Munich Re-Germanwatch Briefing 2004 Insuring the Uninsurable: Climate Change and Insurance Reinhard Mechler IIASA May 10, 2004 Financing natural disaster risk in developing countries: the case of Honduras

Transcript

Munich Re-Germanwatch Briefing 2004Insuring the Uninsurable:

Climate Change and Insurance

Reinhard Mechler

IIASA

May 10, 2004

Financing natural disaster risk in developing countries:the case of Honduras

Overview

1. General remarks: risk financing for developing countries

2. Honduras: effects after Hurricane Mitch

3. Implications for climate change work

4. Conclusions

“Insurer of last resort”

Market for risk transfer

MFIsLending Portfolio

Public sectorInfrastructure

Private SectorHousing, machinery etc.

“Reinsurer of last resort”

Reserve fund

Loss financing in developing countries

Private sector: Low uptake of commercial insurance in lower-income countries

Often not available Need insurance culture and institutions ExpensiveGovernment has to provide

financing post-disaster

>9,361 3,031-9,360 761-3,030 <760

0%

5%

10%

15%

20%

25%

30%

GDP [USD]

Ratio of insured losses to total losses according to country income groups for period 1985-1999

29%

9%

2%1%

Source: Munich Re 2000

Role of infrastructure

High poverty- and growth relevance (clean water, roads, schools etc.)

Bottlenecks in developing countries Adverse selection and moral hazard can be dealt with

Issues in disaster management and loss financing

• Disaster management (used to be) retroactive (ex-post)– Losses financed to large extent by international donors and MFIs– Financing gaps and time lags for developing countries– Little incentives for investments into ex –ante risk management

International aid and development funding agencies, besides sharing consternation at delays, disruptions, and increased costs, have the strong view that wisely planned hazard and vulnerability reduction efforts and funding before a catastrophe pay excellent dividends in reducing economic impacts. Mitigation expenditures are a very small fraction of the funds spent on reconstruction in the aftermath of catastrophes (Pollner 2000: 44)

• Objectives: – More emphasis on loss reduction (mitigation)– Reduction of vulnerability– Risk financing solutions

• Disaster management (ex-ante+ex-post) as crucial element of sustainable development

Risk financing (Risk transfer)

• Benefits – Quick compensation:

– Smaller financing gap

– Covariant risk transferred inter-regionally or internationally

– Incentives for loss reduction

• Costs– Premia/costs considerable, usually larger than expected annual loss,

creating opportunity costs

– Costs annually

– Costs today, benefits in future

Current activities in Honduras

• Workshop held in March for finance ministery, next meeting in May, strategy paper

• Steps underway

1. Risk assessment, financial vulnerability

2. Analysis of current insurance arrangements in Honduras

3. Analysis of protection of uncovered liabilities: E(X)=10 million US$/year

4. Pool for support of poor and affected?Contingent credit arrangements?

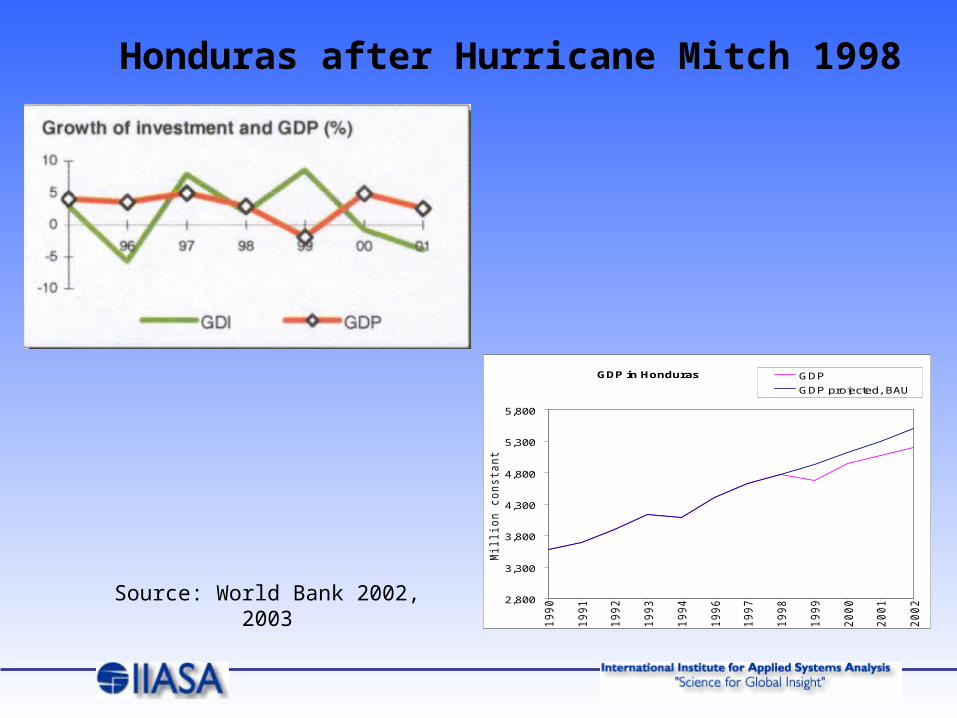

Honduras after Hurricane Mitch 1998

Source: World Bank 2002, 2003

GDP in Honduras

2,800

3,300

3,800

4,300

4,800

5,300

5,800

19

90

19

91

19

92

19

93

19

94

19

96

19

97

19

98

19

99

20

00

20

01

20

02

Mill

ion

co

nsta

nt

19

97

US

D

GDP

GDP projected, BAU

Time lag: Transportation bottlenecks after Mitch

[travel time to markets]

Before After

Source: World Bank 1999

Financing drives recovery

Sources: World Bank 2002

Low domestic savings, reliance on aid and borrowingLow domestic savings, reliance on aid and borrowing

Aid and borrowing(% GNP)

-

3

6

9

12

15

18

1996 1997 1998 1999 2000

Aid

Net financial flows, IDA

Storm and flood hazard

Honduras Storm and Flood Exposure

0.9

0.91

0.92

0.93

0.94

0.95

0.96

0.97

0.98

0.99

1

0 10 20 30 40

% Capital Stock Destroyed

Obligations of government

1. Reconstruction of public assets: roads, bridges, schools, hospitals: Exposed and uninsured public assets: 1.6 billion USD (=12.3% of total capital stock) according to bottom-up WB analysis 2001

2. Help private households and businesses with rebuilding

3. Provide relief to the poor

Total assets/capital stock for 2004: 13.9 billion USD

Risk assessment

Hurricane Mitch 1998: 2,000 million USD in direct losses of total assets (private and public), 18% of capital stock > 100 year event

Storm/flood/landslide

Probability Return period (years) Loss (%) Infrastr. loss (Mill. USD) Loss (%) Infrastr. loss (Mill. USD)10% 10 2.4% 39 0.8% 212% 50 4.6% 76 5% 1301% 100 11.6% 189 12% 312

0.5% 200 17% 278 - -0.2% 500 28.5% 465 31% 806

Expected loss 0.5% 8.6 0.4% 11.2

World BankAssets: 1600 Mill USD

IIASA/Swiss ReAssets: 2600 Mill USD

EarthquakeWorld Bank

Probability Return period (years) Loss (%) Infrastr. loss (Mill. USD) Loss (%) Infrastr. loss (Mill. USD)10% 10 - - 0.1% 32% 50 - - 0.8% 21