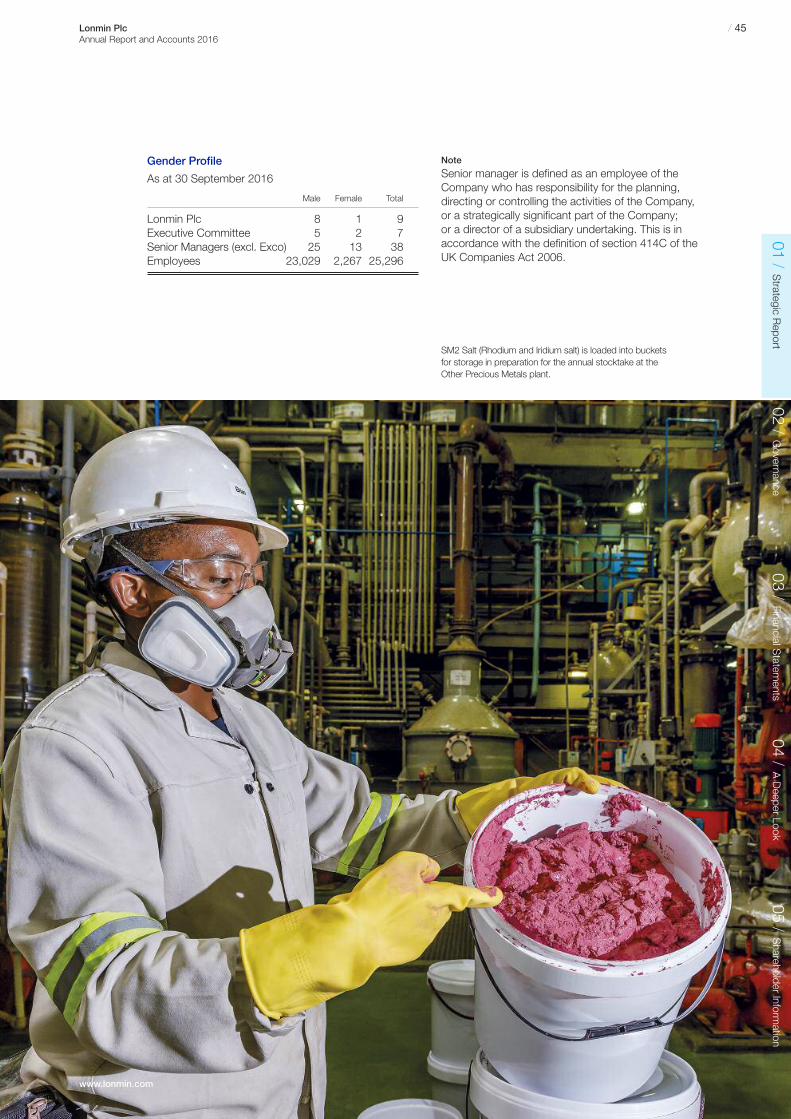

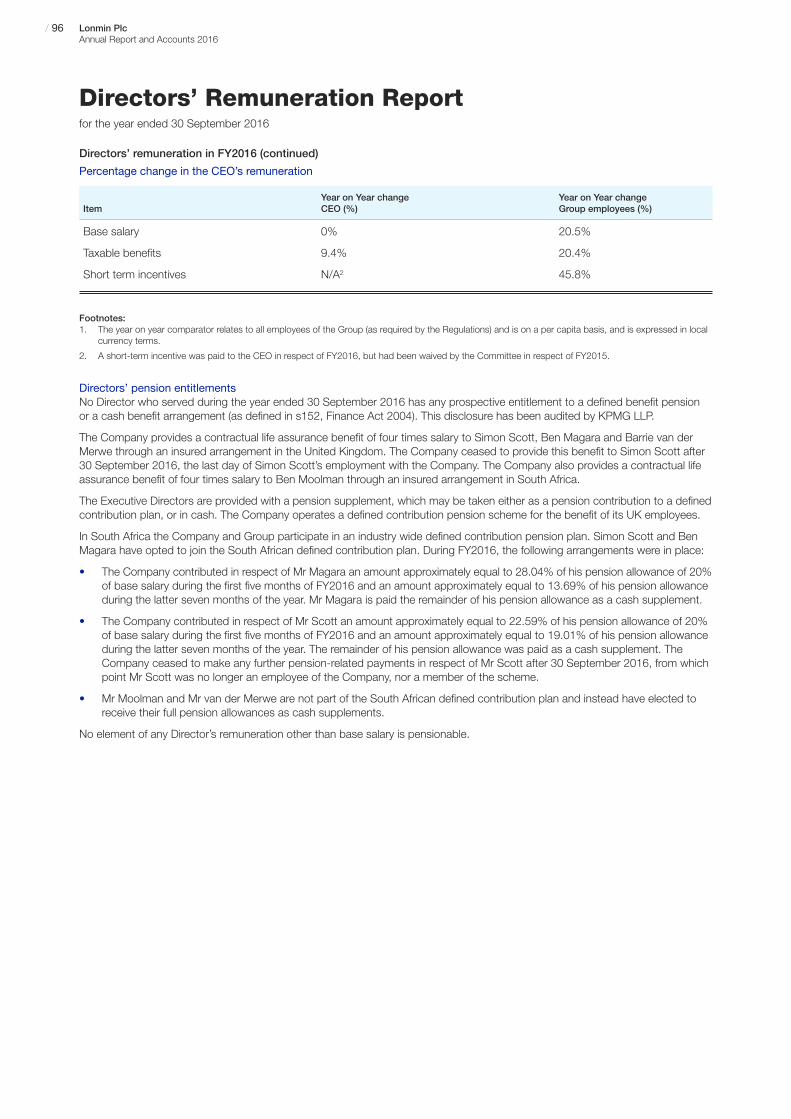

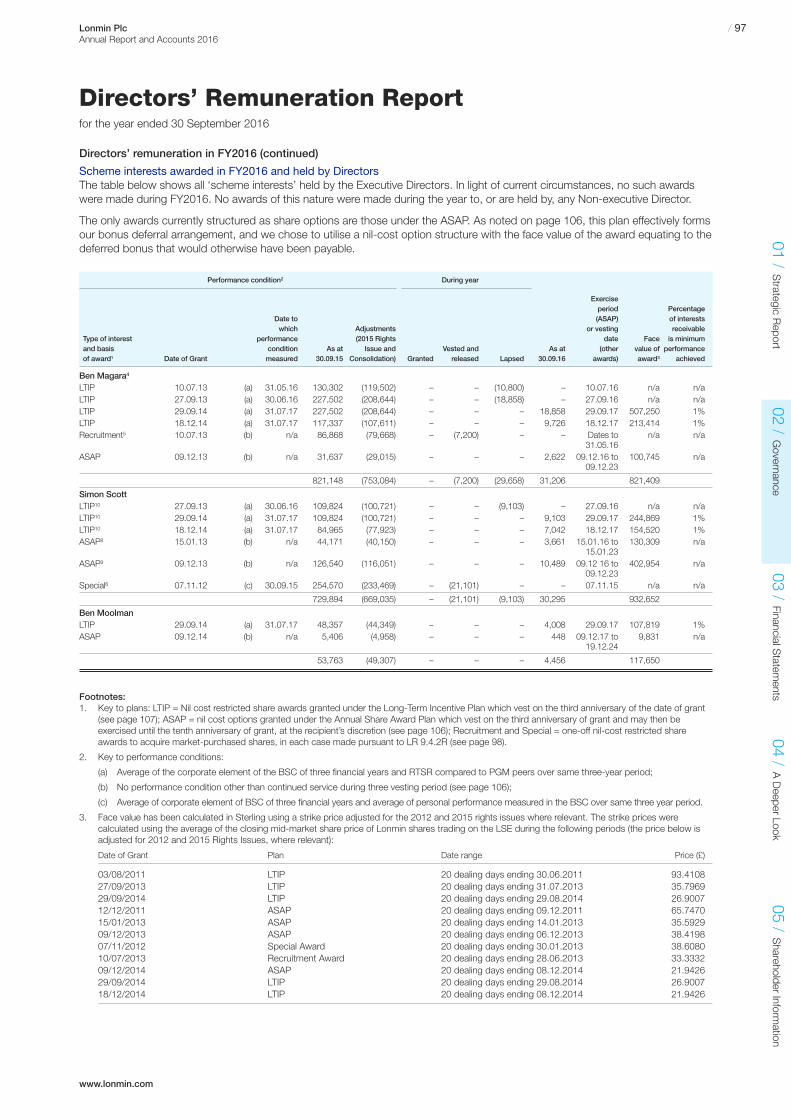

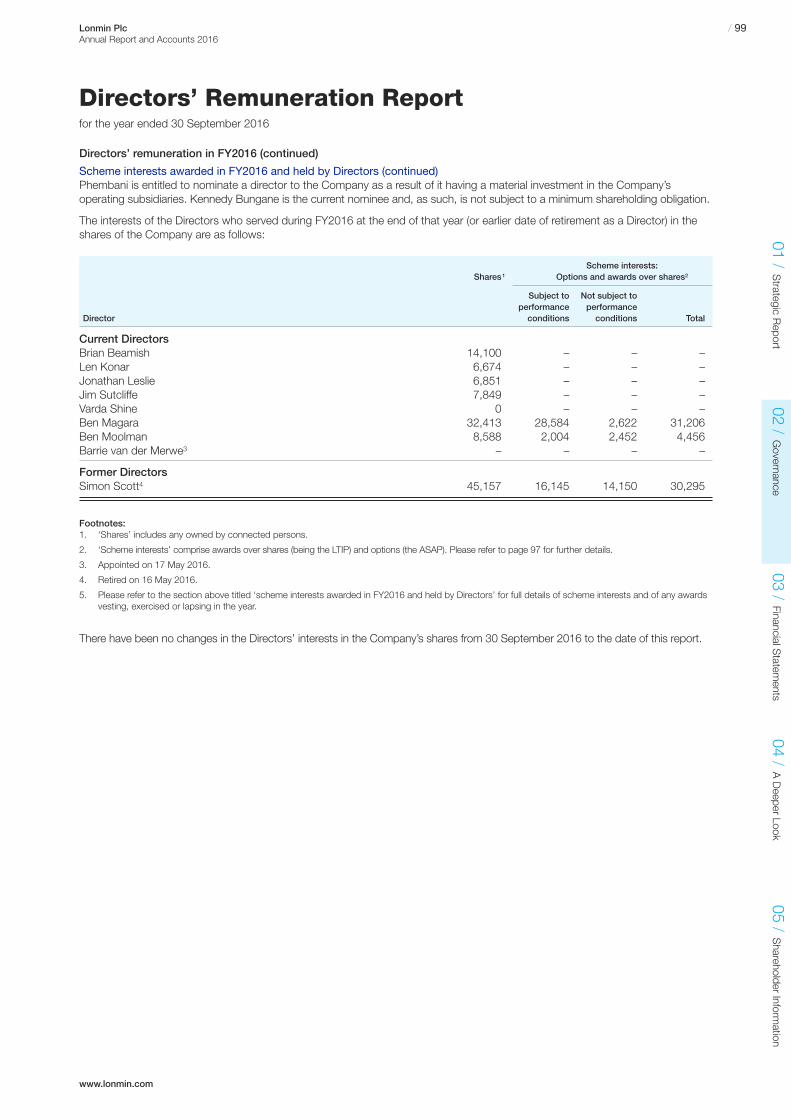

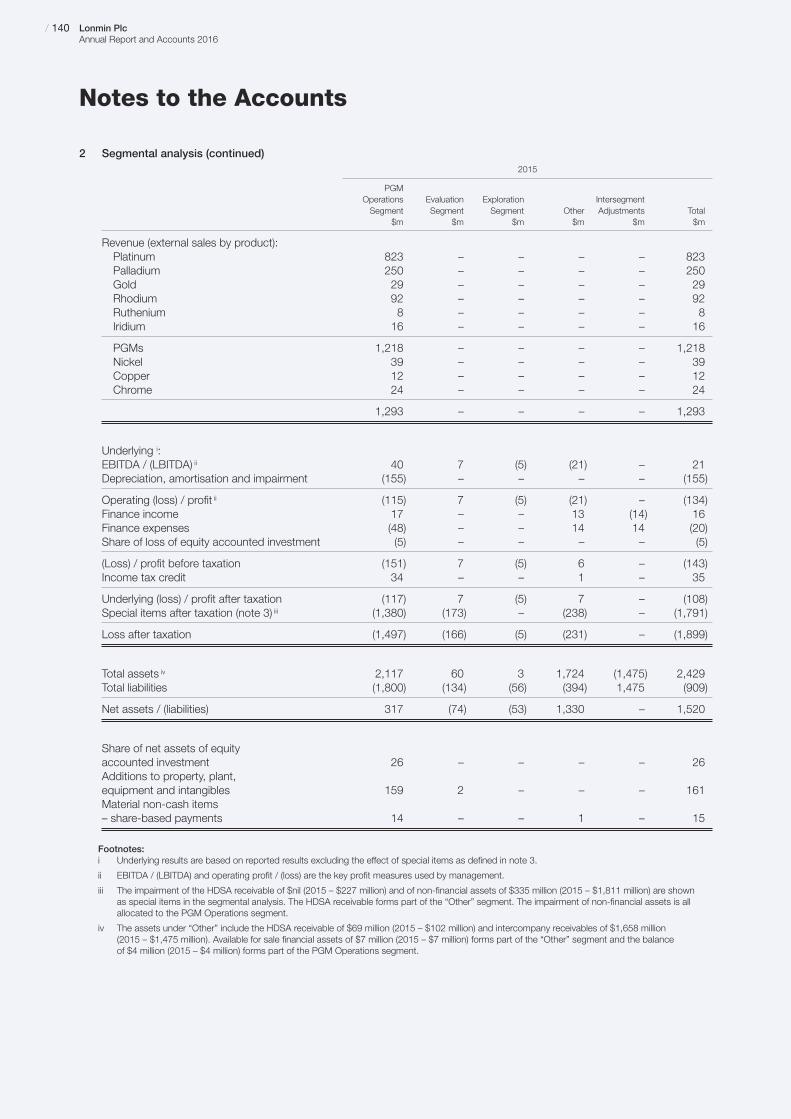

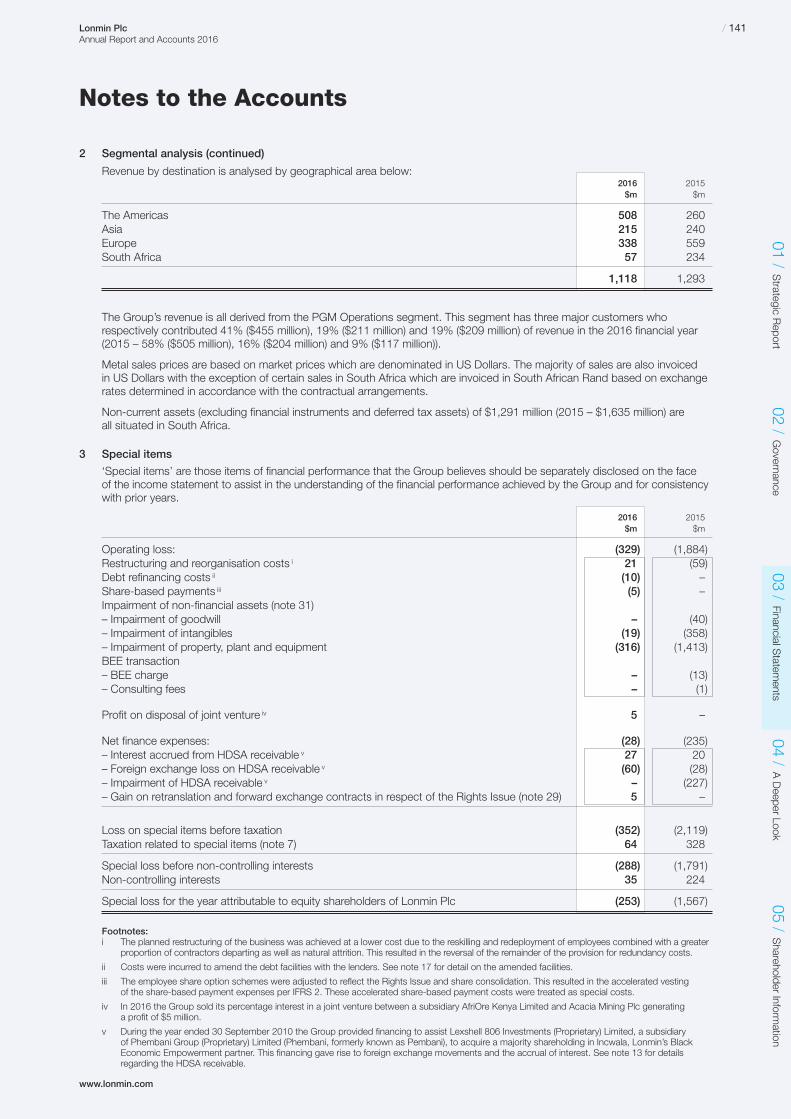

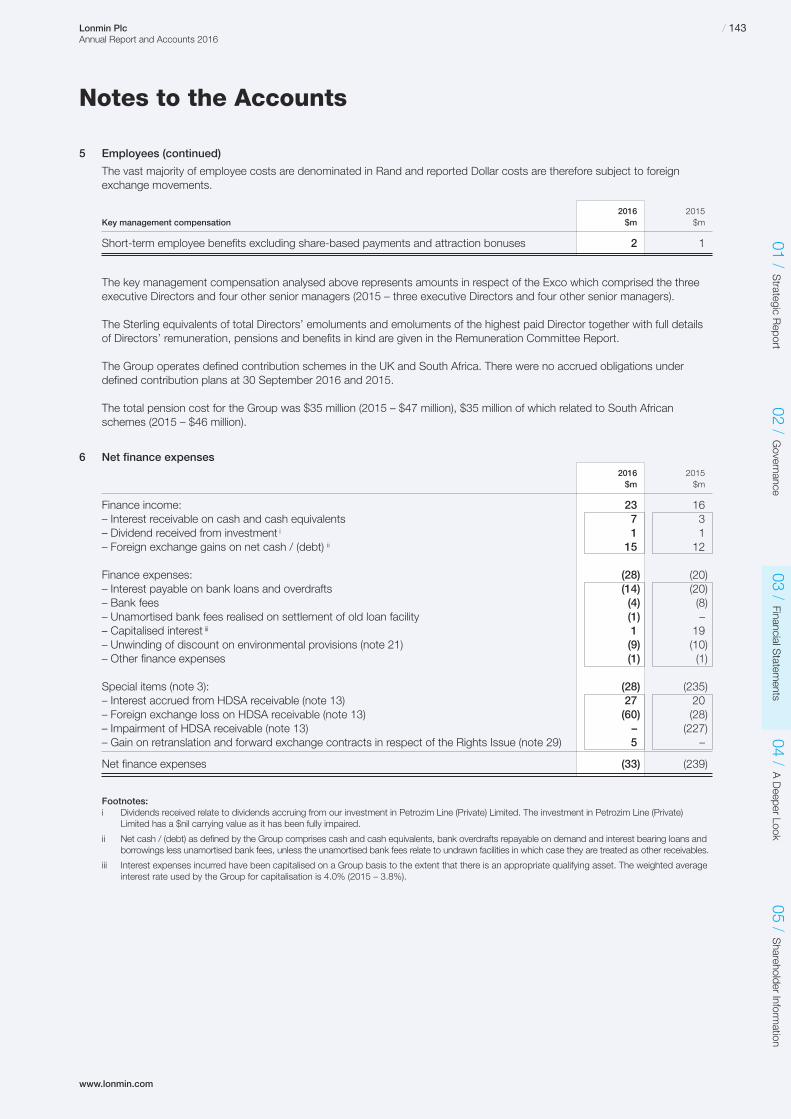

216

Annual Report and Accounts 2016 For the year ended 30 September 2016 Lonmin Plc MUCH ACHIEVED WELL REPOSITIONED

Lonmin P

lcA

nnual Report and A

ccounts for the year ended 30 Septem

ber 2016

www.lonmin.com

Lonmin PlcRegistered in England, Company Number 103002Registered Office: 4 Grosvenor Place, London SW1X 7YL

Annual Report and Accounts 2016For the year ended 30 September 2016

Lonmin Plc

MUCH ACHIEVEDWELL REPOSITIONED

See further information at www.lonmin.com

LONMIN HAS BEEN CHALLENGED MANY TIMES IN OUR

HISTORY, AND EACH TIME WE HAVE SEIZED THE

OPPORTUNITIES THOSE CHALLENGES HAVE PRESENTED.

Lonmin is a primary producer of Platinum Group Metals (PGMs).These metals are essential for many industrial applications,especially catalytic converters for internal combustion engineemissions, as well as their widespread use in jewellery andinvestment. Saleable by-products produced from our PGMmining include gold, copper, nickel, chrome and cobalt.

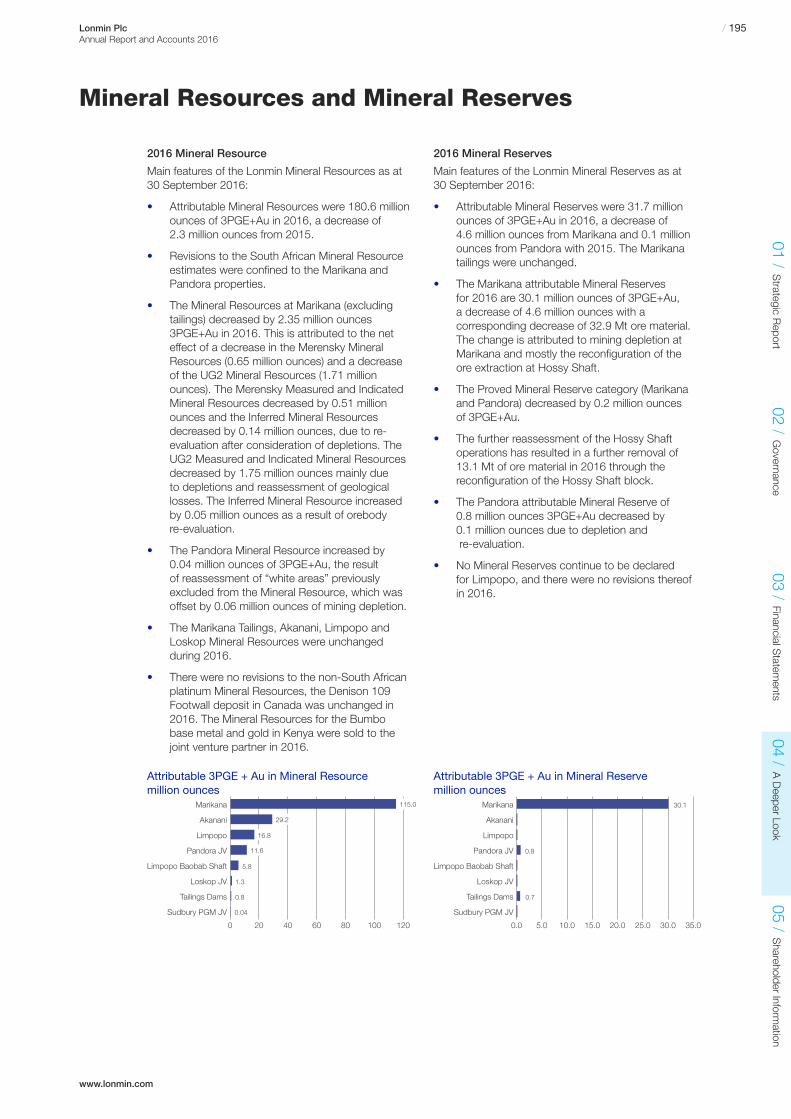

Our core operations, consisting of 11 shafts and inclines, are situated in theBushveld Igneous Complex in South Africa, a country which hosts nearly 80%of global PGM resources. We have been granted a New Order Mining Licenceby the South African government for our core operations, which runs to 2037and is renewable to 2067. We have resources of 181 million troy ounces(3PGE + Au) and 32 million ounces (3PGE + Au) of reserves.

www.lonmin.com

Lonmin PlcAnnual Report and Accounts 2016

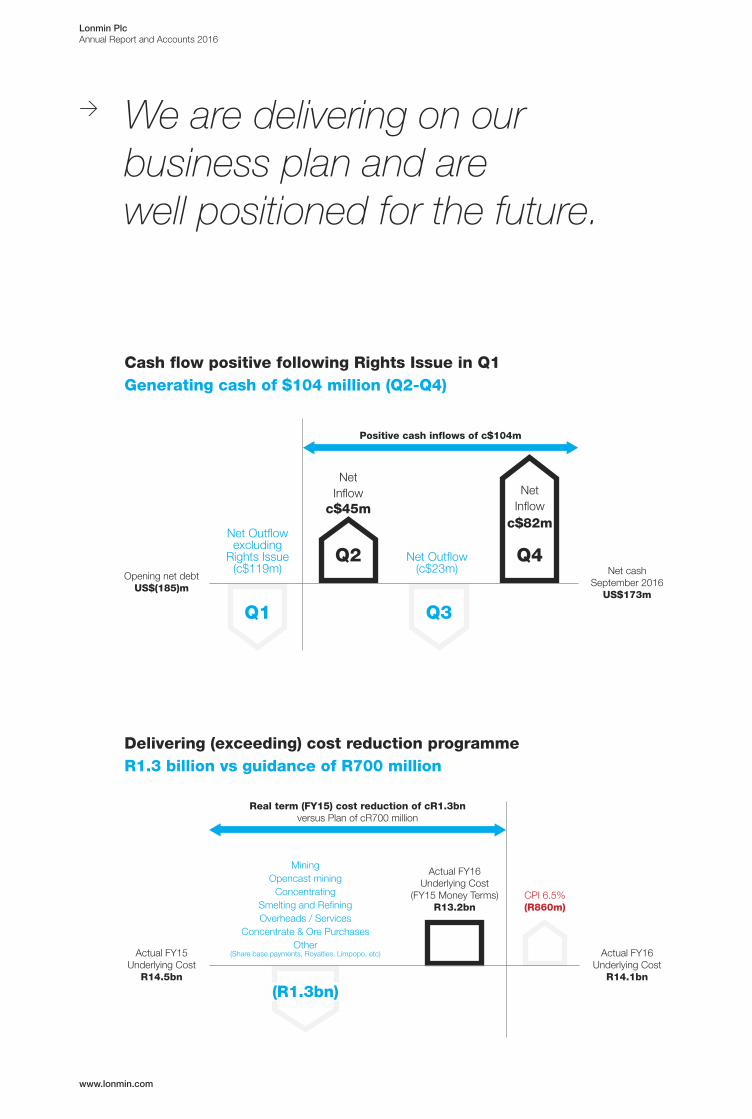

> We are delivering on ourbusiness plan and arewell positioned for the future.

Cash flow positive following Rights Issue in Q1Generating cash of $104 million (Q2-Q4)

Q2 Q4

Q1 Q3

Net Outflowexcluding

Rights Issue(c$119m)

Net Outflow(c$23m)

NetInflow

c$45mNet

Inflowc$82m

Net cashSeptember 2016

US$173m

Opening net debtUS$(185)m

Positive cash inflows of c$104m

Delivering (exceeding) cost reduction programmeR1.3 billion vs guidance of R700 million

(R1.3bn)

MiningOpencast mining

ConcentratingSmelting and RefiningOverheads / Services

Concentrate & Ore PurchasesOther

(Share base payments, Royalties, Limpopo, etc)

CPI 6.5%(R860m)

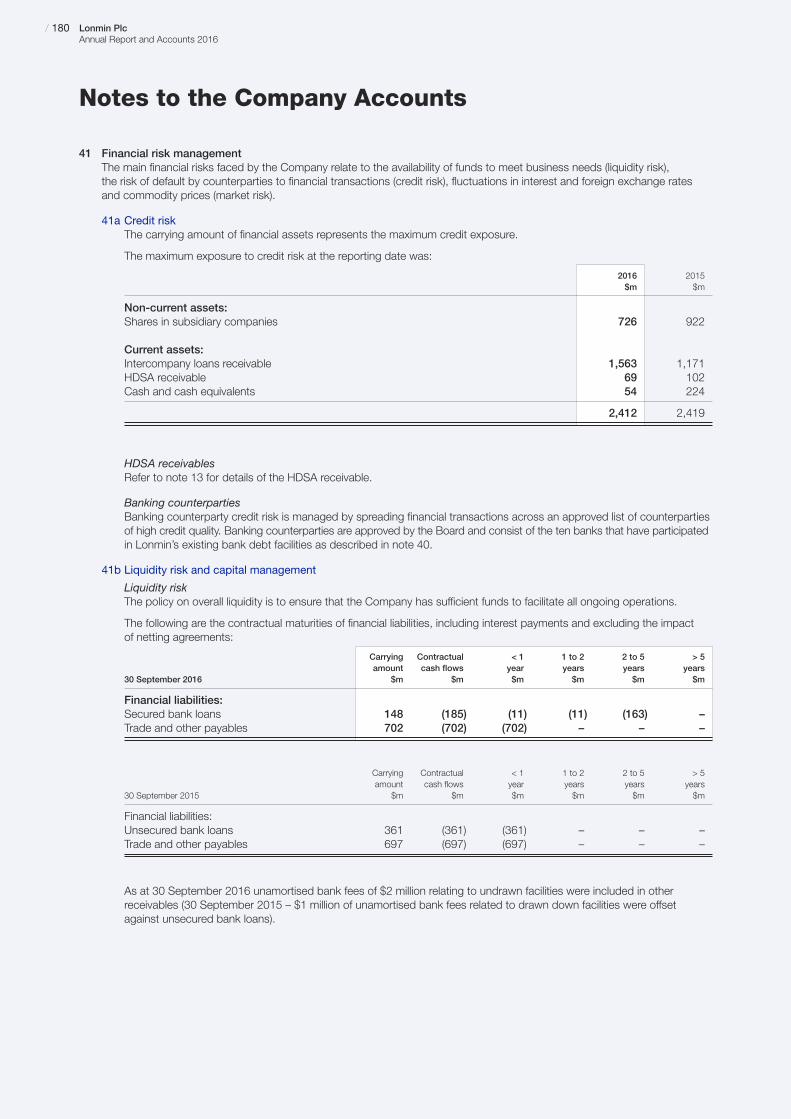

Actual FY16Underlying Cost

(FY15 Money Terms)R13.2bn

Actual FY16Underlying Cost

R14.1bn

Actual FY15Underlying Cost

R14.5bn

Real term (FY15) cost reduction of cR1.3bnversus Plan of cR700 million

Lonmin PlcAnnual Report and Accounts 2016

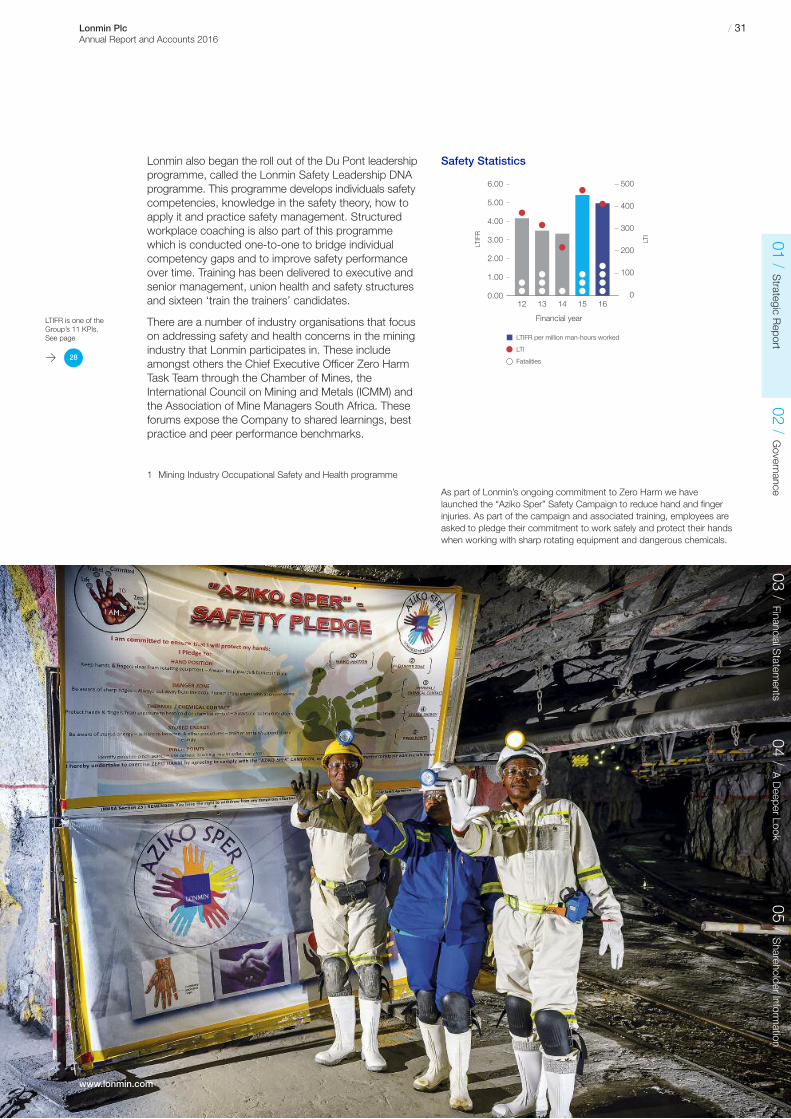

01 Underground locomotives have been fitted with anti-collision detection devices providing earlywarning of oncoming locomotives.

02 Underground employees are supplied with proximity detection devices providing early warningfor people and vehicles.

03 Ongoing innovation in the Processing Division was the foundation for the conceptualisation,construction and successful commissioning of the Other Precious Metals (OPM) plant at thePrecious Metals Refinery, which uses the latest third generation technology for improvedRhodium and Iridium recoveries. The OPM contributed to additional release of 25,280 ouncesof Rhodium and 13,068 ounces of Iridium.

Our belief is that Zero Harm is possible and ouraim is to provide a safe working environment forall of our employees, our contractors and thecommunities we operate in.

Our goal is for every person in the business tohave a personal understanding of, and respectfor, the importance of safety in the workplacethrough entrenching safety principles, increasingvisibility on fatality and injury prevention andencouraging a safe high performance culture.Zero Harm can be achieved if the risks that leadto serious or fatal accidents are managedconsistently – we need to reach our productiontargets to sustain the Company and our families,but safety always comes first.

> Safety comes first in everything we do…

Lonmin PlcAnnual Report and Accounts 2016

Our initiatives around employeewellness, financial literacy andcounselling as well as the technicalsolutions around debottleneckinglogistics continue to bear fruit. Likemost things, it is a journey, and one we cannot lose focus on if we are tosucceed for you, our shareholdersand indeed all our stakeholders.

> Working better together. Improving relationships. … Building trust

01 Lonmin’s bursar students receive mining orientation at the Vulindlela Training Centre.

02 Removing a sample from the palladium circuit in the Primary Separation Departmentat the Precious Metal Refinery.

03 The employee infill apartments pictured have been built in the areas between existingconverted hostel blocks to utilise the space available and to access existing bulkinfrastructure. Phase 1 of construction saw 325 units completed at Karee inJanuary 2016.

Lonmin PlcAnnual Report and Accounts 2016

Everything we are now doing, thechanges we have introduced, and theplans we have for the future are allfocused on creating a sustainablebusiness, benefiting our employees and host communities and critically,driving value for you, our shareholders.

> A company that actssustainably will also beregarded as more successfulin the long-term…

01 The Bapo Ba Mogale Community have been awarded four procurement contractsin terms of the 2014 Bapo Transaction – pictured here are the Bapo managementteam after being awarded the Yellow Equipment contract with a gross value ofR45million per annum over a five year period, totalling R225 million.

02 Learners from Tlhapi Moruwe Primary in Wonderkop play during break – Lonminbuilt eight new classrooms and ablution facilities at this school during 2016.Lonmin currently supports 22,500 learners at schools in and around our operations.

03 Employees commit to the “Aziko Sper” Finger Safety Campaign by leaving theirpalm imprint on a board at their workplace.

Lonmin PlcAnnual Report and Accounts 2016

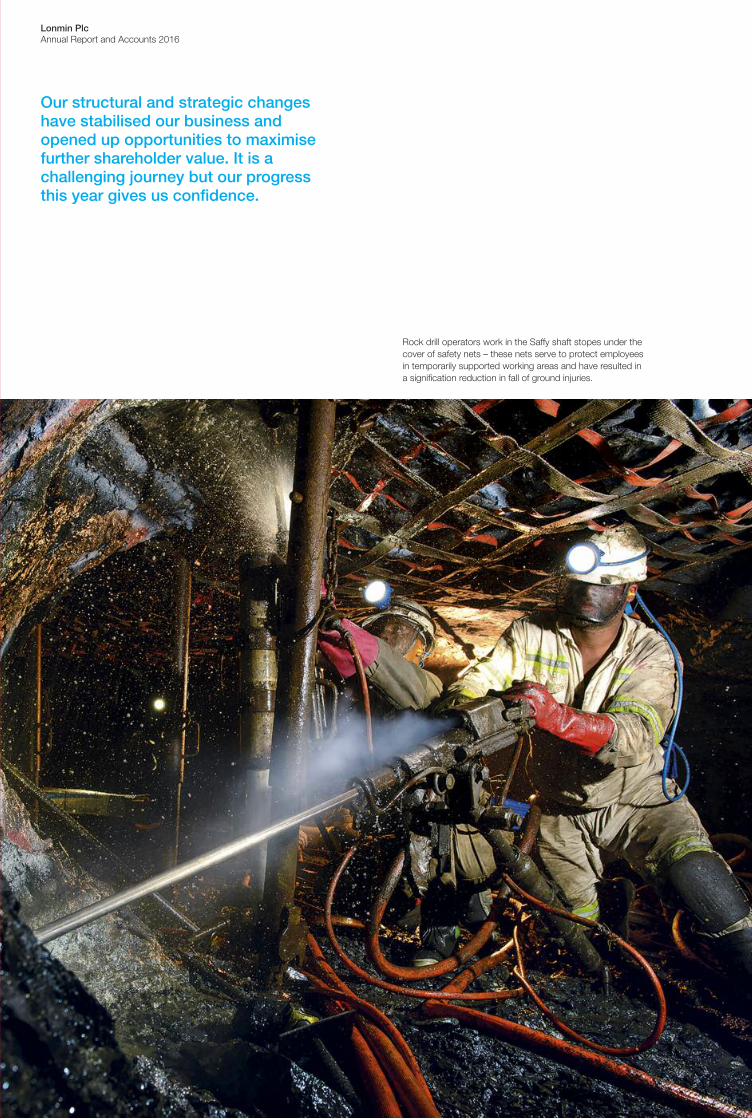

Our structural and strategic changeshave stabilised our business andopened up opportunities to maximisefurther shareholder value. It is achallenging journey but our progressthis year gives us confidence.

Rock drill operators work in the Saffy shaft stopes under thecover of safety nets – these nets serve to protect employeesin temporarily supported working areas and have resulted ina signification reduction in fall of ground injuries.

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 01Lonmin PlcAnnual Report and Accounts 2016

>04 Chairman’s Letter06 Chief Executive Officer’s Letter08 Our Business Model11 Our Strategy18 Market Review and Outlook20 Principal Risks and Viability28 Key Performance Indicators (KPIs)30 Performance

30 Safety32 Financial Review38 Operations44 Sustainability

02 Performance Highlights

01 / Strategic Report

A summary of the changing landscape weoperate in, and how that has shaped ourstrategy and financial position. Plus a reviewof performance against our goals and ourapproach to running a sustainable business.

>54 Board of Directors56 Executive Committee58 Corporate Governance Report74 Audit & Risk Committee Report83 Nomination Committee Report85 Directors’ Remuneration Report114 Directors’ Report

02 / Governance

We explain how we are organised, whatthe Board has focused on and how it hasperformed, our diversity practices, how wecommunicate with our shareholders andhow our Directors are rewarded.

> 03 / Financial Statements

The statutory financial statements of boththe Group and the Company and associatedaudit reports.

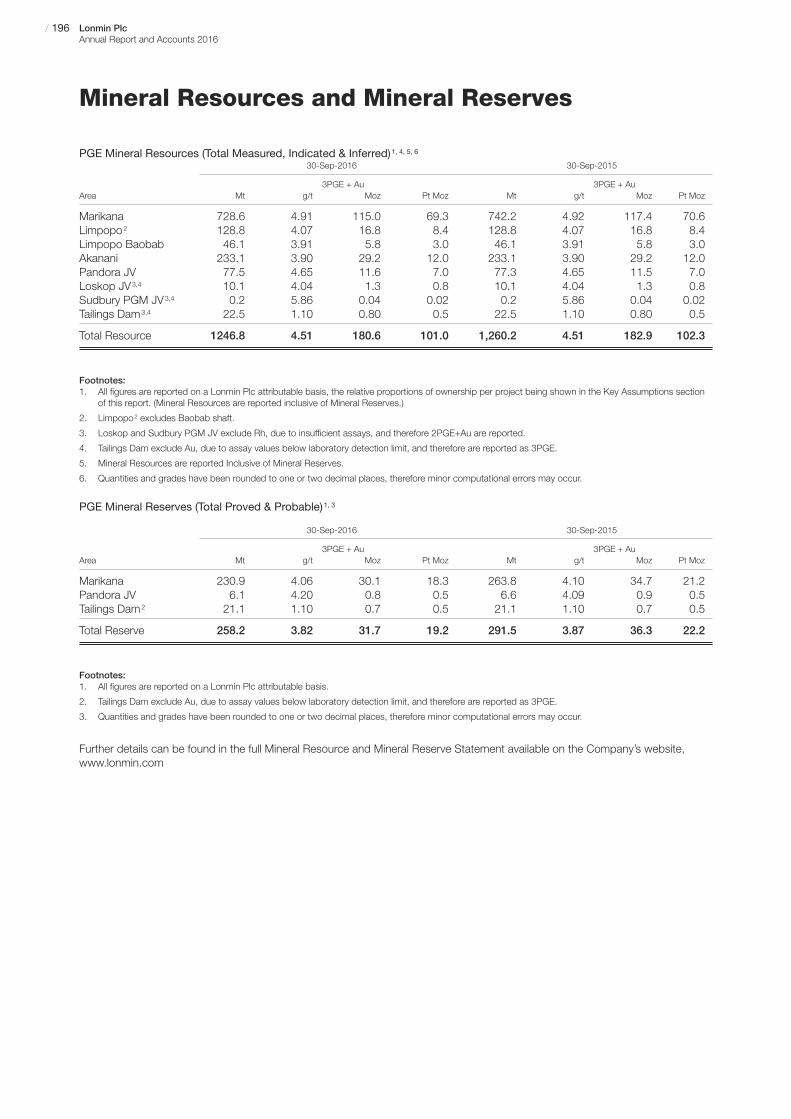

>188 Consolidated Group Five Year Financial Record189 Operating Statistics – Five Year Review195 Mineral Resources and Mineral Reserves

04 / A Deeper Look

Key financial and operational statisticsover the past five years and a summaryof our mineral resource and mineralreserve information.

>198 Shareholder Information200 Corporate Information201 Reporting Calendar202 Acronyms and Abbreviations203 The Sixteen-Eight Memorial Trustibc Lonmin Charter

05 / Shareholder Information

Additional information for shareholdersincluding our forthcoming reporting calendar.

Welcometo our 2016 Annual Report

120 Independent Auditor’s Report124 Responsibility Statement of the Directors in Respect of the Annual Report and Accounts125 Consolidated Income Statement125 Consolidated Statement of Comprehensive Income126 Consolidated Statement of Financial Position127 Consolidated Statement of Changes in Equity128 Consolidated Statement of Cash Flows129 Notes to the Accounts172 Lonmin Plc Company Balance Sheet173 Lonmin Plc Company Statement of Changes in Equity174 Lonmin Plc Company Statement of Cash Flows175 Notes to the Company Accounts

/ 02 Lonmin PlcAnnual Report and Accounts 2016

Performance HighlightsWe have now sustainably repositioned the business, not only to withstand the current low PGM price environment, but to also seize opportunities tomaximise value for shareholders and all our stakeholders.

Below we outline some key achievements of the year and guidance for 2017.

• Highlights– The successful completion of the reorganisation has improved Lonmin’s profitability and

resulted in the business being cash flow positive after capital expenditure despite thecontinuing low PGM pricing environment

– Underlying operating profit increased to $7 million from a loss of $134 million in the prior year– Cash improved from $69 million at end of first quarter to $173 million at year end– Liquidity improved from $422 million at end of first quarter to $537 million at year end– Sales of 735,747 Platinum ounces, exceeded the sales guidance of 700,000 Platinum ounces,

supported by our smelter clean-up and metal release from improved processing technology– Achieved cost reduction of R1.3 billion, 86% higher than the target of R700 million– Underlying costs decreased by 3.2% to R14.1 billion – unit costs increased by 4.0% to

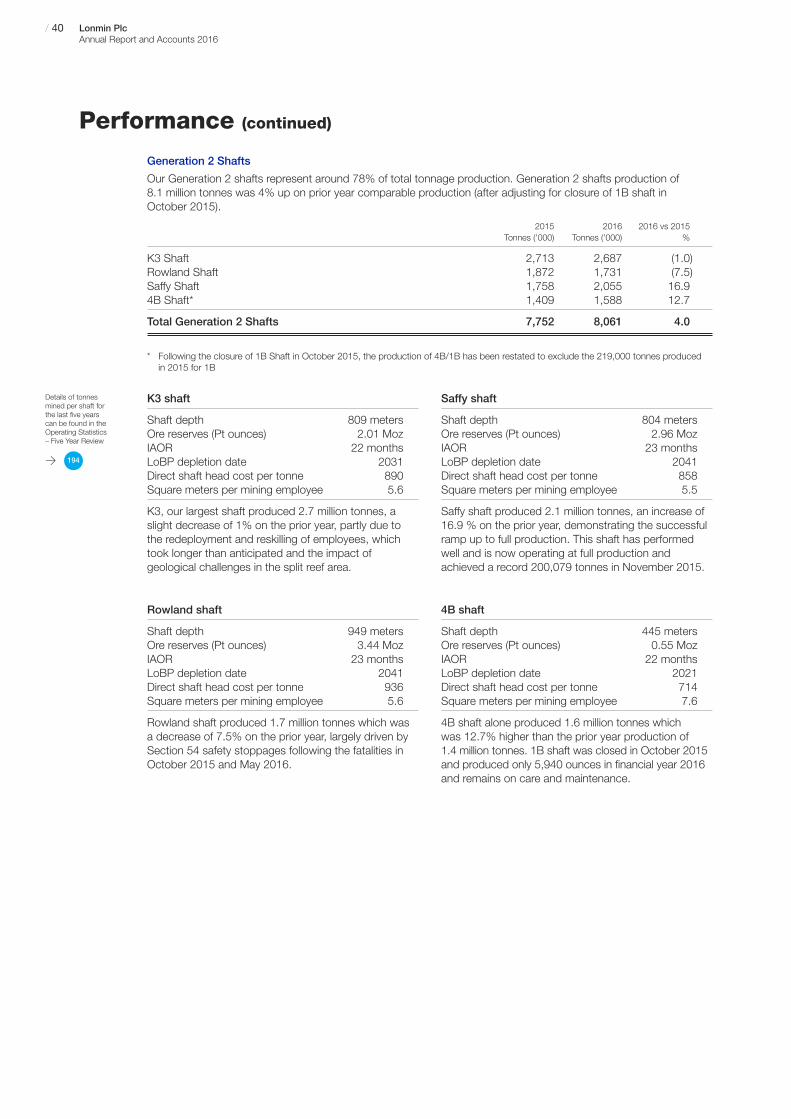

R10,748, despite 8.2% increase in labour costs– Concentrator recoveries of 86.6% continue to be industry leading– Generation 2 shafts production of 8.1 million tonnes, 4.0% up on prior year on a comparable

basis, and productivity up 5.0%, notwithstanding rationalisation of the workforce by 19.0%– The planned decline of our Generation 1 shafts is on track, reducing our high cost production

in an oversupplied market– Saffy shaft production up 16.9% and has reached steady state– Average Rand full basket price (including base metals) up 7.5% on prior year, at R11,637

per PGM ounce– Peaceful and non-disruptive conclusion of multi-year wage agreement, reflects a maturing

relationship with the unions and employees– Preserved Immediately Available Ore Reserves (IAOR) which stand at 22.4 months,

providing us with operational flexibility

• Safety– Determined to continuously improve our overall safety performance– Saddened by the loss of four employees during the year despite our best efforts to achieve

Zero Harm in all our operations– Lost Time Injury Frequency Rate (LTIFR) improved by 8.1% to 4.97 (2015: 5.41)

• Guidance for financial year 2017– Platinum sales between 650,000 and 680,000 ounces– Unit costs remain under pressure; expected to be in the range of R10,800 to R11,300 per

PGM ounce– Capital expenditure to be funded from cash generated from operating activities and third

party funding. Our 2017 guidance is expected to be increased to approximately R1.8 billionwhich includes R400 million related to the Bulk Tailings Treatment (BTT) project

www.lonmin.com

StrategicReport

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation/ 03Lonmin Plc

Annual Report and Accounts 2016

04 Chairman’s Letter06 Chief Executive Officer’s Letter08 Our Business Model11 Our Strategy18 Market Review and Outlook20 Principal Risks and Viability28 Key Performance Indicators (KPIs)30 Performance

30 Safety32 Financial Review38 Operations44 Sustainability

01/

A summary of the changing landscape we operate in,and how that has shaped our strategy and financial position.Plus a review of performance against our goals and our approach to running a sustainable business.

/ 04 Lonmin PlcAnnual Report and Accounts 2016

Chairman’sLetter

“I am pleased with the strongerposition we are in but thereis still much to do and yourBoard is concentrated onensuring that your Companyachieves its targeted objectivesover the medium term. It is achallenging journey but ourprogress this year gives usconfidence.”

Brian BeamishChairman

Dea r Fellow Sha reholder,Early in the 2016 financial year your Company completed asuccessful Rights Issue which, together with the renewal ofour debt facilities, shaft closures, workforce reduction and theimplementation of a focused Business Plan, has put us in astronger position to steer Lonmin through the current low PGMpricing environment. The steps taken by the Board and ourExecutive Management team were necessary to reinforce thebusiness, while preserving the future value of our high qualityasset base and long-term mining rights. I would like to thankshareholders for their support and for understanding the realityof our position during what was a challenging period.

We were all deeply saddened by the loss of four employeesduring the year despite our best efforts to achieve zero harm inall our operations. I would like to add my heartfelt condolencesto those of our Chief Executive, Ben Magara, to the families andfriends of the deceased. Safety underpins all that we do and,as always, remains an absolute priority for the Group and ourExecutive Management.

For the last three quarters of the financial year, we havemanaged Lonmin to be cash flow positive after capitalexpenditure. As we stated in our Prospectus at the time ofthe Rights Issue, our objectives are to reduce fixed costs,keep capital expenditure to the minimum necessary, improveefficiencies, and, at the same time, preserve the Company’slong-term value. As part of this, we also announced thereorganisation of the business which saw us reduce our overallworkforce and focus on our core Generation 2 shafts.

The strength of Lonmin’s relationship with its unions has beenput to the test over the year with the reorganisation and wagenegotiations. By maintaining a constructive and regulardialogue throughout, your Company was able to keep joblosses to the minimum necessary, and, in October 2016,reached a satisfactory outcome to the current wage negotiations.Both achievements were gained without labour disputes orwork stoppages. This is a clear recognition of the work bothour Management and the unions have put into building andnurturing effective relationships. The focus must now be oncontinuing to rebuild morale throughout our operations,especially after the reorganisation.

Sustainability remains central to our business and is dependenton our relationship with our employees and fulfilling our socialand community responsibilities. We are pleased with theprogress we have made in employee wellness and remainconfident that these initiatives, including financial literacy andcounselling, will continue to yield encouraging results.

I am particularly pleased with our efforts to create a transformedorganisation. Our Historically Disadvantaged South Africanrepresentation at management level in Lonmin is now at 52.3%versus the Mining Charter’s required target of 40%.

Pleasingly, our focus on continuous improvement initiatives hasresulted in a downward trend in energy consumption per PGMounce, critical to the energy challenges in South Africa.

Many of the challenges we share with the wider industry arelinked to the broader systemic socioeconomic problems inSouth Africa. While we remain absolutely committed to playingour part in delivering changes and improvements to the extentthat our resources allow, it is only by working in partnership withall stakeholders – both state and-non state – that we can reallybegin to address these issues.

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 05Lonmin PlcAnnual Report and Accounts 2016

Since the period end, we announced the acquisition of AngloAmerican Platinum’s 42.5% stake in Pandora Joint Venture,bringing Lonmin’s total ownership of the asset to 92.5%. Thisacquisition allows us to consolidate our position in this relativelyshallow and high grade mineral resource providing an attractiveoption for development by Eastern Platinum Limited in both theshort and longer term.

The year saw two Board changes. First the appointment ofKennedy Bungane as a Non-Executive Director. Kennedy isCEO of Phembani Group Proprietary Limited, which mergedwith Lonmin’s Black Economic Empowerment partnerShanduka Group (Proprietary) Limited (Shanduka). Kennedyhas a wealth of corporate experience and his appointment is inline with our original contractual arrangements with Shanduka.

In May, Simon Scott stepped down as Chief Financial Officerand as a Director of the Company. We wish Simon everysuccess in the future and thank him for his contribution to thebusiness over what was a very challenging period.

We were delighted to be able to welcome Barrie van der Merweas Simon’s replacement and as a member of the Board. Barriehas brought with him extensive knowledge and experience ofthe mining industry and the South African business environmentand has already made a significant contribution to the business.

As always, the Board is under constant review to ensure thatan acceptable balance of individuals is maintained and thatthe collective skills and experience of its members continueto be refreshed.

Looking at the year as a whole, I am pleased to be able toreport that Lonmin has now strengthened its ability to deal withthe difficult market conditions which are being experienced bythe PGM sector. There is still much to do but the Board and ourExecutive Management are concentrating their efforts to ensurethat your Company achieves its targeted objectives over themedium term to ensure sustainability and preserve long-termvalue for our shareholders. It is a challenging journey, but ourprogress this year reinforces our confidence. We continue toexplore options to create value for our shareholders, with theinitiation of the Bulk Tailings Treatment project, the sale of ourstake in a non-core gold exploration joint venture in Kenya andthe Pandora acquisition being excellent examples of what hasbeen achieved in this regard so far.

Your Board cannot recommend a dividend for the year, but myfellow Directors and I would like to thank all our shareholders fortheir continued support. I would also like to extend my thanksto my colleagues on the Board, our management team and allour workforce.

Yours faithfully,

Brian BeamishChairman

“Our structural and strategicchanges stabilised thebusiness, generated cashand have opened upopportunities to maximisefurther shareholder value.”

Ben MagaraChief Executive Officer

/ 06 Lonmin PlcAnnual Report and Accounts 2016

Chief ExecutiveOfficer’s Letter

Dea r Fellow Sha reholder,Improving cash and liquidity were our priorities for 2016 andthese results demonstrate good progress in these two areas.After our Rights Issue which strengthened our balance sheetand the renewal of our bank facilities, we delivered on ourpromises to our shareholders:

maintaining a strict focus on cash, which ensured that for•the three quarters following the successful reorganisationof the business we were cash flow positive after capitalexpenditure and improved operating profit to $7 million,from a loss of $134 million in 2015;

increasing our net cash position from $69 million with•total liquidity of $422 million at the end of quarter one, to$173 million with total liquidity of $537 million at the year end;

reducing costs by R1.3 billion, 86% higher than our target•as well as contained capital expenditure;

timely conclusion of a multi-year wage agreement; and•

preserving Immediately Available Ore Reserves, at•22.4 months, giving us operational flexibility.

Our structural and strategic changes stabilised the business,generated cash and have opened up opportunities to maximisefurther shareholder value. Our improving cash position and liquidityshows that we have repositioned the Company. Supported byour long-life, shallow ore resources, I am confident that we arecapable of meeting the immediate challenges and equipped totake advantage of any continued market improvement.

Safety is essential for good performance and remains our priority.With regret I confirm that Zilindile Ndumela, Goodman Mangisa,Fanelekile Giyama and Siphilo Makhende were fatally injuredduring the year. Our condolences go to their families and lovedones. Overall Lost Time Injury Frequency Rate improved by 8.1%.We remain determined to better our overall safety performanceand have further enhanced our focus on safety improvements.I absolutely believe Zero Harm is realistic and achievable.

Reorganisation

The reorganisation of the Group, in line with the Business Plan,was successfully completed in the first half of the year with atotal of 5,433 employees and contractors leaving the businessbetween 30 June 2015 and 31 March 2016. A further 1,428employees were reskilled and redeployed into vacant, moreproductive roles. The reorganisation, whilst successful in beingcompleted without business interruptions, did nonethelesshave a disruptive impact on mining production, with totaltonnes mined falling below our ambitious Business Plan target.

As the disruption created by the rationalisation process settlesdown, we expect the mining teams to start to improve levelsof production. Additionally, a number of initiatives have beenactioned to support the achievement of planned output for 2017.

Performance

Despite the reorganisation, we achieved Platinum sales of735,747 ounces, exceeding our guidance of 700,000 Platinumounces, assisted by the impressive efforts of our Processingteam, which released 73,186 Platinum ounces from the smelterclean-up project and metal release from our new Other PreciousMetals Plant (OPM). I would like to praise the Processing team’sentrepreneurial approach and high performance culture.

We mined a total of 10.3 million tonnes, a decrease of 8.8%on 2015, reflecting the planned decline in production from ourolder Generation 1 shafts, which are being wound down aspart of our strategy to reduce high cost production. 2016 sawthe orderly closure of our 1B shaft and the cessation of ownproduction from Newman shaft.

Tonnes mined from our core Generation 2 shafts were up 4.0%on a comparable basis. Saffy shaft, which is now operating atfull production, performed notably well, offsetting the weakerperformance of K3 and Rowland shafts, which were affected bythe redeployment and reskilling of employees; absenteeism ofkey personnel; and higher incidents of safety stoppages in thefirst nine months of the year. Productivity at our Generation 2shafts increased 5.4% to a five year high of 5.9 square metersper person.

We made efforts to improve the performance of our processingplants over recent years and the concentrators have achievedlevels of PGM recoveries amongst the highest in their history.We continue to pursue various initiatives to utilise our excessprocessing capacity; the Bulk Tailings Treatment (BTT) projectbeing an example of this.

Cash and Liquidity, Profitability, Cost Savings andCapital expenditure

The reorganisation resulted in the business delivering underlyingoperating profit of $7 million compared to underlying loss of$134 million in 2015 and meant the business was cash positiveafter capital expenditure for the last three quarters of the year.Our net cash position increased to $173 million (R2.4 billion)with total liquidity of $537 million (R7.5 billion) at the year end.We benefited from a cash flow injection of circa R350 million(around $24 million) realised from permanently reducing our metalin process stock following the commissioning of the OPM Plant.

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 07Lonmin PlcAnnual Report and Accounts 2016

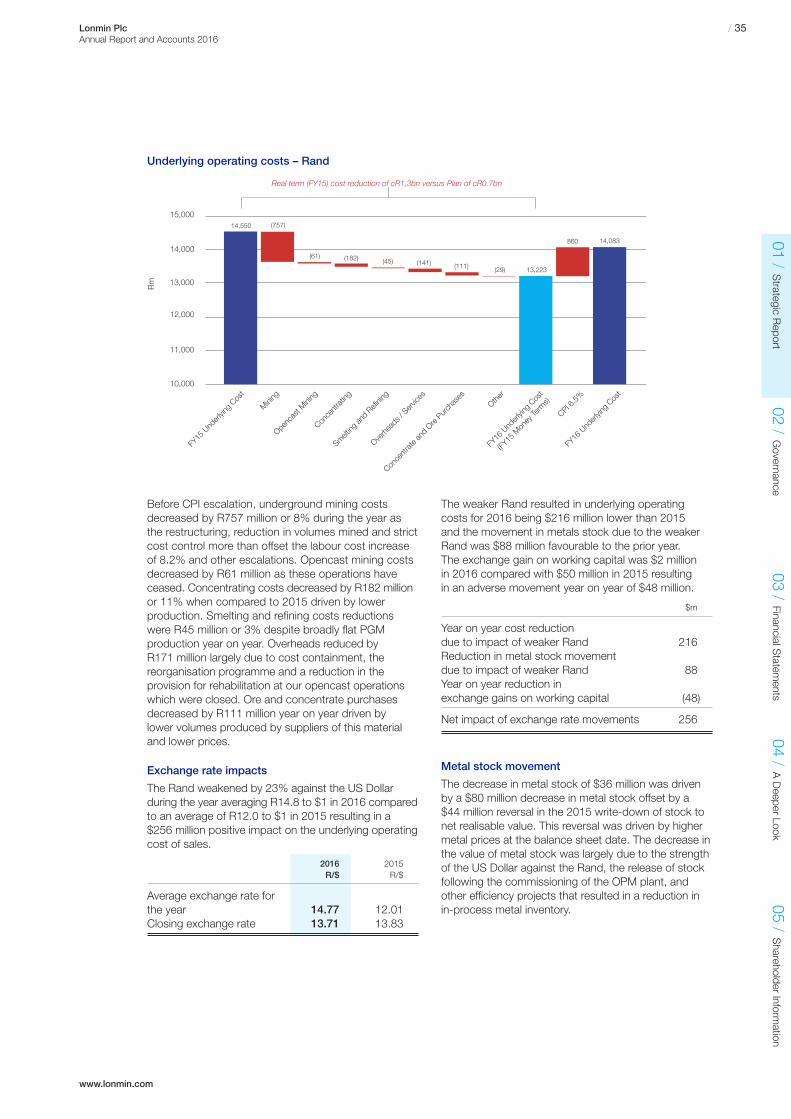

Underlying costs decreased by 3.2% to R14.1 billion. Wedelivered cost reductions of R1.3 billion (in real terms) over thecourse of the year, which was 86% ahead of our Business Plantarget of R700 million.

We contained unit costs to R10,748, a 4.0% increase yearon year, in spite of the 8.2% increase in labour wages and thedisruption from the reorganisation, which was marginally aheadof the revised guidance provided in our Q3 production report.The increase reflects the production challenges experienced in ourmining operations, where the majority of our costs are incurred,highlighting a need to build on our productivity improvements.

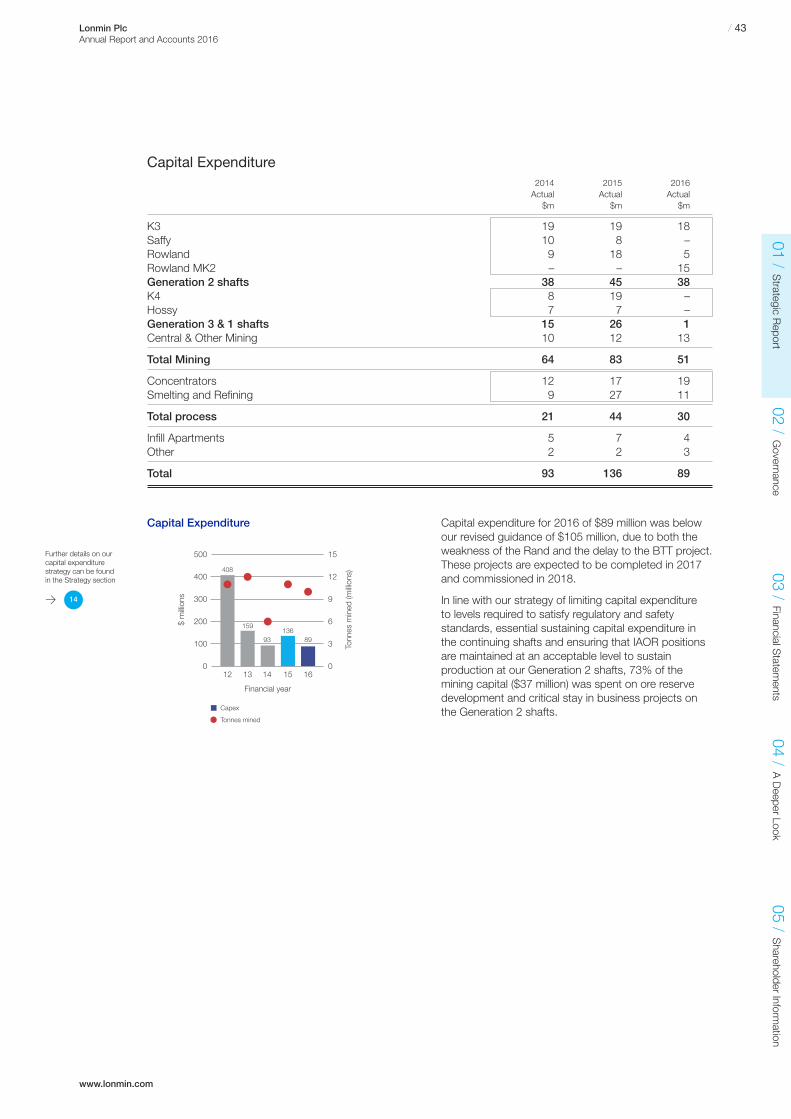

Capital expenditure was contained to $89 million, less thanour revised guidance of $105 million due to the delay of theBTT project. During 2016, $50 million competitive third partyfunding was secured for our BTT project with the first trancheof $9 million received in the fourth quarter.

During the year an impairment charge of $335 million wasincurred, reflecting the weakened rhodium price long-termoutlook and strengthened Rand to US Dollar exchange ratein the second half.

Wage Settlement

On 31 October, we announced our agreement with Associationof Mineworkers and Construction Union (AMCU) on wages andconditions of service. The agreement, effective from 1 July 2016to 30 June 2019, provides employees with a realistic andcompetitive outcome and was negotiated without any businessinterruptions, demonstrating the reducing risk in this area. The impact of this is an average annual increase of 7.6%.

Bapo Ba Mogale

Four contracts were awarded to the Bapo Ba Mogale (Bapo)under the terms of the 2014 Transaction and have beenimplemented. The award of these contracts has resulted inLonmin far exceeding the procurement undertakings given tothe Bapo. Our relationship with the Bapo continues to evolve aswe support them to build capacity and governance structureswithin their organisation.

Pandora

On 11 November, we entered into a sale and purchase agreementto acquire Anglo American Platinum’s (AAP) 42.5% stake inPandora, bringing our total ownership in the asset to 92.5%.The acquisition, for a minimum of R400 million (nominal terms)and a maximum of R1 billion, over six years, increases ourexposure to an asset with good long-term developmentpotential. The Pandora Joint Venture made an operating loss ofR109 million in 2016, with Lonmin’s 50% share being reflectedin these accounts. However, Lonmin received a contribution ofR117 million from ore purchase agreements, which offsets thejoint venture loss. Adjacent to our Saffy shaft, Lonmin expectsto be able to access additional ounces without having to incurfurther capital expenditure, allowing us to defer capital todeepen the Saffy shaft. Additionally, Lonmin will realise anannual rental fee of approximately R46 million, for a three-yearperiod, from AAP for the use of the Baobab concentrator inLimpopo. The transaction is expected to become unconditionalduring 2017 following the fulfilment of all conditions precedent.

The Market

During the year, the PGM pricing environment remained weakalthough the platinum market deficit has widened. In theshort-term we expect markets to remain subdued, howeverwe still believe the long-term market fundamentals are strong.

PGMs have a vital role to play as we move towards a greenerglobal economy. Platinum and palladium’s role in reducing harmfulemissions remains key and is of growing relevance for developingmarkets, which are increasingly adopting more stringentemissions standards. Growth in jewellery demand from India andthe United States has recently offset the slowdown in Chinaand we believe the drivers of platinum investment and demandare robust. When market sentiment improves, I am confident thatwe will see an improvement in platinum prices primarily becauseof the extended under-investment in the primary supply.

Outlook

We expect Platinum sales for 2017 to be between 650,000 and680,000 ounces which takes into account the positive impactof various initiatives such as the smelter clean-up. We remainvigilant in our cost control and expect our overheads andsupport services structures to align with our sales profile.Unit costs will remain under pressure until we see a sustainedimprovement in production throughput from mining and areexpected to be in the range of R10,800 to R11,300 per PGMounce. Like costs, our capital expenditure is predominantlyincurred in Rands. Therefore, going forward, our capitalexpenditure guidance will be provided in Rands rather thanUS Dollars. Our 2017 guidance is approximately R1.8 billion;the increase on previous guidance reflects the delay to theBTT project which is third party funded and accounts forR400 million. Capital expenditure will be maintained at theminimum level required for the safe and efficient running ofthe Group’s operating, as we continue to focus on our aimof being cash positive after capital expenditure.

Conclusion

Today, the business is well positioned with disruption fromthe reorganisation process reducing. The Mining Division hasstabilised following the reorganisation and is in a strong positionto move forward. We are focused on our core Generation 2shafts. We are well placed to drive essential and sustainedimprovements in productivity and a number of initiatives havebeen implemented to address mining’s performance. Gettingprofitable ounces out of the ground is an essential priority.

The work we do would not be possible without our employees.We continue on our journey to improve their wellbeing andfinancial literacy and have been encouraged by the results ofthe initiatives we put in place to achieve this. Our employeesdeserve decent living standards and must have a choice ofhow and where they want to live. Achieving our vision forsustainable, integrated settlements requires careful planning,consultation and coordination between all stakeholders –employees themselves, communities, potential funders,developers, unions, local municipalities and Government.To this end, Lonmin and its organised labour are reviewingemployee living standards as part of the human settlementsstrategy, which should realise a tactical plan that addressesemployees’ wishes, needs, security and affordability to ensurea fit-for-purpose and decent standard of living.

We have come a long way during 2016. I am particularlypleased with our return to profitability and the increase in ourcash position and liquidity. We are now well positioned toexplore options to maximise value for our shareholders andall our stakeholders; the acquisition of Pandora being a goodexample of this.

Yours faithfully,

Ben MagaraChief Executive Officer

/ 08 Lonmin PlcAnnual Report and Accounts 2016

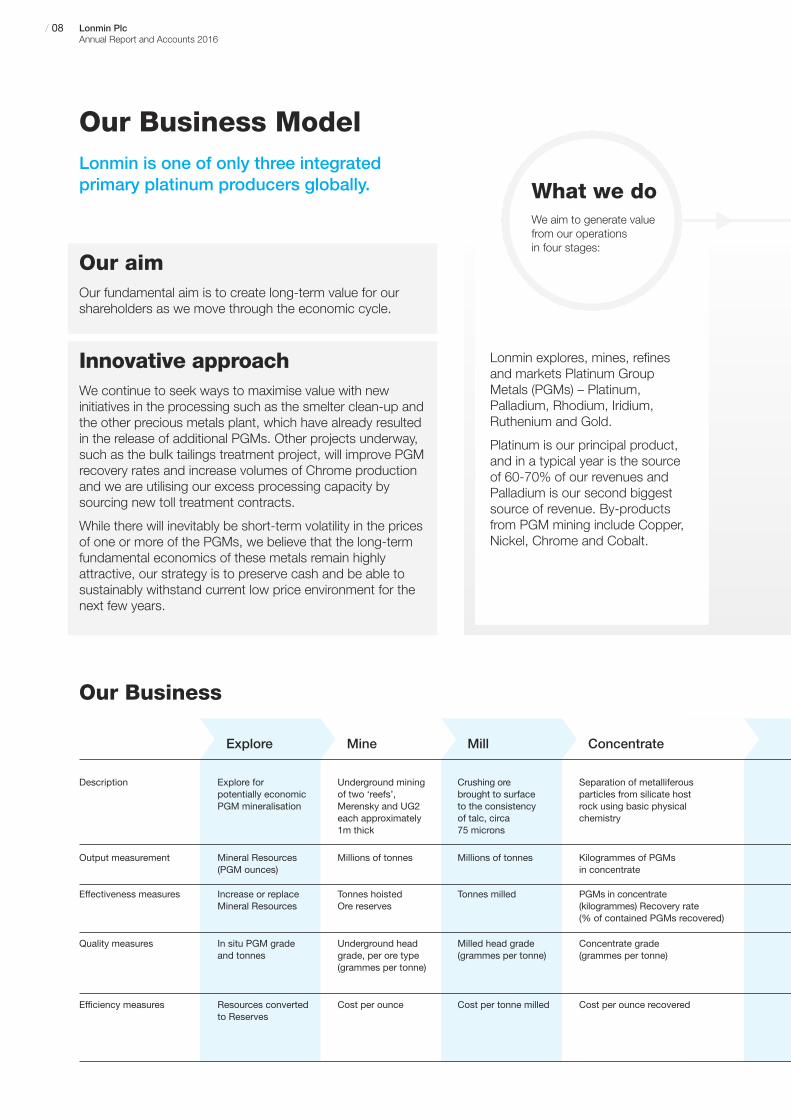

Our Business ModelLonmin is one of only three integratedprimary platinum producers globally.

Our aimOur fundamental aim is to create long-term value for ourshareholders as we move through the economic cycle.

Innovative approachWe continue to seek ways to maximise value with newinitiatives in the processing such as the smelter clean-up andthe other precious metals plant, which have already resultedin the release of additional PGMs. Other projects underway,such as the bulk tailings treatment project, will improve PGMrecovery rates and increase volumes of Chrome productionand we are utilising our excess processing capacity bysourcing new toll treatment contracts.

While there will inevitably be short-term volatility in the pricesof one or more of the PGMs, we believe that the long-termfundamental economics of these metals remain highlyattractive, our strategy is to preserve cash and be able tosustainably withstand current low price environment for thenext few years.

Lonmin explores, mines, refinesand markets Platinum GroupMetals (PGMs) – Platinum,Palladium, Rhodium, Iridium,Ruthenium and Gold.

Platinum is our principal product,and in a typical year is the sourceof 60-70% of our revenues andPalladium is our second biggestsource of revenue. By-products from PGM mining include Copper,Nickel, Chrome and Cobalt.

Our Business

MineExplore Mill Concentrate

Description Underground miningof two ‘reefs’,Merensky and UG2each approximately1m thick

Crushing orebrought to surfaceto the consistencyof talc, circa75 microns

Separation of metalliferousparticles from silicate hostrock using basic physicalchemistry

Output measurement Millions of tonnes Millions of tonnes Kilogrammes of PGMsin concentrate

Effectiveness measures Tonnes hoistedOre reserves

Tonnes milled PGMs in concentrate(kilogrammes) Recovery rate(% of contained PGMs recovered)

Quality measures Underground headgrade, per ore type(grammes per tonne)

Milled head grade(grammes per tonne)

Concentrate grade(grammes per tonne)

Efficiency measures Cost per ounce Cost per tonne milled Cost per ounce recovered

Explore forpotentially economicPGM mineralisation

Mineral Resources(PGM ounces)

Increase or replaceMineral Resources

In situ PGM gradeand tonnes

Resources convertedto Reserves

What we doWe aim to generate valuefrom our operationsin four stages:

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 09Lonmin PlcAnnual Report and Accounts 2016

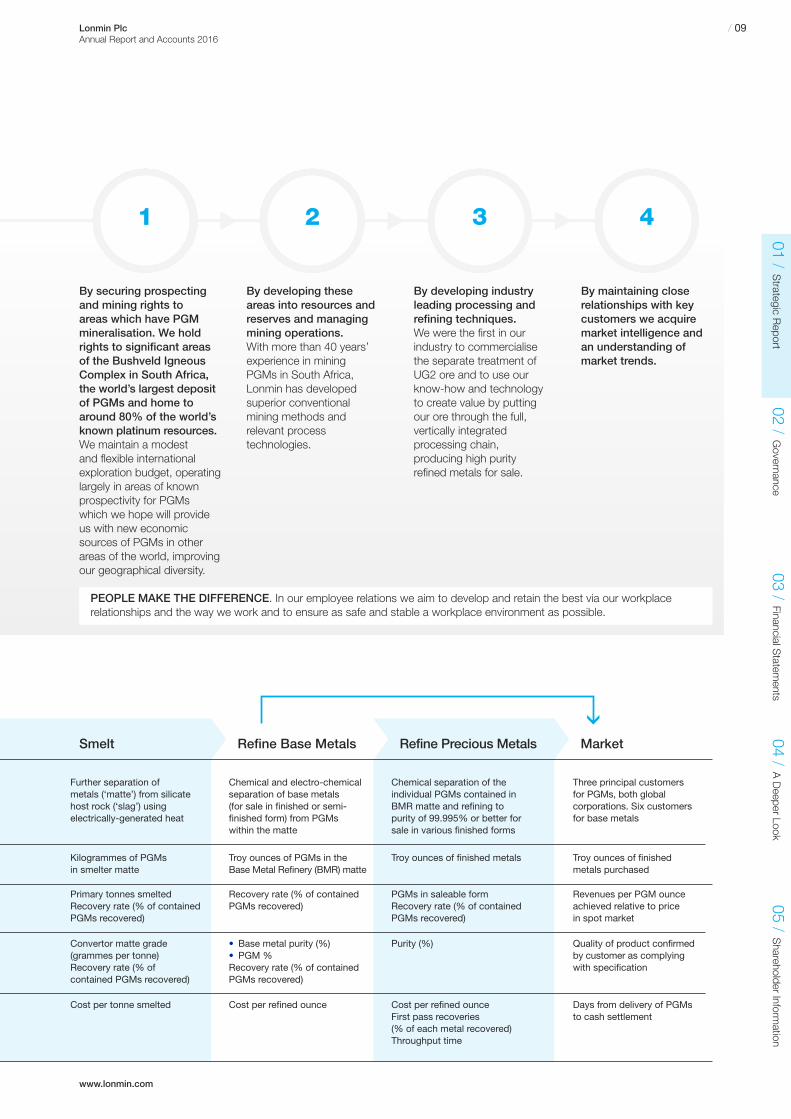

1 2 3 4

By developing theseareas into resources andreserves and managingmining operations.With more than 40 years’experience in miningPGMs in South Africa,Lonmin has developedsuperior conventionalmining methods andrelevant processtechnologies.

By developing industryleading processing andrefining techniques.We were the first in ourindustry to commercialisethe separate treatment ofUG2 ore and to use ourknow-how and technologyto create value by puttingour ore through the full,vertically integratedprocessing chain,producing high purityrefined metals for sale.

By maintaining closerelationships with keycustomers we acquiremarket intelligence andan understanding ofmarket trends.

PEOPLE MAKE THE DIFFERENCE. In our employee relations we aim to develop and retain the best via our workplacerelationships and the way we work and to ensure as safe and stable a workplace environment as possible.

Smelt Refine Base Metals Refine Precious Metals Market

By securing prospectingand mining rights toareas which have PGMmineralisation. We holdrights to significant areasof the Bushveld IgneousComplex in South Africa,the world’s largest depositof PGMs and home toaround 80% of the world’sknown platinum resources.We maintain a modestand flexible internationalexploration budget, operatinglargely in areas of knownprospectivity for PGMswhich we hope will provideus with new economicsources of PGMs in otherareas of the world, improvingour geographical diversity.

Further separation ofmetals (‘matte’) from silicatehost rock (‘slag’) usingelectrically-generated heat

Chemical and electro-chemicalseparation of base metals(for sale in finished or semi-finished form) from PGMswithin the matte

Chemical separation of theindividual PGMs contained inBMR matte and refining topurity of 99.995% or better forsale in various finished forms

Three principal customersfor PGMs, both globalcorporations. Six customersfor base metals

Kilogrammes of PGMsin smelter matte

Troy ounces of PGMs in theBase Metal Refinery (BMR) matte

Troy ounces of finished metals Troy ounces of finishedmetals purchased

Primary tonnes smeltedRecovery rate (% of containedPGMs recovered)

Recovery rate (% of containedPGMs recovered)

PGMs in saleable formRecovery rate (% of containedPGMs recovered)

Revenues per PGM ounceachieved relative to pricein spot market

Convertor matte grade(grammes per tonne)Recovery rate (% ofcontained PGMs recovered)

• Base metal purity (%)• PGM %Recovery rate (% of containedPGMs recovered)

Purity (%) Quality of product confirmedby customer as complyingwith specification

Cost per tonne smelted Cost per refined ounce Cost per refined ounceFirst pass recoveries(% of each metal recovered)Throughput time

Days from delivery of PGMsto cash settlement

Preserving our ValuesWe preserve and protect this value creation potential in five ways:

Governance

We have created andmaintain a robustinternal control andreporting environment,with strong processesfor risk identification andmitigation, implementedby a dynamicmanagement team and overseen by anexperienced Board of Directors;

Read more onGovernance on pages

> 54

Culture

We are seeking todevelop a value basedculture where thebehaviour of allemployees, managers,Directors and othershelps to promote anethical, responsible andfair approach to how we do business;

Read more onCulture on pages

> 16

Relationships

We work hard atestablishingrelationships with a widerange of stakeholdersfrom employees andtheir trades unions,through communitiesand local government,suppliers, contractors,customers and otherbusiness counterparties,to national governmentin its many guises andthe providers of ourfunding – lending banksand our shareholders;

Read more onRelationships on pages

> 15

Sustainability

We believe that there isonly one way to sustainsuccess, by taking allcritical risks into accountwhen we are planningahead. Working safely,respecting those withwhom we work andprotecting theenvironment are all partof our core processes;and

Read more onSustainability on pages

> 44

Transformation

We embracetransformation as abusiness imperative. We endeavour to playour full part inaddressing historicinequalities and creatingthe conditions in whichcurrent and futuregenerations cansucceed in creating a shared purpose.

Read more onTransformation on page

> 16

/ 10 Lonmin PlcAnnual Report and Accounts 2016

Our Business Model (continued)

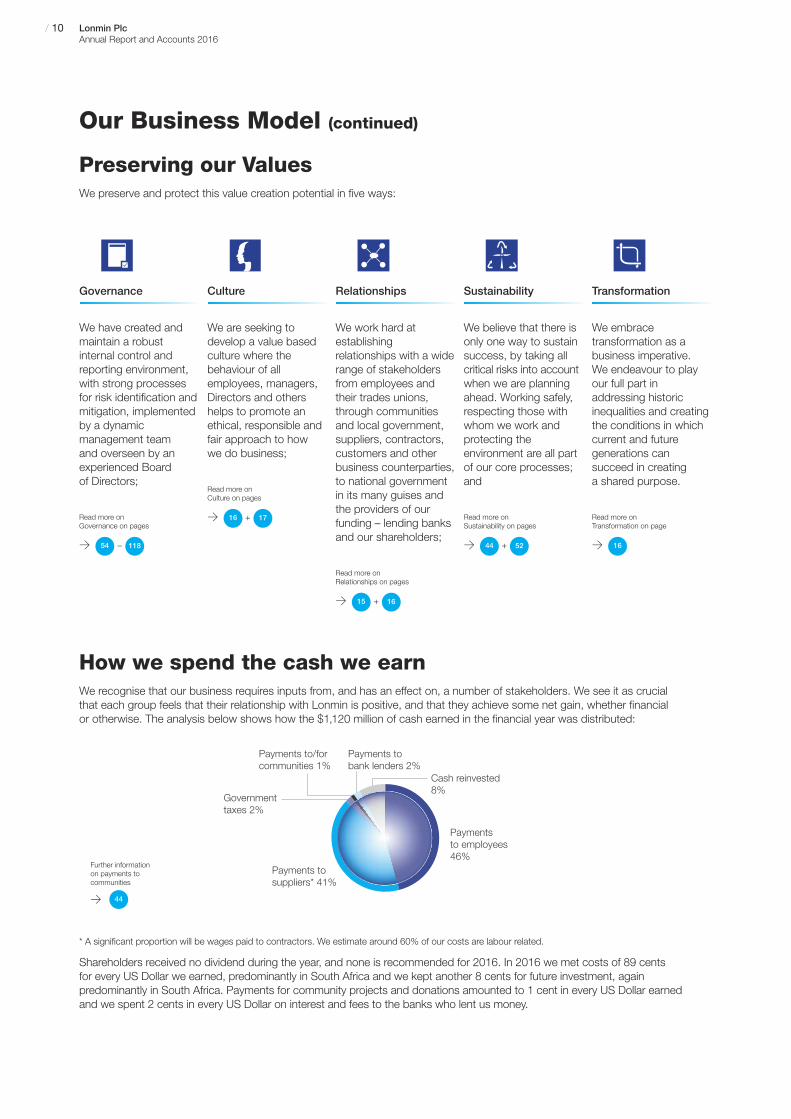

How we spend the cash we earnWe recognise that our business requires inputs from, and has an effect on, a number of stakeholders. We see it as crucialthat each group feels that their relationship with Lonmin is positive, and that they achieve some net gain, whether financial or otherwise. The analysis below shows how the $1,120 million of cash earned in the financial year was distributed:

* A significant proportion will be wages paid to contractors. We estimate around 60% of our costs are labour related.

Shareholders received no dividend during the year, and none is recommended for 2016. In 2016 we met costs of 89 centsfor every US Dollar we earned, predominantly in South Africa and we kept another 8 cents for future investment, againpredominantly in South Africa. Payments for community projects and donations amounted to 1 cent in every US Dollar earnedand we spent 2 cents in every US Dollar on interest and fees to the banks who lent us money.

Cash reinvested8%

Paymentsto employees46%

Payments tosuppliers* 41%

Governmenttaxes 2%

Payments tobank lenders 2%

Payments to/forcommunities 1%

> 44

Further information on payments tocommunities

16+

52+118–

17+

Background

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 11Lonmin PlcAnnual Report and Accounts 2016

Our Strategy

At least 70% of platinum and rhodium supply is producedin South Africa, and Lonmin is one of only three integratedprimary PGM producers globally.

Quality asset base; large long-life reserves

The Group’s mineral resources provide a source ofsupply that is expected to last for decades at currentand anticipated future rates of mining of between600,000 – 700,000 Platinum ounces per annum. As at 30 September 2016, the Group’s mineral reserves and mineral resources were as follows:

(in Moz) 3PGE + Au(*1) Pt

Proved 2.3 1.4Probable 29.4 17.8

Total Mineral Reserves 31.7 19.2

Measured 7.3 4.6Indicated 102.6 56.7Inferred 70.7 39.7

Total Mineral Resources (*2) 180.6 101.0

(*1) – 3PGE + AU means Platinum, Palladium, Rhodium and Gold

(*2) – Resources are reported inclusive of reserves

The Western Limb of the Bushveld Igneous Complexcontains two economic sources of PGM bearing orethat occur as stratified layers, or ‘reefs’; UG2 andMerensky. While the ratio of platinum to other PGMs inthe two reefs is broadly similar, UG2 ore in the Group’sprincipal mining areas in the Bushveld Igneous Complexis generally of a higher grade than Merensky ore, andoccurs over a greater width, making this ore moreeconomic to extract, with a lower risk of dilution bymining waste material from above or below the payablereef. We will continue to predominantly mine the UG2reef rather than the Merensky reef, as we have over thelast twenty years, with UG2 ore typically comprisingapproximately 70 to 75% of the Group’s total production.

Low cost and shallow mining operations

Our mining operations at an average depth of 600metres below surface are shallower than the industryaverage of 900-1000 metres below surface with a wideUG2 reef averaging 124 cm, minimising dilution.

Marikana has a diverse portfolio of shafts at differentstages of their life cycle, which are split into threecategories, namely Generation 1, 2 and 3 shafts. TheGeneration 1 shafts are smaller, older shafts in the latterstages of their operational life. As detailed in the BusinessPlan outlined at the time of our Rights Issue, ourHossy shaft, previously a Generation 2 shaft, has beenreclassified as a Generation 1 shaft, and remains ontarget for planned closure in 2017. The Generation 2shafts are our larger, long-life and newer shafts. OurGeneration 3 vertical shaft, K4, continues to offerbrownfield replacement optionality for the Group andrepresents one of the most capital efficient projects.It currently remains on care and maintenance.

Optionality

In the longer term, the Directors believe the Group hasa number of attractive brownfield expansion opportunitiesthat could potentially be developed when the PGMpricing environment improves, including the K4 shaft,the Rowland MK2 resources, opening up of furtherlevels of Saffy shaft, the Pandora E3 deepening projectand E4 Pandora project. The Limpopo operations,currently on care and maintenance, also offer a uniqueopportunity to develop what the Directors believe to bea sizeable mechanised operation in a sustained higherprice environment. In addition, the Akanani Mining (Pty)Limited (Akanani) project offers the prospect of a large,long-life, low cost and highly mechanised mine whichgives us optionality in the long-term.

We sold our stake in a non-core gold exploration jointventure in Kenya for $5 million during the year, butthrough our joint ventures with Vale S.A. and WallbridgeMining Company Limited, we retain our internationalexploration projects in Canada. Limited work alsocontinues on the exploration licences that we hold inNorthern Ireland. While our international projects offeran opportunity of competitive advantage and areshallow or highly mechanisable, in line with theBusiness Plan, allocation of funds to such projects isrestricted and consequently activity will remain minimalon these projects through financial year 2017.

/ 12 Lonmin PlcAnnual Report and Accounts 2016

Our Strategy (continued)

Much has been achieved and the Company is nowwell positioned for upturn and to maximise value forshareholders. In the long-term, our strategy is togenerate value from our mine-to-market businessby utilising our value chain, especially our processinginfrastructure and capabilities.

Our strategy focuses on the following four pillars whichtake into account our responsibilities around social andcommunity investment:

1) Operational Excellence;

2) Enhance balance sheet strength;

3) Our People and Relationships; and

4) Our Corporate Citizenship Agenda.

The end of 2015 saw the implementation of ourBusiness Plan, the amending of our debt facilities andthe undertaking of a Rights Issue to strengthen theGroup’s balance sheet. These actions were designedto enable the Group to operate in the low PGM pricingenvironment, whilst at the same time preserving itslong-term value.

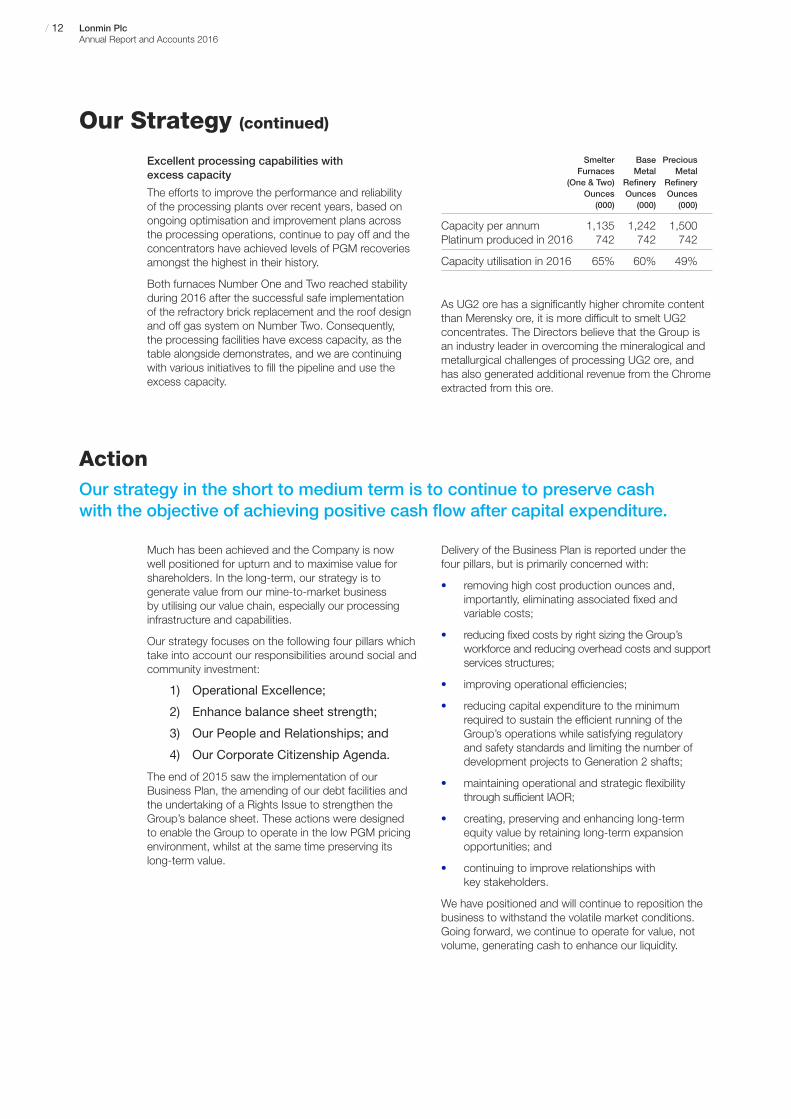

Excellent processing capabilities withexcess capacity

The efforts to improve the performance and reliabilityof the processing plants over recent years, based onongoing optimisation and improvement plans acrossthe processing operations, continue to pay off and theconcentrators have achieved levels of PGM recoveriesamongst the highest in their history.

Both furnaces Number One and Two reached stabilityduring 2016 after the successful safe implementation of the refractory brick replacement and the roof designand off gas system on Number Two. Consequently,the processing facilities have excess capacity, as thetable alongside demonstrates, and we are continuingwith various initiatives to fill the pipeline and use theexcess capacity.

Smelter Base PreciousFurnaces Metal Metal

(One & Two) Refinery RefineryOunces Ounces Ounces(000) (000) (000)

Capacity per annum 1,135 1,242 1,500Platinum produced in 2016 742 742 742

Capacity utilisation in 2016 65% 60% 49%

As UG2 ore has a significantly higher chromite contentthan Merensky ore, it is more difficult to smelt UG2concentrates. The Directors believe that the Group isan industry leader in overcoming the mineralogical andmetallurgical challenges of processing UG2 ore, andhas also generated additional revenue from the Chromeextracted from this ore.

Delivery of the Business Plan is reported under thefour pillars, but is primarily concerned with:

removing high cost production ounces and,•importantly, eliminating associated fixed andvariable costs;

reducing fixed costs by right sizing the Group’s•workforce and reducing overhead costs and supportservices structures;

improving operational efficiencies;•

reducing capital expenditure to the minimum•required to sustain the efficient running of theGroup’s operations while satisfying regulatoryand safety standards and limiting the number ofdevelopment projects to Generation 2 shafts;

maintaining operational and strategic flexibility•through sufficient IAOR;

creating, preserving and enhancing long-term•equity value by retaining long-term expansionopportunities; and

continuing to improve relationships with•key stakeholders.

We have positioned and will continue to reposition thebusiness to withstand the volatile market conditions.Going forward, we continue to operate for value, notvolume, generating cash to enhance our liquidity.

ActionOur strategy in the short to medium term is to continue to preserve cashwith the objective of achieving positive cash flow after capital expenditure.

1. Operational Excellence

Our main priority remains the performance of our Marikana operations which are some of the best in the industry, interms of quality, safety and efficiency. We believe our Marikana operations remain amongst the best hard rock narrowtabular mining operations in the Western Limb.

Profitability and returns are crucial. The Group is highly geared to the PGM pricing environment and the Rand / US Dollarexchange rate. We operate for value, not for volume. Given the present PGM market, we believe that the priority in theshort-term is to make sustainable improvements in productivity and cash and bolster liquidity.

To improve cash margins, we strive to ensure that our core Generation 2 shafts reach the most efficient and profitablepositions in terms of safety, costs, production and productivity as the Generation 1 shafts reach the end of their lives.

Safety•

Safety remains at the heart of all that we do. Our ambition to achieve Zero Harm starts with the safety, health and wellbeing of our employees and extends to everything we do including minimising the environmental impact of our operations.

Our approach to safety is defined in the Lonmin Safety and Sustainable Development Policy, Sustainable DevelopmentStandards and the Fatal Risk Control Protocols and the Lonmin Mining Life Rules, a set of non-negotiable rules thattarget the risk areas responsible for the majority of fatal or serious accidents.

Removing high cost production ounces•

The Business Plan accelerates our core strategy of focusing on our larger Generation 2 shafts and will result ina reduction of the sales profile for the Group to approximately 650,000 – 680,000 Platinum ounces for 2017 ashigh-cost production continues to be wound down. Our guidance has been revised upwards marginally to accountfor initiatives like the smelter clean-up.

The closure of inefficient areas and shafts will continue through 2017. As previously noted, our Hossy shaft remainson track for planned care and maintenance closure in 2017. Our Newman shaft has now ceased production fromLonmin crews. Newman is currently being mined by contractors and future extraction of the remaining ore reservesusing contract mining will be assessed annually.

Two Generation 1 shafts, E1 and W1, were initially intended to be put on care and maintenance. These contractormanaged shafts were subsequently allowed to continue mining following a revised cash generative contractordevelopment plan and more favourable terms. These shafts continue to produce profitable ounces and, as such, are expected to remain operational under the current contractor model for financial year 2017. The viability of theseshafts is reassessed annually.

• Long-term option – remaining on care and maintenance

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 13Lonmin PlcAnnual Report and Accounts 2016

• Opencast

Generation 1

Generation 2

Generation 3

• E1, W1

• E2, E3 (incl. JV 100%)

• Newman

• 1B

• Hossy

• K3• Rowland• Saffy• 4B

• K4

8

Shafts Focus

4

4

8

8

4

4

4

4

n/a

• Merensky pit closed. UG2 low cost ounces opened –to close in 2017

Status

• Under contract mining – annual re-evaluation

• Delivering operational performance

• 1B – Closed Oct 2015. On care and maintenance

• Orderly closure and placed on care and maintenanceby end of FY17

• Continued operational performance• Continued operational performance• Continued operational performance• Continued operational performance

Tonnesmined in

2015 (’000 tonnes)

8• Lonmin own production stopped Oct 2016. Undercontract mining

Shafts of the future

230

328

1,002

765

220

2,7131,8721,7581,409

953

49

Tonnesmined in

2016 (’000 tonnes)

49

304

827

346

6

2,6871,7312,0551,588

Total Gen 2 7,7528,061

712

–

Total Gen 1/OC 3,4972,244Generation 2 contribution to total tonnes mined

Restructuring programme on track – focusing on core Generation 2 shafts in an oversupplied market

4%

36%

78% 69%

/ 14 Lonmin PlcAnnual Report and Accounts 2016

Our Strategy (continued)

1. Operational Excellence (continued)

Reducing fixed costs•

We remain vigilant in containing our costs. Overheads and support services structures are constantly reviewed toalign with the reduced sales profile.

We delivered cost reductions of R1.3 billion (in financial year 2015 money terms) over the course of 2016, which is 86%ahead of our Business Plan target of R700 million, achieved through the reduction in the size of the Group’s workforce,overhead costs and support service structures, controlling of variable cost in line with lower mining / concentratingproduction and total cost of ownership projects. However, the lower than expected output from mining, due to lowerproductivity achievements, has resulted in a downward revision of our total cost reduction target for the two-yearperiod ended 30 September 2017 from R2.3 billion to R1.8 billion in real terms.

Also reflecting the challenges experienced in achieving efficiencies and productivity improvements in the MiningDivision over the course of the year, the Group’s unit cost per PGM ounce produced exceeded our guidance.While these are industry wide issues, productivity and efficiency improvements remain key focus areas for the Groupgoing forward and a number of initiatives are already underway to address mining’s performance. We are revising theGroup’s unit cost per PGM ounce produced to a range of R10,800-11,300 for the year ended 30 September 2017and will review the guidance for 2018 in due course.

Maintaining reduced capital expenditure•

Capital expenditure will be maintained at the minimum level required for the safe and efficient running of the Group’soperations. Aligning our capital expenditure guidance with costs, this is now being provided in Rand rather than inUS Dollars. The Group expects total capital expenditure for the year ending 30 September 2017 to be increased toapproximately R1.8 billion, which includes R400 related to the BTT project, which should be sufficient to keep theGroup’s existing assets in operation and to comply with legislative, Safety, Health and Environmental and Socialresponsibility requirements without compromising our bank covenants.

The Group continues utilising capital portfolio optimisation tools with the aim of ensuring that capital expenditure isinvested only in the most cash generative development projects available to the Group with the aim of predominantlyfunding capital expenditure through free cash flow generated by operating activities.

At K3 future project capital is expected to be spent on ore reserve development to access an additional two levels(25 and 26) on the UG2 decline, whilst extraction of the Rowland MK2 UG2 resource via the existing Rowland shaftinfrastructure is anticipated to result in production from this area from 2018 onwards.

The Group’s planned capital expenditure includes the expansion capital expenditure for the BTT project. In total,approximately R400 million is included for this project in the total planned capital expenditure for the financial year 2017.

Maintaining operational and strategic flexibility•

We intend to maintain a clear strategic focus on the Group’s mineral resources, mining and processing infrastructureat Marikana. Prior investment in this area means as at 30 September 2016 the Group had IAOR equating to 22.4months of mining at planned levels of production. This provides Lonmin with a competitive advantage, givingoperational and strategic flexibility for market upturn.

Creating, preserving and enhancing long-term equity value•

We seek to identify projects which add value by making use of our excess processing capacity. As part of theseefforts, and in line with our focus on low cost ounces and near term cash, work is underway on the BTT project.Additionally, during the year, we signed a toll treating contract with Jubilee Platinum Plc, which will commence duringfinancial year 2017, producing 12,000 Platinum ounces in 2017 and 17,000 Platinum ounces per annum thereafter.

The BTT involves the re-mining of Lonmin’s Eastern Tailings Dam and the reprocessing of 26 million tonnes of tailingsmaterial at a rate of 300,000 tonnes per month. Once at steady state, the project is expected to deliver the lowestcost ounces in the Lonmin portfolio, producing about 29,000 ounces of Platinum per year or some 55,000 ouncesof PGM (from tailings with a grade of 1.42 grammes per tonne with a recovery rate of 35%). The project is expectedto be mined by a contractor over a seven-year period and to be commissioned and ramped up to full productionduring the 2018 financial year. The Chrome is expected to be recovered in a new Chrome spiral plant and the containedPGMs are expected to be recovered in the Group’s UG2 concentrator. Further to this project, there are a number ofadditional tailings dams available for life extension in the Western Dam, for potential exploitation in the future.

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 15Lonmin PlcAnnual Report and Accounts 2016

1. Operational Excellence (continued)

Creating, preserving and enhancing long-term equity value (continued)•

Post period end we announced that we had entered into a Sale and Purchase Agreement to acquire AngloAmerican Platinum’s (AAP) 42.5% stake in the Pandora Joint Venture (the Transaction). The Pandora Joint Venturemade an operating loss of R109 million in 2016, with Lonmin’s 50% share being reflected in these accounts.However, Lonmin received a net contribution of R117 million from ore purchase agreements, which offsetsthe joint venture loss. The Transaction allows Lonmin to consolidate its position in this relatively shallow andhigh-grade mineral resource, providing an attractive option for development in both the short and longer term.One of the benefits is that this will facilitate Lonmin being able to access the Pandora Joint Venture ore reserve fromour adjacent Saffy shaft. This is a low- to no- capital option to produce additional ounces and also allows us to defercapital to deepen the Saffy shaft. The Pandora Joint Venture contributed 32,509 Platinum ounces to Lonmin in the2016 financial year.

The agreement is for a deferred cash payment of 20% of the distributable free cash flows generated by the Pandora E3operations on an annual basis for a period of six years, subject to a minimum total deferred consideration of R400 million(in nominal terms) and a maximum total consideration of R1 billion (in nominal terms). AAP will also receive 20% of anyproceeds of any Pandora Joint Venture resources that are disposed of within that six year period. AAP will be grantedcontinued access to, and full operational control of our Baobab concentrator for a further period of three years from the date of completion of the Transaction. AAP will pay Lonmin, with immediate effect, an annual rental fee ofapproximately R46 million. The Transaction is expected to become unconditional during 2017 following the fulfilmentof all conditions precedent.

2. Enhance Balance Sheet Strength

At the beginning of financial year 2016, we carried out a Rights Issue and amended debt facilities to strengthen thebalance sheet.

Our stated aim at that time was to manage the business to be cash flow positive after capital expenditure whilstmaintaining optionality to grow production over time when pricing improves.

We achieved this in 2016 and intend to deliver on this going forward. Our balance sheet will be managed prudentlyand conservatively with future capital expenditure being funded from free cash flow generated by operations.

3. Our People and Relationships

Black Economic Empowerment (BEE)•

Our BEE equity ownership is at least 26% and we strive to maintain this in line with the requirements of theMining Charter.

Continuing to improve relationships with key stakeholders•

Our efforts to solidify and improve relations with our employees and their representative trade unions continue.We accept that building trust and strong relationships is a never ending journey.

We continue to enhance our role as the primary source of communication by seeking to communicate directly withemployees. We believe that this direct engagement, through the existing line management structures and periodiccommunication forums, forms part of the way we work and the basis of creating empowered, high performanceteams. Through the leadership development and team effectiveness training programmes, we continue toencourage our managers to manage this direct engagement.

Management and unions continue to engage on a regular basis at different levels to ensure timely communicationand resolution of issues at appropriate levels.

We also have regular engagement with our majority union, AMCU, in line with our Relationship Charter.

/ 16 Lonmin PlcAnnual Report and Accounts 2016

Our Strategy (continued)

3. Our People and Relationships (continued)

Transformation•

Lonmin embraces transformation as a business imperative and has made significant progress in this regard. We arecommitted to playing our part in addressing historic inequalities and creating the conditions in which current andfuture generations can succeed in creating a shared purpose. The Mining Charter requires a focus on increasing thenumber of Historically Disadvantaged South Africans (HDSAs) in management and the number of women in mining.

Transformation is monitored and overseen at Board level by the Social, Ethics and Transformation Committee.Transformation considerations are incorporated into recruitment, succession, skills development and talentmanagement functions to develop an internal pipeline of HDSAs, including women. Lonmin’s bursary and graduatedevelopment programmes prioritise HDSAs in order to build the future supply of appropriate candidates. Targetsrelating to transformation are included in the Corporate Balanced Scorecard that is used to measure performancefor the incentive scheme.

People•

Our mining model is labour intensive and our people make the difference and are the vehicle by which our strategy is effected through the day to day operations.

The Company values the contribution made by all its employees and recognises that morale and retention remainunder pressure as a result of the reorganisation and continuing cost constraints, which have limited salary increasesand development opportunities.

We believe that our employees deserve decent living standards and should have a choice of how and where theywant to live. These choices should allow for personal circumstances, affordable and market-related rates andintegration into the broader society during their employment with us. Lonmin and its organised labour are reviewingemployee living standards as part of its new human settlement strategy.

Progress against our human resources targets is measured through monthly reporting of key internal indicators aswell as integrating certain targets as part of the Lonmin corporate objectives. Lonmin’s human resources strategy,policies and procedures align with our operating country’s labour laws and other relevant frameworks, guidelines and codes of practice. These include in South Africa, the social development requirements of the Minerals andPetroleum Resource Development Act (MPRDA) that are defined in the Company’s Social and Labour Plan (SLP),the human rights provision in the International Council on Mining and Metals principles of sustainable developmentand the United Nations Global Compact.

The Company also reports to the Department of Minerals and Resources (DMR) against the broad-based economicdevelopment requirements of the Mining Charter, which include housing and living conditions, employment equityand human resource development (HRD).

As announced in October 2013, Lonmin remains committed to spending R500 million over the five-year period to2018 towards employee accommodation and community bulk services.

4. Our Corporate Citizenship Agenda

Stakeholder engagement and corporate communication•

Our business begins and ends with relationships and the quality of those relationships are central to our success andthat of our stakeholders. Genuine stakeholder engagement and relationship building has allowed us to understandstakeholder expectations and to communicate on key issues transparently, consistently and in a timely manner.

Social licence to operate•

Maintaining our social licence to operate through securing the trust and acceptance of communities andstakeholders is material as they host our operations. This is achieved through:

stakeholder engagement to ensure realistic expectations are understood and managed;•

community investment initiatives to address social issues;•

transformation initiatives to meet the Government’s social and economic development goals;•

ethical business practices that include a commitment to upholding human rights; and•

corporate and community partnerships.•

This is very much work in process and is based on an acknowledgement that trust must be restored andcommunities healed.

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 17Lonmin PlcAnnual Report and Accounts 2016

4. Our Corporate Citizenship Agenda (continued)

Social Labour Plans (SLP)•

Our commitment to corporate citizenship defines our duty to contribute to the wellbeing and development of thecommunities that host, and are affected by, our operations. This duty is formalised in the SLP obligations under the terms of our mining rights. Our broader social licence to operate depends on strong relationships with our hostcommunities. The Company’s ability to build financial capital in the long-term is critically dependent on a predictableand stable operating environment, which is only possible if we have good relationships with our immediatecommunities and labour sending areas.

Investing in the long-term social, economic and infrastructural development of our host communities translates into an investment in our current and future employee base, and ultimately is a direct investment in the sustainabilityof the mines themselves.

Human Rights•

Lonmin is committed to respecting the human rights of both its workforce and those who may be affected by its operations, and continues to seek to implement the United Nations Guiding Principles on Human Rights (the Guiding Principles) throughout its operations.

In August 2015, a human rights working group was established, comprising representatives from all areas of thebusiness including risk, security, health and safety, environment, labour, community, supply chain, legal, companysecretarial and communications.

Lonmin’s current human rights policy was adopted by the Board in November 2015. The policy is explicitly informed by the Guiding Principles, as well as the United Nations Universal Declaration of Human Rights and other international instruments. Respect for human rights is also enshrined in Lonmin’s Code of Business Ethics.

Lonmin recently commissioned a gap analysis study, which was undertaken and completed during financial year2016. This study sought to analyse Lonmin’s human rights policy and procedural framework in the context of theGuiding Principles and best practice in the mining industry. The findings are currently being assessed by the internal working group.

As part of the ongoing process, Lonmin is embarking on development of an internal human rights due diligencechecklist to help ensure full compliance with the relevant policies and systems. A pilot study, focusing on the issueof women in mining, has been commissioned and is expected to be carried out early in financial year 2017. A newhuman rights training programme in relation to the Guiding Principles is also scheduled to be rolled out to Lonmin’smanagers and executives during financial year 2017.

Modern Slavery Act and procurement•

As stated in the human rights policy, Lonmin’s human rights commitment includes a prohibition on modern slavery in all its forms, including human trafficking and forced or compulsory labour. Lonmin also seeks to ensure that itscounterparties conduct their own operations in line with these standards.

Lonmin’s vendor approval process already requires potential suppliers to answer specific questions in relation tohuman rights, including whether the supplier has its own human rights policy and whether it provides human rightstraining to its staff. In addition, the standard terms and conditions applicable to contracts with suppliers requireLonmin’s counterparties to adhere to a range of legislation relevant to human rights, including the South AfricanLabour Relations Act (66 of 1995), the Basic Conditions of Employment Act (75 of 1997), the Compensation forOccupational Injuries and Diseases Act (130 of 1993), as well as Lonmin’s own Sustainable Development Standardsand Code of Business Ethics. These acts and standards contain wide-ranging human rights stipulations, including asto health and safety at work, working hours, freedom of association, the prohibition of child labour, non-discriminationand freedom from forced labour and corporal disciplinary practices.

In addition to the above, Lonmin is currently undertaking a review of its procurement application processes, with the intention of further improving its ability to identify and exclude from its supply chain product and serviceproviders whose operations fall short of meeting Lonmin’s standards.

Further details, including the Lonmin’s human rights policy, can be found on Lonmin’s website:

www.lonmin.com

/ 18 Lonmin PlcAnnual Report and Accounts 2016

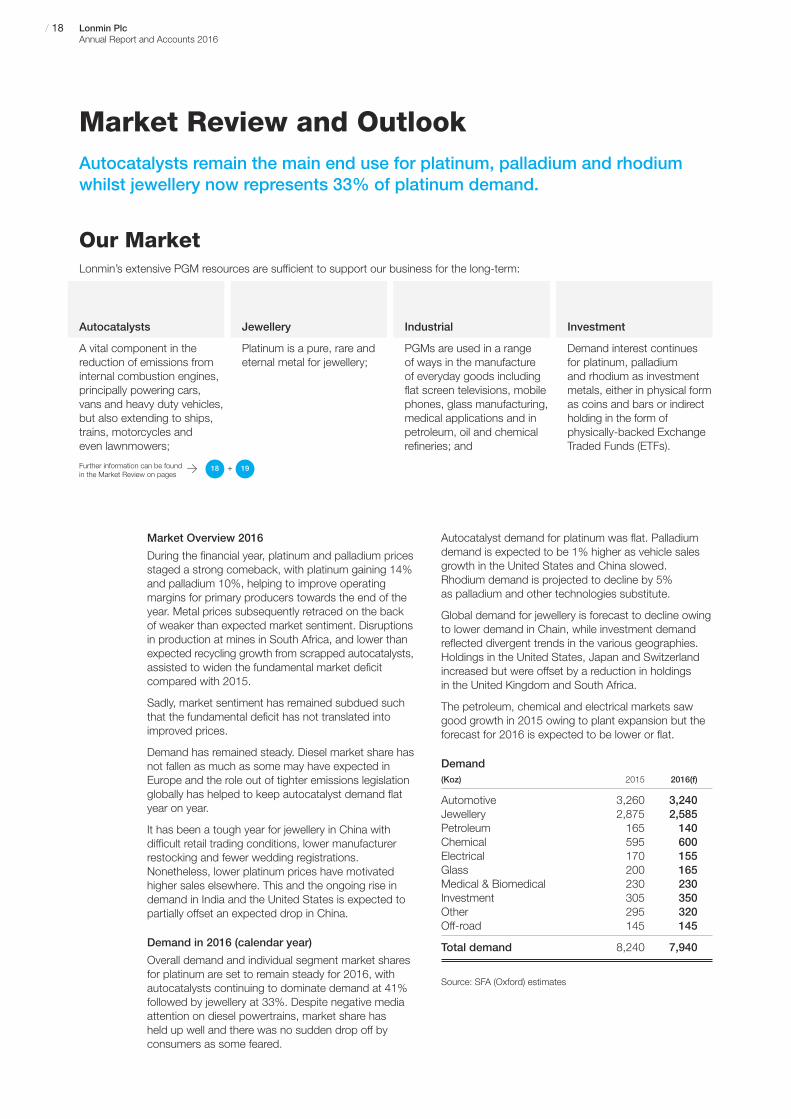

Market Review and OutlookAutocatalysts remain the main end use for platinum, palladium and rhodiumwhilst jewellery now represents 33% of platinum demand.

Our MarketLonmin’s extensive PGM resources are sufficient to support our business for the long-term:

Autocatalysts

A vital component in thereduction of emissions frominternal combustion engines,principally powering cars,vans and heavy duty vehicles,but also extending to ships,trains, motorcycles andeven lawnmowers;

Investment

Demand interest continuesfor platinum, palladiumand rhodium as investmentmetals, either in physical formas coins and bars or indirectholding in the form ofphysically-backed ExchangeTraded Funds (ETFs).

Industrial

PGMs are used in a rangeof ways in the manufactureof everyday goods includingflat screen televisions, mobilephones, glass manufacturing,medical applications and inpetroleum, oil and chemicalrefineries; and

Jewellery

Platinum is a pure, rare andeternal metal for jewellery;

Market Overview 2016

During the financial year, platinum and palladium pricesstaged a strong comeback, with platinum gaining 14%and palladium 10%, helping to improve operatingmargins for primary producers towards the end of theyear. Metal prices subsequently retraced on the backof weaker than expected market sentiment. Disruptionsin production at mines in South Africa, and lower thanexpected recycling growth from scrapped autocatalysts,assisted to widen the fundamental market deficitcompared with 2015.

Sadly, market sentiment has remained subdued suchthat the fundamental deficit has not translated intoimproved prices.

Demand has remained steady. Diesel market share hasnot fallen as much as some may have expected inEurope and the role out of tighter emissions legislationglobally has helped to keep autocatalyst demand flatyear on year.

It has been a tough year for jewellery in China withdifficult retail trading conditions, lower manufacturerrestocking and fewer wedding registrations.Nonetheless, lower platinum prices have motivatedhigher sales elsewhere. This and the ongoing rise indemand in India and the United States is expected topartially offset an expected drop in China.

Demand in 2016 (calendar year)

Overall demand and individual segment market sharesfor platinum are set to remain steady for 2016, withautocatalysts continuing to dominate demand at 41%followed by jewellery at 33%. Despite negative mediaattention on diesel powertrains, market share hasheld up well and there was no sudden drop off byconsumers as some feared.

Autocatalyst demand for platinum was flat. Palladiumdemand is expected to be 1% higher as vehicle salesgrowth in the United States and China slowed.Rhodium demand is projected to decline by 5%as palladium and other technologies substitute.

Global demand for jewellery is forecast to decline owingto lower demand in Chain, while investment demandreflected divergent trends in the various geographies.Holdings in the United States, Japan and Switzerlandincreased but were offset by a reduction in holdingsin the United Kingdom and South Africa.

The petroleum, chemical and electrical markets sawgood growth in 2015 owing to plant expansion but theforecast for 2016 is expected to be lower or flat.

Demand(Koz) 2015 2016(f)

Automotive 3,260 3,240Jewellery 2,875 2,585Petroleum 165 140Chemical 595 600Electrical 170 155Glass 200 165Medical & Biomedical 230 230Investment 305 350Other 295 320Off-road 145 145

Total demand 8,240 7,940

Source: SFA (Oxford) estimates

> 18 19+Further information can be foundin the Market Review on pages

01 /Strategic R

eport02 /

Governance

03 /Financial S

tatements

04 /A Deeper Look

05 /Shareholder Inform

ation

www.lonmin.com

/ 19Lonmin PlcAnnual Report and Accounts 2016

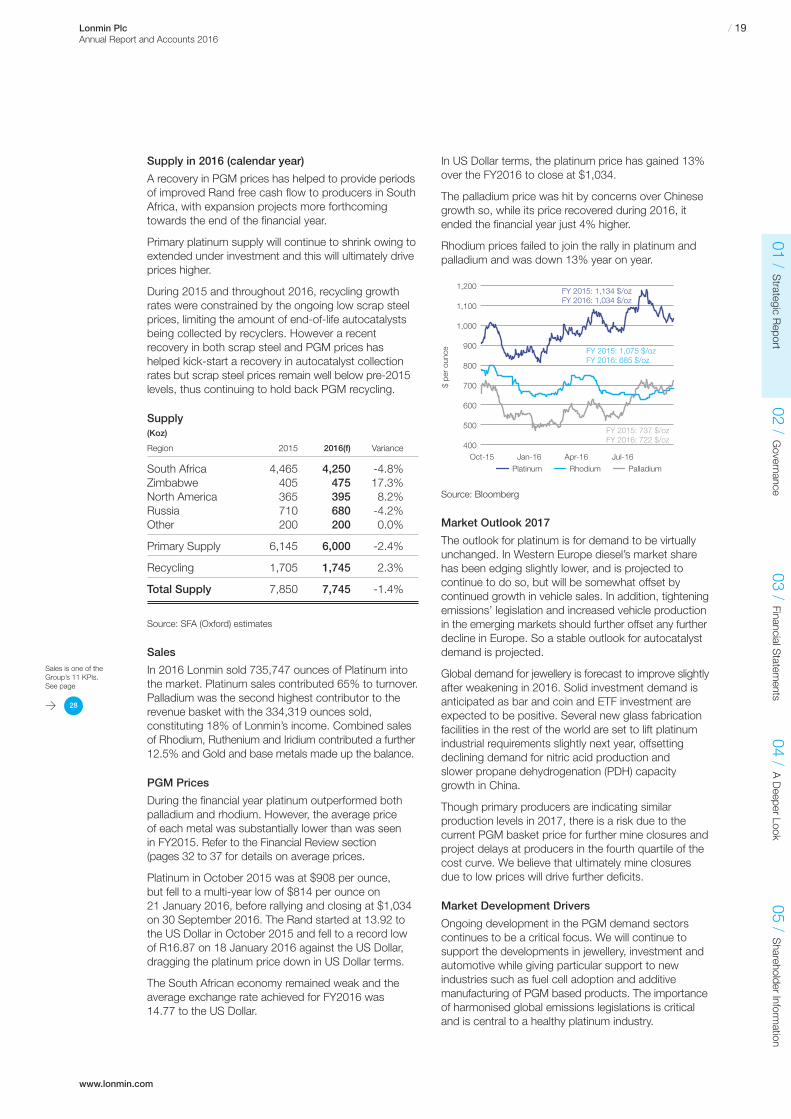

Supply in 2016 (calendar year)

A recovery in PGM prices has helped to provide periodsof improved Rand free cash flow to producers in SouthAfrica, with expansion projects more forthcomingtowards the end of the financial year.

Primary platinum supply will continue to shrink owing toextended under investment and this will ultimately driveprices higher.

During 2015 and throughout 2016, recycling growthrates were constrained by the ongoing low scrap steelprices, limiting the amount of end-of-life autocatalystsbeing collected by recyclers. However a recentrecovery in both scrap steel and PGM prices hashelped kick-start a recovery in autocatalyst collectionrates but scrap steel prices remain well below pre-2015levels, thus continuing to hold back PGM recycling.

Supply(Koz)

Region 2015 2016(f) Variance

South Africa 4,465 4,250 -4.8%Zimbabwe 405 475 17.3%North America 365 395 8.2%Russia 710 680 -4.2%Other 200 200 0.0%

Primary Supply 6,145 6,000 -2.4%

Recycling 1,705 1,745 2.3%

Total Supply 7,850 7,745 -1.4%

Source: SFA (Oxford) estimates

Sales

In 2016 Lonmin sold 735,747 ounces of Platinum intothe market. Platinum sales contributed 65% to turnover.Palladium was the second highest contributor to therevenue basket with the 334,319 ounces sold,constituting 18% of Lonmin’s income. Combined salesof Rhodium, Ruthenium and Iridium contributed a further12.5% and Gold and base metals made up the balance.

PGM Prices

During the financial year platinum outperformed bothpalladium and rhodium. However, the average price of each metal was substantially lower than was seen in FY2015. Refer to the Financial Review section (pages 32 to 37 for details on average prices.

Platinum in October 2015 was at $908 per ounce,but fell to a multi-year low of $814 per ounce on21 January 2016, before rallying and closing at $1,034on 30 September 2016. The Rand started at 13.92 tothe US Dollar in October 2015 and fell to a record lowof R16.87 on 18 January 2016 against the US Dollar,dragging the platinum price down in US Dollar terms.

The South African economy remained weak and theaverage exchange rate achieved for FY2016 was14.77 to the US Dollar.

In US Dollar terms, the platinum price has gained 13%over the FY2016 to close at $1,034.

The palladium price was hit by concerns over Chinesegrowth so, while its price recovered during 2016, itended the financial year just 4% higher.

Rhodium prices failed to join the rally in platinum andpalladium and was down 13% year on year.

Source: Bloomberg

Market Outlook 2017

The outlook for platinum is for demand to be virtuallyunchanged. In Western Europe diesel’s market sharehas been edging slightly lower, and is projected tocontinue to do so, but will be somewhat offset bycontinued growth in vehicle sales. In addition, tighteningemissions’ legislation and increased vehicle productionin the emerging markets should further offset any furtherdecline in Europe. So a stable outlook for autocatalystdemand is projected.

Global demand for jewellery is forecast to improve slightlyafter weakening in 2016. Solid investment demand isanticipated as bar and coin and ETF investment areexpected to be positive. Several new glass fabricationfacilities in the rest of the world are set to lift platinumindustrial requirements slightly next year, offsettingdeclining demand for nitric acid production andslower propane dehydrogenation (PDH) capacitygrowth in China.

Though primary producers are indicating similarproduction levels in 2017, there is a risk due to thecurrent PGM basket price for further mine closures andproject delays at producers in the fourth quartile of thecost curve. We believe that ultimately mine closuresdue to low prices will drive further deficits.

Market Development Drivers

Ongoing development in the PGM demand sectorscontinues to be a critical focus. We will continue tosupport the developments in jewellery, investment andautomotive while giving particular support to newindustries such as fuel cell adoption and additivemanufacturing of PGM based products. The importanceof harmonised global emissions legislations is criticaland is central to a healthy platinum industry.

$ pe

r ou

nce

FY 2015: 737 $/ozFY 2016: 722 $/oz

RhodiumPlatinum

400

500

600

700

800

1,000

900

1,100

1,200

Palladium

FY 2015: 1,075 $/ozFY 2016: 685 $/oz

FY 2015: 1,134 $/ozFY 2016: 1,034 $/oz

Oct-15 Jan-16 Apr-16 Jul-16

> 28

Sales is one of theGroup’s 11 KPIs.See page

/ 20 Lonmin PlcAnnual Report and Accounts 2016

Principal Risks and ViabilityLonmin’s top principal risks are described on the following pages together withtheir potential impact, mitigating strategies and the perceived change in theserisks since the previous financial year.