Municipal Brief Puerto Rico Credit & Market Update 18 April 2017 Wealth Management Research Thomas McLoughlin, Head Americas Fixed Income, [email protected]; Kristin Stephens, Senior Municipal Strategist Americas, [email protected]; Paul Jacobson, Municipal Strategist Americas, [email protected]• On 13 March, the Financial Oversight and Management Board for Puerto Rico (the "FOMB" or the "Oversight Board") certified the Commonwealth's 10-year fiscal plan, which now becomes the broad operating framework within which Puerto Rico must develop budgets going forward. Prices on Puerto Rico general government bonds broadly declined in response. • The plan, which incorporates less optimistic economic and revenue projections than initially envisioned, has been critiqued for opacity on certain assumptions. It also proposes to repay only 23.5% of debt service between June 2017 and 2026, and does not differentiate as to how various types of debt would be treated in this event. Creditor groups viewed this as a violation of the requirements set forth under the Puerto Rico Oversight, Management, and Economic Stability Act ("PROMESA" or the "Act"). We continue to anticipate losses across the debt stack, regardless of security pledge. • Litigation between general obligation ("GO") and Puerto Rico Sales Tax Financing Corporation ("COFINA") bondholders was halted by a 20 March appellate court ruling. With the Congressionally-imposed stay on litigation expiring on 1 May, and consensual debt negotiations expected to begin only this month, the likelihood of negotiated resolutions on this and other complex claims is low. Although the Commonwealth and the FOMB had petitioned to extend the stay, there are no indications that Congress is prepared to comply with that request. • The Rosselló Administration sought, and tentatively obtained, further concessions under a revised Restructuring Support Agreement ("RSA") between forbearing creditors and the Puerto Rico Electric Power Authority ("PREPA"). Uninsured PREPA bonds rallied on the news. • Moody's lowered ratings across an assortment of Puerto Rico credits this month and revised the rating outlook to negative from developing. The rating actions were attributed to a perceived diminished capacity for repayment. A certified fiscal plan On Monday, 13 March, the Financial Oversight and Management Board for Puerto Rico (the "FOMB" or the "Oversight Board") certified the Commonwealth of Puerto Rico's 10-year fiscal plan. The plan This report has been prepared by UBS Financial Services Inc. (UBS FS). Analyst certification and required disclosures begin on page 13.

Transcript

Municipal BriefPuerto Rico Credit & Market Update18 April 2017

Wealth Management ResearchThomas McLoughlin, Head Americas Fixed Income, [email protected]; Kristin Stephens, Senior Municipal Strategist Americas,[email protected]; Paul Jacobson, Municipal Strategist Americas, [email protected]

• On 13 March, the Financial Oversight and Management Boardfor Puerto Rico (the "FOMB" or the "Oversight Board")certified the Commonwealth's 10-year fiscal plan, which nowbecomes the broad operating framework within which PuertoRico must develop budgets going forward. Prices on PuertoRico general government bonds broadly declined in response.

• The plan, which incorporates less optimistic economic andrevenue projections than initially envisioned, has been critiquedfor opacity on certain assumptions. It also proposes to repayonly 23.5% of debt service between June 2017 and 2026, anddoes not differentiate as to how various types of debt would betreated in this event. Creditor groups viewed this as a violationof the requirements set forth under the Puerto Rico Oversight,Management, and Economic Stability Act ("PROMESA" or the"Act"). We continue to anticipate losses across the debt stack,regardless of security pledge.

• Litigation between general obligation ("GO") and PuertoRico Sales Tax Financing Corporation ("COFINA") bondholderswas halted by a 20 March appellate court ruling. With theCongressionally-imposed stay on litigation expiring on 1 May,and consensual debt negotiations expected to begin only thismonth, the likelihood of negotiated resolutions on this andother complex claims is low. Although the Commonwealthand the FOMB had petitioned to extend the stay, there areno indications that Congress is prepared to comply with thatrequest.

• The Rosselló Administration sought, and tentatively obtained,further concessions under a revised Restructuring SupportAgreement ("RSA") between forbearing creditors and thePuerto Rico Electric Power Authority ("PREPA"). UninsuredPREPA bonds rallied on the news.

• Moody's lowered ratings across an assortment of Puerto Ricocredits this month and revised the rating outlook to negativefrom developing. The rating actions were attributed to aperceived diminished capacity for repayment.

A certified fiscal planOn Monday, 13 March, the Financial Oversight and ManagementBoard for Puerto Rico (the "FOMB" or the "Oversight Board") certifiedthe Commonwealth of Puerto Rico's 10-year fiscal plan. The plan

This report has been prepared by UBS Financial Services Inc. (UBS FS). Analyst certification and required disclosuresbegin on page 13.

is based upon certain assumptions regarding economic growth, pop-ulation, and available cash flow for debt repayment. The Board's cer-tification was provided after some delay, and only after the FOMBrejected the original plan submitted by Governor Ricardo RossellóNevares on 28 February. While the initial version had been criticizedfor the use of revenue assumptions that were overly optimistic, thecertified plan is predicated upon more challenging economic andgrowth assumptions. Interestingly enough, it incorporates an opti-mistic estimate of population loss. To the extent that populationdecline matches or exceeds the rate we have witnessed recently, thefinancial results are likely to be worse than forecast.

In the absence of any corrective action, the certified plan estimatesa cumulative financing gap of USD 66.865bn from FYs 17-26. Thebudget deficit declines to approximately USD 32bn if debt service pay-ments of USD 35.158bn are excluded (USD 66.865bn- USD 35.158bn= USD 31.708bn).1 To the extent that the Rosselló Administration isable to implement an aggregate USD 40bn of revenue and spendingmeasures, which is by no means assured, the government is still leftwith approximately USD 8bn of remaining funds for the payment ofdebt service (USD 40bn of budget adjustments - USD 32bn deficit =USD 8bn remaining available for debt service). On 27 March, cred-itors and bond insurers sent a joint letter to the FOMB outlining theirthoughts on some of the shortcomings of the certified plan and howit stands in violation of PROMESA.

The fiscal plan does not differentiate as to how available funds fordebt service would be allocated across the eighteen different types ofdebt included in the restructuring proposal. There is no clarity on theprioritization of the payment of principal over interest, for example,or senior lien relative to subordinate lien debt. The plan also fails toaccount for approximately USD 49bn of reported net pension liabil-ities. Implementation risk is high, in our view, and could necessitatefurther debt service haircuts. We reiterate our expectation that bond-holders will see losses across the full debt stack, regardless of thesecurity pledge. The degree of complexity and uncertainty that facesbondholders is high.

A stay on creditor litigation is scheduled to expire on 1 May andconsensual debt negotiations are expected to begin only this month.We believe the complexity of competing claims, and the limited timeavailable in which to address them, increases the likelihood that thesematters will be resolved in federal court under Title III of PROMESA.We discuss the differences between PROMESA Title III and Title VI inmore detail in an Appendix to this report. Although the Common-wealth and the FOMB have petitioned to extend the stay, the prob-ability of this occurring is low, in our view. The Congress is in themidst of a two week recess, and is preoccupied by other legislativeinitiatives.

A sharper economic contractionThe more severe economic contraction, now forecasted in the cer-tified plan, is largely unexplained. Governor Rosselló's original plan

Municipal Brief

CIO WM Research 18 April 2017 2

was more optimistic. We believe that reductions in the size and bud-geted expenditures of the Puerto Rico government, as well as the pos-sible loss of future dollars from Washington, may be responsible forthe downward revision. The certified plan also may have been inten-tionally designed to forecast economic growth conservatively, andthus revenue collection, going forward. This would increase the like-lihood of plan benchmarks being met, and establish a lower bar fromwhich to begin debt restructuring negotiations.

As shown in Fig. 1, GNP in the certified plan is anticipated to con-tinue to contract through 2021, with 2022 the first year of sus-tained economic growth. If we align these projections with the legacyGovernment Development Bank ("GDB") of Puerto Rico's EconomicActivity Index ("EAI"), the Commonwealth will have experiencednearly 15 years of economic contraction. We believe that the shift inits economy will have lasting changes and consequences.

Fiscal plan incorporates only a 0.2% yearly popu-lation declinePuerto Rico's certified fiscal plan presupposes a 0.2% yearly popu-lation decline between 2017 and 2026, an important assumption thatunderpins many other economic and revenue projections. Based onthe actual trend of population decline on the island, we view theforecast as optimistic, at best. The plan offers little insight into howthis estimate was formulated.

Puerto Rico's population fell 0.85% in 2016, 4.25 times the assumedrate of loss in the certified plan (-0.85 / -0.20 = 4.25x). The last timePuerto Rico experienced a population decline of 0.2% or less wasin 2005 at -0.156%, based on data released by the now non-opera-tional GDB (see Fig. 2). On a trailing 16-year basis, the island's averageannual population loss has been -0.34%, a full 14bps higher thanforecast in the certified plan. The US Census Bureau estimates thatbetween 2025 and 2050, Puerto Rico's population will decline at anaverage annual rate of 0.59%.

Fig. 1: Projected annual GNP growth

-4%

-3%

-2%

-1%

0%

1%

2%

3%

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026Certified plan Proposed plan

Source: Puerto Rico Fiscal Agency and Financial Authority(AAFAF), UBS, as of 13 April 2017

Fig. 2: Puerto Rico historical and projected annual population declines

Note: US Census Bureau projection is the average annual projected decline from 2025-50. Source: US Census Bureau, Puerto Rico Fiscal Agencyand Financial Authority (AAFAF), UBS, as of 12 April 2017

Municipal Brief

CIO WM Research 18 April 2017 3

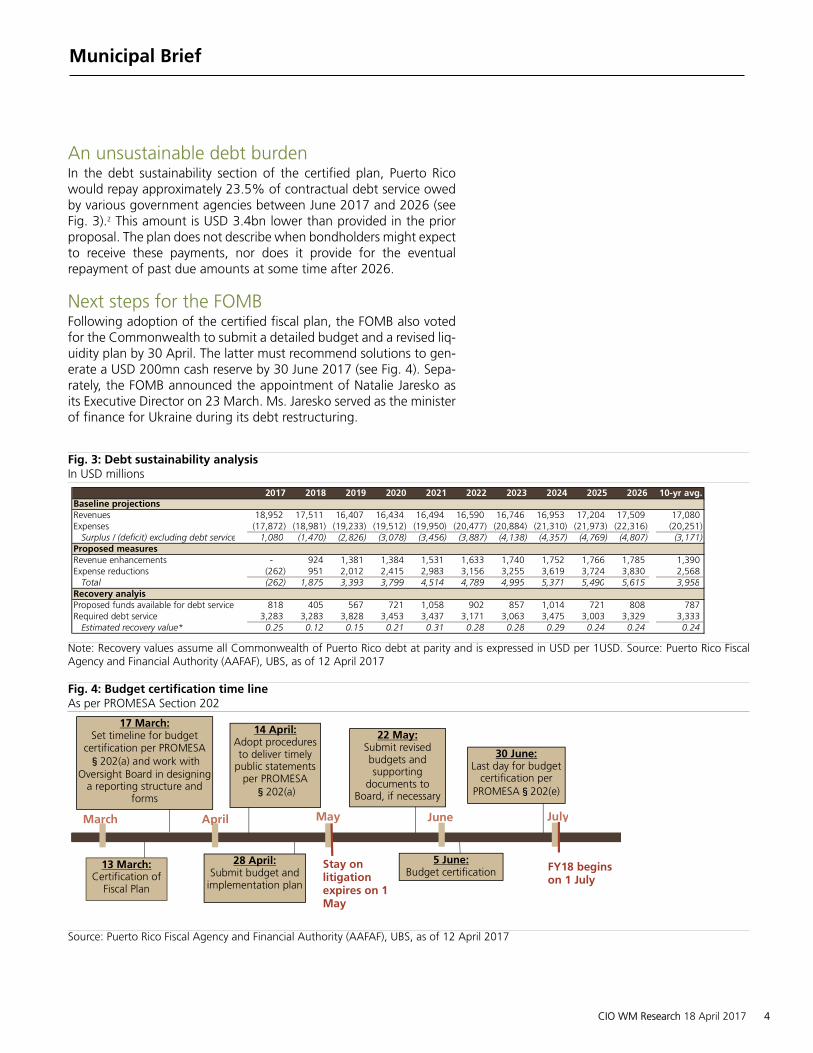

An unsustainable debt burdenIn the debt sustainability section of the certified plan, Puerto Ricowould repay approximately 23.5% of contractual debt service owedby various government agencies between June 2017 and 2026 (seeFig. 3).2 This amount is USD 3.4bn lower than provided in the priorproposal. The plan does not describe when bondholders might expectto receive these payments, nor does it provide for the eventualrepayment of past due amounts at some time after 2026.

Next steps for the FOMBFollowing adoption of the certified fiscal plan, the FOMB also votedfor the Commonwealth to submit a detailed budget and a revised liq-uidity plan by 30 April. The latter must recommend solutions to gen-erate a USD 200mn cash reserve by 30 June 2017 (see Fig. 4). Sepa-rately, the FOMB announced the appointment of Natalie Jaresko asits Executive Director on 23 March. Ms. Jaresko served as the ministerof finance for Ukraine during its debt restructuring.

Fig. 3: Debt sustainability analysisIn USD millions

Note: Recovery values assume all Commonwealth of Puerto Rico debt at parity and is expressed in USD per 1USD. Source: Puerto Rico FiscalAgency and Financial Authority (AAFAF), UBS, as of 12 April 2017

Fig. 4: Budget certification time lineAs per PROMESA Section 202

March April June

13 March:Certification of

Fiscal Plan

17 March:Set timeline for budget

certification per PROMESA§202(a) and work with

Oversight Board in designinga reporting structure and

forms

14 April:Adopt proceduresto deliver timely

public statementsper PROMESA§202(a)

28 April:Submit budget and

implementation plan

FY18 beginson 1 July

July

Stay onlitigationexpires on 1May

May

22 May:Submit revisedbudgets andsupporting

documents toBoard, if necessary

5 June:Budget certification

30 June:Last day for budget

certification perPROMESA§202(e)

Source: Puerto Rico Fiscal Agency and Financial Authority (AAFAF), UBS, as of 12 April 2017

Municipal Brief

CIO WM Research 18 April 2017 4

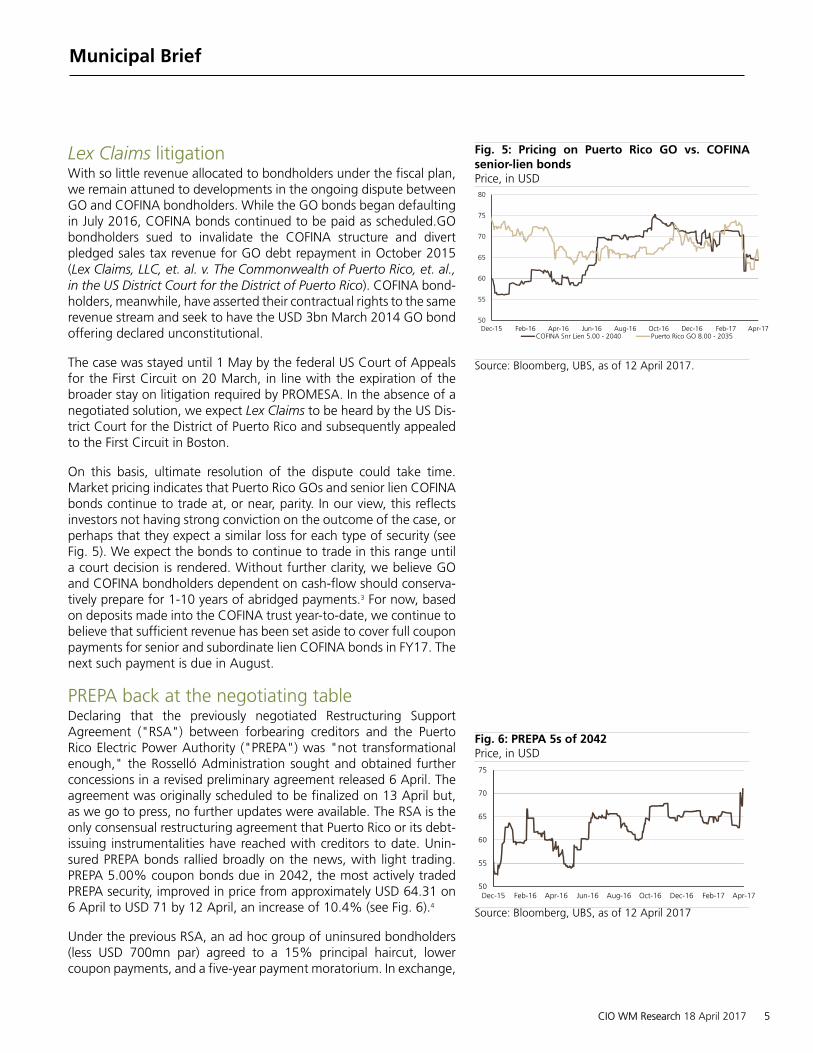

Lex Claims litigationWith so little revenue allocated to bondholders under the fiscal plan,we remain attuned to developments in the ongoing dispute betweenGO and COFINA bondholders. While the GO bonds began defaultingin July 2016, COFINA bonds continued to be paid as scheduled.GObondholders sued to invalidate the COFINA structure and divertpledged sales tax revenue for GO debt repayment in October 2015(Lex Claims, LLC, et. al. v. The Commonwealth of Puerto Rico, et. al.,in the US District Court for the District of Puerto Rico). COFINA bond-holders, meanwhile, have asserted their contractual rights to the samerevenue stream and seek to have the USD 3bn March 2014 GO bondoffering declared unconstitutional.

The case was stayed until 1 May by the federal US Court of Appealsfor the First Circuit on 20 March, in line with the expiration of thebroader stay on litigation required by PROMESA. In the absence of anegotiated solution, we expect Lex Claims to be heard by the US Dis-trict Court for the District of Puerto Rico and subsequently appealedto the First Circuit in Boston.

On this basis, ultimate resolution of the dispute could take time.Market pricing indicates that Puerto Rico GOs and senior lien COFINAbonds continue to trade at, or near, parity. In our view, this reflectsinvestors not having strong conviction on the outcome of the case, orperhaps that they expect a similar loss for each type of security (seeFig. 5). We expect the bonds to continue to trade in this range untila court decision is rendered. Without further clarity, we believe GOand COFINA bondholders dependent on cash-flow should conserva-tively prepare for 1-10 years of abridged payments.3 For now, basedon deposits made into the COFINA trust year-to-date, we continue tobelieve that sufficient revenue has been set aside to cover full couponpayments for senior and subordinate lien COFINA bonds in FY17. Thenext such payment is due in August.

PREPA back at the negotiating tableDeclaring that the previously negotiated Restructuring SupportAgreement ("RSA") between forbearing creditors and the PuertoRico Electric Power Authority ("PREPA") was "not transformationalenough," the Rosselló Administration sought and obtained furtherconcessions in a revised preliminary agreement released 6 April. Theagreement was originally scheduled to be finalized on 13 April but,as we go to press, no further updates were available. The RSA is theonly consensual restructuring agreement that Puerto Rico or its debt-issuing instrumentalities have reached with creditors to date. Unin-sured PREPA bonds rallied broadly on the news, with light trading.PREPA 5.00% coupon bonds due in 2042, the most actively tradedPREPA security, improved in price from approximately USD 64.31 on6 April to USD 71 by 12 April, an increase of 10.4% (see Fig. 6).4

Under the previous RSA, an ad hoc group of uninsured bondholders(less USD 700mn par) agreed to a 15% principal haircut, lowercoupon payments, and a five-year payment moratorium. In exchange,

Fig. 5: Pricing on Puerto Rico GO vs. COFINAsenior-lien bondsPrice, in USD

50

55

60

65

70

75

80

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Feb-17 Apr-17COFINA Snr Lien 5.00 - 2040 Puerto Rico GO 8.00 - 2035

they would have received new securitization bonds to be issued by abankruptcy-remote entity created under the PREPA Revitalization Act,the PREPA Revitalization Corporation ("PREPA-RC"). The revised RSA,now under discussion, appears to be premised upon the followingterms:

• A 15% haircut for uninsured bonds, which would be exchangedfor tax-exempt securitized bonds at a ratio of 85%;

• Securitized bonds accompanied by either a 4.75% coupon if theinvestor selects the current interest rate bond (CIB) option, or a5.50% coupon for capital appreciation bonds (CABs);5

• Final maturity of all of restructured bonds extended to 1 July2047, with both the CIBs and CABs having a 10-year call;

• Restructured bonds no longer required to have an investmentgrade rating for the RSA to close, but this condition remains apost-closing requirement;6

• Non-RSA signatories would presumably be compelled to partic-ipate in the RSA through implementation of Title III of PROMESA;and

• Elimination of Options C and D under the original RSA.7,8

Debt restructuring under the RSA still hinges upon court validationand the creation of PREPA-RC. Until that new legal entity is createdand subsequently validated, the debt restructuring cannot occur evenif the Oversight Board allows the RSA to proceed. It is possible thatthe Puerto Rico Supreme Court will eventually render the final opinionon this matter. We believe court validation could occur in mid to late2017.

Moody's strikes againMoody's lowered the ratings across an assortment of Puerto Ricocredits and revised the rating outlook to negative from developingon 5 April. The rating actions were attributed to a perceived dimin-ished capacity for repayment. The following securities saw their ratingdecline from Ca to C as a result: (i) GDB senior notes; (ii) EmployeesRetirement System pension obligation bonds; (iii) Puerto Rico Infras-tructure Finance Authority bonds secured by federal rum tax transferpayments; (iv) Convention Center District Authority hotel occupancytax bonds; and (v) Puerto Rico Highways and Transportation Authority1998 resolution bonds. Simultaneously, the rating on the Puerto RicoIndustrial Development Company's commercial property rent-securedbonds was lowered to Ca from Caa3.

Moody's believes that each of these securities faces more severelosses than it previously had expected. The rating agency continues tomaintain a higher rating of Caa3 on Commonwealth GO and guar-anteed debt, and on revenue bonds issued by COFINA, the PuertoRico Aqueduct and Sewer Authority ("PRASA"), and PREPA. Moody'srevised the rating outlook on the power utility to negative from devel-oping on 6 April. In its view, the modified RSA "introduces addi-tional risk and uncertainty to the execution of a final consensualagreement."

Municipal Brief

CIO WM Research 18 April 2017 6

Market updatePuerto Rico debt declined rather dramatically in price following therelease of the certified fiscal plan. For example, as shown in Fig. 7, theCommonwealth's benchmark GOs, the 8.00% coupon bonds due in2035, lost approximately 12.3% of their value since the beginningof March (from USD 73.77 to USD 64.65).9 Subordinate lien COFINAbonds carrying a 5.25% coupon due in 2041 fell from USD 47.54 toUSD 38.73, or 18.3%, over the same timeframe.10 Meanwhile, theprice of senior lien COFINA bonds weakened by 9.6%, with a 5.25%coupon bond due in 2040 moving from USD 71.26 to USD 64.40 (seeFig. 8).11

We believe there are a number of reasons why the Commonwealth'sbenchmark GO bonds trade at a price of approximately USD 65. First,the 8s of 2035 are considered to be an "on-the-run" security, inmunicipal parlance. This means that the bond is the most recentlyissued cusip, is held in the hands of predominately institutionalinvestors, has the largest par amount outstanding, and trades morefrequently. It is considered, by far, to be the most liquid in the PuertoRico GO market.

Puerto Rico's legacy GO bonds would be considered "off-the-run"securities, by contrast. These bonds are more widely held by retailinvestors and mutual funds that have had Puerto Rico exposure formany years; holders that are less likely to trade their positions. Thelegacy bonds, despite having the same legal claim, have a lower dollarprice and trade less frequently.12

Fig. 7: Price trends, Puerto Rico GO 8.00% due 1July 2035Last price in USD

Sales Tax Financing Corporation subordinate lien Puerto Rico Electric Power AuthorityPuerto Rico General Obligation Sales Tax Financing Corporation senior lienPuerto Rico Aqueduct and Sewer Authority

Source: MSRB trade data, Bloomberg, UBS, as of 12 April 2017.

Municipal Brief

CIO WM Research 18 April 2017 7

Over time, we expect Puerto Rico's benchmark and legacy GO debtto more broadly converge in price, irrespective of coupon and/ormaturity, comparable to the trading pattern observed in mid-2016(see Fig. 9). For now, however, we expect elevated price volatilityacross Puerto Rico's securities as we near the next phase of theCommonwealth's eventual debt restructuring, either through a con-sensual agreement or in more adversarial court proceedings.

So why are defaulted GO bonds still trading atUSD 65?Volatility and internal rate of return ("IRR") support current tradinglevels.13 Although the GO bonds are in default, they do have a con-stitutional claim and first lien on available revenue. The precise defi-nition of "available revenue" will be contested, of course, but the GObondholders are better positioned than many other creditors.

On the downside, GO bondholders are striving to protect themselvesunder a worst case scenario. For example, if a buyer of Puerto RicoGO 8s of 2035 were to purchase the securities today at USD 65, andwe assume that bond maturity is extended 10 years to 2045 in arestructuring, coupon is reduced by 66% (from 8% to 2.72%), andprincipal is lowered by 50%, the purchaser would receive an IRR of1.15% per year if the restructured bonds are held to maturity (seeFig. 10).

Fig. 9: Puerto Rico GO price comparison, 8s of 2035vs. 5s of 2041Price, in USD

50

55

60

65

70

75

80

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16 Feb-17 Apr-17Puerto Rico GO 8.00 - 2035 Puerto Rico GO 5.00 - 2041

Source: Bloomberg, UBS, as of 12 April 2017

Fig. 10: Potential restructured cash flow for Puerto Rico GO 8s of 2035

Restructured maturity 7/1/2045 Date Principal Interest Lost cash flowRestructured coupon 2.72% 4/13/2017 -65,000 - 1,733

Principal recovery 50% 7/1/2017 - - 8,000

Estimated IRR 1.15% 7/1/2018 - - 8,000

7/1/2019 - - 8,000

7/1/2020 - - 8,000

7/1/2021 - - 8,000

7/1/2022 - - 8,000

7/1/2023 - - 8,000

7/1/2024 - - 8,000

7/1/2025 - - 8,000

7/1/2026 - 2,720 5,280

7/1/2027 - 2,720 5,280

7/1/2028 - 2,720 5,280

7/1/2029 - 2,720 5,280

7/1/2030 - 2,720 5,280

7/1/2031 - 2,720 5,280

7/1/2032 - 2,720 5,280

7/1/2033 - 2,720 5,280

7/1/2034 - 2,720 5,280

7/1/2035 - 2,720 5,280

7/1/2036 - 2,720 -

7/1/2037 - 2,720 -

7/1/2038 - 2,720 -

7/1/2039 - 2,720 -

7/1/2040 - 2,720 -

7/1/2041 - 2,720 -

7/1/2042 - 2,720 -

7/1/2043 - 2,720 -

7/1/2044 - 2,720 -

7/1/2045 32,500 2,720 -

10 yrsnon-payment

Note: Puerto Rico GO 8.00% of 2035 originally issued on 3/17/2014. Analysis is based on potential bond restructuring to mature on 7/1/2045with 10 years non-payment (started on 1 July 2016) Source: UBS, as of 12 April 2017

Municipal Brief

CIO WM Research 18 April 2017 8

We previously established that these securities have a high level ofprice volatility. On 14 March, their value declined by 7 points (fromapproximately USD 72.45 to USD 66.93, or 7.61%) in one session fol-lowing the adoption of the certified fiscal recovery plan.14 Conversely,on good news, such as a favorable court development, the better liq-uidity exhibited by the 8s of '35 would likely result in a sharp upwardprice movement, allowing an institutional investor to quickly capturereturn on investment.

Conclusion and outlookPuerto Rico's economy has been contracting despite an economicrecovery elsewhere in the United States. The persistent recession hasamounted to a lost decade for the island. Population loss continuesand the probability of receiving substantial incremental financial assis-tance from Washington is low.

The prior gubernatorial administration made little progress in its nego-tiations with creditors. The Puerto Rico Electric Power Authority hadthe financial capacity to restructure its debt expeditiously but it stilltook two years to reach an agreement. There is a negligible chance,in our view, the Commonwealth can execute subsequent agreementsacross the capital structure in a fraction of the time it took to do sofor PREPA.

The certified fiscal plan has some inconsistencies, in our view. It failsto reduce spending year-to-year and does not distinguish betweenessential and non-essential government services. The population esti-mates appear far too optimistic. There is no differentiation amongvarious constitutional and statutory liens. The absence of precisionmay be purposeful, to encourage further negotiation and to extractconcessions from institutional investors and bond insurers.

We believe the risks associated with implementation of the certifiedplan are exceptionally high. Puerto Rico has been in discussions withits creditors for more than a year without making much headway. Thelikelihood of achieving broad-based consensual debt restructuringacross a disparate group of creditors within a timeframe of approxi-mately two weeks is exceedingly low. We expect subsequent litigationto be costly and protracted and for negotiations between creditorsand the Commonwealth to become even more contentious over time,regardless of the outcome of the PREPA discussions.

We anticipate that most of the island's outstanding debt will berestructured pursuant to Title III of PROMESA. Creditors are likely tocontest the proceedings on the basis that the Commonwealth didnot engage in good faith negotiations when there was time to doso. Conservatively, we believe that bondholders, excluding those withPREPA obligations where likely impairment has been negotiated sep-arately, should prepare for 1–10 years of abridged payments on theirholdings and significant losses on their investments.

Municipal Brief

CIO WM Research 18 April 2017 9

Appendix I

PROMESA's debt restructuring processPROMESA provides two paths for Puerto Rico and its instrumentalitiesto restructure existing debt obligations: Title VI (voluntary) and TitleIII (Federal Court). Title VI provides the process for a voluntary nego-tiated settlement, while Title III permits the Federal Court to approve aplan submitted by the Commonwealth and/or one of its instrumental-ities. Such plan would be binding even upon dissenting creditors. Thisoption is available only after the entity has made good faith efforts toreach a consensual restructuring with creditors.

Title VI (voluntary)Sections 601 and 104(i) of PROMESA provide a process for submissionand approval of a voluntary agreement to modify contractual bondclaims. This modification may be proposed by a debtor or by bond-holders, which differs from bankruptcy court convention where onlythe debtor is permitted to submit proposals to the court. If proposedby the bondholders, the Oversight Board has the authority to acceptthe proposal on behalf of the debtor.

The Oversight Board, together with debtor as issuer of the bonds, willseparate each proposed modification into separate groups based on:• At least one group per issuer;

• Secured bonds will be in separate groups;

• Separate groups will be established based on seniority for issuerswith multiple series of bonds outstanding; and

• Separate groups will be established for bonds guaranteed by theCommonwealth.

Proposed modifications must be accepted by no less than 50% of theoutstanding principal amount of the affected bonds in the particularpool entitled to vote, and by two-thirds of the aggregate outstandingprincipal amount of bonds in such pool of those who actually vote,in order to be approved.

Next, the Oversight Board must vote to certify the hypothetical debtrestructuring proposal if it satisfies the conditions under section 104(i)of PROMESA. The proposed modification will not become effective forholders until an order approving the qualifying modification has beenentered by federal district court. Only a federal court can abdicatecontractual obligations.

Modification of contractual debt obligations are binding on allholders, irrespective of if they have given consent or participated inthe negotiations, as long as the required majorities of holders of thebonds and the issuer have consented to the modification.

Municipal Brief

CIO WM Research 18 April 2017 10

Title III (Federal Court)After getting approval from the Oversight Board, Puerto Rico and/orits instrumentalities may file a petition with the Federal district courtseeking to restructure debt under Title III. This is similar to seekingbankruptcy protection under Chapter 9.

The following conditions have to be satisfied for a case to proceed:• The entity must be the Commonwealth of Puerto Rico or one of

its instrumentalities;

• The Oversight Board issued a certification to such an entity;

• The entity desires to restructure;

• Prior to the restructuring proposal, the Oversight Board has cer-tified that the entity made good faith efforts to reach consensualrestructuring;

• The entity has taken steps to deliver timely audited financial state-ments and other information for an interested person to makean informed decision;

• A fiscal plan for the entity is in place; and

• A qualifying modification under Title VI is not in place.

The federal district court may confirm a debt adjustment plan if itmeets the following criteria:

• The plan complies with the provisions of the bankruptcy codemade applicable under Title III of PROMESA;

• The plan complies with the provisions of PROMESA;

• The debtor is not prohibited by law from taking action necessaryto carry out the plan;

• Any other legislative, regulatory, or electoral approvals are inplace;

• The plan is determined to be in the best interest of creditors andfeasible (with the best interest of creditors test determined asbeing better than any other non-bankruptcy alternatives availableto creditors); and

• The plan is consistent with the fiscal plan approved by the Over-sight Board.

Municipal Brief

CIO WM Research 18 April 2017 11

End notes1 Through January 2017, the Commonwealth has missed USD 2.4bn of payments on these obligations.2 The certified plan includes the following types of Commonwealth debt obligations in the restructuring proposal: GO, GO-guaranteed, Puerto Rico Public Building Authority (PBA), COFINA, the Puerto Rico Highways and Transportation Authority(PRHTA), the Puerto Rico Infrastructure Financing Authority (PRIFA), Puerto Rico Convention Center District Authority(PRCCDA), Puerto Rico Public Finance Corporation (PFC), University of Puerto Rico (UPR), Puerto Rico Employees RetirementSystem (ERS), GDB, and Puerto Rico Industrial Development Corporation (PRIDCO). It explicitly excludes PREPA, the PuertoRico Aqueduct and Sewer Authority (PRASA), the Puerto Rico Housing Finance Authority (HFA), Children's Trust, the PuertoRico Industrial Investment Corporation, and municipality-related debt.3 The funds for COFINA's 1 August 2017 debt service payment are currently held with the trustee. It is unknown at thistime if those funds will be released to bondholders. Our base case assumption is for the payment to be made.4 Bloomberg BVAL pricing, CUSIP: 74526QA285 Previous versions of the RSA gave coupon ranges for the CIB and CAB bonds. In this revised RSA proposal, these couponpayments are now fixed at 4.75% and 5.50% respectively.6 The RSA proposal explicitly says the "Investment grade rating is no longer a condition to RSA closing; remains a conditionpost-closing." It is unclear to us what the RSA proposal language surrounding "post-closing" means.7 Option C originally permitted PREPA to tender for bonds at an undisclosed price.8 Option D originally allowed for no more than USD 700mn of uninsured legacy PREPA revenue bonds to remain out-standing. These legacy PREPA bondholders would have received their revenues under the pre-existing flow-of-funds underPREPA's indenture.9 Bloomberg BVAL pricing (CUSIP: 74514LE86).10 Bloomberg BVAL pricing (CUSIP: 74529JLM5).11 Bloomberg BVAL pricing (CUSIP: 74529JNU5).12 The Puerto Rico 8% coupon bonds due in 2035 (CUSIP: 74514LE86) have embedded in their indenture a provisionthat requires any legal proceeding regarding payment on these securities to be held in a New York State court venue.We believe that certain terms established under PROMESA supersede this provision; however, there is uncertainty as tothe ultimate validity of this legal provision. If upheld, it raises the possibility that these securities could be treated as aseparate creditor class in a debt restructuring scenario, with legal proceedings possibility held in duel locations. This isnot our base-case assumption.13 The internal rate of return (IRR) on an investment is the annualized effective compound return, or rate of return. In fixedincome, the IRR is used as a proxy to calculate theoretical yield of an investment on defaulted or restructured securities.14 Bloomberg BVAL price change between 13 and 14 March 2017 (CUSIP: 74514LE86).

Municipal Brief

CIO WM Research 18 April 2017 12

Appendix

Analyst certificationEach research analyst primarily responsible for the content of this research report, in whole or in part, certifies that withrespect to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect hisor her personal views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directlyor indirectly, related to the specific recommendations or views expressed by that research analyst in the research report.

Statement of RiskMunicipal bonds - Although historical default rates are very low, all municipal bonds carry credit risk, with the degree of risk largely followingthe particular bond’s sector. Additionally, all municipal bonds feature valuation, return, and liquidity risk. Valuation tends to follow internal andexternal factors, including the level of interest rates, bond ratings, supply factors, and media reporting. These can be difficult or impossible toproject accurately. Also, most municipal bonds are callable and/or subject to earlier than expected redemption, which can reduce an investor’stotal return. Because of the large number of municipal issuers and credit structures, not all bonds can be easily or quickly sold on the openmarket.

Terms and AbbreviationsTerm / Abbreviation Description / Definition Term / Abbreviation Description / DefinitionGO General Obligation Bond TEY Taxable Equivalent Yield (tax free yield divided by

100 minus the marginal tax rate)MMD Municipal Market Data