FINANCING SMES AND ENTREPRENEURS 2016: AN OECD SCOREBOARD 12th OECD LEED Forum on Partnerships and Local Development 18-19 April 2016, Venice iam Koreen, Deputy Director D Centre for Entrepreneurship, SMEs and Local Development www.oecd.org/cfe/sme

Transcript

www.oecd.org/cfe/sme

FINANCING SMES AND ENTREPRENEURS 2016: AN OECD SCOREBOARD

12th OECD LEED Forum on Partnerships and Local Development18-19 April 2016, Venice

Miriam Koreen, Deputy DirectorOECD Centre for Entrepreneurship, SMEs and Local Development

www.oecd.org/cfe/sme 2

1. Overview of the SME finance Scoreboard

2. Emerging trends in SME financing

3. Recent policy developments

4. Medium-term outlook

Overview

www.oecd.org/cfe/sme 3

What isFinancing SMEs and Entrepreneurs 2016: An

OECD Scoreboard?

Rationale:• Need for comparable and timely statistical information on SME

access to finance

Objectives: • Improve the understanding of business financing conditions,

trends and needs• Assist policy makers in designing and evaluating policies and

programmes relevant to SME access to finance• Monitor the implications of financial reforms on SME access to

finance

4

Rationale and objectives

Current Scoreboard indicators

DEBT

1. SME loans / business loans 7. SME loans used/SME loans authorized

2. SME short term loans/SME loans

8. SME non-performing loans/SME loans

3. SME loan guarantees 9. SME interest rates

4. SME guaranteed loans 10. Interest rate spreads (small vs. large firms)

5. SME direct government loans 11. SME collateral requirements6. Rejection rate

NON-BANK FINANCE OTHER12. Venture and growth capital 15. SME payment delays13. Leasing and higher purchases

16. SME bankruptcies

14. Factoring and invoice discounting

www.oecd.org/cfe/sme 6

Emerging trends in SME financing

www.oecd.org/cfe/sme 7

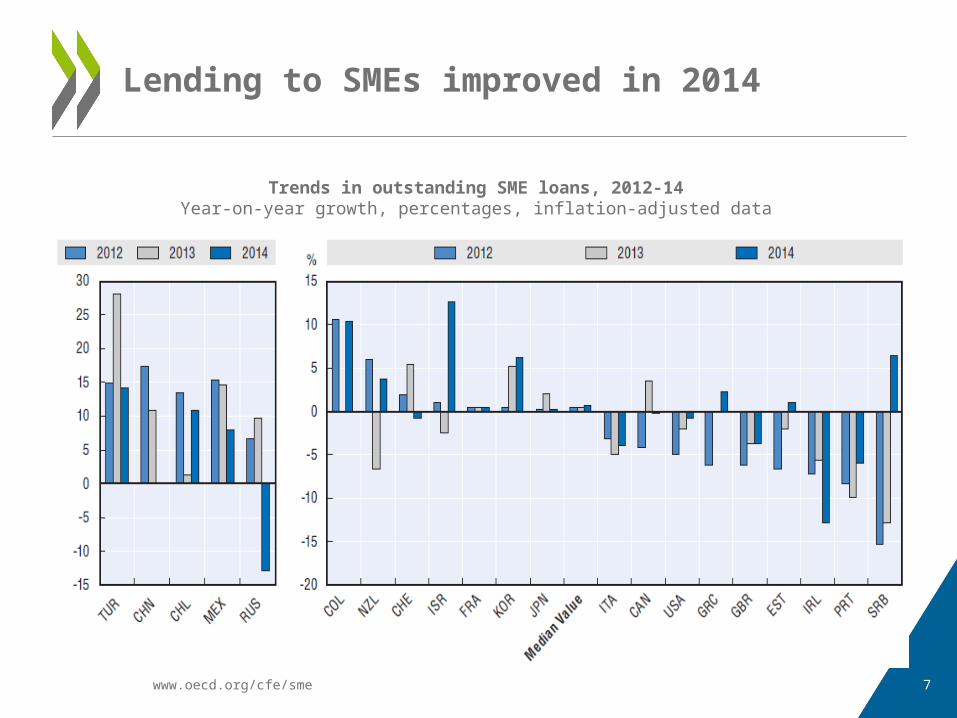

Lending to SMEs improved in 2014

Trends in outstanding SME loans, 2012-14Year-on-year growth, percentages, inflation-adjusted data

www.oecd.org/cfe/sme 8

Credit conditions generally eased in 2014 but remain challenging for many SMEs

Trends in average interest rates on SME loans, 2011-14Year-on-year change

www.oecd.org/cfe/sme 9

SME bankruptcies are declining

Trends in bankruptcy rates, 2013-14Year-on-year change

PRT ESP AUS NLD DNK USA KORGRC NZL JPN CHECOL BEL SWEEST CAN CZE GBR AUT FRANOR SVK RUS ITA-40

-30

-20

-10

0

10

www.oecd.org/cfe/sme 10

Trends in non-performing loans, 2012-14 Year-on-year percentage change

NPLs show a diverse picture and are weighing on business lending in several countries

Notes: *Data on total non-performing loans **Canada reports on the 90-day delinquency rate for small businesses.

www.oecd.org/cfe/sme 11

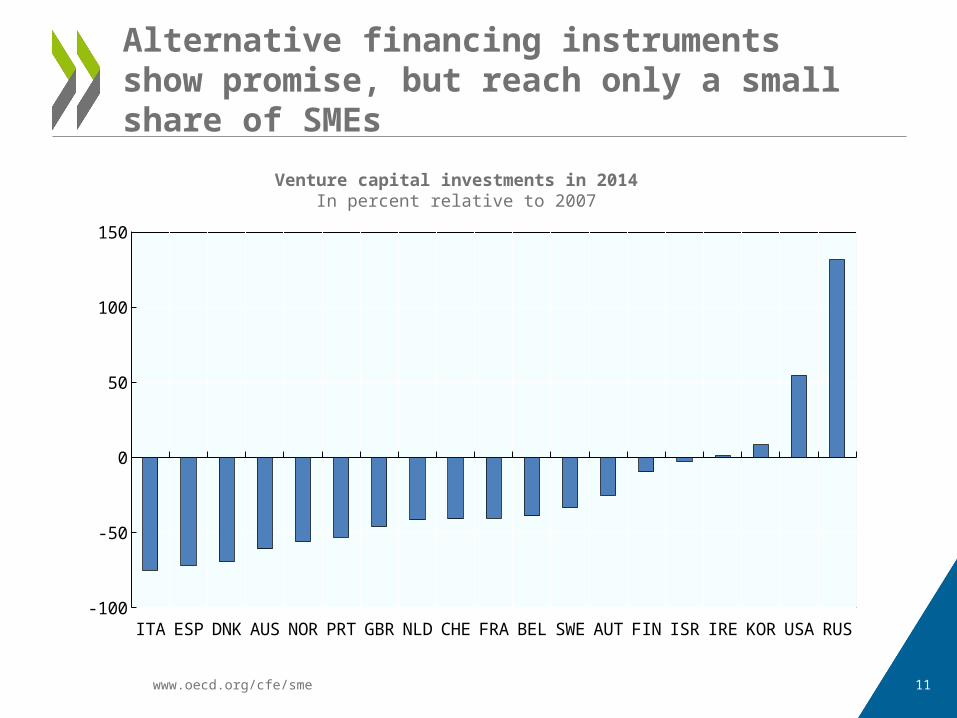

Alternative financing instruments show promise, but reach only a small share of SMEs

Venture capital investments in 2014In percent relative to 2007

ITA ESP DNK AUS NOR PRT GBR NLD CHE FRA BEL SWE AUT FIN ISR IRE KOR USA RUS-100

-50

0

50

100

150

www.oecd.org/cfe/sme 12

• Address a clear financing gap by targeting firms at the seed and early stage with a high risk-return profile

• Provide services beyond financing, including mentoring, business advice and access to networks

• Policy initiatives in this area: co-investment schemes (e.g. Korea, Spain and UK) tax incentives (e.g. Italy, Israel and Turkey) provision of financial support towards network development (such as

“France angels”) financial literacy programmes for recipients of angel investments (e.g.

Canada, Portugal and Mexico)

Business angel investments targeting young, innovative, high-growth firms

www.oecd.org/cfe/sme 13

Recent policy developments

www.oecd.org/cfe/sme 14

Government loan guarantees as a percentage of GDP in 2014

Loan guarantees continue to be the most widespread policy instrument to support SMEs

www.oecd.org/cfe/sme 15

• Targeting young innovative SMEs more explicitly– Austria’s promotional bank activities or repayable grants in New Zealand

• Stimulating equity investments, through:– Tax incentives (Australia and Sweden)– Direct government investment such as seed capital funds (Canada and

Chile)– Regulatory reforms (China and Turkey)

• Efforts to increase SMEs participation in GVCs (Australia and Finland)

Other policy initiatives

www.oecd.org/cfe/sme 16

Medium-term outlook

www.oecd.org/cfe/sme 17

• Downward risks in the macro-economic outlook persist:– And could reverse gains made in recent years

• SMEs remain over-reliant on bank credit– Banks continue to deleverage– More efforts are needed to broaden the range of financial instruments

used by SMEs

• The OECD can assist policy making in this area– G20/OECD High Level Principles on SME Financing– Development of effective approaches for the implementation of the

principles

SME financing will remain fragile in the medium term