Trade Operations Division Midwest Global Trade Association Educational Seminar Antidumping & Countervailing Duty (AD/CVD) November 21 st , 2014 DISCLAIMER: This material is intended to provide guidance. Recognizing that many complicated factors are involved in Customs and Border Protection matters, an importer may wish to obtain a binding ruling under 19 CFR Part 177. Reliance solely on this information may not be considered reasonable care. Importers are referred to Treasury Decision 97-96, which was published in the Federal Register of December 4, 1997, and in the Customs Bulletin of December 17, 1997, for in-depth information on the concept of reasonable care. Import Specialists Minneapolis Area Service Port

Transcript

Trade Operations Division Midwest Global Trade Association Educational Seminar

DISCLAIMER: This material is intended to provide guidance. Recognizing that many complicated factors are involved in Customs and Border Protection matters, an importer may wish to obtain a binding ruling under 19 CFR Part 177. Reliance solely on this information may not be considered reasonable care. Importers are referred to Treasury Decision 97-96, which was published in the Federal Register of

December 4, 1997, and in the Customs Bulletin of December 17, 1997, for in-depth information on the concept of reasonable care.

Import Specialists

Minneapolis Area Service Port

Briefing Outline

AD/CVD Definitions

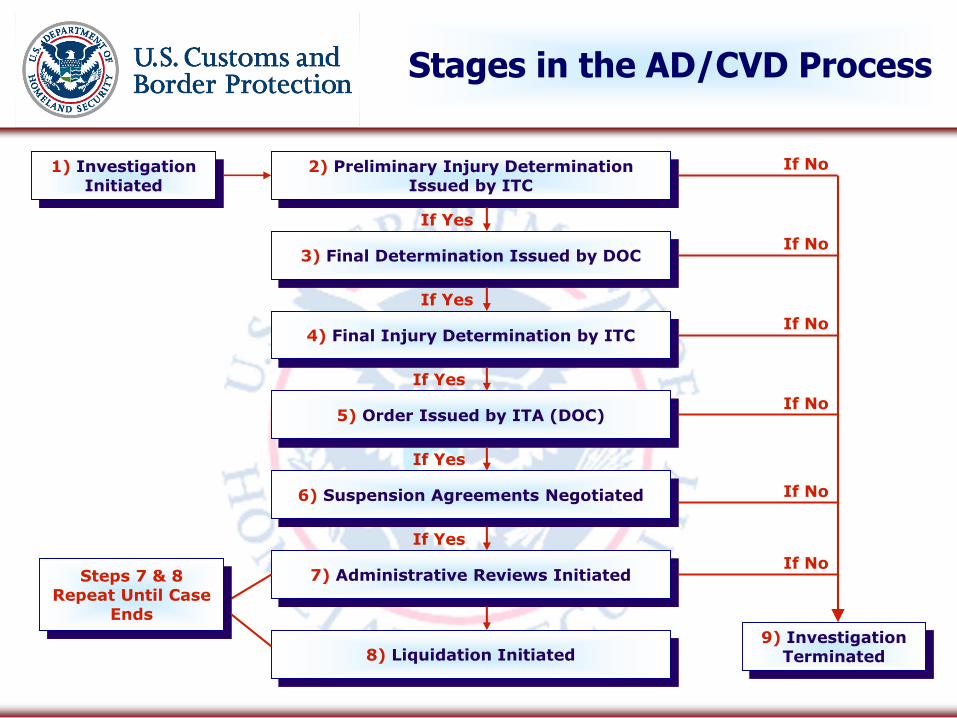

Stages in the AD/CVD Process

Retrospective AD/CVD System

Website Material for AD/CVD Program & Guidelines

CBP AD/CVD Process

Determining the AD/CVD Case Number & Rate

Scope Rulings

Certificates of Reimbursement

CBP AD/CVD Liquidation Process

Best Practices for AD/CVD Compliance

Import Specialist Division

Commodity Assignments & Contact Information

AD/CVD Definitions

A supplemental duty or subsidy assessed on imported merchandise subject to either an anti-dumping duty (AD) or a countervailing duty (CV) order.

Anti-Dumping

Dumping occurs when a foreign producer sells a product in the United States at a price that is below that producer’s sales price in its home market, or at a price that is lower than its cost of production.

Countervailing Duty

Subsidizing occurs when a foreign government provides financial assistance to benefit the production, manufacture, or exportation of a good.

Importers Pay Estimated AD/CVD Duties Upon Importation of Goods

The U.S. Department of Commerce, Upon Request, Conducts Reviews to Determine Final AD/CVD Liability

CBP Assesses Final AD/CVD Duties as Instructed by the U.S. Department of Commerce

Web Site Material AD/CVD Program & Guidelines

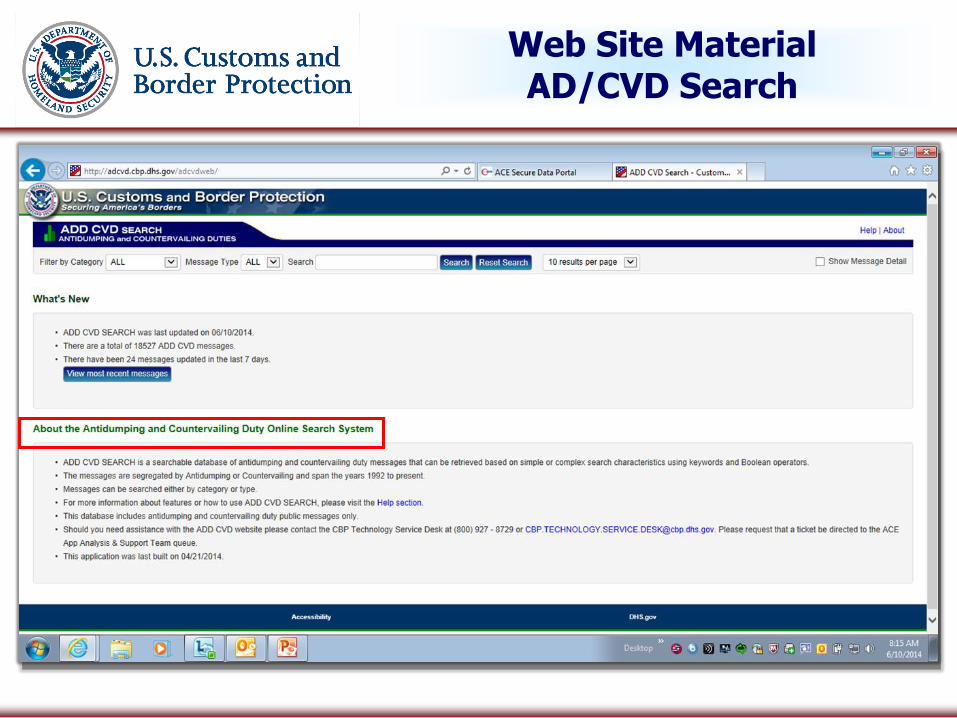

Web Site Material AD/CVD Search

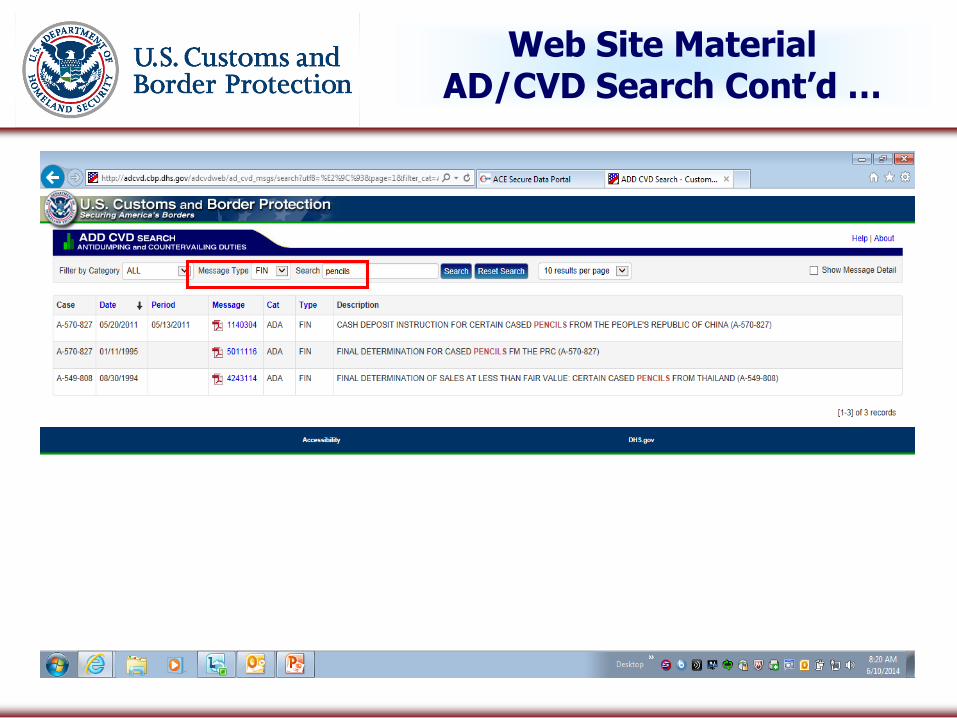

Web Site Material AD/CVD Search Cont’d …

Web Site Material AD/CVD Search Cont’d …

Web Site Material AD/CVD Search Cont’d …

Scope Description

Web Site Material AD/CVD Data - Active Cases

Web Site Material AD/CVD Data Active Cases Cont’d …

CBP AD/CVD Process

ABI System Alerts Filer to Possible AD/CVD for a Particular Tariff Number

Filer Queries ABI for the Particular Tariff Number & Country to Determine if an AD/CVD Case Exists

Tariff Numbers are Provided for Convenience Only … It’s Necessary to Consult the Actual Scope Description for the Particular Case

The ABI Query Should also Provide the Specific Case Numbers and the Applicable AD/CVD Deposit Rates

Determining the AD/CVD Case Number & Rate

Most AD/CVD Cases Follow this Hierarchy when Determining the Applicable Case Number & Rate:

1. If Exporter Has Its Own Rate – Use that Rate

2. If Exporter Does Not Have Its Own Rate, but the Manufacturer Has Its Own Rate – Use Manufacturer’s Rate

3. If Neither the Exporter or Manufacturer Has Its Own Rate – Use the “All Other” Rate

Case Numbers are Created as Follows:

1. First Character Designates Whether Antidumping (A) or Countervailing Duty (C)

2. Next Three Numbers are the Country Code

3. Next Three Numbers Identify the Particular Case

4. Last Three Digits Designate the Particular Exporter, Manufacturer, or even a Combination Thereof … For “All Others”, these Numbers will be Zeros

Determining the AD/CVD Case Number & Rate Cont’d …

A-570-827-004

Determining the AD/CVD Case Number & Rate Cont’d …

Possible to Have Both an AD Case and a CVD Case for a Given Commodity … an Example is Pasta

Some Exporters or Manufacturers are Excluded from a Particular AD/CVD Order … if Excluded, Type 01 Consumption Entries May be Filed

Some Exporters or Manufacturers have an Initial AD/CVD Deposit Rate of Zero … if Zero Deposit Rate, Type 03Consumption Entries Must Still be Filed, with Applicable AD/CVD Case Information

Remember the Initial Deposit Rate is an Estimate Only … the Final Rate Could Be Different

Scope Rulings

If There is any Doubt as to Whether Merchandise is Subject to an AD/CVD Case, an Importer Should Request a Scope Ruling from the Dept. of Commerce (DOC)

A Scope Ruling Must be Obtained Prior to Liquidation of the Entry

The Applicability of AD/CVD is Not a Protestable Issue with CBP under Sec. 514

Certificates of Reimbursement

DOC Regulations Require that the Importer File, Prior to Liquidation, a Certificate Advising Whether the Importer has Entered into an Agreement or has otherwise Received Reimbursement of the Antidumping Duties

The Certificate Must Be Signed by a Competent Officer of the Importer … a Broker May Not Sign the Certificate on Behalf of the Importer

A Certificate may be Created for each Entry, or a Blanket Certificate may be Used for a 12-month Period or the Administrative Review Period, Whichever is Longer

Certificates of Reimbursement Cont’d …

If the Importer Fails to Provide a Reimbursement Certificate Prior to Liquidation, CBP must Presume that Reimbursement has Occurred and the Antidumping Duties must be Doubled

CBP has been Instructed to No Longer Reject Entries or Issue Requests for the Submission of a Reimbursement Certificate

The Guidance for Certificates of Reimbursement may be Found on the CBP Website, including a Sample Blanket Certificate

In Most Cases, a Certificate of Reimbursement is Required Only for Antidumping Cases … Not for CVD

CBP AD/CVD Liquidation Process

CBP Must Suspend Liquidation of Entries until Liquidation Instructions are Issued by the DOC … Instructions will be Issued for a Particular Period of Review – Usually One Year

AD/CVD Assessed at Time of Liquidation May Differ Significantly from Initial Estimated Deposit Rate

Oftentimes, Liquidation Instructions for a Specific Exporter or Manufacturer Instruct CBP to Liquidate Only Those Entries Imported by a Specific Company at a Preferred Lower Rate ... the Instructions May Indicate that Entries with Other Importers of Record are to be Liquidated at the “All Other” Rate

For Entries having Several Different AD/CVD Cases, the Suspension of Liquidation Will Not be Lifted until Instructions have been Issued for the Last Case Number

CBP AD/CVD Liquidation Process Cont’d …

Interest is Attributed to All Increases and Refunds of AD/CVD if the Entries are Made On or After the Date of the Order (i.e. When the Cash Deposit Became Mandatory) … Prior to the Date of the Order, No Interest is Payable or Refundable

During the Bonding Period (Prior to the Order), a Separate Single Entry Bond (SEB) Must be Filed for Each Entry if the AD/CVD Deposit Rate is 5% or Greater

If the Rate is Less Than 5%, the Continuous Bond is Sufficient

If an SEB is Used for the Entry and the Rate is Less Than 5%, the Amount of AD/CVD Must be Taken Into Consideration When Calculating the Amount of the Entry SEB

Best Practices for AD/CVD Compliance

Use ACE

The Written Scope of the Order is Dispositive

Estimated AD/CVD Duties are Due on Imports Entered or Withdrawn from Warehouse, for Consumption On or After the Effective Date

Keep Up to Date on Which Exporters/Manufacturers are Applicable to Each Case Number and Cash Deposit Rate

Pay Close Attention to Supply Chains Involving Exporter-Specific Rates

Do Your Due Diligence on Your Suppliers

Be Prepared to Document Your Entry Data

Utilize PEAs, PSCs and Prior Disclosures

Import Specialist (IS) Assigned HTS Commodities

Minneapolis Port of Entry: One Commodity Team Comprised of Two “Sub-Team”/Focus Areas

Harmonized Tariff Schedule of the United States (HTSUS) Description/Sections/Chapters

[NOTE: The following areas of Chapter 98 are handled by the Entry Unit: American Goods Returned (9801.00.10 - 9801.00.90); Defense Articles (9808.00.10 - 9808.00.80; and TIB's (9812.00.20 – 9813.00.75)]

X X

Minneapolis IS Unit – Contact Information

Senior Import Specialist

Michael Carriere

612-348-1690 x166Focus Area 376

Senior Import Specialist

Jeremy Olson

612-348-1690 x129Focus Area 377

Import Specialist

Peter Conniff

612-348-1690 x128Focus Area 377

Supervisory Import Specialist

Kristi L. Johnson

612-348-1690 x146

Import Specialist

Bradley Clemence

612-348-1690 x148Focus Area 376

Import Specialist

Robert Burandt

612-348-1690 x121Focus Area 376

Import Specialist

Jason Fu

612-348-1690 x135Focus Area 377

Please Feel Free to Contact an IS with any Additional Questions.Thank You!

![Harmonized Tarriffs[1]](https://static.documents.pub/doc/80x56/577d2cbd1a28ab4e1eacc307/harmonized-tarriffs1.jpg)