37

June 2012 MPX CORPORATE PRESENTATION

June 2012

MPX CORPORATE PRESENTATION

The material that follows is a presentation of general background information about MPX Energia S.A. and its subsidiaries (collectively, “MPX”

or the “Company ”) as of the date of the presentation. It is information in summary form and does not purport to be complete. No

representation or warranty, express or implied, is made concerning, and no reliance should be placed on, the accuracy, fairness, orcompleteness of this information.

This presentation may contain certain forward-looking statements and information relating to MPX that reflect the current views and/orexpectations of the Company and its management with respect to its performance, business and future events. Forward looking statementsinclude, without limitation, any statement that may predict, forecast, indicate or imply future results, performance or achievements, andmay contain words like “may”, “plan”, “believe”, “anticipate”, “expect”, “envisages”, “will likely result”, or any other words or phrases of similar

meaning. Such statements are subject to a number of risks, uncertainties and assumptions. We caution you that a number of importantfactors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in thispresentation. In no event, neither the Company, any of its affiliates, directors, officers, agents or employees nor any of the placementagents shall be liable before any third party (including investors) for any investment or business decision made or action taken in reliance onthe information and statements contained in this presentation or for any consequential, special or similar damages.

This presentation does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase any securities.

Neither this presentation nor anything contained herein shall form the basis of any contract or commitment whatsoever.

Recipients of this presentation are not to construe the contents of this summary as legal, tax or investment advice and recipients shouldconsult their own advisors in this regard.

The market and competitive position data, including market forecasts, used throughout this presentation were obtained from internalsurveys, market research, publicly available information and industry publications. Although we have no reason to believe that any of thisinformation or these reports are inaccurate in any material respect, we have not independently verified the competitive position, marketshare, market size, market growth or other data provided by third parties or by industry or other publications. MPX, the placement agentsand the underwriters do not make any representation as to the accuracy of such information.

This presentation and its contents are proprietary information and may not be reproduced or otherwise disseminated in whole or in partwithout MPX’s prior written consent.

DISCLAIMER

2

MPX AT A GLANCE

1

A PROVEN RECORD OF ACHIEVEMENT

4

IPO: US$ 1.1

billion raised

1,080 MW

contracted in the

A-5 Auction

2007 First acquisition of

mining rights in

Colombia

365 MW contracted in

the A-5 Auction

Construction works at

TPP Pecém I begin

2008 Construction works

at TPPs Itaqui and

Pecém II begin

Acquisition of

interest in 7 onshore

exploratory blocks in

the Parnaíba basin

2009

MPX Colombia – 1st

Technical Report:

coal resources of

144 MM tons

License granted for

TPP Parnaiba

(1,863 MW)

Initiation of drilling

campaign in the

Parnaíba basin

2010

TPP Parnaíba licensed

capacity increased to

3,722 MW

Power supply

contracts secured for

1,193 MW and

construction works at

TPP Parnaíba begin

D&M estimates for

risked resources in

the Parnaíba basin

amount to over 11Tcf

Declaration of

commerciality for 2

gas fields with

estimated production

of 6 MM m3/day

2011 MPX/E.ON

partnership

Drawdown of bridge-

loans totaling R$ 1.6

billion for natural

gas production and

power generation in

the Parnaíba Basin

Spin-off of

Colombian coal

assets to a new

company listed at

the BM&FBOVESPA

E.ON’s acquisition of

minority interest at

MPX through a R$

1.0 billion capital

increase

2012

4

The First Five Years

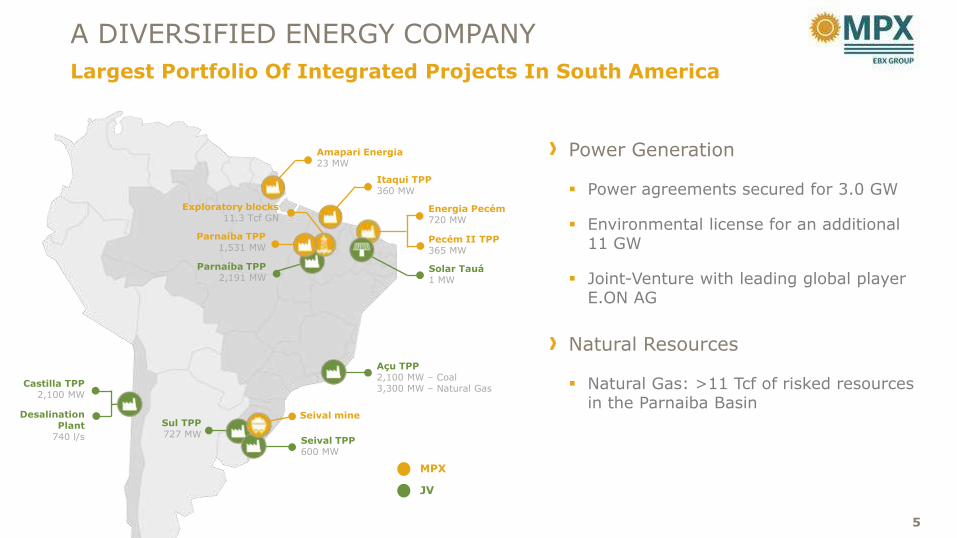

A DIVERSIFIED ENERGY COMPANY

Largest Portfolio Of Integrated Projects In South America

Açu TPP2,100 MW – Coal3,300 MW – Natural Gas

Amapari Energia23 MW

Itaqui TPP360 MW

Energia Pecém720 MW

Pecém II TPP365 MW

Solar Tauá1 MW

Parnaíba TPP1,531 MW

Exploratory blocks11.3 Tcf GN

Seival mine

Seival TPP600 MW

Sul TPP727 MW

Castilla TPP2,100 MW

Desalination Plant

740 l/s

Parnaíba TPP2,191 MW

JV

MPX

Power Generation

Power agreements secured for 3.0 GW

Environmental license for an additional 11 GW

Joint-Venture with leading global player E.ON AG

Natural Resources

Natural Gas: >11 Tcf of risked resources in the Parnaiba Basin

5

MPX OWNERSHIP STRUCTURE

6

EIKE BATISTA

Free Float

Contracted Power

Generation

Natural Resources

100% 50%

50%

Energia Pecém

(365 MW)

Pecém II

(365 MW)

Itaqui

(365 MW)

TPP Parnaíba

(1,087 MW)

Amapari

(12 MW)

Seival

OGX Maranhão

MPX- E.ON JV50/50

53.9% 11.7%34.3%

TPP Parnaíba

(1,534 MW)

Açu – Natural

Gas (3,300 MW)

Açu – Coal

(2,100 MW)

Castilla - Coal

(2,100 MW)

Sul and Seival -

Coal (1,327 MW)

Greenfield Thermal

Generation

50% 50%

50%

Supply & Trading

Renewables

New Projects

100%

(after conclusion of capital increase, assuming no subscription by minority shareholders)

EXPERIENCED MANAGEMENT TEAM TO EXECUTE ON

STRATEGIC VISION

Partner at Villemor Amaral Advogados (2002-2004) and Tozzini, Freire & Silva Advogados (2001-2002)

General Counsel at MMX Mineração e Metálicos S.A.

Legal Director at General Motors Corp. in Lisbon and Delphi Automotive Systems

Marcus Bernd TemkeCOO

Over 20 years of experience in operations at multinational corporations

COO at Rio Polímeros S.A.

Holds an MBA from COPPEAD-UFRJ

Over 25 years of experience in the financial area at multinational corporations

CFO at MMX Mineração e Metálicos S.A.

CFO at Unisys in Brazil and Germany

Eduardo KarrerCEO & IRO

Over 22 years of experience in a wide range of M&A and corporate finance transactions related to the natural

resources, electricity, sanitation and logistics sectors

CEO at El Paso Brasil Ltda.and Rio Polímeros S.A..

Executive manager for the Gas&Energy and International Markets divisions at Petrobrás

Rudolph IhnsCFO

Xisto Vieira FilhoOfficer for Regulatory Affairs & Commercialization

Former National Secretary for Energy

Coordinator of the Subcommittees for Electricity Studies of the Interconnected System and Secretary of National

Energy Policy Committee of Brazil

Chairman of the Board of Directors of CHESF and Eletrosul and Board member of Eletrobrás, Furnas, Cepel and

Grupo Rede

Former president of the National Committee of Cigré (Conference Internationale des Grand Réseaux Électriques)

Bruno ChevalierGeneral Counsel

7

INVESTMENT CONSIDERATIONS

2

Exposure to Brazil’s growing energy demand

Tax-advantaged thermal power plants coming on-line in 2012

Attractive monetization of natural gas resources

Robust pipeline of thermal projects to meet Brazil’s need for a more reliable

electric system

Joint-venture with E.ON to develop strong portfolio of energy assets while

unlocking value of Colombian coal assets

Experienced management team to execute on strategic vision

INVESTMENT CONSIDERATIONS

9

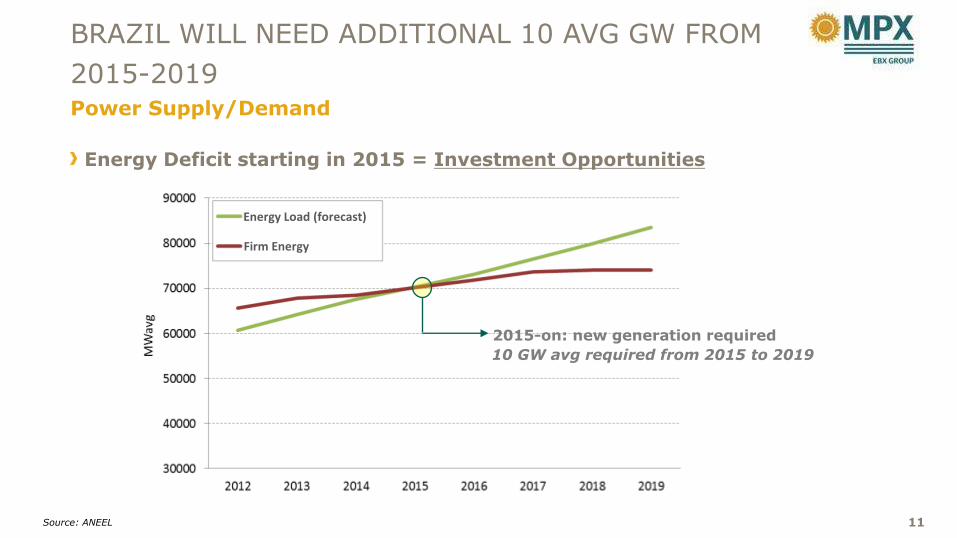

EXPOSURE TO BRAZIL’S GROWING ENERGY DEMAND

3

Energy Deficit starting in 2015 = Investment Opportunities

BRAZIL WILL NEED ADDITIONAL 10 AVG GW FROM

2015-2019Power Supply/Demand

Source: ANEEL 11

2015-on: new generation required

10 GW avg required from 2015 to 2019

Firm Energy

Energy Load (forecast)

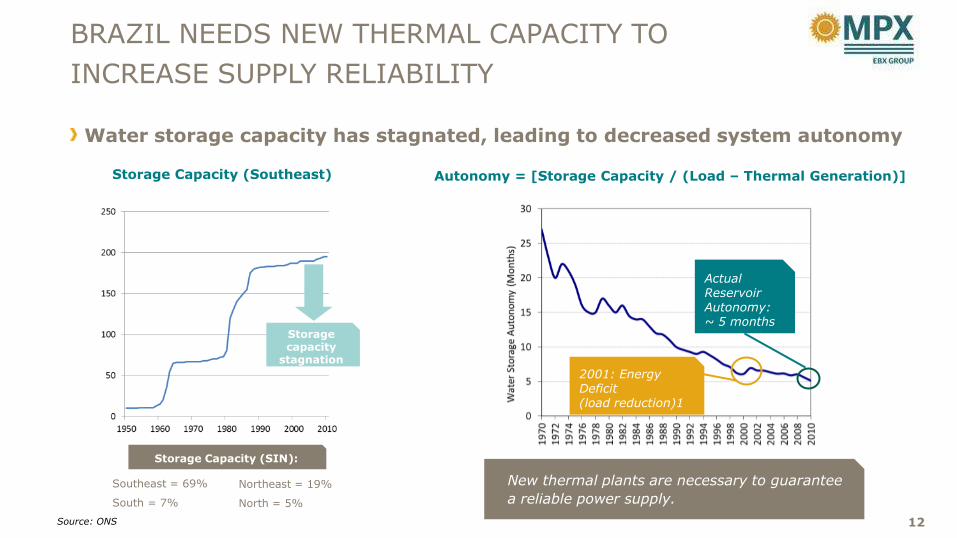

Water storage capacity has stagnated, leading to decreased system autonomy

BRAZIL NEEDS NEW THERMAL CAPACITY TO

INCREASE SUPPLY RELIABILITY

12Source: ONS

Storage Capacity (Southeast)

Storage Capacity (SIN):

Autonomy = [Storage Capacity / (Load – Thermal Generation)]

New thermal plants are necessary to guarantee

a reliable power supply.Northeast = 19%

North = 5%

Storage capacity

stagnation

Southeast = 69%

South = 7%

2001: Energy Deficit(load reduction)1

Actual Reservoir Autonomy: ~ 5 months

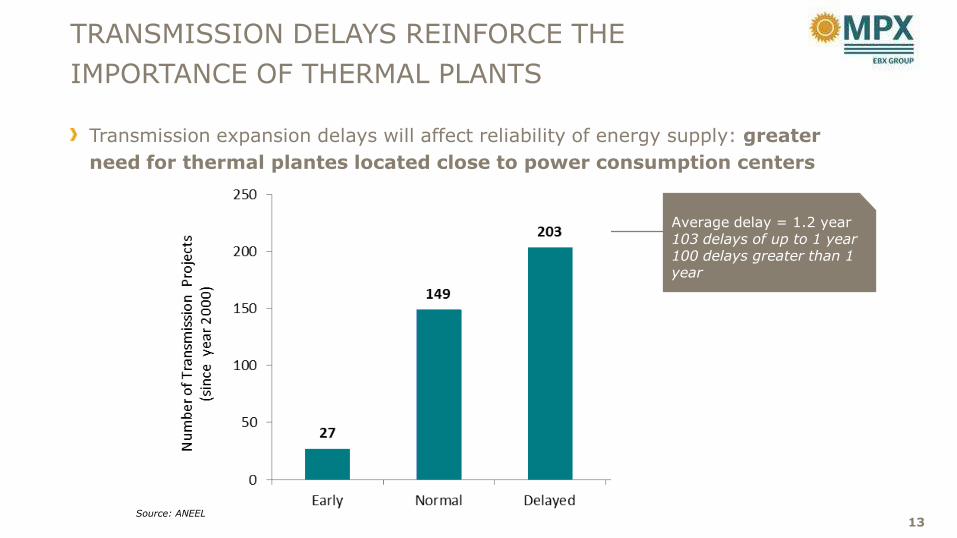

Transmission expansion delays will affect reliability of energy supply: greater

need for thermal plantes located close to power consumption centers

TRANSMISSION DELAYS REINFORCE THE

IMPORTANCE OF THERMAL PLANTS

13Source: ANEEL

Average delay = 1.2 year103 delays of up to 1 year100 delays greater than 1 year

TAX-ADVANTAGED THERMAL POWER PLANTS COMING ON-LINE STARTING IN 2012

4

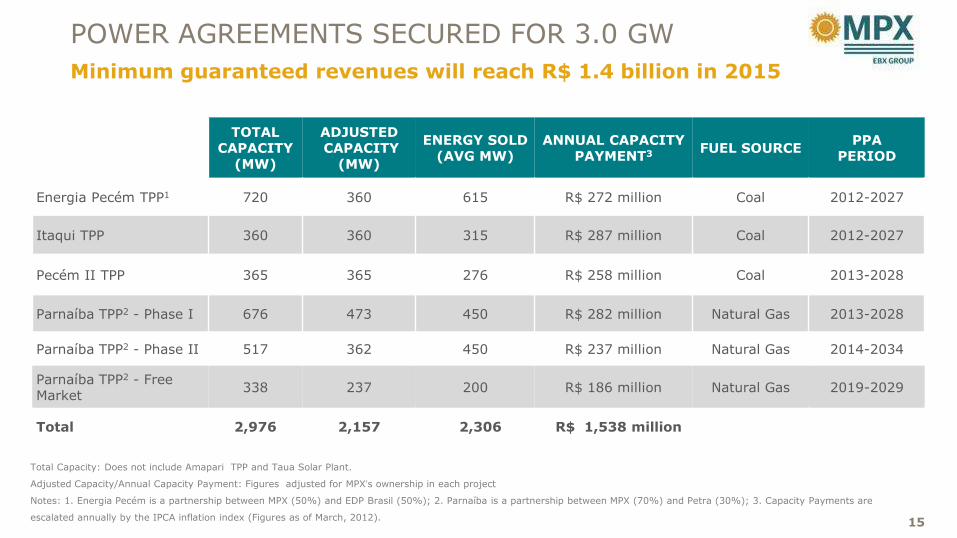

POWER AGREEMENTS SECURED FOR 3.0 GW

Minimum guaranteed revenues will reach R$ 1.4 billion in 2015

15

TOTAL CAPACITY

(MW)

ADJUSTEDCAPACITY

(MW)

ENERGY SOLD (AVG MW)

ANNUAL CAPACITY PAYMENT3 FUEL SOURCE

PPA PERIOD

Energia Pecém TPP1 720 360 615 R$ 272 million Coal 2012-2027

Itaqui TPP 360 360 315 R$ 287 million Coal 2012-2027

Pecém II TPP 365 365 276 R$ 258 million Coal 2013-2028

Parnaíba TPP2 - Phase I 676 473 450 R$ 282 million Natural Gas 2013-2028

Parnaíba TPP2 - Phase II 517 362 450 R$ 237 million Natural Gas 2014-2034

Parnaíba TPP2 - Free Market

338 237 200 R$ 186 million Natural Gas 2019-2029

Total 2,976 2,157 2,306 R$ 1,538 million

Total Capacity: Does not include Amapari TPP and Taua Solar Plant.

Adjusted Capacity/Annual Capacity Payment: Figures adjusted for MPX’s ownership in each project

Notes: 1. Energia Pecém is a partnership between MPX (50%) and EDP Brasil (50%); 2. Parnaíba is a partnership between MPX (70%) and Petra (30%); 3. Capacity Payments are

escalated annually by the IPCA inflation index (Figures as of March, 2012).

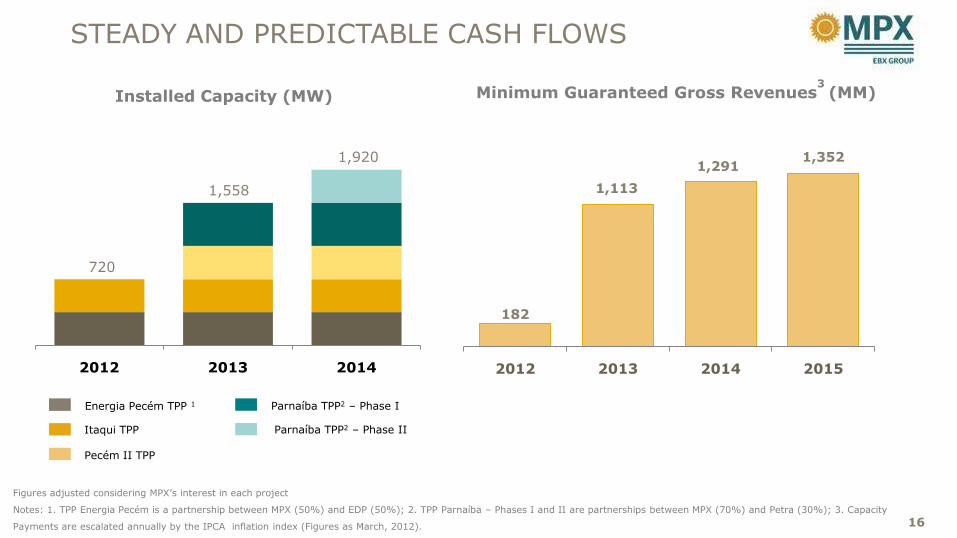

STEADY AND PREDICTABLE CASH FLOWS

16

Minimum Guaranteed Gross Revenues3

(MM)Installed Capacity (MW)

720

1,558

1,920

2012 2013 2014

Energia Pecém TPP 1

Itaqui TPP

Pecém II TPP

Parnaíba TPP2 – Phase I

Parnaíba TPP2 – Phase II

Figures adjusted considering MPX’s interest in each project

Notes: 1. TPP Energia Pecém is a partnership between MPX (50%) and EDP (50%); 2. TPP Parnaíba – Phases I and II are partnerships between MPX (70%) and Petra (30%); 3. Capacity

Payments are escalated annually by the IPCA inflation index (Figures as March, 2012).

182

1,113

1,2911,352

2012 2013 2014 2015

ENERGIA PECÉM TPP (720 MW)

Execution highlights

The plant is in the commissioning

phase

Coal conveyor belt already in

operation

Next steps:

Steam to turbine and Turbine no

load test

Synchronization and load tests

Commercial Operation

Estimated Remaining Capex until

completion*: R$ 199 million

17Energia Pecém is a partnership between MPX (50%) and EDP Brasil (50%)

* From April 2012

ITAQUI TPP (360 MW)

Execution highlights

Currently in hot commissioning

stage. First firing of the boiler has

been carried out

Turbine assembly completed

FGD (Flue Gas Desulfurization):

electrical and instrumentation tests

completed

Estimated Remaining Capex until

completion*: R$ 291 million

18* From April 2012

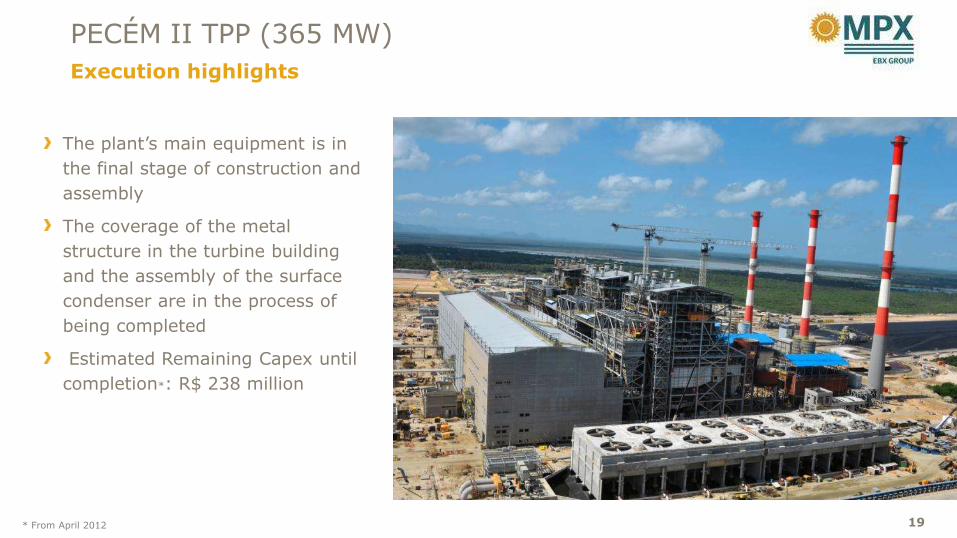

PECÉM II TPP (365 MW)

Execution highlights

The plant’s main equipment is in

the final stage of construction and

assembly

The coverage of the metal

structure in the turbine building

and the assembly of the surface

condenser are in the process of

being completed

Estimated Remaining Capex until

completion*: R$ 238 million

19* From April 2012

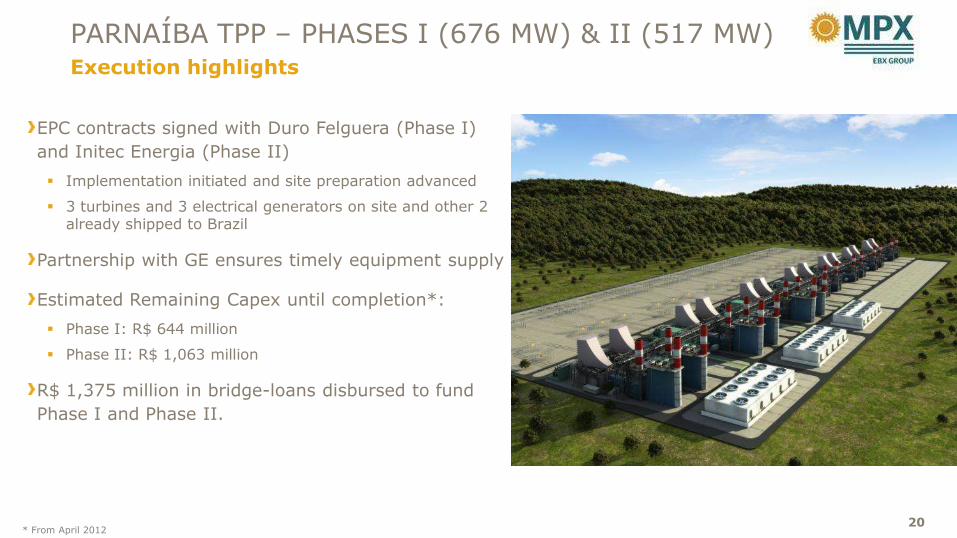

PARNAÍBA TPP – PHASES I (676 MW) & II (517 MW)Execution highlights

EPC contracts signed with Duro Felguera (Phase I)

and Initec Energia (Phase II)

Implementation initiated and site preparation advanced

3 turbines and 3 electrical generators on site and other 2 already shipped to Brazil

Partnership with GE ensures timely equipment supply

Estimated Remaining Capex until completion*:

Phase I: R$ 644 million

Phase II: R$ 1,063 million

R$ 1,375 million in bridge-loans disbursed to fund

Phase I and Phase II.

20* From April 2012

ATTRACTIVE MONETIZATION OF NATURAL GAS RESOURCES

5

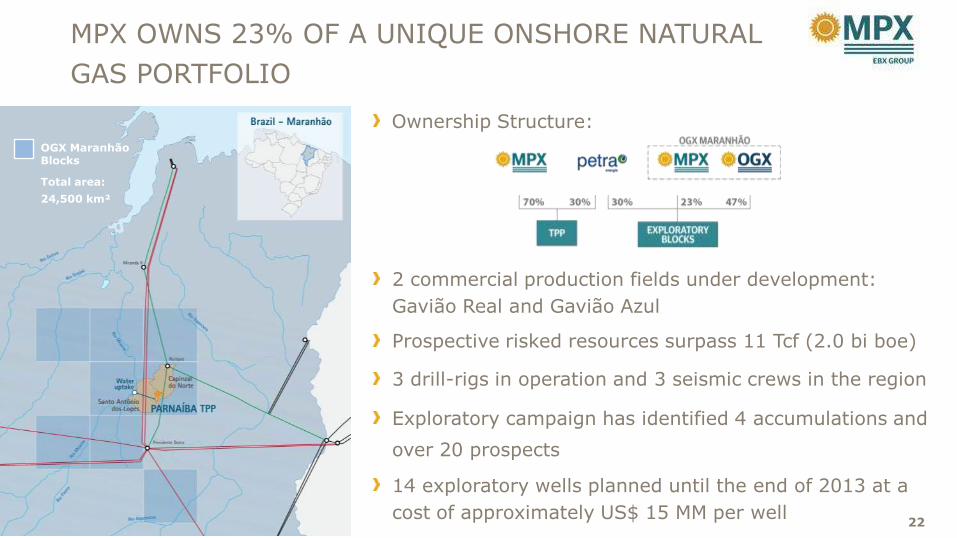

MPX OWNS 23% OF A UNIQUE ONSHORE NATURAL

GAS PORTFOLIO

Ownership Structure:

2 commercial production fields under development:

Gavião Real and Gavião Azul

Prospective risked resources surpass 11 Tcf (2.0 bi boe)

3 drill-rigs in operation and 3 seismic crews in the region

Exploratory campaign has identified 4 accumulations and

over 20 prospects

14 exploratory wells planned until the end of 2013 at a

cost of approximately US$ 15 MM per well 22

OGX MaranhãoBlocks

Total area:

24,500 km²

On schedule to start production at Gavião

Real and Gavião Azul in 2H2012

Estimated capacity in 2013: 6 MM m³/day (212 MM ft³)

6 development wells concluded and 2 in progress

Construction of Gas Treatment Unit initiated (EPC by Valerus-Geogas)

Competitive costs:

Estimated capex: US$ 450 MM

Maintenance capex: < US$ 1.0 MM/year

Average operating cost: US$ 0.30/1,000ft³

R$ 600 million bridge-loan to fund

production development disbursed in

January 2012

GAS PRODUCTION IS PLANNED TO START IN 2H12

Initial production of 6 MM m3/day will supply TPP Parnaíba– Phases I & II

23

Thermal power plant located at <

2km from gas fields

2.2 GW licensed and still uncontractedcould demand further 11 MM m3/day

Inexpensive connection to the electrical grid

Limited competition in natural gas

Tax-advantaged region can attract

industrial investments with gas is

available

ATTRACTIVE OPPORTUNITIES TO MONETIZE

ADDITIONAL PRODUCTION

Efficient Integration of Natural Gas Resources with Energy Production

24

JOINT-VENTURE WITH E.ON TO DEVELOP ROBUST PIPELINE OF THERMAL PROJECTS

6

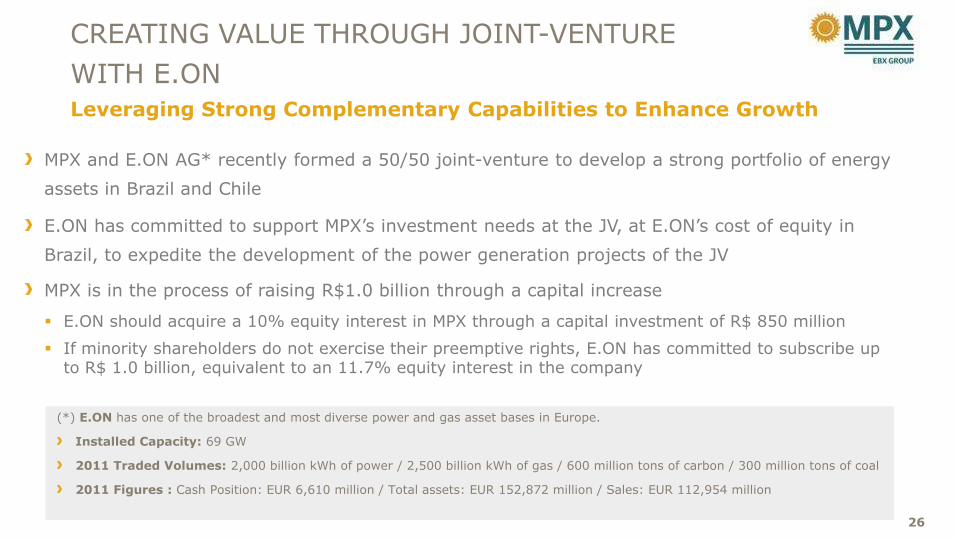

MPX and E.ON AG* recently formed a 50/50 joint-venture to develop a strong portfolio of energy

assets in Brazil and Chile

E.ON has committed to support MPX’s investment needs at the JV, at E.ON’s cost of equity in

Brazil, to expedite the development of the power generation projects of the JV

MPX is in the process of raising R$1.0 billion through a capital increase

E.ON should acquire a 10% equity interest in MPX through a capital investment of R$ 850 million

If minority shareholders do not exercise their preemptive rights, E.ON has committed to subscribe up to R$ 1.0 billion, equivalent to an 11.7% equity interest in the company

CREATING VALUE THROUGH JOINT-VENTURE

WITH E.ON

Leveraging Strong Complementary Capabilities to Enhance Growth

26

(*) E.ON has one of the broadest and most diverse power and gas asset bases in Europe.

Installed Capacity: 69 GW

2011 Traded Volumes: 2,000 billion kWh of power / 2,500 billion kWh of gas / 600 million tons of carbon / 300 million tons of coal

2011 Figures : Cash Position: EUR 6,610 million / Total assets: EUR 152,872 million / Sales: EUR 112,954 million

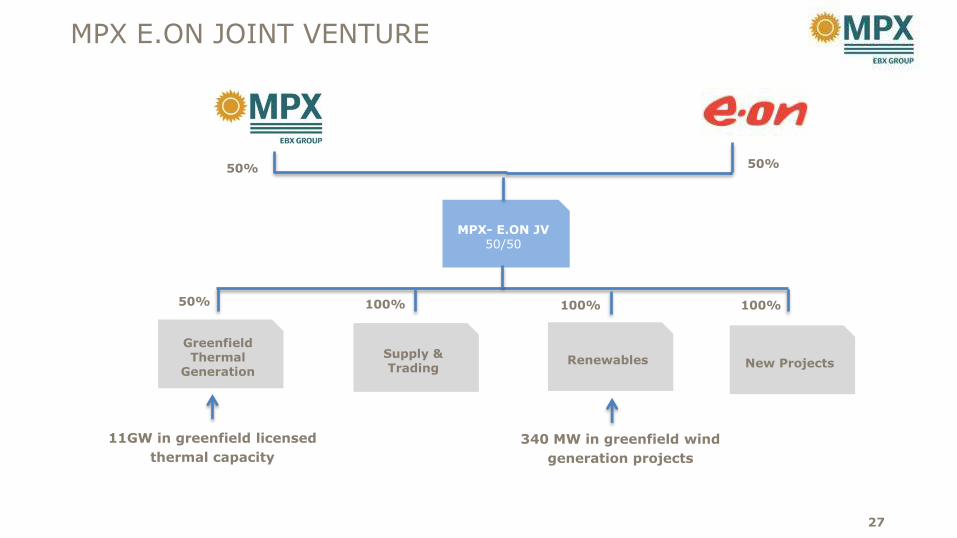

MPX E.ON JOINT VENTURE

27

50%

MPX- E.ON JV50/50

Greenfield Thermal

Generation

50%

Supply & Trading

Renewables New Projects

11GW in greenfield licensed

thermal capacity

50% 100% 100% 100%

340 MW in greenfield wind

generation projects

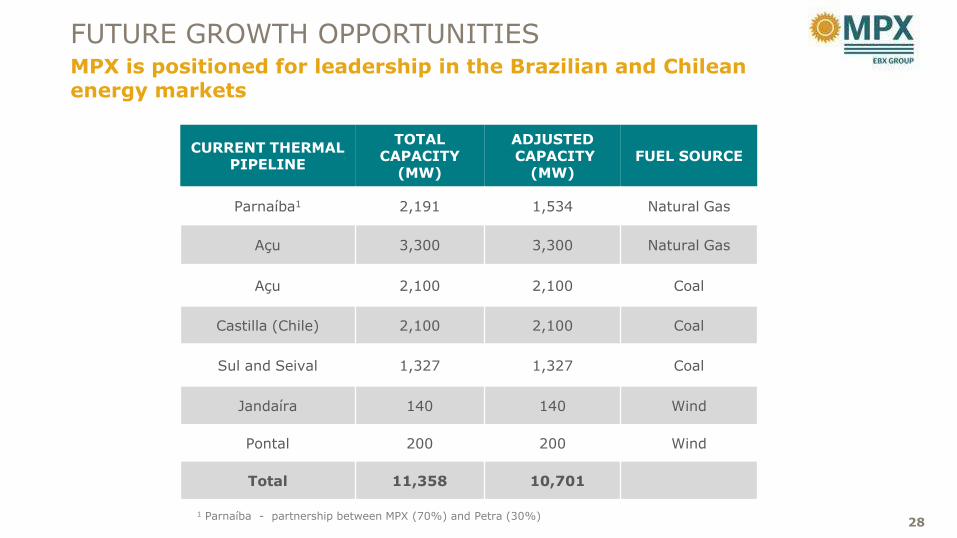

FUTURE GROWTH OPPORTUNITIESMPX is positioned for leadership in the Brazilian and Chilean energy markets

CURRENT THERMAL PIPELINE

TOTAL CAPACITY

(MW)

ADJUSTEDCAPACITY

(MW)FUEL SOURCE

Parnaíba1 2,191 1,534 Natural Gas

Açu 3,300 3,300 Natural Gas

Açu 2,100 2,100 Coal

Castilla (Chile) 2,100 2,100 Coal

Sul and Seival 1,327 1,327 Coal

Jandaíra 140 140 Wind

Pontal 200 200 Wind

Total 11,358 10,701

1 Parnaíba - partnership between MPX (70%) and Petra (30%)28

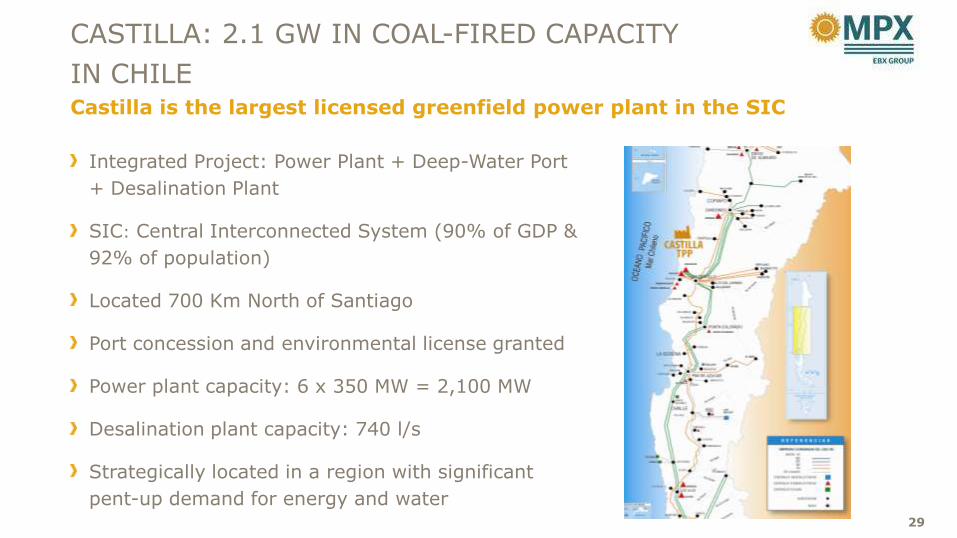

Integrated Project: Power Plant + Deep-Water Port

+ Desalination Plant

SIC: Central Interconnected System (90% of GDP &

92% of population)

Located 700 Km North of Santiago

Port concession and environmental license granted

Power plant capacity: 6 x 350 MW = 2,100 MW

Desalination plant capacity: 740 l/s

Strategically located in a region with significant

pent-up demand for energy and water

CASTILLA: 2.1 GW IN COAL-FIRED CAPACITY

IN CHILECastilla is the largest licensed greenfield power plant in the SIC

29

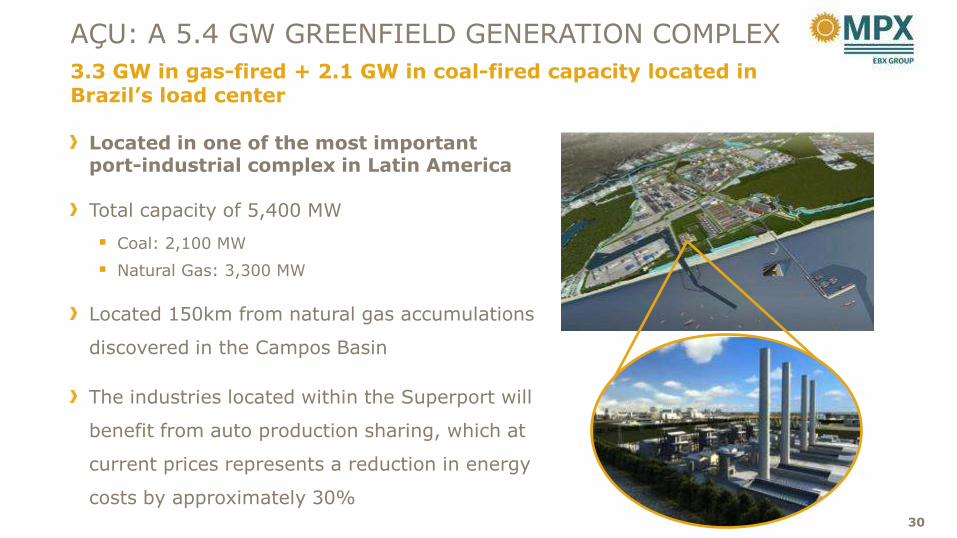

AÇU: A 5.4 GW GREENFIELD GENERATION COMPLEX

3.3 GW in gas-fired + 2.1 GW in coal-fired capacity located in Brazil’s load center

Located in one of the most important port-industrial complex in Latin America

Total capacity of 5,400 MW

Coal: 2,100 MW

Natural Gas: 3,300 MW

Located 150km from natural gas accumulations

discovered in the Campos Basin

The industries located within the Superport will

benefit from auto production sharing, which at

current prices represents a reduction in energy

costs by approximately 30%30

MPX Sul and MPX Seival:

Capacity: 727 MW + 600 MW

Fluidized Coal Bed technology

Lower emissions resulting from the mix burning of coal and wood chips

Seival Mine:

Partnership between MPX and Copelmi –one of Brazil’s largest coal miner

Operating License granted

152 MM tons in proven reserves and 459 MM tons in total resources

Located in a region with limited hydro

potential and transmission constraints.

SUL + SEIVAL: 1.3 GW INTEGRATED TO A

LIGNITE MINE Open-pit mine with low mining costs, located adjacent to the power plants, resulting in competitive fuel costs

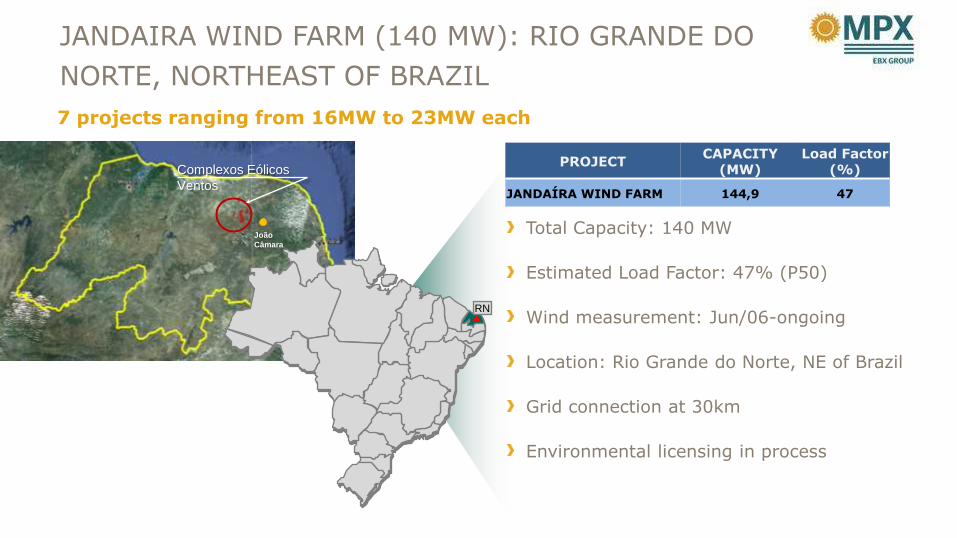

31

João

Câmara

Complexos Eólicos

Ventos

RN

PROJECTCAPACITY

(MW)Load Factor

(%)

JANDAÍRA WIND FARM 144,9 47

JANDAIRA WIND FARM (140 MW): RIO GRANDE DO

NORTE, NORTHEAST OF BRAZIL

Total Capacity: 140 MW

Estimated Load Factor: 47% (P50)

Wind measurement: Jun/06-ongoing

Location: Rio Grande do Norte, NE of Brazil

Grid connection at 30km

Environmental licensing in process

7 projects ranging from 16MW to 23MW each

RS

PROJECTCAPACITY

(MW)Load Factor

(%)

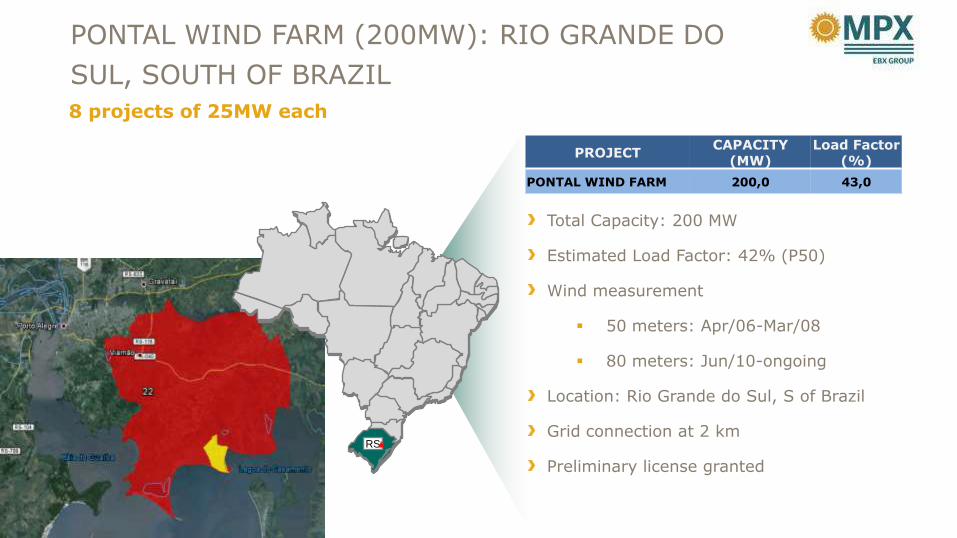

PONTAL WIND FARM 200,0 43,0

PONTAL WIND FARM (200MW): RIO GRANDE DO

SUL, SOUTH OF BRAZIL

8 projects of 25MW each

Total Capacity: 200 MW

Estimated Load Factor: 42% (P50)

Wind measurement

50 meters: Apr/06-Mar/08

80 meters: Jun/10-ongoing

Location: Rio Grande do Sul, S of Brazil

Grid connection at 2 km

Preliminary license granted

FINANCIAL HIGHLIGHTS

7

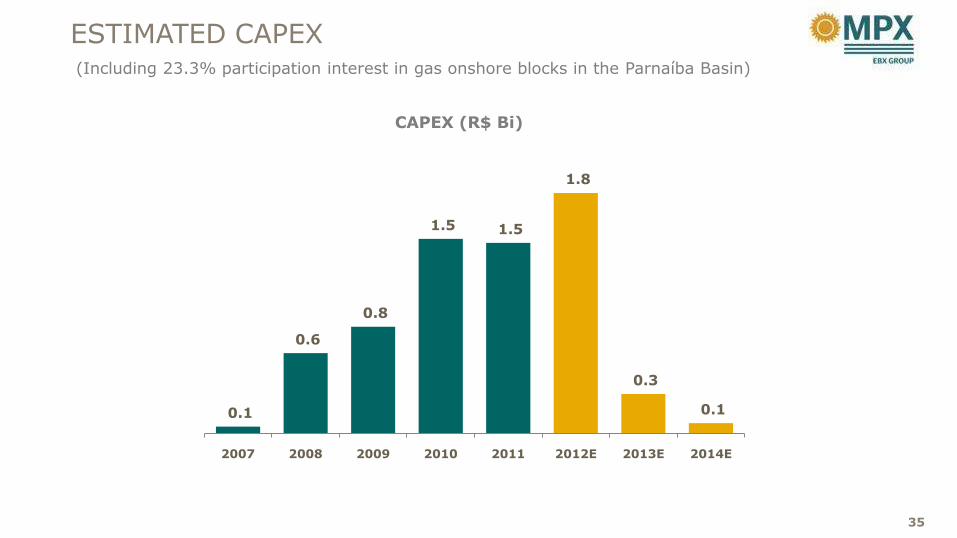

ESTIMATED CAPEX

35

CAPEX (R$ Bi)

(Including 23.3% participation interest in gas onshore blocks in the Parnaíba Basin)

0.1

0.6

0.8

1.5 1.5

1.8

0.3

0.1

2007 2008 2009 2010 2011 2012E 2013E 2014E

Debt Maturity Profile**

(R$ million)

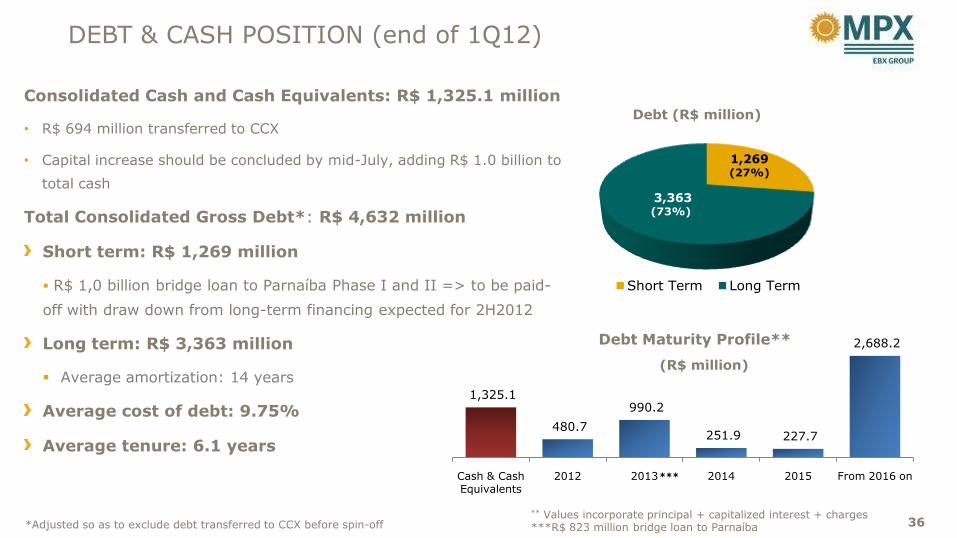

DEBT & CASH POSITION (end of 1Q12)

36

Consolidated Cash and Cash Equivalents: R$ 1,325.1 million

• R$ 694 million transferred to CCX

• Capital increase should be concluded by mid-July, adding R$ 1.0 billion to

total cash

Total Consolidated Gross Debt*: R$ 4,632 million

Short term: R$ 1,269 million

R$ 1,0 billion bridge loan to Parnaíba Phase I and II => to be paid-

off with draw down from long-term financing expected for 2H2012

Long term: R$ 3,363 million

Average amortization: 14 years

Average cost of debt: 9.75%

Average tenure: 6.1 years

Debt (R$ million)

** Values incorporate principal + capitalized interest + charges***R$ 823 million bridge loan to Parnaíba

1,269(27%)

3,363(73%)

Short Term Long Term

1,325.1

480.7

990.2

251.9 227.7

2,688.2

Cash & Cash Equivalents

2012 2013 2014 2015 From 2016 on

*Adjusted so as to exclude debt transferred to CCX before spin-off

***