47

MMC/NERA Operational Risk : An Assessment of Global Market Practices March 18, 2003

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | terence-alan-flynn |

| View: | 219 times |

| Download: | 4 times |

MMC/NERA

Operational Risk : An Assessment of Global Market Practices

March 18, 2003

MMC/NERA – Operational Risk Management: Phase II Study 2

Table of Contents

• Introduction

• Approaches to Operational Risk Management

• Capture of Operational Risk Loss Data

• Capital Allocation for Operational Risk

• Transfer of Operational Risk

• Conclusions

IntroductionIntroduction

MMC/NERA – Operational Risk Management: Phase II Study 4

NERA Is A Marsh & McLennan Company (MMC)

Guy Carpenter Reinsurance Broking & Services• Reinsurance broking advice and services• Sophisticated natural hazard modeling• Guy Carpenter Catastrophe Index• Instrat - Dynamic financial

modeling for insurersNational EconomicResearch Associates(NERA)Economic Consulting• Risk Assessment and Analysis• Risk Modeling and Valuation• Mitigation Strategy Design and Execution• Legal Liability and Regulatory Advisory

William M. MercerHR Consulting• Advice and services to

manage HR risks• Advice and services to manage

treasury risks

Consulting2001 Revenue: $2.1 billion

Risk & Insurance Services2001 Revenue: $5.2 Billion

MarshInsurance Broking & Risk Management Services• Insurance broking and advice• Risk control and business continuity planning

services for operational, property, casualty andIT risks

• Risk information systems and technology• Structuring and placement of innovative risk

financing alternatives`

Mercer ManagementConsultingStrategy Consulting• Analysis and expertise in strategic risks• Analysis and expertise in supply chain risks• Modeling and research capabilities for

business risks

Investment Management2001 Revenue: $2.6 billion

Putnam InvestmentsInvestment Services• $328 Billion in assets managed

(average 2001)• International portfolio management

MMCTotal 2001 Revenues: $9.9 billion

MMC/NERA – Operational Risk Management: Phase II Study 5

Introduction: Operational Risk Capabilities

• MMC has assembled an Operational Risk Team from experts across its different entities in an effort to provide cutting edge expertise and advice for its clients on the complex and ongoing issue of operational risk. As part of this effort the MMC Operational Risk Team has been developing a number of tools to assist its clients in the financial sector in addressing some ongoing concerns related to operational risk, including:

– Operational Risk Management Benchmarking Project

– MMC Operational Risk Loss Event Database

– Analytic quantification methods for Operational Risk within financial institutions incorporating qualitative and quantitative estimation techniques

– Analysis of insurance effectiveness for covering operational risk

MMC/NERA – Operational Risk Management: Phase II Study 6

Introduction: Review of Global Operational Risk Benchmark

• MMC’s Operational Risk Management Global Benchmark study was conducted in two phases. Phase I sought to provide comparative data on current operational risk management practices at financial institutions and identify likely trends in the industry as captured in four distinct categories:

– Approaches to Operational Risk Management (people, processes and systems)

– Capture of Operational Risk Loss Data

– Economic and Regulatory Capital Allocation

– Risk Transfer

• During Phase I, over 75 interviews were conducted in conjunction with written questionnaire surveys with global banking institutions. Interviews were conducted worldwide between June, 2002 and August, 2002. Participating institutions were located in the United States, Canada, Europe, Japan, Australia and South Africa.

• MMC presented results to the Risk Management Group of the Basel Committee on Banking Supervision in Paris in September, 2002.

• MMC presented individual benchmark presentations to 45 participants

MMC/NERA – Operational Risk Management: Phase II Study 7

Introduction: Phase II Study

• MMC’s Operational Risk: Emerging Best Practices Study seeks to provide regulators and participating firms extended data on outstanding issues relating to operational risk management. These issues include industry practices in resources and processes, the development of economic capital allocation models for operational risk, and the inclusion of insurance mitigation in operational risk management practices.

• Over 30 interviews were conducted with global banking institutions during phase II resulting in NERA having conducted over 100 interviews over both studies. The Phase II institutions were selected from the Phase I study for follow-up due to their robust thinking in operational risk management. Interviews were conducted worldwide between December, 2002 and January, 2003. Participating institutions were located in the United States, Canada, the United Kingdom, Europe, Japan, and Australia.

• Throughout both studies, MMC presented results to individual country regulators including:– The Federal Reserve System (New York and Washington, DC)

– Office of the Comptroller of the Currency (OCC)

– Bank of Japan

– Canadian Office of the Superintendent of Financial Institutions (OSFI)

– Financial Services Authority

– De Nederlandsche Bank

– Deutsche Bundesbank

– Australian Prudential Regulation Authority

MMC/NERA – Operational Risk Management: Phase II Study 8

North America North America UK/Europe UK/Europe Japan/Australia

AmSouth Bank Marshall & Illsley Corp.

Abbey National Group Deutsche Bank Australia and New Zealand Bank

Bank of America Corp. Merrill Lynch ABN Amro Group Dexia Group Bank of Tokyo-Mitsubishi

The Bank of New York Co. MBNA Corp. Allied Irish Bank Dresdner Bank Bank of Yokohama, Ltd.

Bank One Corp. Riggs Bank BBVA S.A. Erste Bank der Osterreichischen Sparkassen AG

Bank of Queensland Ltd.

Bear, Stearns & Co. U.S. Bancorp Banco Santander ING Bank Bendigo Bank Ltd.

Citigroup Inc. Union Bank of California

Bank of Ireland Intesa BCI Commonwealth Bank of Australia

Comerica, Inc. Wachovia Corp. Barclays Bank KBC Group Macquarie Bank Ltd.

First Tennessee National Corp.

Wells Fargo & Co. Bayerische Hypotheken und Vereinsbank (HVB Group)

Lloyds TSB Mizuho Holdings, Inc.

Hibernia Corp. Bank of Montreal Bayerische Landesbank Girozentrale

Nordea AB National Australia Bank, Inc.

JP Morgan Chase & Co. Bank of Nova Scotia Caisse des Depots et Consignations

Royal Bank of Scotland Sumitomo Mitsui Banking Corp.

KeyCorp Canadian Imperial Bank of Commerce (CIBC)

Capitalia Gruppobancario San Paolo – IMI Suncorp-Metway Ltd.

Legg Mason, Inc. RBC Financial Group Commerzbank Societe Generale Groupe St. George Bank Ltd.

M&T Bank Toronto-Dominion Bank

Credit Agricole Standard Chartered Bank UFJ Holdings, Inc.

South Africa South Africa Credit Lyonnais Swedebank Westpac Banking Corp.

ABSA The Nedcor Group Credit Suisse Group UBS AG

First Rand Bank Standard Bank of South Africa

Danske Bank Westdeutsche Landesbank

Participating Institutions

Approaches to Operational Risk Management

Approaches to Operational Risk Management

MMC/NERA – Operational Risk Management: Phase II Study 10

Resources in Centralized Operational Risk Management Function

• Firms have agreed on common definitions with the Basel Committee and have subsequently established independent operational risk functions.

• Other than the smallest domestic banks, firms have enacted operational risk management functions universally.

Does your firm have an operational risk management function?

90%

3%7%

Current Planned No Response

MMC/NERA – Operational Risk Management: Phase II Study 11

Resources in Centralized Operational Risk Management Function

• Firms have bolstered their operational risk management functions over the past few years, and many believe they have reached a critical mass.

– Around 80% of firms in the study have more than 5 people employed at the corporate level in the centralized operational risk management function. This number tends to be bolstered even more with other support functions who have the identified operational risk management duties. These typically include:

IT support and programmers

Information security

Centralized security

Insurance

What resources (FTEs) are employed in the corporate level in the centralized operational risk management

function?

21%

33%

8%

38%

Less than 5 5-10 10-15 More than 15

MMC/NERA – Operational Risk Management: Phase II Study 12

Extent of Operational Risk in Business Decisions• 63% of the banks responding said that operational risk was considered in

overall business and strategy decisions.– A number of methods of consideration were noted, though the most common were methods

based on examination of how the economic capital charge for operational risk would be impacted by a change in business plans/strategy.

– A large number of the respondents noted that before a new business or product is launched it must undergo an operational risk assessment.

A few banks noted that operational risk attracted special attention in considering and managing acquisitions.

Does your bank consider operational risk when making overall business/strategy decisions?

63%

38%

Yes No

Does your bank consider operational risk when making overall business/strategy decisions?

15

54

9

2

43

6

0

2

4

6

8

10

12

14

16

Overall North America Europe Other

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 13

Comparisons & Progress Over the Last 6 Months• Firms use operational risk considerations in strategy decisions to a similar

extent as firms with strategic policies outlined in the Phase I Study. The same firms that outlined such policies in Phase I, now implement those policies in strategic decision-making.

– In the Phase I study, 67% of the firms cited policies that outlined operational risk management use in overall strategic objectives.

– The assessment of policies outlining strategic objectives and subsequent strategic considerations resulted in the following breakdown from the same 24 firms in Phase I and Phase II of the study.

PHASE I PHASE II

Does your bank consider operational risk when making overall business/strategy decisions?

63%

38%

Yes No

Do your firm's policies clearly define the objectives of ORM and how they relate to overall strategic objectives?

67%

33%

Current Planned

MMC/NERA – Operational Risk Management: Phase II Study 14

Operational Risk Reports• Firms’ operational risk reporting varies widely but always includes some cut

of senior management, usually through an operational risk committee. – Business Units are often integral in creating the reporting, often being derived from risk

self-assessments or collection efforts from the business units. The dissemination is usually through individual Business Unit Managers.

The 17% who do not provide reports to business units largely have fundamentally and geographically diverse business lines – the reports created are general company-wide reviews and the business lines are left to their management to decide unit reporting.

All Boards of Directors are aware of operational risks, though several firms are waiting for data and review experience to support ongoing reporting to the Board.

Are operational risk reports provided to the Board of Directors?

79%

21%

Yes No

Are operational risk reports provided to business units?

83%

17%

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 15

Comparisons & Progress Over the Last 6 Months• Firms have extended their operational risk reporting to include all firms reporting

to senior management and extensive reporting to the Board of Directors.– The reporting lines noted in both studies resulted in the following breakdown from the same 24

firms in Phase I and Phase II of the study.

PHASE I PHASE II

Does the Board of Directors periodically review operational risk management reports, including

operational risk exposures and loss experience?

54%

42%

Current Planned

Does Senior Management periodically review operational risk management reports, including

operational risk exposures and loss experience??

83%

17%

Current Planned

Are operational risk reports provided to the Board of Directors?

79%

21%

Yes No

Are operational risk reports provided to Senior Management?

100%

0%

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 16

Operational Risk Reports

• Operational risk reports that usually are presented to an operational risk committee are often only changed slightly for the Board of Directors and business unit documents.

– At around 25% of the firms, reports were given quarterly to risk committees though firms ranged from monthly to annually.

– More than half of the operational risk reports to the Board were presented annually as a section of the risk report and quarterly as a review from a group-wide risk review.

– Reports typically included:

Analysis and commentary on the operational risk environment, including Basel initiatives

Top operational risks for the group and specific business units’ risks

Representations of risk controls/action plans to combat the stated risks

Reports of specific losses, causes and outcomes

Reports of loss database developments

Reports of self-assessment data

Expectations and “hot spots” for future operational risk management

MMC/NERA – Operational Risk Management: Phase II Study 17

The Use of Self-Assessments

Is your firm utilitizing self-assessments in operational risk management?

79%

21%

Current Pilot

Is your firm utilitizing self-assessments in operational risk management?

19

755

1 2 2

7

-

5

10

15

20

Overall North America UK/Europe Japan/Australia

Current Pilot

• The depth and detail of the self-assessments varied by firm and often varied within business units. The use of self-assessments in capital allocation signaled more depth and accuracy as business units were incentivized by capital allocation. In general, self-assessments were used to:

Creates scenarios for deriving distributions in a capital allocation model

Act as the basis of scorecards for business units, often adjusting business unit specific capital allocation

Monitoring tool for management, and contributor to expert scenario analysis for risk control

Act as the basis of allocating an aggregated pool of capital across the business units

Promote sound operational risk management that identifies problem areas and initiates action plans

MMC/NERA – Operational Risk Management: Phase II Study 18

Description of Risk Scorecards

Is your firm utilitizing scorecards in operational risk management?

67%

21%

13%

Current Pilot No Scorecard

• 67% of banks interviewed are currently using scorecards as a tool in managing operational risk.

– 15 of the 19 firms that have current self-assessment programs, also utilize scorecard systems.

– Scorecards give some firms a way of viewing risk versus the mitigants of risk, as well as probability and severity. It is used simply to find where inherent risks are high and where controls are not commensurate with the risk.

Is your firm utilitizing scorecards in operational risk management?

16

75

31 1 1

53

1 1

4

-2468

1012141618

Overall North America UK/Europe Japan/Australia

Current Pilot No Scorecard

MMC/NERA – Operational Risk Management: Phase II Study 19

Comparisons & Progress Over the Last 6 Months• Only 36% of all firms in the Phase I study used risk self-assessments or

scorecards to help determine economic capital for operational risk.– A comparison of banks that participated in both studies reveal that at least pilot scorecard and

self-assessments have been implemented where banks had planned to implement them.– The consideration of risk self-assessments or scorecards in capital allocation models resulted

in the following breakdown from the same 24 firms in Phase I and Phase II of the study.

PHASE I PHASE II

Does your firm use risk-self assessments or scorecards to help determine economic capital for

operational risk?

58%

8%

33%

Current Planned Anticipated

Is your firm utilitizing self-assessments in operational risk management?

79%

21%

Current Pilot

Is your firm utilitizing scorecards in operational risk management?

67%

21%

13%

Current Pilot No Scorecard

MMC/NERA – Operational Risk Management: Phase II Study 20

Key Risk Indicators, Risk Thresholds & Limits

• The majority of banks interviewed currently use Key Risk Indicators (KRIs) to manage operational risk on an ongoing basis. All of the banks that do not use Key Risk Indicators are either in the process of identifying and implementing them or are planning to undertake an effort to develop them in the foreseeable future.

– Banks are in the process of monitoring potential firm-wide KRIs, often relying on their own business units’ experiences in collecting KRIs.

Does your bank currently use KRIs to manage operational risk on an ongoing basis?

71%

29%

Yes No

Does your bank currently use KRIs to manage operational risk on an ongoing basis?

17

7

4

7

2 2 3

6

0

5

10

15

20

Overall North America Europe Other

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 21

Comparisons & Progress Over the Last 6 Months• The use of key risk indicators to proxy operational risk exposures in the

ongoing management of operational risk has expanded over the last six months.

– 54% of the firms that were in both studies were not actively using key risk indicators in Phase I, while the percentage dropped to just 29% who were not using them in the Phase II study.

– The use of key risk indicators resulted in the following breakdown from the same 24 firms in Phase I and Phase II of the study.

PHASE I PHASE II

Does your bank currently use KRIs to manage operational risk on an ongoing basis?

71%

29%

Yes No

Does your firm use risk indicators to proxy the level of operational risk exposure?

42%

8%

46%

Current Planned Anticipated

Capture of Operational Risk Loss Data

Capture of Operational Risk Loss Data

MMC/NERA – Operational Risk Management: Phase II Study 23

Operational Risk Loss Events: Types, Examples

• Most banks have begun collecting operational risk loss data generally adaptable to Basel guidelines:

Potential Loss Events

Discretionary losses

External fraud

Financing losses

Insurance claims

Internal fraud

Legal settlements

Policy violations

Processing losses

Trading losses

External effects

Natural Disasters

Management processes

Personnel/HR losses

Physical loss damage

Sales practices

Technology

Transaction and business processes

Unauthorized activities

Basel Level 1 Event Types

Internal Fraud

External Fraud

Employment Practices and Workplace Safety

Clients, Products, and Business Services

Damage and Physical Assets

Business Disruption and System Failures

Execution, Delivery and Process Management

MMC/NERA – Operational Risk Management: Phase II Study 24

How Long Have You Been Capturing Losses?

For how long has your firm been capturing operational loss events in its operational loss database?

21%

15%

27%

37%

Less than 1 Year 1-3 YearsGreater than 3 Years No Response

For how long has your firm been capturing operational loss events in its operational loss database?

14

7

4

25

6

12

7

10

4 42

18

7 7

43

0

5

10

15

20

25

30

Overall North America Europe Other

Less than 1 Year 1-3 YearsGreater than 3 Years No Response

For how long has your firm been capturing operational loss events in its operational loss database?

3

4 44

5

8 8

3 3 3

1

8

5

3

2

3

0

1

2

3

4

5

6

7

8

9

Under $75B $75B - $200B $200B - $500B Over $500B

Less than 1 Year 1-3 YearsGreater than 3 Years No Response

• Most firms have begun to systematically collect operational risk losses within the last 3 years – all firms with systems in place longer than that have generally just adjusted general ledger systems and use historical GL collections within the database.

MMC/NERA – Operational Risk Management: Phase II Study 25

Capture of the Basel Committee’s Historical Window

Is the historical window captured in your firm’s internal operational loss database at least three years?

40%

7%

52%

Yes No No Response

Is the historical window captured in your firm’s internal operational loss database at least three years?

27

108

35

9

17

9

52 3

0

9

0

5

10

15

20

25

30

35

40

Overall North America Europe Other

Yes No No Response

Is the historical window captured in your firm’s internal operational loss database at least three years?

7

9

5

8

9 9 9

3

1

0

1

6

0

1

2

3

4

5

6

7

8

9

10

Under $75B $75B - $200B $200B - $500B Over $500B

Yes No No Response

• Most firms do not yet have the three years of historic data proposed by the Basel Committee, although many have just started the data collection process and plan on having the historical data by 2006.

– “We question the veracity of going back to get data that far in the past, so while we don’t have the three years of data now, we will have it by 2006.”

MMC/NERA – Operational Risk Management: Phase II Study 26

Breadth and Scope of Data Collection Efforts• 52% of banks surveyed in Phase II have all business units currently

contributing to their operational loss databases. The majority of banks placed the ultimate responsibility on each business unit to report losses.

– While the thresholds for losses collected by banks varied from as high as $10,000 (US) to as low as one penny, the majority of banks are collecting all losses regardless of size.

– Some firms are struggling with issues related to timing. Firms expressed confusion on accounting for the date of a loss: on the day that the event occurs, the day that the bank finds out about it, or the date that the full loss is realized.

How comprehensive is your bank's internal loss data by business unit?

52%

13%

35%

CompleteAlmost CompleteMost, But Not All Business Units

MMC/NERA – Operational Risk Management: Phase II Study 27

Comparisons & Progress Over the Last 6 Months• Since the Phase I Study, firms have implemented more definite operational risk

management plans resulting in broader resources, reporting and database development.

– The assessment of breadth of data collection resulted in the following breakdown from the same 24 firms from Phase I and Phase II.

PHASE I PHASE II

– Losses are now collected by all of our Phase II participants, with over half of the participants believing that their collection processes are complete.

– The utilization of operational risk considerations in business decisions is growing slowly, but has maintained its importance in merger and acquisitions analyses.

Does yourfirm systematically collect internal operational loss data?

83%

17%

Yes No

How comprehensive is your bank's internal loss data by business unit?

52%

13%

35%

CompleteAlmost CompleteMost, But Not All Business Units

MMC/NERA – Operational Risk Management: Phase II Study 28

Determination and Tracking Losses in Market and Credit Risk

• Firms were generally evenly split in their method for dealing with operational losses associated with market and credit risk, and several noted the need for further regulatory guidance on the issue.

– The method for tracking operational risk losses associated with market and credit risk that is used by around a third of the firms is earmarking those events having an operational risk component to them but leaving them in the credit or market risk bucket for economic capital purposes.

– Earmarking these losses allows for both the ability to recognize the need for additional controls, and the opportunity to retroactively parse out operational risk losses once a clearly defined policy is put into place.

How does your firm track the operational risk losses related to market and credit activities?

29%

33%

21%

17%

Policy Clearly DeliniatesDetermined on a Case-by-Case BasisEach Loss is Earmarked and Left in Market and CreditHave Not Examined This Issue

Capital Allocation for Operational Risk

Capital Allocation for Operational Risk

MMC/NERA – Operational Risk Management: Phase II Study 30

Approaches to Calculating Economic Capital

• Firms have taken two different approaches to creating distributions for modeling economic capital:

– Some firms have implemented a loss distribution approach based mainly on internal data, external data or most often some combination of both.

– Other firms have implemented a loss distribution approach based mainly on scenario analysis, often taken from risk and control self-assessments:

Some scenarios are developed from analyses of internal loss events

Other scenarios are developed from analyses of external events with some rough scaling and filtering of possible events.

– The few firms that have not implemented a model for capital distribution are moving towards one of these methods this year.

What approach are you using to calculate economic capital allocation?

46%

54%

Loss-data based LDAScenario-based LDA

What approach are you using to calculate economic capital allocation?

11

64

13

7

3 31

02

468

10

1214

Overall North America UK/Europe Japan/Australia

Loss-data based LDA Scenario-based LDA

MMC/NERA – Operational Risk Management: Phase II Study 31

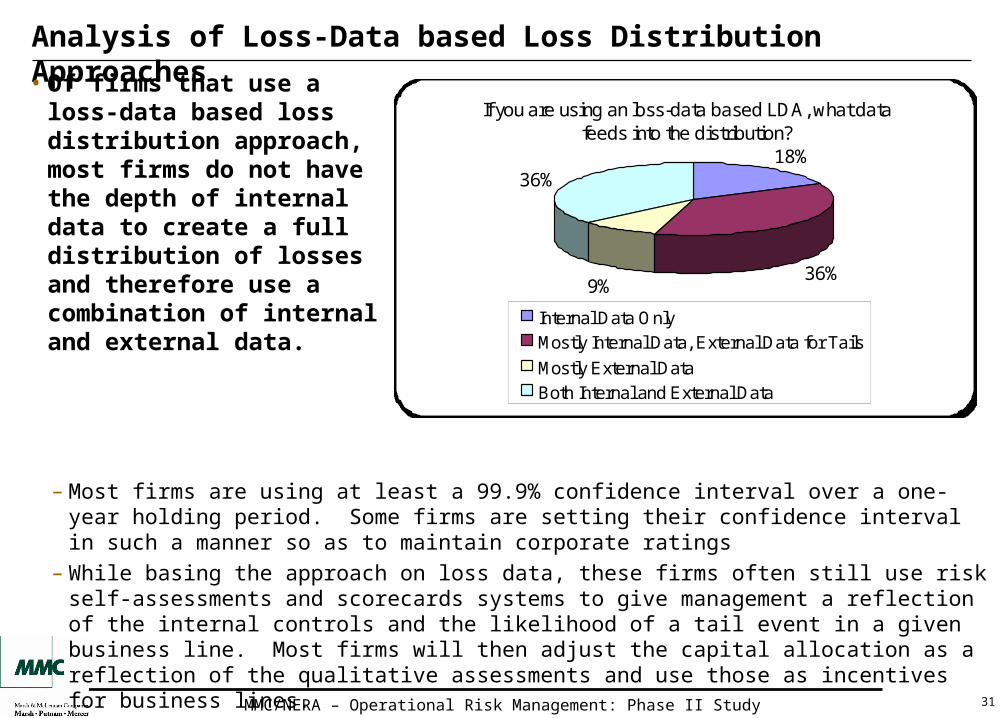

Analysis of Loss-Data based Loss Distribution Approaches

• Of firms that use a loss-data based loss distribution approach, most firms do not have the depth of internal data to create a full distribution of losses and therefore use a combination of internal and external data.

If you are using an loss-data based LDA, what data feeds into the distribution?

18%

9%

36%

36%

Internal Data Only

Mostly Internal Data, External Data for Tails

Mostly External Data

Both Internal and External Data

– Most firms are using at least a 99.9% confidence interval over a one-year holding period. Some firms are setting their confidence interval in such a manner so as to maintain corporate ratings

– While basing the approach on loss data, these firms often still use risk self-assessments and scorecards systems to give management a reflection of the internal controls and the likelihood of a tail event in a given business line. Most firms will then adjust the capital allocation as a reflection of the qualitative assessments and use those as incentives for business lines.

MMC/NERA – Operational Risk Management: Phase II Study 32

Analysis of Scenario Based LDA Calculations• Of firms that use a scenario-based

approach, nearly 70% of the firms derive scenarios from a self-assessment process, while the remainder do top-down scenarios elicited from senior management.

• All of the firms in the study have collected internal operational risk losses though firms using scenario approaches have used the loss data in different ways:

As support for framing of scenarios in the self-assessment process or in reviewing and auditing self-assessments some firms have used the data to back-test and validate their scenario analyses.

lf you are using a scenario approach, what are the scenarios based on?

69%

31%

Bottom-up Scenarios, Typically from Self-assessmentsTop-down Scenarios from Experts or External Data

lf you are using a scenario approach, how do you use internal data?

46%38%

15%Support for ScenariosSmall Part of Current ModelCollected for Future Modeling

MMC/NERA – Operational Risk Management: Phase II Study 33

Comparisons & Progress Over the Last 6 Months• Since the Phase I Study, firms’ economic capital allocation models have

evolved with much more emphasis placed on quantitative approaches relying on loss data.

– In the Phase I study, 29% of the firms used loss-data based distribution approaches (Quantitative), while that number jumped to 46% several months later.

– The assessment of capital allocation models resulted in the following breakdown from the same 24 firms in Phase I and Phase II of the study.

PHASE I PHASE II

– The evolution of loss databases in the last half-year contribute to the loss-data based LDA approaches taken in Phase II of the study.

What approach are you using to calculate economic capital allocation?

46%

54%

Loss-data based LDAScenario-based LDA

If you currently assess economic capital for operational risk, what method describes your assessment?

29%

71%

Quantitative/Actuarial ApproachQualitative/Expert Opinion Approach

MMC/NERA – Operational Risk Management: Phase II Study 34

Use of Internal Data• All firms in the study are currently collecting internal data and plan to use it in

operational risk modeling by 2006.– However, today only half of the firms in the study are currently using internal data in their

economic capital allocation models:

50% of the firms use internal data as a direct input into a distribution model. Some firms use internal data exclusively, while others use it as a very small input into a more diversified distribution

25% of the firms are collecting data with the expectation that it will be useful for modeling after several more year’s worth of data for depth and breadth of operational risk losses

25% of the firms use internal data to support internal scenario analysis as well as to validate or back-test the expectations generated from different models; these firms also expect to use internal data as a key input in future capital allocation models

How are you currently using internal operational risk loss data?

50%

25%

25%

Part of Current ModelWarehousing for Future ModelingUsed for Scenario Support/Validation/Future Modeling

How are you currently using internal operational risk loss data?

12

6

4

6

4

1 1

6

2 2 22

-

2

4

6

8

10

12

14

Overall North America UK/Europe Japan/Australia

Part of Current ModelWarehousing for Future ModelingUsed for Scenario Support/Validation/Future Modeling

MMC/NERA – Operational Risk Management: Phase II Study 35

External Data – Comparisons & Progress Over the Last 6 Months• Nearly 80% of firms in the study use external data, while the vast majority of

those firms use it to simply benchmark themselves.– Most firms still have problems filtering and scaling external data, making the use of it in

modeling difficult. – The consideration of external data utilization in capital allocation models resulted in the

following breakdown from the same 24 firms in Phase I and Phase II of the study.

PHASE I PHASE II

How are you currently using external operational risk loss data?

54%

21%

25%

Analyzing Scenarios/BenchmarkingPart of Current ModelNot Using External Data

Does your firm use external loss data as a supplement to its internal loss data?

29%29%

42%

Current Planned No

MMC/NERA – Operational Risk Management: Phase II Study 36

Recognition of Internal Control Factors

• 54% of the banks surveyed adjust their economic capital allocation for operational risk according to some measurement of the effectiveness of internal controls

– Most of those banks that did not account for internal controls in their economic capital allocations were planning on instituting some adjustment in the future, though a few banks did not see any value in the exercise.

– A number of banks insisted that the ability to reduce capital in this manner provided a good incentive for banks to improve their controls.

Does your bank's allocation of economic capital for operational risk take into account internal controls?

54%

46%

Yes No

Does your bank's allocation of economic capital for operational risk take into account internal controls?

13

45

11

45

2

4

0

2

4

6

8

10

12

14

Overall North America Europe Other

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 37

What Constitutes a “Tail” Risk?

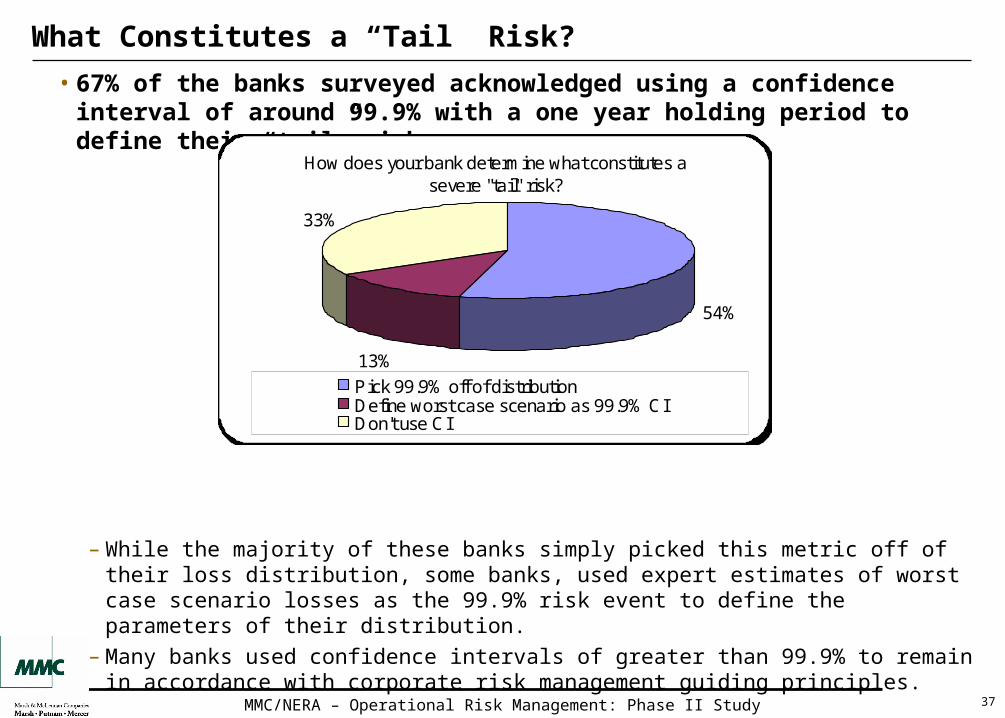

• 67% of the banks surveyed acknowledged using a confidence interval of around 99.9% with a one year holding period to define their “tail” risks.

– While the majority of these banks simply picked this metric off of their loss distribution, some banks, used expert estimates of worst case scenario losses as the 99.9% risk event to define the parameters of their distribution.

– Many banks used confidence intervals of greater than 99.9% to remain in accordance with corporate risk management guiding principles.

How does your bank determine what constitutes a severe "tail" risk?

54%

33%

13%

Pick 99.9% off of distributionDefine worst case scenario as 99.9% CIDon't use CI

Transfer of Operational RiskTransfer of Operational Risk

MMC/NERA – Operational Risk Management: Phase II Study 39

Use of Insurance in Operational Risk Management• The utilization of insurance to mitigate operational risk is an evolving issue that

most firms have not reached a consensus on, but which all firms agree should have a place in the future of operational risk management.

– Outstanding issues remain in the development of insurance as a mitigant in operational risk. These issues include:

The development of modeling capabilities is evolving and thus how to include insurance in the models is unclear.

The regulators have yet to identify the extent to which insurance will be included in the mitigation of operational risk capital.

It is difficult to purchase insurance right now in the markets with very high deductibles and premiums.

There is no singular definition for a tail event, and while it includes fraud in some cases, in other cases large property losses from weather-related events are considered the worst-case scenarios.

Finally, there is a split in the analytical rigor of firms, some of whom develop sophisticated quantitative modeling, while others believe traditional and conventional approaches to insurance are currently sufficient to meet mitigation requirements.

MMC/NERA – Operational Risk Management: Phase II Study 40

Use of Insurance as a Mitigant in Calculating Economic Capital• The utilization of insurance mitigation in capital allocation models is now

beginning to grow with over a quarter of the firms in the study considering its effects in their internal models.

– The timing of when it is considered varies from independent inclusion into Monte Carlo simulations to qualitative consideration by business units during the self-assessment process.

“For each category and each department, we have the loss data and the insurance appropriate to that category and the coverage and limits on lower and upper parameters.”

“In the self-assessment process, the business units should tell us how the risks are mitigated by insurance and report only a net risk.”

Does your firm consider the risk-mitigating effect of insurance in its capital allocation model?

27%

73%

Yes No

Does your firm consider the risk-mitigating effect of insurance in its capital allocation model?

85

2

22

107

51

0

5

10

15

20

25

Overall North America UK/Europe Japan/Australia

Yes No

MMC/NERA – Operational Risk Management: Phase II Study 41

Comparisons & Progress Over the Last 6 Months• Since the Phase I Study, firms’ economic capital allocation models have

evolved resulting in much more focused consideration of the risk-mitigating effects of insurance.

– 57% of all the firms in the Phase I study did not know or did not respond to the extent which insurance reduces economic capital, with only 12% saying it worked in their capital allocation models. The remaining 31% of firms noted no reduction from insurance mitigation.

– The consideration of insurance into evolving models resulted in the following breakdown from the same 30 firms in Phase I and Phase II.

PHASE I PHASE II

– The 41% of firms in Phase I with no expressed view have now formed their positions which trends towards more inclusion of insurance in the economic capital models.

To what extent does your use of insurance reduce the economic capital you allocate to operational risk?

21%

41%

38%

WellNot Well/No ReductionDon't Know/No Response

Do you anticipate the incorporation of insuranc in your economic capital model?

27%20%

53%

Already IncorporatedForesee Future IncorporationNo Future Incorporation

MMC/NERA – Operational Risk Management: Phase II Study 42

Mapping of Insurance into Loss Event Types

Does your firm have methods in place to map insurance to loss event types?

30%

70%

Yes No

Does your firm consider the risk-mitigating effect of insurance in its capital allocation model?

9

5

2

21

97

52

0

5

10

15

20

25

Overall North America UK/Europe Japan/Australia

Yes No

• Most firms acknowledge that they track the types of insurance available and the types of events they cover, but most have not formally mapped those to specific loss event types.

– Some firms have not mapped insurance because of time constraints while other firms note that insurance policies can fall into multiple categories, making the exercise moot.

MMC/NERA – Operational Risk Management: Phase II Study 43

Operational Risk Losses and Insurance Performance• Firms have encountered a large variety of operational risk losses, with

insurance performing well within its expectations.– Most firms are not experiencing the large losses from which they could evaluate the

effectiveness of insurance in major tail risk situations, but insurance has performed well in addressing losses actually encountered.

– Smaller firms contend that their tail events are not large enough to warrant buying the high deductible insurances, but rather consist of unexpected property losses or system breakdowns.

– Insurance has performed very well in traditional policies, including resounding support for the property insurance regarding World Trade Center losses.

– Typical loss experiences include:

Property damages from various sources including external events and fire

Weather-related property losses due to floods, tornados, etc.

Internal fraud

External fraud

MMC/NERA – Operational Risk Management: Phase II Study 44

Operational Risk Losses and Insurance Performance• Firms have encountered some losses that are not insurable or lawsuits that

have made recovery untimely or unattainable.– Several firms have encountered regulatory fines as their largest operational risk losses and

there is no insurance available to protect against that risk.

– Firms contend that the lawsuits necessary to recover losses from some events are prohibitively expensive, resulting in a loss because recovering it would cost more than the loss itself.

– The markets are so expensive in insurance right now that most firms feel the insurance industry needs to work with them to try and meet their evolving operational risk needs, though several firms remain skeptical of insurance offsets.

– Typical loss experiences include:

Trading losses due to untimely execution

Regulatory fines

Credit default events

Reporting errors

Various lawsuits

ConclusionsConclusions

MMC/NERA – Operational Risk Management: Phase II Study 46

Conclusions

• Financial institutions’ approach to operational risk management has been evolving rapidly over the past 6 months, and emerging best practices have resulted in several key areas:

– Resources are growing to a critical mass

– Reporting has grown and familiarity with operational risk is pervading the banks

– Self-assessment systems and data collection have been implemented in preparation for 2006

• Two disparate approaches have been adopted in economic capital allocation, though firms vary widely still on how they incorporate self-assessment data, scorecard data, internal and external loss data, key risk indicators and insurance considerations. The two approaches are:

– A loss data-based Loss Distribution Approach

– A scenario-based Loss Distribution Approach

• Insurance is beginning to be incorporated into capital allocation models, and has performed well in many ways, though its utilization in operational risk management is still largely undetermined.

MMC/NERA – Operational Risk Management: Phase II Study 47

Contact Information• Robert Mackay

Senior Vice PresidentNational Economic Research Associates, Inc.1255 23rd St., NWWashington, DC 20037Tel: (202) 466-9291Email: [email protected]

• Bradley P. ZiffVice PresidentNational Economic Research Associates, Inc.1166 Avenue of the AmericasNew York, NY 10036Tel: (212) 345-7717Email: [email protected]

• Geremy Connor Analyst

National Economic Research Associates, Inc.1166 Avenue of the AmericasNew York, NY 10036Tel: (212) 345-6773Email: [email protected]

• Chris Bolton Analyst

National Economic Research Associates, Inc.1255 23rd St., NWWashington, DC 20037Tel: (202) 466-9205Email: [email protected]