MOODYS.COM 23 MARCH 2015 NEWS & ANALYSIS Corporates 2 » Foregoing Content Creation, Apple Beefs up Streaming, a Credit Positive » Higher US Defense Spending Proposals Are Credit Positive for Contractors » Murray Energy's $1.4 Billion Deal for Controlling Stake in Foresight Is Credit Positive » Brazil Homebuilder PDG Plans to Pay Down Debt with Equity Issuance, a Credit Positive » Microsemi's Planned Acquisition of Vitesse Is Credit Negative » Russian Mortgage Rate Subsidies Will Not Overcome Slack Housing Demand Infrastructure 9 » Petro Rabigh's $5.2 Billion Project Financing Deal Is Credit Positive for Sumitomo Chemical » Kansai Electric Retirement Plan for Older Nuclear Reactors Is Credit Positive Banks 12 » GE Capital's Sale of Its Australia and New Zealand Consumer Lending Operations Is Credit Positive » No Bail Out for Banco de Madrid Sets the Stage for Depositor Losses » Norway's Tighter Mortgage Underwriting Standards Are Credit Positive for Banks and Covered Bonds » China Reins in Securities Companies' Stock Repo Business, a Credit Positive Sovereigns 18 » Israeli Elections Signal Economic Policy Cohesion, a Credit Positive Sub-sovereigns 20 » German Local Governments and Public-Sector Pfandbriefe Will Benefit from Infrastructure and Climate Initiative US Public Finance 22 » Puerto Rico Debt Restructuring Is Increasingly Likely, a Credit Negative » Dwindling Federal Transportation Funds Threaten Revenues States Use to Pay Debt Covered Bonds 26 » Sweden's Proposed Mortgage Amortisation Requirement Would Be Credit Positive for Covered Bonds CREDIT IN DEPTH US Dollar Strength Hurts Countries with Large External Financing Needs 28 The strengthening US dollar has prompted a sharp currency depreciation and/or a significant decline in the foreign exchange reserves of a number of countries. To the extent that these fluctuations reflect capital outflows or significantly lower external inflows, they are credit negative for countries with large external funding needs. Countries with sizable current account deficits, such as Turkey and South Africa, are vulnerable to weaker external net inflows. A weaker exchange rate is also credit negative for countries with large pending external debt payments, such as Turkey, Malaysia and Chile. RATINGS & RESEARCH Rating Changes 34 Last week, we downgraded Becton Dickinson, Royal Philips, Eurasian Development Bank, Ghana and International Investment Bank, and upgraded Masco, Volkswagen, VWR Funding, Autovia de la Mancha, Sumitomo Life and Paraguay, among other rating actions. Research Highlights 40 Last week, we published on North American exploration and production, China’s rebalancing, South Carolina Electric & Gas, Bonneville Power Administration and Tennessee Valley Authority, bank rating methodology, US Federal Home Loan Banks, Chinese insurers, El Salvador, Canada, Germany, euro-area sovereigns, sovereign bond contract modifications, Namibia, African sovereigns, US higher education, US local government, aircraft ABS, US consumer loan ABS, Indian auto loan ABS, US ABS CDOs and US TruPS CDOs, among other reports. RECENTLY IN CREDIT OUTLOOK » Articles in Last Thusday’s Credit Outlook 45 » Go to Last Thursday’s Credit Outlook

Transcript

MOODYS.COM

23 MARCH 2015

NEWS & ANALYSIS Corporates 2 » Foregoing Content Creation, Apple Beefs up Streaming, a

Credit Positive » Higher US Defense Spending Proposals Are Credit Positive

for Contractors » Murray Energy's $1.4 Billion Deal for Controlling Stake in

Foresight Is Credit Positive » Brazil Homebuilder PDG Plans to Pay Down Debt with Equity

Issuance, a Credit Positive » Microsemi's Planned Acquisition of Vitesse Is Credit Negative » Russian Mortgage Rate Subsidies Will Not Overcome Slack

Housing Demand

Infrastructure 9 » Petro Rabigh's $5.2 Billion Project Financing Deal Is Credit

Positive for Sumitomo Chemical » Kansai Electric Retirement Plan for Older Nuclear Reactors Is

Credit Positive

Banks 12 » GE Capital's Sale of Its Australia and New Zealand Consumer

Lending Operations Is Credit Positive » No Bail Out for Banco de Madrid Sets the Stage for

Depositor Losses » Norway's Tighter Mortgage Underwriting Standards Are Credit

Positive for Banks and Covered Bonds » China Reins in Securities Companies' Stock Repo Business, a

Credit Positive

Sovereigns 18 » Israeli Elections Signal Economic Policy Cohesion, a

Credit Positive

Sub-sovereigns 20 » German Local Governments and Public-Sector Pfandbriefe Will

Benefit from Infrastructure and Climate Initiative

US Public Finance 22 » Puerto Rico Debt Restructuring Is Increasingly Likely, a

Credit Negative » Dwindling Federal Transportation Funds Threaten Revenues

CREDIT IN DEPTH US Dollar Strength Hurts Countries with Large External Financing Needs 28

The strengthening US dollar has prompted a sharp currency depreciation and/or a significant decline in the foreign exchange reserves of a number of countries. To the extent that these fluctuations reflect capital outflows or significantly lower external inflows, they are credit negative for countries with large external funding needs. Countries with sizable current account deficits, such as Turkey and South Africa, are vulnerable to weaker external net inflows. A weaker exchange rate is also credit negative for countries with large pending external debt payments, such as Turkey, Malaysia and Chile.

RATINGS & RESEARCH Rating Changes 34

Last week, we downgraded Becton Dickinson, Royal Philips, Eurasian Development Bank, Ghana and International Investment Bank, and upgraded Masco, Volkswagen, VWR Funding, Autovia de la Mancha, Sumitomo Life and Paraguay, among other rating actions.

Research Highlights 40

Last week, we published on North American exploration and production, China’s rebalancing, South Carolina Electric & Gas, Bonneville Power Administration and Tennessee Valley Authority, bank rating methodology, US Federal Home Loan Banks, Chinese insurers, El Salvador, Canada, Germany, euro-area sovereigns, sovereign bond contract modifications, Namibia, African sovereigns, US higher education, US local government, aircraft ABS, US consumer loan ABS, Indian auto loan ABS, US ABS CDOs and US TruPS CDOs, among other reports.

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Thusday’s Credit Outlook 45 » Go to Last Thursday’s Credit Outlook

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Corporates

Foregoing Content Creation, Apple Beefs up Streaming, a Credit Positive Apple Inc. (Aa1 stable) announced on 9 March that it will provide the new HBO Now standalone streaming service, along with possible live TV streaming offerings, through Apple TV. The plans are credit positive because they are further evidence that Apple will not seek to create its own media and entertainment offerings, or make a significant acquisition of a large media company. By foregoing an expensive foray into video content creation, Apple eliminates production risks while adding more options for its customers to consume video.

The company is following its long-held strategy of providing access to media over various Apple devices controlled through the App Store and iTunes, which, in turn, cements the loyalty of its customers to the iOS ecosystem. Also, by facilitating easy-to-use and legal video streaming options, Apple is providing a neutral distribution outlet for the content without competing with content creators and networks.

Apple’s allure to content owners is the more than 500 million iOS users worldwide, in addition to the largest installed base of streaming players. Just as Apple’s global reach was beneficial in securing digital music rights around the world, it should help the company negotiate video streaming terms in international markets. Apple shipped a total of 25 million Apple TV units since first introducing the unit in 2007, about double the installed base of rival Roku boxes.

We think that the revenues from Apple’s new streaming services will largely offset the recent declines of downloaded music over iTunes. By offering HBO Now (exclusive for three months) and potentially through a content-light TV subscription service, Apple may generate $200-$300 million in annual revenues. More importantly, Apple will offer a competitive service and a potentially less expensive option to people who eschew more expensive traditional, larger pay-TV packages (i.e., so-called cord-shavers/cutters).

Over-the-top (OTT) viewing, which is viewing television programming over the Internet, particularly binge viewing of previously aired serialized programming, is sapping television ratings and stalling ad revenue growth for traditional pay-TV networks. But proposed OTT services such as Apple’s will offer live video streaming of television shows and certain sports broadcasts, which could lead to more subscribers disconnecting their pay-TV service.

Still, we do not believe that Apple’s or other OTT streaming services threaten the main business models of cable and telco because these distributors are the key last mile providers of high-speed Internet service (ISPs) to consumers and small businesses. In order to get the best quality video streaming service, customers have to subscribe to higher speed data plans from their ISPs, which generally carry richer margins. If a great rush of customers elect to drop their pay-TV service in favor of OTT, it would pressure the ISPs to increase Internet capacity and in turn raise broadband rates.

Plus, cutting the cord on traditional pay-TV is economically attractive only to people who do not watch a wide variety of TV or only watch video content on their computers. There are also limited options to watching live television online. When varying tastes, larger families and multiple TV sets are added into the cost/benefit equation, cord-cutting loses its appeal. If cord-cutters try to replicate the pay TV offerings in the online world, the total cost quickly exceeds the value of the sub-$100 double play (TV and Internet) and triple play (TV, Internet and phone) packages offered by the traditional pay-TV providers. Therefore, as content owners continue to experiment with OTT distribution models, we view Apple and other enablers of streaming media as complementing the ISPs business model.

Gerald Granovsky Senior Vice President +1.212.553.4198 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

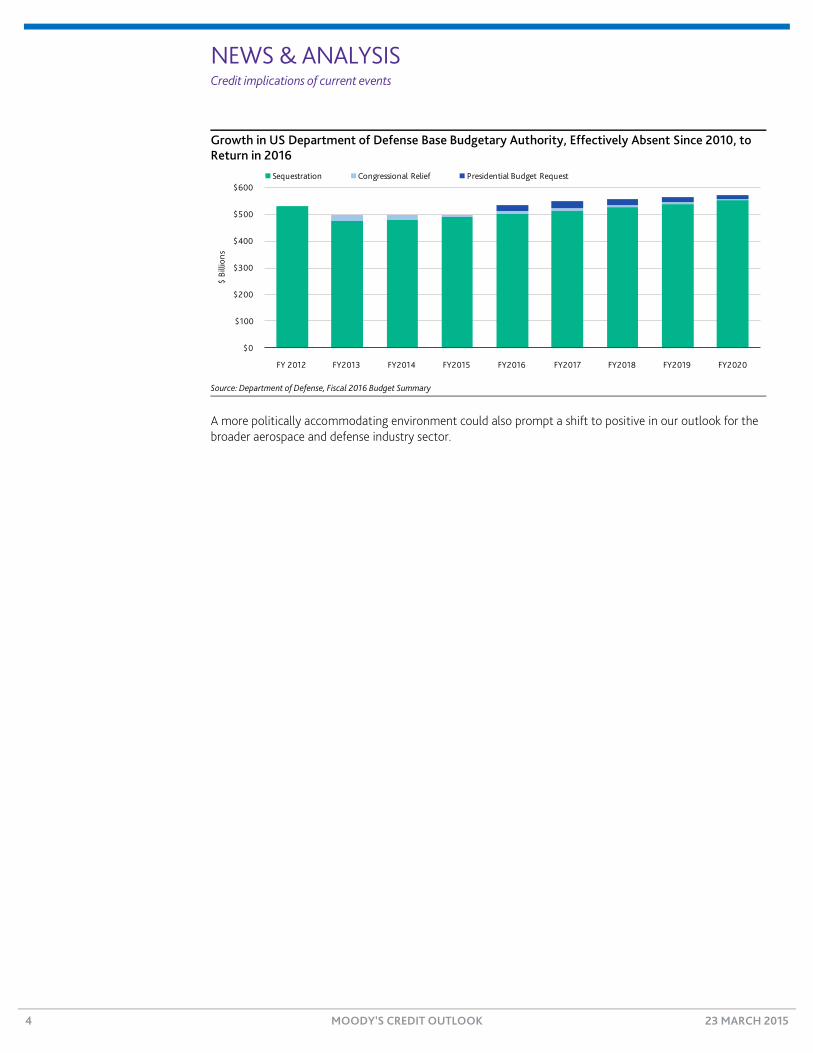

Higher US Defense Spending Proposals Are Credit Positive for Contractors On 18 March, the US Senate submitted its initial budgetary request for the Department of Defense’s (DoD) 2016 fiscal year, one day after the House Budget Committee’s submission of the same. While we anticipate potentially large revisions prior to final passage, the key take-away from our perspective is that the total defense spending request from both the House and Senate is materially higher than what is currently permitted under sequestration-imposed budget caps.

Increased spending would effect at least modest relief from sequestration-mandated constraints and would be credit positive for US and NATO-member-nation defense contractors like General Dynamics Corporation (A2 stable), The Boeing Company (A2 stable), Raytheon Company (A3 stable), Lockheed Martin Corporation (Baa1 positive), Northrop Grumman Corporation (Baa1 stable) and Huntington Ingalls Industries, Inc. (Ba1 stable), for which US defense-related outlays represent the preponderance of the total addressable market.

The total spending request is at least $590+ billion as currently proposed, including the Senate’s 19 March additional funding request of $38 billion; the House request looks to be as high as $613 billion at the moment, albeit with some added complexity. Notwithstanding the implied requisite legislative relief, when coupled with the DoD’s earlier fiscal 2016 budget request, which exceeds legislative budgetary caps by nearly 7% ($534 billion from $499 billion), it seems increasingly clear that the political will now exists to reverse the five-year downturn in US defense spending.

Although these initial budgetary submissions are largely symbolic exercises, we believe an improving US economy coupled with increased geopolitical risk is prompting broader acceptance of the need for a strategy-driven defense budget, rather than the budget-driven defense strategy that has largely shaped US defense spending since 2010.

Even so, other factors are still apt to constrain industry revenue growth, dilute margins and pressure cash flows, at least through 2016, and subsequently temper an otherwise improving outlook. Noteworthy constraints include the normal course lag between budget actions and the timing of outlays, lasting affordability initiatives, reduced forward funding for supplemental overseas contingency operations, heightened competition for increasingly limited future market opportunities, and the lingering absence of political consensus that is needed to more seamlessly effect legislation upon which industry planning relies.

We believe that the initial DoD and congressional base budgetary requests broadly define the upper and lower bounds of likely budget outcomes for fiscal 2016 (beginning October 2015). Full adoption of either request is unlikely, however, and modest relief (in line with past practice) is more likely. We anticipate an outcome similar to the late 2013 passage of the Ryan-Murray Bipartisan Budget Act, which led to a two-year easing of otherwise lower sequestration-imposed budget caps for 2014-15.

Because political consensus-building has been in short supply for the past few years, some measures included within both the Senate and House submissions (the proposed repeal of Obamacare, for example) suggest that this year’s budget request will be contentious. Despite partisan tensions, we expect that the ultimate budget agreement will exceed sequestration-mandated base budget caps of $499 billion, effectively growing for the first time since 2010, and on more than a nominal basis, but falling well short of the DoD’s $534 billion request. As shown in the exhibit below, we believe the DoD base budget will incorporate low single-digit percentage growth from 2016 through fiscal 2020, which should translate into modest revenue growth after several years of decline for the long-cycle prime defense contractors beginning 2016-17. Higher base budgets would boost revenue performance for shorter-cycle contractors like L-3 Communications Corporation (Baa3 negative) and Exelis, Inc. (Ba1 stable) on a more immediate basis.

Russell Solomon Senior Vice President +1.212.553.4301 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Growth in US Department of Defense Base Budgetary Authority, Effectively Absent Since 2010, to Return in 2016

Source: Department of Defense, Fiscal 2016 Budget Summary

A more politically accommodating environment could also prompt a shift to positive in our outlook for the broader aerospace and defense industry sector.

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Murray Energy’s $1.4 Billion Deal for Controlling Stake in Foresight Is Credit Positive On 15 March, Murray Energy Corporation (B2 positive) announced that it will buy a controlling stake in Foresight Energy GP LLC and Foresight Energy LP, a parent of Foresight Energy, LLC (B2 positive), for about $1.4 billion. The deal ties Murray’s Illinois Basin and Northern Appalachian coal mining business to Foresight’s Illinois Basin mines to create one of the biggest US thermal coal producers, a credit positive for both companies because of potential competitive, logistical and cost advantages from merging major miners operating in two key coal-producing regions. After the deal’s announcement, we upgraded Murray Energy’s rating to B2 positive, from B3 stable and confirmed Foresight’s B2 positive rating.

Under the planned deal, Murray will acquire a controlling interest in Foresight Energy LP and Foresight Energy GP LLP, giving it about 80% of general partner interests and 50% of limited partner interests in Foresight. Foresight founder Christopher Cline will retain approximately a 20% general partner interest and 36% limited partner interest.

The transaction is transformative in nature, significantly increasing the size and scale of Murray's operations. We expect the $1.4 billion purchase price will be financed with debt and produce a combined entity that would have had adjusted pro-forma consolidated debt/EBITDA at the end of 2014 of roughly 4.4x. Although leverage for the combined company is higher than each company's standalone leverage (adjusted debt/EBITDA of 3.6x for Foresight and 3.1x for Murray), the combined credit profile would improve because of the competitive advantages and synergies. We expect that debt/EBITDA, as adjusted, for the consolidated company would decline to around 4x over the next two years. The combined company will benefit from logistical advantages in moving coal down the Mississippi for export and the low-cost position of Foresight mines in the Illinois basin, as well as Murray's low-cost Northern Appalachian mines acquired from CONSOL Energy Inc. (Ba3 negative) in 2013.

The transaction may help support prices in the Illinois basin by bringing together the two major competing players in the region, and could potentially shift some production to Foresight's lower-cost mines from Murray's Illinois basin operations. Coal from the Illinois basin has more sulfur than coal from other regions, and plants that burn it must have scrubbers that remove enough of the sulfur to comply with environmental regulations. Therefore, this high-sulfur coal tends to be consumed by larger baseload coal plants. These plants are less likely to face retirements and instead will run harder to make up for lost capacity as the smaller and less efficient coal plants continue to retire, making the Illinois Basin the only growing coal-producing basin in the US.

However, Murray’s move for Foresight comes at a challenging time for the coal industry, which is facing low natural gas prices and the implementation of federal Mercury and Air Toxic Standards over the next year. Henry Hub natural gas prices have tracked below $3 per million British thermal units early this year, and absent a rapid recovery, will likely drive some energy companies to switch from coal to natural gas for generating electricity in the next several months. Meanwhile, spot prices have declined in all major coal basins.

Anna Zubets-Anderson Vice President - Senior Analyst +1.212.553.4617 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Brazil Homebuilder PDG Plans to Pay Down Debt with Equity Issuance, a Credit Positive Last Wednesday, PDG Realty S.A. Empreendimentos e Participações (PDG, B3 negative), one of Brazil’s largest homebuilders, said it plans to raise up to BRL500 million ($156 million) in new equity by early June 2015. The equity issuance is credit positive for PDG because the company will use proceeds to reduce its BRL2.2 billion in corporate debt due between now and mid-2016.

Without the equity issuance, difficult refinancing conditions and weak fundamentals in Brazil’s homebuilding market would likely leave PDG insufficient cash flow to pay its coming corporate debt maturities, starting with BRL1.1 billion due in the second and third quarters of this year. PDG’s controlling shareholder, private equity firm Vinci Partners Investimentos Ltda. (unrated), has committed to buy at least BRL300 million if there are enough non-subscribed shares.

The proposed capital increase, which will go to a shareholder vote on 6 April, would set an issuance price of BRL0.44/share, slightly higher than the current market price of BRL0.40/share. The proposal adds an additional incentive, giving new equity investors a warrant for every 2.5 common shares they buy as part of this issuance. These warrants mature in April 2018, three years after the vote, but investors can exercise them at any time before then at the exercise price of BRL0.75/share. Exercising the warrants would total BRL205-BRL340 million in additional equity issuances through April 2018.

São Paulo-based PDG, including minority investments in other companies, has 87 projects in 13 states in Brazil, spanning virtually all price segments. In 2014, PDG generated net revenues of BRL4.3 billion and net losses of BRL475 million. Since 2012, PDG has faced significant execution difficulties after pursuing an aggressive growth strategy in 2006-11. The company has made strong improvements in unifying its businesses and enhancing its internal processes and controls since 2013, which will boost PDG’s cash generation this year and in 2016 compared with 2014 levels.

Still, PDG’s credit metrics remain under considerable strain, amid sales cancellations and Brazil’s deteriorating industry dynamics. More broadly, Brazil's weakening macroeconomic fundamentals, a likely rise in unemployment and reduced availability of mortgages and other financing, will hurt Brazil’s housing demand and real estate prices this year.

Under such difficult conditions, the proposed equity increase, along with PDG’s other possible asset monetization strategies, will be crucial in the company’s effort to improve liquidity and attain a more sustainable capital structure, as shown in the exhibit below. Even a relatively modest equity issuance of BRL300 million would improve PDG’s interest coverage, debt and free cash flow metrics noticeably, and a BRL500 million issuance would do so even more.

Effect of the Different Size Equity Raises on PDG Realty’s 2015 and 2016 Credit Metrics

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Microsemi’s Planned Acquisition of Vitesse Is Credit Negative Last Wednesday, Microsemi Corporation (Ba2 stable) said that it had agreed to acquire Vitesse Semiconductor Corp. (unrated) for about $389 million. Although the acquisition is strategically sound, the planned transaction is credit negative because it will increase leverage.

Microsemi expects to complete the acquisition by the end of June. The company plans to fund the purchase with a new term loan of about $325 million, which will increase pro forma adjusted debt/EBITDA to more than 4.50x from 3.17x for the 12 months that ended 28 December 2014. Although the transaction will reduce the company’s cash balance by about $67 million, Microsemi will be doubling the size of its revolver to $100 million, providing additional liquidity to offset the decline in cash.

Leverage should decline quickly as Microsemi uses free cash flow to reduce debt (free cash flow totaled $170.6 million during the 12 months that ended 31 December 2014). EBITDA has been declining at Vitesse as revenue growth in new products over the past few years has failed to fully offset declines in the company’s legacy portfolio. But we expect the Vitesse acquisition to result in cost savings through the elimination of duplicative operating and administrative functions, which will contribute to modest EBITDA growth at the newly merged company. This growth, combined with debt repayment, should reduce adjusted debt/EBITDA to around 3.5x over the next 18 months.

Vitesse supplies Ethernet integrated circuits, software and systems to the telecommunications, defense, aerospace and industrial markets. The planned acquisition will expand the portfolio of products that Microsemi provides to its existing telecommunications customer base and adds a base of new customers. Microsemi’s much larger customer base and operating scale should boost Vitesse’s revenue and margins. Longer term, Microsemi should also benefit by integrating its timing products with Vitesse’s telecommunications carrier products.

Terrence Dennehy Vice President - Senior Analyst +1.212.553.1015 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Russian Mortgage Rate Subsidies Will Not Overcome Slack Housing Demand On 13 March, the Russian government approved a new state programme to subsidise mortgage interest rates for purchases of new middle-income housing. Although the programme will support new contract sales and is credit positive for Russian developers such as LSR Group OJSC (B2 stable), it will not outweigh the slowing demand for new houses amid Russia’s deteriorating macroeconomic and financial environment.

The government will compensate banks for capping their interest rates at 12% for mortgages issued between 1 March 2015 and 1 March 2016. The subsidies are to cover the whole life of mortgages, but will be cancelled once the Central Bank of Russia’s key rate goes down to 8.5%. The government has already provided RUB20 billion (around $320 million) from the state budget, which should be sufficient to cover one year of the programme. The maximum amount of a subsidised loan cannot exceed RUB8 million (around $135 thousand) for the purchase of a new home in Moscow, the Moscow region and St. Petersburg, and RUB3 million (around $50 thousand) for other regions of Russia. Russia’s largest developers operate in this middle-income segment.

The programme was developed to curb the mortgage market’s slowing growth, and in particular, the sharp rise of interest rates following the Central Bank of Russia’s December 2014 increase to its key interest rate to 17% from 9.5% as of November 2014. After a very strong 2012-14, when mortgage lending grew at an annual rate of above 30%, this year, lending contracted 11% in January, according to the Agency for Housing Mortgage Lending OJSC (Ba1 negative) estimates. Although in February and March 2015, the CBR reduced the rate to 15% and 14% respectively, it still remains too high to make mortgages affordable for many.

The subsidised interest rate of 12% is a competitive rate not only under the current circumstances, but also compared with the average interest rate of 12.5% in 2014, when the mortgage market was booming. Hence, we believe that the subsidised loans will bring in some borrowers who could not afford a higher mortgage rate and those who were waiting for any kind of incentive before buying a home.

Given the constantly growing importance of mortgages for Russia’s housing market in the past several years, the government also plans to stimulate the construction segment via this programme. In 2014, mortgages contributed 40%-50% of total new contract sales, with this share reaching up to 80% for select projects. We expect the programme to positively affect developers, with the largest ones becoming the main beneficiaries because they are more trusted by both banks and buyers during the current economic crisis.

However, the programme will not be sufficient to overcome the negative effect of Russia’s macroeconomic situation. The subsidies are set to cover around RUB400 billion ($6.4 billion) of new loans, which was only around 55% of mortgages issued for purchases of new homes in 2014. Additionally, housing demand in Russia will remain hurt by negative labour market trends and declining real personal incomes amid real GDP contracting by 5.5% and accelerated inflation of 15%, which we forecast for this year. Moreover, abnormally strong demand for residential real estate in 2014, driven by consumers’ desire to protect savings amid increasing macroeconomic risks and high ruble exchange rate volatility, may not carry through this year. Overall, according to the Ministry of Construction, this year’s mortgage market may fall almost two-thirds to around RUB800 billion ($13 billion) from RUB1.7 trillion ($27 billion) assuming a positive contribution from subsidised mortgages. Construction volumes should decline by around 10%-15% in 2015, reflecting a time lag of the effect of weaker demand, which will likely take its full effect only in 2016.

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Infrastructure

Petro Rabigh’s $5.2 Billion Project Financing Deal Is Credit Positive for Sumitomo Chemical Last Tuesday, Sumitomo Chemical Co., Ltd. (Baa2 stable) announced that its 37.5%-owned Rabigh Refining and Petrochemical Company (Petro Rabigh, unrated) had signed project financing agreements with a syndicate of international banks for the Rabigh Phase II project in Rabigh, Saudi Arabia. The financing deal is credit positive for Sumitomo Chemical because it significantly increases the likelihood that the upgrade and expansion of Petro Rabigh’s existing facility will be completed on schedule and subsequently increase the company’s profitability.

The approximately $5.2 billion of project financing constitutes more than 60% of the nearly $8.1 billion total expansion cost. Sumitomo Chemical and Saudi Aramco (unrated), which also holds a 37.5% stake in Petro Rabigh, will cover the remaining project costs in equal parts. Phase II will enlarge the facility’s ethane cracker and add a new processing facility that will source its inputs from Rabigh Phase I. The vertical integration and expansion will allow Petro Rabigh to produce a variety of higher value-added petrochemical products.

In the nine months ended 31 December 2014, Phase I of Petro Rabigh contributed the majority of Sumitomo Chemical’s ¥20 billion equity in earnings of affiliates and 20% of the company’s total pretax income of ¥100 billion. The $10 billion project began operations in April 2009.

Phase II’s construction is currently underway, and if it becomes operational in early 2016 as planned, we expect that it will gradually increase the equity earnings contribution to ¥40 billion when expanded facility shifts to full utilization. Phase II will improve the cost structure and profitability of Sumitomo Chemical’s petrochemical and plastics business, which constitutes about 35% of the company’s consolidated revenue. Increased profitability would help Sumitomo Chemical reduce its debt/EBITDA below its long-term target of 5.0x, from 5.6x currently. A delay in production start or lower-than-expected contribution from Rabigh Phase II would negatively pressure Sumitomo Chemical’s rating.

The deal, which involves government-affiliated financing partners including Japan Bank for International Cooperation (A1 stable) and Saudi Arabia's Public Investment Fund (unrated), as well as major Japanese and international banks, diversifies the project’s funding sources and reduces Sumitomo Chemical’s direct liabilities. However, Sumitomo Chemical and Saudi Aramco will still remain liable for a part of the off-balance-sheet project financing amount as guarantor per the terms and conditions of the project financing agreement.

The agreement marks an important milestone in the execution of Sumitomo Chemical’s long-term business strategy, because it reflects the confidence of important government-affiliated financing partners as well as major international banks.

Kailash Chhaya Vice President - Senior Analyst +81.3.5408.4201 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Kansai Electric Retirement Plan for Older Nuclear Reactors Is Credit Positive Last Tuesday, Japan’s Kansai Electric Power Company, Incorporated (A3 negative) announced that it will make the sector’s first move to retire highly aged nuclear reactors, retiring its 44-year-old Mihama 1 and 42-year-old Mihama 2 plants. Prompting its decision was an announcement last week from Japan’s Ministry of Economy, Trade and Industry (METI) that decommissioning cost will be allowable in the cost base for such nuclear generators, thus making them recoverable via the tariff charged to customers.

This is credit positive for utility companies because they will now be spared from bearing the cost of decommissioning without compensation and from significant capital expenditures to meet new safety requirements. We estimate that the benefit to Kansai will be ¥2-¥3 billion per year over 10 years once the pass-through takes effect.

Following Kansai’s announcement, Chugoku Electric Power Company, Incorporated (A3 stable) announced that it would retire its Shimane 1 plant, while Kyushu Electric Power Company, Incorporated (A3 negative) said that it will decommission its Genkai 1 plant.

Kansai was among the most financially affected nuclear electricity generators following the Fukushima accident in 2011, and its cash flow and profits will be important to mend its damaged finances and liquidity. Before the Fukushima accident, Kansai generated about half of its electricity through nuclear power. All of its nuclear plants are shut down today.

For nuclear reactors more than 40 years old in July 2015, the utilities must decide by then whether to apply to extend the plants’ lives. If the companies want extensions, they must undergo safety assessments that will likely result in significant capital spending to meet the more stringent safety requirements established after the Fukushima accident. Many older plants are small and inefficient, and it may not be economically feasible to make necessary upgrades.

Until METI’s announcement, utilities have been reluctant to decommission older plants because doing so would require the companies to record large and immediate losses. Some utilities that rely heavily on nuclear plants have been reporting losses every year since the Fukushima accident.

METI has previously assessed that retiring an older plant will result in a loss of about ¥21 billion on average, based on their book value. Depreciating this amount and collecting it through cost recovery over 10 years means that the companies can pass through to its customers about ¥2 billion per year on average. We estimate the pass-through will be slightly less for the older plants Kansai is retiring.

As highlighted in the exhibit below, the retiring plants are relatively small and less efficient. Kansai’s three other older plants, Mihama 3, Takahama 1 and Takahama 2 are larger than Mihama 1 and 2, and have capacities of 826 megawatts each. Because of their relatively large scale, Kansai is conducting further assessments to extend their lives to 60 years. Combined, these three plants account for about 10% of Kansai’s total power generation capacity. As the rest of the plants approach 40 years in age, the utilities must decide whether to apply to extend the lives of those plants. We expect the utilities will choose to retire at least the smaller ones.

Mariko Semetko Vice President - Senior Analyst +81.3.4508.4209 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Japan’s Aging Nuclear Power Plants Utility Company Rating and Outlook Plant Age Capacity in Megawatts

* JAPC Unrated Tsuruga 1 45 357

* Kansai A3 negative Mihama 1 44 340

* Kansai A3 negative Mihama 2 42 500

Kansai A3 negative Takahama 1 40 826

* Chugoku A3 stable Shimane 1 40 460

Kansai A3 negative Takahama 2 39 826

* Kyushu A3 negative Genkai 1 39 559

Kansai A3 negative Mihama 3 38 826

Shikoku Unrated Ikata 1 37 566

JAPC Unrated Tokai Daini 36 1,100

Kansai A3 negative Ohi 1 35 1,175

Kansai A3 negative Ohi 2 35 1,175

* Plants that will be decommissioned.

Sources: Company filings

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Banks

GE Capital’s Sale of Its Australia and New Zealand Consumer Lending Operations Is Credit Positive Last Sunday, General Electric Company (GE, Aa3 stable) announced that it will sell the Australia and New Zealand consumer finance businesses of GE’s finance subsidiary General Electric Capital Corporation (A1 stable) to an investor group that includes Varde Partners, Inc., Kohlberg Kravis Roberts & Co. LP and Deutsche Bank for AUD8.2 billion ($6.3 billion). The sale is credit positive for GE Capital because it further reduces non-core operations, market funding risks and complexity, and aids GE Capital in its gradual transition toward a core set of business lines that are more closely aligned with GE’s industrial units.

GE’s sale of the Australian and New Zealand units is consistent with GE’s strategy to reduce the risks of GE Capital’s large global financial services operations, which had total assets of $500.2 billion at 31 December 2014. GE CEO Jeffrey Immelt recently said that GE will shrink GE Capital even further to 25% of GE’s total earnings, down from previous guidance of 35%, with 75% of earnings coming from GE’s industrial operations. GE Capital contributed 42% to GE’s profits in 2014 and more than 50% before the global financial crisis.

The transactions come on the heels of other recent divestitures from GE Capital’s non-core consumer finance segment, notably the fourth-quarter 2014 sale of GE Money Bank AB in Sweden, Denmark and Norway to Banco Santander S.A., and agreement to sell Budapest Bank to the government of Hungary. In August 2014, GE Capital completed a 15% initial public offering of its $50 billion North American retail finance business, Synchrony Financial, with plans to exit the remaining 85% ownership interest through a split-off of shares to participating GE shareholders later this year.

After GE reaches its target of GE Capital contributing 25% of GE’s overall earnings, GE Capital will be more closely aligned with its parent’s industrial operations. GE Capital’s verticals in healthcare finance, energy financial services and aviation services will remain core operations, drawing on GE’s extensive expertise in these sectors. To some extent, these operations also provide captive financing to GE’s customers, and are therefore of higher strategic importance, a positive for their financial stability.

After the pending sales of the Australian and New Zealand consumer finance operations and the Synchrony split-off, GE Capital’s assets will have declined by nearly $200 billion since 2008. We estimate that GE Capital has an additional $65 billion of existing so-called red assets that it will eventually sell or exit, with other divestiture candidates likely to be added to reach the 25% earnings target.

GE Capital’s smaller scale reduces the risks associated with its wholesale funding profile, for both itself as well as for GE. Since the financial crisis, GE Capital has reduced market funding risks in other ways, including through an increase in cash balances, reduced use of commercial paper funding, and an extension of its average debt maturities. However, GE Capital continues to rely on market access to fund its extensive operations and refinance existing indebtedness. GE is exposed to GE Capital’s market funding risks because of its support of GE Capital, including through an income maintenance agreement.

GE Capital’s declining footprint reduces the risks stemming from non-core operations, including volatile asset quality performance and below average returns. As an additional credit positive, the sales reduce GE Capital’s organizational complexity, although we expect that it will continue to have sizable global operations even after it reaches its scale reduction objective. GE Capital will also continue to have business and geographic diversification that exceeds most other non-bank lenders, a credit positive.

Mark Wasden Vice President - Senior Credit Officer +1.212.553.4866 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

No Bail Out for Banco de Madrid Sets the Stage for Depositor Losses Last Wednesday, Spain’s Fund for Orderly Bank Restructuring (FROB) announced that it will not bail out Banco de Madrid (unrated) after the institution filed for bankruptcy on Monday. The FROB’s decision is credit negative for the bank’s depositors because it sets the stage for uninsured depositors to incur losses. This marks the first time that a Spanish bank has not been bailed out since the banking crisis began.

The FROB had the option to either restructure or implement an orderly resolution of Banco de Madrid. In both scenarios, the bank’s depositors would have probably received the support of public funds and avoided facing losses, as has been the case with all the Spanish banks (mostly savings banks) that have failed since the domestic banking crisis began in 2008. However the FROB determined that Banco de Madrid did not meet either option’s criteria, which primarily relate to preserving stability in Spain’s financial system.

The bankruptcy process for Banco de Madrid, which has €1.4 billion of total assets, had been on hold while the bankruptcy court awaited word from the FROB about a potential bailout. Now that the FROB has issued its decision, Banco de Madrid will likely be liquidated, with uninsured deposits facing the risk of losses.

As of November 2014, Banco de Madrid held customer deposits of nearly €695 million. At this stage, it is uncertain how much of this total amount will be covered by the Spanish Deposit Guarantee Fund, which guarantees up to €100,000 per depositor. Certain depositors, namely credit and financial institutions, public administrations and related parties, are not guaranteed. The eventual recovery amount for these depositors, and those with deposits totalling more than €100,000, will depend on the resolution of the bankruptcy process. The outcome of that process is difficult to predict given the lack of precedent.

The Bank of Spain intervened in Banco de Madrid on 10 March following the Andorran regulator’s decision to intervene in Banco de Madrid parent Banco Privado de Andorra (unrated). The intervention of Banco Privado de Andorra was prompted by the investigation by the Financial Crimes Enforcement Network of the US Treasury into allegations of money laundering. On 16 March, Banco de Madrid’s provisional administrators, who the Bank of Spain had appointed, decided to apply for bankruptcy and suspend the bank’s operations in response to the serious deterioration in Banco de Madrid’s financial position arising from sizable withdrawals of funds by customers.

Alberto Postigo Vice President - Senior Credit Officer +34.91.768.8230 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Norway’s Tighter Mortgage Underwriting Standards Are Credit Positive for Banks and Covered Bonds Last Tuesday, Norway’s financial regulator, Finanstilsynet, proposed tighter mortgage loan underwriting standards, including a requirement to amortise mortgages, applying a higher stress level for interest rates and reducing banks’ ability to deviate from these requirements. If implemented, these standards would be credit positive for Norwegian banks and covered bonds because they would assist in maintaining stable asset quality and limiting the growth of household indebtedness in a low interest rate environment.

Stricter underwriting guidelines would improve the credit quality of mortgages on bank’s balance sheets and in cover pools. New loans would remain restricted to a maximum loan-to-value ratio (LTV) of 85%, but personal guarantees (sureties) that are often provided by parents for first-time homebuyers would no longer be allowed as a justification to exceed the limit. Finanstilsynet has also proposed a minimum 2.5% annual amortization from the first year for all mortgages until the LTV falls to 65%. The proposed rule reflects a tightening because the current guidelines require amortization only down to 70% LTV, and do not quantify a minimum annual amortization. Indeed, our default rate expectation for a residential loan with a 65% LTV is just about half of our default expectation for a loan with an 85% LTV, reflecting the increased risk of high-LTV loans.

Finanstilsynet proposed requiring that banks assume a six-percentage-point increase of the interest rate when checking borrower affordability, up one percentage point from the previous five-percentage-point stress rate requirement. This reflects the lower market interest rates that form the basis of the calculation. Importantly, banks will no longer be allowed to bypass the stress test based on a special prudential assessment of the borrower’s circumstances.

The financial regulator also recommended that the Ministry of Finance establish the underwriting requirements in the form of regulation, contrary to the current requirements, which are only guidelines. This step is positive because it would stop banks’ from deviating from the underwriting requirements, and give the regulator a basis for tighter supervisory follow-up action. Finanstilsynet’s survey last year of residential lending showed an increase in the proportion of mortgages with a high LTV, which indicated that a number of banks had relaxed lending practices.

Norwegian household indebtedness is high by international standards and has risen more quickly than incomes (see exhibit). Consequently, Norway’s ratio of debt to income is high at 201% compared with the European Union average of around 100% (based on latest available data). Increasing property prices, low interest rates, a robust general economy and generous social security benefits have prevented nonperforming loan levels from rising from low levels.

Alexander Zeidler Vice President - Senior Analyst +44.20.7772.8713 [email protected]

Elise Savoye, CFA Assistant Vice President - Analyst +33.1.5330.1079 [email protected]

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

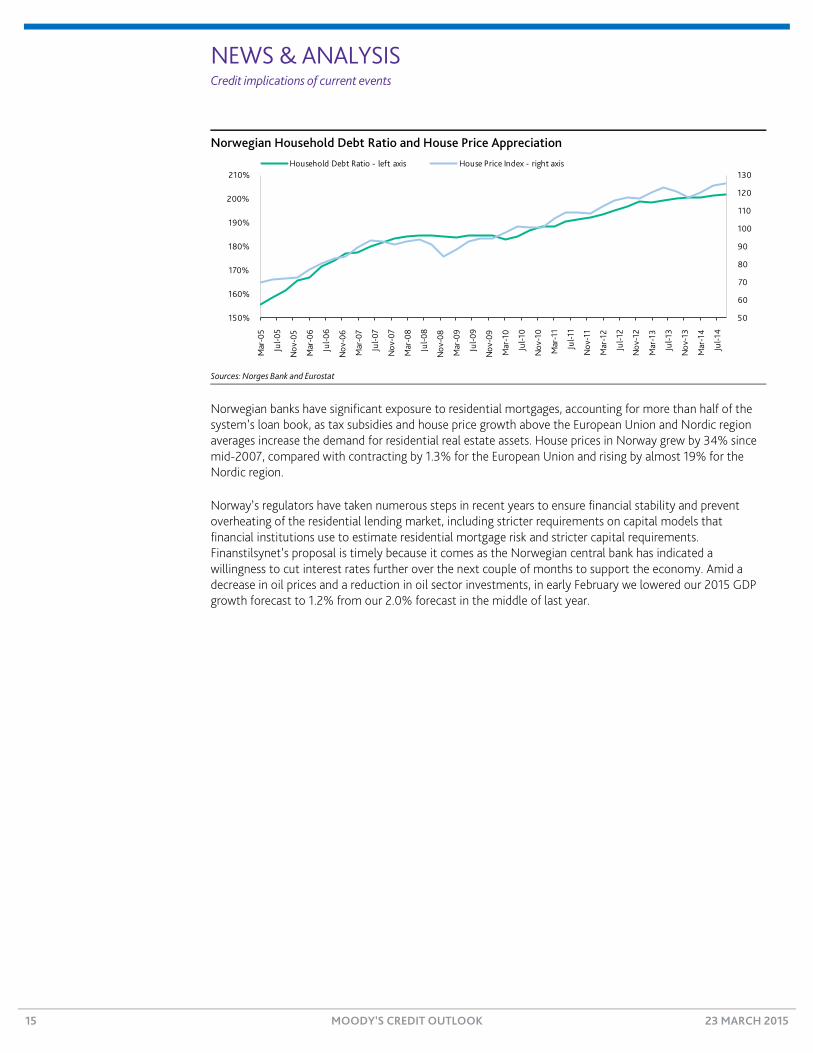

Norwegian Household Debt Ratio and House Price Appreciation

Sources: Norges Bank and Eurostat

Norwegian banks have significant exposure to residential mortgages, accounting for more than half of the system’s loan book, as tax subsidies and house price growth above the European Union and Nordic region averages increase the demand for residential real estate assets. House prices in Norway grew by 34% since mid-2007, compared with contracting by 1.3% for the European Union and rising by almost 19% for the Nordic region.

Norway’s regulators have taken numerous steps in recent years to ensure financial stability and prevent overheating of the residential lending market, including stricter requirements on capital models that financial institutions use to estimate residential mortgage risk and stricter capital requirements. Finanstilsynet’s proposal is timely because it comes as the Norwegian central bank has indicated a willingness to cut interest rates further over the next couple of months to support the economy. Amid a decrease in oil prices and a reduction in oil sector investments, in early February we lowered our 2015 GDP growth forecast to 1.2% from our 2.0% forecast in the middle of last year.

50

60

70

80

90

100

110

120

130

150%

160%

170%

180%

190%

200%

210%

Mar

-05

Jul-0

5

Nov

-05

Mar

-06

Jul-0

6

Nov

-06

Mar

-07

Jul-0

7

Nov

-07

Mar

-08

Jul-0

8

Nov

-08

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Jul-1

0

Nov

-10

Mar

-11

Jul-1

1

Nov

-11

Mar

-12

Jul-1

2

Nov

-12

Mar

-13

Jul-1

3

Nov

-13

Mar

-14

Jul-1

4

Household Debt Ratio - left axis House Price Index - right axis

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

China Reins in Securities Companies’ Stock Repo Business, a Credit Positive On 17 March, the Securities Association of China issued guidance for securities companies’ repurchase (repo) business using stock as collateral (i.e., stock-pledged repo loans). The new guidance sets required risk management components and processes, and caps total loans at 200% of a company’s net capital,1 and loans to a single borrower at 10% of its net capital.

This guidance is credit positive for China’s securities companies because it will incentivize them to strengthen their risk management in this relatively new and exponentially growing business. We believe China’s larger securities companies are in a better position to grow their stock-pledged repo business than smaller companies because they generally have better risk management systems and access to capital markets. This will benefit companies such as CITIC Securities Company Limited (Baa1 stable) and Haitong Securities Company Limited (unrated), which are listed on stock exchanges in China and Hong Kong.

Compared to securities companies’ other primary lending activities such as margin financing, loans secured with stock-pledged repo agreements can be used for varied purposes, have longer maturities and less liquid collateral – factors underlying their growth – but they also have greater credit, market and liquidity risks. We expect stock-pledged repo growth among larger securities companies to accelerate with the currently rising stock market and positive market sentiment (see Exhibit 1).

EXHIBIT 1

Outstanding Stock-Pledged Repo Balance of Select Large Chinese Securities Companies

Everbright = China Everbright Securities Co. Ltd.; China Merchants = China Merchants Securities Co. Ltd; Guosen = Guosen Securities Co. Ltd.; Orient = Orient Securities Co. Ltd. CITICS, Haitong, China Everbright; China Merchants and Guosen have not published their 2014 results.

Sources: Company data

In particular, the caps on total and single-borrower repo lending will help limit the industry’s leverage and concentration risks. We see the overall cap as largely preemptive because the ratio of stock-pledged repo to net capital is still far below 200% for most major securities companies (see Exhibit 2). Based on the industry’s reported net capital of RMB568 billion as of December 2014, the caps would limit the loans available for stock-pledged repo business at around RMB1.3 trillion.

1 Net capital is risk-adjusted capital after deducting risk weighted assets from total equity.

0

2

4

6

8

10

12

14

16

CITICS Haitong Guangfa Huatai China Everbright China Merchants Guosen Orient

RMB

Billi

ons

Dec-13 Jun-14 Dec-14

Sean Hung Assistant Vice President - Analyst +852. 3758.1503 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

EXHIBIT 2

Total Loans for Stock-Pledged Repo to Net Capital and Total Equity of Select Large Securities Companies

Note: CITICS, Haitong, China Everbright, China Merchants and Guosen data is first-half 2014 data. Other data is for 2014. Sources: Company data

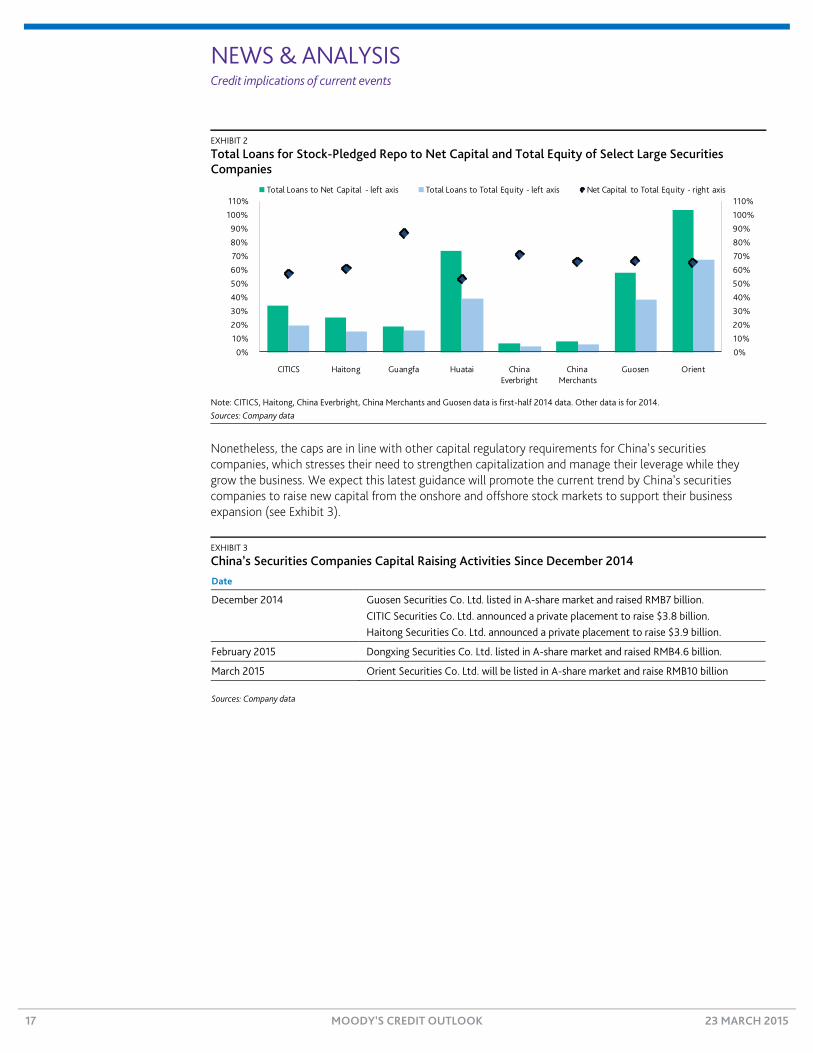

Nonetheless, the caps are in line with other capital regulatory requirements for China’s securities companies, which stresses their need to strengthen capitalization and manage their leverage while they grow the business. We expect this latest guidance will promote the current trend by China’s securities companies to raise new capital from the onshore and offshore stock markets to support their business expansion (see Exhibit 3).

EXHIBIT 3

China’s Securities Companies Capital Raising Activities Since December 2014 Date

December 2014 Guosen Securities Co. Ltd. listed in A-share market and raised RMB7 billion. CITIC Securities Co. Ltd. announced a private placement to raise $3.8 billion. Haitong Securities Co. Ltd. announced a private placement to raise $3.9 billion.

February 2015 Dongxing Securities Co. Ltd. listed in A-share market and raised RMB4.6 billion.

March 2015 Orient Securities Co. Ltd. will be listed in A-share market and raise RMB10 billion

Sources: Company data

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

CITICS Haitong Guangfa Huatai China Everbright

China Merchants

Guosen Orient

Total Loans to Net Capital - left axis Total Loans to Total Equity - left axis Net Capital to Total Equity - right axis

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Sovereigns

Israeli Elections Signal Economic Policy Cohesion, a Credit Positive Last Tuesday, Israel’s incumbent Prime Minister Benjamin Netanyahu won a surprising and decisive victory in general elections that will likely result in a more quickly formed and stable government coalition and cohesive economic policy than the preceding short-lived incongruent administration. Consequently, we expect the government to present Israel’s parliament, the Knesset, with a budget within roughly 100 days of its formation, as required. Although the precise compromises within the new budget remain to be seen because the probable choice for finance minister will be someone new to the post, we expect the government’s fiscal rules to contain spending growth and keep credit metrics for Israel (A1 stable) on their well-established improving trend, a credit positive.

Disagreements over the 2015 budget were the proximate cause of the government’s early dissolution in December 2014, but the dispute was just one of many within the coalition formed in March 2013. Israel’s many-party system with proportional representation and low vote thresholds has never resulted in a majority government in the 120-seat Knesset in the country’s 67-year history. Twenty-five parties contested last week’s election and 10 parties won sufficient votes to elect members of the Knesset (MKs). Prime Minister Netanyanhu’s right-leaning Likud Party won 30 seats, more than any other party. The new center-left grouping, the Zionist Union (see exhibit below), won 24 seats, the second largest amount. President Reuven Rivlin is currently consulting with the party leaders to decide which of them will be able to form a workable coalition most quickly, and is widely expected to choose Mr. Netanyahu, who has indicated his choices about building a new coalition.

Israeli Parliament Composition by Party and Number of Seats

Source: Haaretz

Pundits expect the new government to comprise center-right parties Likud, with Mr. Netanyahu as prime minister; along with Moshe Kahlon’s new Kulanu Party, which won 10 seats; the ultra-orthodox parties of Shas and UTJ, with 13 seats; followed by the combined 13 seats of the right-wing parties of Jewish Home and Yisrael Beiteinu. This would constitute a commanding majority by Israeli standards of 67 seats. Mr. Kahlon is likely to be the next finance minister because of the number of seats his party controls and his popularity after having broken up the cell phone monopoly after he became communications minister in 2009. Such a government would likely be inherently more stable than a coalition led by the center-left Zionist Union, which would struggle to put together a majority.

Once formed, the new government will need to start building a consensus among coalition members about the 2015 budget, which was never finalized. Without a finalized budget, the government continues to operate on the basis of the amount allocated in the previous year’s budget, with monthly spending capped at one twelfth of that budget. This constraint will likely mean that regardless of the 2015 budget outline, the budget deficit will narrow relative to last year’s 2.9% of GDP outcome.

Likud30

Zionist Union24

UTJ6Joint List of Arab parties

13

Yesh Atid11

Kulanu10

Jewish Home8

Shas7

Yisrael Beiteinu 6

Meretz5

120 seats

Kristin Lindow Senior Vice President +1.212.553.3896 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

The negotiations over the budget will not be easy – they never are in Israel given the diversity of interests in any coalition. We expect that a two-year budget will be promulgated given how late in the year the 2015 budget will be finalized, such as was done after the elections in 2011 and 2013. The avoidance of another round of budget negotiations later in the year will save considerable time and potentially reduce the political capital expended in this budget round.

Moreover, although the dominant issue in Mr. Kahlon’s own campaign was the high cost of living chiefly related to the issue of housing costs, this stance is not antithetical to Likud’s economic views. On the other hand, clashes between these two parties in the anticipated coalition could still occur over time should attempts to overcome the scarcity of available land – the key element keeping house prices high – begin to challenge vested interests.

Nonetheless, the economy’s recovery from last year’s Gaza conflict should lead to rapid consensus over the budget allocations since it means that the revenue situation has been more favorable than expected in the never-finalized 2015 budget proposal of the former government, and the uninterrupted improvement in the government’s credit metrics will therefore likely continue. With a dominant 67-seat majority likely, we expect the new administration will be more long-lived than the last, providing time to coalesce public opinion around key issues facing the country.

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Sub-sovereigns

German Local Governments and Public-Sector Pfandbriefe Will Benefit from Infrastructure and Climate Initiative On 18 March, the Government of Germany (Aaa stable) adopted a draft law to support financially weak municipalities via a separate estate fund earmarked for projects in infrastructure and climate protection. Participating municipalities need to contribute a minimum of 10% of a project’s cost from their own capital, and the central government will provide the remaining funds. The new programme shows the central government’s support for municipalities and is credit positive for local governments and public-sector Pfandbriefe. Municipal debt accounts for 28% of cover pool assets of the German public-sector Pfandbriefe that we rate.

According to the central government, municipal investment for the maintenance, refurbishment and conversion of local infrastructure has increased over the past two years. However, only financially strong municipalities have been in the position to increase their investments, while financially weaker municipalities scaled down on their investments. We believe that a divergence in the investment behaviour between strong and weak municipalities leads to discrepancies in the quality of regional infrastructure, which then affects the region’s attractiveness to companies and work force. According to the federal statistical office Destatis’ population study and forecast, populations in the Eastern states of Brandenburg (Aa1 stable), Mecklenburg-Western Pomerania (unrated), Saxony (unrated), Saxony-Anhalt (Aa1 stable) and Thuringia (unrated), which are among those with little own-source revenues, will decrease by 16% by 2030.

In Germany, financial support and supervision of municipalities is a responsibility of the 16 regional governments, the Laender. Over the years, the Laender have implemented programs to provide financial transfers to assist municipalities in financial stress. In turn, municipalities that accepted assistance had to commit to savings measures, leading the weaker municipalities’ to trim their infrastructure investment. The German central government’s initiative therefore specifically aims to provide funds earmarked for infrastructure investments and climate protection for these financially weaker municipalities.

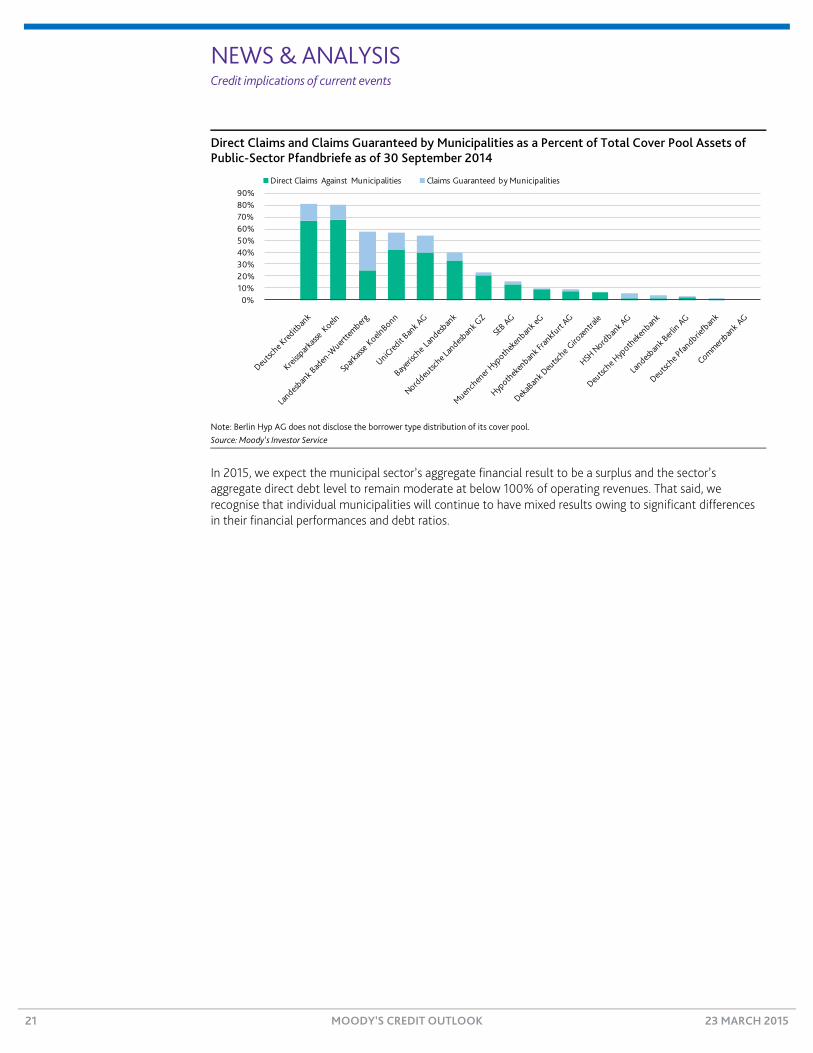

The central government’s initiative is also credit positive for public-sector Pfandbriefe. German municipalities, which have total outstanding debt of around €135 billion, traditionally fund their investments and general expenses with bank loans. According to the Pfandbrief Act, municipal debt is eligible for cover pools and more than 50% of the municipal’s debt is refinanced via public-sector Pfandbriefe. Among the 17 public-sector covered bond programmes that we rate in Germany, five cover pools are exposed to municipal debt in excess of 50%, as shown in the exhibit. The covered bond issuer benefitting the most from the central government’s initiative is Deutsche Kreditbank. Its cover pool not only consists of 81% direct claims and claims guaranteed by municipalities, but also 56% of the obligors are located in the five Eastern German Laender.

Patrick Widmayer Assistant Vice President - Analyst +49.69.70730.715 [email protected]

Harald Sperlein Vice President - Senior Analyst +49.69.70730.906 [email protected]

Martin Lenhard Vice President - Senior Analyst +49.69.70730.743 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Direct Claims and Claims Guaranteed by Municipalities as a Percent of Total Cover Pool Assets of Public-Sector Pfandbriefe as of 30 September 2014

Note: Berlin Hyp AG does not disclose the borrower type distribution of its cover pool. Source: Moody’s Investor Service

In 2015, we expect the municipal sector’s aggregate financial result to be a surplus and the sector’s aggregate direct debt level to remain moderate at below 100% of operating revenues. That said, we recognise that individual municipalities will continue to have mixed results owing to significant differences in their financial performances and debt ratios.

0%10%20%30%40%50%60%70%80%90%

Direct Claims Against Municipalities Claims Guaranteed by Municipalities

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

US Public Finance

Puerto Rico Debt Restructuring Is Increasingly Likely, a Credit Negative On Sunday, legislators in Puerto Rico (Caa1 negative) unveiled plans to hold a referendum authorizing the US commonwealth to default on its debt. The credit-negative discussions, regardless of whether they culminate in enacted legislation, signal the rising likelihood of a consolidated debt restructuring that affects not only public corporations, but also the central government’s general obligation and other tax- backed securities.

Elected officials in Puerto Rico have now taken several steps that indicate their eroding willingness to pay central government and public corporation debt after a prolonged period of economic stagnation and rapid debt accumulation. A law enacted in June 2014 provided a framework for some Puerto Rico public corporations to restructure their debt. The law also had implications for central government obligations because it showed the government’s decreasing willingness to repay its debt in general.

The legislature’s latest effort again underscores that political forces will encourage the government to put a higher priority on allocating funds to public services rather than debt service, making bondholders shoulder part of the fiscal burden. The proposed referendum would effectively waive constitutional requirements to prioritize Puerto Rico’s general obligation and government-guaranteed debt service payments over other purposes. Such populist proposals may gain increased prominence as Puerto Rico’s 2016 general election approaches. Even the Puerto Rico Sales Tax Financing Corporation senior bonds, which at B3 negative are Puerto Rico’s highest-rated security, may be vulnerable to such efforts as elected officials strive to keep up service levels or to bolster the local economy.

So far, Puerto Rico’s other initiatives aimed at facilitating a debt restructuring have not resulted in viable legal mechanisms. On 6 February, a US District Court judge ruled as unconstitutional last June’s public corporation debt restructuring law, citing Congress’ intent that municipal bankruptcy should occur “only pursuant to a uniform federal law.” A proposal introduced last month to revise the US Bankruptcy Code so that Puerto Rico’s municipalities and public corporations could make use of it has not advanced in Congress.

To be sure, defaults and restructurings can occur even apart from a formal legal framework, as debt restructuring by the Puerto Rico Electric Power Authority (PREPA, Caa3 negative) demonstrates. We expect that PREPA’s restructuring, under a forbearance agreement with bondholders, will entail bondholder losses of 20%-35%.

Legislative actions aimed at weakening Puerto Rico’s legal obligations to existing investors have coincided with rising yields on Puerto Rico’s outstanding bonds. As shown in the exhibit below, this can occur even when interest rates in general are declining. The yield spread between Puerto Rico’s 2035 general obligation bonds and comparable Aaa-rated tax-exempt debt widened to 620 basis points in early July, after passage of the public corporation debt restructuring law, from 450 basis points three months earlier. The spread was 661 basis points as of 16 March. The current legislative discussions risk diminishing Puerto Rico’s ability to issue about $2 billion of petroleum products tax-backed debt that the government is relying on to replenish liquidity in coming weeks.

Generic 30-Year Aaa General Obligation Puerto Rico 2035 General Obligation Spread

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Dwindling Federal Transportation Funds Threaten Revenues States Use to Pay Debt On 12 March, the US Congressional Budget Office (CBO) estimated that the federal Highway Trust Fund (HTF) will run out of money this summer. The forecast highlights the urgency that Congress faces to pass a new highway spending bill or extend the current one to avoid an interruption in federal aid to state transportation and transit agencies starting as soon as 31 May. States and transit agencies use US Department of Transportation (DOT) funding to pay debt service on billions of dollars in grant anticipation bonds (GARVEEs) issued to fund transportation projects. The CBO forecast and continued congressional uncertainty surrounding the annual $53 billion in transportation aid is credit negative for GARVEEs, although some states are adapting by reducing infrastructure spending, building reserves and raising fuel taxes to increase their own resources.

States have a number of options to address stagnant and uncertain federal transportation funds. In December, the Tennessee (Aaa stable) Department of Transportation said it would reduce annual project work by $250 million, a move followed by Missouri (Aaa stable) and Arkansas (Aa1 stable). On the revenue side, Iowa (Aaa stable), Utah (Aaa stable) and South Dakota (lease appropriation Aa2 stable) are among the latest states to raise fuel taxes. Indiana (Aaa stable), on the other hand, has used public-private partnerships to fund its infrastructure needs. Other state responses include increased general fund support, taking on more debt and raising tolls.

Before Congress passed the transportation funding extension last year, the DOT provided guidance on what a funding interruption might mean. The DOT said it would need to either delay or reduce reimbursements to state transportation entities by 27% if the HTF fell below a $5 billion threshold. The balance is currently $11 billion and the CBO projects that it will fall below $5 billion sometime this summer. States expect reimbursement delays and reductions and are preparing to take actions to ensure they have sufficient funds to make required debt service payments. The HTF is the primary source of federal transportation aid to states and mass transit agencies.

The 18.4-cent federal gas tax has not been raised since 1993. The tax and a separate levy on diesel fuel account for 83% of HTF revenues. Funding has not kept pace with growing infrastructure needs, resulting in a $14 billion annual structural imbalance in the HTF.

Last June, we downgraded most GARVEE ratings secured solely by federal transportation grants to reflect the increased risk of a disruption in HTF funding prompting states to tap into their own funds to pay debt service on GARVEEs.

For decades, Congress authorized HTF funding for five- and six-year periods, funded by dedicated transportation taxes, which provided states with funding certainty. With fiscal challenges, Congress moved to a shorter two-year authorization in 2012 and a 10-month extension last year. With overall HTF spending outpacing dedicated revenues, Congress has addressed the imbalance by transferring a cumulative $65 billion of general funds to the HTF from 2008-14 (see exhibit). Funds already transferred will not be affected by any congressional impasse over whether to raise the debt limit.

Julius Vizner Assistant Vice President - Analyst +1.212.553.0334 [email protected]

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Covered Bonds

Sweden’s Proposed Mortgage Amortisation Requirement Would Be Credit Positive for Covered Bonds Last Wednesday, Finansinspektionen, Sweden’s financial regulator, proposed that all new mortgage loans starting on 1 August 2015 should amortise down to 50% of the property value at a minimum annual rate depending on the mortgage’s loan-to-value ratio (LTV) at origination. This proposal, which we see as likely to take effect, would be credit positive for Swedish covered bonds because it would constrain household indebtedness and build up home equity.

Lansforsakringar Hypotek Covered Bonds (Aaa) and Skandiabanken Swedish Pool – Mortgage Covered Bonds (Aaa) would benefit the most from the regulation because their Swedish residential mortgages comprise 91% and 100% of their cover pools, respectively.

The new amortisation proposal would slow the growth of Swedish household indebtedness, which is high by European standards and has increased by almost 50% since 2002, according to Eurostat. Swedish households in the lowest income decile have a high average debt-to-disposable income ratio (DTI) of 347%, while households in the highest income decile have an average DTI of 251%, according to Sveriges Riksbank, Sweden’s central bank. With housing loans typically the largest source of indebtedness, the accumulation of substantial debt exposes households to house price declines and interest rate increases. This exposure is further exacerbated by Sweden’s high level of home ownership, largely because of constraints on rental pricing and availability.

Over time, increased amortisation would reduce the average LTVs in covered bond asset portfolios. The Finansinspektionen proposes that new mortgage loans, typically capped at a maximum LTV of 85%, would be amortised at 2% of the loan per year until the LTV falls to 70%, at which point the amortisation would be 1% per year until the LTV falls to 50%. The requirement has a countercyclical element because LTV variations owing to house price changes would only be factored in every five years at the earliest. The amortisation of the loans should therefore lead to sustainable reductions in asset portfolio LTVs, albeit at a slow pace given that the regulation is only applicable to new loans. To indicate some of the benefit of this, our default rate expectation for a loan with a 50% LTV is just about half of our expectation for a loan with a 70% LTV, reflecting the increased risk of high LTV loans.

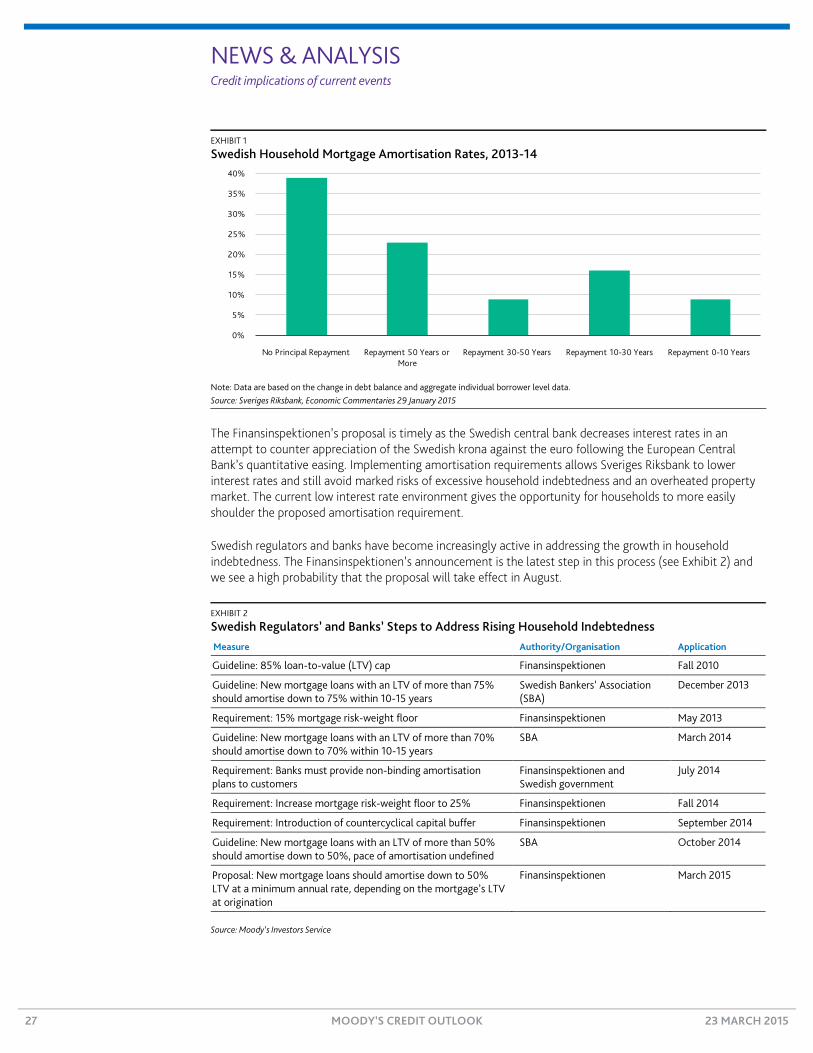

The Finansinspektionen’s proposal would further counter the current lack of an amortisation culture among mortgage borrowers, thereby supporting the credit quality of mortgage loans backing covered bonds. Over time, borrowers would build up increased home equity. In its statement, the central bank pointed to the low repayment levels of mortgage borrowers, and showed that about 40% of households did not make principal payments between 2013-14 and that 23% made payments at a rate requiring longer than 50 years to repay their debt (see Exhibit 1). Building up home equity would reduce the risk of borrowers defaulting and limit losses in the event that a property must be liquidated.

Alexander Zeidler Vice President - Senior Analyst +44.20.7772.8713 [email protected]

Jane Soldera Vice President - Senior Credit Officer +44.20.7772.5318 [email protected]

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

EXHIBIT 1

Swedish Household Mortgage Amortisation Rates, 2013-14

Note: Data are based on the change in debt balance and aggregate individual borrower level data. Source: Sveriges Riksbank, Economic Commentaries 29 January 2015

The Finansinspektionen’s proposal is timely as the Swedish central bank decreases interest rates in an attempt to counter appreciation of the Swedish krona against the euro following the European Central Bank’s quantitative easing. Implementing amortisation requirements allows Sveriges Riksbank to lower interest rates and still avoid marked risks of excessive household indebtedness and an overheated property market. The current low interest rate environment gives the opportunity for households to more easily shoulder the proposed amortisation requirement.

Swedish regulators and banks have become increasingly active in addressing the growth in household indebtedness. The Finansinspektionen’s announcement is the latest step in this process (see Exhibit 2) and we see a high probability that the proposal will take effect in August.

EXHIBIT 2

Swedish Regulators’ and Banks’ Steps to Address Rising Household Indebtedness Measure Authority/Organisation Application

Guideline: 85% loan-to-value (LTV) cap Finansinspektionen Fall 2010

Guideline: New mortgage loans with an LTV of more than 75% should amortise down to 75% within 10-15 years

Swedish Bankers’ Association (SBA)

December 2013

Requirement: 15% mortgage risk-weight floor Finansinspektionen May 2013

Guideline: New mortgage loans with an LTV of more than 70% should amortise down to 70% within 10-15 years

SBA March 2014

Requirement: Banks must provide non-binding amortisation plans to customers

Finansinspektionen and Swedish government

July 2014

Requirement: Increase mortgage risk-weight floor to 25% Finansinspektionen Fall 2014

Requirement: Introduction of countercyclical capital buffer Finansinspektionen September 2014

Guideline: New mortgage loans with an LTV of more than 50% should amortise down to 50%, pace of amortisation undefined

SBA October 2014

Proposal: New mortgage loans should amortise down to 50% LTV at a minimum annual rate, depending on the mortgage’s LTV at origination

Finansinspektionen March 2015

Source: Moody’s Investors Service

0%

5%

10%

15%

20%

25%

30%

35%

40%

No Principal Repayment Repayment 50 Years or More

Repayment 30-50 Years Repayment 10-30 Years Repayment 0-10 Years

CREDIT IN DEPTH Detailed analysis of an important topic

28 MOODY’S CREDIT OUTLOOK 23 MARCH 2015

Credit in Depth

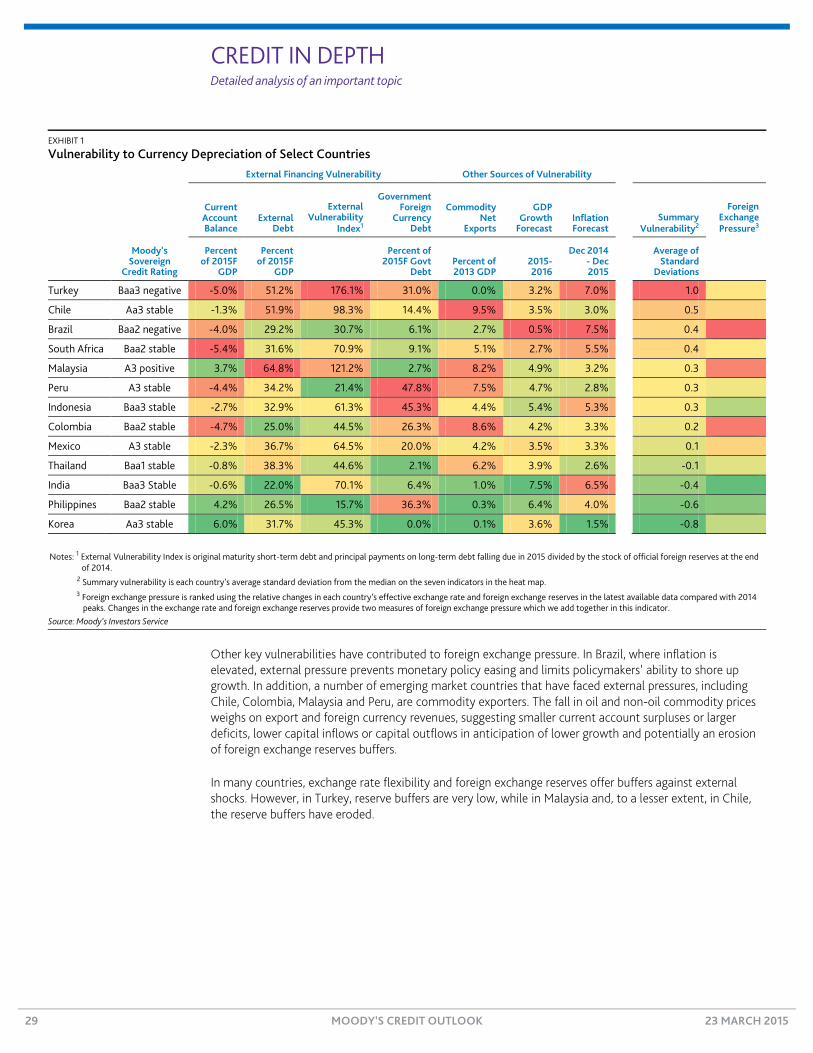

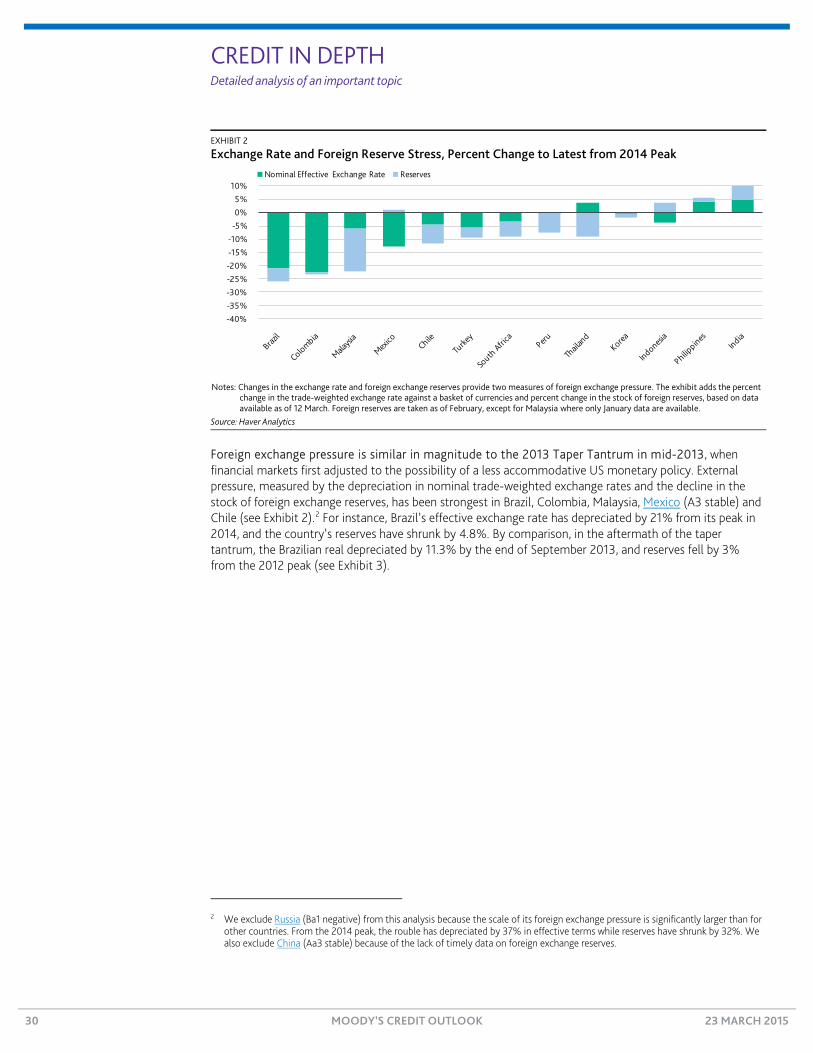

US Dollar Strength Hurts Countries with Large External Financing Needs In recent weeks, the strengthening US dollar has prompted a sharp currency depreciation and/or a significant decline in the foreign exchange reserves of a number of countries. To the extent that these fluctuations reflect capital outflows or significantly lower external inflows, they are credit negative for countries with large external funding needs. Countries with sizable current account deficits, such as Turkey (Baa3 negative) and South Africa (Baa2 stable), and to a lesser extent, Colombia (Baa2 stable) and Brazil (Baa2 negative), are vulnerable to weaker external net inflows, because this would point to potential difficulty in financing deficits.

A weaker exchange rate is also credit negative for countries with large pending external debt payments, such as Turkey, Malaysia (A3 positive) and Chile (Aa3 stable) because it raises the cost of repaying and refinancing foreign currency debt and suggests shrinking foreign reserves to meet external obligations that are difficult to refinance.

We illustrate the linkages between foreign exchange pressure and vulnerability to external financing needs in Exhibit 1 for a range of large emerging market countries. We assess external financing vulnerability using four indicators: current account balances, overall external debt, external debt repayments due in the short term relative to foreign exchange reserves, and the share of foreign currency debt in total government debt. The countries under most intense foreign exchange pressure are also those with large external financing needs. Vulnerability is particularly high in Turkey, where downward pressure on the lira’s foreign exchange rate has so far been less severe than in some of the most affected emerging market countries, although it has intensified recently.

Marie Diron Senior Vice President +44.20.7772.1059 [email protected]

Notes: 1 External Vulnerability Index is original maturity short-term debt and principal payments on long-term debt falling due in 2015 divided by the stock of official foreign reserves at the end

of 2014. 2 Summary vulnerability is each country’s average standard deviation from the median on the seven indicators in the heat map. 3 Foreign exchange pressure is ranked using the relative changes in each country’s effective exchange rate and foreign exchange reserves in the latest available data compared with 2014

peaks. Changes in the exchange rate and foreign exchange reserves provide two measures of foreign exchange pressure which we add together in this indicator. Source: Moody’s Investors Service