The Malaysian Palm Oil FORTUNE is MPOC's (Malaysian Palm Oil Council) monthly market update covering the latest development in the oils and fats market. This newsletter can now be downloaded via MPOC's Website (http://www.mpoc.org.my). You can also make use of the Malaysian Palm Oil FORTUNE as your platform to advertise your products/services. We are ready to offer advertisement space in each monthly issue at very affordable rates.

WITH its import of palm oil from Malaysia recorded at 337,563 metric tonnes (MT) for the period January to November 2009, Iran is also the Middle East’s second largest importer of Malaysian palm oil after Egypt’s 588,957 MT. In fact, it has surpassed the import value recorded for the country in 2008. Due to this development, UAE’s position as the largest importer of Malaysian palm oil in the region west of Asia has been overtaken by Iran. Despite the global economic downturn and fluctuation in global commodities prices during this period, export of palm oil to Malaysia’s top five importing countries in the region has shown better improvement, except for UAE. Besides Iran, positive growth has been seen in exports to Oman, Saudi Arabia and Yemen. Our exports to these three countries in the January-November 2009 period exceeded their total import of Malaysian palm oil recorded in 2008, especially in Saudi Arabia and Iran (Table 1). After many years of dominating the biggest share and playing a significant role in the oils and fats market of West Asia and the Middle East, UAE has been hit hard by the global economic crisis. The economic growth of the Emirates has been affected and caused a great impact on its business environment. The financial crisis and debt in UAE could prolong its economic recovery, leading to slower business activities and lower demand – and eventually affect many industries in the country, including its oils and fats industry. The UAE is a major trading partner for Iran, with trade dominated by UAE exports to Iran. The bulk of merchandise supplied to Iran by UAE is products imported into UAE from foreign markets and repackaged for shipment to Iran. Iran represents about 14% of UAE’s total exports, including re-exports. About 86% of UAE’s import of palm oil is for re-export, with Iran being one of the major re-export destinations. However, the rising cost of re-exporting the commodity has prompted most companies to look for alternatives, including shipping the cargo directly to the final destinations. Previously, most of the companies, including those run by the Iranians, would ship their cargo into UAE for storage in warehouses and repackaging before being shipped to the final destinations. The world’s shipping freight rates have gone down but the rates in UAE remain the same. Therefore, some analysts suggested the cheaper mode of shipping palm oil directly from Malaysia to the Middle East destinations, since this will save the cost of storage. Iran is rich in natural resources, and its economy is highly dependent on the production and export of crude oil to finance government spending. Although Iran has vast petroleum reserves to meet the world’s energy needs, it lacks edible oils and fats supplies to meet local consumption. Moreover, as the most populous country in the Middle East with a population exceeding 73 million, Iran’s MALAYSIAN PALM OIL COUNCIL KKDN PP 14669/05/2010 (024659) VOL: 12 2009 MPOC FORTUNE MARKETING & MARKET DEVELOPMENT DIVISION For more information, please contact Tel : 603 - 7806 4097 Fax: 603 - 7806 2272 DIRECTOR Wira Adam [email protected]MANAGER Muhammad Kharibi Zainal Ariffin [email protected]MARKET ANALYSTS Asia Pacific Desmond Ng Kok Hooi [email protected]Lim Teck Chaii [email protected]South Asia Fatimah Zaharah Md Nan [email protected]Middle-East Mohamad Suhaili Hambali [email protected]Africa Nor Iskahar Nordin [email protected]Europe Azriyah Azian [email protected]Americas Ahmad Fadzli Abdul Aziz [email protected]Continued on page 9 ® Table 1: Malaysia’s Top 5 Palm Oil Importers in the West of Asia 2006 2007 2008 Jan-Nov Jan-Nov Change Change 2008 2009 (Vol) (%) Iran 245,716 231,071 259,511 248,827 337,563 88,736 35.7 UAE 302,736 360,509 357,949 346,888 172,323 (174,565) -50.3 Oman 73,939 96,359 92,942 86,706 93,157 6,451 7.4 Yemen 94,094 109,316 63,119 59,671 74,050 14,379 24.1 Saudi Arabia 59,421 33,736 28,121 27,104 43,978 16,874 62.3 Source: Exports Statistics from MPOB West Asian Countries Country Capital Bahrain Manama Georgia Tbilisi Iran Teheran Iraq Baghdad Israel Tel Aviv Jordan Amman Kuwait Kuwait City Lebanon Beirut Oman Muscat Qatar Doha Saudi Arabia Riyadh Syria Damascus U.A.E. Abu Dhabi Yemen Sanaa Iran: Biggest Importer of Malaysian Palm Oil West of Asia

Transcript

WITH its import of palm oil from Malaysia recorded at 337,563 metric tonnes (MT) for the period January to November 2009, Iran is also the Middle East’s second largest importer of Malaysian palm oil after Egypt’s 588,957 MT. In fact, it has surpassed the import value recorded for the country in 2008. Due to this development, UAE’s position as the largest importer of Malaysian palm oil in the region west of Asia has been overtaken by Iran.

Despite the global economic downturn and fluctuation in global commodities prices during this period, export of palm oil to Malaysia’s top five importing countries in the region has shown better improvement, except for UAE. Besides Iran, positive growth has been seen in exports to Oman, Saudi Arabia and Yemen. Our exports to these three countries in the January-November 2009 period exceeded their total import of Malaysian palm oil recorded in 2008, especially in Saudi Arabia and Iran (Table 1).

After many years of dominating the biggest share and playing a significant role in the oils and fats market of West Asia and the Middle East, UAE has been hit hard by the global economic crisis. The economic growth of the Emirates has been affected and caused a great impact on its business environment. The financial crisis and debt in UAE could prolong its economic recovery, leading to slower business activities and lower demand – and eventually affect many industries in the country, including its oils and fats industry.

The UAE is a major trading partner for Iran, with trade dominated by UAE exports to Iran. The bulk of merchandise supplied to Iran by UAE is products imported into UAE from foreign markets and repackaged for shipment to Iran. Iran represents about 14% of UAE’s total exports, including re-exports. About 86% of UAE’s import of palm oil is for re-export, with Iran being one of the major re-export destinations.

However, the rising cost of re-exporting the commodity has prompted most companies to look for alternatives, including shipping the cargo directly to the final destinations. Previously, most of the companies, including those run by the Iranians, would ship their cargo into UAE for storage in warehouses and

repackaging before being shipped to the final destinations. The world’s shipping freight rates have gone down but the rates in UAE remain the same. Therefore, some analysts suggested the cheaper mode of shipping palm oil directly from Malaysia to the Middle East destinations, since this will save the cost of storage.

Iran is rich in natural resources, and its economy is highly dependent on the production and export of crude oil to finance government spending. Although Iran has vast petroleum reserves to meet the world’s energy needs, it lacks edible oils and fats supplies to meet local consumption. Moreover, as the most populous country in the Middle East with a population exceeding 73 million, Iran’s

A MONTH ago, I was expecting an uptrend correction if the price of Palm Oil futures in Bursa Malaysia (FCPO) stays below RM2,520 per metric tonne, but the uptrend persisted and went above RM2,520. I have mentioned that if the price breaks above RM2,520, it shall rally and test the next resistance level at RM2,650. The price of FCPO went as high as RM2,726 and settled at RM2,702 when this article was written – and it seems like the bulls are charging,

The rise in the price of crude palm oil was primarily because of increasing demand in the past few weeks and the US dollar has started to weaken again. The crude oil price rally also helps boost the price of FCPO. Furthermore, demand of oil is expected to continue as most countries face the worst winter in decades.

In mid-December, renowned analyst Dorab Mistry was bullish and expected price to rise to RM2,800 in the short term and to remain bullish for the year 2010 as major replanting exercise cuts palm oil output. This was said at his presentation at the Malaysia-India Palm Oil Trade Fair and Seminar (POTS). I was also a speaker there and although I expected an immediate technical correction, I also expressed that if the RM2,600 resistance level is broken, price may rally to RM2,800. The price went above RM2,600 a few days after the event.

The rainy weather in December may affect the output of crude palm oil in Malaysia and Indonesia. Supply may not be able to meet demand, especially in China, where palm oil usage is expected to rise because of the extreme cold weather and the coming Chinese New Year in mid-February.

The FCPO price trend is still strong upwards, being supported by the short term 30-day moving average. The short to long term moving averages continue to rise. The price tested the 30-day moving average on Dec 23 and rebounded to rally to the current level. The 30-day moving average is currently at RM2,550. The medium and long term 60- and

90-day moving averages are between RM2,300 and RM2,400, with the price currently at RM2,702.

The momentum has started to favour the bulls again after being weak in the month of November. RSI and Momentum indicators started to make new pivot highs again and are above the middle level. The MACD indicator recently went above its moving average. Trading volume has weakened from a daily average of 8,700 contracts to an average of 7,600 contracts now, but this is probably because of the holiday month of December.

With the strong bullish momentum in the uptrend, the price of FCPO may extend its bullish trend to the resistance level at RM2,800 before we see any significant correction. Any short term pullback may be an opportunity to buy until price reaches this resistance level. The short term support level is currently at RM2,600, based on the short term moving average which is also the previous immediate resistance level. In the longer term, FCPO has a price target of RM3,100 based on a 5-month triangle pattern that was confirmed in early November.

MARKETWatchWby Benny LeeChief Market StrategistNextView Group

Mr. Benny Lee is a private trader, trainer and sought-after speaker in the financial market. He is the Chief Market Strategist for NextView Group. NextView Group is a group of companies in the Asian region that provides a leading real-time investment tool for both professional and retail investors.

NextView is also a leading Investor Education training provider. For

more information, log on to www.nextview.com.

The above analysis and commentary is based on the writer’s personal opinion towards the price of crude palm oil using technical analysis and should not be construed as any form of investment advice. The writer will not be responsible for any decision made from using the above article.

MPOC FORTUNE • 3

Palm Oil Prices May Extend Bullish Trend

FCPO daily chart as at 6 January 2010. Charted by Benny Lee using NextView Advisor Professional

North Port, Port Klang

- Fima Bulking Services Berhad

- Fimachem Sdn Bhd

- Fima Liquid Bulking Sdn Bhd

- Fima Freight Forwarders Sdn Bhd

Butterworth

- Fima Palmbulk Services Sdn Bhd

Jalan Parang, 2nd Extension, North Port, 42000 Port Klang, Selangor, MALAYSIA Tel: +603 - 3176 7211 Fax: +603 - 3176 5641 Email: [email protected]

http://www.fimabulking.com

Located in a free commercial zone offer excellent opportunities for• Import and export• Transhipment• MDEX tender (approved

delivery point)• Regional collection / distribution hub

Facilities available : • Carbonsteel• Coated & stainless tanks come

with heating facilities & nitrogen blanketing.

Malaysia’s Largest Independent Common-user Multi-purpose Liquid

Bulk Terminal Operator

MPOC FORTUNE • 5

MARKETInsightsIns gAS 2009 draws to a close, the question of the lips of everyone in the edible oils trade in India is, “How happy is the year 2010 going to be for the people involved in the trade, in one way or another?” An analysis of what transpired during the past 12 months is necessary to get a glimpse of the way forward.

The oil year 2008-09 witnessed a phenomenal jump in imports of all vegetable oils, a development not seen since imports were opened up in 1994.

As can be seen from the table above, imports have been increasing gradually since 2005-06, peaking in 2008-09 at 8.66 MMT, a jump of 2.35 MMT (or a whopping 37%) over the previous year. The trade has tried to explain this sharp increase but there is really no single, credible reason for this. Among the reasons put forward have been:

• Increase in consumption resulting from higher incomes;

• High degree of price elasticity: lower average prices, specially for imported palm oil that boosted consumption;

• Government of India schemes, such as mid-day meals, subsidised oil through PDS and various unemployment schemes boosting demand; and

• Depreciation of the US dollar against the Indian rupee by about 5% further made oils more affordable.

Of course, India’s increased import of edible oils has resulted in the usual hue and cry about its negative impact on domestic production, resulting in calls for measures to curb imports through a review of the import tariff regime. In light of rising inflation rates, this may not find favour with the policy makers.

Import of Refined vs. Crude Edible OilsAnother aspect of imports during 2008-09 has been a shift in the ratio of imports of refined oils to crude vegetable oils. Imports of refined oils, principally RBD

Palm Olein, has increased sharply from 126,000 MT in 2006-07 to 1.24 MMT in 2008-09. This can be attributed directly to lower international prices coupled with lower import duties. The inability of the domestic processing industry to absorb the entire production of stearin from the fractionation of CPO and high local

refining costs have been other reasons for the higher imports of RBD Palm Olein.

As can be seen, imports of refined oils accounted for 15% of the total imported oils in 2008-09.

Import of Palm and Soft Oils The lower import duties seemed to have worked in favour of palm oils. In percentage terms, palm oil imports may have fallen from 86% in the previous year to 80% in the edible oils import basket for

2008-09. However, in absolute quantities, palm oil imports have increased by 1.7 million MT compared with an increase of 0.8 million MT in imports of other soft oils.

The tables below reflect the growing trend in favour of palm oils over the past few years.

Prospects for 2009-10Though it is difficult to imagine a repeat performance of a 37% growth in imports, it is a foregone conclusion that, barring intervention, imports in 2009-10 should continue to see an increase. Stability in international prices, combined with lower forecast prospects for the upcoming kharif crop, lends credence to this possibility. A 7% fall is expected in oil production in the next kharif season, from 5.4 MMT to 5 MMT. This does not bode well for domestic edible oils production for 2009-10.

India’s heavy reliance on imports is set to continue. This signals a happy new year for international traders in vegetable oils. Indian industry and consumers should also benefit from the availability of imported oils at international prices. If international prices were to rise, it will also signal a happy new year for Indian farmers in terms of better returns from their crops.

It seems like it will be a good year for all in 2010, except probably the policy makers who have the challenging task of striking a balance between the interests of the consumers and the farmers. Bhavna

India,The Challenges Continues

Imports of Vegetable Oils (2004-05 to 2008-09) – In Million Metric Tonnes

A NEW brand image is being initiated to give Malaysian Palm Oil an even greater boost in the global edible oils and fats market. Though voluntary, as the scheme now is, it will provide the “green” product assurance across the supply chain, from cultivation to end consumers and derived products.

This was revealed by Malaysian Palm Oil Council (MPOC) Chief Executive Officer Tan Sri Dr Yusof Basiron at the Palm Oil Trade Seminar (POTS) sessions in Bangladesh and India this month.

This green product, to be called MALAYSIAPALM, will be backed by research and development from the Malaysian Palm Oil Board (MPOB), and the MALAYSIAPALM Brand Scheme will be open to growers, millers, refiners and traders who are keen to participate.

Pointing out the huge global demand for palm oil as food as well as a biofuel source, Tan Sri Dr Yusof said Malaysian palm oil, which has been endorsed by the Roundtable on Sustainable Palm Oil (RSPO), also boasts a proven track

record of good business practices and ethics in trade.

This has put Malaysia in its leading position as a reliable supplier of consistent quality palm oil products, a good image that will help MALAYSIAPALM to be differentiated as a quality brand and fetch a higher value. This was also why, he added, Malaysian palm oil plantations have been hardly affected by the anti-palm oil lobby that pushes issues of deforestation and the killing of wildlife such as the orang utan.

Major buyers like China, India and the countries in the Middle East, and increasingly, the United States, choose Malaysian palm oil because of its long history of cultivation and therefore, quality assurance through good agricultural and production practices that have been certified by RSPO.

On its part, Tan Sri Dr Yusof said, the Government of Malaysia was enforcing, as well as expediting, the production of sustainable palm oil in the country to ensure the industry meets the growing

global demand, as well as to create a higher value for Malaysian palm-based products.

Malaysian palm oil companies were already trapping methane to lower greenhouse gas (GHG) emissions. MPOB was doing more research into other forms of biomass usage to further increase GHG emission savings, all of which will defuse tactics of the anti-palm oil lobby to disfavour the use of palm oil in biofuel, and put Malaysian palm oil in a better position to meet European Union and US requirements for biofuel production in their countries.

As for Bangladesh in particular, Tan Sri Dr Yusof said the import of Malaysian palm oil by the country has been declining, from close to 450,000 metric tonnes (MT) in 2006 to 150,000 MT in 2007; 270,000 MT in 2008 and a mere 50,000 MT between January and October 2009.

This declining trend was worrying because Malaysia values Bangladesh as an important and favoured partner in the palm oil trade. The country requires 1.4

Boosting Malaysia’s Oil PalmExports with MALAYSIAPALM

MPOC FORTUNE • 7

million MT of oils and fats annually to meet domestic demand and he noted that Bangladesh had to import 88% of this demand.

He cautioned that demand for edible oils and fats all over the world was increasing rapidly, with global consumption increasing by 4 to 6 million MT a year. Malaysia was among only seven countries in the world that were major net exporters of edible oils and fats – which meant that Bangladesh would have to compete with the rest of the world for its supplies.

Another presenter at both the POTS sessions, MPOB Director Kalanithi Nesaretnam, said the many years of food and nutritional research put into palm oil have brought about beneficial results and today palm oil enjoys the position of being a superior, functional and nutritive oil.

MPOB-funded research findings on palm oil have been published on 218 occasions in 12 journals around the world, among them the American Journal of Clinical Nutrition, the United Nations Univ Food & Nutrition Bulletin, Asia Pacific Journal of Clinical Nutrition and the International Journal of Food Sciences and Nutrition.

With 85% of the world’s palm oil production used as food, Kalanithi said, the already established facts about palm oil are that it provides a concentrated source of calories, the essential fatty acids the body requires; it is a carrier for fat soluble vitamins such as A, D, E and K; and the oil enhances the palatability and satiety of food.

Today, MPOB has introduced innovative healthy oil products that include high oleic oils, lower saturated palm olein and high diglyceride palm oil products that are also

highly versatile. The chemical composition of palm oil suits most food product formulations.

The oil also has a very wide range of product derivatives and as far as nutritive value is concerned, palm oil is rich in antioxidants such as tocopherol, tocotrienol and carotenoids. All of these qualities have enabled the successful use of palm oil and its derivatives in the manufacture of many food products, including palm-based cheese, trans-free margarines, butter oil substitutes, animal fat replacers and shortening.

The usage of the oil in food is set to expand even further, Kalanithi said, especially in the EU and the US, once labelling of food and food products in relation to trans fats becomes compulsory. Palm oil is a nutritious oil that does not contain trans fatty acids, and neither is it genetically modified.

Meanwhile, Associate Professor Dr Pramod Khosla of the Department of Nutrition & Food Science at the Wayne State University in Detroit, Michigan,

USA, presented research and laboratory test results to prove the nutritional benefits of palm oil over other edible oils.

In his paper on Nutritional Benefits of Palm Oil, Dr Khosla said palm oil and its products serve a multitude of nutritional needs. Besides being free of trans fat, adequate supply made palm oil the most important player for edible oils on the global stage.

The natural fatty acid profile of palm oil eliminates the need for hydrogenation, which is vital for trans fat-free formulations. This has led to a vast array of manufacturers and food producers in the United States to use palm oil blended with other oils.

In the United States, he said, there are today in the market numerous popular brands of zero-trans fat margarines, shortening, baking margarines, doughnut fry oils, butter, butter blend, bakers’ margarine, cake and icing shortening and other frying oils and shortening that use palm oil. ED

These presentations were made at the POTS sessions in Dhaka, Bangladesh, on Dec 12, 2009, and in New Delhi, India, on Dec 15, 2009. To learn more about the leading global role Malaysian Palm Oil is playing today, go to the MPOC website at www.mpoc.org.my

700

600

500

400

300

200

100

2006

2007

2008

0

'000

MT

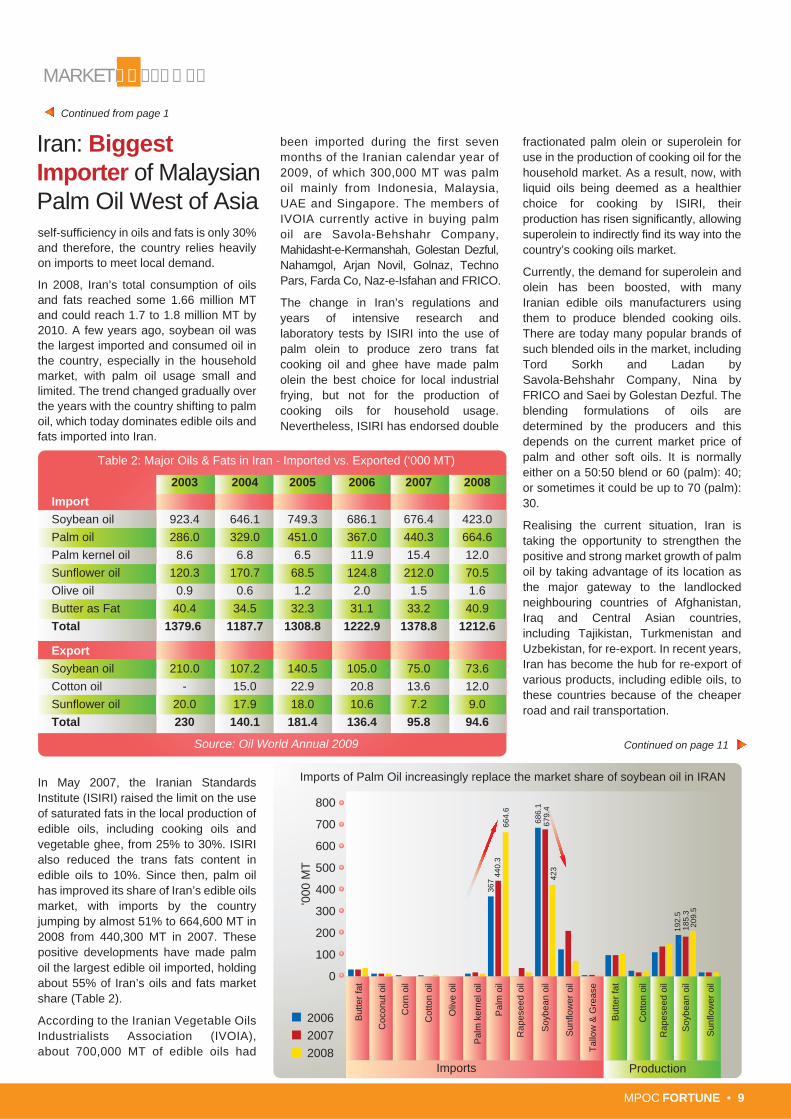

self-sufficiency in oils and fats is only 30% and therefore, the country relies heavily on imports to meet local demand.

In 2008, Iran’s total consumption of oils and fats reached some 1.66 million MT and could reach 1.7 to 1.8 million MT by 2010. A few years ago, soybean oil was the largest imported and consumed oil in the country, especially in the household market, with palm oil usage small and limited. The trend changed gradually over the years with the country shifting to palm oil, which today dominates edible oils and fats imported into Iran.

In May 2007, the Iranian Standards Institute (ISIRI) raised the limit on the use of saturated fats in the local production of edible oils, including cooking oils and vegetable ghee, from 25% to 30%. ISIRI also reduced the trans fats content in edible oils to 10%. Since then, palm oil has improved its share of Iran’s edible oils market, with imports by the country jumping by almost 51% to 664,600 MT in 2008 from 440,300 MT in 2007. These positive developments have made palm oil the largest edible oil imported, holding about 55% of Iran’s oils and fats market share (Table 2).

According to the Iranian Vegetable Oils Industrialists Association (IVOIA), about 700,000 MT of edible oils had

been imported during the first seven months of the Iranian calendar year of 2009, of which 300,000 MT was palm oil mainly from Indonesia, Malaysia, UAE and Singapore. The members of IVOIA currently active in buying palm oil are Savola-Behshahr Company, Mahidasht-e-Kermanshah, Golestan Dezful, Nahamgol, Arjan Novil, Golnaz, Techno Pars, Farda Co, Naz-e-Isfahan and FRICO.

The change in Iran’s regulations and years of intensive research and laboratory tests by ISIRI into the use of palm olein to produce zero trans fat cooking oil and ghee have made palm olein the best choice for local industrial frying, but not for the production of cooking oils for household usage. Nevertheless, ISIRI has endorsed double

fractionated palm olein or superolein for use in the production of cooking oil for the household market. As a result, now, with liquid oils being deemed as a healthier choice for cooking by ISIRI, their production has risen significantly, allowing superolein to indirectly find its way into the country’s cooking oils market.

Currently, the demand for superolein and olein has been boosted, with many Iranian edible oils manufacturers using them to produce blended cooking oils. There are today many popular brands of such blended oils in the market, including Tord Sorkh and Ladan by Savola-Behshahr Company, Nina by FRICO and Saei by Golestan Dezful. The blending formulations of oils are determined by the producers and this depends on the current market price of palm and other soft oils. It is normally either on a 50:50 blend or 60 (palm): 40; or sometimes it could be up to 70 (palm): 30.

Realising the current situation, Iran is taking the opportunity to strengthen the positive and strong market growth of palm oil by taking advantage of its location as the major gateway to the landlocked neighbouring countries of Afghanistan, Iraq and Central Asian countries, including Tajikistan, Turkmenistan and Uzbekistan, for re-export. In recent years, Iran has become the hub for re-export of various products, including edible oils, to these countries because of the cheaper road and rail transportation.

MARKETInsightsIns gContinued from page 1

Table 2: Major Oils & Fats in Iran - Imported vs. Exported (‘000 MT)

2003 2004 2005 2006 2007 2008

Import

Soybean oil 923.4 646.1 749.3 686.1 676.4 423.0

Palm oil 286.0 329.0 451.0 367.0 440.3 664.6

Palm kernel oil 8.6 6.8 6.5 11.9 15.4 12.0

Sunflower oil 120.3 170.7 68.5 124.8 212.0 70.5

Olive oil 0.9 0.6 1.2 2.0 1.5 1.6

Butter as Fat 40.4 34.5 32.3 31.1 33.2 40.9

Total 1379.6 1187.7 1308.8 1222.9 1378.8 1212.6

Export

Soybean oil 210.0 107.2 140.5 105.0 75.0 73.6

Cotton oil - 15.0 22.9 20.8 13.6 12.0

Sunflower oil 20.0 17.9 18.0 10.6 7.2 9.0

Total 230 140.1 181.4 136.4 95.8 94.6

Source: Oil World Annual 2009

Imports of Palm Oil increasingly replace the market share of soybean oil in IRAN

800

But

ter

fat

Coc

onut

oil

Cor

n oi

l

Cot

ton

oil

Cot

ton

oil

Oliv

e oi

l

Pal

m k

erne

l oil

Pal

m o

il

Rap

esee

d oi

l

Rap

esee

d oi

l

Soy

bean

oil

Soy

bean

oil

Sun

flow

er o

il

Sun

flow

er o

il

Tal

low

& G

reas

e

But

ter

fat

Imports Production

367

440.

366

4.6

423

686.

1

192.

518

5.3

209.

5

679.

4

Continued on page 11

MPOC FORTUNE • 9

Iran: Biggest Importer of MalaysianPalm Oil West of Asia

We highlight a positive approach from the Malaysian Government that could potentially benefit the Malaysian palm oil industry. If you are keen to improve your sustainability index and produce palm oil with an overall lower carbon footprint, this could be the opportunity.

You need to look no further than the link below:

Website:

Malaysia Energy Centre: http://www.ptm.org.my

Green Technology Financing Scheme: http://www.gtfs.my

Hotline: Green Technology Financing Scheme: 1-800-88-4837

To promote green technology, the Government will establish a fund amounting to RM1.5 billion. This fund will provide soft loans to companies that supply and utilise green technology. For suppliers, the maximum financing is RM50 million and for consumer companies RM10 million. The Government will bear 2% of the total interest rate. In addition, the Government will provide a guarantee of 60% on the financing amount, with the remaining 40% by banking institutions. Loan applications can be made through the National Green Technology Centre. This scheme will commence on 1 January 2010 and is expected to benefit 140 companies…

Green Technology Funding Available From the Malaysian Government!

“

”

CONTRACTS & ARBITRATION WORKSHOP 9 – 10 April 2009

Grand Dorsett Subang Hotel

The Palm Oil Refiners Association of Malaysia (PORAM) 801C/802A, Block B Executive Suites, Kelana Business Centre, 97, Jalan SS7/2, 47301 Kelana Jaya, Selangor, Malaysia. Tel: 603-7492 0006 Fax: 603-7492 0128 E-mail : [email protected]

Contact: Susila / Liza / Krish

About the workshop

This 2 day workshop is designed to provide fundamental understanding of contracts, performance and enforcement of contracts and the practice of dispute resolution in the palm oil industry. The workshop will cover topics:-

Understanding the Contract Terms & Clauses Charter Party Contract Terms Related to Surveying Common Disputes in the Sales & Carriage of Palm Oil

Trade Trade Dispute Solving Mechanisms PORAM Rules of Arbitration and Appeal Case Studies Note: Contract & Arbitration Workshop syllabus can be downloaded

from www.poram.org.my

This workshop is beneficial for all oil/fats personnel who are directly or indirectly involved with contracts. It is particularly tailored for traders, marketing executives, operations managers and executives, procurement officers, contract & legal department personnel and individuals wishing to familiarise themselves with the arbitration process and to receive training as arbitrators.

Continued from page 9

MPOC FORTUNE • 11

Facing challenges in trading with the Western countries, Iran has sought to strengthen ties with Asian countries. Several countries in Central Asia have declared their interest in boosting economic engagement with Iran, including Tajikistan. Iran, Turkey and Azerbaijan have held discussions on building a joint railway through the three countries in order to enhance relations, trade and travel. Iran also has pursued increased integration with its neighbours in the Middle East. Merchandise trade with the Middle East has grown, for even if Arab nations may be weary of Iran’s nuclear ambitions, they value trade and investment relations with the country.

Many are hoping that positive economic engagement with Iran will mitigate international tensions over Iran’s nuclear ambitions.

Due to the political and financial pressures on Iran’s government from many parties, the business class has particularly been hit by the international sanctions. Iranian companies reportedly have great difficulty opening bank accounts abroad and getting banks to honour Letters of Credit. Subsequently, some Iranian businesses have had to shift to other regional banks or to other countries not susceptible to international sanctions and engage in cash-based transactions as well.

Despite all these obstacles, Iran is still continuing and increasing its intake of palm oil from Malaysia. For that reason, Malaysian exporters need to ensure an active and sustainable presence in the Iran’s edible oils market and establish strong relationships with major local importers of the oil.

A huge business potential awaits Malaysian investors in Iran. We should look into setting up a bulking installations at Bandar Abbas port, which would be a great advantage for both importers and exporters. In fact, local companies will buy from such a facility to avoid the hassle of importation. Some of the advantages of such a facility for buyers include saving the cost of shipping, guarantee of continuous supplies, especially during the peak periods, as well as protection from price fluctuation on commodity market.

Refinery owners in Malaysia should also consider setting up refineries or packing plants in joint ventures, which will ensure the usage of Malaysian palm oil as the main raw material for Iran’s food production. It is very crucial for Malaysia, as the world’s largest palm oil exporter, to continue strengthening its role as the major supplier of palm oil to Iran specifically, and to West Asia and the Middle East as a whole. Haznita

MARKETInsightsIns gIran: Biggest Importer of MalaysianPalm Oil West of Asia

Table 3: Imports of Edible Oils over the 1st 7 Months of the Two Consecutive Iranian Years (Current Year vs Last Year)

PRODUCT From March 21 – From March 21 – Oct 21, 2008 Oct 21, 2009 Change (%)

Weight Value Weight Value Weight Value (MT) (USD) (MT) (USD)

Total 411,955 434,276,315 688,832 573,398,883 67 32

Source: The Iranian Vegetable Oils Industrialist Association (IVOIA)Note: The Iranian calendar year usually begins within a day of March 21 of every year

Crude & RBD Oils

MPOCOffices

WorldwideMalaysian Palm Oil Council (MPOC)2nd Floor Wisma Sawit Lot 6, SS 6, Jalan Perbandaran47301 Kelana Jaya, SelangorTel: 603-7806 4097Fax: 603-7806 2272www.mpoc.org.my

American Palm Oil Council Suite # 690, 21515 Hawthorne Blvd.Torrance CA 90503, USATel: +1 (310) 944 3910Fax: +1 (310) 944 3544www.americanpalmoil.comE-mail: [email protected]: Mohd Salleh Kassim