SAVVY SHOPPING SESSION #5 Money Management The Money Management sessions have been developed for the HSBC Opportunity Partnership in collaboration with Catch22, St Giles Trust, The Prince's Trust, Tomorrow's People and pfeg (Personal Finance Education Group)

Transcript

Savvy ShoppingSESSION #5

Money Management

The Money Management sessions have been developed for the HSBC Opportunity

Partnership in collaboration with Catch22, St Giles Trust, The Prince's Trust, Tomorrow's

People and pfeg (Personal Finance Education Group)

Session #5

IntroductIon

Marketing offers, terms and conditions, and linked products are all part of today’s shopping experience, but this can prove a daunting and, at

times, intimidating prospect for many young people. This session looks at developing the skills required to question the appropriateness of offers,

investigate full terms and conditions, and understand the consequences of inappropriate use of store cards. It also begins to explore the legal rights of the consumer. This session links well to Session 3 – Spending and Saving.

By the end of the session the young people will:

Be able to compare offers and choose the most appropriate to an individual’s needs

Appreciate the importance of reading the small print in sales contracts

Know basic consumer rights in relation to the purchase of goods

LearnIng outcoMeS reSourceS

Session #5

Facilitator's Notes

SettIng the Scene

Ask the young people if they have picked up a bargain recently. Take feedback and then ask how they know it was a bargain. Some of the young people may say that there was a particular offer on the item they bought. Ask them to name as many different types of offer as they have come across.

This may include:

• Buy one get one free• A percentage discount• A certain amount off• Discount for buying online• Promotion codes

Explain that most offers are a form of marketing aimed at persuading people to buy particular products. If you needed the product anyway then you have made a saving, but if the offer has tempted you to spend on something you don’t need then it might not be such a bargain after all – the marketing has influenced your decision.

The area of supermarket marketing can be an interesting area to explore further with young people. The psychology of placing goods in different places within the store, using different colours and even the use of appropriate smells can influence shopping behaviour.

15minsStarter

Session #5

Facilitator's Notes

deaL or no deaL 15mins

Introduce this exercise by asking the group if they know the television programme “Deal or No Deal”. Explain to the group that we are going to play a short game now and that they are going to have a go at working out the best deals for five different scenarios. Place the cards showing the five deals in Resource 1 – Deal or No Deal in different places around the room. Give each young person one of the ‘DEAL’ cards. Read out the first scenario and ask the young people to put their ‘DEAL’ card next to the best deal for that scenario. Once all of the young people have made a decision and placed their card, find out if there is a general consensus. Explore why the young people chose the deal they did, and if anyone chose differently find out their reasoning.

Give out a ‘NO DEAL’ card to each young person and ask them to place it on one of the offers which would definitely not be a good deal for the scenario, and again ask for reasons why. The best deal solutions have been provided so that you can give answers. There can be a number of different options for the ‘No Deal’ selection therefore no answers have been provided, but it is useful to discuss the reasoning behind the young people’s decisions.

Once all of the young people have made a decision and placed their card, find out if there is a general consensus. Explore why the young people chose the deal they did, and if anyone chose differently find out their reasoning. Ask which of the offers would definitely not be a good deal for the scenario, and again ask for reasons why. The best deal solutions have been provided so that you can give answers.

Continue the activity with all five of the scenarios. If you have time at the end you could ask the young people to come up with a scenario for themselves; they could read it out for the others in the group to have a go at answering.

The key learning from this activity is that whether an offer is a ‘good’ deal or not depends upon the circumstances. Explain that whilst an offer may be right for some, it may not be appropriate for others.

Core Activity

Session #5

Facilitator's Notes

Store cardS 10minsCore Activity

Find out if any of the young people have been asked if they want to take out a store card when they have bought items from a shop (usually clothing retailers). Explain that shops often offer a discount on your purchases if you take out their store card. The cost of your purchases is put on the card and then you pay it off in a similar way to a credit card. Read through Resource 2 – Rhiannon’s Case Study. Discuss the choices that Rhiannon made in the case study. What could she have done differently?

The distinction between store cards and credit cards is fairly slight, and as such young people are often confused with the differences. It can be worth expanding on these to ensure the young people know how the two differ e.g. store cards can be used to pay for goods in only one store or chain of stores, whereas credit cards can be used far wider.

revIew 5mins

Recap on the learning objectives for the session and discuss with the young poeple whether they feel they now understand those learning objectives:

• Be able to compare offers and chose the most appropriate to an individual’s needs• Appreciate the importance of reading the small print in sales contracts• Know basic consumer rights in relation to the purchase of goods

Core Activity

Session #5

Facilitator's Notes

extenSIon 15mins

Understanding your consumer rights is a key part of being a savvy shopper. Hand out the situations in Resource 3 – Refund or Not? Ask the young people to decide, for each situation, whether they think they would be able to get a refund or not. Take feedback for each one along with the young people’s reasoning. Answers are provided in Resource 3 – Refund or Not? – Answers.

Summarise that all goods purchased from a retailer should be:

• Of satisfactory quality• As described• Fit for purpose

These apply irrespective of whether the goods are on offer or in a sale. Any goods failing any of these are entitled to a full refund on return to the retailer. Share with the young people that this all falls under the Sale of Goods Act 1979.

Young people tend to find the best bargains online, sometimes from sites in countries outside of the EU. If there is time, you may want to consider the fact that as consumers they have far less protection in the event of faulty, counterfeit, or even non receipt of the goods. The level of cover depends upon each individual countries' law. Irrespective of these consumer laws the problem of raising a complaint can be difficult in itself, especially in countries for which English is not a first language. In some cases the cost of returning the goods makes the process prohibitive. If the young people are going to buy from abroad they should check out the company to ensure it is reputable, and what the returns policy is before trading.

Core Activity

Session #5

Facilitator's Notes

Budget A way of planning for the money you have coming in and going out.

SeSSIon gLoSSary

Consumer Credit Act, 1974

The Act requires most businesses that lend money or provide credit to be licensed, and provides consumers with a variety of rights.

Tariff This is simply a list of prices for different good or services. Gas, electricity and mobile device prices often use a tariff system.

Debit card A plastic card that can be used to purchase goods and services. The money spent will come straight out of your bank account.

Deposit A sum of money paid up front to secure a product, service or property.

Sale of Goods Act 1979

This legislation states that goods must be as described, of satisfactory quality and fit for purpose. It details the consumer rights if these are not adhered to.

Store card A plastic card that provides credit on purchases in particular stores up to a certain amount. It is used as a method of payment only in the stores it is linked to.

Reward cards (also Loyalty cards)

A card which encourages shopping at one particular store or outlet by rewarding the consumer with points they can accumulate and spend in store instead of cash or discounted products.

Session #5

Continued on next page

Resource #1

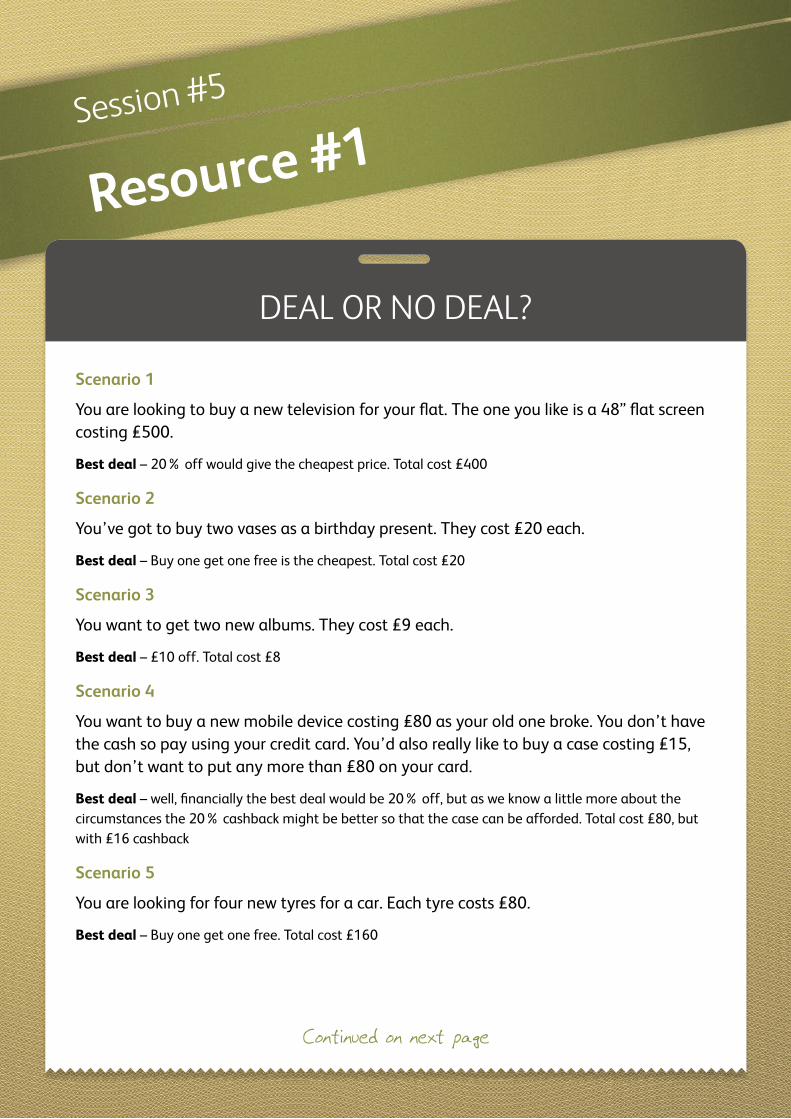

deaL or no deaL?

Scenario 1

You are looking to buy a new television for your flat. The one you like is a 48” flat screen costing £500.

Best deal – 20% off would give the cheapest price. Total cost £400

Scenario 2

You’ve got to buy two vases as a birthday present. They cost £20 each.

Best deal – Buy one get one free is the cheapest. Total cost £20

Scenario 3

You want to get two new albums. They cost £9 each.

Best deal – £10 off. Total cost £8

Scenario 4

You want to buy a new mobile device costing £80 as your old one broke. You don’t have the cash so pay using your credit card. You’d also really like to buy a case costing £15, but don’t want to put any more than £80 on your card.

Best deal – well, financially the best deal would be 20% off, but as we know a little more about the circumstances the 20% cashback might be better so that the case can be afforded. Total cost £80, but with £16 cashback

Scenario 5

You are looking for four new tyres for a car. Each tyre costs £80.

Best deal – Buy one get one free. Total cost £160

Session #5

Resource #1

BUY 1 GET 1 FREE

20% off

Get 20% Cashback

£10 off40% off when you

buy three

Session #5

Resource #1

DEAL

DEAL

DEAL

DEAL

NO DEAL

NO DEAL

NO DEAL

NO DEAL

Session #5

Resource #2

rhIannon’S caSe Study

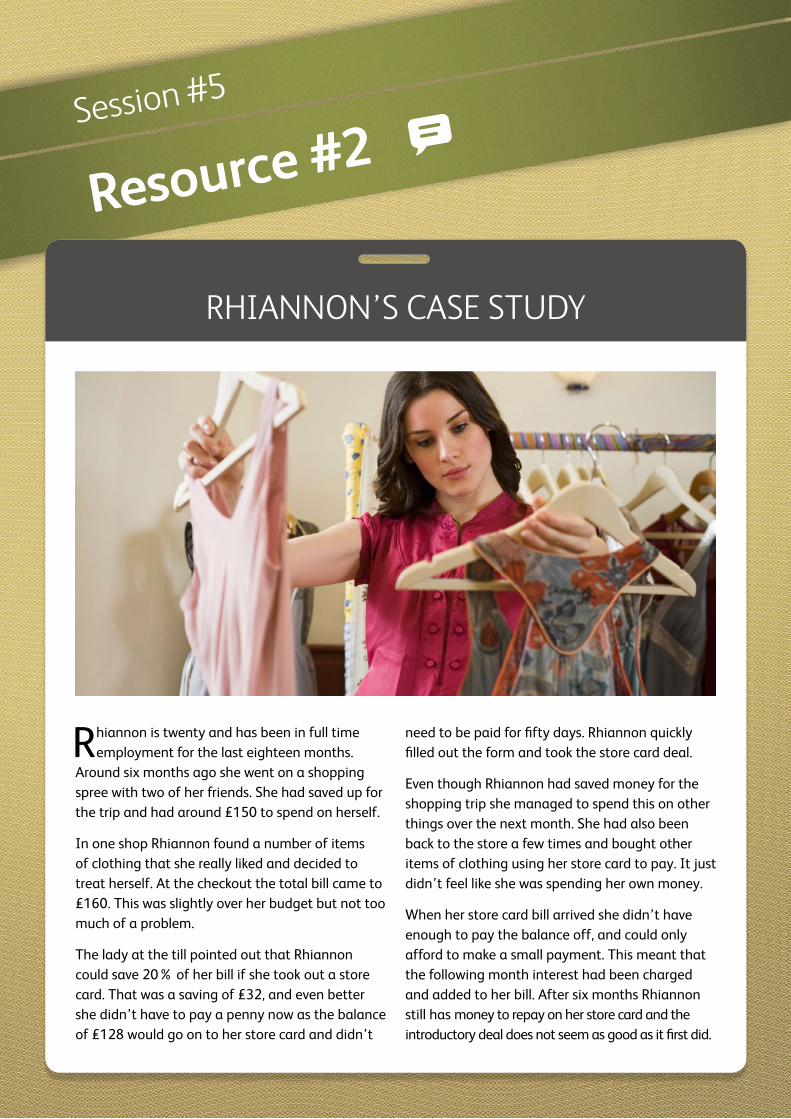

Rhiannon is twenty and has been in full time employment for the last eighteen months.

Around six months ago she went on a shopping spree with two of her friends. She had saved up for the trip and had around £150 to spend on herself.

In one shop Rhiannon found a number of items of clothing that she really liked and decided to treat herself. At the checkout the total bill came to £160. This was slightly over her budget but not too much of a problem.

The lady at the till pointed out that Rhiannon could save 20% of her bill if she took out a store card. That was a saving of £32, and even better she didn’t have to pay a penny now as the balance of £128 would go on to her store card and didn’t

need to be paid for fifty days. Rhiannon quickly filled out the form and took the store card deal.

Even though Rhiannon had saved money for the shopping trip she managed to spend this on other things over the next month. She had also been back to the store a few times and bought other items of clothing using her store card to pay. It just didn’t feel like she was spending her own money.

When her store card bill arrived she didn’t have enough to pay the balance off, and could only afford to make a small payment. This meant that the following month interest had been charged and added to her bill. After six months Rhiannon still has money to repay on her store card and the introductory deal does not seem as good as it first did.

Session #5

Resource #3

refund or not?

Situation 1

You bought a top in a bit of a rush and didn’t have time to try it on in the shop. Once you get home you put it on and realise that it really doesn’t suit you. Are you entitled to a full refund?

Situation 2

After a lot of searching around you find a motorbike you like at a local dealers. You pay a deposit and then go home to sort out insurance for when you collect it. The insurance quotes are far higher than you expected and this means that you can no longer buy the bike. Are you entitled to get your deposit back?

Situation 3

You buy an electronic toy for a friend’s child. They take it out of its packaging and realise that the sound is not working. The packaging has been thrown away. Are you entitled to a full refund?

Situation 4

You buy a new television from an electrical retailer. You pay the full price of £450 using your credit card. They do not deliver on the day they said, and when you try to phone them the line is dead. You find out the business has closed down. Are you entitled to a full refund?

Session #5

Resource #3 FacilitatoR'S noteS

refund or not?

Situation 1You bought a top in a bit of a rush and didn’t have time to try it on in the shop. Once you get home you put it on and realise that it really doesn’t suit you. Are you entitled to a full refund?

The legal answer is you are not entitled to a full refund. There is nothing wrong with the top and therefore the shop does not legally have to give a refund. In practice many shops have a returns policy which allows refunds to be given if customers change their minds. In this case the products will still need to have their original packaging and labels and, in most cases, you will need your proof of purchase (a receipt is perfect).

Situation 2After a lot of searching around you find a motorbike you like at a local dealers. You pay a deposit and then go home to sort out insurance for when you collect it. The insurance quotes are far higher than you expected and this means that you can no longer buy the bike. Are you entitled to get your deposit back?

The legal answer is no, unless the dealer states that it is a refundable deposit. The deposit is a commitment to buy, and as such the trader stops trying to sell that product. Keeping the deposit is compensation for not being able to sell the bike. In reality some traders may have their own policies in relation to deposits and take each case on its own merits.

Situation 3You buy an electronic toy for a friend’s child. They take it out of its packaging and realise that the sound is not working. The packaging has been thrown away. Are you entitled to a full refund?

Yes, a full refund should be provided. The item is faulty, and irrespective of whether the packaging is intact, or even there at all, you are entitled to a full refund. Remember that in most cases proof of purchase will be required, and if you paid for the item using a card (debit or credit) the retailer will normally only credit the amount back to the same card.

Situation 4You buy a new television from an electrical retailer. You pay the full price of £450 using your credit card. They do not deliver on the day they said, and when you try to phone them the line is dead. You find out the business has closed down. Are you entitled to a full refund?

This is an interesting one. Because you did not receive your goods from the retailer they effectively owe you the money you have paid. As they have gone into liquidation you become a creditor of the business (someone they owe money too). The problem is that there will be a large number of creditors, and the chances of getting all of your money back will be very low and may take a very long time. In this situation however, there is another solution. As you paid for the goods worth over £100 using a credit card you are covered by Section 75 of the Consumer Credit Act 1974. This states that the credit card provider is equally liable for any purchases over £100. By contacting your credit card company they will usually credit the money back to your card and then chase the claim against the retailer themselves.

This material is owned by pfeg, produced on 01/03/14

The UK’s leading financial education charity

pfeg Fifth Floor 14 Bonhill St. London EC2A 4BX www.pfeg.orgfollow us on twitter @pfeg_org

pfeg is a registered charity. Registered number 1081639 pfeg is a company limited by guarantee. Registered number 3943766