28

Money Management: Part 1

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | caren-walsh |

| View: | 222 times |

| Download: | 0 times |

Money Management: Part 1

Homework

(Passport page 18)

How’s It Going?

Money Management

• Tracking our Spending

• Setting Goals

• Creating a Budget

What Do You Know?

(Pre-Test page 4)

Let’s Talk About

You

Did You Know?• 61% of U.S. households don't have a budget.

• More than 11 million Americans have no idea how much they spend on food, housing and entertainment and don’t keep track of overall spending.

• 24% of U.S. households report not paying all their bills on time.

• 1 in 3 adults (34%) carry credit card debt from month-to-month. 15% or 35 million people carry $2,500 or more of credit card debt monthly.

• 32% of U.S. adults do not save any portion of their income for retirement, and 34% have no emergency savings.

Source: April 2014 Consumer Financial Literacy Survey by Harris Interactive, Inc

Budgeting Process

Organize Data

Periodic and Goal Spending

Build Budget

Evaluate and

Adjust Plan

TrackingData

Collection

Tracking Your Spending

• Write down where your money goes ~ every dime, every dollar.

• Consider the automatic spending that you may have in place (payroll withholdings, EFT payments, child support, etc.).

• Track it for a minimum of two weeks ~ preferably for a month.

• Where are your temptations? What needs to be controlled?

• Is it a want or a need?

Separating Wants and NeedsWants Needs

Home phone (landline)

Cell phone(s)

Cable or satellite television

High-speed internet access

Gym membership or other memberships

Eating out at restaurants

A second or third vehicle for kids to drive

Vacation trips

New clothing for every style and season

Purchasing music, books or other hobby items

Going to concerts, movies or other events

Being able to buy lunch instead of “brown bagging” it

Types of Expenses

• Fixed• Variable• Periodic

• Discretionary• Non-discretionary

Organize DataTRACKER $$

X-Mart: apples, socks, paper

$ 23.59

Car Payment $259.34

Convenience Store: gas and coffee

$35.97

Electricity $ 159.75

Rent $950

Restaurant: lunch

$8.23

CATEGORY $$

Groceries $ 5.39

Eating Out $ 9.66

Auto $ 293.88

Misc $7.25

Housing $1,109.75

Clothing 10.95

Spending Tracker By Category

Week 1 Week 2 Week 3 Week 4 Total

Housing 850 120 75 1045

Groceries 250 20 100 370

Auto 50 300 100 50 500

Debt 100 100

Entertainment 30 10 70 10 120

Clothing 50 50

Savings 100 100 200

Medical 120 45 120 285

Miscellaneous 35 20 55

Investments 50 50 100

Education/Childcare

Charitable 30 30 30 30 120

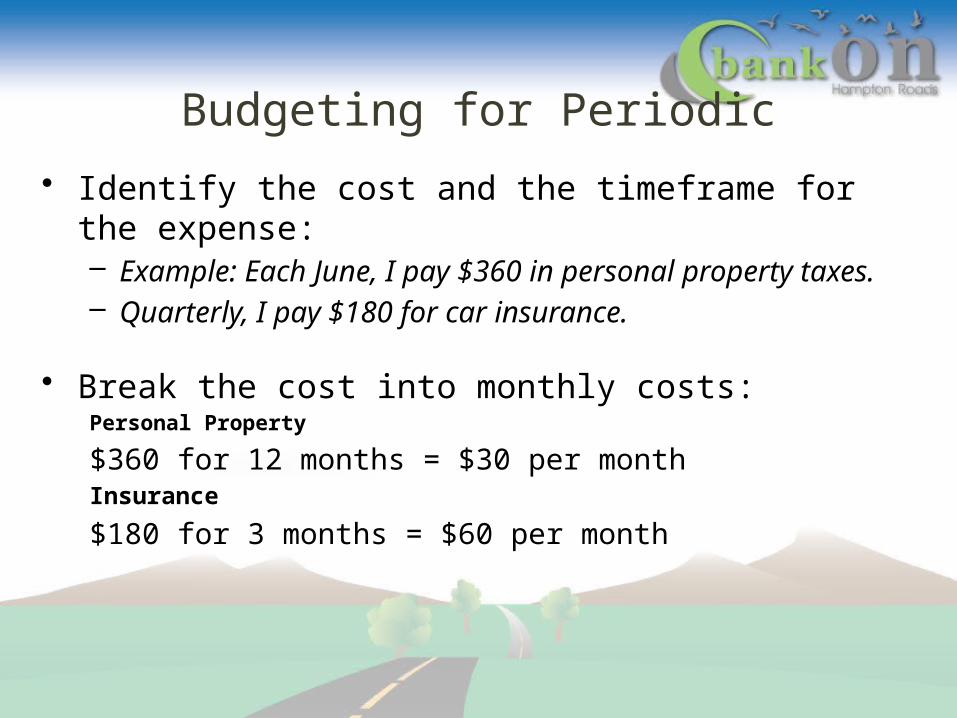

Budgeting for Periodic

• Identify the cost and the timeframe for the expense:– Example: Each June, I pay $360 in personal property

taxes.– Quarterly, I pay $180 for car insurance.

• Break the cost into monthly costs:Personal Property

$360 for 12 months = $30 per monthInsurance

$180 for 3 months = $60 per month

Planning for the Periodic

Frequency# of Months Amount Monthly

Property Tax Annual 12 $360 $30

Insurance Quarterly 3 $180 $60

Furniture/Appliances Every 3 years 36 $720 $20

Home Repairs Annual 12 $600 $50

Car Maintenance/Repair2 times per

yr. 6 $300 $50

Membership/Dues Annual 12 $60 $5

Holidays/Birthdays Annual 12 $1200 $100

Subscriptions Annual 12 $60 $5

Vacation Annual 12 $1200 $100

Weddings/Events Annual 12 $120 $10

Tuition/Books/School 3 times per

yr. 4 $400 $100

Clothing Quarterly 3 $120 $40

Planning for the Periodic Expense Budget Spent Saved

January School/Clothing 570 520 50

February Insurance 570 180 390

March Car Maintenance 570 300 270

April Taxes/Clothing/School 570 800 -230

May Insurance/Graduation 570 480 90

June Personal Property/Birthday 570 460 110

July Clothing/Vacation 570 1,320 -750

August Insurance/Back to School 570 580 -10

September Car Maintenance/Dues 570 360 210

October Clothing/School 570 520 50

November Insurance 570 180 390

December Holidays 570 1,200 -630

Setting Goals

• Short-Term Goals: less than one year

• Long-Term Goals: more than one year

• S.M.A.R.T. Goals

S.M.A.R.T. Goals• Specific: State exactly what is to be done

• Measurable: Include how the goal can be measured

• Actionable: Determine steps to reach the goal

• Realistic: Do not set goals for something unrealistic

• Time-Bound: State when the goal will be met

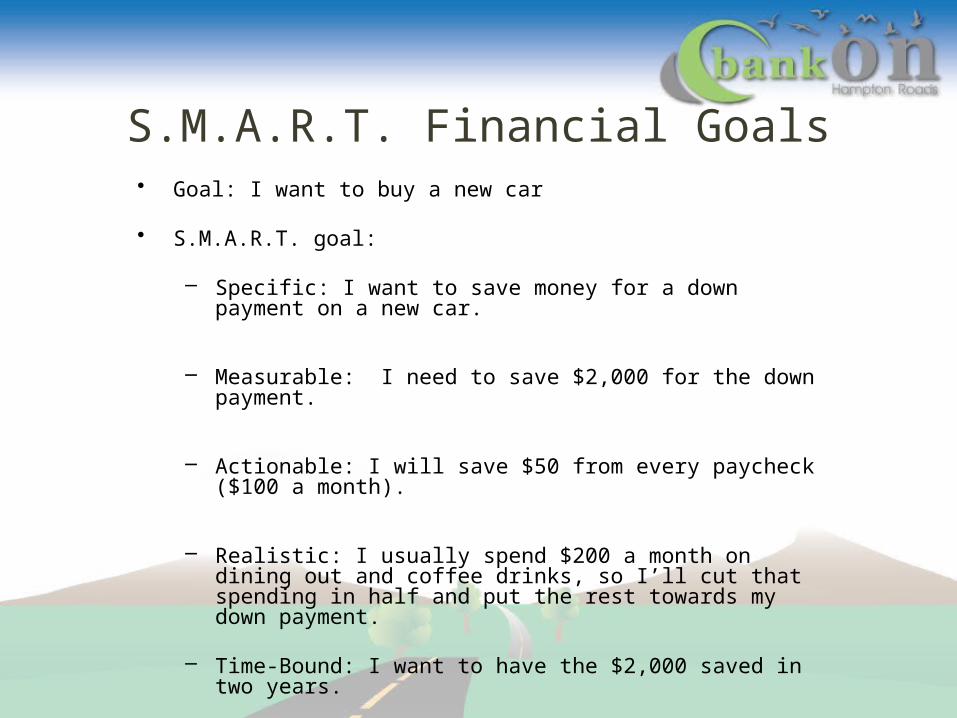

S.M.A.R.T. Financial Goals• Goal: I want to buy a new car

• S.M.A.R.T. goal:

– Specific: I want to save money for a down payment on a new car.

– Measurable: I need to save $2,000 for the down payment.

– Actionable: I will save $50 from every paycheck ($100 a month).

– Realistic: I usually spend $200 a month on dining out and coffee drinks, so I’ll cut that spending in half and put the rest towards my down payment.

– Time-Bound: I want to have the $2,000 saved in two

years.

Budgeting for Goals• Identify the cost and the timeframe for

the goal:– Example: I want to save $3,000 over the next

two years for a down payment on a new car.• Break the cost into annual costs

– $3,000 for 2 years = $1,500 per year• Divide annual cost by 12 to get monthly

amount needed:– $1,500/12 = $125 monthly

Prioritizing Goals• Rank Goals in order of importance.

– What is your number one priority?

– Engage the entire family.

• Prioritizing Goals helps when evaluating spending choices.

• When there are conflicts among goals, highest priority wins.

Strategies for Goals

When conflicts arise for achieving goals: 1.Evaluate: What is really most important?2.Can one goal be adapted (modified) to allow both to be achieved?3.Can I generate income or reduce expenses to make both goals possible?

Problem Solving

Goal: Have $1,000 saved for holidays so that you can purchase gifts and visit family members in another state.

Conflict: You also need $800 to purchase books for the January semester of college. You are working to complete your degree.

It is currently September, and you don’t think you will have enough money for both. What are your options?

Creating YOUR Budget• Your spending trackers.

– Remember, you’ll need at least two weeks worth of data, but more is even better.

• Historical data from paystubs, bank and credit card statements.

• Your S.M.A.R.T. goals and other priorities (paying off debt, vacation, etc.). – Be sure to record how much money you’ll

need for these.• Your income and expenses ~ fixed, variable and

periodic.

Tracking/Collecting DataWHERE DID $$$ GO?

HISTORICAL RECORDS

WHERE SHOULD $$$ GO?

FUTURE PLANNING

Spending Tracker Emergency Savings

Bank Statements Periodic Expense Planner

Credit Card Statements S.M.A.R.T Goals

Computer/Online: Quicken/Mint/etc.

Debt Repayment

What Have You Learned?(Post-Test page 18)

Homework

(Passport page 22)

Questions?