50

MoneyWi$e: Money Management MoneyWi$e Money Management Training Welcome MoneyWi$e is a joint financial education project of Consumer Action and Capital One

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | beverly-atkins |

| View: | 217 times |

| Download: | 1 times |

MoneyWi$e: Money Management

MoneyWi$eMoney Management Training

Welcome

MoneyWi$e is a joint financial education project of Consumer Action and Capital One

MoneyWi$e: Money Management

The Money Management course will give you...

An understanding of what good money management is and why it is important

Skills and ideas to help you better manage your money

MoneyWi$e: Money Management

Money Management

Session One (Two hours)

MoneyWi$e: Money Management

Course objectives

This seminar will help you understand:– How to prepare a budget– How to balance your accounts– How to cut back on expenses– Ideas for increasing your income– How to save more– How to set financial goals

MoneyWi$e: Money Management

In participants’ folders

Manage Your Money Wisely (brochure) Checkbook Balancing Activity

(worksheet) Money Management Self Evaluation Three Sample Profiles (class exercise) Financial Goals Worksheets Take-home Budget Worksheet Money Management Seminar

Evaluation Form

MoneyWi$e: Money Management

Money management

What is money management?– Knowing how to save, spend and

invest your money so that you and your family can successfully work toward your financial goals

MoneyWi$e: Money Management

Money management activities

What activities go with money management?– Tracking your spending.– Making a budget.– Balancing your checkbook.– Using credit wisely.– Setting long- and short-term goals.– Earmarking money for savings.

MoneyWi$e: Money Management

Be a wise money manager

Wise money management can help you:– Pay your bills on time.– Make it through times when you are

not working.– Save money.– Plan for short- and long-term goals.

MoneyWi$e: Money Management

Budgeting

What is a budget?– A spending plan to help you

forecast and control your expenses.

MoneyWi$e: Money Management

Making a budget

How do you make a budget?– You need to figure out how much

you spend each month and compare that amount to your take-home pay.

– Track your spending for a set period of time, like a month, in order to figure out how much money you spend.

MoneyWi$e: Money Management

Tracking your spending

What are some ways to track how much money you are spending each day, each week, or each month?

MoneyWi$e: Money Management

Ways to track spending

Keep a notebook handy and write down everything you buy and every bill you pay.

Keep all your receipts in an envelope or shoe box.

Create a computer file for entering your income and expenses.

MoneyWi$e: Money Management

Your budget

What are some of the things that should be included in your budget?

MoneyWi$e: Money Management

Your budget may include:

– Housing – Food (groceries, restaurants,

snacks)– Automobile (payments, gas,

repairs, insurance, commuting expenses)

– Clothing & personal grooming– Utilities (electric, gas, water, cable)– Credit card payments

MoneyWi$e: Money Management

Your budget may include:

– Student loan payments– Child care– Insurance payments– Entertainment (movies, concerts,

books)– Medical bills– Vacations– Income taxes

MoneyWi$e: Money Management

Making your budget work

Does your income cover your expenses?

If not, you need to figure out how to spend less or earn more.

MoneyWi$e: Money Management

Bank accounts

A bank account is an important money management tool.

How can a bank account help you manage your money wisely?

MoneyWi$e: Money Management

Bank accounts

A bank account helps you keep track of your spending and how much money you have available.

Use your checkbook register to write down and deduct:– Every check you write– Every ATM or debit card transaction

or purchase– Any bank fees you pay

MoneyWi$e: Money Management

Benefits of a bank account:

Money is safe. Each account is insured. Canceled checks prove you paid

a bill. Having a bank account can save

you money.

MoneyWi$e: Money Management

Let’s take a break

Please come back in 15 minutes.

MoneyWi$e: Money Management

Let’s balance a sample checkbook

Take out the checkbook balancing activity from your folders:– Review the sample bank statement.– Balance the sample checkbook

register.– Balance the sample account using

the checkbook balancing worksheet.

MoneyWi$e: Money Management

Cutting back on expenses

What are some ways to cut back on expenses?

MoneyWi$e: Money Management

Ideas to help you cut back

Shop around and compare prices.

Make a shopping list and stick to it.

Prepare meals and bag lunches at home.

Don’t shop recreationally—you could be tempted to buy things you don’t need

MoneyWi$e: Money Management

More ways to cut back

Use the public library for books, magazines, videos.

Join a buying co-op. Lower your thermostat when

away or sleeping. Walk instead of drive. Look for a free bank account.

MoneyWi$e: Money Management

Increase your income

Ways to earn extra money:– Part-time or weekend job.– Take advantage of income tax

programs, such as the Earned Income Tax Credit.

– Start a home-based business.– Rent out a room.

MoneyWi$e: Money Management

Setting financial goals

Short-term goal (1-2 years) — buying a new car, getting a degree or planning a wedding.

Long-term goal (5-10 years or more) — owning a home, starting a family, paying for college or retiring.

MoneyWi$e: Money Management

Working toward your goals

A savings plan allows you to work steadily toward your financial goals.

The take-home ‘Financial Goals Worksheet’ will help you figure out a savings plan that works with your particular goals.

MoneyWi$e: Money Management

Take-home activity

The Financial Goals Worksheet and Chart can be found in each of your folders.

Complete the worksheets at home.

Bring the completed worksheet back for the second session.

See you next time!

MoneyWi$e: Money Management

Money Management

Session Two (Two hours)

MoneyWi$e: Money Management

Money Management

Welcome back!

In this session we will focus on saving, investing, insurance, credit and debt

MoneyWi$e: Money Management

Saving & investing

Let’s review your Financial Goals Worksheet.

Saving and investing can help you to reach your short-term and long-term goals.

MoneyWi$e: Money Management

How to save more

“Pay yourself first” by scheduling automatic deposits on pay day that go into your savings account or IRA (individual retirement account)

MoneyWi$e: Money Management

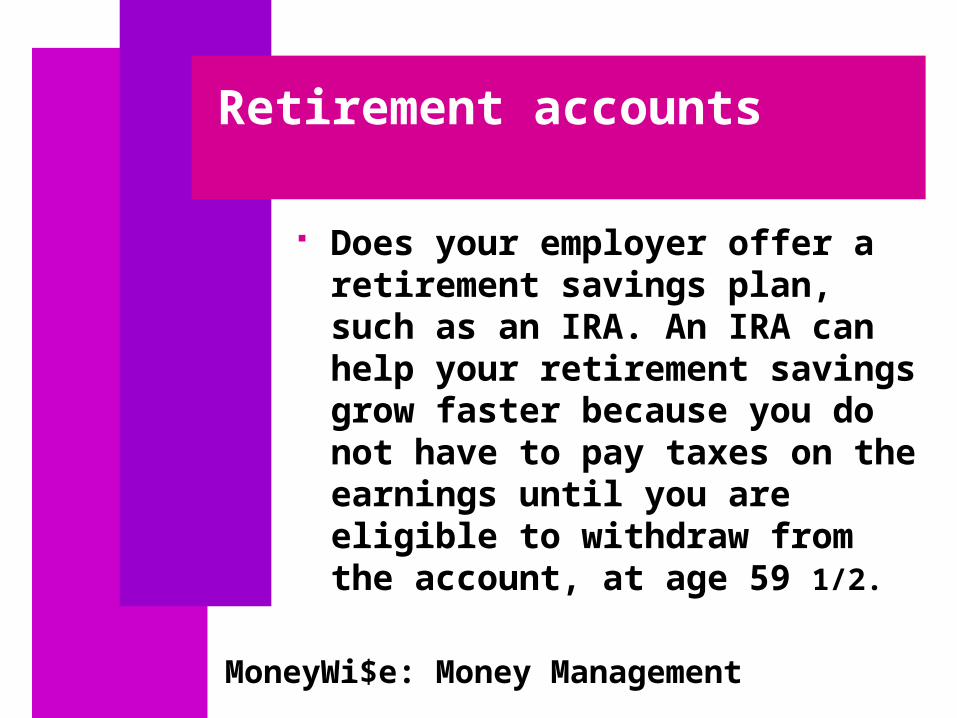

Retirement accounts

Does your employer offer a retirement savings plan, such as an IRA. An IRA can help your retirement savings grow faster because you do not have to pay taxes on the earnings until you are eligible to withdraw from the account, at age 59 1/2.

MoneyWi$e: Money Management

Saving - CDs

A CD (certificate of deposit) is a safe way to save.– Like savings accounts, CDs are

insured by the government.– CDs often earn a higher interest

rate than savings accounts do.– However, CDs require that you

leave your money for a set period of time, such as six months or a year.

MoneyWi$e: Money Management

Investing

An investment is the use of money to create more money

Stocks, bonds and mutual funds are all types of investments

Consider an investment advisor. Be cautious—investments are

not government-insured and you could lose your money.

MoneyWi$e: Money Management

Insurance

What are the benefits of having insurance?

Insurance protects you against financial ruin as a result of an unforeseen catastrophe like fire, theft or medical emergency.

MoneyWi$e: Money Management

Kinds of insurance

What are the most important types of insurance for you and your family?– Automobile insurance– Health insurance– Homeowner’s or renter’s insurance– Life insurance

MoneyWi$e: Money Management

Saving money on insurance

Always ask if you are eligible for any insurance discounts.

Internet sites can help you compare premiums:– QuoteSmith (www.quotesmith.com)– Quicken Insurance

(www.insuremarket.com)

MoneyWi$e: Money Management

Credit

Good credit can help you:– Rent an apartment– Purchase a home– Get a job– Set up phone and power service.– Buy ‘big-ticket’ items without cash– Borrow money– Obtain a credit card– Rent a car

MoneyWi$e: Money Management

To build good credit...

Pay your bills on time. If you carry a balance, pay as

much as you can each month.

MoneyWi$e: Money Management

Rebuilding credit

If you have damaged your credit, try applying for credit with local businesses or for a secured credit card (a bank credit card backed by money you deposit in a bank account)

MoneyWi$e: Money Management

Home equity loans

Home equity loans can be used to consolidate debt.

Be very careful before taking out a loan secured by your home (a home equity loan or line of credit).

If you fail to make a payment, you risk losing your home.

MoneyWi$e: Money Management

Good credit

Try to avoid these expensive credit options:– Pawn shops, pay day loans, and car

title pawn shops– Offers to buy things on credit with

deferred interest– Credit cards with rates higher than

the national average (currently about 13.50%)

MoneyWi$e: Money Management

Overwhelmed by debt?

The National Foundation for Consumer Credit - (800) 388-2227 or www.nfcc.org can refer you to a credit counselor in your area. Low- or no-cost services help you establish a repayment plan.

Debtors Anonymous (781) 453-2743; debtorsanonymous.org

MoneyWi$e: Money Management

Let’s take a break

Please come back in 15 minutes.

MoneyWi$e: Money Management

Money management activity

Break into small groups. Review sample profiles. Discuss how the people in the

sample profile can get back on track.

Select a spokesperson from each group to present your ideas.

MoneyWi$e: Money Management

Take-home budget worksheet

In your folder you’ll find a budget worksheet.

Track your spending for a while and then complete this worksheet at home.

Keep yourself focused on creative ways to save money.

MoneyWi$e: Money Management

Questions?

Let’s try to answer some of your questions about money management.

MoneyWi$e: Money Management

Now you can grade us!

Please fill out the seminar evaluation form and leave it with me on your way out.

MoneyWi$e: Money Management

Congratulations!

Congratulations on completing the Money Wi$e “Manage Your Money Wisely” seminar!

You’ve taken a big step toward wise money management.

Put what you’ve learned into practice—you can do it!