Monetary Policy without Money? The "Scissors Effect" Reconsidered Peter Spahn Economics Faculty, University of Hohenheim, Stuttgart, Germany In former times, central banks applied a "scissors effect", i.e. the combined use of open- market and interest rate policies, in order to strengthen the control of the banking sector when monetary stability was highly endangered. Modern monetary policy in general lets the quantity of base money adjust to the liquidity needs of commercial banks and now also macro theory has acknowledged short-term interest rate variations as the key policy tool. But without quantitative restrictions the scope of financial transactions at times tends to enlarge grossly, making the economy prone to asset price bubbles. It is not nec- essary to restore any monetary targeting for goods market inflation. However, central banks should observe money and credit aggregates in order to detect evolving asset mar- ket bubbles and react, if necessary, by open-market transactions. Discretionary liquidity policies can signal higher risks to market agents, enforce a containment of commercial banks' credit activities and support the course of interest rate policies. Keywords: open-market policy; asset price bubble; euro money market; ECB strategy JEL classification: E5 [The Bank of England] might, undoubtedly, at all seasons, sufficiently limit its paper [money] by means of the price at which it lends. Henry Thornton (1802: 254) 1. Introduction At present times, when central banks, practically all around the world, have embarked on a course of issuing money seemingly without bound, academic macro theory has advanced to a state where the variable M (i.e. money in various aggregates) finally has dropped from the main equations. Whereas Goodhart (2007) warns that downgrading of the role of money has gone too far, Woodford (2008), as a leading protagonist of New Keynesian Macroeconomics, endeavours to show that control of monetary ag- gregates is unnecessary to maintain macro stability, which mostly is understood as keeping the rate of inflation at the target level. Critics who steadfastly propagate the usefulness of the quantity theory in practical monetary policy making (e.g., Reynard 2007) receive only weak support, even on the part of those who have earned substan- tial reputation in the defence of monetary traditions in macroeconomics (e.g., Nelson 2007). The trend instability of velocity, a phenomenon that first was seen in the UK and the US, and that later also showed up in the euro zone, has undermined monetary

Transcript

Monetary Policy without Money? The "Scissors Effect" Reconsidered Peter Spahn Economics Faculty, University of Hohenheim, Stuttgart, Germany

In former times, central banks applied a "scissors effect", i.e. the combined use of open-market and interest rate policies, in order to strengthen the control of the banking sector when monetary stability was highly endangered. Modern monetary policy in general lets the quantity of base money adjust to the liquidity needs of commercial banks and now also macro theory has acknowledged short-term interest rate variations as the key policy tool. But without quantitative restrictions the scope of financial transactions at times tends to enlarge grossly, making the economy prone to asset price bubbles. It is not nec-essary to restore any monetary targeting for goods market inflation. However, central banks should observe money and credit aggregates in order to detect evolving asset mar-ket bubbles and react, if necessary, by open-market transactions. Discretionary liquidity policies can signal higher risks to market agents, enforce a containment of commercial banks' credit activities and support the course of interest rate policies.

[The Bank of England] might, undoubtedly, at all seasons, sufficiently limit its paper [money] by means of the price at which it lends.

Henry Thornton (1802: 254) 1. Introduction

At present times, when central banks, practically all around the world, have embarked

on a course of issuing money seemingly without bound, academic macro theory has

advanced to a state where the variable M (i.e. money in various aggregates) finally has

dropped from the main equations. Whereas Goodhart (2007) warns that downgrading

of the role of money has gone too far, Woodford (2008), as a leading protagonist of

New Keynesian Macroeconomics, endeavours to show that control of monetary ag-

gregates is unnecessary to maintain macro stability, which mostly is understood as

keeping the rate of inflation at the target level. Critics who steadfastly propagate the

usefulness of the quantity theory in practical monetary policy making (e.g., Reynard

2007) receive only weak support, even on the part of those who have earned substan-

tial reputation in the defence of monetary traditions in macroeconomics (e.g., Nelson

2007). The trend instability of velocity, a phenomenon that first was seen in the UK

and the US, and that later also showed up in the euro zone, has undermined monetary

2

policy strategies that are built on the money-inflation nexus. The ECB argument stat-

ing the necessity of the famous "monetary pillar" for safeguarding price stability in

long run seems hardly convincing in the light of the ECB's anti-inflation performance:

successfully maintaining price stability month-by-month must logically imply main-

taining it over long run as well (Galí et al. 2004; Woodford 2007).

However, the recent repeated experience of credit-driven asset market bubbles in

some countries, which found their bank-balance-sheet side effects in vigorous broad-

money dynamics, casts some doubts on the general sufficiency of mere interest rate

policies. Their stabilizing forces usually are demonstrated in New Neoclassical (also

misnamed New Keynesian) models where small deviations from "natural" equilib-

rium values can be contained. It is an unresolved question however what to do if infla-

tion already has slipped out of control, or in a scenario of asset inflation. Open-market

operations now are assessed to be useful in the current depression; the counterpart of

"quantitative easing" however remains neglected.

Modern authors claim that interest rate setting always has been the essence of

central banking and that the attempts of quantitatively managing monetary aggregates

have been, at best, futile (Bindseil 2004; Disyatat 2008; Keister et al. 2008). Maybe

this message is somewhat rash and influenced by monetarism's loss of reputation in

the sphere of macro theory. True, finally even Friedman himself confessed that he

would not recommend monetary targeting again.1 But even if the monetarist approach

of stabilizing cycles and inflation suffers from serious drawbacks, it is nevertheless

worthwhile to explore the use of monetary aggregates as an independent central bank

tool that can be applied in phases where macro stability is severely endangered.

Therefore this paper, firstly, reviews some historical experience of the instrumen-

tal use of money in central banking; it asks for the reasons and the results of quantita-

tive liquidity measures. Then it is shown that ECB monetary policies, the success of

achieving its inflation target notwithstanding, lost control over credit dynamics de-

spite rising interest rates. Secondly, the paper explores how money markets can be or-

ganized in order to enable a falling back on quantitative measures if these are assessed

to be necessary. It is suggested, besides the variation of short-term interest rates, to

1 In a 2003 interview he said that "the use of quantity of money as a target has not been a success," and that he is "not sure I would as of today push it as hard as I once did" (reported in Woodford 2008: 1564 n).

3

employ open-market sales as an additional instrument: this signals the central bank's

concern about asset prices, exerts pressure on commercial banks' liquidity status, and

supports the transmission of monetary policy impulses to capital markets. 2. Central bank money and interest rates in historical perspective

2.1 Simultaneous use of open market and discount policies

The norm of an active money supply management was prevalent already in the gold

standard. Here, the extremely inelastic provision of central bank balances after Peel's

Act of 1844 caused recurring banking crises that were cured time and again by tempo-

rarily suspending the strict rule of the required hundred-per-cent marginal backing

regulation (Spahn 2001). In the following decades, the Bank of England developed a

pragmatic way of monetary policy that obeyed to the statutory base money supply re-

striction as a principle, but mainly, following Bagehot (1873), operated by means of

discount rate changes, which were oriented at the equilibrium of the foreign exchange

market. In the first part of the 20th century, both the Bank of England and the Federal

Reserve sometimes used a combination of open-market operations in long-term secu-

rities on the one hand and interest rate policies on the other, which regulated the terms

of short-term credit demanded by commercial banks (Keynes 1930; Lutz 1936).

It could be observed that commercial banks were able to offset the monetary ef-

fects of open-market transactions by quantitatively adjusting their rediscounting at the

Fed. If the aim was to restrain macro dynamics, the Fed would combine selling securi-

ties with increasing the discount rate. Despite this adverse price impulse, the banks of-

ten, in case of a strong liquidity effect of the open-market operation, were forced to

expand discounting. This strategy of increasing the banks' dependency on the refi-

nancing channel, which then helped to enforce changes of central bank interest rates,

was coined the "scissors effect" (Friedman and Schwartz 1963: 272). Although

Keynes and Friedman were much in favour of open-market operations (Bindseil

2004), in post-war economic policy this tool was employed more in textbook analysis

than in practical central banking. However, there were episodes when central banks

actively sought to rely on quantitative liquidity measures that could help to implement

the course of interest rate policies. Two of these episodes are analyzed in the next two

Sections.

4

2.2 The Bundesbank's "pragmatic monetarism"

The Bundesbank's style of monetary policy operations at its beginning was still an-

chored in the interwar gold standard traditions, but during the 1970s took up the

growing influence of monetarism in academia. Looking at the period from the mid

1960s up to the early 1980s, we discover three interesting episodes, each of them

characterized by a monetary restriction followed by a macroeconomic recession,

which found their through in 1967, 1975 and 1982, respectively.2 The Bundesbank's

policy course can be expressed by the discount and the lombard rate, which represent

ordinary and emergency short-term lending to the banking sector, and the call money

rate, which gauges liquidity stress in the interbank money market (Figure 1). Figure 1: Growth rate (y-o-y) of CMB (monetary base corrected for changes of minimum re-serve requirements) and short-term interest rates in Germany.3

0

4

8

12

16

1965.1 1968.1 1971.1 1974.1 1977.1 1980.1 1983.1

g_CMBlombardcall moneydiscount

The Bundesbank's money supply activities, however, cannot be simply be measured

by means of the growth rate of base money (notes in circulation and commercial

banks' accounts). This aggregate can hardly be understood as a central bank tool,

rather its course is the result of an interaction of monetary policy decisions, commer-

cial bank behaviour and non-bank activities. In the 1970s, the Bundesbank defined a

"corrected monetary base" that controlled the original data for changes in minimum

reserve requirements. The path of this CMB aggregate does not differ that much from

2 There was a further attempt of monetary tightening at around 1970, which was broken off after massive capital inflows; it had only minor consequences for the real sector. The Bundesbank's final stabilization project in the early 1990s is neglected here because liquidity operations were also charged with the task of establishing the German currency union. 3 Except otherwise indicated, data source in the following Sections is Bundesbank, Fed and ECB, depending on the national character of the data at issue.

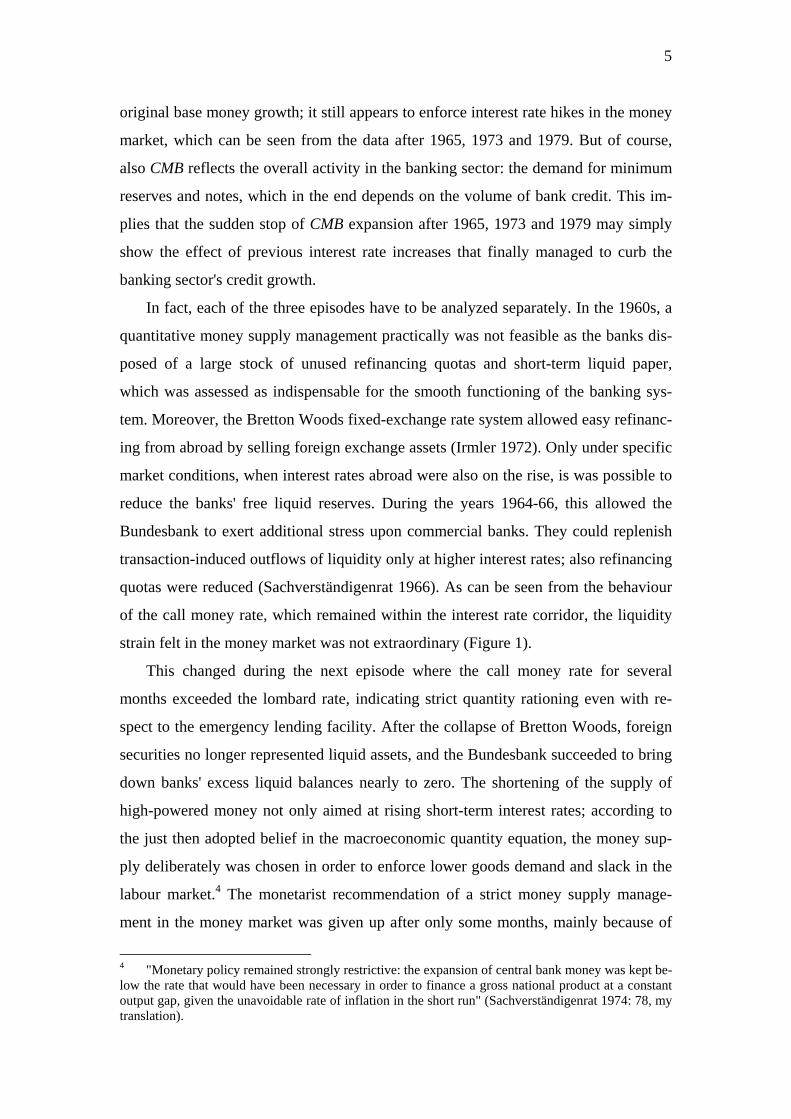

5

original base money growth; it still appears to enforce interest rate hikes in the money

market, which can be seen from the data after 1965, 1973 and 1979. But of course,

also CMB reflects the overall activity in the banking sector: the demand for minimum

reserves and notes, which in the end depends on the volume of bank credit. This im-

plies that the sudden stop of CMB expansion after 1965, 1973 and 1979 may simply

show the effect of previous interest rate increases that finally managed to curb the

banking sector's credit growth.

In fact, each of the three episodes have to be analyzed separately. In the 1960s, a

quantitative money supply management practically was not feasible as the banks dis-

posed of a large stock of unused refinancing quotas and short-term liquid paper,

which was assessed as indispensable for the smooth functioning of the banking sys-

tem. Moreover, the Bretton Woods fixed-exchange rate system allowed easy refinanc-

ing from abroad by selling foreign exchange assets (Irmler 1972). Only under specific

market conditions, when interest rates abroad were also on the rise, is was possible to

reduce the banks' free liquid reserves. During the years 1964-66, this allowed the

Bundesbank to exert additional stress upon commercial banks. They could replenish

transaction-induced outflows of liquidity only at higher interest rates; also refinancing

quotas were reduced (Sachverständigenrat 1966). As can be seen from the behaviour

of the call money rate, which remained within the interest rate corridor, the liquidity

strain felt in the money market was not extraordinary (Figure 1).

This changed during the next episode where the call money rate for several

months exceeded the lombard rate, indicating strict quantity rationing even with re-

spect to the emergency lending facility. After the collapse of Bretton Woods, foreign

securities no longer represented liquid assets, and the Bundesbank succeeded to bring

down banks' excess liquid balances nearly to zero. The shortening of the supply of

high-powered money not only aimed at rising short-term interest rates; according to

the just then adopted belief in the macroeconomic quantity equation, the money sup-

ply deliberately was chosen in order to enforce lower goods demand and slack in the

labour market.4 The monetarist recommendation of a strict money supply manage-

ment in the money market was given up after only some months, mainly because of

4 "Monetary policy remained strongly restrictive: the expansion of central bank money was kept be-low the rate that would have been necessary in order to finance a gross national product at a constant output gap, given the unavoidable rate of inflation in the short run" (Sachverständigenrat 1974: 78, my translation).

6

intolerable interest rate volatility, and then was substituted by a concept where nar-

rowly-defined money was chosen as an intermediate target.5

The next monetary restriction in the early 1980s, prompted by the aim to defend

the internal and external value of the mark, was accompanied by substantial sales of

currency reserves that implied concomitant liquidity losses in the German banking

sector. These losses provided a convenient background for decisions on interest rate

increases. The Bundesbank also stopped ordinary lombard borrowing, which was sub-

stituted by an "extra" lombard facility at even higher rates; money market rates thus

were kept inside the corridor.

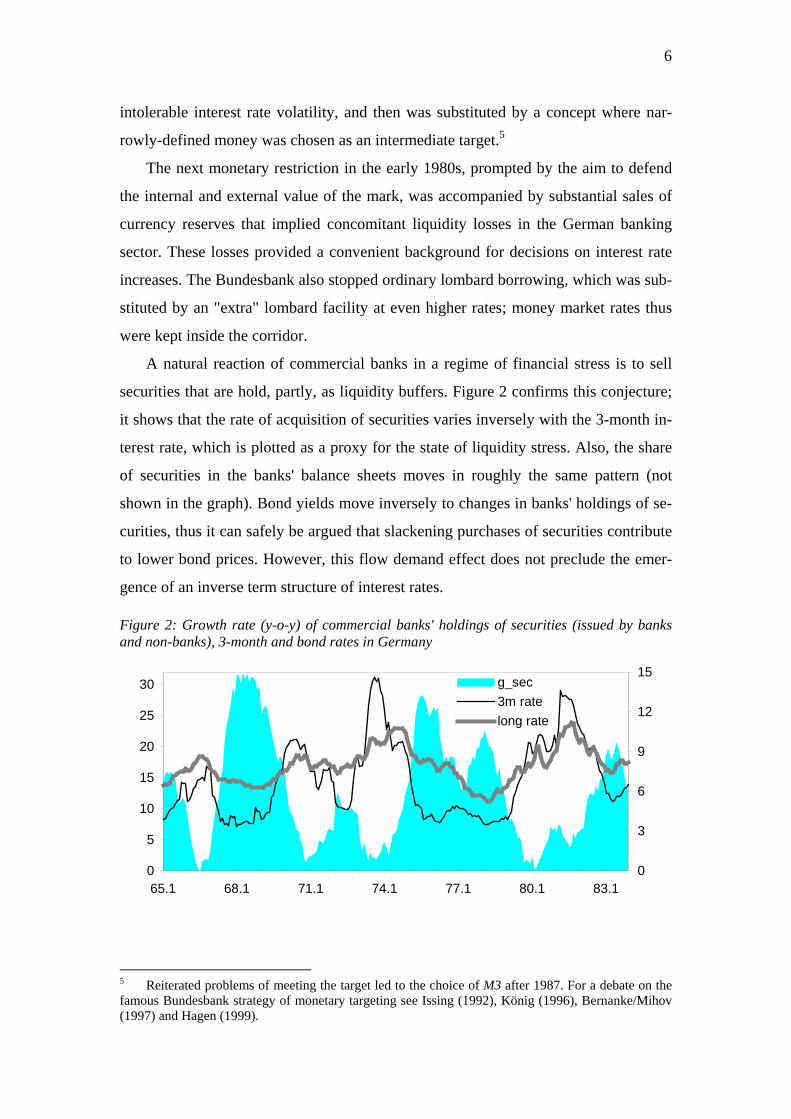

A natural reaction of commercial banks in a regime of financial stress is to sell

securities that are hold, partly, as liquidity buffers. Figure 2 confirms this conjecture;

it shows that the rate of acquisition of securities varies inversely with the 3-month in-

terest rate, which is plotted as a proxy for the state of liquidity stress. Also, the share

of securities in the banks' balance sheets moves in roughly the same pattern (not

shown in the graph). Bond yields move inversely to changes in banks' holdings of se-

curities, thus it can safely be argued that slackening purchases of securities contribute

to lower bond prices. However, this flow demand effect does not preclude the emer-

gence of an inverse term structure of interest rates. Figure 2: Growth rate (y-o-y) of commercial banks' holdings of securities (issued by banks and non-banks), 3-month and bond rates in Germany

0

5

10

15

20

25

30

65.1 68.1 71.1 74.1 77.1 80.1 83.10

3

6

9

12

15g_sec3m ratelong rate

5 Reiterated problems of meeting the target led to the choice of M3 after 1987. For a debate on the famous Bundesbank strategy of monetary targeting see Issing (1992), König (1996), Bernanke/Mihov (1997) and Hagen (1999).

7

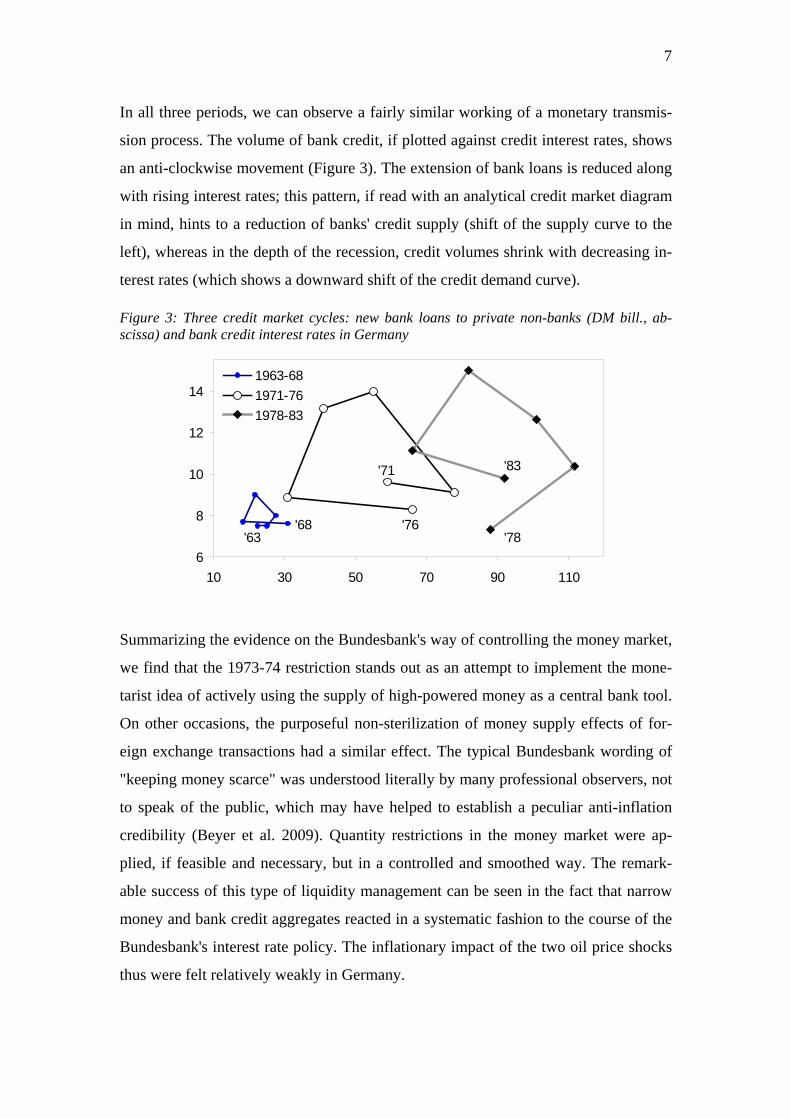

In all three periods, we can observe a fairly similar working of a monetary transmis-

sion process. The volume of bank credit, if plotted against credit interest rates, shows

an anti-clockwise movement (Figure 3). The extension of bank loans is reduced along

with rising interest rates; this pattern, if read with an analytical credit market diagram

in mind, hints to a reduction of banks' credit supply (shift of the supply curve to the

left), whereas in the depth of the recession, credit volumes shrink with decreasing in-

terest rates (which shows a downward shift of the credit demand curve). Figure 3: Three credit market cycles: new bank loans to private non-banks (DM bill., ab-scissa) and bank credit interest rates in Germany

6

8

10

12

14

10 30 50 70 90 110

1963-681971-761978-83

'63'68

'71

'76'78

'83

Summarizing the evidence on the Bundesbank's way of controlling the money market,

we find that the 1973-74 restriction stands out as an attempt to implement the mone-

tarist idea of actively using the supply of high-powered money as a central bank tool.

On other occasions, the purposeful non-sterilization of money supply effects of for-

eign exchange transactions had a similar effect. The typical Bundesbank wording of

"keeping money scarce" was understood literally by many professional observers, not

to speak of the public, which may have helped to establish a peculiar anti-inflation

credibility (Beyer et al. 2009). Quantity restrictions in the money market were ap-

plied, if feasible and necessary, but in a controlled and smoothed way. The remark-

able success of this type of liquidity management can be seen in the fact that narrow

money and bank credit aggregates reacted in a systematic fashion to the course of the

Bundesbank's interest rate policy. The inflationary impact of the two oil price shocks

thus were felt relatively weakly in Germany.

8

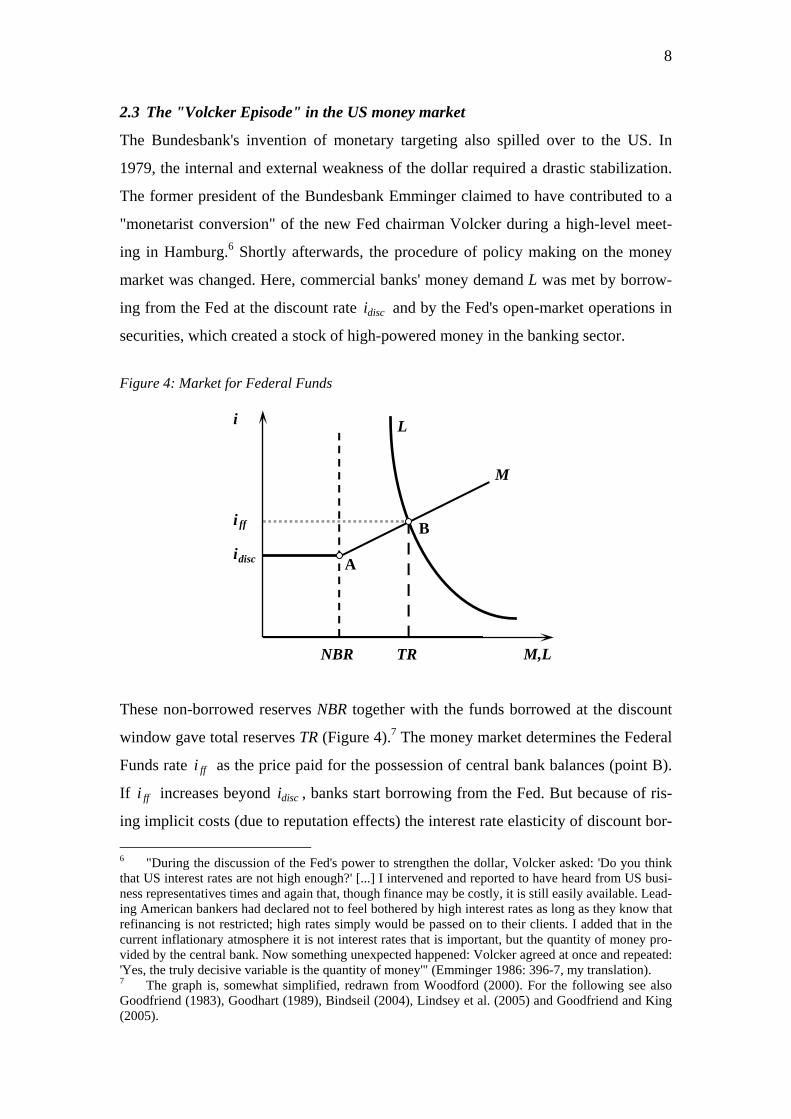

2.3 The "Volcker Episode" in the US money market

The Bundesbank's invention of monetary targeting also spilled over to the US. In

1979, the internal and external weakness of the dollar required a drastic stabilization.

The former president of the Bundesbank Emminger claimed to have contributed to a

"monetarist conversion" of the new Fed chairman Volcker during a high-level meet-

ing in Hamburg.6 Shortly afterwards, the procedure of policy making on the money

market was changed. Here, commercial banks' money demand L was met by borrow-

ing from the Fed at the discount rate disci and by the Fed's open-market operations in

securities, which created a stock of high-powered money in the banking sector.

Figure 4: Market for Federal Funds

L

M,L

i

NBR

ffi

M

disci

TR

A

B

These non-borrowed reserves NBR together with the funds borrowed at the discount

window gave total reserves TR (Figure 4).7 The money market determines the Federal

Funds rate ffi as the price paid for the possession of central bank balances (point B).

If ffi increases beyond disci , banks start borrowing from the Fed. But because of ris-

ing implicit costs (due to reputation effects) the interest rate elasticity of discount bor- 6 "During the discussion of the Fed's power to strengthen the dollar, Volcker asked: 'Do you think that US interest rates are not high enough?' [...] I intervened and reported to have heard from US busi-ness representatives times and again that, though finance may be costly, it is still easily available. Lead-ing American bankers had declared not to feel bothered by high interest rates as long as they know that refinancing is not restricted; high rates simply would be passed on to their clients. I added that in the current inflationary atmosphere it is not interest rates that is important, but the quantity of money pro-vided by the central bank. Now something unexpected happened: Volcker agreed at once and repeated: 'Yes, the truly decisive variable is the quantity of money'" (Emminger 1986: 396-7, my translation). 7 The graph is, somewhat simplified, redrawn from Woodford (2000). For the following see also Goodfriend (1983), Goodhart (1989), Bindseil (2004), Lindsey et al. (2005) and Goodfriend and King (2005).

9

rowing is less than perfect. This can be expressed, at the right from point A, as a posi-

tively-sloped money supply function ( )ff discM f i i= − .

Usually the Fed had chosen a narrow corridor for the Federal Funds rate as its

policy target, and adjusted NBR and the discount rate accordingly. But given the high

rating of the employment target in US policy making, and the factual obligation to de-

fend every interest move in the public, it proved difficult to organize a stable majority

in the Federal Open Market Committee (FOMC) that would vote for drastic interest

rate increases, which economically were felt to be necessary in a situation where in-

flation appeared to slip out of anybody's control. Thus discretionary policy decisions

only managed to implement small rate increases (Figure 5).

Figure 5: Growth rate of non-borrowed reserves (y-o-y, adjusted for seasonally effects and for changes in reserve requirements), Federal Funds rate, 10-year Treasury Bond yield and period of monetary targeting (rectangle)

Volcker realized that "when you have to make an explicit decision about interest rates

all the time, people don't like to do it" (quoted in Lindsey et al. 2005: 216), and there-

fore successfully promoted a strategic policy move, which sought to persuade the

public that a "fundamental" new regime for safeguarding the dollar was imple-

mented8, and which circumvented the troublesome task of justifying each single inter-

est rate decision. In a nutshell9, the new approach consisted of the following steps: 8 "My feeling was that putting even more emphasis on meeting the money supply targets and chang-ing operating techniques and thereby changing psychology a bit, we might actually get more bang for the buck [...]. The traditional method of making small moves has in some sense, though not completely, run out of psychological gas" (Paul Volcker, quoted in Lindsey et al. 2005: 202-3). 9 Obviously there is a risk of oversimplification as Bindseil (2004) reports that, even many years af-ter that episode, debates within (!) the Fed continue about how these procedures actually worked.

10

• Estimate a M1 growth that promises to keep inflation in check; • calculate, via cash outflows and reserve requirements, an according path of total

reserve demand on the part of the banking sector; • read off the corresponding money market rate of interest from the commercial

banks' demand function L; • change the volume of NBR, i.e. shift the vertical line and thus let the function

( )M ⋅ move upwards (in most cases) so that it intersects the money demand func-tion at the implicit interest rate target;10

• communicate interest changes as market-driven events, not directly controlled by the FOMC, but emphasize the broad money target instead.11

After October 1979, the change of NBR factually was managed to drive the Federal

Funds rate towards the presumed equilibrium value. Although the stock of the mone-

tary base developed quite evenly, NBR growth and the Federal Funds rate behaved in

a very volatile manner, and the inverse moves of these two variables can be read off

clearly from the data (Figure 5). Also, there can be no doubt about the causal direc-

tion, working from the money supply side to the short-term rate of interest; its move-

ment was mirrored, although clearly damped, by the long-term rate. However, active

reserve supply management was practised for a short period only. The Fed let the

"monetarist experiment" fade out in autumn 1982. After returning to moderate infla-

tion, there was no need for drastic interest rate moves, thus the temptation to use

monetary targets as a smokescreen for unpopular decisions on interest rates was no

longer given.

The strategy of using quantitative money supply restrictions as an active tool of

central banking was rated as a failure from nearly all camps of theorists and policy

makers. The reasons are manifold:

• The control procedure was extremely complicated and susceptible to various esti-mation problems. Basically, the approach tried to operate on a chain of intermedi-ate targets, where (a part of) base money was controlled in order to move short-term interest rates, which in turn was hoped to influence narrow and broad money aggregates, and finally prices. More than once, Volcker and his colleagues during FOMC sessions admitted to feel "lost" and "confused" about what they were actu-

10 This comes down to a rather indirect way of controlling balances: "The FOMC chooses an initial intermeeting path for non-borrowed reserves designed to induce the banking system to obtain a target volume of borrowed reserves from the discount window" (Goodfriend 1983: 353, my emphasis). 11 "The Committee recognized that the switch to a reserve-based approach to monetary control would be more likely to allow the federal funds rate in the short run to move as necessary to whatever level would prove consistent with more restrained money growth and lower inflation" (Lindsey et al. 2005: 214). Henry Wallich (quoted ibid.: 216, cf. Blinder 1998: 29) argued likewise: "At the policy level, the reserve-based procedure has the advantage of minimizing the need for Federal Reserve deci-sions concerning the funds rate. Interest rates become a byproduct, as it were, of the money-supply process."

11

ally doing (Bindseil 2004). • The approach did not really provided clear hints about where to go. It could not be

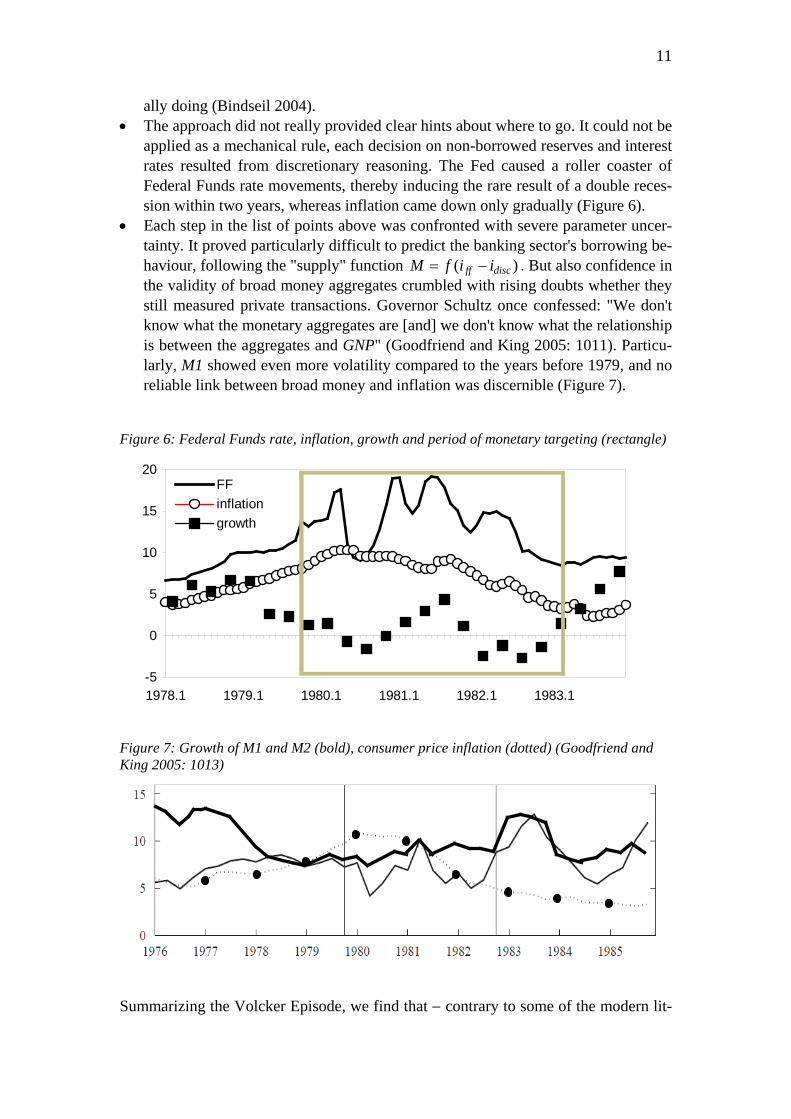

applied as a mechanical rule, each decision on non-borrowed reserves and interest rates resulted from discretionary reasoning. The Fed caused a roller coaster of Federal Funds rate movements, thereby inducing the rare result of a double reces-sion within two years, whereas inflation came down only gradually (Figure 6).

• Each step in the list of points above was confronted with severe parameter uncer-tainty. It proved particularly difficult to predict the banking sector's borrowing be-haviour, following the "supply" function ( )ff discM f i i= − . But also confidence in the validity of broad money aggregates crumbled with rising doubts whether they still measured private transactions. Governor Schultz once confessed: "We don't know what the monetary aggregates are [and] we don't know what the relationship is between the aggregates and GNP" (Goodfriend and King 2005: 1011). Particu-larly, M1 showed even more volatility compared to the years before 1979, and no reliable link between broad money and inflation was discernible (Figure 7).

Figure 6: Federal Funds rate, inflation, growth and period of monetary targeting (rectangle)

-5

0

5

10

15

20

1978.1 1979.1 1980.1 1981.1 1982.1 1983.1

FFinflationgrowth

Figure 7: Growth of M1 and M2 (bold), consumer price inflation (dotted) (Goodfriend and King 2005: 1013)

Summarizing the Volcker Episode, we find that − contrary to some of the modern lit-

12

erature (Disyatat 2008) − a liquidity effect from active money supply policies to

short-term interest rates is surely visible. But actually the Fed pursued a rather

opaque, multi-step intermediate-target approach, which basically rested on a monetar-

ist money-inflation nexus that failed to be borne out. Instead of triggering off a tem-

porary liquidity squeeze that aimed to support a clearly communicated interest rate

policy, the Fed got caught up in medium-term mix of quantitative and price-theoretic

control signals that probably destabilized output and employment. It is however also

probable that the public avowal to the new slogan of money supply restrictions, even

if barely understood, helped to contain inflationary expectations.

2.4 Supply and use of euro base money

The ECB was presumed to continue, partly, the German tradition of central bank be-

lief in the quantity theory of money. It tried to avoid the impression that the quantity

of high-powered money was a demand-determined variable. Most probably, a key

reason was that as a "successor" of the Bundesbank, which made money supply con-

trol its trademark, it was hardly recommendable to downgrade any symbols of the be-

lief in the quantity theory (Woodford 2008). Moreover, it appears to be a common-

place to insist on the principle that money should be kept "scarce".

Figure 8: Commercial banks' bids and base money allotment (€ bill.) in ECB's main refinanc-ing operations

0

200

400

600

800

1000

1200

1400

1600

7.1.99 17.1.01 22.1.03 5.1.05 10.1.070

20

40

60

80

100

bidsallotmentinverse ratio (right)

8500

Even when operating in the fixed-rate modus of its repo tender policies, the ECB most

of the time fixed a maximum volume of refinancing credit that was extended to the

13

commercial banking sector. This limitation was binding: during the first two years

since its inception, commercial banks' bids exceeded the ECB's allotment of base

money in a vast extent; the allotment-bid ratio finally, in summer 2000, fell below 1%

(Figure 8)! Overbidding in no way was caused by a liquidity shortage, but rested on

the speculation of imminent policy rate increases that induced commercial banks to

stock up on cheap reserves. After switching to variable-rate tender allotment, ratios

normalized at around 80%, and their volatility further diminished when in March

2004 the duration of repo transactions was shortened to one week, thereby doubling

their volume (ECB 2008).

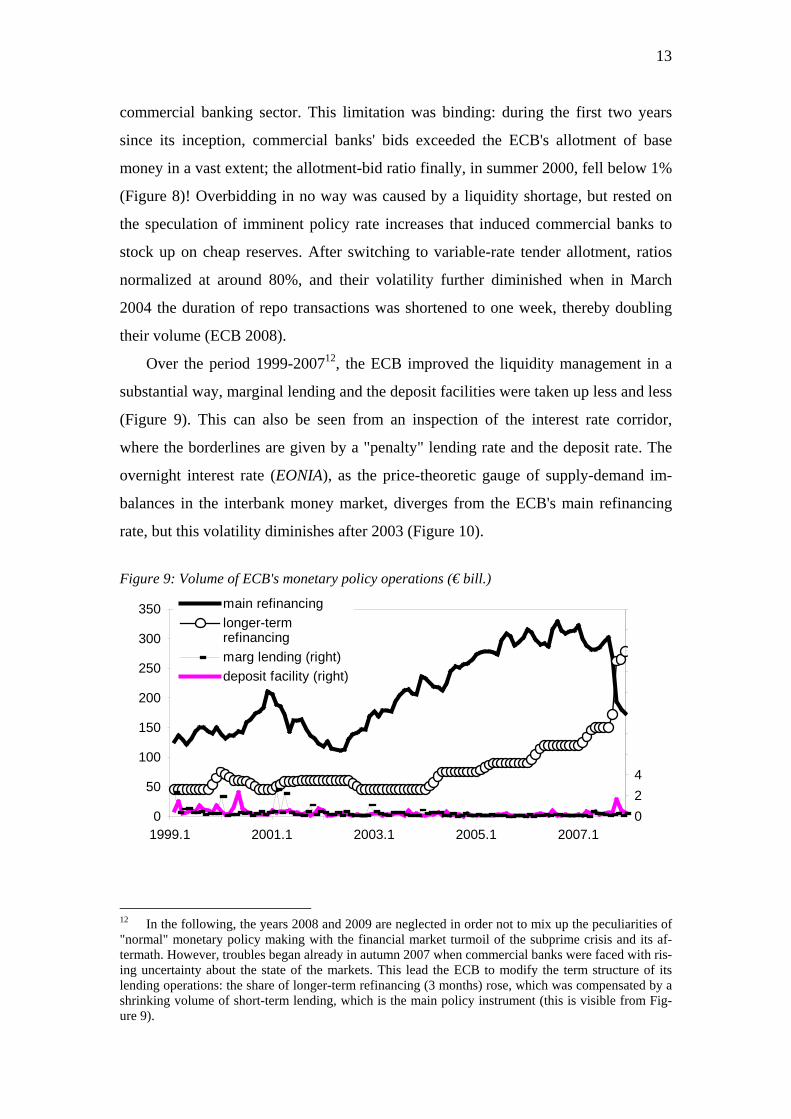

Over the period 1999-200712, the ECB improved the liquidity management in a

substantial way, marginal lending and the deposit facilities were taken up less and less

(Figure 9). This can also be seen from an inspection of the interest rate corridor,

where the borderlines are given by a "penalty" lending rate and the deposit rate. The

overnight interest rate (EONIA), as the price-theoretic gauge of supply-demand im-

balances in the interbank money market, diverges from the ECB's main refinancing

rate, but this volatility diminishes after 2003 (Figure 10).

Figure 9: Volume of ECB's monetary policy operations (€ bill.)

12 In the following, the years 2008 and 2009 are neglected in order not to mix up the peculiarities of "normal" monetary policy making with the financial market turmoil of the subprime crisis and its af-termath. However, troubles began already in autumn 2007 when commercial banks were faced with ris-ing uncertainty about the state of the markets. This lead the ECB to modify the term structure of its lending operations: the share of longer-term refinancing (3 months) rose, which was compensated by a shrinking volume of short-term lending, which is the main policy instrument (this is visible from Fig-ure 9).

14

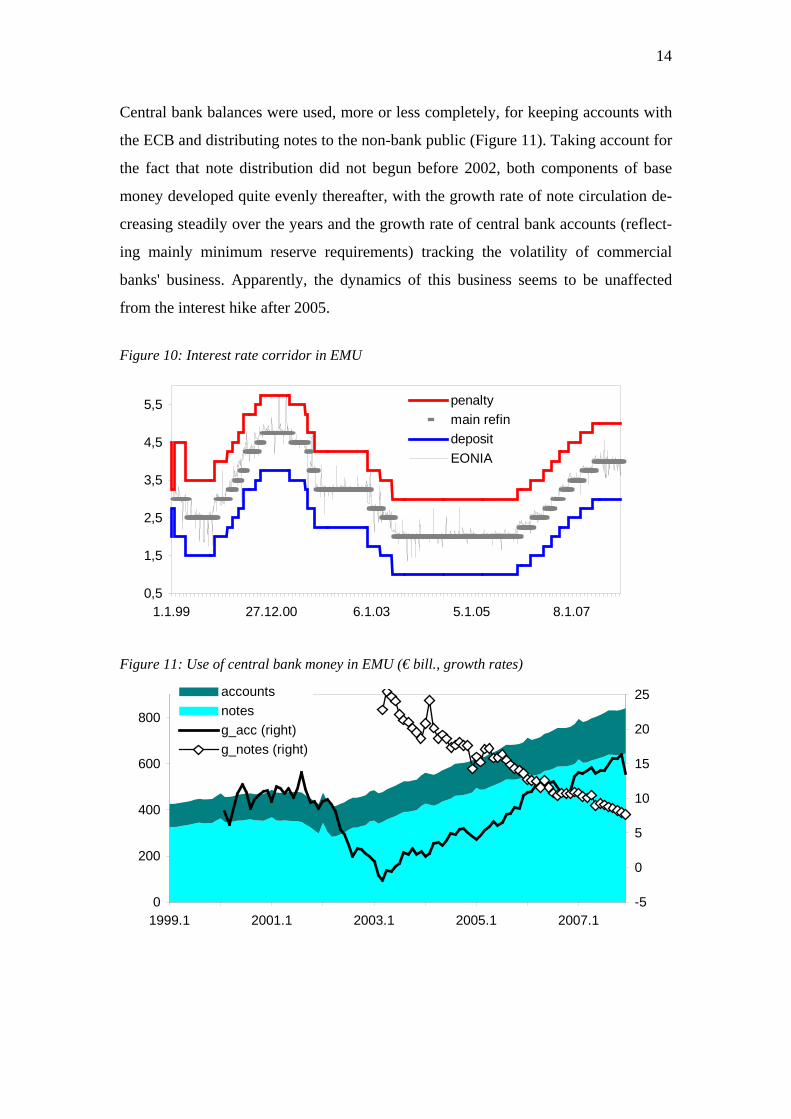

Central bank balances were used, more or less completely, for keeping accounts with

the ECB and distributing notes to the non-bank public (Figure 11). Taking account for

the fact that note distribution did not begun before 2002, both components of base

money developed quite evenly thereafter, with the growth rate of note circulation de-

creasing steadily over the years and the growth rate of central bank accounts (reflect-

ing mainly minimum reserve requirements) tracking the volatility of commercial

banks' business. Apparently, the dynamics of this business seems to be unaffected

from the interest hike after 2005.

Figure 10: Interest rate corridor in EMU

0,5

1,5

2,5

3,5

4,5

5,5

1.1.99 27.12.00 6.1.03 5.1.05 8.1.07

penaltymain refindepositEONIA

Figure 11: Use of central bank money in EMU (€ bill., growth rates)

0

200

400

600

800

1999.1 2001.1 2003.1 2005.1 2007.1-5

0

5

10

15

20

25accountsnotesg_acc (right)g_notes (right)

15

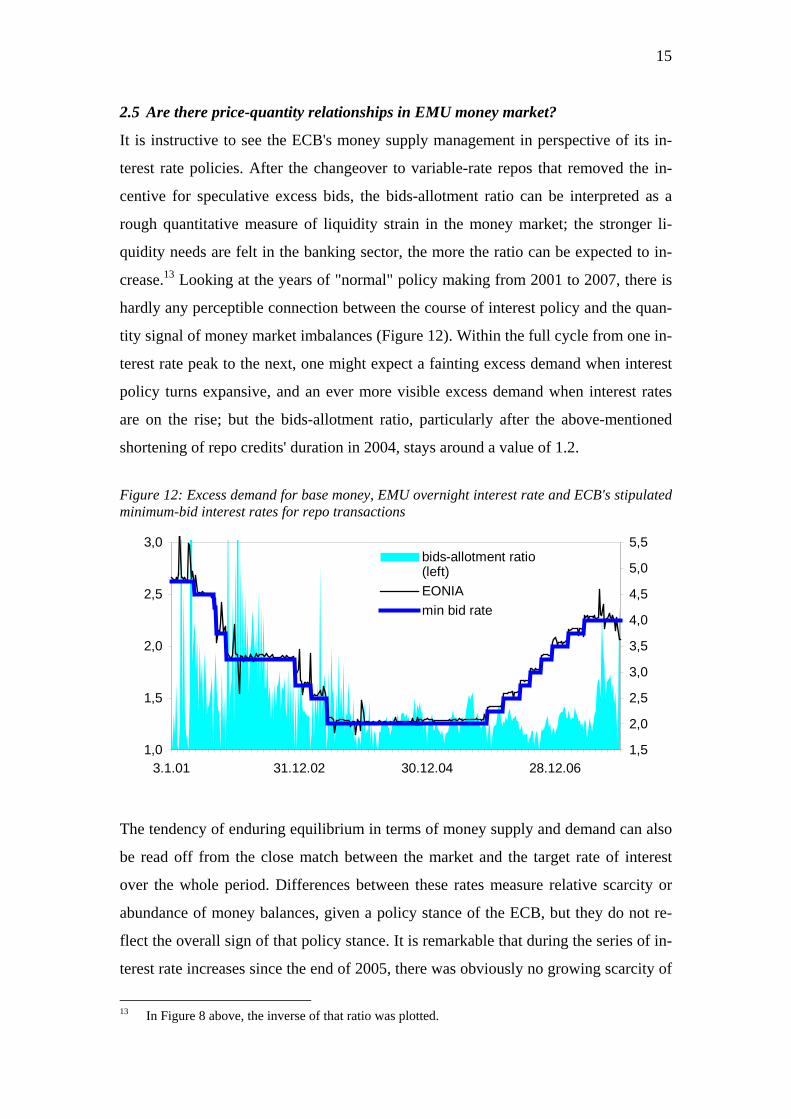

2.5 Are there price-quantity relationships in EMU money market?

It is instructive to see the ECB's money supply management in perspective of its in-

terest rate policies. After the changeover to variable-rate repos that removed the in-

centive for speculative excess bids, the bids-allotment ratio can be interpreted as a

rough quantitative measure of liquidity strain in the money market; the stronger li-

quidity needs are felt in the banking sector, the more the ratio can be expected to in-

crease.13 Looking at the years of "normal" policy making from 2001 to 2007, there is

hardly any perceptible connection between the course of interest policy and the quan-

tity signal of money market imbalances (Figure 12). Within the full cycle from one in-

terest rate peak to the next, one might expect a fainting excess demand when interest

policy turns expansive, and an ever more visible excess demand when interest rates

are on the rise; but the bids-allotment ratio, particularly after the above-mentioned

shortening of repo credits' duration in 2004, stays around a value of 1.2.

Figure 12: Excess demand for base money, EMU overnight interest rate and ECB's stipulated minimum-bid interest rates for repo transactions

1,0

1,5

2,0

2,5

3,0

3.1.01 31.12.02 30.12.04 28.12.061,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

5,5bids-allotment ratio(left)EONIAmin bid rate

The tendency of enduring equilibrium in terms of money supply and demand can also

be read off from the close match between the market and the target rate of interest

over the whole period. Differences between these rates measure relative scarcity or

abundance of money balances, given a policy stance of the ECB, but they do not re-

flect the overall sign of that policy stance. It is remarkable that during the series of in-

terest rate increases since the end of 2005, there was obviously no growing scarcity of

13 In Figure 8 above, the inverse of that ratio was plotted.

16

high-powered money; Figure 11 shows that the stock of base money (notes and ac-

counts) remained on a steady path, with an accelerating growth rate of central bank

accounts. Despite switching to a restrictive course of interest rate policies, the ECB

was accommodating in quantity terms; the behaviour of balances' growth rate was

procyclical.

Nevertheless, the spread of EONIA vis-à-vis the ECB's target rate is generally

positive, which might be interpreted as the result of a liquidity deficit. In order to

judge this argument we have to look more closely into the ECB's money market op-

erations. In American-type repo auctions, banks are invited to place individual bids

where final transactions are settled by using the individual bank's offered interest rate.

Banks may place multiple offers at different interest rates, making the aggregated

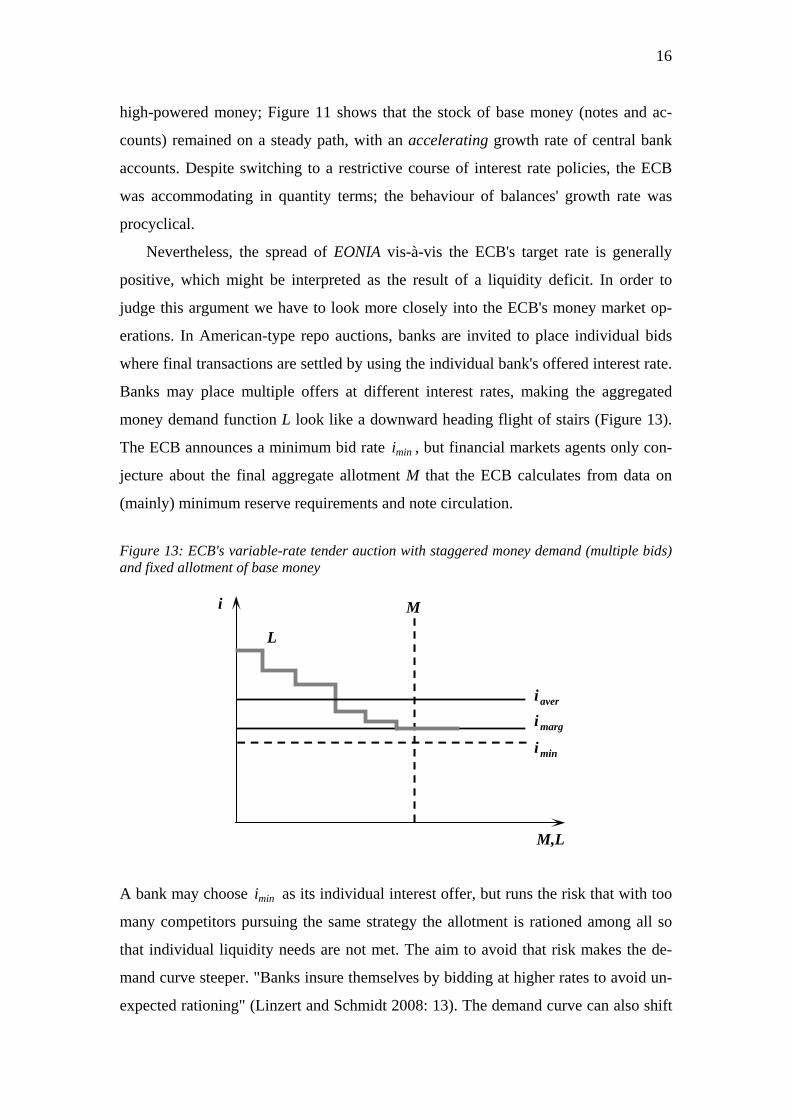

money demand function L look like a downward heading flight of stairs (Figure 13).

The ECB announces a minimum bid rate mini , but financial markets agents only con-

jecture about the final aggregate allotment M that the ECB calculates from data on

(mainly) minimum reserve requirements and note circulation.

Figure 13: ECB's variable-rate tender auction with staggered money demand (multiple bids) and fixed allotment of base money

L

M,L

i

averi

mini

M

margi

A bank may choose mini as its individual interest offer, but runs the risk that with too

many competitors pursuing the same strategy the allotment is rationed among all so

that individual liquidity needs are not met. The aim to avoid that risk makes the de-

mand curve steeper. "Banks insure themselves by bidding at higher rates to avoid un-

expected rationing" (Linzert and Schmidt 2008: 13). The demand curve can also shift

17

upwards resulting in an intersection of L and M above the mini line. This market equi-

librium determines the effective marginal bid rate margi . As each banks pays its own

offered rate there is also an average bid rate averi , which necessarily lies above mini .

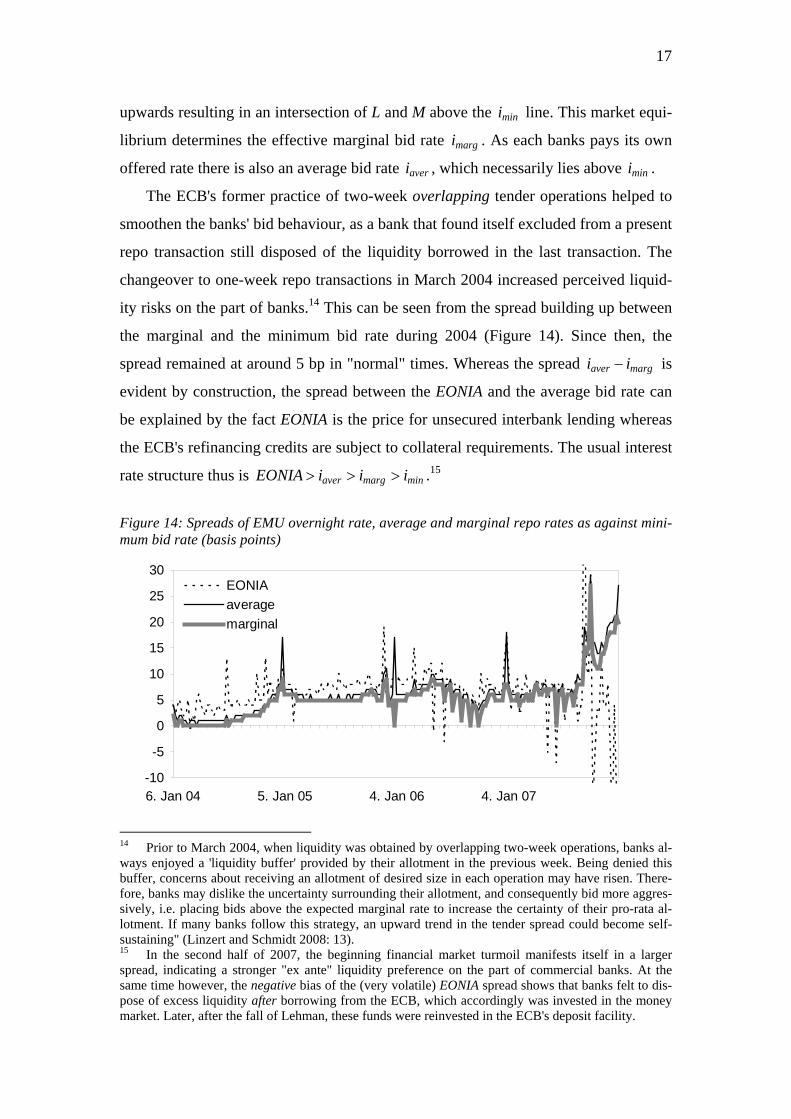

The ECB's former practice of two-week overlapping tender operations helped to

smoothen the banks' bid behaviour, as a bank that found itself excluded from a present

repo transaction still disposed of the liquidity borrowed in the last transaction. The

changeover to one-week repo transactions in March 2004 increased perceived liquid-

ity risks on the part of banks.14 This can be seen from the spread building up between

the marginal and the minimum bid rate during 2004 (Figure 14). Since then, the

spread remained at around 5 bp in "normal" times. Whereas the spread aver margi i− is

evident by construction, the spread between the EONIA and the average bid rate can

be explained by the fact EONIA is the price for unsecured interbank lending whereas

the ECB's refinancing credits are subject to collateral requirements. The usual interest

rate structure thus is aver marg minEONIA i i i> > > .15

Figure 14: Spreads of EMU overnight rate, average and marginal repo rates as against mini-mum bid rate (basis points)

-10

-5

0

5

10

15

20

25

30

6. Jan 04 5. Jan 05 4. Jan 06 4. Jan 07

EONIAaveragemarginal

14 Prior to March 2004, when liquidity was obtained by overlapping two-week operations, banks al-ways enjoyed a 'liquidity buffer' provided by their allotment in the previous week. Being denied this buffer, concerns about receiving an allotment of desired size in each operation may have risen. There-fore, banks may dislike the uncertainty surrounding their allotment, and consequently bid more aggres-sively, i.e. placing bids above the expected marginal rate to increase the certainty of their pro-rata al-lotment. If many banks follow this strategy, an upward trend in the tender spread could become self-sustaining" (Linzert and Schmidt 2008: 13). 15 In the second half of 2007, the beginning financial market turmoil manifests itself in a larger spread, indicating a stronger "ex ante" liquidity preference on the part of commercial banks. At the same time however, the negative bias of the (very volatile) EONIA spread shows that banks felt to dis-pose of excess liquidity after borrowing from the ECB, which accordingly was invested in the money market. Later, after the fall of Lehman, these funds were reinvested in the ECB's deposit facility.

18

The upshot of all this is that the various spreads with respect to the minimum bid rate

should not be seen as reflecting a deliberate policy of shortening the money supply.

Rather these spreads are caused by structural features of the EMU money market and

the techniques of liquidity provision. The series of interest rate increases that started

in December 2005 basically had no bearing on the structure of these short-term rates.

True, there is no target for base money in EMU. But the accommodating behav-

iour of monetary policy with respect to the supply of narrow money obviously also

had repercussions on business conditions in the banking sector at large, on the growth

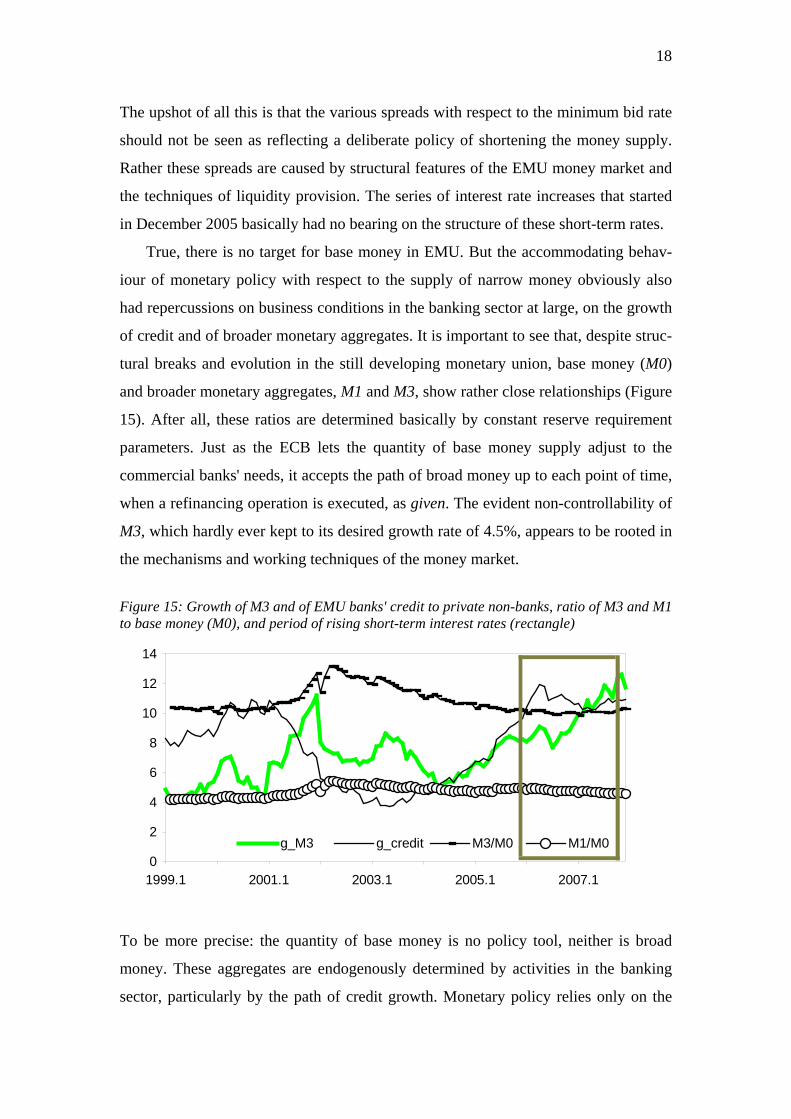

of credit and of broader monetary aggregates. It is important to see that, despite struc-

tural breaks and evolution in the still developing monetary union, base money (M0)

and broader monetary aggregates, M1 and M3, show rather close relationships (Figure

15). After all, these ratios are determined basically by constant reserve requirement

parameters. Just as the ECB lets the quantity of base money supply adjust to the

commercial banks' needs, it accepts the path of broad money up to each point of time,

when a refinancing operation is executed, as given. The evident non-controllability of

M3, which hardly ever kept to its desired growth rate of 4.5%, appears to be rooted in

the mechanisms and working techniques of the money market.

Figure 15: Growth of M3 and of EMU banks' credit to private non-banks, ratio of M3 and M1 to base money (M0), and period of rising short-term interest rates (rectangle)

0

2

4

6

8

10

12

14

1999.1 2001.1 2003.1 2005.1 2007.1

g_M3 g_credit M3/M0 M1/M0

r

To be more precise: the quantity of base money is no policy tool, neither is broad

money. These aggregates are endogenously determined by activities in the banking

sector, particularly by the path of credit growth. Monetary policy relies only on the

19

relative-price effect that is triggered by a change of short-term interest rates:

i credit M3 base moneyΔ → Δ → Δ → Δ (Disyatat 2008). Put differently: the central

bank adjusts base money supply not before its previous interest rate impulses have

succeeded to alter the path of commercial banks' credits and deposits. However, the

recent experience of a continuing increase of credits and deposits despite a series of

restrictive interest rate moves since December 2005 (Figure 15) raises some doubts

whether this instrument alone is always sufficient to control activities in the banking

sector. Credit growth flattened out after a while, but M3 growth resumed.

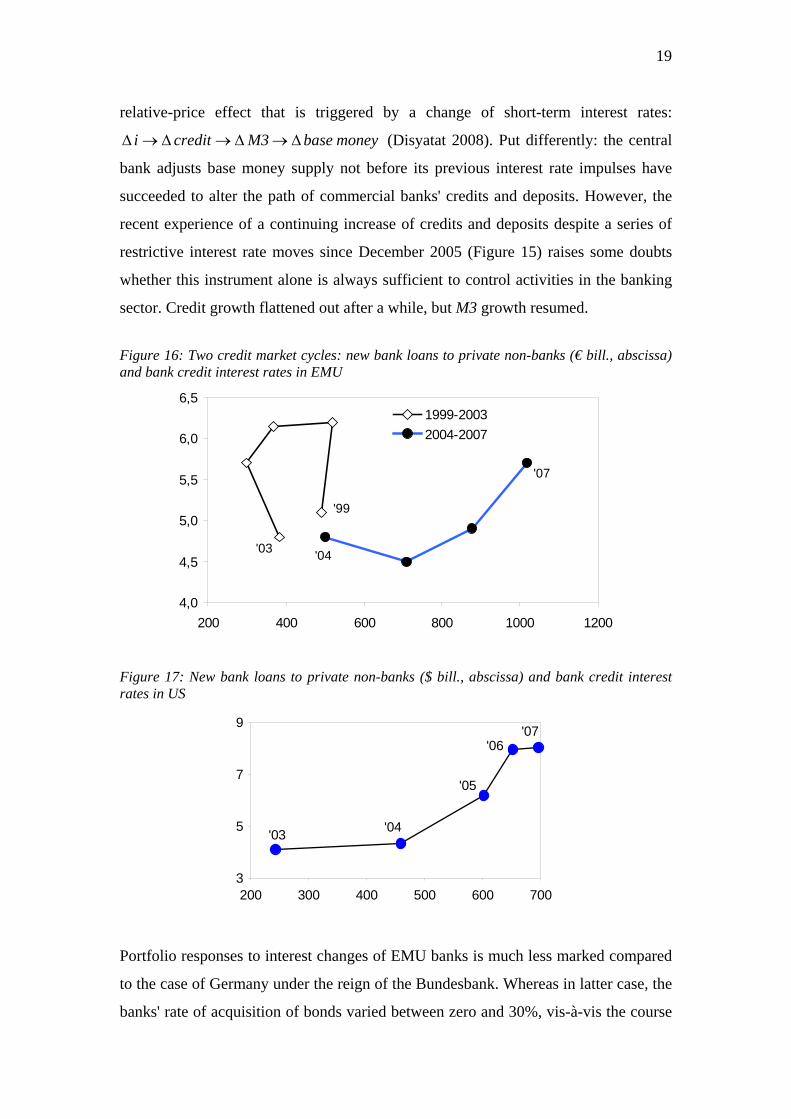

Figure 16: Two credit market cycles: new bank loans to private non-banks (€ bill., abscissa) and bank credit interest rates in EMU

4,0

4,5

5,0

5,5

6,0

6,5

200 400 600 800 1000 1200

1999-20032004-2007

'99

'03 '04

'07

Figure 17: New bank loans to private non-banks ($ bill., abscissa) and bank credit interest rates in US

3

5

7

9

200 300 400 500 600 700

'07'06

'05

'04'03

Portfolio responses to interest changes of EMU banks is much less marked compared

to the case of Germany under the reign of the Bundesbank. Whereas in latter case, the

banks' rate of acquisition of bonds varied between zero and 30%, vis-à-vis the course

20

of short-term interest rates, this reaction is much more muted in the case of EMU.

This can be interpreted to indicate that EMU banks, in times of monetary restriction,

feel less liquidity stress in quantitative terms. A second distinction from the former

German case is the pattern of prices and quantities on the credit market (Figures 3 and

16). It has been argued above that a north-western movement of the market equilib-

rium point in times of a monetary restriction can be understood as a shift of the credit

supply curve that in turn signals a fundamental reaction of the banking sector with re-

spect to the policy stance of the central bank. This type of market behaviour cannot be

observed after 2000. Particularly after 2005, loan supply simply follows a series of

expansive credit demand shifts; ECB interest rate policies for a long time were not

able to stop credit market dynamics. The same pattern of market behaviour can be ob-

served in the US16 from 2003 to 2007 where the volume of new loans grew along with

rising bank credit interest rates and − not shown in Figure 17 − rising Federal Funds

rates.

3. Re-inventing money as a policy tool

Although the ECB has an eye on broad money aggregates, executing some kind of

money supply restriction was not a serious option. The "monetary pillar" never was

intended to impinge on the technique of liquidity policies. It seems that modern theory

and practise of central banking has given up the strategic use of monetary aggregates

altogether. Independence of base money and short-term interest rates nowadays seems

to be the characteristic feature in many countries. Disyatat, who gives further empiri-

cal impressions of monetary policies in EMU, US, UK and Australia, concludes:

"Balances [i.e. central bank accounts] are generally anchored around a fixed trend

while interest rates can be varied across a wide range and there is no perceptible link

between the two" (2008: 4).

The question is whether we can do better. This is not meant to indicate a plea for

returning to monetarism or any kind of monetary targeting. The never ending stream

of papers showing the long-term co-integration of money and prices17 in no way

proves any causality from money to prices (Woodford 2008). Also, the much debated

16 Due to space limitations, a more detailed analysis of the US money market cannot be given here. 17 One of the latest examples is Benati (2009).

21

efficiency of monetary aggregates as information tools, enhancing the decision basis

of interest moves, is not the point of issue here. Rather, the coincidence of the modern

"norm" of endogenous base money supply and the repeated occurrence of asset mar-

ket bubbles in recent times lends support to the tentative hypothesis that there is more

than just an accidental concurrence: if commercial banks, as a rule, do not perceive to

be exposed to any quantitative liquidity constraints, there is a larger temptation to en-

gage in excess lending, particularly if central banks interest rates are low.

But banks may hope to pass on also rising refinancing costs to their customers;

hence, a series of small increases of short-term interest rates may be insufficient to

halt an asset market bubble if macro prospects still look bright and markets are liquid.

The more fundamental point is that the success of monetary policy, containing infla-

tion for any past period, may increase the willingness on the part of market agents to

incur higher risks in the sphere of financial investment, which in turn raises the prob-

ability of assets price bubbles (Borio and Lowe 2002; Trichet 2008).

Recurring to the scissors effect may provide central banks with an additional tool,

besides the ordinary practise of short-term interest management, that can be employed

in times of monetary stress: in periods of asset price bubbles or run-away inflation.

Changing the quantity of base money, in order to modify the liquidity conditions in

the macro economy, can represent an independent monetary policy instrument if the

money market is organized as a "floor system", which has been suggested by Good-

friend (2002) and Keister et al. (2008). Here, the policy target interest rate coincides

with a deposit rate that remunerates voluntary holdings of money balances with the

central bank. This establishes a kink in the commercial banks' demand function for

high-powered money L; it shows a zero slope as long as the money supply M exceeds

the banks' primary money demand (i.e. borrowed reserves) at the target rate 0i∗ (Fig-

ure 18). In order to maintain a market equilibrium at point A, the central bank injects,

e.g. by means of open-market purchases of long-term securities, an amount of AB of

non-borrowed reserves into the financial system, which are held in central bank ac-

counts yielding the deposit rate of interest. Varying 1M M> provides "liquidity ser-

vices" to the private sector, which was specified by Goodfriend (already in 2002!) as a

kind of "quantitative easing" in times of deflation and financial market stress.

Of course, both policy tools can also be applied to execute a monetary restriction.

Starting from A, a rise of the target rate from 0i∗ to 1i∗ can be accompanied by a reduc-

22

tion of the money supply to 1M or 2M ; open-market sales of securities tend to in-

crease the capital market rate of interest. A further reduction of base money supply

below 2M will bring about a liquidity squeeze within the banking system that causes

the money market rate of interest to exceed the (new) target rate. At first sight, this

appears to cause a "signalling" problem: either the central bank is considered as being

unable to realize the target rate it has communicated to the public, or it might be re-

proached for deviating from the announced target. But massive reductions of base

money, which will cause a gap between the effective and the target rate of interest, are

no part of the regular way of policy making; central banks will recur to these meas-

ures on rare occasions only. Here, an announcement that the scissors strategy might

cause money market rates to rise beyond the target rate will even emphasize the cen-

tral bank's determination to bring (asset and/or goods) prices back on track.

Figure 18: Market for central bank reserves in a floor system

M,L

*0i

i

*1i

L

AB

M0M1M2 4. Conclusions

The debate about the role of money in policy making for decades has been dominated

by the varying reputation of the quantity theory, i.e. the claim that the path of prices is

controlled by the central bank's money supply management. The use of the quantity of

high-powered money as a mere tool to vary liquidity conditions in the financial sys-

tem, although grown out of a long history of central banking, today appears as "old

fashioned", because it contradicts two basic modern axioms:

23

• Properly chosen changes of short-term interest rates are sufficient to maintain macroeconomic stability; and

• the commercial banking sector's liquidity needs should be provided without fric-tions in order to maintain the smooth functioning of the financial system.

Repeated occurrences of asset price bubbles give the impression that financial mar-

kets may have reached a state where they work too "frictionless". And although a

thorough re-regulation should contribute to a more cautious behaviour of financial

market agents, a more resolute control of macro financial conditions might be the part

that central banks should take over in order to lean against pronounced price increases

on goods and asset markets. Temporary application of restrictive open-market policies

are apt to signal higher risks in financial markets; to force commercial banks to reduce

credit supply and to liquidate assets; to emphasize the effects emanating from rising

short-term policy target rates; and to support the transmission of these interest rate

policies to the capital market.

These considerations finally allow a suggestion for reforming the "two-pillar

strategy" of the ECB: whereas the monetary pillar gives only dubious support to the

task of controlling ordinary inflation, monetary analysis, i.e. monitoring bank balance

sheets and financial markets activity, may serve as a early warning system for detect-

ing asset price bubbles and as a guide for deciding on the employment of open-market

policies.

References Bagehot, W. 1873. Lombard Street − A Description of the Money Market. Hyperion: West-

port 1979. Benati, L. 2009. Long Run Evidence on Money Growth and Inflation. ECB Working Paper

1027, Frankfurt. Bernanke, B. S., and I. Mihov. 1997. What Does the Bundesbank Target? European Eco-

nomic Review 41: 1025-1053. Beyer, A. et al. 2009. Opting out of the Great Inflation − German Monetary Policy after the

Break Down of Bretton Woods. ECB Working Paper 1020, Frankfurt. Bindseil, U. 2004. The Operational Target of Monetary Policy and the Rise and Fall of the

Reserve Position Doctrine. ECB Working Paper 372, Frankfurt. Blinder, A. S. 1998. Central Banking in Theory and Practice. MIT Press: Cambridge / Lon-

don. Borio, C., and P. Lowe. 2002. Asset Prices, Financial and Monetary Stability − Exploring the

Nexus. BIS Working Paper 114, Basel. Disyatat, P. 2008. Monetary Policy Implementation − Misconceptions and Their Conse-

quences. BIS Working Papers 269, Basel. Emminger, O. 1986. D-Mark, Dollar, Währungskrisen. DVA: Stuttgart.

24

European Central Bank. 2008. 10th Anniversary of the ECB. Monthly Bulletin, Special Edi-tion, May.

Friedman, M., and A. J. Schwartz. 1963. A Monetary History of the United States, 1867-1960. Princeton University Press: Princeton 1990.

Galí, J. et al. 2004. The Monetary Policy Strategy of the ECB Reconsidered. Monitoring the European Central Bank 5, CEPR, London.

Goodfriend, M. 1983. Discount Window Borrowing, Monetary Policy, and the Post-October 6, 1979 Federal Reserve Operating Procedure. Journal of Monetary Economics 12: 343-356.

Goodfriend, M. 2002. Interest on Reserves and Monetary Policy. Federal Reserve Bank of New York, Economic Policy Review, May, 1-8.

Goodfriend, M., and R. G. King. 2005. The Incredible Volcker Disinflation. Journal of Mone-tary Economics 52: 981-1015.

Goodhart, C. A. E. 1989. The Conduct of Monetary Policy. Economic Journal 99: 293-346. Goodhart, C. A. E. 2007. Whatever Became of the Monetary Aggregates? National Institute

Economic Review, 200: 56-61. Hagen, J. von. 1999. Money Growth Targeting by the Bundesbank. Journal of Monetary

Economics 43: 681-701. Irmler, H. 1972. The Deutsche Bundesbank's Concept of Monetary Theory and Monetary Pol-

icy. In: Brunner, K., ed.: Proceedings of the First Konstanzer Seminar on Monetary The-ory and Monetary Policy. Beihefte zu Kredit und Kapital, 1, Berlin, 137-164.

Issing, O. 1992. Theoretical and Empirical Foundations of the Deutsche Bundesbank's Mone-tary Targeting. Intereconomics 27: 289-300.

Keister, T. et al. 2008. Divorcing Money from Monetary Policy. Federal Reserve Bank of New York, Economic Policy Review, September, 41-56.

Keynes, J. M. 1930. A Treatise on Money, 2: The Applied Theory of Money. The Collected Writings of John Maynard Keynes, Vol. VI, Macmillan: London and Basingstoke 1971.

König, R. 1996. The Bundesbank's Experience of Monetary Targeting. In: Deutsche Bundes-bank, ed.: Monetary Policy Strategies in Europe. München, 107-140.

Lindsey, D. E. et al. 2005. The Reform of October 1979 − How It Happened and Why. Fed-eral Reserve Bank of St. Louis Review 87: 187-235.

Linzert, T., and S. Schmidt. 2008. What Explains the Spread between the Euro Overnight Rate and the ECB's Policy Rate? ECB Working Paper 983, Frankfurt.

Lutz, F. A. 1936. Das Grundproblem der Geldverfassung. In: Geld und Währung. Mohr: Tübingen 1962, 28-102.

Nelson, E. 2007. Comment on Samuel Reynard 'Maintaining Low Inflation - Money, Interest Rates, and Policy Stance'. Journal of Monetary Economics 54: 1472-1479.

Reynard, S. 2007. Maintaining Low Inflation - Money, Interest Rates, and Policy Stance. Journal of Monetary Economics 54: 1441-1471.

Sachverständigenrat. 1966. Expansion und Stabilität. Jahresgutachten 1966/67. Bonn. Sachverständigenrat. 1974. Vollbeschäftigung für morgen. Jahresgutachten 1974/75. Bonn. Spahn, H.-P. 2001. From Gold to Euro − On Monetary Theory and the History of Currency

Systems. Springer: Berlin and Heidelberg. Thornton, H. 1802. An Enquiry into the Nature and Effects of the Paper Credit of Great Brit-

ain. Kelley: New York 1962. Trichet, J.-C. 2008. Risk and the Macro-Economy. Speech at the Conference "The ECB and

its Watchers X", Frankfurt. Woodford, M. 2000. Monetary Policy in a World Without Money. International Finance 3/2:

229-260. Woodford, M. 2007. Does a 'Two-Pillar Phillips Curve' Justify a Two-Pillar Monetary Strat-

egy? Columbia University, New York. Woodford, M. 2008. How Important Is Money in the Conduct of Monetary Policy? Journal of