17

MTN Group Limited – A growth strategy Phuthuma Nhleko Group President and CEO

MTN Group Limited– A growth strategy

Phuthuma NhlekoGroup President and CEO

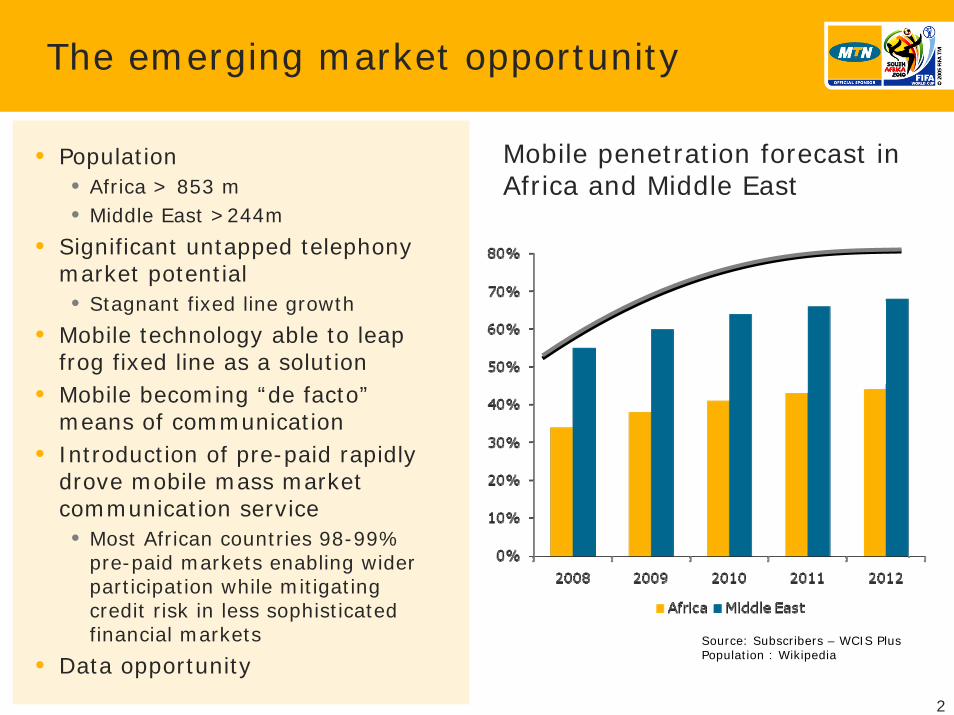

The emerging market opportunity

• Population • Africa > 853 m• Middle East >244m

• Significant untapped telephony market potential• Stagnant fixed line growth

• Mobile technology able to leap frog fixed line as a solution

• Mobile becoming “de facto”means of communication

• Introduction of pre-paid rapidly drove mobile mass market communication service• Most African countries 98-99%

pre-paid markets enabling wider participation while mitigating credit risk in less sophisticated financial markets

• Data opportunity

Mobile penetration forecast in Africa and Middle East

Source: Subscribers – WCIS PlusPopulation : Wikipedia

2

MTN’s opportunity

IranMarket size 52,5mMarket share 32%Penetration 50%GDP/capita 5,247

Cote d’IvoireMarket size 7.8mMarket share 40%Penetration 36%GDP/capita 1,250

UgandaMarket Size 14,9mMarket share 50%Penetration 19%GDP/capita 469

NigeriaMarket size 80mMarket share 43%Penetration 31%GDP/capita 1,490

CameroonMarket size 7.5mMarket share 60%Penetration 30%GDP/capita 1,290

South AfricaMarket Size 56mMarket share 36%Penetration 89%GDP/capita 6,170

GhanaMarket size 15,2mMarket share 52%Penetration 42%GDP/capita 786

MENAWECA

SEA

SyriaMarket size 11,7mMarket share 46%Penetration 38%GDP/capita 2,238

SudanMarket size 18,3mMarket share 25%Penetration 22%GDP/capita 1,631

AfghanistanMarket size 13mMarket share 29%Penetration 18%GDP/capita 457

Date : Sep 08Source GDP : IMF 2008 estimate

Group subscribers

80,736

Group ARPU$14

Population516.5m

Weightedaverage

penetration38.2%

3

Only key ops detailed

4

Building blocks of the growth strategy

To be the leader in telecommunications in emerging markets

Increased competitiveness

Execution excellence

ConsolidationLeverage existing footprint Convergence

Best practice Procurement synergies

Value proposition

Hub and cluster Diversification Skills

optimisation Brand

5

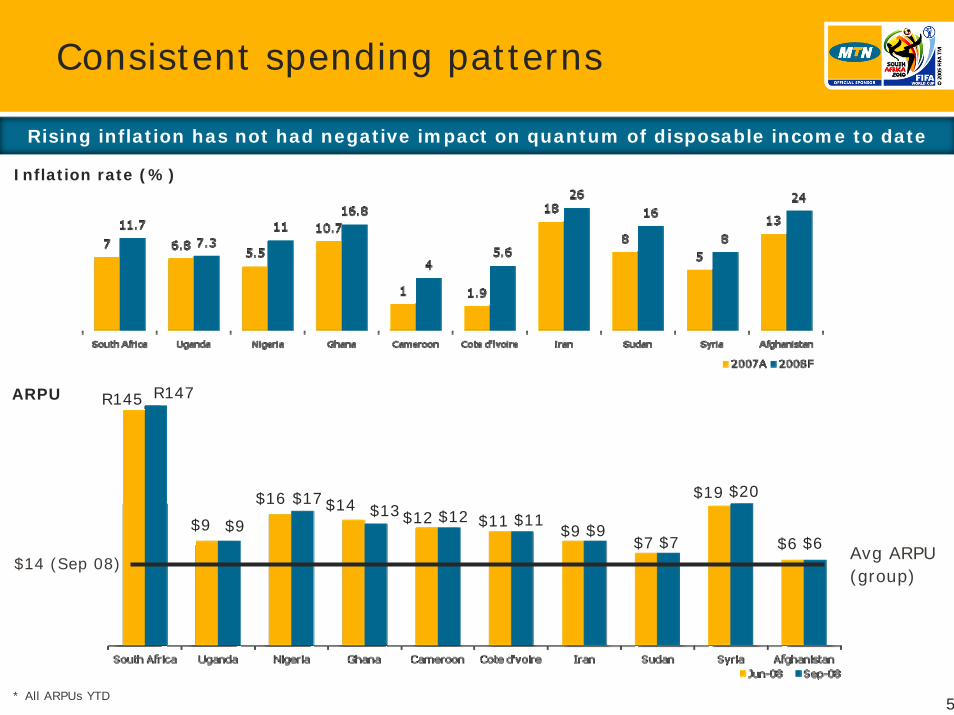

Consistent spending patterns

Avg ARPU (group)

$14 (Sep 08)

Rising inflation has not had negative impact on quantum of disposable income to date

R145 R147

$9

* All ARPUs YTD

Inflation rate (%)

$9

$16 $17 $14 $13$12 $12 $11 $11$9 $9

$19 $20

$7 $7 $6 $6

ARPU

6

FX backdrop

Exchange rates LC: USD

Well positioned

South Africa Uganda Nigeria Ghana Cameroon Cote

d’lvoire Iran Sudan Syria Afghani-stan

No of National

GSM operators

3 5 4 6 3 4 2 3 2 4

To launch - 1 1 2 - - 1 - 1 -

Market position 2 1 1 1 1 1 2 3 2 3

Market share

(Jun 08)36% 50% 43% 52% 60% 40% 32% 25% 46% 29%

Other ISP’sWimax CDMA

operator

CDMA operators

Fixed line & ISP’s

Fixed line and

CDMA

Fixed line & ISP’s

Strong fixed line

CDMA operators -BOT CDMA

operators

Well positioned in an increasing competitive environment

7

10,87710,877

Investing for growth

Investing to take advantage of the large market potential

9,7649,764

7,2127,212

5,2535,253

Capex spend in period

8

• Significant network infrastructure spend

• H1 spend represents 40% of ZAR25bn target for 2008 in line with 2007 H1 spend

• USD 3bn committed at Jun 08, including accelerated approvals for H1 2009 network capex

• 2006 marginal capex / subscriber impacted by Investcom acquisition

• 2008 capex spend in ZAR influenced by changes in fx rates (2008 target of ZAR25bn estimated at average fx rate of 7.22)

• Capex 2009 still under review

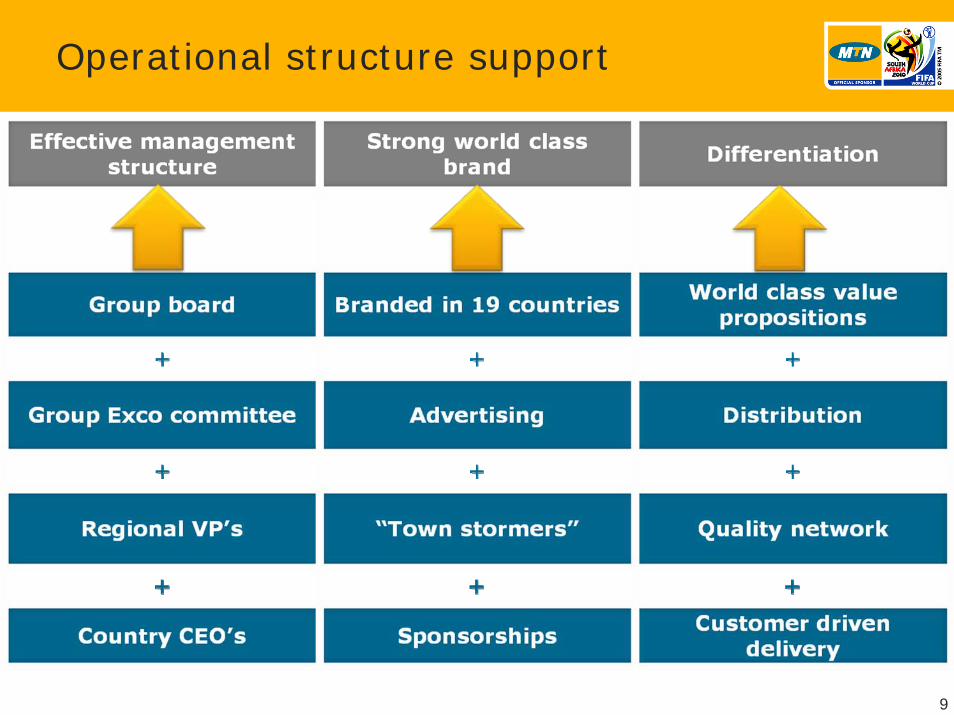

Operational structure support

9

Integrated service provision

• South Africa• Data as a % revenue – 12% (Jun08)

• Improved data propositions

• Purchase of Verizon (subject to CC approval)

• Nigeria• Data as a % of revenue -3% (Jun08)

• Renewed focus on leveraging VGC and XS Broadband

• Mobile TV

• Ghana• Launch of Blackberry

• Extensive Edge deployment

• Iran • Data as a % of revenue -8%

• SMS 93% of data revenue

• VAS launched

10

Positioning ourselves as an integrated service provider

Data RevenueZAR (million)

As % of revenue 4.9% 5.1% 5.9% 6.4%

Managing risks

11

Portfolio management

MTN Group

Total(Revenue ZAR million)

*** difference in HO companies* 9 months* 6 months

Increased diversification

51 595

12

15%15%

42%42%

46 128

16%16%

46%46%

38%38%43%43%

7%7%

41%41%

51%51%

40%40%

60%60%

19 405 23 73027 212

66%66%

34%34%32%32%

70%70%

73 417

MENA

Margin managment

EBITDA Contribution % EBITDA Margin %

Difference in HQ companiesComparatives June to June

2007SEA

2007

2007WECA

2008

2007MENA

2008

2007*MTN Group

2008

100

100

8

11

54

34

57

30

44.4

42.6

25.4

54.2

35.5

29.5

52.9

33.5

13

Other considerations

•World recession

•Economic slowdown in Africa and ME

•Slowing GDP growth although still positive

•Impact of oil and commodity prices

•Access to funding

•Balance sheet structure

•Local funding

•No material re-financing

•Strong cash flows

•Governance

•JSE / King code

•Management stability

14

Global backdrop MTN

15

Looking forward…

Thank you

Questions

© 2008 Mobile Telephone Networks. All rights reserved.17

Notice

The information contained in this document has not been verified independently. No representation or warranty express or implied is made as to and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information or opinions contained herein. Opinions and forward looking statements expressed represent those of the Company at the time. Undue reliance should not be placed on such statements and opinions because by nature, they are subjective to known and unknown risk and uncertainties and can be affected by other factors that could cause actual results and Company plans and objectives to differ materially from those expressed or implied in the forward looking statements.

Neither the Company nor any of its respective affiliates, advisors or representatives shall have any liability whatsoever (based on negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation and do not undertake to publicly update or revise any of its opinions or forward looking statements whether to reflect new information or future events or circumstances otherwise.

This presentation does not constitute an offer or invitation to purchase or subscribe for any securities and no part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever.