27

Monopoly

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | marilyn-whitehead |

| View: | 218 times |

| Download: | 2 times |

Monopoly

Monopoly

• Market with a single supplier of a good or service

-- Examples

a. Local telephone

b. Utilities

c. DeBeers (South African Firm) controls 80% of the production of diamonds

-- No close substitutes

-- Natural or legal barriers to entry prevent competition

No Close Substitutes

• Partial Substitutes – Bottled water may substitute for part of a city’s water supply; however, for laundry, showers and other purposes, there is no competitive substitute

• New products can weaken a monopoly – Pakistan Post Office vs TCS, Email, Fax

• New products can create a monopoly – IBM PC opened the door for microsoft’s DOS

Barriers to Entry

• Natural Barriers to Entry

-- Technology enable one firm to meet entire demand at a lower price than two or more firms could

-- Economies of Scale – one firm cheaper than others

-- Acquisition of Competitors

-- Utilities are an example (Power Plants)• Legal Barriers to Entry

-- Ownership of a natural resource

-- Patents

-- Public Franchise

-- Exclusive licenses

Barriers to Entry

• Control over an essential resource

• Economies of scale

• Legal barriers

• Required scale for innovation

• Economies of being established

Monopoly – Pricing/Production Constraints

• Since a monopoly is the only supplier in town, what prevents it from charging and producing whatever it wants?

• Answer – The monopoly still faces a downward sloping demand curve for what it produces.

• A monopolist faces a tradeoff between price and the quantity sold.

-- To sell a larger volume, the monopolist must accept a lower price

Monopoly – A downward Sloping Demand Curve

• Marginal Revenue (the change in total revenue divided by the change in quantity sold) is always less than price.

• The Marginal Revenue Curve always lies below the Demand Curve.

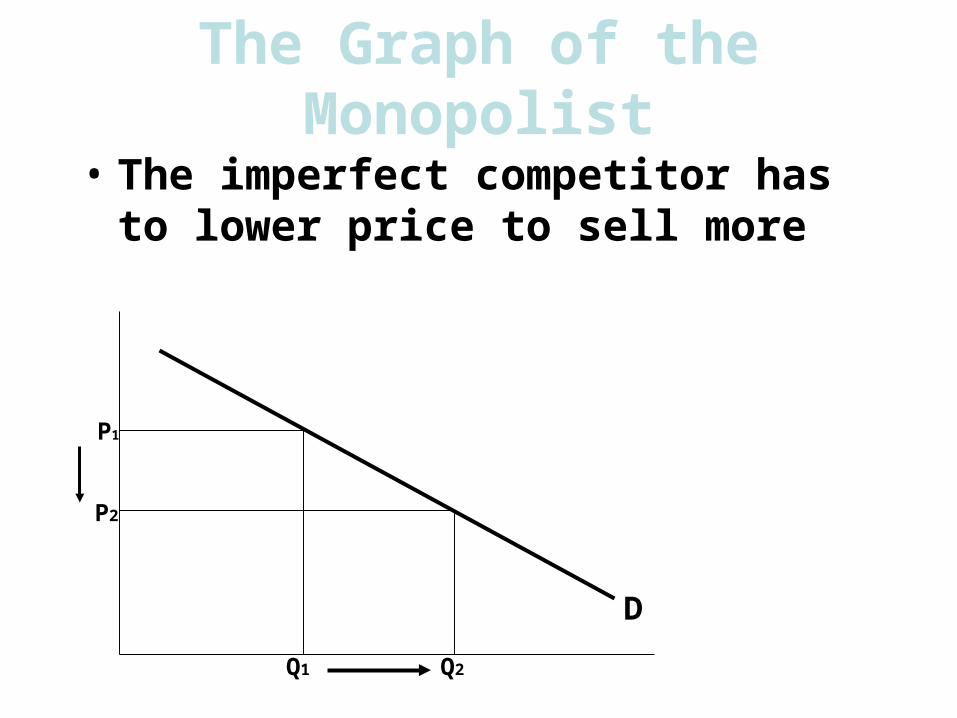

The Graph of the Monopolist

• The imperfect competitor has to lower price to sell more

D

Q2Q1

P2

P1

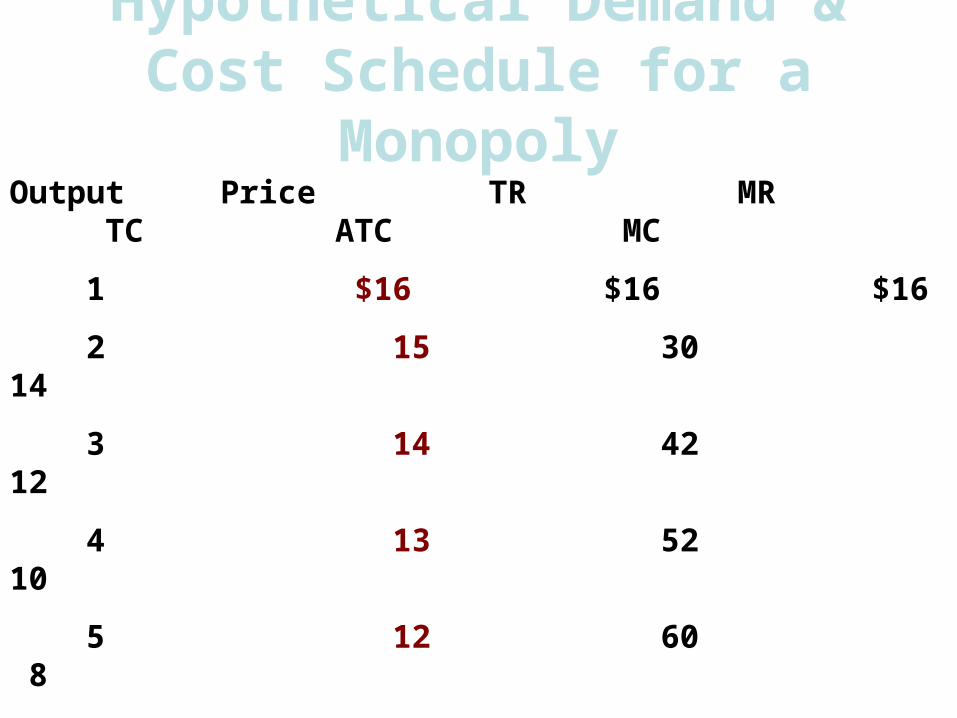

Hypothetical Demand & Cost Schedule for a Monopoly

Output Price TR MR TC ATC MC

1 $16 $16 $16

2 15 30 14

3 14 42 12

4 13 52 10

5 12 60 8

6 11 66 6

7 10 70 4

Output

20

18

16

14

12

10

8

6

4

2

0

ATC

D

MR

0 1 2 3 4 5 6 7

MC

The Monopolist Making a Profit(Calculating the Monopolist’s Profit)

Price

The ATC at five units of output is about $9.90

ATC

Output

20

18

16

14

12

10

8

6

4

2

0

ATC

D

MR

0 1 2 3 4 5 6 7

MC

The Monopolist Making a Profit(Calculating the Monopolist’s Profit)

Price

ATC

Total Profit = (Price – ATC) X Output= ($12 - $9.90) X 5 ($2.10 X 5)

= $10.50

Monopoly – Output/Price Decision

• Even the monopoly wants to maximize its profits• Demand constraints, however, limit the ability of the

monopoly to charge high prices and produce high volumes

• Especially, the price elasticity of demand proves a limit to the monopoly’s market power

• So, the monopoly still maximizes profit where MR=MC, and

• Normally, the monopoly is able to earn economic profit and do so indefinitely

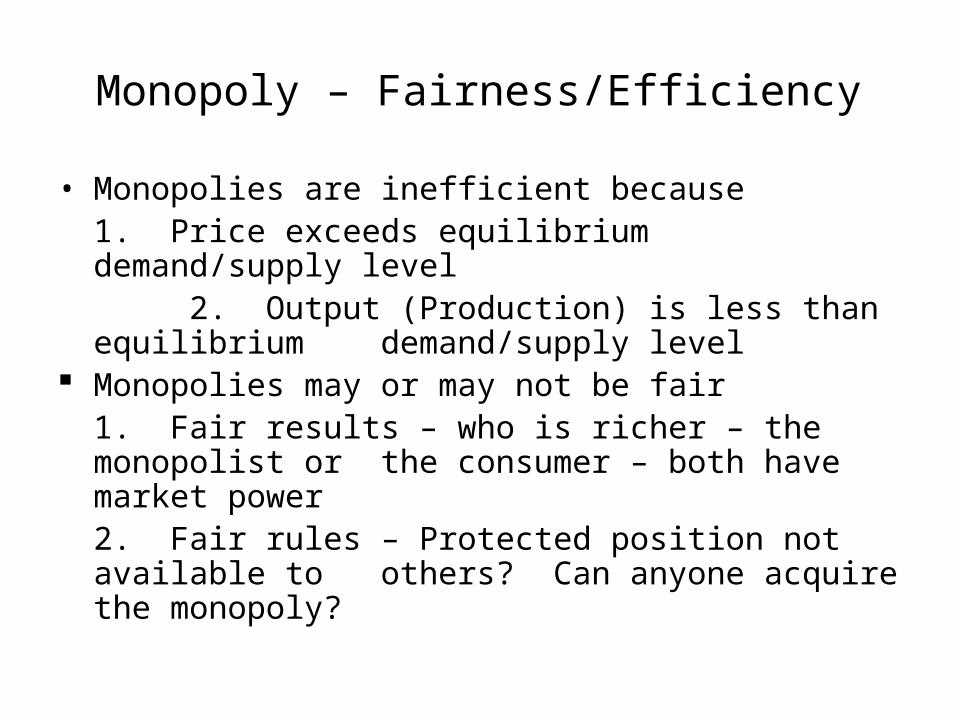

Monopoly – Fairness/Efficiency

• Monopolies are inefficient because1. Price exceeds equilibrium demand/supply level

2. Output (Production) is less than equilibrium demand/supply level

Monopolies may or may not be fair1. Fair results – who is richer – the monopolist or the consumer – both have market power2. Fair rules – Protected position not available to others? Can anyone acquire the monopoly?

The Monopolist in the Short Run and the Long Run

• There is no distinction between the short run and the long run for the monopolists– If there is a demand for their product or service

they make a profit (economic profits)– If there is not enough demand for their product

for them to make a profit they go out of business

Output

ATC

MC

D

MR

0 1 2 3 4 5 6

8

10

12

14

16

18

20

22

24

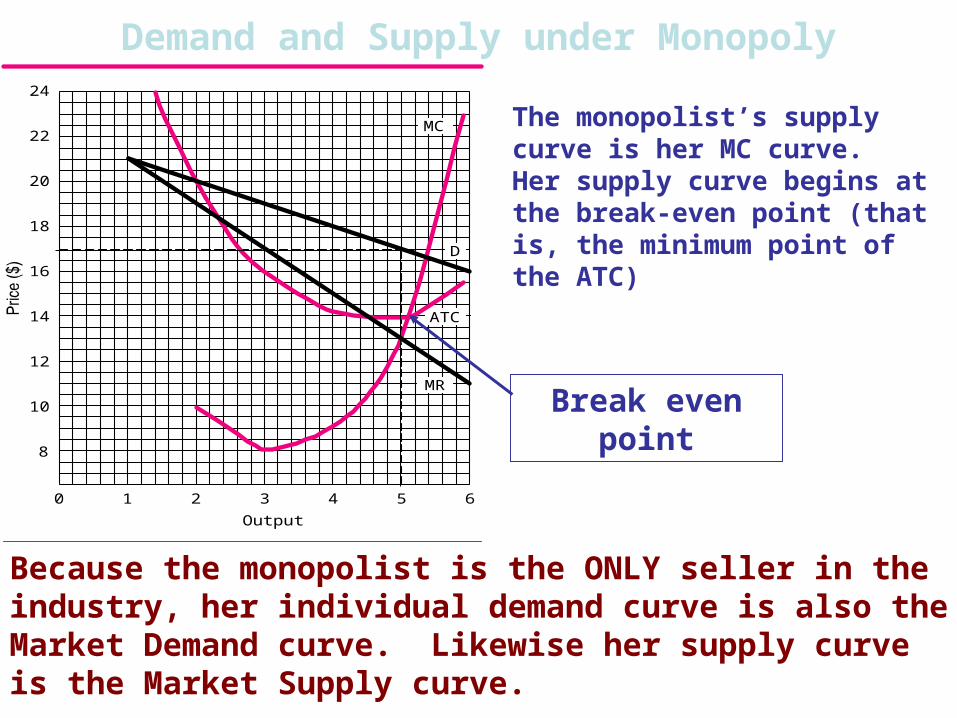

Demand and Supply under Monopoly

Because the monopolist is the ONLY seller in the industry, her individual demand curve is also the Market Demand curve. Likewise her supply curve is the Market Supply curve.

The monopolist’s supply curve is her MC curve. Her supply curve begins at the break-even point (that is, the minimum point of the ATC)

Break even point

Limits to Monopoly Power

• The ultimate limit to monopoly power may come from the government or from the market itself– If a firm gets too big or too bad, or both,

the government may decide to step in using antitrust laws

– The market limits monopoly power basically through the development of substitutes

Economies of Scale and Natural Monopoly

• There are only two justifications for monopoly– Economies of Scale justify bigness

because sometime only a firm with the capability of a very large output can produce anywhere close to the minimum point of its ATC

– Natural Monopoly is a situation where one firm is able to provide a service at a lower cost than could several competing firms

When Is Bigness Bad?

• Monopolies tend to be inefficient because they do not produce at the minimum point on their ATC– This prevents resources from being allocated

in the most efficient manner

• Big business always has great political power– Economic power is easily converted into

political power

• The monopolist may engage in price discrimination

Gains from Monopoly

• When there are potential advantages over a competitive alternative

-- Economies of Scale – e.g. Public Utilities

-- Incentives to Innovate – Larger firms can spend more money on R&D

The concept of “Critical Mass” – Until a firm reaches a certain size, it cannot perform the R&D functions required to maintain viability and innovation – e.g. the pharmaceutical industry

When Is Bigness Good?

• Natural monopolies can take advantage of economies of scale and deliver services much more cheaply than a multitude of competing firms

• It is probably all right if a firm is big because it is very good

• If a firm is big because it is bad is another story

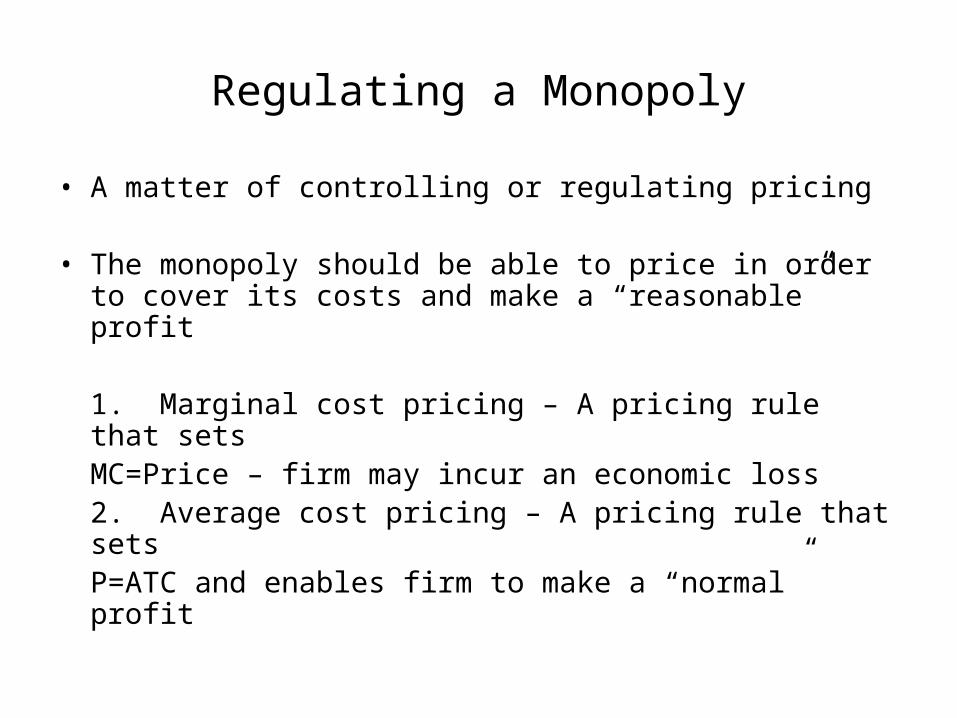

Regulating a Monopoly

• A matter of controlling or regulating pricing

• The monopoly should be able to price in order to cover its costs and make a “reasonable” profit

1. Marginal cost pricing – A pricing rule that sets MC=Price – firm may incur an economic loss

2. Average cost pricing – A pricing rule that sets P=ATC and enables firm to make a “normal”

profit

Two Policy Alternatives

• Two ways to prevent public utilities from charging outrageous prices–government regulation

–government ownership

Conclusion

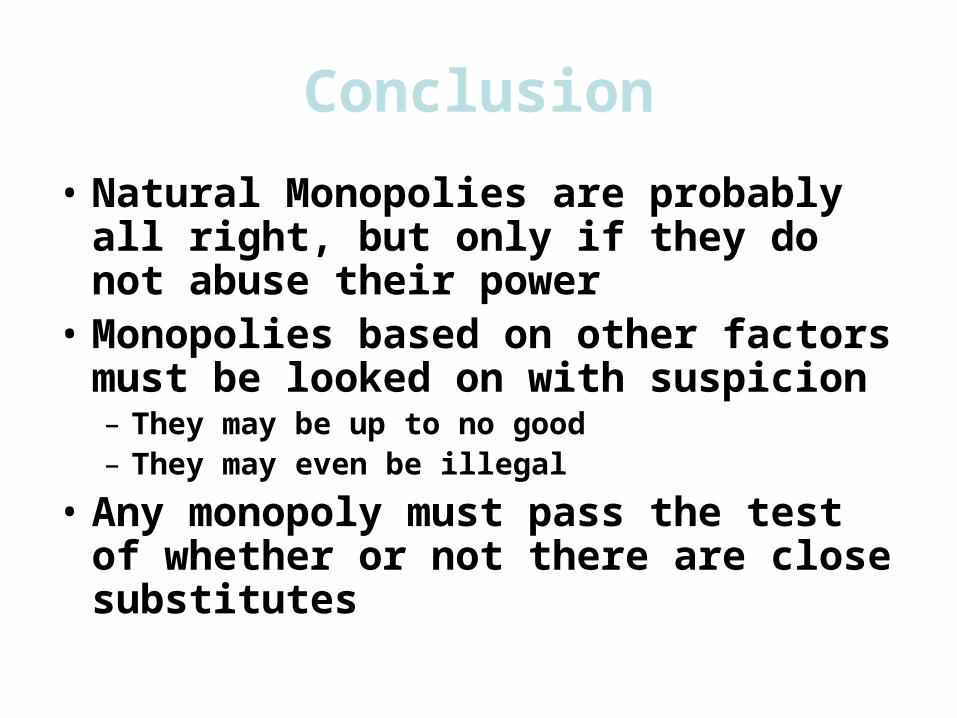

• Natural Monopolies are probably all right, but only if they do not abuse their power

• Monopolies based on other factors must be looked on with suspicion– They may be up to no good– They may even be illegal

• Any monopoly must pass the test of whether or not there are close substitutes

Reference: Introduction to Economicsby

Lieberman & HallChapter seven: Perfect Competition

Slides by John F. Hall