29

MUMBAI RESIDENTIAL & OFFICE JULY TO DECEMBER 2017 KnightFrank.co.in

| Date post: | 23-Jan-2018 |

| Category: |

Real Estate |

| Upload: | knight-frank-india |

| View: | 256 times |

| Download: | 1 times |

MUMBAIRESIDENTIAL & OFFICEJULY TO DECEMBER 2017

KnightFrank.co.in

2

RESIDENTIAL RECAP H1 2017

New launches fell 36%;

sales dropped by 8% YoY

Unsold inventory of 138,652 units

remained a concern

3

First time DROP in Mumbai residential

prices in the decade starting 2010

Considering all discounts in the

form of stamp duty waivers,

floor rise charge, rental

schemes, the effective discount

has been in the range of

11-12%

Annual price change

4

5,659

6,0726,547 7,085

7,796

7,994

8,120

7,717

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2010 2011 2012 2013 2014 2015 2016 2017

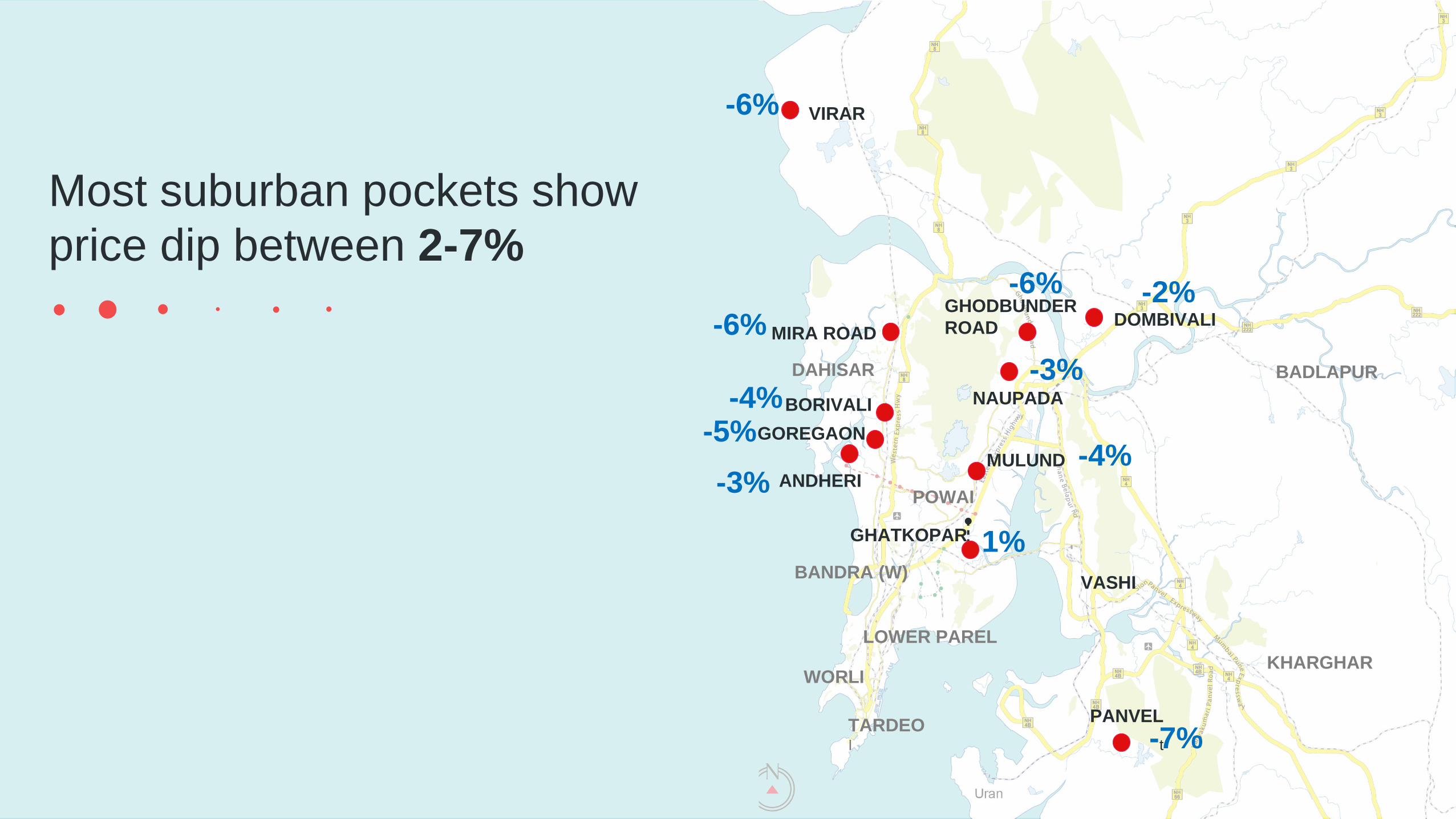

-5%

YoY

GHATKOPAR 1%

LOWER PAREL

WORLI

MULUND -4%

POWAI

PANVEL

t-7%

KHARGHAR

VASHI

DOMBIVALI

-2%

BADLAPUR

MIRA ROAD-6%

VIRAR-6%

TARDEOI

DAHISAR

BORIVALI-4%

BANDRA (W)

GOREGAON-5%

NAUPADA

-3%

GHODBUNDER

ROAD

-6%

ANDHERI-3%

Most suburban pockets show

price dip between 2-7%

70

80

90

100

110

120

130

140

CPI Mumbai

Residential prices decline by

5% compared to an inflation

growth of 5.5% in 2017

Deal sweetened: Gap between retail inflation and home

prices widens

6

CPI

MUMBAI

7

Mumbai is marching towards the

Knight Frank Affordability

Benchmark* of

4.5

(*house price to income ratio)

2017

7.82010

11

8

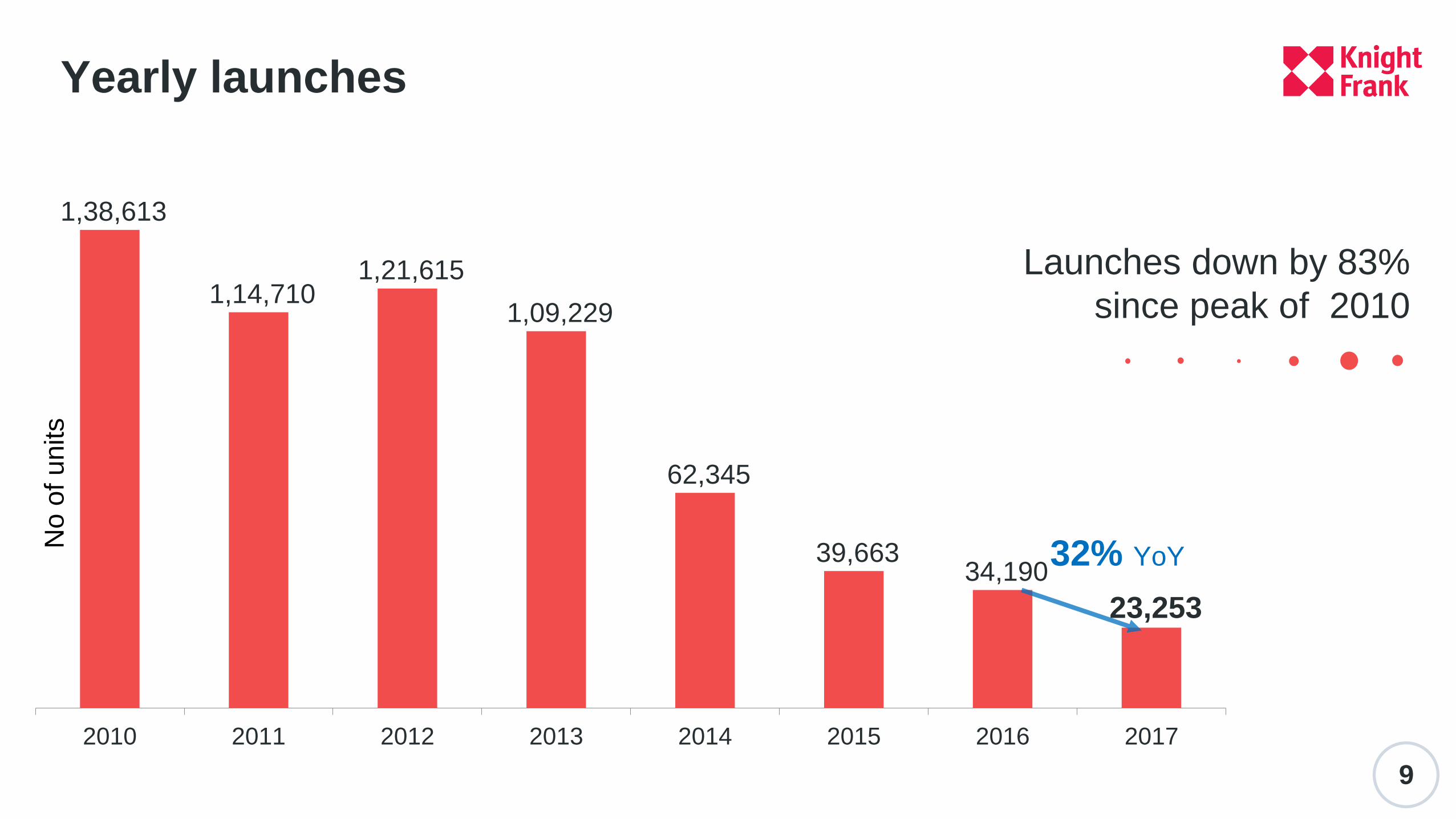

Launches come to a near-halt

Yearly launches

9

1,38,613

1,14,710 1,21,615

1,09,229

62,345

39,663 34,190

23,253

2010 2011 2012 2013 2014 2015 2016 2017

32% YoY

No o

f units

Launches down by 83%

since peak of 2010

10

35,512

26,833

18,887 20,776

24,450

9,740

15,763

7,490

H1 2014 H2 2014 H1 2015 H2 2015 H1 2016 H2 2016 H1 2017 H2 2017

23% YoY

Half-yearly launches

Launches continue to

drop in H2 2017

No o

f units

11

Sales under pressure,

developers blink

12

Quarterly sales

Uptick in quarterly

sales witnessed

No o

f units

17,392

21,903

17,182

8,416

15,265

Q4 2013 Q4 2014 Q4 2015 Q4 2016 Q4 2017

DEMONETISATION

13

60,179

41,981 41,369

32,717

36,505 34,135

30,179

H2 2010 H2 2011 H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

Half-yearly sales

Despite19% YoY growth, sales were down to 50%

of H2 2010 levels in H2 2017

25,403

14

1,08,680

96,226

85,978

74,094 67,715

62,581 60,374 62,256

2010 2011 2012 2013 2014 2015 2016 2017

3%

Yearly sales

Thane, Chembur to Mulund and

Mira Bhayander to Virar have recorded

significant growth in sales over H2 2016

Which micro-market saw maximum change in sales in H2?

Thane

Peripheral

Western Suburbs

Western Suburbs

Central Mumbai

South Mumbai

Central

Suburbs Navi Mumbai

Peripheral

Central Suburbs

+52%

7,190 units

+5%

2,882 units

398 units

+140%

245 units

+1%

+44%

3,495 units

+16%

9,685 units

3,269 units

+32%

3,015 units

-26%

16

Slide in launches pull down

unsold inventory

Unsold inventory

valued at

INR 131,000 crore –

6% of

Maharashtra’s

2017-18 GDP

17

Unsold inventory, age and QTS

Unsold

inventoryQuarters-to-sell

Age of

inventory

H1 2014 2,13,742 11.7 8.8

H2 2014 2,04,070 11.5 10.1

H1 2015 1,94,510 12.1 11

H2 2015 1,81,151 11.1 11.9

H1 2016 1,70,630 10.2 12.6

H2 2016 1,54,967 10.1 13.2

H1 2017 1,38,653 8.8 11.7

H2 2017 1,15,964 7.6 15.6

QTS and age in quarters

Unsold units

19,329

QTS 11.7

Age 16.0

Unsold units

4,175

QTS 18.3

Age 19.4

THANE Unsold units

11,697

QTS 8.1

Age 13.3

PERIPHERAL WESTERN

SUBURBSUnsold units

15,701

QTS 5.1

Age 17.2

WESTERN

SUBURBS

CENTRAL

MUMBAI Unsold units

18,379

QTS 11.6

Age 13.6Unsold units

929

QTS 12.4

Age 16.4SOUTH

MUMBAI

CENTRAL

SUBURBS

NAVI

MUMBAI

Unsold units

21,842

QTS 11

Age 14.7

Unsold units

23,912

QTS 4.5

Age 15.9

PERIPHERAL

CENTRAL SUBURBSLocations such as Lower Parel,

Worli, Prabhadevi in Central

Mumbai worst performing

markets, more than four years

to offload inventory

Age and QTS in quarters

KEY FINDINGS

19

01 03

02 04

New launches down by 83%

from peak in 2010

For the first time in this decade,

Mumbai sees a decline in

weighted average prices in 2017

• Base price down by 5% YoY

• Effective prices down by 11-12% YoY

Unsold inventory down

by 25% YoY

• Drastic fall in launches reduce inventory levels that impacted quarters-to-sell to 7.9 quarters from a high of 12 quarters three years back

Sales in 2017 rose by

3% YoY

• Residential sales in H2 2017 were 19% better than demonetisation-hit H2 2016 on account of base effect. 12% lower than average H2 sales between 2013-15

• Homes launches in H2 2017 dropped by 23% YoY

• 2017 saw 32% fewer launches YoY

20

Transactions fell by 19% for want of

quality space

Vacancy level surged to 22% in H1 2017

although BKC & Lower Parel maintained

single digit vacancy pushing rentals up

by 6% YoY

OFFICERECAP H1 2017

Yearly new completions

21

12

7.6

9.2

5.8 5.9

10.4

0

2

4

6

8

10

12

2012 2013 2014 2015 2016 2017

76%

YoY

in m

nsq

ft

Large volume of supply

adds pressure on

vacancy rates and

rentals

The office market witnessed the

highest transaction volumes in the

last 5 years

23

6.006.25

7.34 7.507.07

7.53

2012 2013 2014 2015 2016 2017

Transactions up

by 6% YoY

Yearly new transactions

24

2.62.4

4.85.0

3.3

4.4

H2 2012 H2 2013 H2 2014 H2 2015 H2 2016 H2 2017

Transactions up

by 36% YoY

Large transactions by

IT/ITeS and co-

working players pull

up H2 2017

Half-yearly transactions

25

22.8%22.6%

21.6%

19.6%

20.2%

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

2013 2014 2015 2016 2017

Vacancy

Vacancy levels increased

on account of huge supply

Central Mumbai and BKC and

off-BKC remain in single digits

26

127

111 118

104

121115

-

20

40

60

80

100

120

140

2012 2013 2014 2015 2016 2017

INR

/sq

ft/m

on

thWeighted average rental movement

High transactions in

peripheral markets pull

down weighted average

rentals by 5% YoY in

2017

BKC & OFF-BKC

CBD & OFF-CBD

CENTRAL

MUMBAI

PBD

SBD

CENTRAL

SBD WEST

Central Mumbai witnessed the highest growth in rentals in 2017

PBD

INR 160-250/sq ft/month

-3%12 month change

INR 220-330/sq ft/month

4%

INR 80-140/sq ft/month

3%

INR 80-150/sq ft/month

3% INR 50-90/sq ft/month

-4%

INR 170-200/sq ft/month

7%

28

Industry H2 2016 H2 2017

BANKING,

FINANCIAL

SERVICES &

INSURANCE

31% 23%

IT/ITES 16% 20%

MANUFACTURING 33% 11%

OTHER SERVICES 20% 46%

What was the share of demand by industry in H2 2017

• IT/ITeS and Other Services segments

particularly co-working recorded

significant growth in transactions

• GST implementation related challenges

led to drop in manufacturing’s share

Interchange

KEY FINDINGS

01 03

02 04

29

New supply higher by

76% YoY

• New office supply hit double digits for the first time since 2012

Vacancy sees a marginal

rise from 19% to 20.2%

• BKC and Lower Parel remain in single digit vacancy

Co-working demand has a

big role in the jump in

transactions

• This segment has been emerging as a new

occupier category similar to the e-commerce

wave of 2014–15 in Bengaluru

Peripheral markets see

increased demand

• Demand in peripheral markets pull office

leasing by 6% in 2017