability and use of ICTs. 8. Regulatory environment. 9. Physical security

Factors determining ETI:1. Infrastructure

2. Market access

3. Border administration

4. Business environment

Source: WEF(2008)Source: WEF(2008)

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

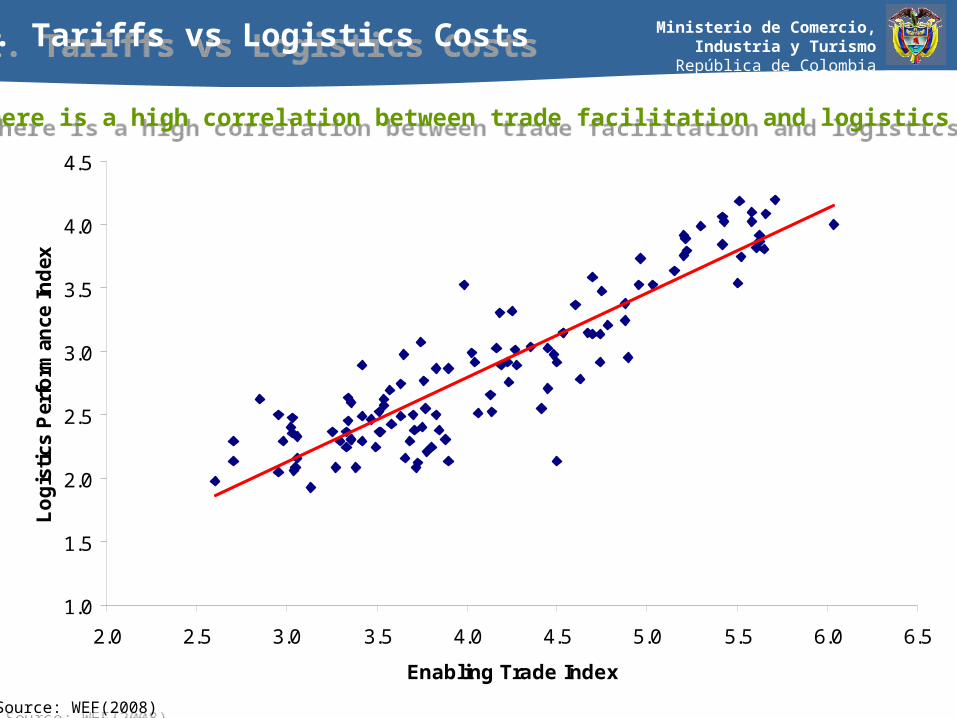

Ministerio de Comercio, Industria y TurismoRepública de Colombia

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5

Enabling Trade Index

Lo

gis

tics

Per

form

ance

In

dex

Source: WEF(2008)Source: WEF(2008)

There is a high correlation between trade facilitation and logisticsThere is a high correlation between trade facilitation and logistics

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Source: WEF(2008)Source: WEF(2008)

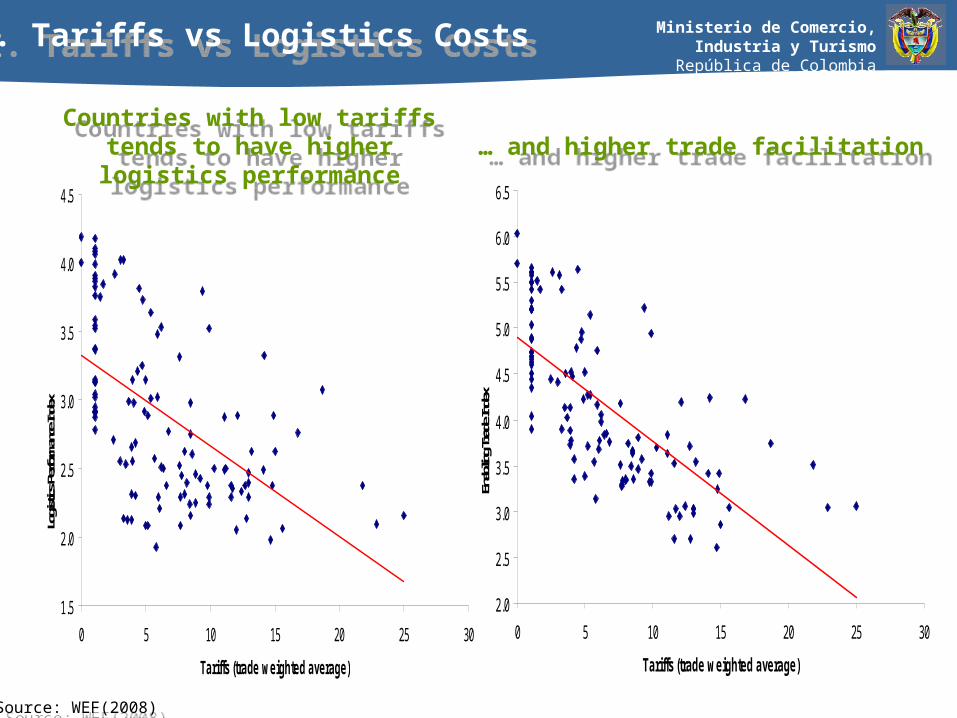

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0 5 10 15 20 25 30

Tariffs (trade weighted average)

Logis

tics P

erform

ance

Index

Countries with low tariffs tends to have higher logistics performance

Countries with low tariffs tends to have higher logistics performance

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

0 5 10 15 20 25 30

Tariffs (trade weighted average)

Enab

ling T

rade I

ndex

… and higher trade facilitation… and higher trade facilitation

III. Tariffs vs Logistics CostsIII. Tariffs vs Logistics Costs

Ministerio de Comercio, Industria y TurismoRepública de Colombia

IV. Logistics in ColombiaA. Current situationB. Challenges

Ministerio de Comercio, Industria y TurismoRepública de Colombia

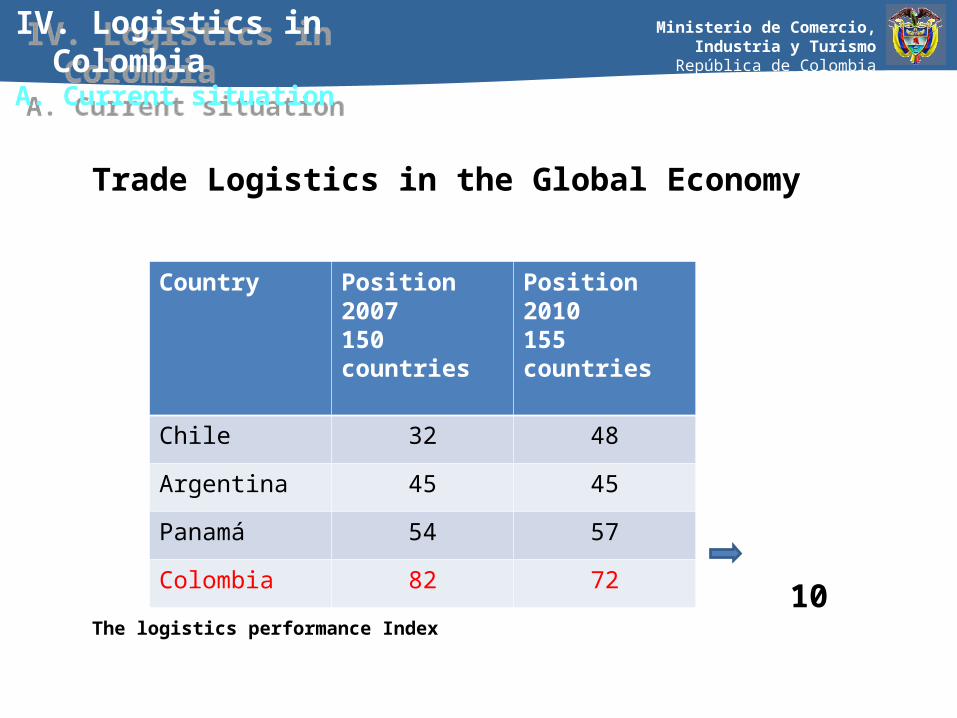

Trade Logistics in the Global Economy

10The logistics performance Index

Country Position 2007150 countries

Position 2010155 countries

Chile 32 48

Argentina 45 45

Panamá 54 57

Colombia 82 72

IV. Logistics in Colombia

A. Current situation

IV. Logistics in Colombia

A. Current situation

Ministerio de Comercio, Industria y TurismoRepública de Colombia

2007Colombia had no Logistics National PolicyAll customs administration was with physical documents and

authorizations required dealing with multiple institutions. Partial electronic processing

There was no coordination among institutions for physical inspections

2010Colombia has a Logistics National Policy that is been

implementedCustoms administration documents and procedures are digital

and using a ‘single window’ (VUCE/MUISCA)Simultaneous inspection procedures for exports through ports,

work on improvement of risk assessments and plan for the provision of scanners

IV. Logistics in Colombia

A. Current situation

IV. Logistics in Colombia

A. Current situation

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Source: WEF(2010)Source: WEF(2010)

(% countries below)(% countries below)

Competitive advantageCompetitive advantage

Competitive disadvantageCompetitive disadvantage

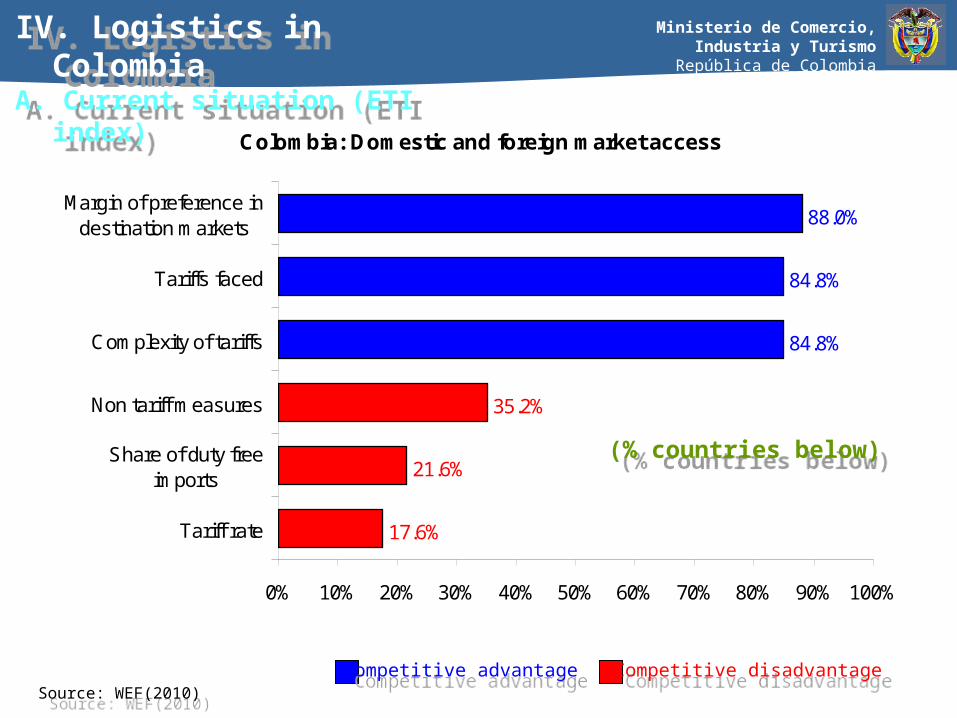

Colombia: Domestic and foreign market access

17.6%

21.6%

35.2%

84.8%

84.8%

88.0%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Tariff rate

Share of duty freeimports

Non tariff measures

Complexity of tariffs

Tariffs faced

Margin of preference indestination markets

IV. Logistics in ColombiaA. Current situation (ETI index)

IV. Logistics in ColombiaA. Current situation (ETI index)

Ministerio de Comercio, Industria y TurismoRepública de Colombia

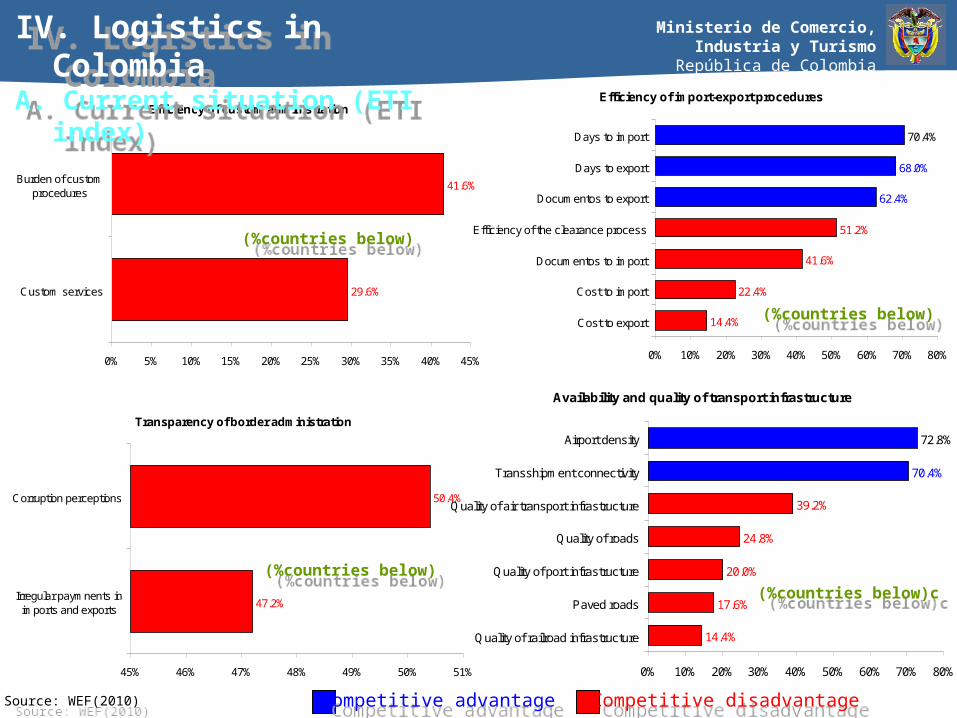

Efficiency of custom administration

41.6%

29.6%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Custom services

Burden of customprocedures

Efficiency of import-export procedures

70.4%

14.4%

22.4%

41.6%

51.2%

62.4%

68.0%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Cost to export

Cost to import

Documentos to import

Efficiency of the clearance process

Documentos to export

Days to export

Days to import

Transparency of border administration

47.2%

50.4%

45% 46% 47% 48% 49% 50% 51%

Irregular paymnents inimports and exports

Corruption perceptions

Availability and quality of transport infrastructure

72.8%

70.4%

39.2%

24.8%

20.0%

17.6%

14.4%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Quality of railroad infrastructure

Paved roads

Quality of port infrastructure

Quality of roads

Quality of air transport infrastructure

Transshipment connectivity

Airport density

Competitive advantageCompetitive advantage

Competitive disadvantageCompetitive disadvantage

Source: WEF(2010)Source: WEF(2010)

(%countries below)(%countries below)

(%countries below)(%countries below)

(%countries below)c(%countries below)c

(%countries below)(%countries below)

IV. Logistics in ColombiaA. Current situation (ETI index)

IV. Logistics in ColombiaA. Current situation (ETI index)

Ministerio de Comercio, Industria y TurismoRepública de Colombia

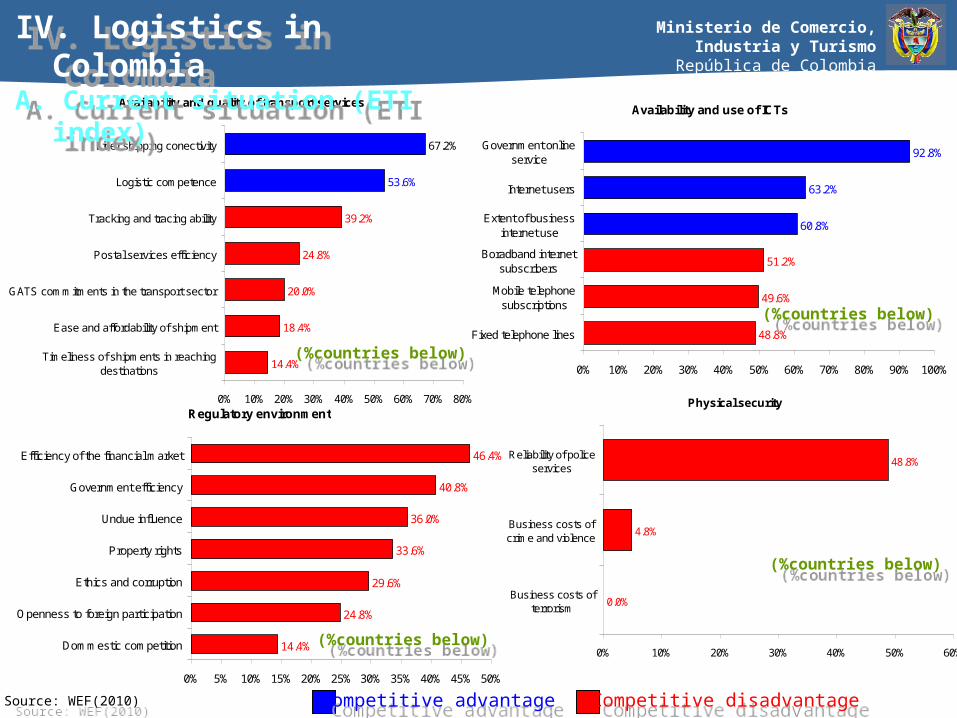

Availability and quality of transport services

67.2%

14.4%

18.4%

20.0%

24.8%

39.2%

53.6%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Timeliness of shipments in reachingdestinations

Ease and affordability of shipment

GATS commitments in the transport sector

Postal services efficiency

Tracking and tracing ability

Logistic competence

Liner shipping conectivity

Availability and use of ICTs

92.8%

63.2%

60.8%

51.2%

49.6%

48.8%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fixed telephone lines

Mobile telephonesubscriptions

Boradband internetsubscribers

Extent of businessinternet use

Internet users

Government onlineservice

Regulatory environment

46.4%

40.8%

36.0%

33.6%

29.6%

24.8%

14.4%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Dommestic competition

Openness to foreign participation

Ethics and corruption

Property rights

Undue influence

Government efficiency

Efficiency of the financial market

Physical security

0.0%

4.8%

48.8%

0% 10% 20% 30% 40% 50% 60%

Business costs ofterrorism

Business costs ofcrime and violence

Reliability of policeservices

Competitive advantageCompetitive advantage

Competitive disadvantageCompetitive disadvantage

Source: WEF(2010)Source: WEF(2010)

(%countries below)(%countries below)

(%countries below)(%countries below)

(%countries below)(%countries below)

(%countries below)(%countries below)

IV. Logistics in ColombiaA. Current situation (ETI index)

IV. Logistics in ColombiaA. Current situation (ETI index)

Ministerio de Comercio, Industria y TurismoRepública de Colombia

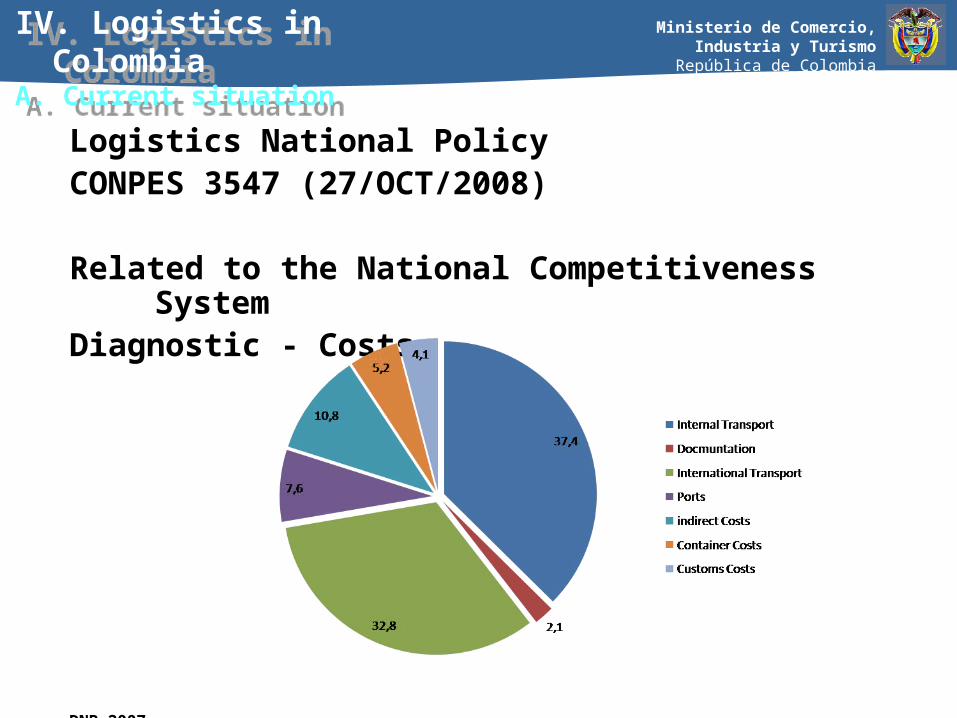

Logistics National PolicyCONPES 3547 (27/OCT/2008)

Related to the National Competitiveness SystemDiagnostic - Costs

DNP 2007

IV. Logistics in Colombia

A. Current situation

IV. Logistics in Colombia

A. Current situation

Ministerio de Comercio, Industria y TurismoRepública de Colombia

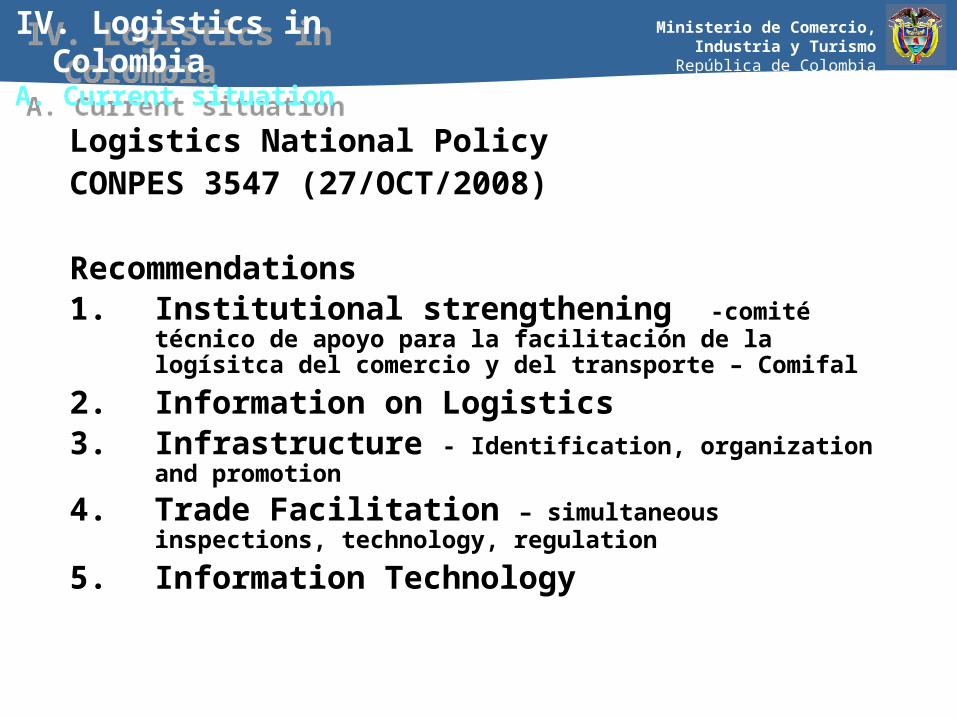

Logistics National PolicyCONPES 3547 (27/OCT/2008)

Recommendations1. Institutional strengthening -comité técnico de apoyo

para la facilitación de la logísitca del comercio y del transporte – Comifal

2. Information on Logistics3. Infrastructure - Identification, organization and promotion

4. Trade Facilitation – simultaneous inspections, technology, regulation

5. Information Technology

IV. Logistics in Colombia

A. Current situation

IV. Logistics in Colombia

A. Current situation

Ministerio de Comercio, Industria y TurismoRepública de Colombia

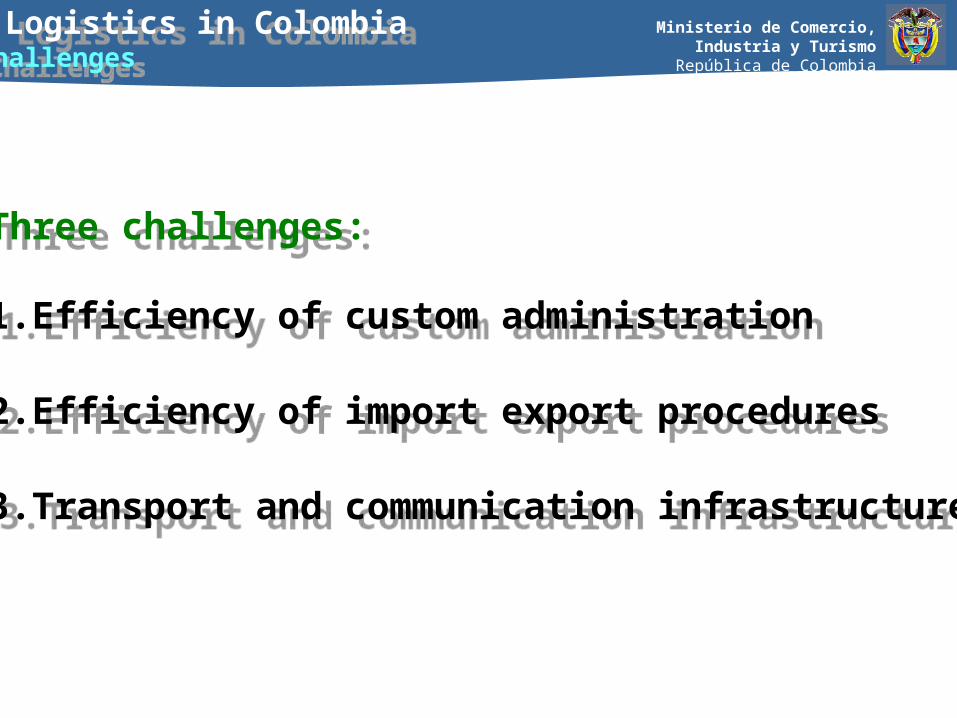

Three challenges:

1.Efficiency of custom administration

2.Efficiency of import export procedures

3.Transport and communication infrastructure

Three challenges:

1.Efficiency of custom administration

2.Efficiency of import export procedures

3.Transport and communication infrastructure

IV. Logistics in ColombiaB. Challenges

IV. Logistics in ColombiaB. Challenges

Ministerio de Comercio, Industria y TurismoRepública de Colombia

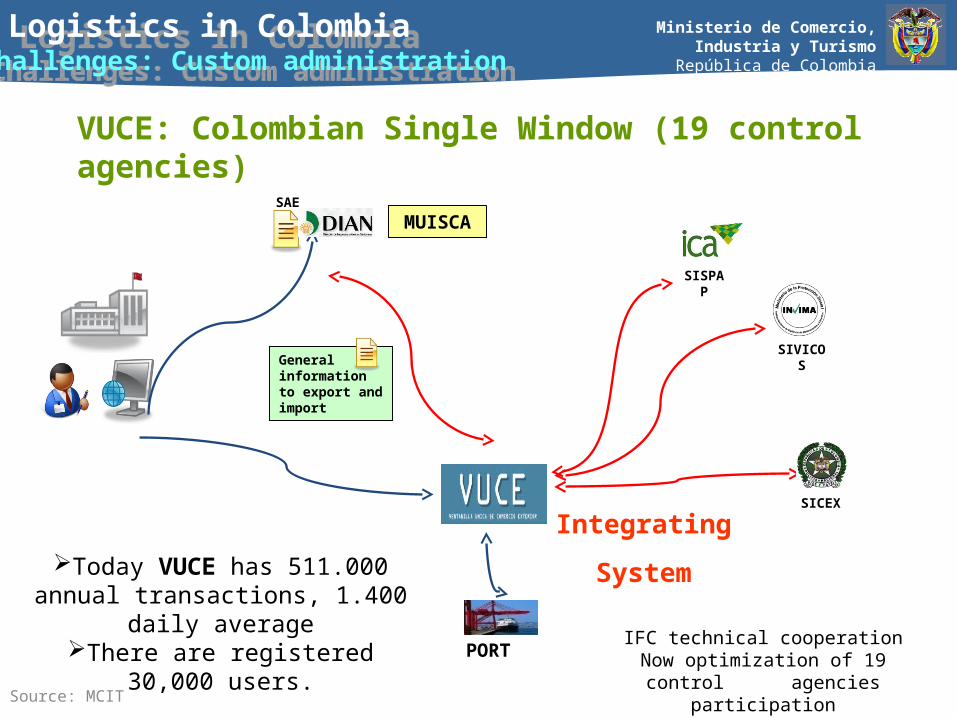

Source: MCIT

General information to export and import

MUISCASAE

PORT

SICEX

SISPAP

SIVICOS

Integrating

System

VUCE: Colombian Single Window (19 control agencies)

IV. Logistics in ColombiaB. Challenges: Custom administration

IV. Logistics in ColombiaB. Challenges: Custom administration

Today VUCE has 511.000 annual transactions, 1.400 daily average

There are registered 30,000 users.IFC technical cooperation

Now optimization of 19 control agencies participation

Ministerio de Comercio, Industria y TurismoRepública de Colombia

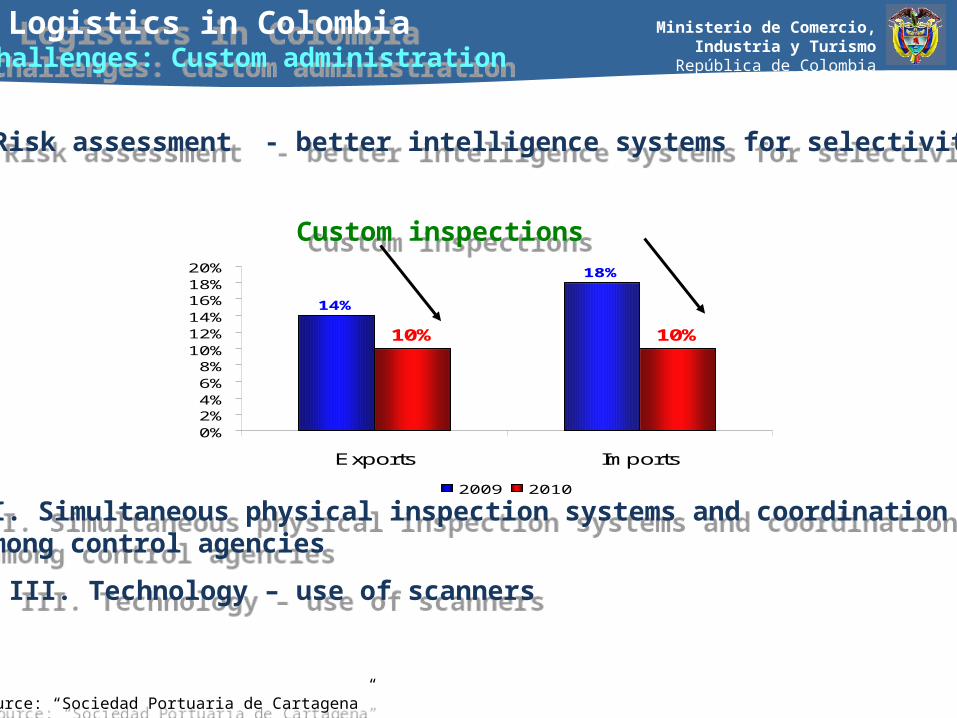

14%

18%

10% 10%

0%2%4%6%8%

10%12%14%16%18%20%

Exports Imports

2009 2010

Custom inspectionsCustom inspections

Source: “Sociedad Portuaria de Cartagena”Source: “Sociedad Portuaria de Cartagena”

IV. Logistics in ColombiaB. Challenges: Custom administration

IV. Logistics in ColombiaB. Challenges: Custom administration

I. Risk assessment - better intelligence systems for selectivity (WB)I. Risk assessment - better intelligence systems for selectivity (WB)

II. Simultaneous physical inspection systems and coordination among control agencies

II. Simultaneous physical inspection systems and coordination among control agencies

III. Technology – use of scannersIII. Technology – use of scanners

Ministerio de Comercio, Industria y TurismoRepública de Colombia

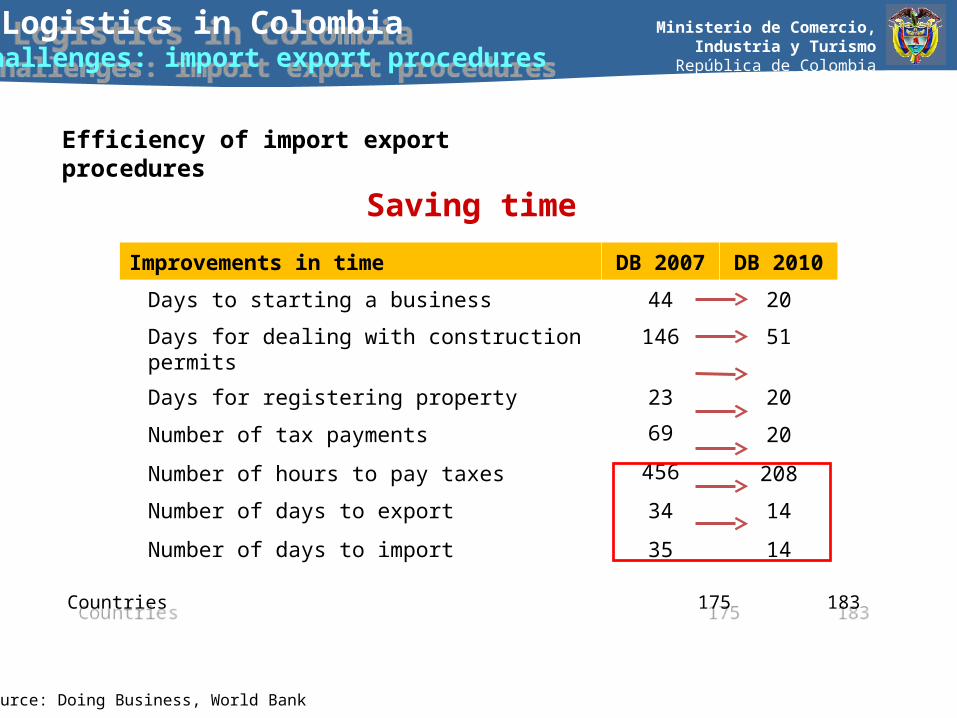

Saving time

Source: Doing Business, World Bank

Improvements in time DB 2007 DB 2010

Days to starting a business 44 20

Days for dealing with construction permits 146 51

Days for registering property 23 20

Number of tax payments 69 20

Number of hours to pay taxes 456 208

Number of days to export 34 14

Number of days to import 35 14

Efficiency of import export procedures

Countries 175 183 Countries 175 183

IV. Logistics in ColombiaB. Challenges: import export procedures

IV. Logistics in ColombiaB. Challenges: import export procedures

Ministerio de Comercio, Industria y TurismoRepública de ColombiaIV. Logistics in ColombiaIV. Logistics in Colombia

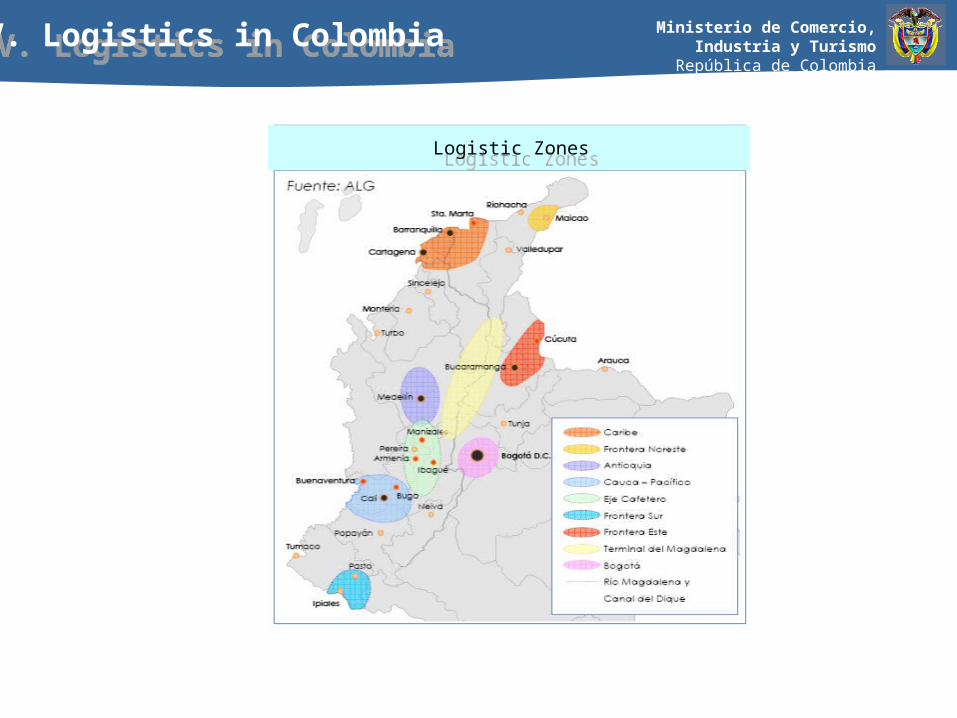

Logistic ZonesLogistic Zones

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Logistics Corridors PlanLogistics Corridors Plan

Source: DNPSource: DNP

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Logistics Platform PlanLogistics Platform Plan

Source: DNPSource: DNP

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

Ministerio de Comercio, Industria y TurismoRepública de Colombia

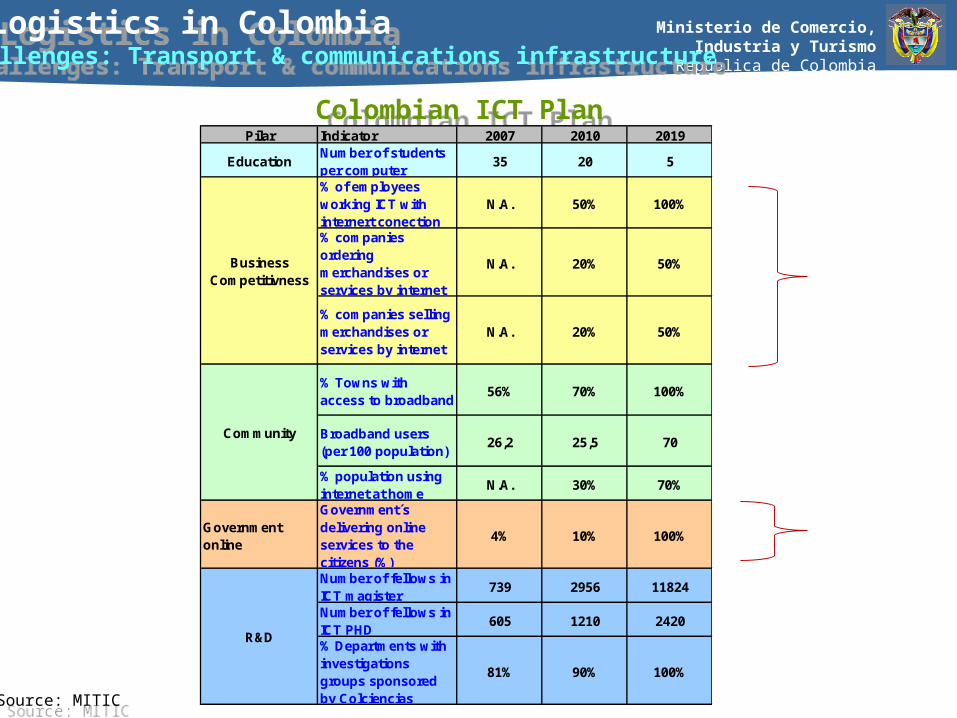

Colombian ICT PlanColombian ICT Plan

Source: MITICSource: MITIC

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

IV. Logistics in ColombiaB. Challenges: Transport & communications infrastructure

Pilar Indicator 2007 2010 2019

EducationNumber of students per computer

35 20 5

% of employees working ICT with internert conection

N.A. 50% 100%

% companies ordering merchandises or services by internet

N.A. 20% 50%

% companies selling merchandises or services by internet

N.A. 20% 50%

% Towns with access to broadband

56% 70% 100%

Broadband users (per 100 population)

26,2 25,5 70

% population using internet at home

N.A. 30% 70%

Government online

Government´s delivering online services to the citizens (%)

4% 10% 100%

Number of fellows in ICT magister

739 2956 11824

Number of fellows in ICT PHD

605 1210 2420

% Departments with investigations groups sponsored by Colciencias

81% 90% 100%

Business Competitivness

Community

R&D

Ministerio de Comercio, Industria y TurismoRepública de Colombia

Closing remarks

- Colombia has managed dramatic economic and social changes in the last few years, is committed to its effective insertion into the World economy and to the creation of a better business environment

- Trade Policy and advances in Logistics are complementary and necessary for competitiveness

- Logistics dimensions are varied and require substantial interagency work

- In the case of Colombia, Logistics and Trade Facilitation are very much on the agenda of the country facing many challenges

- Advances requiere the commitment of both the private and the public sector

Ministerio de Comercio, Industria y TurismoRepública de Colombia

GABRIEL DUQUE MILDENBERGViceminister for Foreign Trade

June 7th, 2010

COLOMBIAN TRADE POLICY

AND LOGISTICS