48

Agent missouri November-December 2012 Vol. 21 No. 6 special focus: products and services treat yourself to all of the products and services MAIA brings you

| Date post: | 20-Feb-2016 |

| Category: |

Documents |

| Upload: | missouri-association-of-insurance-agents |

| View: | 215 times |

| Download: | 5 times |

Age

nt

missouri

No

vem

ber

-Dec

emb

er 2

012

Vo

l. 21

No

. 6

spec

ial fo

cus:

products

and

servi

ces

treat yourself to all of the products and services MAIA brings you

For more details, contact your Business Development Manager or Customer Service at 1.800.442.0593 or [email protected]

The MEM DifferenceMissouri Employers Mutual has established itself as a consistent, credible resource for your clients’ work comp needs.

With 17 years of market leadership, we have earned our reputation of offering competitive rates combined with exceptional service and our personalized approach to workplace safety. And we’re just getting started.

For a true work comp partner for you and your clients, contact MEM, Missouri’s No. 1 provider of workers compensation.

www.mem-ins.com

WHAT DO YOU EXPECT FROM YOUR WORK COMP CARRIER?

www.worksafecenter.com

november-december 2012 missouriagent 3

contentsSpecial Focus: Products and Services5 Tips for a Successful Agency 24Products and Services 26Big “I” Markets 27Strategize, Evaluate, Contemplate 7Don’t Take Your Telephone for Granted 21MAIA staff profile: Monica Mize 22CISR Program Expands to 9 Choices 23MAIA Committees 29MAIA Staff 33Microinsurance Makes Big Social Impact 38

AdvertisersACUITY 8AmTrust North America 16BC&M 20Swiss Re 32 Burns & Wilcox 4Couri Insurance Associates 14EMC Insurance Companies 47FCCI Insurance Group 37Gateway Underwriters Agency 36IPMG 31

missouriagent

3315 Emerald Lane, P.O. Box 1785, Jefferson City, MO 65102-1785 • 800-617-3658 in Mo. Phone 573-893-4301 • FAX 573-893-3708E-mail: [email protected]: www.missouriagent.org

Publisher Larry CaseEditor Amy J. Hoffman, AIPAdvertising Manager Amy J. Hoffman, AIP

Officers of the MAIAPresident Doug Clift, CIC, St. LouisPresident-Elect Brian Harrison, CIC, ColumbiaVice President Louis Landwehr, CIC, CRM, Jeff CitySec’y-Treasurer Randy Baker, Kennett IIABA National Director Mitchell C. Mills, CWCC, ClintonPIA National Director Richard Minor, CIC, Hannibal Past President Byron Robison, Springfield

Board of DirectorsRegion 1 Ricky Baker, CIC, ChillicotheRegion 2 Darren Smiley, MexicoRegion 3 Chris Rupp, LUTCF, CIC, LibertyRegion 4 Shane Davolt, LibertyRegion 5 Lee Wilbers Jr., LUTCF, CLU, CFP, Jefferson CityRegion 6 Jim Baxendale, CPCU, St. LouisRegion 7 Jeff Mentel, J.D., St. LouisRegion 8 Jane Dobrinic, CIC, CPCU, St. LouisRegion 9 Randy Smart, MarionvilleRegion 10 Tom Montileone, CIC, CISR, AIS, SpringfieldRegion 11 Steve Rackley, CIC, CISR, GainesvilleRegion 12 Mark Gibbins, PortagevilleAt-Large #1 Wil Turner, CIC, BeltonAt-Large #2 Vickie Winkler, CISR, CIC, Ste. GenevieveAt-Large #3 John Patterson, ChesterfieldCo. Rep. Ben Finan, Maryland HeightsCo. Rep Jim Lay, CIC, CPCU, Springfield

Staff of the MAIAExecutive Vice President Larry CaseVice President of Operations Sheryl Van LeerVice President of Marketing Lindsay Griffin, AIPInsurance Services Manager Leona LoethenEvents Manager Jeanne Blomberg, AIPDatabase Administrator Laura BerendzenCustomer Service Representative Theresa Flippin, AIPCustomer Service Representative Monica Mize, AIPEditor Amy J. Hoffman, AIPMembership Services Representative Kelli Kloeppel, AIPEducation Director Emily KoenigsfeldAdministrative Assistant Dawn Patterson

MISSOURI AGENT (USPS 709-210) is published bimonthly by the Missouri Association of Insurance Agents, 3315 Emerald Lane, Jefferson City, MO 65109, phone 573-893-4301. Periodical postage paid at Jefferson City, Mo.

MAIA does not necessarily endorse any of the companies advertising in this publication. Subscription rate for members is $25 per year, which is included in dues.

Address & Other Changes

Notify Missouri Agent if you change your address, change your agency name, or drop or change producers (who are voting members of the association). Write to Missouri Agent, P.O. Box 1785, Jefferson City, MO 65102-1785 or e-mail [email protected].

POSTMASTER: Send address changes to Missouri Agent, P.O. Box 1785, Jefferson City, MO 65102-1785.

© 2012 Missouri Association of Insurance Agents

On the Cover: Tis the season to partake of all that MAIA offers its members — during the holidays and all year long. Story on page 26.

Volume 21, No. 6

JM Wilson 12MAIA Partners 48MEM Insurance 2Missouri Rural Services 40M.J. Kelly 38Ringwalt & Liesche 10SECURA 42Surplus Lines Association of Mo. 45The Hartford 18West Bend 6

Age

nt

missouri

mo

nth

1-m

on

th2

2012

Vo

l. 21

No

. 6

spec

ial fo

cus:

products

and

servi

ces

treat yourself to all of the products and services MAIA brings you

DepartmentsFrom the President 5The Legal Side 9Technicalities 10From the DIFP 13Technology 15News & Know-How 19

Errors & Omissions 34Regulatory Actions 43 Agency News 45Company Partner News 46Classifieds 46

No one writes Excess/Umbrella with the capacity and speed of Burns & Wilcox.

Put the power and speed of the Burns & Wilcox pen

to work for you: Solidify your clients’ coverage with

our breadth of proprietary Excess/Umbrella solutions.

Derived from our exclusive binding contract authority,

our assets allow us to quote and bind policies at rocket

speed. When it comes to securing your clients’ financial

interests, think fast. Think the largest independent

wholesale broker – Burns & Wilcox.

Commercial • Personal • Professional • Brokerage • Binding • Risk Management Services

Overland Park, Kansas | 913.451.3135toll free 866.476.0439 | fax 913.451.3156overlandpark.burnsandwilcox.com

St. Louis, Missouri | 314.819.0400toll free 800.331.4128 | fax 314.819.0440stlouis.burnsandwilcox.com

31637_BURNS_Rocket Pen_KS1_MO1_Missouri Agent_APPROVED.indd 1 10/8/12 2:04 PM

november-december 2012 missouriagent 5

What I didn’t know I didn’t know

Doug Cliftpresident, MAIA

After a long, hot summer of record tempera-tures in Missouri, we can finally get outside and enjoy the cooler weather. I love fall; it’s always a season of change: changes in the weather, changes in the wardrobe (just ask my wife), changes in family routines as kids head back to school — which means that it’s also a time for learning new things.

I’ve had a lot of changes recently and also realize I’ve become a learner. From my first na-tional IIABA meeting, I’ve learned what I didn’t know I didn’t know. (Follow that?) I’d like to share my education with you. I’ve put some of MAIA’s best practices into place, and perhaps you will too when I share a little of what I’ve learned: How MAIA can help your agency be even more successful.

My first IIABA board meeting, which I at-tended with Larry Case and Mitchell Mills, was an eye-opening experience and something I wish all independent agents could experience firsthand.

The IIABA is a very large and powerful orga-nization with more than 22,000 members na-tionwide, but it is experiencing the same prob-lems many other national associations have: loss of membership and, more importantly, the challenge to stay relevant.

As I sat in a planning session with other state presidents, we learned that IIABA currently has 52 different “businesses” or programs. As we went around the table, we were hard pressed as a group to even name five of the 52!

We asked each other how all of these pro-grams can be relevant to our membership and whether they really create value. Easy questions to ask, but hard to answer since two-thirds of IIABA’s budget comes from revenue generated by members’ services and products.

My education continued as I brought these thoughts to MAIA’s board meeting in Septem-ber. As I was explaining my observations from the national meeting, I got a very good ques-tion from Wil Turner, who is our At-Large 1 representative: How many of our own members

in Missouri know the programs and services that MAIA provides, let alone the 52 national programs? I thought I understood our programs and services pretty well but decided to dig a little deeper and was surprised with what I didn’t know.

MAIA member services and products can easily be reviewed on our website. Some are national programs offered by IIABA. In order to better understand the features and benefits of these programs to our membership, I “in-terviewed” Larry Case. I was very surprised by some of the things I learned. Below are some highlights of the programs administered and run on the state level, which are relevant and bring value to our membership in Missouri.

E&O insuranceOne of the biggest programs we run is the sale of agent errors and omissions coverage with Utica Mutual and Westport. Of course, there are many competing programs, but I learned that both of these programs were designed by agents for agents.

Did you know that Larry and our staff meet with both companies every year? They review their forms and make recommendations on improving coverage to better protect our membership.

For those who have their E&O with other car-riers, can you truly feel comfortable you have the best coverage for the best price? I certainly feel better knowing MAIA is staying on top of this very important coverage for our agency. If you haven’t gotten a quote from MAIA recent-ly, I strongly suggest you give them a try.

Agents umbrella coverageAnother program, which I knew MAIA offered but I had never taken advantage of, is the agents umbrella program offered through Penn National and Swiss Re. This is another program designed by agents for agents. I found out that the Penn National umbrella provides excess coverage over your E&O policy and as

continued on page 41

fromthepresidentNo one writes Excess/Umbrella with the capacity and speed of Burns & Wilcox.

Put the power and speed of the Burns & Wilcox pen

to work for you: Solidify your clients’ coverage with

our breadth of proprietary Excess/Umbrella solutions.

Derived from our exclusive binding contract authority,

our assets allow us to quote and bind policies at rocket

speed. When it comes to securing your clients’ financial

interests, think fast. Think the largest independent

wholesale broker – Burns & Wilcox.

Commercial • Personal • Professional • Brokerage • Binding • Risk Management Services

Overland Park, Kansas | 913.451.3135toll free 866.476.0439 | fax 913.451.3156overlandpark.burnsandwilcox.com

St. Louis, Missouri | 314.819.0400toll free 800.331.4128 | fax 314.819.0440stlouis.burnsandwilcox.com

31637_BURNS_Rocket Pen_KS1_MO1_Missouri Agent_APPROVED.indd 1 10/8/12 2:04 PM

Your customers’ businesses are

special.So it’s important to make

sure they’re well protected.

The insurance professionals at NSI,

West Bend’s specialty division, can

create the right insurance program for

specialized businesses. We have the

knowledge and experience to protect

many kinds of businesses, from

beauty salons to YMCAs to childcare

centers. And our loss prevention and

claim reps are experts at designing

safety programs and handling claims

for specialty businesses.

So talk to the professionals at NSI

to find out how we can help your

customers.

Because if it’s worth insuring,

it’s worth insuring well.

If it’s worth insuring,

it’s worth insuring well.

november-december 2012 missouriagent 7

Larry Caseexecutive vice president, MAIA

Strategize, Evaluate, ContemplateThe arrival of the 2012 college football season marked the beginning of a major transition for the University of Missouri Tigers as they began play in the prestigious Southeastern Confer-ence. While numerous factors impacted the de-cision to make the move, in the end, it brought an opportunity to be a part of what is widely recognized as the best athletic conference in the country.

As Mizzou is making its move, MAIA is also making ours. In conjunction with MU’s transition, MAIA continues its Trusted Choice advertising campaign with Mizzou Sports Properties, expand-ing a partnership we began in 2006. You will now hear both in-game and post-game ads, as well as the featured “Trusted Choice of the Game,” a play cho-sen by Mike Kelly and presented in the post-game football and basketball shows. We also have added brand exposure with a Trusted Choice banner, which will peri-odically appear on the Mizzou athletics website.

Not to be outdone by MU’s effort to be the best, your MAIA board of directors is focused on ensuring that this association is functioning as one of the best in the nation. The strategic planning session held earlier this year has led to some out-of-the-box thinking and energized your leadership and staff to focus on our vision for the future. Their goal is to provide excep-tional value to members and make sure we are well positioned in an ever-evolving insurance marketplace.

At the September board meeting, each member of the board received a copy of the book Race for Relevance, written by association guru Harrison Coerver. Board members will be considering the concepts and ideas presented in this book and how they might intertwine Coerver’s visions with priorities and goals they have for MAIA over the next few years.

We often speak about insurance not being a commodity. It is peace of mind and a promise to provide assistance and service in the event of specific events and to minimize the impact of unfortunate circumstances by rebuilding or replacing property or defending policyholders against potentially disastrous litigation. As-sociation membership is much the same. While

we do have some tangible benefits we can offer, the real benefits of membership are the intangibles.

In every survey, members identify networking opportunities, service, information, advocacy and legislative representation as some of the top reasons you feel membership is important to your business. In other words, you recognize and value the importance of the intangible ben-efits we provide and expect us to be relevant in

representing your interests, whether it is with industry partners or in political

or regulatory arenas.Thus, it is appropriate that we

periodically perform a Self Ex-amination and Critique of our priorities and processes. We must make sure we are on top of our

game and are Seeing Evolutionary Changes so that we can keep you

informed about what pitfalls may lay ahead. And we must make sure that we

are considering appropriate Strategies, Efficien-cies and Collaborations in order to best serve you, our members.

MAIA has always been blessed with very dedicated leaders who give selflessly of their time in order to help perpetuate the indepen-dent agency system and ensure that we have the ability to deliver the services you expect from us. This example of their forward thinking should assure you that you will be able to de-pend on us in the future.

In the end, our goal and our pledge to you is that we will continue to Skillfully Evaluate Challenges you face and provide you with real value for your membership with benefits, such as these:

• Structured Educational Curriculum;• Sensible Expert Consultation;• Stimulating and Enlightened Communica-

tions; and• Sensational Events and Conferences.

Of course, we will expect you to do your part and participate and take advantage of what we provide for you.

SEC you soon. Go Mizzou!

myturn

WE’VE GOTYOUR BACK.

www.acuity.com

facebook.com/acuitywowIntroducing Eva & Ella, the ACUITY Cuties

november-december 2012 missouriagent 9

Lewis E. Melahn, J.D.

WE’VE GOTYOUR BACK.

www.acuity.com

facebook.com/acuitywowIntroducing Eva & Ella, the ACUITY Cuties

More perspectives on producer duties

contingent commissions or in other ways had failed to carry out an expected duty with rea-sonable care, skill and diligence.

As to whether a producer has breached a duty of loyalty to a customer, the Court af-firmed several prior court decisions stating that the scope of a producer’s agency is to procure the insurance requested by the insured and

that a producer has no duty to advise insureds on their insurance needs or on the availability of a particular coverage unless specifically agreeing to do so.

With regard to the fact that Marsh & McLennan collected interest on monies held in trust between the time of collecting the premiums from Emerson and paying the pre-miums to the insurance com-pany, the Court ruled that

while the Missouri statutes clearly note that a producer holds such funds in a trust and fiduci-ary capacity, nothing in the statute gives the policyholder the right to monies other than the premiums agreed to in the insurance policy.

Because the Missouri statutes impose no duty with regard to interest, the Court refused to impose such a duty because of the producer’s limited role in procuring insurance. Finally, the Court likewise refused to expand the producer’s duty to include finding coverage of the lowest possible cost. Since the producer has no duty to advise insureds about what insurance they need or what insurance to buy, the Court would not expand the producer’s duty to include deter-mining the cost of insurance to be paid by the policyholder.

The Court’s findings are all beneficial to producers because the decision declines to expand the duties owed by producers in their relationship with policyholders. However, in all its determinations, the Court holds open the potential that a producer could in fact owe any one of the duties discussed if the producer spe-cifically undertakes to accept it by contract or by a course of conduct.

continued on page 12

thelegalside

In my last article, I discussed potential issues with a producer’s duty to an insurance carrier. There are also issues evolving regarding the duties a producer owes in the relationship with policyholders, especially in situations where the producer acts as a broker for the policyholder.

Earlier this year, the Missouri Supreme Court gave some guidance on the recognized duty of producers, while leaving some questions open to de-terminations based on con-tract or custom.

In the case of Emerson Electric Company v. Marsh and McLennan Companies, Emerson sued, alleging Marsh & McLennan had violated a fiduciary duty of loyalty by accepting contingent com-missions without notice to Emerson, by keeping interest earned on premiums col-lected before payment to the insurance carrier and by failing to provide Emerson with the low-est cost coverage possible.

While the court examined the difference be-tween an agent, who represents the company, and a broker, who represents the policyholder, generally it held that in either situation, the producer’s primary duty to the policyholder is limited to procuring the insurance requested by the policyholder.

In either capacity, the producer has a duty to perform his or her duties with reasonable care, skill and diligence. However, that duty does not extend to advising insureds about what insur-ance they need or what insurance to buy, unless the producer specifically undertakes to do so.

The Supreme Court determined that Sec-tion 375.116 of the Missouri statutes authorizes a broker to receive commissions and makes no distinctions as to the type of commissions; therefore, the receipt of a contingent commis-sion is not of itself a breach of a duty. However, the Court did not throw out the suit, saying that the trial court could still determine whether Marsh & McLennan had specifically undertaken additional duties of disclosure with regard to

Lewis E. Melahn is a practicing attorney in Jef-ferson City. He provides free legal consultation to MAIA members on a limit-ed basis. He served as the director for the Missouri Department of Insurance from 1989-1993. You can contact Lew Melahn at 573-636-5057.

The Court’s findings

are all beneficial to

producers because

the decision declines

to expand the duties

owed by producers in

their relationship with

policyholders.

10 missouriagent november-december 2012

Pitfalls of personal insuranceBefore I go into some of the pitfalls of per-sonal insurance, I thought it best to discuss the fact that personal insurance should not be treated as a commodity.

The definition of commodities from Inves-torGuide.com is, “goods that are supplied to the market without differentiation based on brand, source or other factors.”

As independent agents, this is our sales tool. We can sell differentiation. We have the prod-

ucts to offer our clients and a variety of compa-nies, each of which may have a different under-writing appetite and pricing structure. We also have additional options, which may not be avail-able from the direct market or 1-800 channels. We do not want to sell on price, as we all know the old saying, “Win on price, lose on price.” We want to offer our clients a product that is not just a commodity but something designed specifically for them.

Our goal is to offer our clients a program with features and benefits designed for their specific needs. The information gathering process is the most critical part of designing this program.

During this process, keep in mind the pitfalls that lurk around all the corners. Pitfalls are gaps in coverage. Some of these gaps can be closed; others cannot. We just need to be sure that our client understands the issues involved with the ones that cannot be closed. It is a good idea to work with a coverage checklist to help determine the needs of a client.

While there are more than I can cover in this article, I will review some gaps, which I think are important and are frequently encountered.

All lines• Always name both spouses on all policies.

Spouses who aren’t named on the policy may lose coverage during a separation or divorce. Coverage can cease when one spouse moves out of the household. Read your policy.

• In a divorce situation, don’t remove either spouse or any vehicle without the permission of both in writing. Don’t reduce coverage without permission of both insureds in writing.

• Domestic partners: Name partners as named insureds. Being added as a driver doesn’t add any coverage. Both signatures should be required.

• Be sure all liability limits are the same.

Auto• Children who move out of the household with

a vehicle owned and insured by their parents do not have proper coverage. They will lose coverage for driving or being hurt in non-owned vehicles under their parents’ policy. In the event of an accident with an uninsured or

Jane DobrinicCharles L. Crane Agency Co.

MAIA Technical Committee

Ringwalt & Liesche

COMMERCIAL AUTO

GARAGE LIABILITY

GENERAL LIABILITY

MOTOR TRUCK CARGO

COMMERCIAL PROPERTY

WORKERS’ COMPENSATION

Send submissions to: [email protected]

P: 800-708-7448F: 402-916-3333

Why Quote with Ringwalt & Liesche?

• A++ Markets

• Competitive Rates

• Quick Turnaround

• Attractive Commission

• Online Rater

Whether you’re trying to place an unusual risk or an everyday operation, you can

look to us for a quote! Check us out today at www.ringwalt.com.

technicalities

november-december 2012 missouriagent 11

underinsured driver, there would be no cover-age for this family member if he or she does not have his or her own auto policy. Moving out of the household negates some of the extensions of coverage under the auto policy.

Solution: Transfer the title to the family member and write a policy in the new own-er’s own name.

• Many personal auto policies are introducing step-down coverage or drop-down provi-sions, which limit coverage for some drivers to state minimums ($25,000/$50,000/$10,000 in Missouri). Other policies will reduce coverage for anyone in the household who is not rated on the policy.

Solution: Read your policy carefully.• College students who have roommates have

an additional exposure. Often, car keys are thrown on the counter and the students will frequently use someone else’s car in the household. There is a liability exclusion in the personal auto policy for an auto that is furnished or available for an insured’s regular use. If a student borrows a car in this scenario and is involved in an accident with a car that has no insurance or insufficient limits, the policy will not respond.

This same situation applies when there is a company car in the household. Cars owned by other members of the household, such as roommates or domestic partners, may also be excluded.

Solution: Add the Extended Non Owned Endorsement, naming the individual for whom coverage is provided. This is PP 03 06.

Solution: Get college students and adult children their own policy as soon as is practical.

• Only vehicles acquired by the policyholder are automatically covered when you purchase them. Cars purchased by a family member may not automatically be covered.

Solution: Make arrangements ahead of time with your agent.

• Once you purchase a new vehicle, it immedi-ately begins depreciating in value. That rate of depreciation may be faster than you are paying off the loan. In the event of a total loss, the settlement may be less than what is

owed on the vehicle. This situation can occur whether you buy the car or lease it.

Solution: Anytime a client buys or leases a new car, offer auto loan lease coverage. This coverage prevents you from having to pay this difference out of pocket.

Home• College students may lose coverage under

their parents’ homeowners policy if they turn 24 or become part-time students. Review your coverage. Their college may not be an in-sured location.

Solution: Write a renter’s policy for the student.

• The 2011 revision of the ISO Homeowners Policy has broad-ened coverage for kids’ battery powered toy cars, provided they are designed for kids under the age of seven and can’t exceed 5 mph. (This was excluded in the prior edition of the policy).

• The Incidental Low Power Recreational Motor Vehicle (HO 24 13) can be used to add liability coverage for owned off-road recreational motor vehicles, but the top speed must be 15 mph or less.

• Motor vehicle exclusions in the 2011 revision of the ISO Homeowners Policy exclude cover-age for motor vehicles unless they are used “solely to service a residence.” This broadens coverage, as the prior version read, “used solely to service the insured’s residence.” The 2011 version allows servicing of other resi-dences but not any commercial property, such as helping your local church.

Solution: Be sure to read your policy, as we see significant variations on this exclusion in other policy forms, and advise your client ac-cordingly in writing.

• Property in storage is now covered for 10 percent of the personal property coverage as opposed to the full personal property limit in prior versions of the ISO HO policy.

Solution: This may be increased by adding HO 06-14, Increased Amount of Insurance for

continued on page 12

12 missouriagent november-december 2012

KNOWLEDGECOMES FROM EXPERIENCE

“I go the distance on my bike—just like my 30-year journey with J.M. Wilson. I lead a great team of managers and underwriters that work hard to help our agents be successful.”

Sandi Fritz, CIC Vice President, Underwriting and Branches—and fixture on the bike trail

Connect with Sandi on LinkedIn!

PIA National 2011 MGA of the YearProperty/Casualty • Professional Liability • Surety Commercial Transportation • Personal Lines • Premium Finance

800.666.5692 jmwilson.com

Personal Property Located in a Self-Storage Facility. However, this endorsement may not be available with all companies.

• Be aware of the exclusion for theft, which reads, “The peril of theft does not include loss caused by theft for property while at any other residence owned by, rented to, or occupied by an ‘insured,’ except while an ‘insured’ is temporarily living there.”

Solution: Write an HO5 policy on the pri-mary or a tenant homeowners policy on the temporary location

Excess liabilityAlways offer excess liability coverage. Determin-ing the amount of coverage to purchase should be left up to the insureds. Suggest that they buy as much as they can afford.

Flood insuranceAlways offer flood insurance. You don’t have to be in a special flood hazard area to need this coverage. The homeowners policy does not cover surface water.

Jane Dobrinic, CPCU, CIC, is a manager at Charles L. Crane Agency Co., St. Louis. She is in her third year as a member of the MAIA Technical Committee.

technicalities continued from page 11

What course of conduct might indicate a pro-ducer has accepted such a duty remains subject to speculation; however, the Court did reference a prior court decision in Zeff Distributing Com-pany v. Aetna, where the court found the rela-tionship between the producer and policyholder was such that when the policyholder’s coverage was cancelled, the policyholder could reasonably expect that the producer was going to replace such coverage or advise the policyholder such coverage could not be obtained. By failing to do so, the producer had breached a duty upon which the policyholder had relied, based upon a prior course of conduct.

This case serves as a reminder that producers should not create expectancies by their policy-holders for anything other than the exercise of reasonable diligence to procure the insurance the policyholder desires.

Indicating that a producer can do anything more than that for a policyholder may raise an expectancy and create a duty for the producer that otherwise would not exist.

legalside continued from page 9

november-december 2012 missouriagent 13

Ramifications of Senate Bill 749We have a new health insurance law in Mis-souri, as of the recent veto session of the Mis-souri General Assembly. Senate Bill 749 is now law. It lays out several new requirements for all providers of health insurance coverage, covering contraception, elective abortion and sterilization.

The bill was vetoed by Gov. Jay Nixon in July on the grounds that it was unnecessary and duplicative of the existing contraception stat-ute. The old law, on the books since 2001, gave employers the right to refuse contraceptive coverage for their group health plans, in effect opting out of providing contraception coverage for employees. In such situations, the law also gave employees the right to opt back in to that coverage.

In his veto message, the governor said noth-ing in S.B. 749 “would enhance these substan-tive religious protections that have been in place and afforded to employees and employ-ers and will remain part of Missouri law after my veto today.”

Nevertheless, the legislature overturned the governor’s veto, and S.B. 749 is now law. For the department, that means our legal obligation is strong enforcement of all provisions of the law for which we have authority, namely the new provisions in Chapter 376 RSMo. That chapter applies to insurance companies and fully insured health plans. And we are committed to that.

But I want to bring to your attention several provisions that fall outside the insurance chap-ters. For the first time, there are now require-ments related to coverage of contraception, abortion and sterilization in Chapter 191, the general public health statutes. These require-ments, according to the new law, now apply to “health plan providers” and “health plan spon-sors.” Since these are undefined terms, there is a question about whether they extend to all health plans, including self-insured plans.

Also in Chapter 191, sterilization is men-tioned. This is a subject that does not appear in Chapter 376.

You are aware that our department has no jurisdiction over self-insured health plans or to enforce Chapter 191. So we cannot provide guidance to these plans regarding the new re-

quirements. But I encourage you to consider the ramifications of this new language for all your clients with group health plans. Those clients who have purchased fully insured group plans will certainly need to comply with the new law. But those who are self-insured may be affected as well. They may need to consult with their legal counsel on whether the new state require-ments apply to their health benefit offerings.

Join us for the Director’s Regulatory SummitI want to invite you to a first of its kind confer-ence our department is hosting in December. The Director’s Regulatory Summit will be a one-day event in Columbia, December 6. It will be an opportunity to learn more about department operations, including licensing and our han-dling of agent investigations and market con-duct reviews. Please spread the word to agents and carrier representatives alike. There will be valuable content for all involved in our industry, and we will offer continuing education credit. Visit insurance.mo.gov/summit for more details.

John M. Huffdirector, Mo. DIFP

fromtheDIFP

This article expresses the official views and opinion of the Missouri Department of Insur-ance, Financial Institutions and Professional Registration, which may not necessarily be those reflected by the MIssouri Association of Insurance Agents.

Grow your business. with Couri Associates.

Or Ask one of these strategic partners about Couri Associates’ value

Visit www.couriagents.com/raves/

Retain your identity

Hear what our associates are saying about our focus on agents and our great commissions!

Interested in becoming part of the Couri family? Visit our website,couriagents.com or give Steve Albinger a call at 800-444-1215.

Scan thiswith your

Smartphone QR Reader App.

Search “QR Code” in your App storeto download a mobile reader.

Or

This is just a sampling of the quality carriers Couri represents.

november-december 2012 missouriagent 15

Grow your business. with Couri Associates.

Or Ask one of these strategic partners about Couri Associates’ value

Visit www.couriagents.com/raves/

Retain your identity

Hear what our associates are saying about our focus on agents and our great commissions!

Interested in becoming part of the Couri family? Visit our website,couriagents.com or give Steve Albinger a call at 800-444-1215.

Scan thiswith your

Smartphone QR Reader App.

Search “QR Code” in your App storeto download a mobile reader.

Or

This is just a sampling of the quality carriers Couri represents.

Agency strategies to send and receive personal data securelyDue to growing use of the Internet and mobile technologies in business, errors and omissions underwriters are increasingly asking their appli-cants whether they encrypt or use other protec-tive measures to safeguard client personal data when it is being transmitted. Below are several approaches agencies can take to protect per-sonal data in transit.

Encryption When you think of encryption, consider those codes the military employs to keep conversa-tions unintelligible to the enemy. You can find many definitions of encryption on the Internet, but I like this simple one from Microsoft:

Encryption is a way to enhance the security of a message or file by scrambling the contents so that it can be read only by someone who has the right encryption key to unscramble it. For example, if you purchase something from a website, the information for the transaction (such as your address, phone number, and credit card number) is usually encrypted to help keep it safe. Use encryption when you want a strong level of protection for your information.

Requiring a strong password to gain access to your system is an important security procedure, but it is not the same as encrypting the data within the system.

Personal data Which types of personal data are the most sen-sitive and need to be encrypted when transmit-ted? The definition of personal data can vary by state and is contained in the state data breach notification and privacy laws (www.ncsl.org/issues-research/telecom/security-breach-notifi-cation-laws.aspx), as well as in various federal laws, such as the Health Insurance Portability and Accountability Act of 1996 (www.hhs.gov/ocr/privacy/hipaa/understanding/summary/pri-vacysummary.pdf).

Insurers, too, might employ various defini-tions of personal data in their policies, so it is

Jeff Yatesexecutive director, ACT

incumbent upon the agency to be familiar with not only the specific laws but also the coverage definitions that apply to the agency.

Note also that the applicable state law is based upon the residency of the individual whose personal data is being protected, not the location of the agency. This is an important con-sideration for agencies writing business in mul-tiple states and agencies writing policies that cover individuals who reside in multiple states.

With all of the above caveats, the most com-monly mentioned types of non-public, individu-ally identifiable personal data covered in the laws are those such as social security numbers, driver’s license numbers and other government issued IDs, debit and credit card numbers and PINs, bank and financial account numbers, and protected health information.

While often not mentioned in state laws, other particularly sensitive personal data, which should be protected, includes information com-monly used for security verification (mother’s

continued on page 17

technology

AmTrust has a bouquet of coverage

for small businesses

Your Success is Our Policy.®

AmTrust North AmericaAn AmTrust Financial Company

For more information about how you can write business with AmTrust, please call 877.528.7878 or visit www.amtrustnorthamerica.com.

A.M. Best rating of “A” (Excellent) FSC IX

Complementary workers’ comp and BOP coverage By offering a competitive businessowners policy (BOP) as an individual product or as an accompaniment to our workers’ compensation insurance or commercial auto products, AmTrust has a selection that serves small businesses well.

Better yet, we offer a 10% discount on BOP for our existing workers’ compensation policyholders. An umbrella policy is also available, with limits ranging from $1 million to $10 million to fit over our BOP and commercial auto products.

november-december 2012 missouriagent 17

maiden name, date and place of birth, etc.) or sensitive insurance information (such as jewelry schedules).

It is important for agencies to know what types of personal information they collect, where it is retained and who has access to it. They then need to decide whether they really need to keep this sensitive information.

For example, many agencies no longer retain copies of bank checks and are careful only to pass along credit card numbers to carriers but not to retain them so they do not become sub-ject to the comprehensive payment card indus-try compliance requirements. These agencies are also extremely careful to shred this personal data as soon as it is no longer needed.

Further, if the agency decides it must keep particular sensitive personal data, it should limit access to only those employees who need to see it, to the maximum extent possible. This is par-ticularly true for protected health information. Finally, the agency should be careful to make sure that this personal data is kept off PCs, mobile devices, thumb drives and other devices where there is a significant risk of loss or theft.

PCs and mobile devices Users of PCs and mobile devices should be trained to remove any e-mails with personal data received on these devices as soon as they are read. In addition, the agency should audit to make sure any PCs and mobile devices that can access agency applications are password pro-tected. Further, the agency should implement software that can wipe all of the data off of these devices if they are lost or stolen, restoring them to the original manufacturer’s state.

Secure e-mail E-mail is the first major area where agencies need to begin to encrypt their communications to carriers and clients when personal data is included. Some examples of e-mails likely to include personal data include insurance applica-tions sent to carriers for a quote or to clients to complete and sign, and insurance policies sent to clients.

With respect to e-mails between agencies and carriers (and general agents), ACT recom-mends that transport layer security be imple-mented wherever possible. TLS is an open

standard, which, once implemented between an agency and a car-rier (both parties must have it implemented), renders all of the e-mails between the partners transparent to the end users. In other words, the agent or carrier underwriter does not have to go to a proprietary website to pick up each e-mail. TLS is a great solution for business partners with frequent e-mail communications going back and forth.

Agencies can implement TLS if they have e-mail servers or hosted solutions that offer it. We recommend that the initial TLS set up be handled by the agency’s technology person, who should also verify that it is working prop-erly with each carrier and general agent. You will find a number of resources explaining TLS on the ACT website (www.iiaba.net/act), includ-ing a list of carriers, which have advised us that they have TLS available.

Unfortunately, most agency clients will not have TLS capability. This will require the agency to implement a proprietary e-mail solution as well for these clients. When the agent sends a secure e-mail to the client using one of these proprietary solutions, the client accesses it on the e-mail vendor’s secure website. The secure e-mail tool also enables the client to send a secure e-mail back to the agent, which is help-ful when the client is being asked to complete an application, for example. Fortunately, there are a number of vendors that can help agencies with both TLS hosted e-mails and proprietary e-mails. (Two examples of such vendors are Ap-pRiver and RPost.)

Agency websites It is also critical that agencies provide secure website connections for consumers when they ask the consumer to provide personal data on the website, such as to receive a quote. The website should create a secure “https” tunnel before the consumer can fill out any form that asks for personal data, just as you would see when purchasing something or banking online.

technology continued from page 15

continued on page 18

18 missouriagent november-december 2012

“The Hartford” is The Hartford Financial Services Group Inc. and all of its subsidiaries. © 2012 The Hartford Financial Services Group, Inc. All rights reserved.

thehartford.com

CELEBRATING INDEPENDENTS’ DAY – EVERY DAYAt The Hartford, we happily applaud the independent agents who help us achieve. We believe trust and support are the foundation to building lasting relationships – and enduring success.

354_hart_agent_suppt_ad.indd 1 8/13/12 10:43 AM

If the agency provides a “non-https” free-form text field, which the consumer can use to contact the agency and make requests, there is some risk the consumer will enter private, personal data. Therefore, it is a best practice to take one of the following steps with regard to this free-form text field: (1) secure it; (2) change it to specified fields, which ask only for basic contact information, such as name, phone number, e-mail and address; or (3) in-clude a note warning that the free-form text field is not secure and should not be used to provide any private personal data.

If the agency provides clients with the capa-bility to access their insurance information or documents online, the website should create an https connection before any information can be accessed. Once again, agents should work with their website provider to help them with the technical aspects of creating this secure website capability.

Some agency E&O providers also require the agency to post a privacy statement on its web-site if there is an option for the consumer to submit personal data through the website. It is important that the agency customize its pri-vacy statement to track the agency’s particular data collection, usage, sharing and protection practices with regard to data collected. Honda’s financial services website privacy statement (www.hondafinancialservices.com/help/privacy-policy) provides a good example of the types of information that are typically included in such statements.

ACT resources ACT has developed several resources for agencies to review as they establish and implement their agency’s comprehensive information security program. All of these resources are included on the “Security and Privacy” page of the ACT web-site (www.iiaba.net/act) under the “Quick Links” heading. These resources include a prototype agency information security policy, which agen-cies can use as a template to build their own cus-tomized policy or as a checklist of security issues they should address.

Jeff Yates is executive director of the Agents Council for Technology, which is part of the IIABA. He can be reached at [email protected]. ACT’s website is www.iiaba.net/act. This article reflects the views of the author and should not be con-strued as an official statement by ACT.

technology continued from page 17

november-december 2012 missouriagent 19

Research provides insight into agency performance

The 2012 Best Practices Study marks the 20th edition of the annual benchmarks research for agencies. Over the past 20 years, agencies have endured both hard and soft markets and one of the worst economies since the Great Depres-sion. The 2012 results, which are based primarily on agency data as of Dec. 31, 2011, show that the study’s participating agencies began to face the unusual combination of a hardening mar-ket and a continuing soft economy. As a result, their performance, while improving, remained somewhat suppressed.

Overall, the Best Practices agencies confi-dently held their ground but did not make huge strides in improving agency performance, the 2012 results show. Most agencies appeared to have completed the year with resources and systems in place to move cautiously into an envi-ronment that could present new opportunities — or new challenges.

The 2012 Best Practices Study provides critical performance benchmarks in six agency revenue categories ranging from less than $1.25 million to more than $25 million. Agencies can mea-sure, evaluate and compare results for agency operations, including income and expense distribution, revenue and profitability growth, sales and service staff compensation and productivity, technology expenses, property-casualty and life-health carrier representation, and more.

In addition, the study measures results from its “Rule of 20,” a simple growth and profit-ability balancing equation, which determines if a firm is creating value for shareholders. Small and large firms improved their scores but fell well short of the desired score of 20: Small firms averaged 15.9, and large firms averaged just 14.9. The low but improved scores highlight the struggle of agencies to maintain their value, even as they grow their revenues.

The Best Practices program is a partnership of the Big “I” and Reagan Consulting and is recognized as some of the most thoughtful, effective and valuable resources made available to the industry.

You can learn more about the Best Practices resources and order online, or for questions, email [email protected].

Become a Best Practices agency

Over the past 19 years, the Best Practices Study has examined top performing agencies across the country. For these agencies, inclusion provides the prestigious status of “Best Practices Agency” and opens the doors to many benefits. The next cycle begins January 2013 and is your agency’s chance to be involved.

The process at a glance:Once every three years, the Big “I” requests agency nominations from state associations and company partners. Nominated agencies are invited to participate. If you would like to be considered for nomination, you can fill out the “Self Nomination Form” available online by clicking the “Uncover Industry Best Practices” link on the IIABA home page (www.iiaba.net).

Agencies that choose to participate submit detailed financial and operational information, which is scored and ranked objectively.

The top agencies in six revenue categories are included and deemed “Best Practices Agencies.”

To retain this status, each agency must submit year-end results each year. There is no other commitment.

&news know-howEXTRA!

Obtain your 2012 Best Practices Study update

november-december 2012 missouriagent 21

• How is your receptionist perceived by your customers?

Don’t take for granted that you already know the answer to these questions, Corbett advises. Investigate. If you find that you have people who can’t be superb on the phone, don’t let them answer it. They’re doing serious damage to your business and your brand image, and you may not even be aware of it.

Harry Beckwith, author of Selling the Invis-ible, says, “Every employee should know that every act is a marketing act upon which your success depends. Review every step, from how your receptionists answer to the message on the bottom of your invoices, and ask what you could do differently to attract and keep custom-ers. Make every employee a marketing person.”

Maybe it’s time for your agency ownership to assess the receptionist position. This doesn’t mean buying an automated voice system. In fact, that’s often a bad move from the custom-er’s point of view. But it could mean raising the salary and perks of the receptionist job (How about offering the best parking spot?) so you attract high-level people. In some agencies, it might mean hiring a second receptionist. And it could mean that you stop using that position as a “safe haven” for people who can’t cut it as a customer service representative. If they don’t like to deal with the public, don’t put them at the front desk.

Trusted Choice agencies know that in brand-ing, every brand touch-point matters.

from trustedchoice.com

How is your receptionist perceived by your customers?

Don’t take your

telephone grantedfor

Ask your customers to talk about a critical com-ponent — any critical component — of their commercial general liability package, and they probably won’t be able to answer you. Why is that? Isn’t the product important?

Sure it is. But it’s not the most important “brand touch-point” for your agency. Ask your customers to talk about what they perceive to be a critical component of your agency, and they’ll mention your people. And if you were to probe further, they’ll probably start with your receptionist.

The receptionist? You bet! This individual is on the phone all day with your customers — your very best customers as well as your not-so-best customers. Don’t take that key position, the phone warrior, for granted.

In his excellent book, The 33 Ruthless Rules of Local Advertising, author Michael Corbett says, “Too many companies never put themselves in the consumer’s shoes. If they did, they wouldn’t allow their phone receptionist to make it so dif-ficult for consumers to do business with them.”

It’s about a commitment to the customer. All employees need to share that vision.

Corbett discusses what must happen around your advertising for your firm to be success-ful. Before you cut a check to the local cable TV operator or direct-mail printer to drum up new business, Corbett offers some questions that are appropriate for agency owners to ask themselves:

• Can the person answering your phone make a compelling response to the caller’s requests?

• Have you told your phone receptionist, or anyone who answers your phone, that 83 percent of effective phone communications occurs in the tone of voice?

• Does your receptionist answer your phone no later than the third ring?

• How much training has the person an-swering your phone had in taking care of people who call your business?

• Does your receptionist like talking to people? Is he or she smiling while talk-ing on the phone?

• Does your receptionist consider people who phone with questions or com-plaints a bother, an interruption or a pain?

Go to www.Trusted-Choice.com/agents for more branding tips.

MAIA staff profile:

What is your educational background?Last year, I obtained my certificate in theological counseling. I’m now trying to save money to go back and finish my bachelor’s degree.

Tell us about a typical work day for you.There is never a typical day in insurance. Every day is a new adventure.

What do you enjoy most about your job?No day seems to ever repeat itself. I like doing different things and meeting new people.

What was your first job?The summer I turned 14, I cleaned the school. It wasn’t much fun scraping gum off the chairs and tables.

What has been your most significant accomplishment as a professional?Obtaining my insurance license. Most of you know how hard that test is!

Who has had the biggest influence on your career?My family has always encouraged me, even when I was not sure I could do it. They were right there cheering me on.

Tell us about your family.I have two awesome and handsome boys with my husband Chris. Damian is 18 and

a freshman in college, and Logan is 16 and a junior in high school. I look forward to having grandchildren someday.

Do you have any pets?No, I have a petting zoo filled with my furry family. We have four dogs: Goliath, a Lab mix; Wicket, a pomeranian-sheltie mix; Banshee, half malamute and half husky; and Titan, half Lab and half bull mastiff. We have three cats, Angel, Murphy and Opie. We have a fish, a bird (Tweety) and a chinchilla (Fred Flinstone). All but two of our animals are rescue pets.

What is a goal you’re still trying to accomplish?Finishing college is my personal goal.

Whose biggest fan are you?Chris, who is an awesome husband to me and a wonderful father, and my kids. I am so proud of the men my children have become.

If you were reborn as an animal, what would you want to be?A wolf. They are free, majestic creatures, loyal and protective, and they will do anything for their pack.

What are some qualities you value in a person?Honesty, intelligence, kindness, God fearing, funny and loving.

Monica MizeJoined MAIA: October 2007Title: Customer Service Representative

Monica in BriefFavoritesFood: Anything I don’t have to cookColor: BlueMusic: My iPod has everything from Michael Jackson to Demon Hunter to ‘80s hair bands.TV Show: Pretty Little Liars and The Big Bang TheoryMovie: The Lost Boys, Silver Bullet, The Never Ending Story and Lord of the Rings

Below Left: Monica’s husband Chris and sons, Logan (l) and Damian.

Below Right: The MAIA insurance department

november-december 2012 missouriagent 23

The Certified Insurance Service Representa-tives Program announced the expansion of course offerings for the prestigious designa-tion. This expansion allows participants to select from a variety of courses, based on their personal preference, to earn the CISR designation.

The new options give participants the op-portunity to choose five of the nine courses to specialize in a certain area or mix and match courses to diversify their learning. The new expansion includes:

Commercial linesCommercial Casualty I: commercial general

liability; additional insuredsCommercial Casualty II: business auto policy;

workers’ compensation; excess liabilityInsuring Commercial Property: commercial

property; time element; commercial inland marine

Personal linesInsuring Personal Auto Exposures: personal

automobile exposures and coveragesInsuring Personal Residential Property: home-

owners coverage forms and dwelling firePersonal Lines Miscellaneous: watercraft; rec-

reational vehicles; business activities; and personal umbrella and excess

Related professional topicsAgency Operations: major revision 2012Elements of Risk Management: the five steps

of the risk management processLife & Health Essentials: life and health insur-

ance concepts

To earn the CISR designation, a participant will need to complete the course and pass the final exam for any five of the nine courses. Eight of the nine courses will be available dur-ing MAIA’s 2013 schedule. Visit us online at www.missouriagent.org and click the master calendar link to register for any class. The new courses provide current CISRs excellent update options and are being filed for state CE credit.

program expands to

Personal ResidentialNov. 7, 2012, SpringfieldNov. 14, 2012, IndependenceDec. 4, 2012, ChesterfieldDec. 6, 2012, Cape Girardeau

Commercial Casualty IFeb. 6, 2013, SpringfieldMarch 7, 2013, Cape GirardeauJuly 30, 2013, Chesterfield

Commercial Casualty IIFeb. 20, 2013, Blue SpringsJune 11, 2013, SpringfieldAug. 8, 2013, Cape Girardeau

Commercial PropertyMarch 5, 2013, ChesterfieldJune 25, 2013, Blue Springs

William T. Hold SeminarApril 2, 2013, ChesterfieldOct. 1, 2013, Blue Springs

Personal ResidentialApril 23, 2013, SpringfieldMay 9, 2013, Blue SpringsMay 29, 2013, Chesterfield

Personal Lines MiscellaneousJune 4, 2013, Jefferson CityOct. 30, 2013, Springfield

Agency OperationsAug. 7, 2013, SpringfieldSept. 12, 2013, Blue SpringsSept. 17, 2013, ChesterfieldSept. 19, 2013, Jefferson City

Elements of Risk ManagementAug. 21, 2013, Chesterfield

Personal Auto ExposuresNov. 14, 2013, Blue SpringsDec. 3, 2013, ChesterfieldDec. 5, 2013, Jefferson City

MAIA CISR Schedule 2012-2013

MAIA CIC Schedule 2012-2013Commercial CasualtyNov. 28-Dec. 1, 2012,

IndependenceFeb. 27-March 1, 2013,

Blue Springs

Agency ManagementJan. 30-Feb. 1, 2013,

St. Charles

Commercial PropertyApril 17-19, 2013, St. CharlesNov. 6-8, 2013, Blue Springs

James K. Ruble Graduate Seminar

May 15-16, 2013, Osage BeachSept. 25-26, 2013, St. Charles

Personal LinesJune 19-21, 2013, Springfield

Life & HealthAug. 14-16, 2013, Jefferson

City

CISR 9 choices

Register online at www.missouriagent.org.

24 missouriagent november-december 2012

specialfocus productsandservices

Amy J. Hoffmaneditor, MAIA coverage gaps to sales management. The “Ask

an Expert” feature allows you to submit a spe-cific question to the experts on the VU faculty.

Be active in the industryYou can operate a mom-and-pop on Main Street, but your business

will suffer if you don’t have a foot in the broader industry. MAIA’s annual conferences combine networking opportunities with education and other benefits.

The Small Agency Conference, held each March in Columbia, is a gathering of agency per-sonnel from small to mid-sized Missouri agencies where all employees are welcome. A huge trade show is one of the highlights of this conference, and the Idea Lab is a popu-lar arena to ex-change thoughts on agency auto-mation and tech-nology topics.

The Young Agents Confer-ence is a favorite way for young and new producers to kick off the summer enjoying fellowship and education in a relaxed, family friendly atmosphere.

The Leadership Conference is the cream of the crop for networking among the state’s most suc-cessful and experienced leaders throughout the industry. This conference is aimed at managers, owners and principals, and regulatory and gov-ernment officials are often in attendance.

As a conscientious agent, you should take an active role in government affairs. On both state and federal levels, industry-related proposals are constantly developed and discussed. MAIA and your national associations lead the way in politi-cal advocacy by maintaining strong presences in the Missouri General Assembly and the U.S. Con-gress. You can support these efforts by making contributions to MAPAC, InsurPac and PIAPAC, the associations’ political action committees. We also sponsor Day at the Capitol in Missouri and take a delegation of agents to the national po-litical summits each spring.

1 25tips for a successful agency

Know your productIn this fast-paced, self-serve world, your best asset is your expertise. Clients come to you because you can translate the jargon and assess their needs.

MAIA can help you back that promise with a well-rounded approach to education.

Three designation programs are available for every agency employee, from the CSR to the experienced producer. The Certified Insur-ance Services Representative designation is aimed at CSRs and newer producers. With new classes available in 2013, the CISR program has more to offer than ever.

The Certified Insurance Counselor designa-tion is intended for more experienced pro-ducers and managers. The three-day classes in this program present in-depth analyses of advanced coverages. The CIC designation is a promise to your clients that you can handle their complex risks. Both programs offer con-tinuing education credit with each course.

Finally, the Associate in Insurance Produc-tion designation, awarded through comple-tion of the Elite Force Sales Training School, is for producers who are relatively new to both sales and the insurance industry. This program, offered biennially at MAIA Headquarters, gives students a comprehensive overview of insurance sales.

The Risk Specialist Series is a program that offers niche-based product information to help you grow your book of business and

expand your expertise. Examples include “Insuring Public Entities,” “Insuring Con-tractors,” and our next class to be held in January 2013, “Technology Trends for Insurance Agencies.” Expert instructors lead these two-day seminars, which are usually approved for CE credit.

Live classes are the heart of insurance education, but the best agencies have re-

sources at their fingertips every day. The Big “I” Virtual Risk Consultant allows producers to explore specific coverage markets. Among the resources it offers are checklists, marketing tools and minimum recommended coverages for more than 650 different industries.

The Virtual University is another Big “I” tool. On it, you’ll find articles authored by industry experts, addressing everything from

november-december 2012 missouriagent 25

specialfocus productsandservices

Cover your assetsYou know it. You preach it. But do you practice it? Your agency is teetering on the edge of fail-ure if you don’t have errors and

omissions insurance from a respected and proven carrier, as well as good risk management practices.

MAIA offers E&O coverage through the two best choices in the business*: Westport Insur-ance Co. and Utica Mutual Insurance Group. Both companies offer policies tailored to meet your agency’s specific needs. They are recog-nized throughout the industry for their finan-cial strength and stability.

To help you keep premiums low and man-age risk in your agency at the same time, MAIA presents E&O seminars three times a year. These seminars are approved for ethics CE credit and loss-control credit with Westport and Utica.

Westport clients have access to the E&O Hap-pens website, which offers claims prevention tools, coverage checklists, sample agency pro-cedure manuals, educational articles and other resources.

Finally, MAIA can help you make sure that nothing slips through the cracks by writing an insurance agency umbrella policy through Swiss Re or Penn National with limits up to $10 million over the primary E&O policy.

Be awareThe face of communication is changing so fast you may have a hard time recognizing it, but as a businessperson, you must keep up

with industry news and developments. Wheth-er it’s implementation of the new health care law or the latest best practices for Real Time transactions, MAIA has the information you need to know and the format you want.

Missouri Agent is a hard-copy magazine, which mails six times per year to every voting member. It is a valuable combination of educational articles, commentary and indus-try news.

The monthly electron-ic newsletter, the Agents NewsLine, is e-mailed each

month. Short and timely articles with links to more detailed information keep you up-to-date but require minimal time.

If you’d rather get your information on de-mand, check out the MAIA website, Facebook page and live chat feature. The website has all the information you need about news, associa-tion services, and upcoming events and classes. If you have a question while you’re there, just hit the “Live Chat” button on the bottom of the page. MAIA’s Facebook page is where you’ll get reminders about MAIA registration deadlines, links to industry news and other tidbits to keep you in touch.

Sell itIf you know your product, are active in the industry, have strong E&O coverage and are in touch with the business

world, your agency has a great backbone. Now’s the time to focus on boosting your agency’s sales.

MAIA member agencies are auto-matically enrolled in the Trusted Choice branding program, created by IIABA to give independent agents a strong voice and increase consumer awareness of the independent system. With Trusted Choice, it doesn’t matter how many employees you have or where you hang your shingle: You can be part of a national brand.

Most of the resources available through Trust-ed Choice are completely free. The Marketing Reimbursement Program will even pay you back for agency supplies and website redesign, which incorporate the Trusted Choice logo.

A new tool available through IIABA, Project CAP, works hand-in-hand with Trusted Choice to offer bundled marketing programs, which help agencies build consumer friendly websites and create public relations plans.

A second phase of Project CAP, still in de-velopment, is a consumer website, which

will connect shoppers with independent agencies in their areas and offer online quotes. More information on this tool will be available soon.

*Alternate markets also available.

3

4

5

tips for a successful agency

26 missouriagent november-december 2012

Products and Services

specialfocus productsandservices

IIABA and PIA Federal Legislative Confer-ences, Spring 2013

CSR Development Conference, Nov. 8-9, 2012

Mid-America Tech-nical Conference, Nov. 4-6, 2012

Agency Compliance Lun-cheons, Fall 2013

Crawfish Feast, March 20, 2013Missouri Trusted Choice Big “I” Championship,

Summer 2013

Agency MarketingContact MAIA’s Lindsay Griffin.

Trusted Choice Branding Program TC Mizzou Tiger Sports Ad Campaign TC Marketing Reimbursement Program TC Tag-Ready Ads for Radio, TV and Print TC Consumer Articles TC Mobile AppInformation-on-Hold NetworkProject CAPLogos (Trusted Choice, IIABA and PIA)Member Marketing Activity Center

Agency Information and ResourcesContact MAIA’s Amy Hoffman.

Missouri Agent (bimonthly magazine)www.missouriagent.org (MAIA website)Agents NewsLine (electronic newsletter)Membership Directory (online)Education BulletinFree Legal ConsultationPersonal Assistance from

MAIA StaffLegislative and Special

Updates on Timely Issues

Virtual University (with the “Ask an Expert” feature)

E&O Happens Loss Control Website

Big “I” Advan-tage Virtual Risk Consultant

Best Practices Research and Publications

Agents Council for Technology

Insurance Coverage for AgenciesContact MAIA’s Leona Loethen or Theresa

Flippin.

Errors and Omissions Insurance: property-casu-alty and life-health

Life InsuranceAccidental Death and DismembermentDental and Vision InsuranceLong-Term DisabilityShort-Term DisabilityEmployment Practices LiabilityAgents Umbrella Program

Insurance Coverage for ClientsContact MAIA’s Monica Mize or Kelli Kloeppel.

Personal Umbrella CoverageIn-Home Business PolicyFlood Insurance: write-your-own programBig “I” Markets

Non-Insurance Products and Services

Contact MAIA’s Kelli Kloeppel.

BankDirect and Capital Finance Premium Fi-nancing Programs

Motor Vehicle Reports and Driver Monitoring Products

Employee Testing ServiceCareer CenterRetirement ServicesInsurBanc

Educational OpportunitiesContact MAIA’s Emily Koenigsfeld.

CIC: Certified Insurance Counselor ProgramCISR: Certified Insurance Services Representa-

tive ProgramRisk Specialist SeriesContinuing Education and Specialized

SeminarsE&O Loss Control SeminarsElite Force Sales Training School: new class be-

gins May 2013CIC Scholarships

Conferences and Special EventsContact MAIA’s Jeanne Blomberg.

Leadership Conference (annual state conven-tion), July 17-19, 2013

Small Agency Conference, March 21-22, 2013Young Agents Conference, June 2-4, 2013Day at the Capitol, March 6, 2013

MAIA contact

information:

Phone: 573-893-4301

Toll Free in Mo: 800-617-3658.

Fax: 573-893-3708

www.missouriagent.org

november-december 2012 missouriagent 27

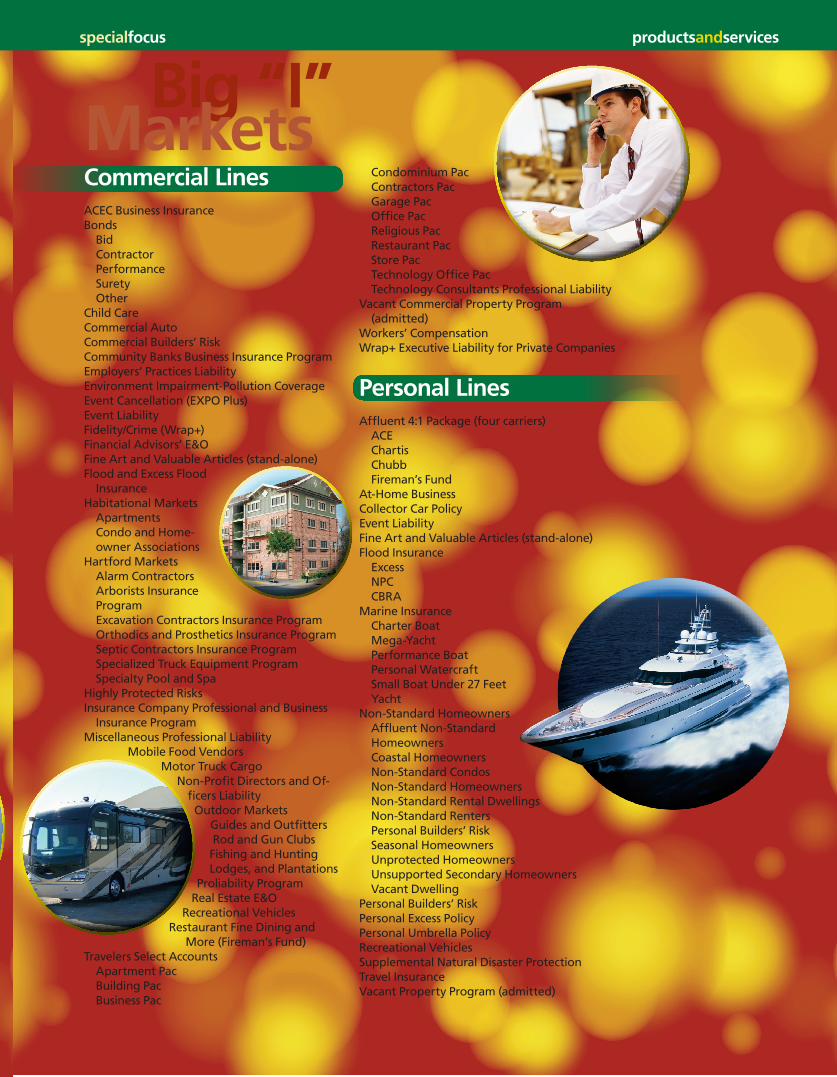

Big “I” Markets

specialfocus productsandservices

Commercial LinesACEC Business InsuranceBonds

BidContractorPerformanceSuretyOther

Child CareCommercial AutoCommercial Builders’ RiskCommunity Banks Business Insurance ProgramEmployers’ Practices LiabilityEnvironment Impairment-Pollution CoverageEvent Cancellation (EXPO Plus)Event LiabilityFidelity/Crime (Wrap+)Financial Advisors’ E&OFine Art and Valuable Articles (stand-alone)Flood and Excess Flood

InsuranceHabitational Markets

ApartmentsCondo and Home-owner Associations

Hartford MarketsAlarm ContractorsArborists Insurance ProgramExcavation Contractors Insurance ProgramOrthodics and Prosthetics Insurance ProgramSeptic Contractors Insurance ProgramSpecialized Truck Equipment ProgramSpecialty Pool and Spa

Highly Protected RisksInsurance Company Professional and Business

Insurance ProgramMiscellaneous Professional Liability

Mobile Food VendorsMotor Truck Cargo

Non-Profit Directors and Of-ficers LiabilityOutdoor Markets

Guides and OutfittersRod and Gun ClubsFishing and Hunting Lodges, and Plantations

Proliability ProgramReal Estate E&O

Recreational VehiclesRestaurant Fine Dining and

More (Fireman’s Fund)Travelers Select Accounts

Apartment PacBuilding PacBusiness Pac

Condominium PacContractors PacGarage PacOffice PacReligious PacRestaurant PacStore PacTechnology Office PacTechnology Consultants Professional Liability

Vacant Commercial Property Program (admitted)

Workers’ CompensationWrap+ Executive Liability for Private Companies

Personal LinesAffluent 4:1 Package (four carriers)

ACEChartisChubbFireman’s Fund

At-Home BusinessCollector Car PolicyEvent LiabilityFine Art and Valuable Articles (stand-alone)Flood Insurance

ExcessNPCCBRA

Marine InsuranceCharter BoatMega-YachtPerformance BoatPersonal WatercraftSmall Boat Under 27 FeetYacht

Non-Standard HomeownersAffluent Non-Standard HomeownersCoastal HomeownersNon-Standard CondosNon-Standard HomeownersNon-Standard Rental DwellingsNon-Standard RentersPersonal Builders’ RiskSeasonal HomeownersUnprotected HomeownersUnsupported Secondary HomeownersVacant Dwelling

Personal Builders’ RiskPersonal Excess PolicyPersonal Umbrella PolicyRecreational VehiclesSupplemental Natural Disaster ProtectionTravel InsuranceVacant Property Program (admitted)

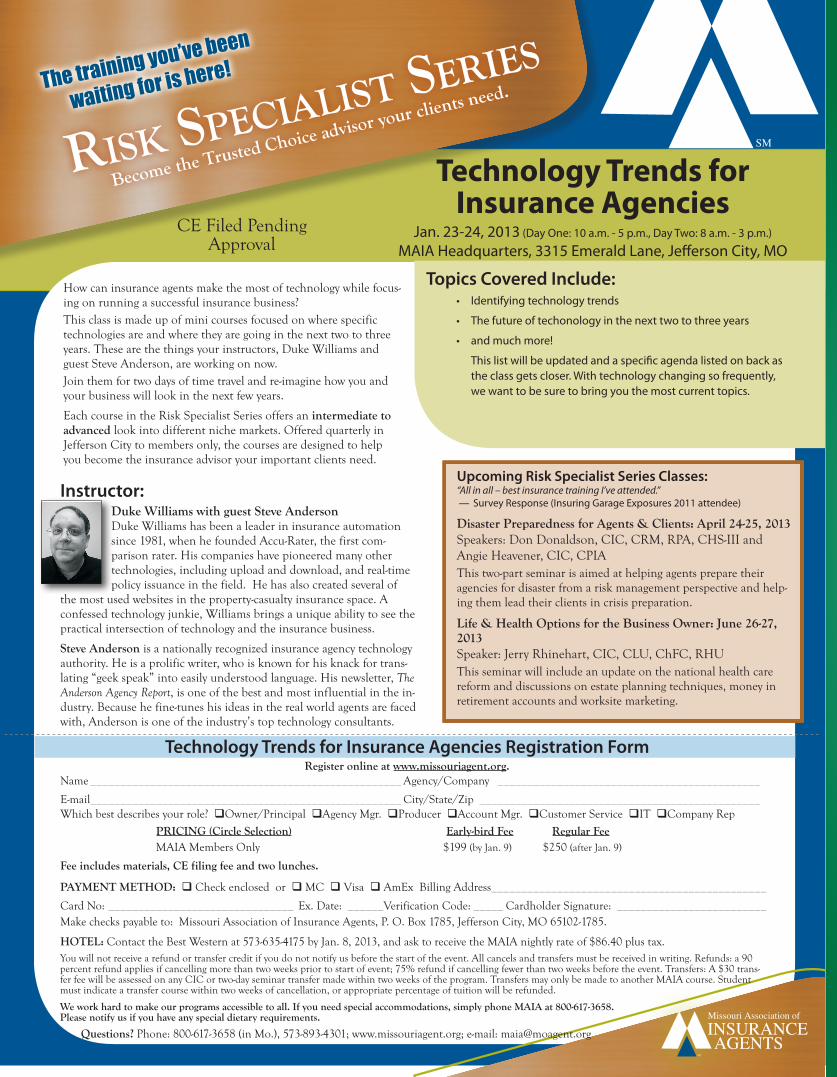

How can insurance agents make the most of technology while focus-ing on running a successful insurance business?This class is made up of mini courses focused on where specific technologies are and where they are going in the next two to three years. These are the things your instructors, Duke Williams and guest Steve Anderson, are working on now.Join them for two days of time travel and re-imagine how you and your business will look in the next few years.

Each course in the Risk Specialist Series offers an intermediate to advanced look into different niche markets. Offered quarterly in Jefferson City to members only, the courses are designed to help you become the insurance advisor your important clients need.

Technology Trends for Insurance Agencies Registration FormRegister online at www.missouriagent.org.

The training you’ve been

waiting for is here!

Risk specialist seRies

Become the Trusted Choice advisor your clients need.

Instructor:Duke Williams with guest Steve Anderson Duke Williams has been a leader in insurance automation since 1981, when he founded Accu-Rater, the first com-parison rater. His companies have pioneered many other technologies, including upload and download, and real-time policy issuance in the field. He has also created several of

the most used websites in the property-casualty insurance space. A confessed technology junkie, Williams brings a unique ability to see the practical intersection of technology and the insurance business.

Steve Anderson is a nationally recognized insurance agency technology authority. He is a prolific writer, who is known for his knack for trans-lating “geek speak” into easily understood language. His newsletter, The Anderson Agency Report, is one of the best and most influential in the in-dustry. Because he fine-tunes his ideas in the real world agents are faced with, Anderson is one of the industry’s top technology consultants.

Technology Trends for Insurance Agencies

Jan. 23-24, 2013 (Day One: 10 a.m. - 5 p.m., Day Two: 8 a.m. - 3 p.m.)

MAIA Headquarters, 3315 Emerald Lane, Jefferson City, MO

• Identifyingtechnologytrends

• Thefutureoftechonologyinthenexttwotothreeyears

• andmuchmore!

Thislistwillbeupdatedandaspecificagendalistedonbackastheclassgetscloser.Withtechnologychangingsofrequently,wewanttobesuretobringyouthemostcurrenttopics.

Topics Covered Include:

Upcoming Risk Specialist Series Classes: “All in all – best insurance training I’ve attended.” — SurveyResponse(InsuringGarageExposures2011attendee)

Disaster Preparedness for Agents & Clients: April 24-25, 2013 Speakers: Don Donaldson, CIC, CRM, RPA, CHS-III and Angie Heavener, CIC, CPIAThis two-part seminar is aimed at helping agents prepare their agencies for disaster from a risk management perspective and help-ing them lead their clients in crisis preparation.

Life & Health Options for the Business Owner: June 26-27, 2013 Speaker: Jerry Rhinehart, CIC, CLU, ChFC, RHUThis seminar will include an update on the national health care reform and discussions on estate planning techniques, money in retirement accounts and worksite marketing.

CE Filed Pending Approval

You will not receive a refund or transfer credit if you do not notify us before the start of the event. All cancels and transfers must be received in writing. Refunds: a 90 percent refund applies if cancelling more than two weeks prior to start of event; 75% refund if cancelling fewer than two weeks before the event. Transfers: A $30 trans-fer fee will be assessed on any CIC or two-day seminar transfer made within two weeks of the program. Transfers may only be made to another MAIA course. Student must indicate a transfer course within two weeks of cancellation, or appropriate percentage of tuition will be refunded.

We work hard to make our programs accessible to all. If you need special accommodations, simply phone MAIA at 800-617-3658. Please notify us if you have any special dietary requirements.

Questions? Phone: 800-617-3658 (in Mo.), 573-893-4301; www.missouriagent.org; e-mail: [email protected]

Name ____________________________________________________ Agency/Company ____________________________________________

E-mail____________________________________________________ City/State/Zip _______________________________________________Which best describes your role? Owner/Principal Agency Mgr. Producer Account Mgr. Customer Service IT Company Rep

PRICING (Circle Selection) Early-bird Fee Regular Fee MAIA Members Only $199 (by Jan. 9) $250 (after Jan. 9)

Fee includes materials, CE filing fee and two lunches.

PAYMENT METHOD: Check enclosed or MC Visa AmEx Billing Address ______________________________________________

Card No: _______________________________ Ex. Date: ______Verification Code: _____ Cardholder Signature: _________________________ Make checks payable to: Missouri Association of Insurance Agents, P. O. Box 1785, Jefferson City, MO 65102-1785.

HOTEL: Contact the Best Western at 573-635-4175 by Jan. 8, 2013, and ask to receive the MAIA nightly rate of $86.40 plus tax.

november-december 2012 missouriagent 29

MAIA 2012-13 committeesBudget and Finance CommitteeThis committee works with the executive vice president on all financial matters and monitors the budget and financial poli-cies of the association. Each year, it presents an annual budget

to the board of directors.

Chairman Randy Baker, T.R. Baker Insurance Agency, Kennett

Doug Clift, Bowersox Insurance Agency Co., St. Louis

Staff Liaison Larry Case, MAIA

Communications and Technology CommitteeThis is a newly formed committee, the result of a merger of the Public Relations Committee and the Technology Commit-tee. It utilizes print and electronic media to enhance the im-age and profile of independent agents while simultaneously working to help agents develop their own communications and technology platforms with the goal of increased profits through branding and workflows. The committee focuses on social networking, website optimization, and various forms of on- and offline advertising, as well as office protocols such as Real Time, download and working with an agency manage-ment system.

Chairman Kevin Krueger, Capstone Insurors, Bolivar

Pauli Clariday, Cameron Insurance Cos., Cameron

Chad Connell, Connell Insurance, BransonShane Davolt, G M Peters Agency, LibertyRoss Ingersoll, Ingersoll Insurance Agency,