23

Fiscal Policy , Poverty , and Income Inequality in Indonesia Ministry of Finance, Republic of Indonesia Fiscal Policy Agency August, 2014

Fiscal Policy, Poverty, and Income Inequality y y q yin Indonesia

Ministry of Finance, Republic of IndonesiaFiscal Policy Agency

August, 2014

Background

41,01 30%4045

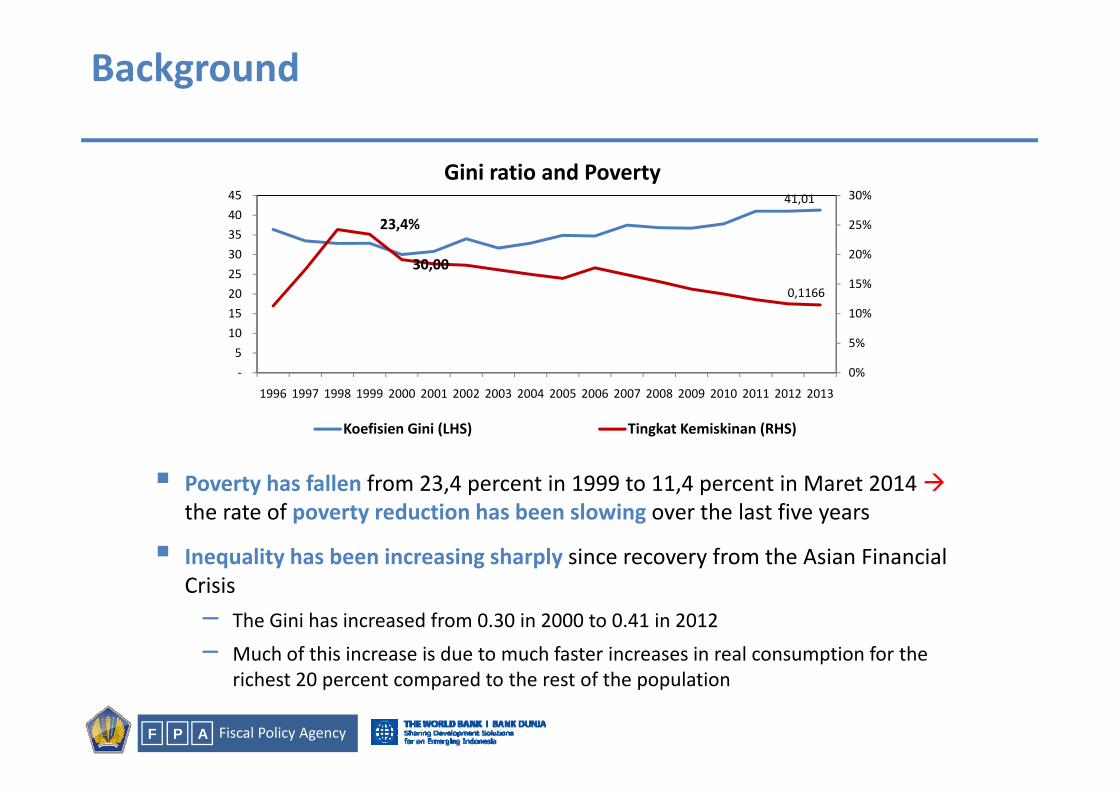

Gini ratio and Poverty

30,00

23,4%

0,116615%

20%

25%

20 25 30 35 40

0%

5%

10%

‐5 10 15

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Poverty has fallen from 23 4 percent in 1999 to 11 4 percent in Maret 2014

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Koefisien Gini (LHS) Tingkat Kemiskinan (RHS)

Poverty has fallen from 23,4 percent in 1999 to 11,4 percent in Maret 2014 the rate of poverty reduction has been slowing over the last five years

Inequality has been increasing sharply since recovery from the Asian Financial Crisis– The Gini has increased from 0.30 in 2000 to 0.41 in 2012

– Much of this increase is due to much faster increases in real consumption for the

Fiscal Policy AgencyP AF

richest 20 percent compared to the rest of the population

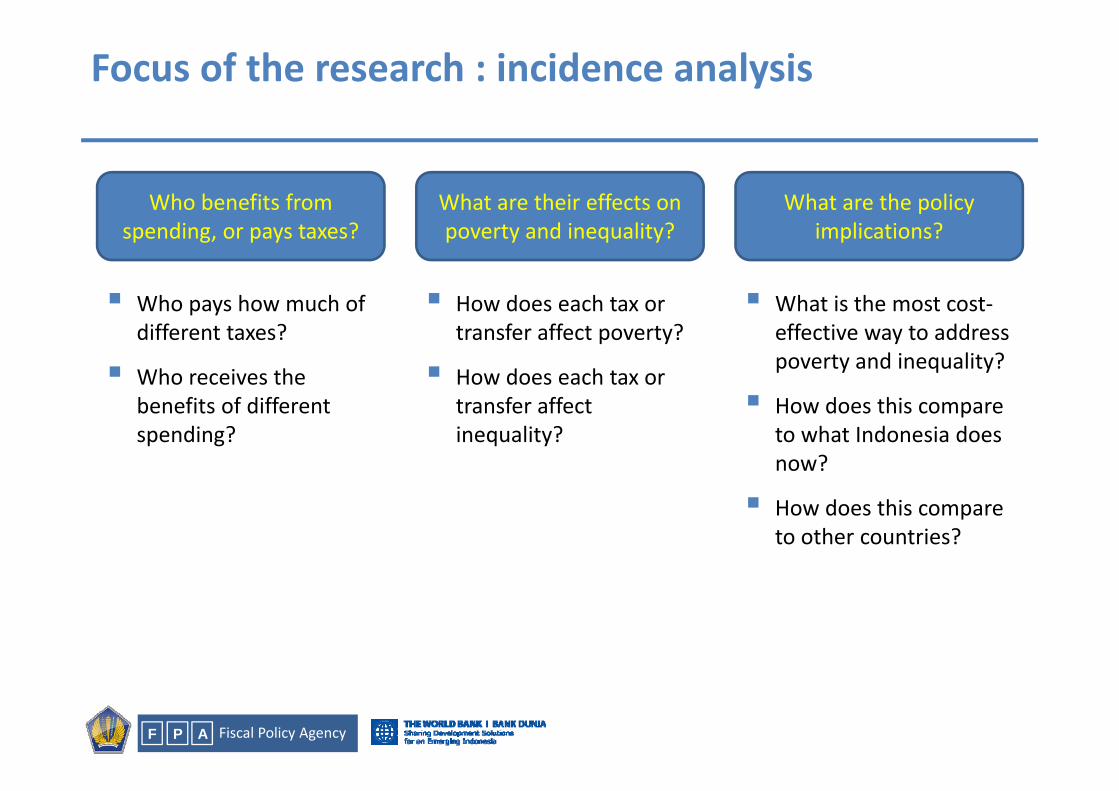

Focus of the research : incidence analysis

Who benefits from What are their effects on What are the policy spending, or pays taxes? poverty and inequality? implications?

Who pays how much of How does each tax or What is the most cost‐Who pays how much of different taxes?

Who receives the

How does each tax or transfer affect poverty?

How does each tax or

What is the most cost‐effective way to address poverty and inequality?

benefits of different spending?

transfer affect inequality?

How does this compare to what Indonesia does now?

How does this compare to other countries?

Fiscal Policy AgencyP AF

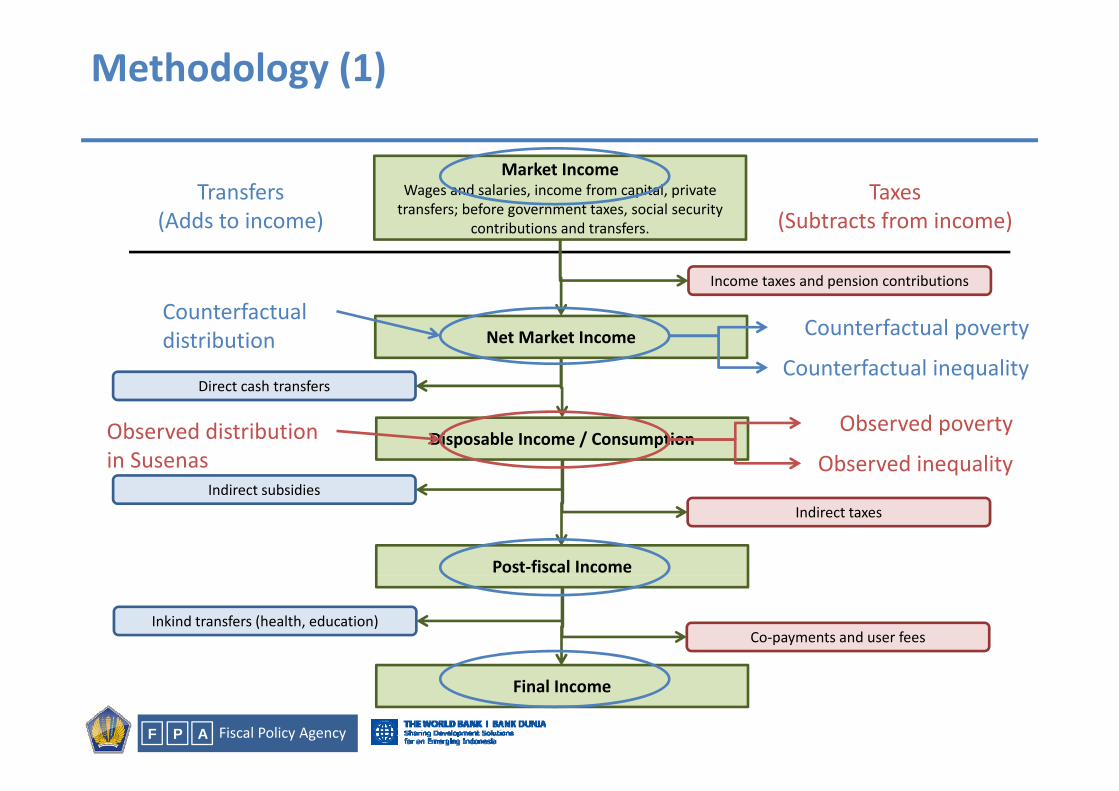

Methodology (1)

Market IncomeWages and salaries, income from capital, private transfers; before government taxes, social security

Transfers(Add t i )

Taxes(S bt t f i )

Income taxes and pension contributions

; g , ycontributions and transfers.(Adds to income) (Subtracts from income)

C t f t lNet Market Income

Direct cash transfers

Counterfactual povertyCounterfactual distribution

Counterfactual inequality

Disposable Income / Consumption

I di b idi

Observed povertyObserved distribution in Susenas Observed inequality

Post‐fiscal Income

Indirect taxesIndirect subsidies

Co‐payments and user feesInkind transfers (health, education)

Fiscal Policy AgencyP AF

Final Income

Methodology (2) : data

We use 2012 fiscal data on different revenues and expenditures– Central and district government

– Broken down by component

We apply standard incidence analysis to these different revenues and expendituresWe apply standard incidence analysis to these different revenues and expenditures– Which households pay how much of each tax?

– Which households receive how much of each transfer or expenditure?

We use 2012 Susenas to allocate these taxes and spending– For each household we know their total consumption (and consumption decile), what

items they consume, and their health and education usagey , g

– For each consumption decile, we determine how much of each tax it is paying

– For each consumption decile, we determine how much of each expenditure it is receivingreceiving

Fiscal Policy AgencyP AF

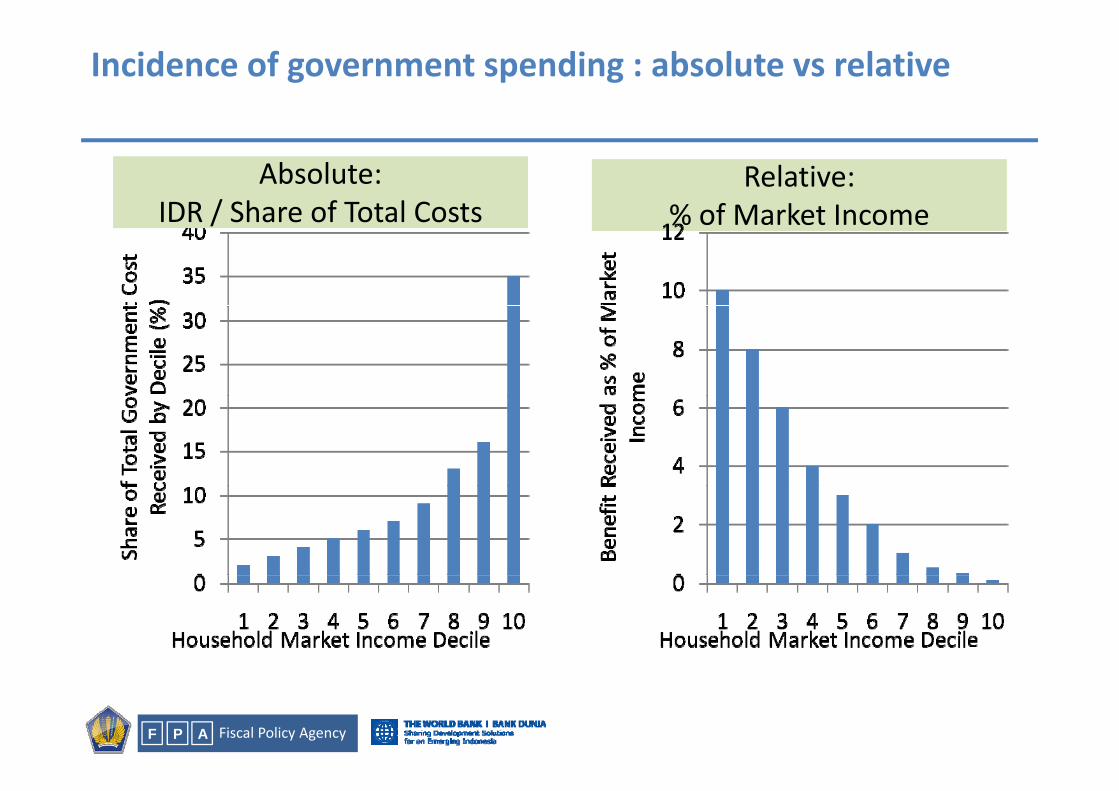

Incidence of government spending : absolute vs relative

Absolute:IDR / Share of Total Costs

Relative:% of Market IncomeIDR / Share of Total Costs % of Market Income

Fiscal Policy AgencyP AF

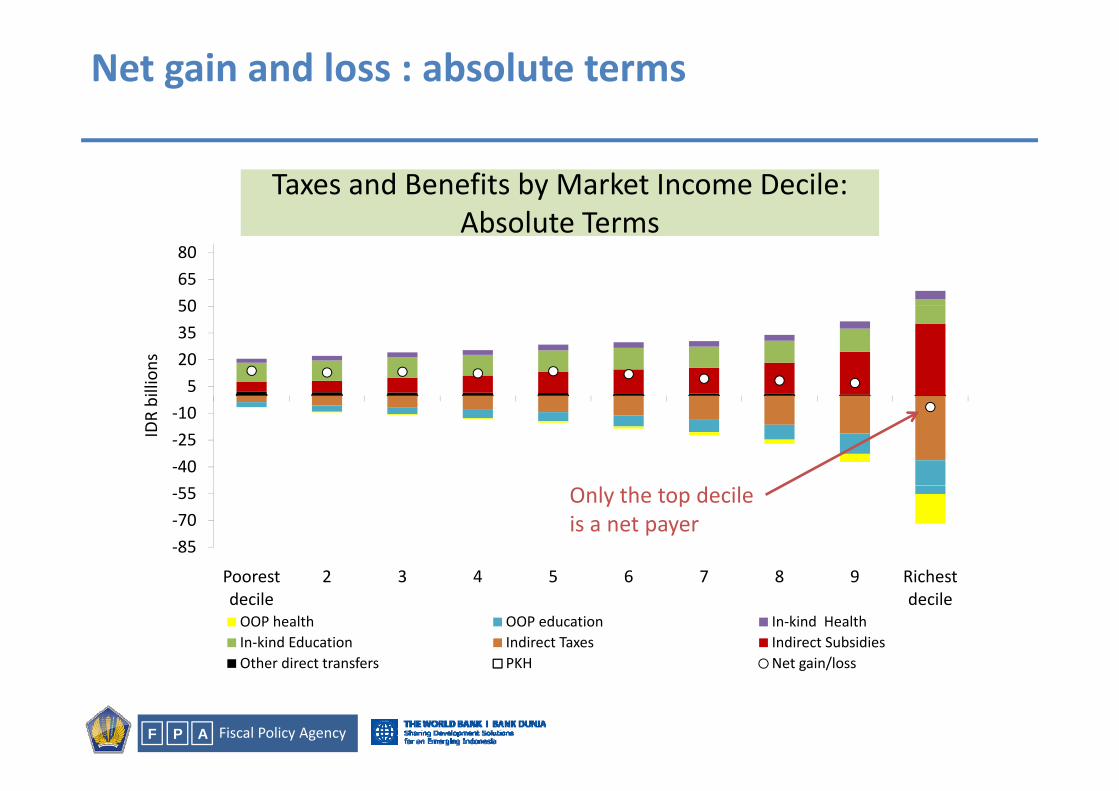

Net gain and loss : absolute terms

Taxes and Benefits by Market Income Decile:Ab l t T

506580

Absolute Terms

5203550

illions

‐40‐25‐10

IDR bi

‐85‐70‐55

Poorest 2 3 4 5 6 7 8 9 Richest

Only the top decile is a net payer

Poorest decile

2 3 4 5 6 7 8 9 Richest decile

OOP health OOP education In‐kind HealthIn‐kind Education Indirect Taxes Indirect SubsidiesOther direct transfers PKH Net gain/loss

Fiscal Policy AgencyP AF

Other direct transfers PKH Net gain/loss

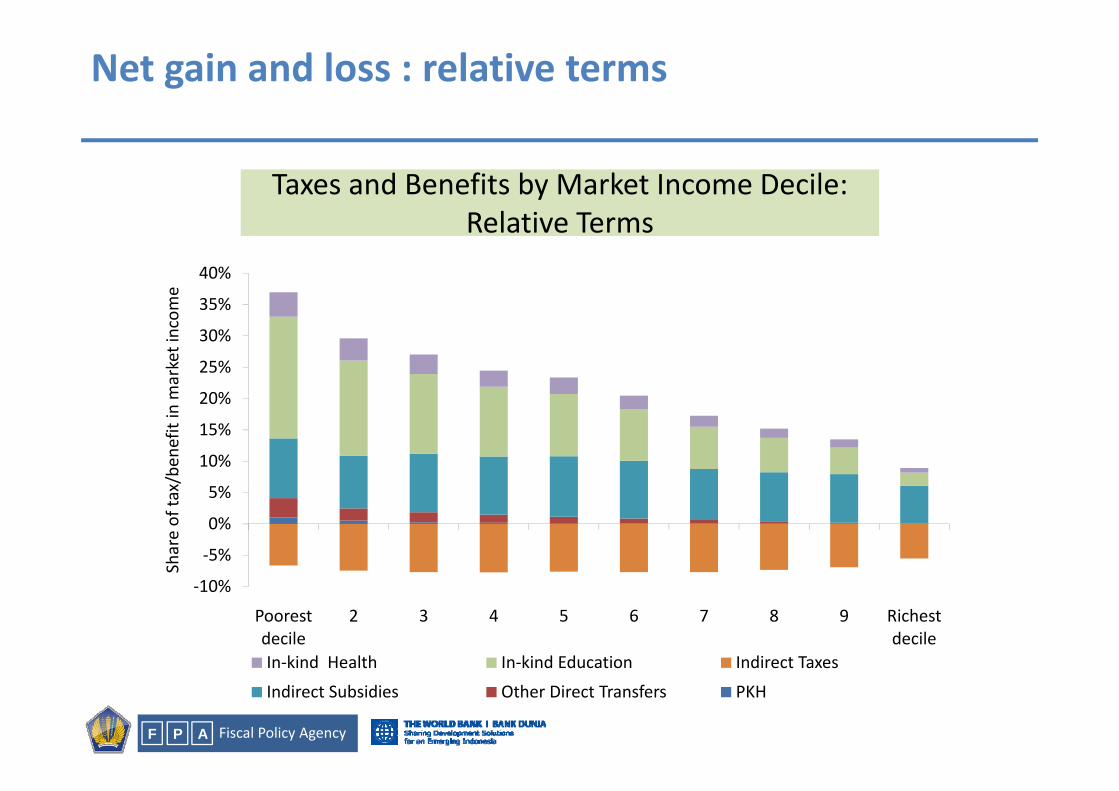

Net gain and loss : relative terms

Taxes and Benefits by Market Income Decile:R l ti T

35%

40%

me

Relative Terms

20%

25%

30%

35%

market incom

10%

15%

20%

x/be

nefit in

m

‐5%

0%

5%

Share of ta

x

‐10%

Poorest decile

2 3 4 5 6 7 8 9 Richest decile

In‐kind Health In‐kind Education Indirect Taxes

Fiscal Policy AgencyP AF

In kind Health In kind Education Indirect Taxes

Indirect Subsidies Other Direct Transfers PKH

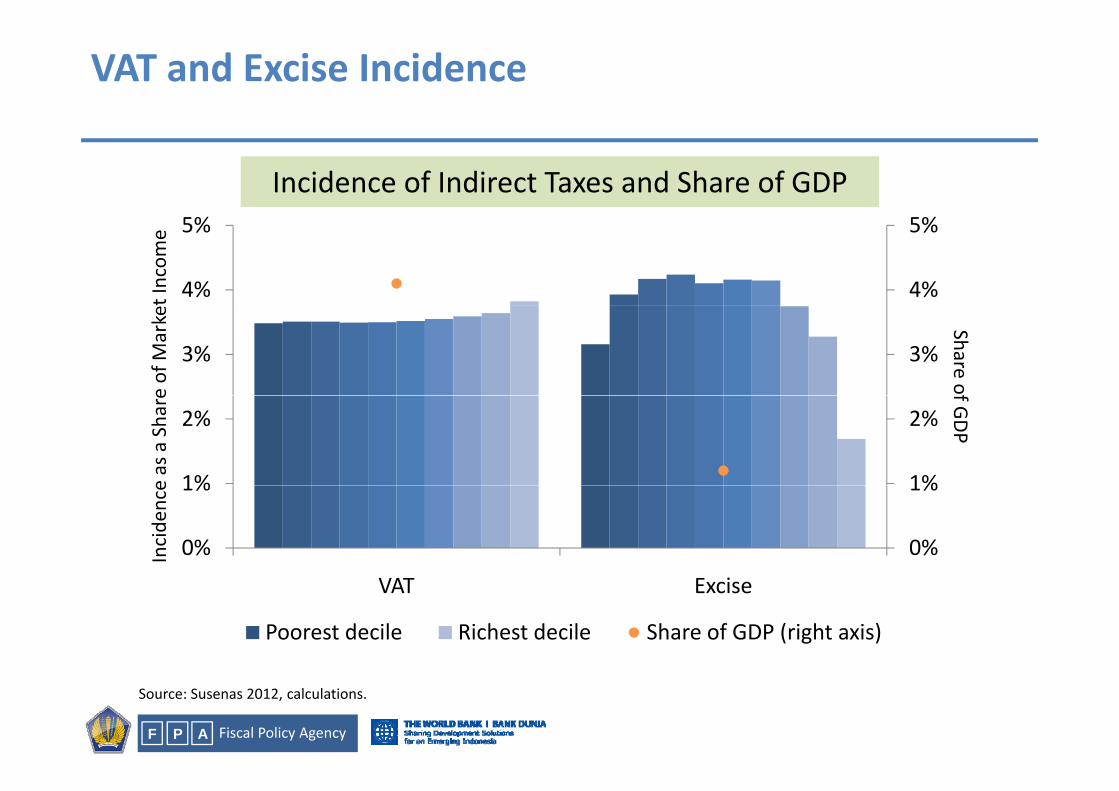

VAT and Excise Incidence

Incidence of Indirect Taxes and Share of GDP

4%

5%

4%

5%

t Incom

e

3%3%

Share ofe of M

arke

1%

2%

1%

2%

f GDP

e as a Share

0%

1%

0%

1%

Incide

nce

VAT Excise

Poorest decile Richest decile Share of GDP (right axis)

Fiscal Policy AgencyP AF

Source: Susenas 2012, calculations.

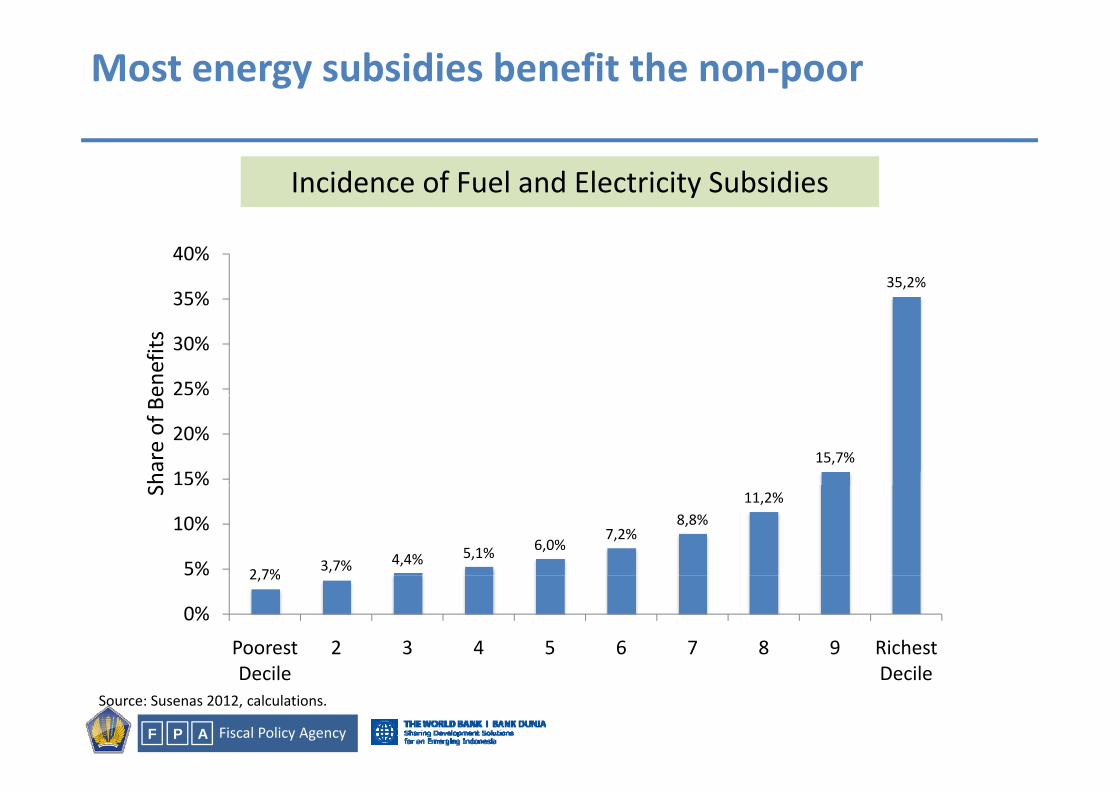

Most energy subsidies benefit the non‐poor

Incidence of Fuel and Electricity Subsidies

35,2%35%

40%

25%

30%

enefits

15,7%15%

20%

hare of B

e

2 7% 3,7% 4,4% 5,1% 6,0%7,2%

8,8%11,2%

5%

10%

%S

2,7%

0%

5%

Poorest 2 3 4 5 6 7 8 9 Richest

Fiscal Policy AgencyP AF

Decile DecileSource: Susenas 2012, calculations.

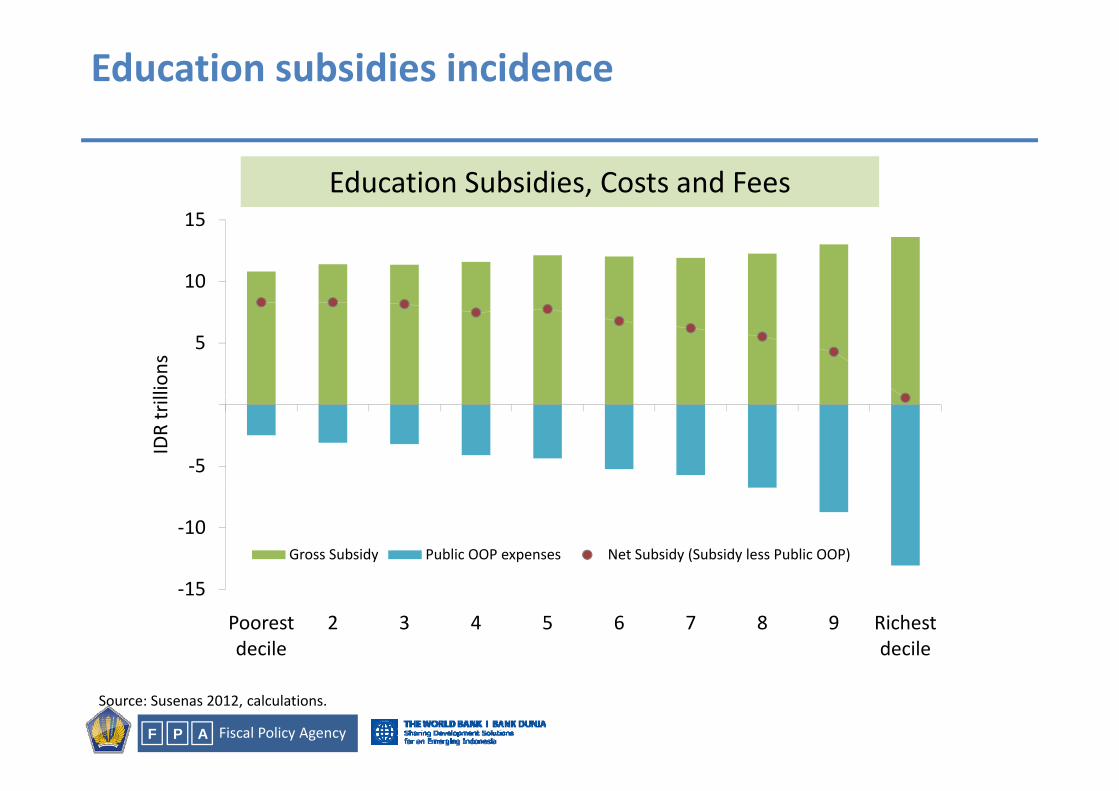

Education subsidies incidence

Education Subsidies, Costs and Fees15

10

15

5

lions

‐5

IDR tril

‐10Gross Subsidy Public OOP expenses Net Subsidy (Subsidy less Public OOP)

‐15

Poorest decile

2 3 4 5 6 7 8 9 Richest decile

Fiscal Policy AgencyP AF

Source: Susenas 2012, calculations.

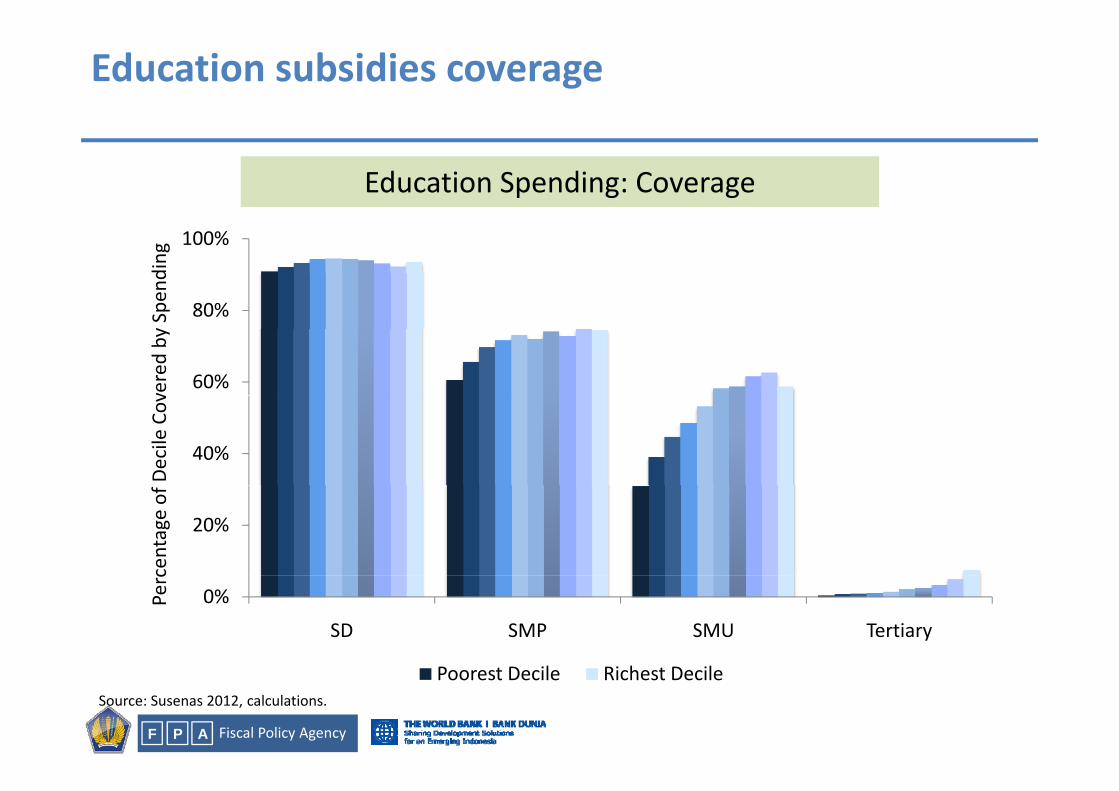

Education subsidies coverage

Education Spending: Coverage

80%

100%

pend

ing

60%

80%

vered by Sp

40%

Decile Cov

20%

centage of

0%

SD SMP SMU Tertiary

Perc

Fiscal Policy AgencyP AF

Poorest Decile Richest DecileSource: Susenas 2012, calculations.

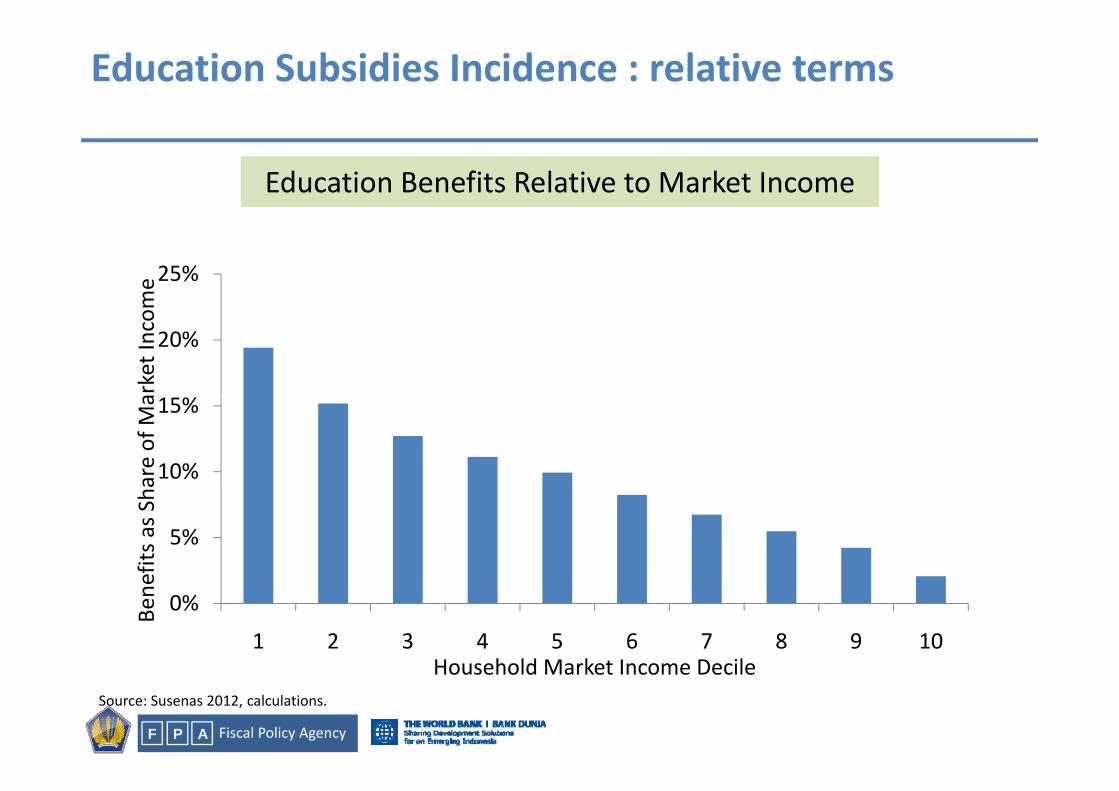

Education Subsidies Incidence : relative terms

Education Benefits Relative to Market Income

25%

me

20%

rket Incom

10%

15%

are of M

a

5%

efits as S

ha

0%

1 2 3 4 5 6 7 8 9 10

Bene

Household Market Income Decile

Fiscal Policy AgencyP AF

Household Market Income DecileSource: Susenas 2012, calculations.

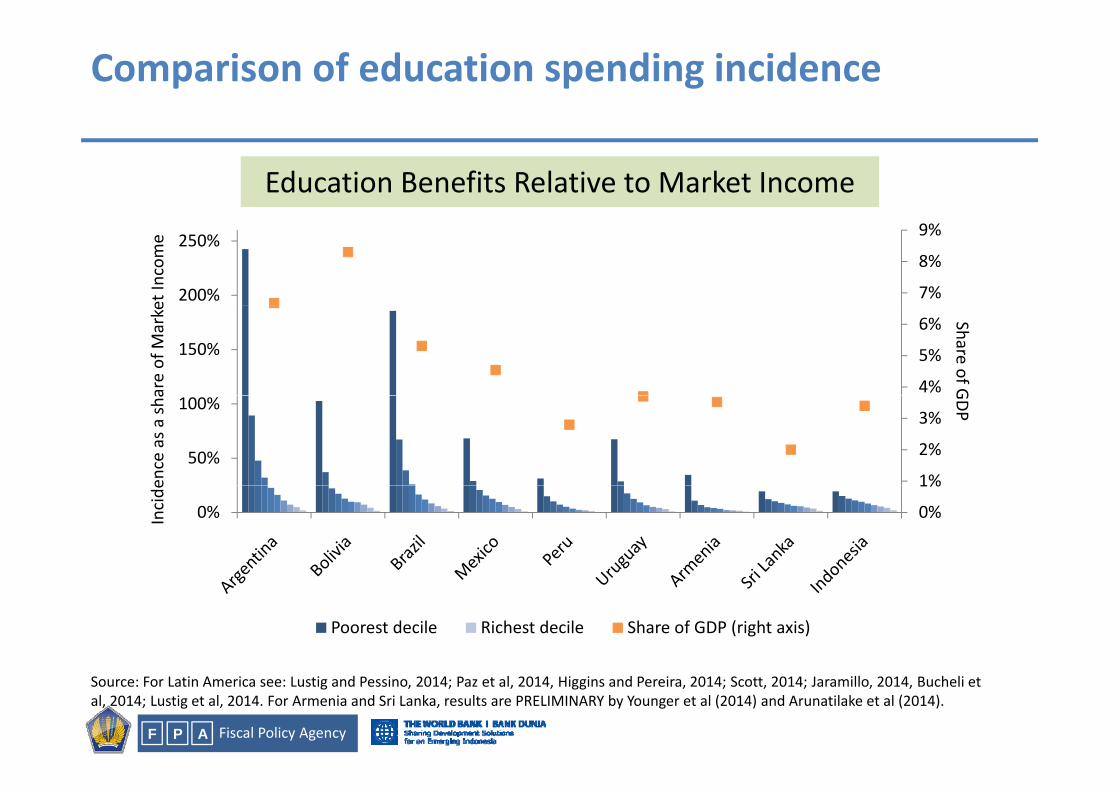

Comparison of education spending incidence

Education Benefits Relative to Market Income

7%

8%

9%

200%

250%

et Income

4%

5%

6%150%

Share of Gare of M

arke

1%

2%

3%

50%

100%

GDP

ence as a

sha

0%

1%

0%Incide

Poorest decile Richest decile Share of GDP (right axis)

Fiscal Policy AgencyP AF

Source: For Latin America see: Lustig and Pessino, 2014; Paz et al, 2014, Higgins and Pereira, 2014; Scott, 2014; Jaramillo, 2014, Bucheli et al, 2014; Lustig et al, 2014. For Armenia and Sri Lanka, results are PRELIMINARY by Younger et al (2014) and Arunatilake et al (2014).

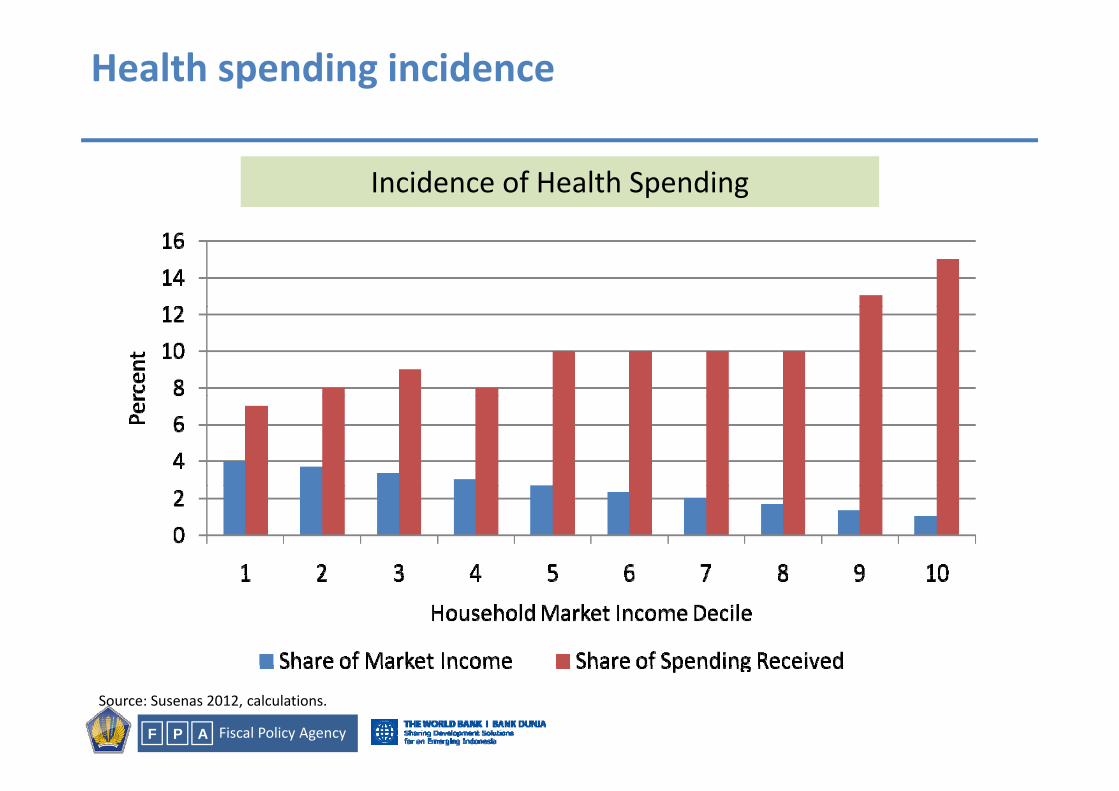

Health spending incidence

Incidence of Health Spending

Fiscal Policy AgencyP AF

Source: Susenas 2012, calculations.

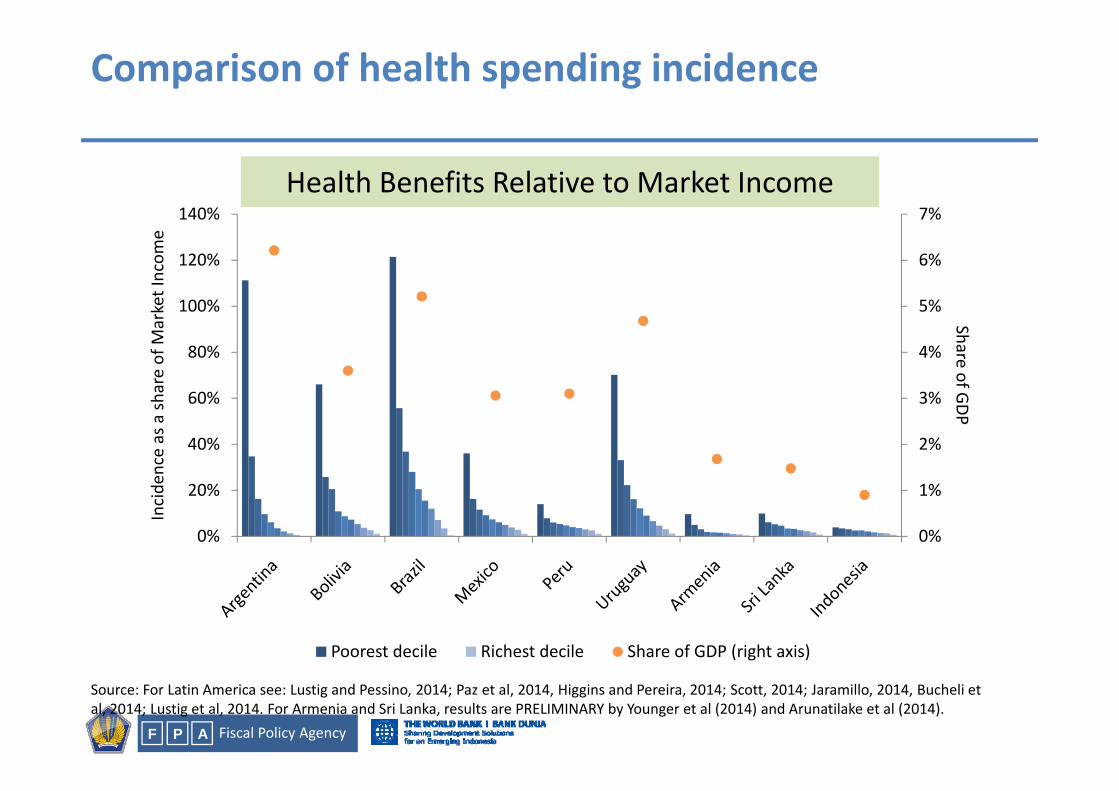

Comparison of health spending incidence

Health Benefits Relative to Market Income7%140%

5%

6%

7%

100%

120%

140%

ket Incom

e

3%

4%

5%

60%

80%

100%

Share of Ghare of M

ark

1%

2%

3%

20%

40%

60% GDP

ence as a

sh

0%

1%

0%

20%

Incid

Poorest decile Richest decile Share of GDP (right axis)

Fiscal Policy AgencyP AF

Source: For Latin America see: Lustig and Pessino, 2014; Paz et al, 2014, Higgins and Pereira, 2014; Scott, 2014; Jaramillo, 2014, Bucheli et al, 2014; Lustig et al, 2014. For Armenia and Sri Lanka, results are PRELIMINARY by Younger et al (2014) and Arunatilake et al (2014).

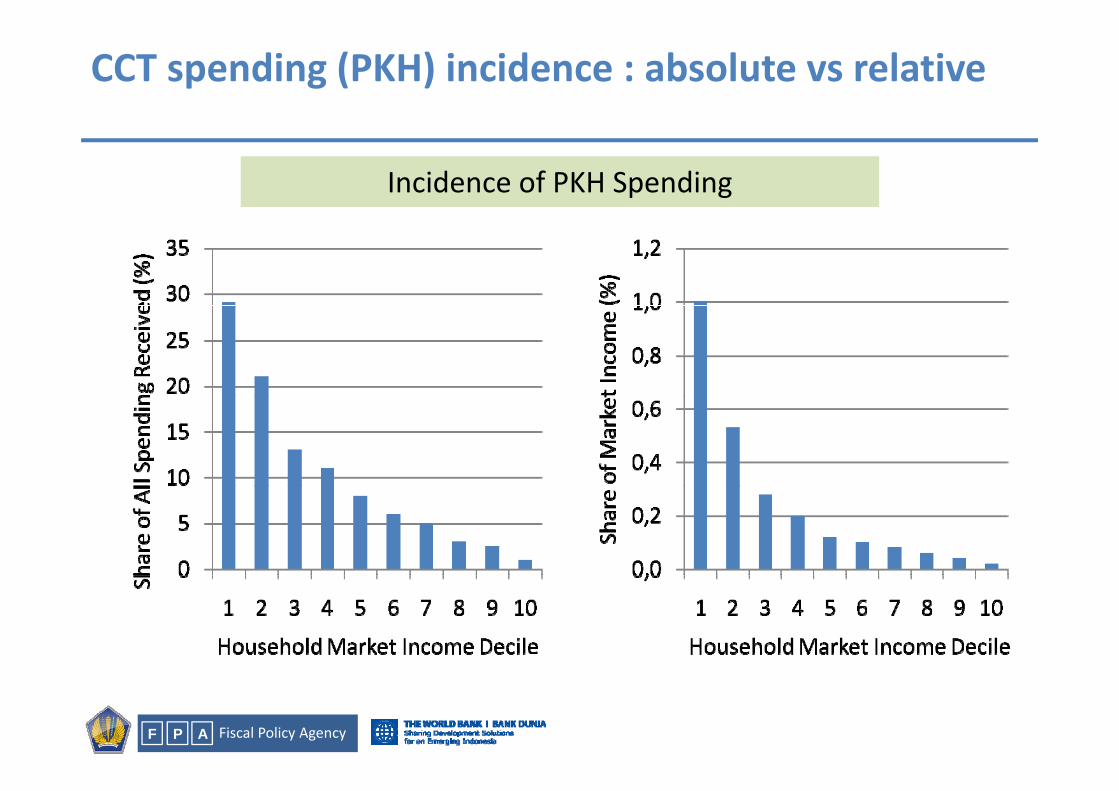

CCT spending (PKH) incidence : absolute vs relative

Incidence of PKH Spending

Fiscal Policy AgencyP AF

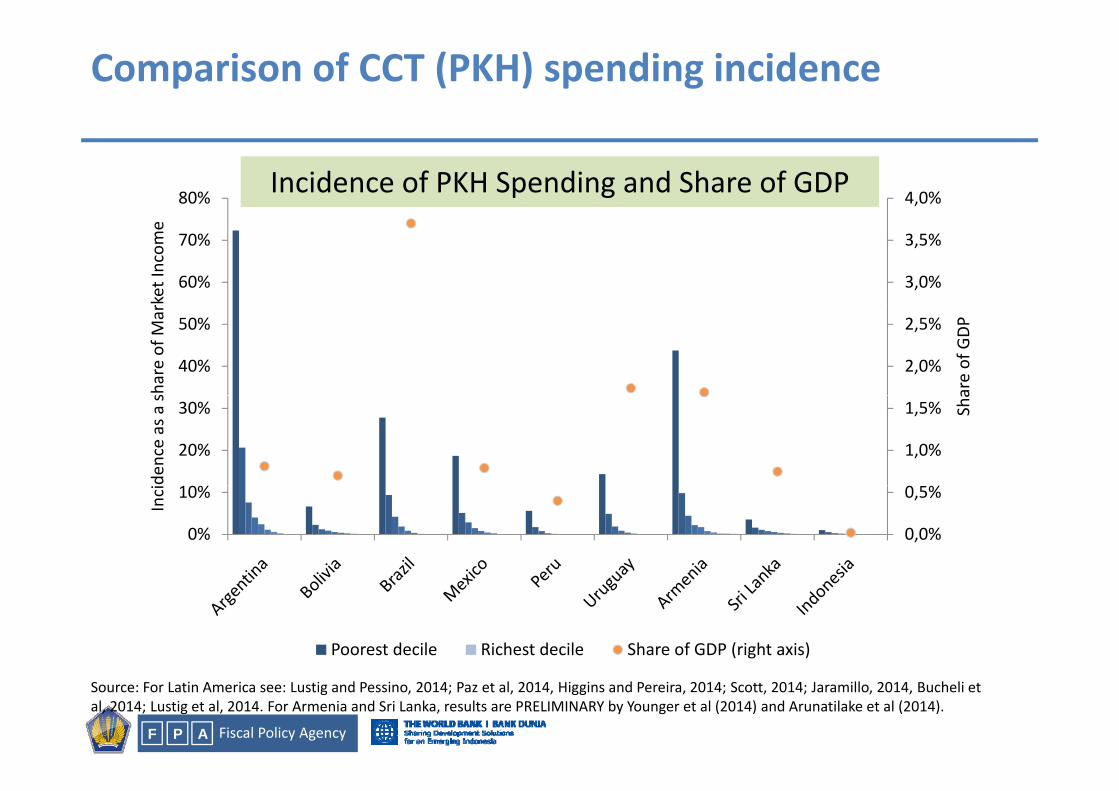

Comparison of CCT (PKH) spending incidence

Incidence of PKH Spending and Share of GDP 4,0%80%

3,0%

3,5%

60%

70%

rket Income

2,0%

2,5%

40%

50%

are of GDP

share of M

ar

1,0%

1,5%

20%

30% Sha

dence as a s

0,0%

0,5%

0%

10%

Inci

Poorest decile Richest decile Share of GDP (right axis)

Fiscal Policy AgencyP AF

Source: For Latin America see: Lustig and Pessino, 2014; Paz et al, 2014, Higgins and Pereira, 2014; Scott, 2014; Jaramillo, 2014, Bucheli et al, 2014; Lustig et al, 2014. For Armenia and Sri Lanka, results are PRELIMINARY by Younger et al (2014) and Arunatilake et al (2014).

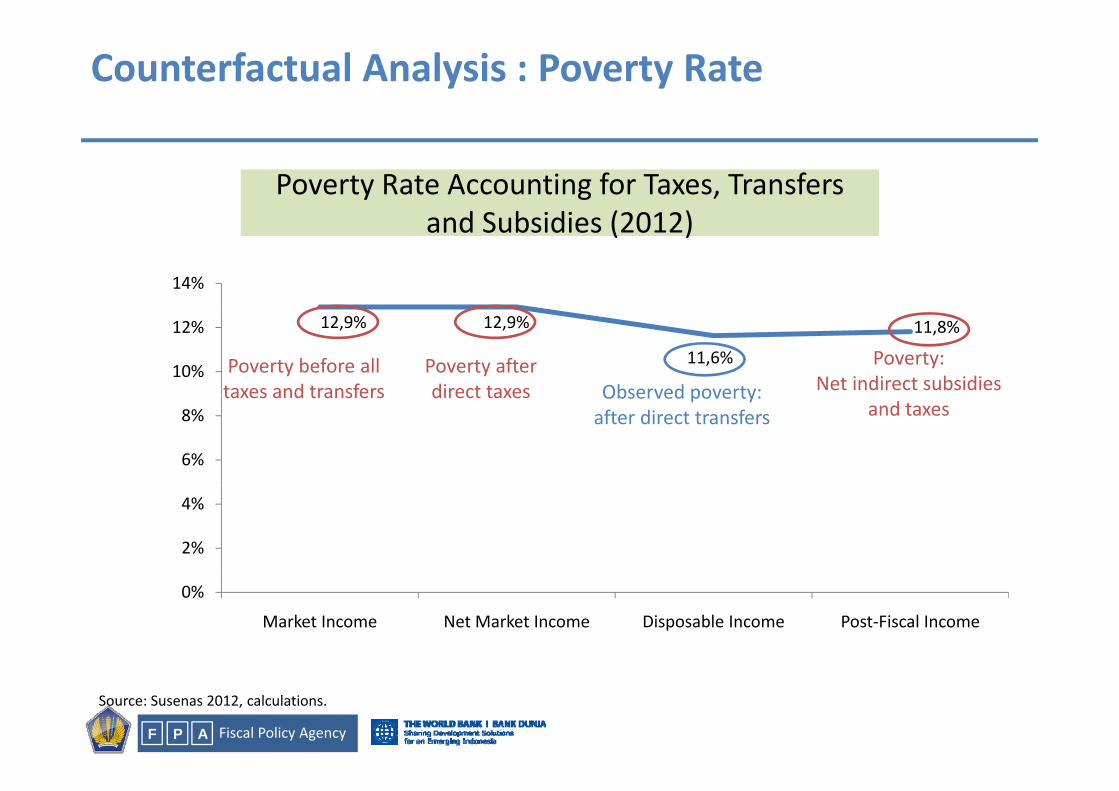

Counterfactual Analysis : Poverty Rate

Poverty Rate Accounting for Taxes, Transfers d S b idi (2012)and Subsidies (2012)

14%

12,9% 12,9%

11,6%

11,8%

10%

12%

Observed poverty:Poverty after direct taxes

Poverty before all taxes and transfers

Poverty:Net indirect subsidies

6%

8%Observed poverty:after direct transfers

direct taxestaxes and transfersand taxes

2%

4%

0%

Market Income Net Market Income Disposable Income Post‐Fiscal Income

Fiscal Policy AgencyP AF

Source: Susenas 2012, calculations.

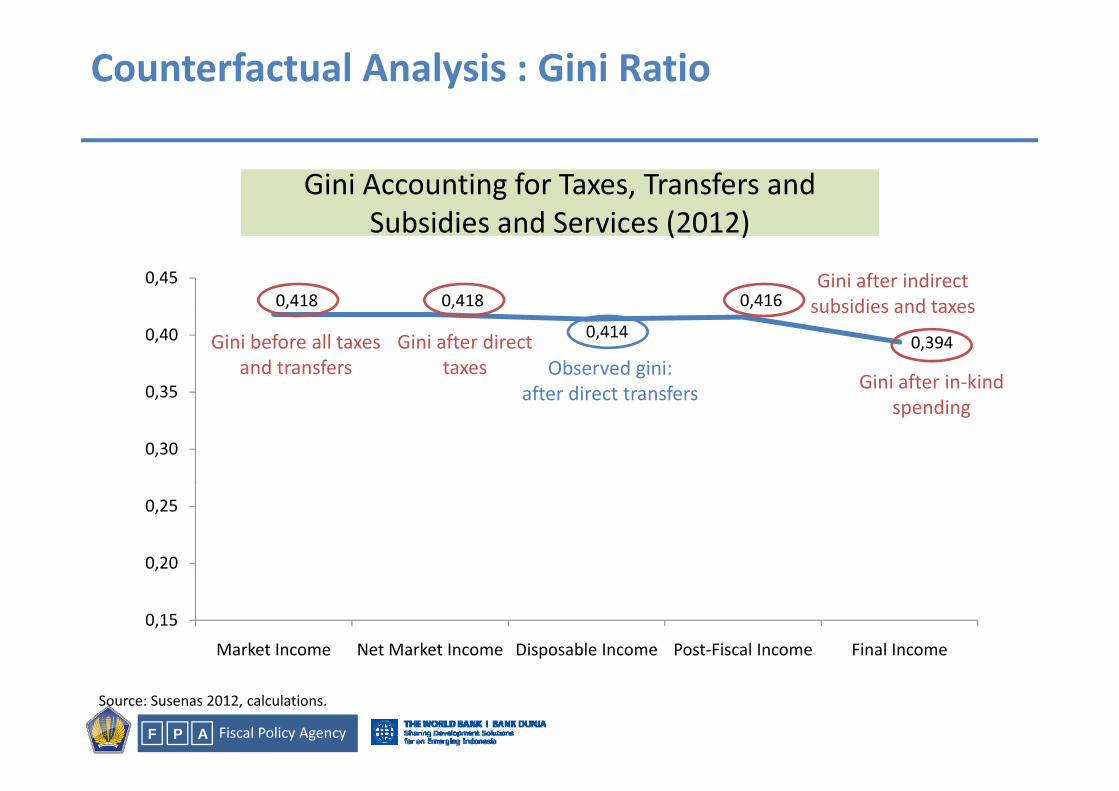

Counterfactual Analysis : Gini Ratio

Gini Accounting for Taxes, Transfers and S b idi d S i (2012)

0,418 0,418 0,4160,45

Subsidies and Services (2012)

Gini after indirect subsidies and taxes0,418 0,418

0,414

0,416

0,394

0,35

0,40

Observed gini:after direct transfers

Gini after direct taxes

Gini before all taxes and transfers

subsidies and taxes

Gini after in‐kind

0,30

0,35 after direct transfersspending

0,20

0,25

0,15

Market Income Net Market Income Disposable Income Post‐Fiscal Income Final Income

Fiscal Policy AgencyP AF

Source: Susenas 2012, calculations.

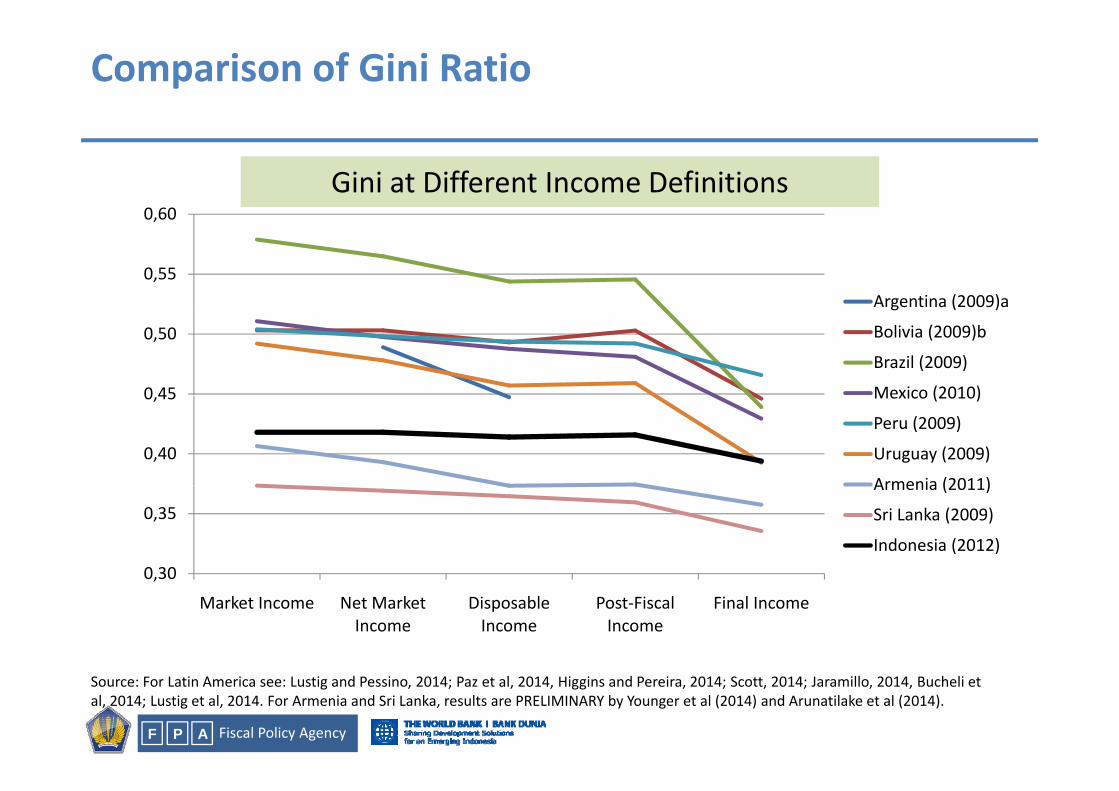

Comparison of Gini Ratio

Gini at Different Income Definitions0 60

0,55

0,60

Argentina (2009)a

0 45

0,50

Argentina (2009)a

Bolivia (2009)b

Brazil (2009)

Mexico (2010)

0,40

0,45 Mexico (2010)

Peru (2009)

Uruguay (2009)

Armenia (2011)

0 30

0,35

Armenia (2011)

Sri Lanka (2009)

Indonesia (2012)0,30

Market Income Net Market Income

Disposable Income

Post‐Fiscal Income

Final Income

Fiscal Policy AgencyP AF

Source: For Latin America see: Lustig and Pessino, 2014; Paz et al, 2014, Higgins and Pereira, 2014; Scott, 2014; Jaramillo, 2014, Bucheli et al, 2014; Lustig et al, 2014. For Armenia and Sri Lanka, results are PRELIMINARY by Younger et al (2014) and Arunatilake et al (2014).

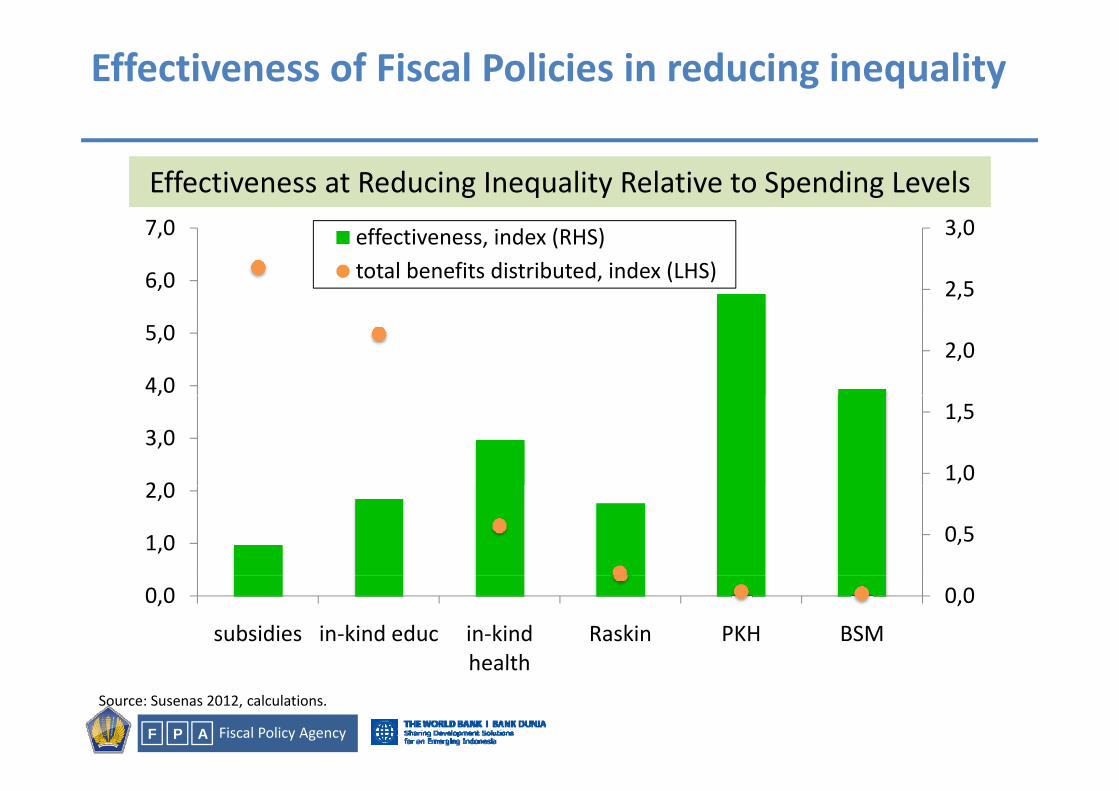

Effectiveness of Fiscal Policies in reducing inequality

Effectiveness at Reducing Inequality Relative to Spending Levels

2,5

3,0

6,0

7,0 effectiveness, index (RHS)total benefits distributed, index (LHS)

2,04,0

5,0

1,0

1,5

2 0

3,0

,

0,51,0

2,0

0,00,0

subsidies in‐kind educ in‐kind health

Raskin PKH BSM

Fiscal Policy AgencyP AF

healthSource: Susenas 2012, calculations.

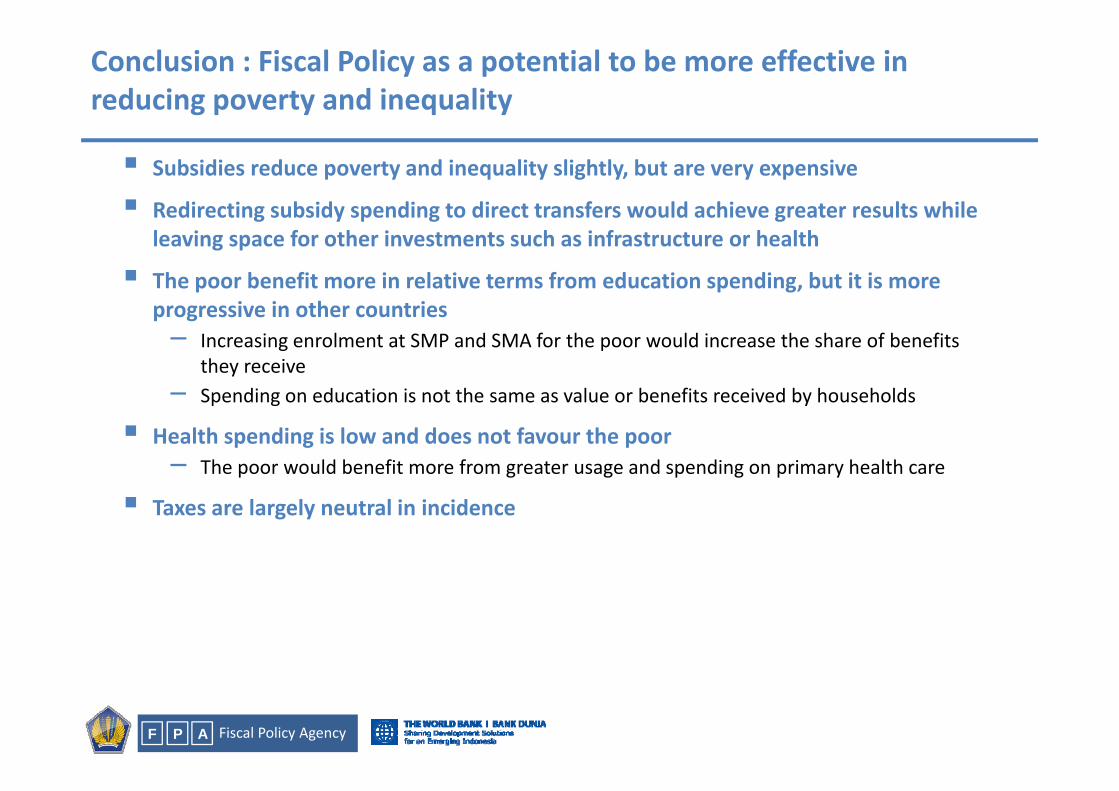

Conclusion : Fiscal Policy as a potential to be more effective in reducing poverty and inequality

Subsidies reduce poverty and inequality slightly, but are very expensive

Redirecting subsidy spending to direct transfers would achieve greater results whileRedirecting subsidy spending to direct transfers would achieve greater results while leaving space for other investments such as infrastructure or health

The poor benefit more in relative terms from education spending, but it is more progressive in other countriesprogressive in other countries– Increasing enrolment at SMP and SMA for the poor would increase the share of benefits

they receive– Spending on education is not the same as value or benefits received by householdsSpending on education is not the same as value or benefits received by households

Health spending is low and does not favour the poor– The poor would benefit more from greater usage and spending on primary health care

Taxes are largely neutral in incidence

Fiscal Policy AgencyP AF