39

Morgan Stanley Conference Robin Freestone Chief Financial Officer 19 November 2008

Morgan Stanley Conference

Robin FreestoneChief Financial Officer

19 November 2008

Forward-looking statements

Except for the historical information contained herein, the matters discussed in this presentation include forward-looking statements. In particular, all statements that express forecasts, expectations and projections with respect to future matters, including trends in results of operations, margins, growth rates, overall market trends, the impact of interest or exchange rates, the availability of financing, anticipated costs savings and synergies and the execution of Pearson's strategy, are forward looking statements. By their nature, forward looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will occur in future. There are a number of factors which could cause actual results and developments to differ materially from those expressed or implied by these forward looking statements, including a number of factors outside Pearson's control. These include international, national and local conditions, as well as competition. They also include other risks detailed from time to time in the company's publicly-filed documents. Any forward looking statements speak only as of the date they are made, and Pearson gives no undertaking to update forward-looking statements to reflect any changes in its expectations with regard thereto or any changes to events, conditions or circumstances on which any such statement is based.

Agenda

Strategy & performance

Resilience

Growth

Diversified Revenue Mix

Europe 12%

US School Curriculum14%

ROW 3%Asia 8%

Europe27%

North America 62%

Revenue by Business Revenue by Geography

North AmericanEducation

41%

InternationalEducation

18%Pro

fessional 5%

Penguin

20%

FT Group

16%Assessment &

Information10%

US Higher Education

14%

Canada 3%

Advertising 5%

Content 11%

RoW 6%

UK 4%

US 10%

Testing 3%Publishing 2%

Asia 3%Americas 2%

Middle East & Africa 1%

The largest education publishing & services company

CengageLearning

HMH

McGraw-Hill

Pearson

CengageLearning

SanomaWSOY

InfinitasLearning

McGraw-Hill

Prisa

Lagardere

Pearson*5.6

2.7

2.5

1.90.3

0.4

0.4

0.7

0.8

1.6

0.2

#1 in Global education publishing & servicesLargest education publisher in the world (US$ revenue in billions, 2007)

#1 in Intl education publishing & servicesLargest education publisher ex-US(US$ revenue in billions, 2007)

Source: Pearson, Company Accounts, Analyst estimates * Pro forma to include Harcourt International

(1) Pearson excludes Government Solutions & Scanners andincludes Harcourt Assessment & International and eCollege.(2) Houghton Mifflin Harcourt (HMH) including HM Riverdeep andHarcourt US Basal & Supplemental.(3) Cengage Learning includes Houghton Mifflin Higher Education

Unique breadth of our education business

Professional testing

International Education*

CengageLearning

Higher Education

School Enterprise Software

Curriculum Software

School Assessment

School Basal & Supplemental

HMHMcGraw-

HillPearsonMarket share

* Non-US Market leader Market participant

The FT Group

Global market for Evaluated Pricing Data by Vendor (2007)

Source: Interactive Data investor day presentation

S&P9%

Interactive Data 63%

Others14%

Reuters 7%

Bear Stearns 5% Telekurs 2%

0 10 20 30

Business Week

Fortune

Forbes

WSJ

The Economist

Financial Times

US % C-Suite readership

Source: Mendelsohn Survey

Penguin

0.8

0.8

0.8

1.2

1.3

1.7

1.9

2.5

Simon & Schuster

De Agostini

Holtzbrinck

Scholastic

HarperCollins

Penguin

Lagardere

Random House

Trade publishing revenues, 2006 ($bn)

Source: Pearson, Company Accounts, Analyst estimates$ amounts converted at the average exchange rate for the year

Content +

Technology and services

International expansion

Efficiency

Business priorities

Sustained financial progress

Operating profit

55--year CAGR: 15% at constant exchange ratesyear CAGR: 15% at constant exchange rates

Margin 10.8% 10.8% 12.4% 13.4% 15.0%

£/$ 1.63 1.83 1.81 1.84 2.00

Margin improvement

Margins

£m 2007 2006 2005 2004

School 13.2% 12.6% 11.4% 9.9%

Higher Education 20.3% 20.3% 20.0% 17.7%

Professional 11.3% 9.6% 7.6% 7.9%

FT Publishing 16.3% 8.7% 6.3% 1.3%

Interactive Data 28.2% 26.8% 26.9% 24.9%

Penguin 8.7% 7.8% 7.5% 6.6%

Pearson 15.0% 13.4% 12.4% 10.8%

Reported margins

Strong cash generation

Operating cash flow

Cash Conversion 71% 98% 113% 97% 108%FCF per share (p) 40.0 52.5 71.4 72.0 85.8

55--year CAGR: 21%year CAGR: 21%

Improvement in ROIC

Return on invested capital

Cash and working capital disciplineAverage working capital/sales

Includes capitalised pre-publication costs and author advances

31.9%30.7% 30.6%

29.4%27.4% 26.3% 25.6%

Capital allocation: dividend growth

Pence per share

17.4 18.8 20.1 21.4 22.3 23.4 24.2 25.427

29.331.6

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Capital allocation: organic investment

Education pre-publication expenditure, $m

283 303 319 344 364421

2002 2003 2004 2005 2006 2007

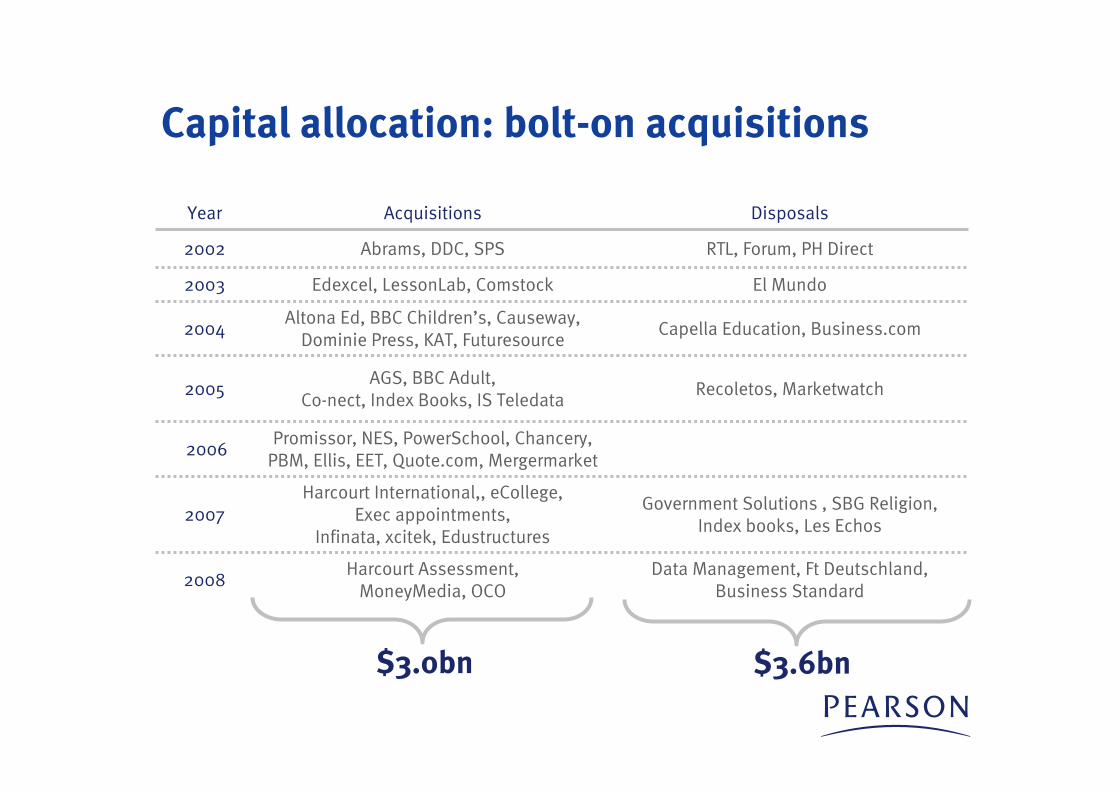

Capital allocation: bolt-on acquisitions

Government Solutions , SBG Religion, Index books, Les Echos

Harcourt International,, eCollege, Exec appointments,

Infinata, xcitek, Edustructures2007

Data Management, Ft Deutschland, Business Standard

Harcourt Assessment, MoneyMedia, OCO

2008

Promissor, NES, PowerSchool, Chancery, PBM, Ellis, EET, Quote.com, Mergermarket

2006

Year Acquisitions Disposals

2002 Abrams, DDC, SPS RTL, Forum, PH Direct

2003 Edexcel, LessonLab, Comstock El Mundo

2004Altona Ed, BBC Children’s, Causeway,

Dominie Press, KAT, FuturesourceCapella Education, Business.com

2005AGS, BBC Adult,

Co-nect, Index Books, IS TeledataRecoletos, Marketwatch

$3.0bn $3.6bn

9 month trading update

Trading in-line with expectations

Sales up 8% and operating profit up 11% at constant exchange rates

Strengthening dollar means eps likely to be towards the top of the consensus rate

“Pearson's strong performance continues. We're naturally cautious about the global economic conditions, but we have

good trading momentum, innovative products, resilient businesses and a strong balance sheet. With those advantages, we believe we are in good shape to prosper and strengthen our

company, even through these turbulent times.”

$ sensitivity

EPS 5¢ change in average rate = +/- 1p

2.00

1.99

2007

1.84

1.96

2006

1.81

1.72

2005

1.631.83Average rate

1.791.92Year end rate

20032004$:£

Resilience:Diversified Revenue Mix

Europe 12%

US School Curriculum14%

ROW 3%Asia 8%

Europe27%

North America 62%

Revenue by Business Revenue by Geography

North AmericanEducation

41%

InternationalEducation

18%Pro

fessional 5%

Penguin

20%

FT Group

16%Assessment &

Information10%

US Higher Education

14%

Canada 3%

Advertising 5%

Content 11%

RoW 6%

UK 4%

US 10%

Testing 3%Publishing 2%

Asia 3%Americas 2%

Middle East & Africa 1%

Resilience: Less exposure to advertising and tech publishing

2000 2007

£3.9bn @ £/$ 1.52 £4.2bn @ £/$ 2.00

Technology Publishing

Advertising

Other

AdvertisingTechnology Publishing

Other

Resilience: More diverse advertiser base

Growth Stable Cyclical

FT Newspaper advertising revenues 1997-2007

25%

30%

35%

40%

45%

50%

55%

60%

65%

2000 2001 2002 2003 2004 2005 2006 2007

Resilience: More diverse revenue base

Advertising revenues

Digital revenues

Resilience: Sustained growth in US educationYear-on-year US publishing industry sales growth

Sources: Pearson, AAP

Higher Education School

01 03 05 079997 01 03 05 079997

New adoptions down 20%+

CAGR = 7% CAGR = 5%

Resilience: fundingEnacted State revenue changes, $bn

(10)

(5)

0

5

10

15

20

1979 1982 1985 1988 1991 1994 1997 2000 2003 2006

Fiscal 1979 to Fiscal 2008 - US$bn

Source: NASBO

Resilience: balance sheet

Net debt/EBITDA Interest cover

1.3x

3.9x

2000 2007

3.1x

7.4x

2000 2007

Resilience: balance sheetDebt maturity profile

850852

350350500

1,750

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

US$m

Source: NASBO

Growth - Education

US Unemployment Rate, % (2007) US Median Weekly Earnings, $ (2007)

0 500 1,000 1,500

< high schooldiploma

High-schoolgraduate

Some college, nodegree

Associate degree

Bachelor'sdegree

Master's degree

Professionaldegree

Doctoral degree

Source: US Department of Labor

0 2 4 6 8

< high schooldiploma

High-schoolgraduate

Some college,no degree

Associatedegree

Bachelor'sdegree

Master'sdegree

Professionaldegree

Doctoraldegree

Global trends: Participation Number of pupils (m)

Source: UNESCO, World Bank

Primary

Secondary

Tertiary

317

50368

132

598 687

1991 2004

Global trends: Investment

Increase in public expenditure on education, 1991 - 2005 (1991=100)

118152 153 169

214253

320

547

UnitedStates

UnitedArab

Emirates

SouthKorea

Poland

Source: World Bank

Technology & Services: Education

Harcourt Assessment

Worldwide School & Professional testing revenues, $m

Technology & Services: Education

MyLab registrations, m

1.4

1.8

2.2

2.9

2004 2005 2006 2007

0.20.3

0.50.7

1.3

1.9

2002 2003 2004 2005 2006 2007

eCollege enrolments, m

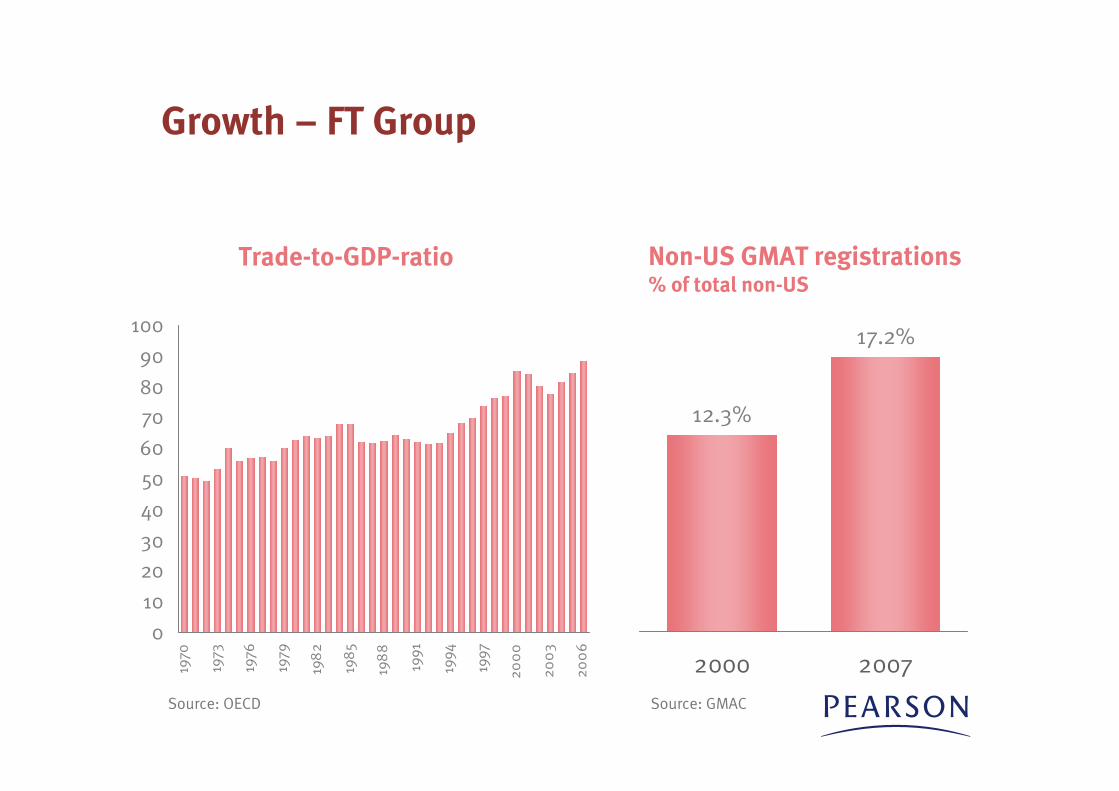

Growth – FT Group

Non-US GMAT registrations% of total non-US

17.2%

12.3%

2000 20070

10

20

30

40

50

60

70

80

90

100

1970

1973

1976

1979

198

2

198

5

198

8

1991

1994

1997

200

0

200

3

200

6

Trade-to-GDP-ratio

Source: OECD Source: GMAC

1997 2007

329,000

541,000

UK

Europe

FT.comAsia

International growth opportunities: FT Group

US

Sources: Audit Bureau of Circulation, Interactive Data

Europe

North America

Interactive Data sales by geography

Asia

Financial Times circulationby geography

Growth - Penguin

25.122.5

18.916.415.6

2000 2010 2020 2030 2040

% UK population aged 65+ years old

Source: US Census Bureau

International growth opportunities: Penguin

Rising literacy in IndiaPopulation (m); Literacy rate (%)

Rising book retail space in India Sq ft (top 3 book stores)

Sources: Ministry of Home Affairs, Office of the Registrar General

Source: Pearson

Technology & services: PenguinE-book units sold by month (US)

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Amazon Kindle launched

Conclusions

Strong market positions

Clear strategy; strong record of performance

Resilient; strong financial position

Good long-term growth markets

Morgan Stanley Conference