17

MP3 / MM740: Strategy & IS Fall 2001 Module 4: E-Commerce & Distribution Channels

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| View: | 214 times |

| Download: | 1 times |

MP3 / MM740: Strategy & ISFall 2001

Module 4: E-Commerce & Distribution Channels

Issues Covered

• Collapsing Channels– failures, successes, the role of value gaps

• Shifting Channels– marketplace to marketspace, channel

pressure, innovation

• New Intermediaries– examples, impact, threats, market creation

• Auction Models– markets of first and last resort

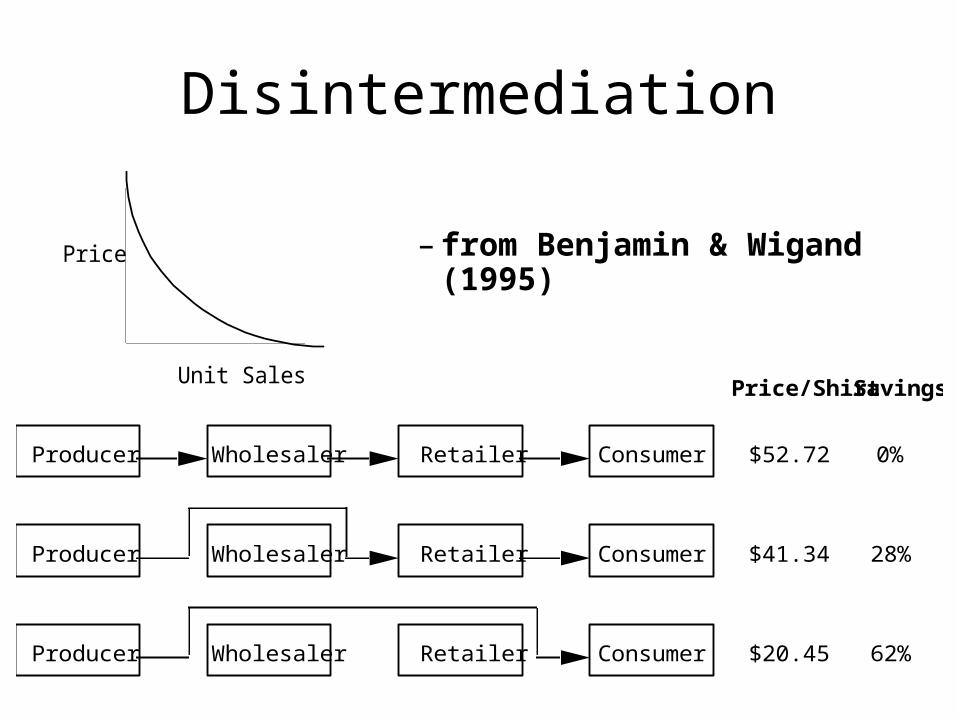

– from Benjamin & Wigand (1995)Price

Unit Sales

Producer Wholesaler Retailer Consumer

Producer Wholesaler Retailer Consumer

Producer Wholesaler Retailer Consumer

Price/Shirt Savings

$52.72

$41.34

$20.45

0%

28%

62%

Disintermediation

Value Gaps

customersretailerdistributorsource firm

Value Added = A,Expense = X

Value Added = B,Expense = Y

Expense Savings = (X+Y) - Cost of New EffortValue Gap = (A+B) - Value Added by New Effort

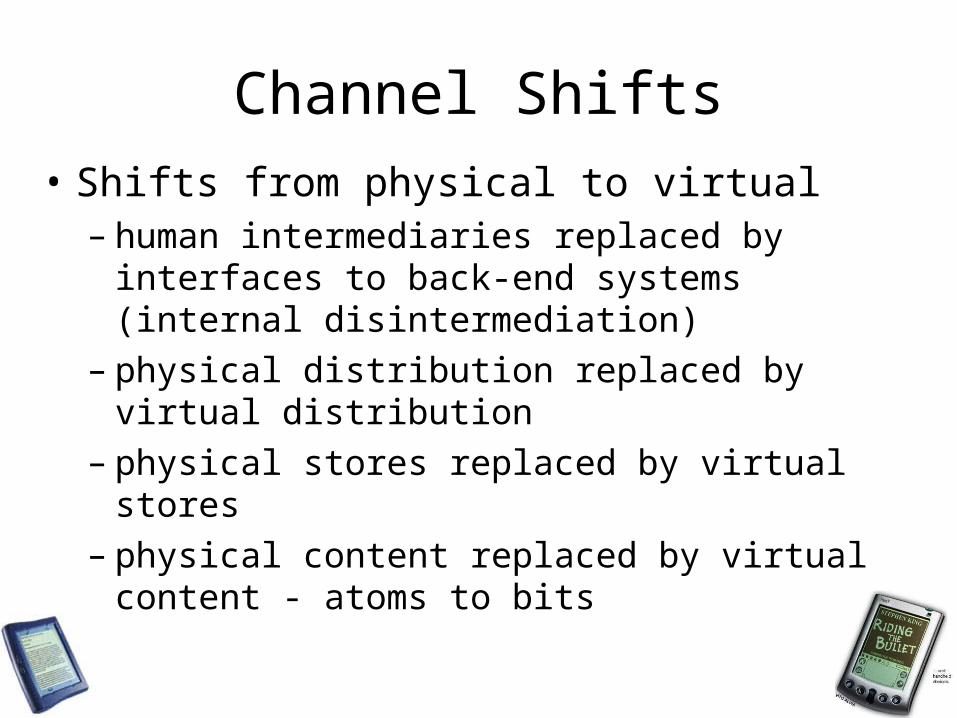

Channel Shifts

• Shifts from physical to virtual– human intermediaries replaced by interfaces to

back-end systems (internal disintermediation)– physical distribution replaced by virtual

distribution– physical stores replaced by virtual stores– physical content replaced by virtual content -

atoms to bits

Channel Pressure

supplier distributor retailer customermanufacturer

Traditional Channels

Online Channels

supplier customermanufacturer

suppliermanufacturer customernew intermediaries

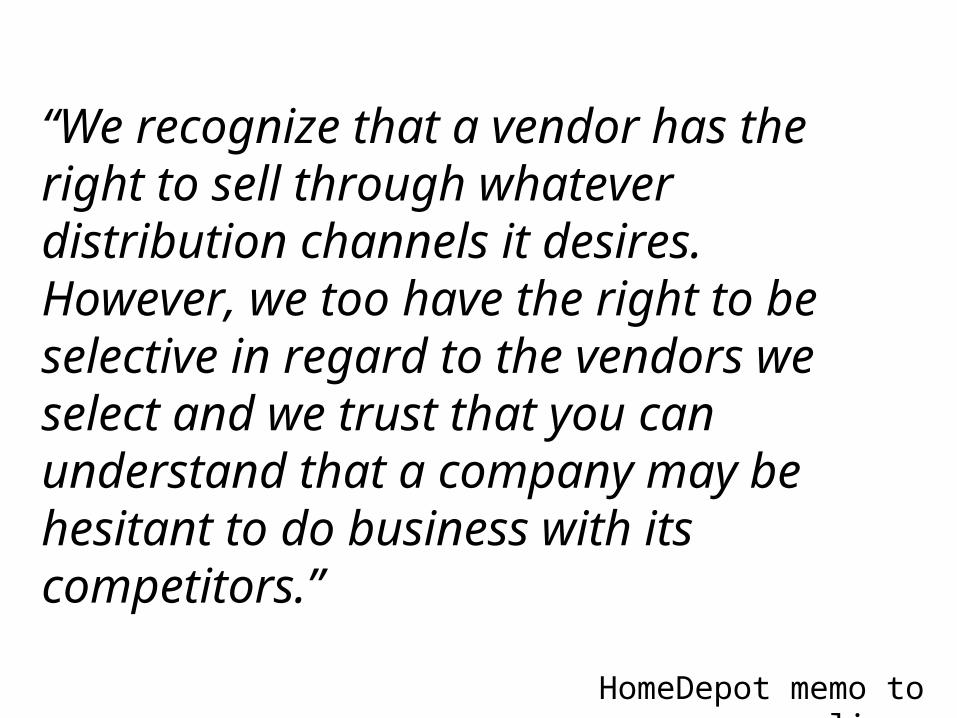

“We recognize that a vendor has the right to sell through whatever distribution channels it desires. However, we too have the right to be selective in regard to the vendors we select and we trust that you can understand that a company may be hesitant to do business with its competitors.”

HomeDepot memo to suppliers

Channel Extending Intermediaries

supplier customer

CEIsupplier

supplier

supplier

customer

customer

customer

Search for opportunities to add value: e.g. high customer search costs, switching costs, low customer satisfaction

Wield new power by consolidating traditional buyers & customers. Become the first-line interface with consumers.

Auction FormatsLiquidation Auctions: (e.g. Priceline, OnSale)

suppliers customersauction

Market Efficiency Auctions: (e.g. eBay)

Seek lowest price on widely available goods and services

auction

disincentives to use auction shrink supply over time

Seek first to maximize existing

channels & reduce inventory

suppliers customersSeek access to unique / rare products or services

incentives to use auction increase supply over time

Auction format is favored over the

inefficiency of existing channels

Issue Price vs. First Day Close

Company DateShares

UnderwrittenUnderwritingShare Price

First Day CloseShare Price Difference

Percent Undervalued

Transmeta 11/7/00 13,000,000 $21 $45 315,250,000$ 115%CoSine 9/26/00 10,000,000 $23 $70 470,000,000$ 204%Active Power 8/8/20 8,000,000 $17 $53 286,000,000$ 210%StorageNetworks 6/30/00 9,000,000 $27 $90 569,250,000$ 234%Red Hat 8/11/99 6,000,000 $14 $52 228,360,000$ 272%mp3.com 7/20/99 12,300,000 $28 $61 405,900,000$ 118%Efficient Networks 7/15/99 4,000,000 $15 $53 152,000,000$ 253%Tibco Software 7/14/99 7,300,000 $15 $40 182,500,000$ 167%China.com 7/13/99 4,200,000 $20 $67 197,862,000$ 236%CommTouch 7/13/99 3,000,000 $16 $24 24,000,000$ 50%eToys 5/19/99 8,300,000 $20 $77 473,100,000$ 285%iVillage 3/18/99 3,500,000 $24 $56 112,000,000$ 133%AutoWeb 3/23/99 5,000,000 $14 $28 71,250,000$ 102%Auto-by-Tel 3/24/99 3,500,000 $23 $40 60,375,000$ 75%Prodigy 2/11/99 8,000,000 $15 $28 105,040,000$ 88%VerticalNet 2/11/99 3,500,000 $16 $45 102,830,000$ 184%Healtheon 2/11/99 5,000,000 $8 $31 116,900,000$ 292%Pacific Internet 2/5/99 3,000,000 $17 $48 93,000,000$ 182%Theglobe.com 11/13/98 3,100,000 $9 $64 168,950,000$ 606%