19

Mobile Payments Overview Technology and Competitive Landscape Dee O’Malley Senior Director, Financial Services Best Buy Co. July 10, 2013

Mobile Payments Overview Technology and Competitive Landscape

Dee O’Malley Senior Director, Financial Services Best Buy Co.

July 10, 2013

Upcoming MAG Educational Opportunities

• WEBINAR: Legal Update featuring Barrie Van Brackle August 14, 2013- 12:00pm-1:00pm CT Registration will be opening soon online at www.merchantadvisorygroup.org

• WEBINAR: Quarterly EMV Update September 2013 More information coming soon!

• Mark Your Calendars! Annual Conference-Celebrating 5 Years in the Big Easy October 7-9, 2013 Astor Crowne Plaza New Orleans New Orleans, LA

Registration Opens online in Mid-July

Contents

• What is a Mobile Payment?

• Mobile Commerce & Payment Trends

• Mobile Shopping Ecosystem

• Proximity Payment Technologies

• Payment Standards

• Mobile Wallet and Payment Data Risks

• Mobile Payment Transaction Flows

• Wallet Landscape

Mobile Purchases From a Retail

Website

Mobile Proximity Payments

at the POS

Mobile Proximity -Closed Loop

Payments

Mobile as the Point of Sale

The Mobile Payment Platform

Direct Carrier Billing

Mobile Web The Mobile Wallet The Mobile “Store Gift Card”

Every Smartphone is a Cash Register

The Everything Else Mobile Payment

Put it On My Bill

Purchasing Goods From a Website Utilizing an Internet Browser From a Smartphone

Paying for Things at a Store with a Mobile Device using NFC, 2D Bar Code or Other “Tap and Go” Technology

Usually a proprietary platform for a merchant to build a mobile payment application that can only be used at their locations. This has only been built for gift cards to date.

Merchants Using a Mobile Device to process a credit card payment. Very different from a mobile wallet

A catch-all category for mobile payment products allowing consumers to make purchases or send money to merchants or other consumers. Can be NFC, 2D, text message or other technology

Consumers buy ringtones, games or other digital content and place the charge on their cell phone bill

What is a Mobile Payment? • There are five types of mobile payments, each with different implications to merchant

systems, technologies, transaction processes, customer experiences and costs

• A mobile payment is a component of a larger mobile commerce experience

• Solutions such as those announced by MCX are a “mobile proximity payment” while

purchases on m.DOT and t.DOT are considered a dotcom transaction due to the process

by which payment credentials are applied to the checkout

m.Merchant

Mobile Commerce & Payments a growing part of the merchant-consumer interaction

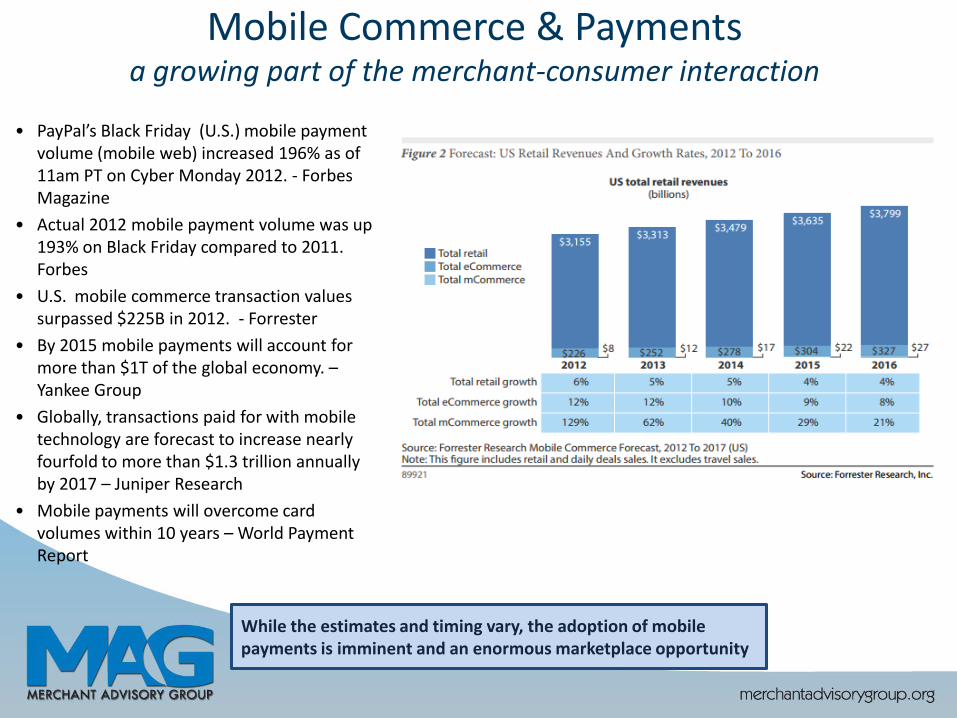

• PayPal’s Black Friday (U.S.) mobile payment volume (mobile web) increased 196% as of 11am PT on Cyber Monday 2012. - Forbes Magazine

• Actual 2012 mobile payment volume was up 193% on Black Friday compared to 2011. Forbes

• U.S. mobile commerce transaction values surpassed $225B in 2012. - Forrester

• By 2015 mobile payments will account for more than $1T of the global economy. – Yankee Group

• Globally, transactions paid for with mobile technology are forecast to increase nearly fourfold to more than $1.3 trillion annually by 2017 – Juniper Research

• Mobile payments will overcome card volumes within 10 years – World Payment Report

While the estimates and timing vary, the adoption of mobile payments is imminent and an enormous marketplace opportunity

Mobile Proximity Payments are growing fast

POS Total Payments Volume by Payment Method, 2011–2017

While relative size is small, mobile proximity payments as a means of tender cannot be ignored

Mobile Shopping Ecosystem • Payments are a core function for

mobile wallets, but value-added services create the strongest proposition for consumers and providers

• Mobile wallet providers (center of graphic) are trying to control and influence the mobile customer experience, including offers, incentives and value-added services

• Most initial mobile wallet offerings are being developed by payments industry outsiders

• Retailers are critical partners for mobile wallet adoption

• Issuers and merchants are likely to face challenges from the rise of new and innovative mobile wallets

The risk of customer and vendor disintermediation is high

Proximity Payment Technologies

NFC RFID 2D BARCODE

• A short range, high frequency,

standards based wireless

communications technology

• Utilizes smart phone’s secure

element (SE) and limit number

of wallets on SE

• Enables exchange of data in

close proximity (2-4 inches)

• Consumer taps or waves

mobile device at POS device

• Utilized by the Google and

ISIS Wallets

• Utilizes radio waves to transfer

data from an electronic tag

(RFID) tag

• Can be read up to several

meters away

• Usually a sticker or embedded

in a credit card and holds

limited wallet data

• A RFID reader transmits an

encoded signal to read the tag,

tag responds with info

• Longer transmission range

makes less secure

• A two dimensional bar code that

can contain payment and

customer identification

information

• Not hardware based and can

store multiple wallets and

credentials

• A mobile device will display a

barcode and is scanned by a

POS device at checkout

• Used in the Starbucks app

today

• Made more secure when

integrated with a cloud that

stores payments and id

credentials

The most successful mobile payment applications are utilizing 2D barcode today

Standards

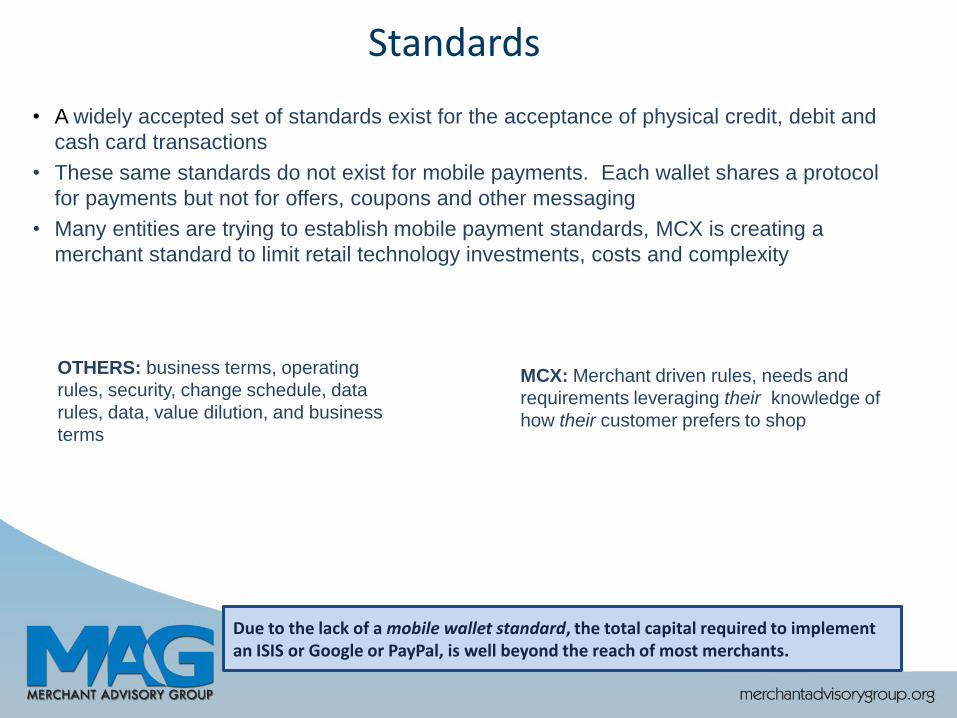

• A widely accepted set of standards exist for the acceptance of physical credit, debit and

cash card transactions

• These same standards do not exist for mobile payments. Each wallet shares a protocol

for payments but not for offers, coupons and other messaging

• Many entities are trying to establish mobile payment standards, MCX is creating a

merchant standard to limit retail technology investments, costs and complexity

MCX: Merchant driven rules, needs and

requirements leveraging their knowledge of

how their customer prefers to shop

OTHERS: business terms, operating

rules, security, change schedule, data

rules, data, value dilution, and business

terms

Due to the lack of a mobile wallet standard, the total capital required to implement an ISIS or Google or PayPal, is well beyond the reach of most merchants.

Potential DATA RISKs with Wallet Providers

POST-STORE PRE- STORE IN-STORE

CUSTOMER MARKETING DATA

Wallet providers delivering marketing

services to collect browsing, shopping,

product lookup, response, redemption and

preference data

The intention is to market consumers with

data that would otherwise have only been

available at a specific merchant.

Data at risk includes: Product preferences,

buying history, payment instrument

preferences across products, merchants and

geographies

END GAME

Unless proactive, widespread change occurs

in the business models of wallet providers,

merchants are at risk of being

disintermediated from our customers and our

suppliers participating in these wallets.

Customer data is at risk of being sold to our

competitors, providers and payment brands.

CUSTOMER TRANSACTION DATA

Based upon features of a wallet (geo-locators,

product lookup, browsing history, electronic

receipts), wallet providers have the potential to

disintermediate merchants to target market and

drive marketing revenues

Data at risk includes: Product purchase , sku,

brand, basket, overall buying history, payment

instrument preferences across products,

merchants and geographies

It is paramount that merchants maintain control of their customer data to maximize the broadest range of digital customer experiences

Mobile payment transaction flow CREDIT CARD PURCHASE WITH PLASTIC

Networks compete for issuers by driving up the interchange costs borne by merchants

Mobile adds cost and complexity to every transaction

Current and new marketplace mobile wallet providers (Google, ISIS, PayPal) are generating income via new fees and costs within the payment ecosystem. Merchants are currently funding these business models

MOBILE CREDIT CARD PURCHASE

Many Wallets, little consistency

Piloting with select merchants

Piloting in Austin and Salt Lake City

In select markets

Market entrants lack incentive to create a balanced customer experience

and payment model due to focus on perpetuating their own one sided

business objectives

MCX appears the only mobile payment alternative that is merchant and consumer centric and is driving a payments paradigm shift

• The mobile payments

marketplace is incredibly

diverse and fragmented

• Due to a lack of standards

across wallets it is cost

prohibitive to participate in

all

• Data ownership / usage and

transaction cost risk will

continue to limit merchant

adoption

Pay with MasterCard

MCX Google ISIS Square PayPal Level UP V.me Paypass

Allows merchant to protect customer data and

use for marketing and servicing

Minimizes long term transactions fees and

establishes rules for transaction processing

Drives cross merchant investment, support and

marketing

Maintain merchant ancillary revenue and avoid

disintermediation

Allows merchant customization of the consumer

experience

appendix

NFC vs 2D comparison 2D BARCODE WITH CLOUD

NFC

Description • Payment credentials and other supporting application data is

secured in the ‘cloud’ or server

• When a transaction is initiated, the data in the cloud is provided to

the Merchant POS via a 2D barcode for completing that

transaction

• Generally, no data is stored on the phone

• User authentication required prior to payments or loyalty data

made available to POS

• A set of technical standards for smartphones and similar

devices to establish secure communication with each other

by touching them together or bringing them into close

proximity

• Applications include contactless transactions, data

exchange, and requires an ICC (Integrated Circuit Chip)

similar to that included in SmartCards, ID cards and

transportation cards

Handset agnostic • Supports a broad range of devices on the market

• No hardware dependencies (eg SIM or ICC Chip)

• Requires a SWP enabled SIM chip or ICC Module

• Many handsets will include NFC in the next 18 months

Able to support both .com

(Card Not Present) and POS

(Card Present) transactions

• Support a broad array of customer commerce touch points

including eCommerce and POS

• Provides architecture flexibility to support changes over time in

order to meet new workflows and interactions

• Only supports POS transactions

Security • Supports multiple security modalities, infrastructure and

deployment fundamentals which are universally considered

sufficient for payment transactions

• Security is based on well known chip and secure

communication with a PKI security framework overlay

• Secure but inflexible

Hardware requirements • It is believed that Cloud based services will not require a

complete hardware overhaul

• NFC requires a device that is NFC-compliant including chip

and communication hardware support

• Hardware at the Point of Sale would need to be retrofitted or

replaced

Primary method of information

exchange

• Payment information is exchange d either through a barcode

scan or via phone capture (taking a picture) with transmission

through a dynamically generated QR or bar-code

• The ‘Cloud’ model can support both the phone capture of a QR

code generated by the POS or a QR code generated by the phone

and then captured by a 2-D scanner (hand-held)

• NFC leverages the contactless card technology enables

devices to share payment information at a distance less

than 4 centimeters

Phone Operating System

support

• Supports iOS (Apple), Android (Samsung, HTC etc), Windows

(Microsoft) and any phone which can either render (show) or

capture a QR code

• Only phones which have been certified and built to support

NFC

• Only Android and Windows OS support to date

In-aisle check out and other

modalities for customer

interaction

• Provides the portability to support in-aisle and other acceptance

devices without any hardware upgrade or implementation

• Requires secure contactless hardware development, testing

and support

MOBILE WALLET LANDSCAPE - as of March 11, 2013

Overview Carrier consortium , created a mobile wallet and

marketing platform. Close partnership with

handset providers

Web and mobile payments platform company leveraging

mobile payments to drive an overall mobile customer

experience

Web and mobile advertising giant leveraging

mobile payments to drive ad revenue –

unsuccessful NFC test, now to offer barcode

Payment

Technology

NFC - Payment credentials stored on the secure

element

Payment credentials stored on the secure element or Web

Transaction - Payment credentials the cloud

Payment credentials stored in the cloud

Devices Only carrier approved handsets ALL Android phones

Hardware

Requirements

POS hardware upgrades for NFC

POS hardware upgrades/integration for mobile/web based

payments

POS hardware upgrades for NFC and/or 2D

barcode

Customer

Experience

Rich customer experience with store locator,

coupons, etc.

End to end customer experience is shopping based not

payments based. Integration of Red Laser and Where?

functionality to drive broader acceptance

Initially focused on couponing and offers and

evolving the end-to-end mobile experience with

a vision to drive payments costs down over

time – avail in store/online

Merchant

Tender Cost

Control

ISIS leverages traditional payment networks

(MasterCard and Visa) and are not incentivized to

change cost paradigm. Current business model

adds costs to every ISIS transaction and account

PayPal is it’s own network and supports traditional and peer

to peer payments. Business model is to drive down

transaction costs and generate additional revenue through

data, analytics and marketing

Google leverages traditional payment networks

(V, MC, AMEX, Discover) and are not

incentivized to change cost paradigm – use the

card present rates. They will generate ad

revenues through data analytics and

advertising

Offers &

Coupons

Customer opt-in for merchant marketing . ISIS

marketing platform will push and manage offers

PayPal analytics and web tracking capabilities to allow for

1:1 targeted offers for merchants

Merchants to pay for mobile marketing efforts

Launch Dates Fall pilot in Austin/Salt Lake 2012 Pilot Q1 2012 – mall test 12/12 Pilot Q4 2011

Current Retail

Partners

Many local merchants who have NFC enabled

terminals as well as larger merchants: Rite Aid,

Macys, Jamba Juice, Sports Authority, AT&T,

TMobile, Verizon mobile stores, Chevron, Whole

Foods, Foot Locker, Petco

Abercrombie & Fitch, Advance Auto Parts, Aéropostale,

AEOutfitters, Barnes & Noble, Foot Locker, Guitar Center,

Jamba Juice, JC P, Jos. A. Bank Clothiers, Nine West,

Office Depot, Rooms To Go, Tiger Direct and Toys “R” Us,

etc.

American Eagle, Urban Outfitters, Toys-R-Us,

Radio Shack, Macy’s, Container Store, Duane

Reade, Sprint, Subway, etc.

Current

Payment

Partners

CapOne, Chase, C-SAM, Barclays, AMEX CapOne, Chase, Discover, VISA, MC, AMEX VISA, MC, Discover, AMEX

Overview Square is a POS and payments

platform allowing for an integrated

customer experience with the

customer picture being rendered

with the payment credentials at the

merchant’s POS

LevelUp is a payment network. With

a zero interchange business model

Visa’s wallet, V.me, is currently

solely an on-line/m payment

solution. Credit/debit cards are

loaded into a V.me account and are

accessed by entering an email

address and password

Master Card has recently re-

launched PayPass: an online /m

payment solution for credit/debit

cards accessed via a one click MC

payment button

Payment Technology Square register and Square card

case app

A credit card is scanned and loaded

into the Level Up app. A token

barcode is created and scanned at

POS

Only online currently, when deployed

at POS will be NFC or customer

keyed email/phone number and

password/PIN

Only online currently, when deployed

at POS will be NFC or customer

keyed email/phone number and

password/PIN

Devices Android and iOS Android and iOS Online only – future: NFC phones Online only – future: NFC phones

Hardware

Requirements

Square Register is an iPad specific

App and POS device. An Iphone

with a dongle also can be used.

Significant POS integration required

Potential POS upgrades for 2D

barcode scanners

POS hardware upgrades/integration

for mobile/web based payments

POS hardware upgrades/integration

for mobile/web based payments

Customer Experience Within the Square app, a customer

searches for a merchant and views

product price detail. Payment

information is retained and the app

triggers a customer photo at POS for

verification by the sales associate

Within the LevelUp app , a consumer

takes a photo of their cards and the

data is loaded to a cloud. The

phone is used to scan the 2D

barcode at POS to initiate the

payment

Customer sets up a v.me account

and enters their credit/debit card

information and creates a password.

Upon online checkout using a v.me

pay button, the customer access

their card of choice by entering email

address and password during the

checkout process

Customer sets up a MC account and

enters their credit/debit card

information and creates a password.

Upon online checkout using paypass

pay button, the customer access

their card of choice by entering email

address and password during the

checkout process

Merchant Tender Cost

Control

Square leverages traditional

payment networks (V, MC, AMEX,

Discover) and are not incentivized to

change cost paradigm. Have

created a standard blended rate

model (2.75% ), Large merchants

can negotiate terms

LevelUp is testing charging zero

interchange in exchange for a

percentage of promotional dollars

used during a purchase – i.e. 35% of

$2 off a $10 purchase

Current card rates apply Current card rates apply

Offers & Coupons Integrated into the solution through

the app

Offers are integrated into the app

and %/$ off are listed by merchant

Customer opts in for marketing

offers. Merchants pay for offers.

Customer opts in for marketing

offers. Merchants pay for offers.

Launch Dates In market In market – concentrated in metros Pilot Q4 2012 – in market 2013 Pilot Q4 2012

Current Retail Partners Thousands of small U.S.

businesses – through the dongle

program. Strategic partnership with

Starbucks

Claim to have 2,500+ small, regional

merchants – mostly restaurants

50+ banks are part of the v.me

network as well as a handful of

merchants – 1-800 Flowers and a

few strictly .com merchants

Unknown

Current Payment

Partners

VISA, MC, Discover, AMEX VISA, MC, Discover, AMEX

VISA, MC, Discover, AMEX

VISA, MC, Discover, AMEX

Square LevelUp MasterPass V.me

MOBILE WALLET LANDSCAPE as of March 11, 2013

1

The Potential Impact of Mobile Payments

Mobile Payment is simply a point-of-sale

payment made through a mobile device, such

as a cellular/smart phone or

a personal digital assistant (PDA)

Threats:

Increased Interchange fees due to more participants in a transaction

Insertion of a third party between retailer and their customer

Opportunities:

Different parties have diverging reasons to use the added benefits and convenience of mobile

payments to capture transaction volume

Traditional networks want to preserve transaction volume

New entrants primarily after consumer information for marketing revenue

Retailers desire lower cost and retain relationship with the customer

2

Mobile Payments Landscape

Delivers Value to the Retailer

De

live

rs V

alu

e to

th

e C

on

su

me

r

LOW HIGH

LO

W

HIG

H

Customer Speed and ease of use

More control over checkout experience

Security

Enhance the in-store shopping experience

The Home Depot Obtain lower transaction cost

Establish a platform for communication with certain

customers

Bolster Data Acquisition

Align in-store shopping experience with online/mobile

The Home Depot Mobile Payments Objectives

3

Source – Bernstein Research

Evaluating Merchants’ Power Play in the Mobile Payments Fray and PayPal/Discover POS Deal

Retailer/Mobile Payment Alignment

* Indicates retail merchants ranked in the top 100 US retailers by revenues according to stores.com