23

Mobile Gaming Forum - 25 January 2012 Mobile Gaming: State of the European Market Jeremy Copp, Vice President Mobile Europe [email protected], +44 7876 567742

| Date post: | 01-Nov-2014 |

| Category: |

Business |

| Upload: | romain-fonnier |

| View: | 723 times |

| Download: | 0 times |

Mobile Gaming Forum - 25 January 2012

Mobile Gaming: State of the European Market

Jeremy Copp, Vice President Mobile Europe

[email protected], +44 7876 567742

2 © comScore, Inc. Proprietary and Confidential.

Agenda

– Mobile Media Landscape

Usage, Devices & Market Drivers

Smartphone Trends

Mobile Gaming

Who Does What & How?

Which Handsets?

Who are the Consumers?

Monetisation

Advertising

Paid Downloads & Freemium

In Game Purchases

Takeaways

3 © comScore, Inc. Proprietary and Confidential.

Mobile Media Landscape

Usage, Devices & Market Drivers

Smartphone Trends

4 © comScore, Inc. Proprietary and Confidential.

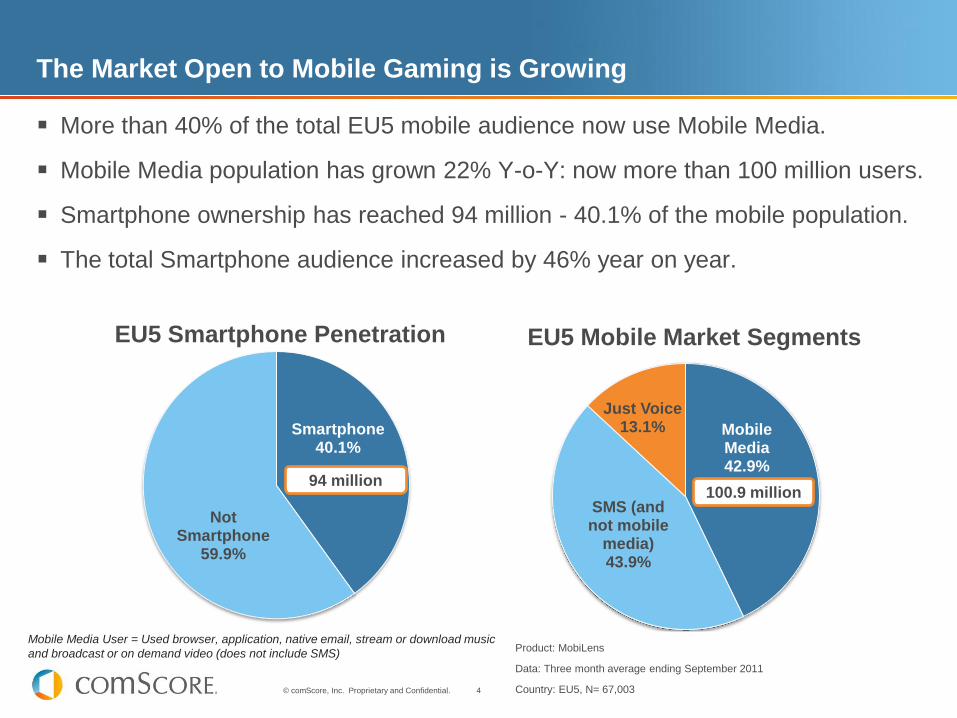

The Market Open to Mobile Gaming is Growing

More than 40% of the total EU5 mobile audience now use Mobile Media.

Mobile Media population has grown 22% Y-o-Y: now more than 100 million users.

Smartphone ownership has reached 94 million - 40.1% of the mobile population.

The total Smartphone audience increased by 46% year on year.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

Mobile Media User = Used browser, application, native email, stream or download music

and broadcast or on demand video (does not include SMS)

Smartphone 40.1%

Not Smartphone

59.9%

EU5 Smartphone Penetration

94 million

Mobile Media 42.9%

SMS (and not mobile

media) 43.9%

Just Voice 13.1%

EU5 Mobile Market Segments

100.9 million

5 © comScore, Inc. Proprietary and Confidential.

Smartphone Ownership a Key Market Driver

Since December 2010, smartphones have dominated new mobile phone purchases

Now more than 59% of devices sold in EU5 are smartphones

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

72% 70% 70% 69% 62% 59%

52% 49% 47% 42% 41%

28% 30% 30% 31% 38% 41%

48% 51% 53% 58% 59%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011

% A

cq

uir

ed

Dev

ice in

Mo

nth

Acquired Device in Month by Type

Not Smartphone Smartphone

6 © comScore, Inc. Proprietary and Confidential.

Google’s Android Has Rapidly Grown its Smartphone Market Share

In the past year, Android increased its market share from 8.3% in September 2010

to its current 26.2%.

Apple has increased its share from 19.4% to 20.7% while all other major operating

systems saw their share decline.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

51.8%

33.9%

8.3%

26.2%

19.4% 20.7%

7.9% 9.5%

10.6%

6.3%

2.0% 3.4% 0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11

% S

mart

ph

on

e I

nsta

lled

Base

Smartphone Operating Systems - Trend

Symbian Google Apple RIM Microsoft Other

- 4%

+361%

+56%

+74%

-13%

+158%

% YoY

Growth

7 © comScore, Inc. Proprietary and Confidential.

Mobile Media User = Used browser, application, native email, stream or download music

and broadcast or on demand video (does not include SMS)

Smartphone Owners are Over 237% More Likely to Use Mobile Media

than Non-Smartphone Users

Smartphones have revolutionized the market for Mobile Media. More than 94% of Apple’s user base

consume Mobile Media.

Google, Apple and RIM platform users over-index on consumption behavior, compared to the

Smartphone average.

Mobile owners with Microsoft and Symbian based devices are less likely to use Mobile Media than the

average Smartphone user.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

94.3%

86.0% 84.8%

68.5%

51.6%

74.2%

22.0%

89.1%

76.5% 75.4%

56.5%

40.0%

64.6%

14.4%

85.7%

76.2% 72.0%

57.9%

40.3%

63.8%

15.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Apple Google RIM Microsoft Symbian Smartphone Not Smartphone

%P

en

etr

ati

on

Mobile Media Consumption by Operating System

Used connected media (except SMS) Used application (except native games) Used browser

8 © comScore, Inc. Proprietary and Confidential.

Mobile Gaming

Who Does What & How?

Which Handsets?

Who Are the Consumers?

9 © comScore, Inc. Proprietary and Confidential.

Most Prevalent Installed Game Genres are Not Always Most Purchased

Most popular genres purchased are not always the same as the most popular installed

Action/adventure, board, card, strategy & casino games highest volume purchases

Arcade, card, strategy & word or number games largest installed volume

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

0

100

200

300

400

500

600

700

800

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Arc

ade

pu

zzle

Card

Str

ate

gy

Wo

rd o

r N

um

be

r

Retr

o a

rca

de

Bo

ard

Quiz

Racin

g

Action/a

dventu

re

Sp

ort

s

Casin

o

Sim

ula

tion

First pe

rson

sh

oote

r

Role

Pla

yin

g G

am

es

Music

/Rhyth

m

Kid

s/F

am

ily

Oth

er

Nu

mb

er

Pu

rch

ased

(000)

Nu

mb

er

Insta

lled

(000)

Most Popular Gaming Genres

Installed Purchased

10 © comScore, Inc. Proprietary and Confidential.

Distinct Audiences for Different Game Genres

Young, heavily male audience for action/adventure, RPG, sports and first person shooter games

Puzzles, card games, quizzes and board games attract an older audience more evenly spread

between genders

Musical and strategy games have a younger, more female demographic

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

Action/adventure

Arcade puzzle

Board

Card

Casino

First person shooter

Music/Rhythm

Role Playing Games

Quiz

Racing

Retro arcade

Kids/Family

Simulation

Sports

Strategy

Word or Number Other

15%

25%

35%

45%

55%

65%

10.0 12.0 14.0 16.0 18.0 20.0 22.0 24.0 26.0 28.0 30.0

% F

em

ale

Median Age

Demographic Profile of Installed Game Users

Size of bubbles = % of the market

Higher on chart = More female

Further to right = Older

11 © comScore, Inc. Proprietary and Confidential.

Consumers Continue to Play Mobile Games Regularly

Over 25% of mobile phone users (62m consumers) played a game in the month

Nearly 13m users play a game almost every day

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Almost every day At least once each week Once to three timesthroughout the month

Ever in month

Pro

po

rtio

n o

f T

ota

l A

ud

ien

ce (

%)

Frequency of Playing Games

12 © comScore, Inc. Proprietary and Confidential.

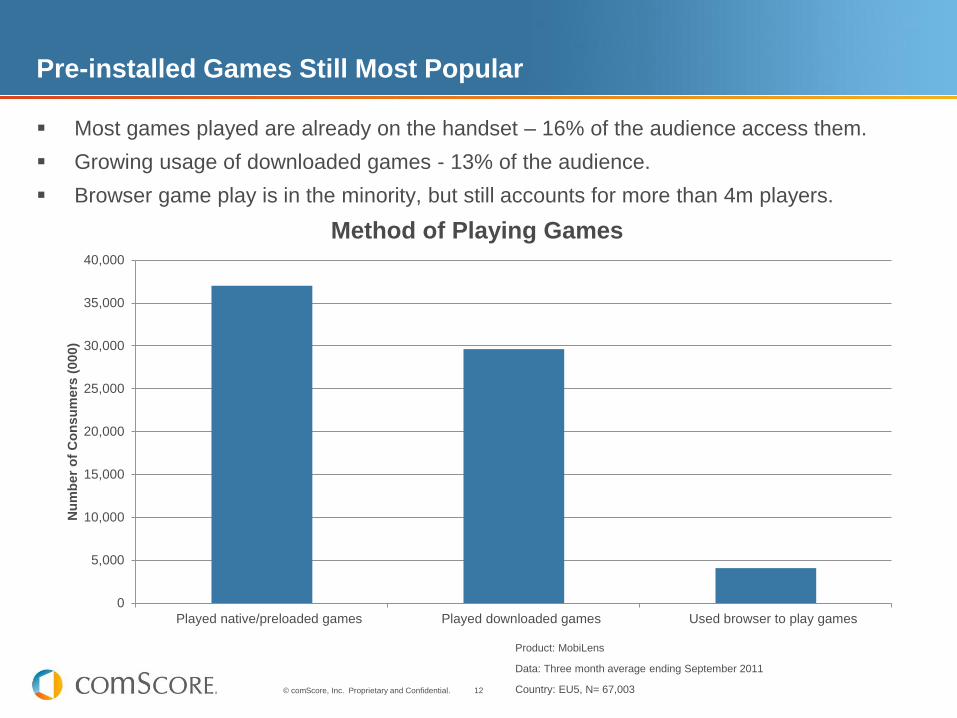

Pre-installed Games Still Most Popular

Most games played are already on the handset – 16% of the audience access them.

Growing usage of downloaded games - 13% of the audience.

Browser game play is in the minority, but still accounts for more than 4m players.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Played native/preloaded games Played downloaded games Used browser to play games

Nu

mb

er

of

Co

nsu

mers

(000)

Method of Playing Games

13 © comScore, Inc. Proprietary and Confidential.

Most Consumers Download Two or Fewer Games Per Month

More than 60% of downloaders added up to two games in the month

Heavy users account for 12% of downloaders, adding 5 or more games in the month

More than one third of those with games installed have five or more on their phone

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

12%

17%

18%

11% 7%

35%

Number of Games Installed

1

2

3

4

5

5+

33%

28%

17%

7%

3% 12%

Number of Games Downloaded in Month

1

2

3

4

5

5+

14 © comScore, Inc. Proprietary and Confidential.

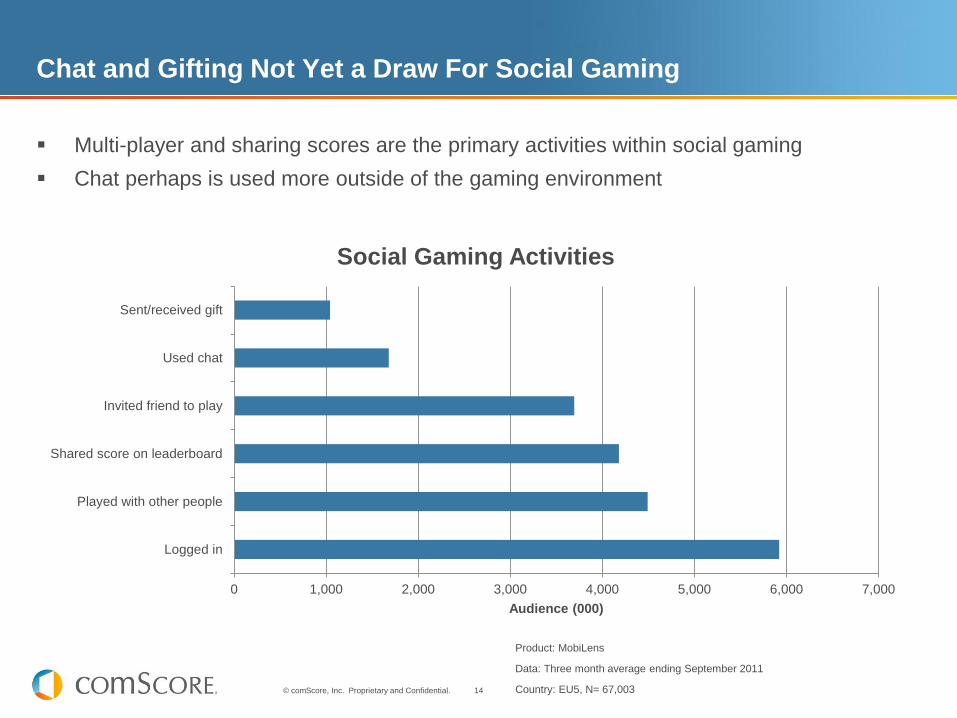

Chat and Gifting Not Yet a Draw For Social Gaming

Multi-player and sharing scores are the primary activities within social gaming

Chat perhaps is used more outside of the gaming environment

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Logged in

Played with other people

Shared score on leaderboard

Invited friend to play

Used chat

Sent/received gift

Audience (000)

Social Gaming Activities

15 © comScore, Inc. Proprietary and Confidential.

iPhone is the Mobile Gaming Device of Choice

iPhones predominate as gaming devices with more than 10m players.

53% of iPhone owners played a game – users of Android based devices show a similar

propensity with 45% playing

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

Handset Model Number Playing Games (000)

Apple - iPhone 4 16GB (Fourth Generation) [GSM] 3,466

Apple - iPhone 3G S 16GB (Third Generation) 1,528

Apple - iPhone 4 32GB (Fourth Generation) [GSM] 1,321

RIM - BlackBerry Curve 8520 1,318

Samsung - Galaxy S I9000 8GB 1,223

Apple - iPhone 3G S 32GB (Third Generation) 1,145

Nokia - 5800 XpressMusic 1,132

HTC - Desire [GSM] 969

Apple - iPhone 3G 16GB (Second Generation) 887

HTC - Wildfire [GSM] 831

Apple - iPhone 3G S 8GB (Third Generation) 789

Samsung - Galaxy S II 16GB (no NFC) 696

Samsung - Galaxy Ace S5830 588

HTC - Desire HD 568

Nokia – 5230 523

Samsung - S5230 521

HTC - Wildfire S [GSM] 515

16 © comScore, Inc. Proprietary and Confidential.

Monetisation

Advertising

Paid Downloads & Freemium

In Game Purchases

17 © comScore, Inc. Proprietary and Confidential.

74.2%

44.2%

39.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Mobile Media Social Networking Played Games

% S

mart

ph

on

e

Methods of Interacting

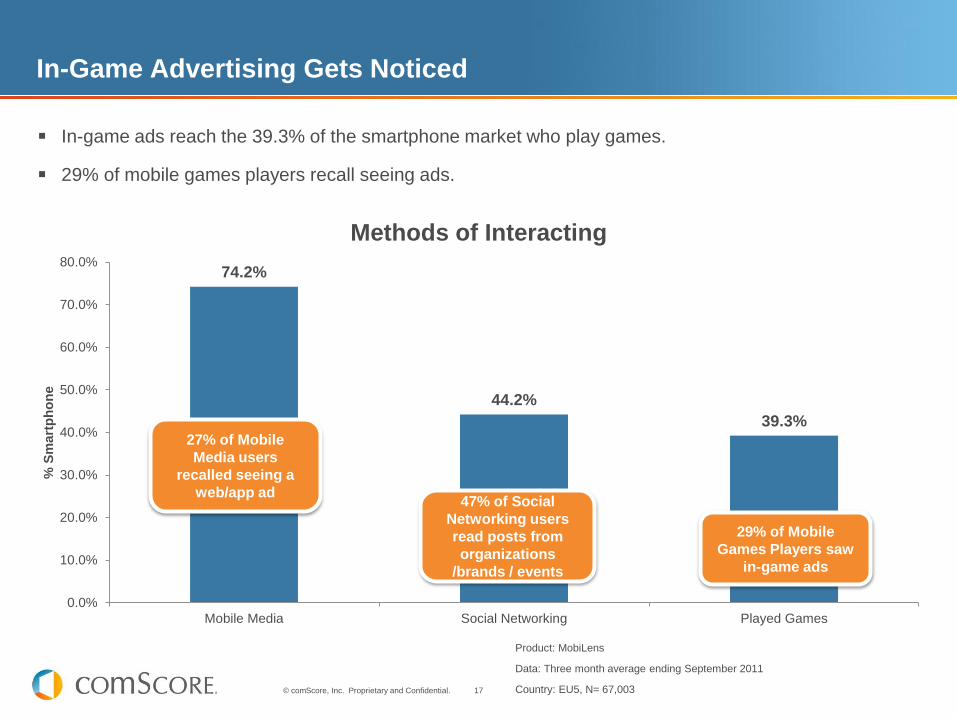

In-Game Advertising Gets Noticed

In-game ads reach the 39.3% of the smartphone market who play games.

29% of mobile games players recall seeing ads.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

27% of Mobile

Media users

recalled seeing a

web/app ad 47% of Social

Networking users

read posts from

organizations

/brands / events

29% of Mobile

Games Players saw

in-game ads

18 © comScore, Inc. Proprietary and Confidential.

Increasingly Users Download Trial Rather Than Purchase

Unsurprisingly more than half of consumers download games for free

Increasing proportion of users are downloading trial versions rather than purchasing games

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

27%

21%

52%

Game Download Methods

Trial only download

Purchased by paying a fee

Downloaded full version of game for free

19 © comScore, Inc. Proprietary and Confidential.

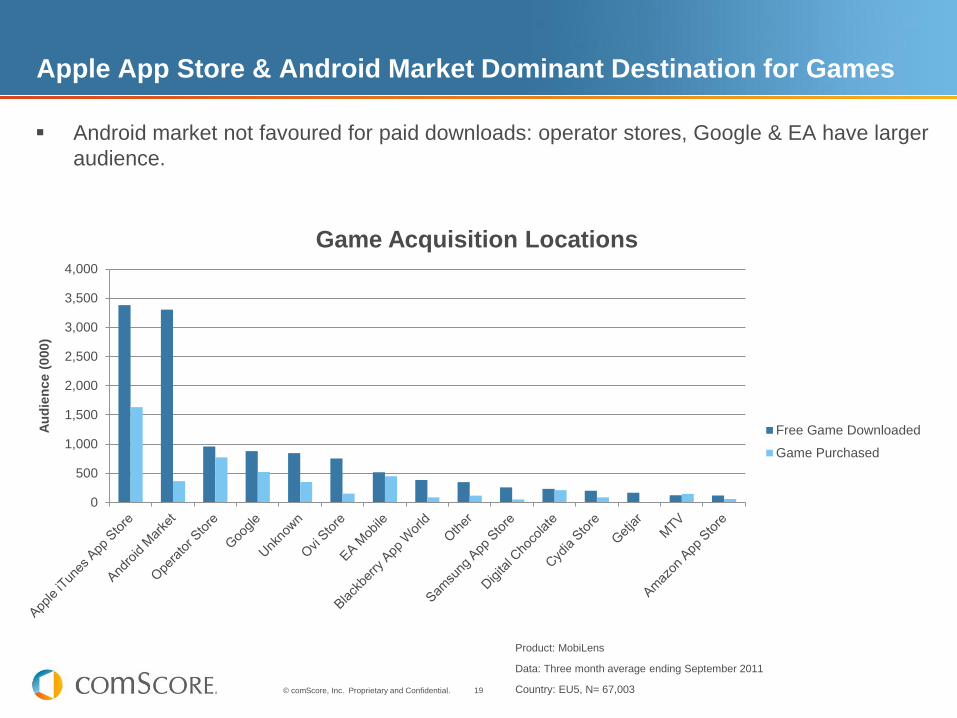

Apple App Store & Android Market Dominant Destination for Games

Android market not favoured for paid downloads: operator stores, Google & EA have larger

audience.

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Au

die

nce (

000)

Game Acquisition Locations

Free Game Downloaded

Game Purchased

20 © comScore, Inc. Proprietary and Confidential.

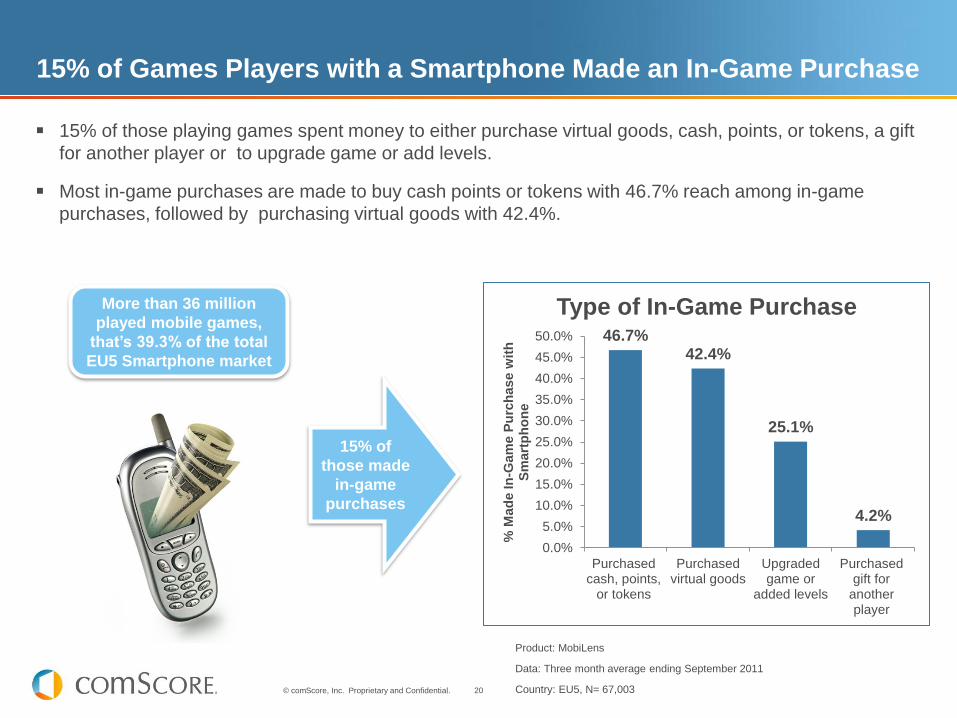

15% of Games Players with a Smartphone Made an In-Game Purchase

Product: MobiLens

Data: Three month average ending September 2011

Country: EU5, N= 67,003

15% of those playing games spent money to either purchase virtual goods, cash, points, or tokens, a gift

for another player or to upgrade game or add levels.

Most in-game purchases are made to buy cash points or tokens with 46.7% reach among in-game

purchases, followed by purchasing virtual goods with 42.4%.

15% of

those made

in-game

purchases

More than 36 million

played mobile games,

that’s 39.3% of the total

EU5 Smartphone market

46.7% 42.4%

25.1%

4.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Purchasedcash, points,

or tokens

Purchasedvirtual goods

Upgradedgame or

added levels

Purchasedgift for

anotherplayer

% M

ad

e In

-Gam

e P

urc

hase w

ith

S

mart

ph

on

e

Type of In-Game Purchase

21 © comScore, Inc. Proprietary and Confidential.

Takeaways

22 © comScore, Inc. Proprietary and Confidential.

Takeaways

The market for mobile gaming in Europe continues to grow – Ever more smartphone owners driving the update in gaming – More than 25% of mobile phone owners in Europe play games every month

The installed base of games & most popular download genres differ – Downloading becoming more popular but browser based games a minority – Ensure you understand the route to market for your products

There are distinct target audiences for different types of games – Know how to reach them with your marketing and delivery channels

The iPhone is a good bet as a target platform – Users have a high propensity to play games – Currently represent the highest volume platform for gamers in Europe – However, Android based phone users show similar characteristics

Monetise through in-game purchases or advertising – Paid downloads a decreasing proportion of the market

Consider the market carefully – how will you reach your target

audience? – The reality as revealed by measurement is often different from intuition