MUTUAL FUNDS: AN OVERVIEW A Mutual fund is a trust that pools the saving of the number of investors who share a common financial goal. The money thus collected is invested by the fund manager in different types of securities depending upon the objective of the scheme. These could range from share to debentures these investments and the capital appreciation realized by the scheme are shared by its unit holders in proportion to the number of units owned by them (prorate). Thus a mutual fund is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed portfolio at a relatively low cost. Anybody with an investment in mutual funds. Each mutual funds scheme has a defined investment objective and strategy. The flow chart below describes broadly the working of a mutual fund: Investors Passed pool their back to money with

Transcript

MUTUAL FUNDS: AN OVERVIEW

A Mutual fund is a trust that pools the saving of the number of investors who share

a common financial goal. The money thus collected is invested by the fund

manager in different types of securities depending upon the objective of the

scheme. These could range from share to debentures these investments and the

capital appreciation realized by the scheme are shared by its unit holders in

proportion to the number of units owned by them (prorate). Thus a mutual fund is

the most suitable investment for the common man as it offers an opportunity to

invest in a diversified, professionally managed portfolio at a relatively low cost.

Anybody with an investment in mutual funds. Each mutual funds scheme has a

defined investment objective and strategy.

The flow chart below describes broadly the working of a mutual fund:

Investors

Passed pool their back to money with

Returns Fund Manager

Generates Invest in Securities

A mutual fund is the ideal investment vehicle for today’s complex and modern

financial scenario. Markets for equity shares, bonds and other fixed income

instruments, real estate, derivatives and other assets have become mature and

information driven. Price changes in these assets are driven by global events

occurring in fare way places. A typical individual is unlikely to have the

knowledge, skills inclination and time to keep track of events, understand their

implications and act speedily. An individual also finds it difficult to keep track of

ownership of his assets, investments., brokerage dues and bank transactions etc.

A mutual fund is the answer to all these situations. It appoints professionally

qualified and experience staff that manages each of these functions on a full times

basis. The large pool of money collected in the fund allows it to hire such at a very

low cost to each investor. In effect, the mutual fund vehicle exploits economics of

scale in all three areas-research, investments and transaction processing. While the

concept of individual coming together the invest money collectively is now new,

the mutual fund its present from is 20th century phenomenon. In fact, mutual funds

gained popularity only after the second world war. Globally there are thousand of

funds offering ten of thousands of mutual funds with different investment

objectives. Today, mutual funds collectively mange almost as much as or more

money as compared to banks.

A draft offer document is to be prepared at the time of lunching the fund.

Typically, it pre species the investment objectives of the fund, the risk associated,

the costs involved in the process and the broad rules fro entry in to and exit from

the fund and other areas of operation. In India, as in countries, these sponsors need

approval from a regulator, SEBI (Security and Exchange Board of India) in our

case SEBI looks at track records of the sponsor and its financial strength in grating

approval to the fund for commencing operations.

A sponsor then hires an asset management company to invest the funds according

to the investment objective. It also hires another entity to bt the custodian of the

assets of the fund and perhaps a third one to handle registry work for the unit

holders (subscribers) of the fund.

In the Indian context, the sponsors promote the asset Management Company

also, in which it holds a majority stake. In many cases a sponsor can hold a 100%

stake in the asset management Company (AMC). E.g. Birla Global Finance is the

sponsor of the Birla Sun Life Asset Management Ltd. Which has floated mutual

funds schemes and also acts as a manger for the funds collected under the

schemes?

BRIEF HISTORY OF MUTUAL FUNDS (MFS)

The end of millennium marks 36 years pf existence of mutual funds in this country.

The ride through these 36 years is not been smooth. Investor opinion is still

divided. While some are for mutual funds other against it.

UTI commenced its operations from July 1964. the impetus for establishing

a formal UTI. On came from the desire to increase the propensity of the middle

and lower groups to save and to invest. UTI came into existence during a period

marked by great political and economic uncertainty in India. With war on the

boards and economic turmoil that depressed the financial market, entrepreneurs

were hesitant to enter capital market. The already existing companies found it

difficult to raise fresh capital, as investors did not responds adequately to new

issues. Earnest efforts were required to canalize saving of the community into

productive uses in order to speed up the process of industrial growth. The them

finance minister, T.T Krishanmachari set up the idea of a unit trust that would be

“open the any person or UTI on o purchase the units offered by the truest.

However this UTI on as we see it, is intended to cater to the needs of individual

investors, and even among them as far as possible, to those whose means are

small”. His ideas took the form of the Unit Trust of India, an intermediary that

would help fulfill the twin objectives of mobilizing retail saving and investing

those savings in the capital market and passing on the benefits so accrued to the

small investors.

UTI commenced its operations from July 1964 “with a view to encouraging saving

and investment and participation in the income, profits and gain occurring to the

corporation from the acquisition, holding, management and disposal of securities.”

Different, provisions of the UTI act laid down the structure of management, scope

of business, powers and functions of the trust as well as accounting, disclosures

and regulatory requirements for the trust.

One things is certain – the fund industry is here to stay. The industry was one

entity show till 1986 when the UTI monopoly was broken when SBI and Can bank

mutual fund entered the area. This was followed by the entry of others like LIC,

IC, etc. sponsored by public sectors banks. Starting with an asset base of Rs. 0.25

ban in 1964 the industry has grown at a compounded average growth rate of

26.34% to its current size Rs. 1130 ban.

The period 1986-1993 can be termed as the period of public sector mutual funds

(PMFs). From one player in 1985 the number increased to 8 in 199. the party did

not last long. When the private sector made its debut in 1993-94, the stock market

was booming.

The opening up of the assets management business to private sector in 1993 saw

international along with the host of domestic players join the party. But for the

equity funds, the period of 1994-96 was one of the worst in the history of Indian

mutual funds.

1999-2000 years of the funds:

Mutual fund have been around for a long period of time precise for 36 yrs. But the

year 1999 saw immense future potential and developments in this sector. This year

signaled the year of resurgence of mutual funds and the regaining of investor

confidence in these MF’s this time around all the participants are developments in

this sector. This year signaled the year of resurgence of mutual funds and the

regaining of investor confidence in these MF’s. this time around all the participants

are involved in the revival of the funds the AMC’s the unit holders, the other

related parties. However the sole factor that give lift to the revival of the funds was

the union budget. The budget brought about a large number of changes in one

stroke. An insight of the union budget on mutual funds taxation benefits is

provided later.

It provided center stage to the mutual funds, made them more attractive and

provides acceptability among the investors. The union budget exempted mutual

fund dividend given out by equity-oriented schemes from, both at the hands of the

investor as well as the mutual fund. No longer were the mutual funds interested in

selling the concept of mutual funds they wanted to talk business which would

mean to increase asset base, and to get asset base and investor base they had to be

fully armed with a whole lot of schemes for every investor. So new schemes for

new IPO’s were inevitable. The quest to attract investors extended beyond just new

schemes. The funds started to regulate themselves and were all out on wining the

trust and confidence of the investors under the ages of the Association of Mutual

funds of India (AMFI)

One can say that the industry is moving from infancy to adolescence, the industry

is maturing and the investor and funds are frankly and openly discussing

difficulties opportunities and compulsions.

FUTURE SCENARIO:

The asset base will continue to grow at an annual rate of about 30 to 35 % over the

next few years as investor’s shift their assets from banks and other traditional

avenues. Some of the older public and private sector players will either close shop

or be taken over.

Out of ten public sector players five will sell out, close down or merge with

stronger players in three to four years. In the private sector this trend has already

started with two mergers and one takeover. Here too some of them will down their

shutters in the near future to come.

But this does not mean there is no room for other players. The market will witness

a flurry of new players entering the arena. There will be a large number of offers

from various asset management companies in the time to come. Some big names

like Fidelity, Principal, Old Mutual etc. are looking at Indian market seriously. One

important reason for it is that most major players already have presence here and

hence these big names would hardly like to get left behind.

In the U.S. most mutual funds concentrate only on financial funds like equity and

debt. Some like real estate funds and commodity funds also take an exposure to

physical assets. The latter type of funds are preferred by corporate’s who want to

hedge their exposure to the commodities they deal with.

For instance, a cable manufacturer who needs 100 tons of Copper in the month of

January could buy an equivalent amount of copper by investing in a copper fund.

For Example, Permanent Portfolio Fund, a conservative U.S. based fund invests a

fixed percentage of it’s corpus in Gold, Silver, Swiss francs, specific stocks on

various bourses around the world, short –term and long-term U.S. treasuries etc.

In U.S.A. apart from bullion funds there are copper funds, precious metal funds

and real estate funds (investing in real estate and other related assets as well.).In

India, the Canada based Dundee mutual fund is planning to launch a gold and a

real estate fund before the year-end.

In developed countries like the U.S.A there are funds to satisfy everybody’s

requirement, but in India only the tip of the iceberg has been explored. In the near

future India too will concentrate on financial as well as physical funds.

The mutual fund industry is awaiting the introduction of DERIVATIVES in the

country as this would enable it to hedge its risk and this in turn would be reflected

in it’s Net Asset Value (NAV).

SEBI is working out the norms for enabling the existing mutual fund schemes to

trade in Derivatives. Importantly, many market players have called on the

Regulator to initiate the process immediately, so that the mutual funds can

implement the changes that are required to trade in Derivatives.

TYPE OF MUTUAL FUNDS

Mutual fund schemes may be classified on the basis of its

structure and its investment objectives.

By Structure:

Open-ended funds

An open-end fund is one that is available for subscription all through the year.

These do not have a fixed maturity. Investors can conveniently buy and sell units at

net asset value (“NAV”) related prices. The key feature of the open-end schemes is

liquidity.

Closed-ended Funds

A closed-end-fund has a stipulated maturity period generally ranging from 3 to 15

years. The fund is open for subscription only during a specified period. Investor

can invest in the scheme at the time of the initial public issue and thereafter they

can by or sell the units of the stock exchanges where they are listed. In order to an

option of selling back the units to the Mutual Fund through periodic repurchase at

NAV related prices. SEBI Regulations Stipulate that at least one of the two exit

routes is provided to the investor.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They

are open for sale or redemption during predetermined intervals at NAV related

prices.

By Investment Objective :

Growth Funds

The aim of growth is to provide capital appreciation over the medium to long-term.

Such schemes normally invest a majority of their corpus in equities. It has been

proven that returns from stocks, have outperformed most other kind of investments

held over the long term. Growth schemes are ideal for investors having a long term

out look seeking growth over a period of time.

Income Funds

The aim of income fund is to provide regular and steady income to investors. Such

schemes generally invest in fixed income securities. Income Funds are ideal for

capital stability and regular income.

Balanced Income

The aim of balanced funds is to provide both growth and regular income. Such

schemes periodically discibute a part of their earning and invest both in equities

and fixed securities in the proportion indicated in their offer documents. In a rising

market, the NAV of these schemes may not normally keep pace, or fall equally

when the market falls. These are ideal for investors looking for a combination of

income and moderate growth.

Money Market Funds

The aim of money market funds is to provide easy liquidity, preservation of capital

and moderate income. These schemes generally invest in safer short-term

instruments such as treasury bills, certificates of deposits, commercial paper and

inter-bank call money. Returns of this schemes may fluctuate depending upon the

interest rates prevailing in the market. These are ideal for corporate and individual

investors as a mean to park their surplus funds for short periods.

Load funds

A load Fund is one that charges a commission for entry or exit. That is each time

you buy or sell units in the fund, a commission will be payable. Typically entry or

exit loads range from 1% to 2% It could be worth paying the load if the fund has a

good performance history.

No-load Fund

A No-Load Fund is one that does not charge a commission for entry or exit. That

is, no commission is payable on purchase or sale of units in the fund. The

advantage of a no load fund is that the entire corpus is put to work

Other Schemes:

Tax Saving Schemes

These schemes offer tax rebate to the investors under specific provision of the

Indian income tax law as the Government offers tax incentives for investment in

specified avenues. Investment made in Equity Liquid Saving Schemes (ELSS) and

Pension schemes are allowed as deduction u/s 88 of the income Tax act, 1961. The

Act also, provides opportunities to investors to save capital gains u/s 54 EA and 54

EB by investing in Mutual Funds, provided the capital asset has been sold prior to

April 1, 2000 and the amount is invested before September 30, 2000.

Special Schemes

Industry Specific Schemes

Industry Specific Schemes invest only in the industries specified in offer

document. The investment of these funds is limited to specific industries like Info

Tech, FMCG, Pharmaceuticals HDFC BANK LTD. calls etc.

Index Schemes

Index Funds attempt to replicate the performance of a particular index such as the

BSE sensex or the NSF 50

Sectoral Schemes

Sectoral Funds are those, which invest exclusively in a specified industry or a

group of industries or various segments such as ‘A’ Group shares or initial public

offerings.

Major Mutual Fund Companies in India

ABN AMRO Mutual Fund Reliance Mutual Fund

Birla Sun Life Mutual Fund Standard Chartered Mutual Fund

Bank of Baroda Mutual Fund Franklin Templeton India Mutual

Fund

HDFC Mutual Fund Morgan Stanley Mutual Fund

India

HSBC Mutual Fund Escorts Mutual Fund

ING Vysya Mutual Fund Alliance Capital Mutual Fund

Prudential ICICI Mutual Fund Benchmark Mutual Fund

State Bank of India Mutual Fund Canbank Mutual Fund

Tata Mutual Fund Chola Mutual Fund

Unit Trust of India Mutual Fund LIC Mutual Fund

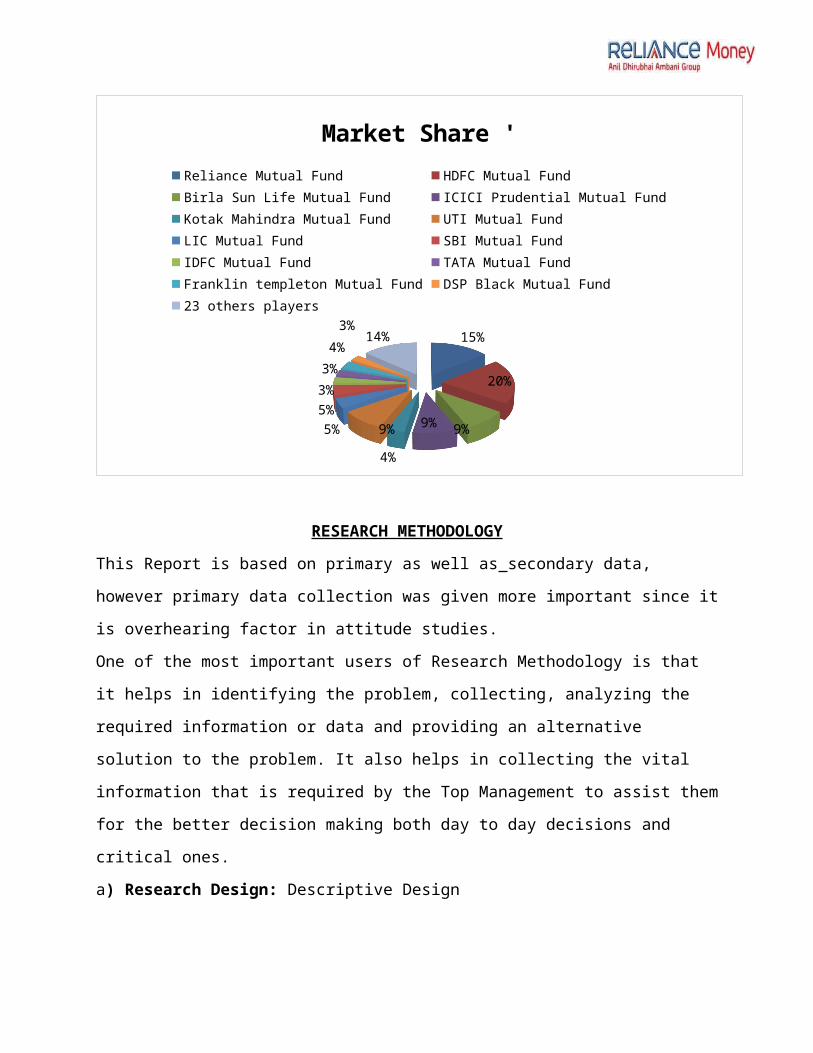

15%

20%

9%9%

4%

9%

5%

5%

3%

3%

4%3% 14%

Market Share 'Reliance Mutual Fund HDFC Mutual Fund Birla Sun Life Mutual FundICICI Prudential Mutual Fund Kotak Mahindra Mutual Fund UTI Mutual FundLIC Mutual Fund SBI Mutual Fund IDFC Mutual FundTATA Mutual Fund Franklin templeton Mutual Fund DSP Black Mutual Fund23 others players

RESEARCH METHODOLOGY

This Report is based on primary as well as secondary data, however primary data collection was

given more important since it is overhearing factor in attitude studies.

One of the most important users of Research Methodology is that it helps in identifying the

problem, collecting, analyzing the required information or data and providing an alternative

solution to the problem. It also helps in collecting the vital information that is required by the

Top Management to assist them for the better decision making both day to day decisions and

critical ones.

a) Research Design: Descriptive Design

b) Data Collection Method: Survey Method

c) Universe: Chandigarh

d) Sampling Method: The sample was collected through personal visits, formally and informal

talks and through filling up the Questionnaire prepared. The data has been analyzed by using

mathematical or statistical tools.

e) Sample Size: 100 respondents

f) Sampling Unit: Businessmen, Government Servant, Retired Individuals majorly HNI’s

g) Data Source: Primary data

h) Data Collection Instrument: Structured Questionnaire

i) Sample Design: Data has been presented with the help of Bar Graph, Pie Chart, and Line

Graph etc.

j) Duration of The Study: The study was carried out for a period of 45 days, from 13th June to

30th July ‘2014.

Questionnaire to analyse perceptions of peoples for Mutual funds

Please go through the following questionnaire and identify the appropriate responses for each of

them. There is no such thing as a correct answer, so feel free to respond. Please forward it as

many peoples as you can. Disclaimer: Your response via this questionnaire will be used strictly

for academic purposes. There will not be any commercial solicitation or usage of the response in

any kind / form whatsoever.

1.What's your Good name?

2. What’s your Age?

3. What is your Qualification?

(a) Under-graduation (b) Graduation (c) Post Graduation (d) Others

4. What is your Occupation?

(a) Government (b) Private (c) Business (d) Others

6. In this highly volatile market, do you think Mutual Funds are a destination for

Investments?

YES

NO

7. Which Mutual Fund Plan do you consider the best?

Balanced Plan

Equity Plan

Income Plan

Other Plan

1. How long would you like to hold your Mutual Funds' Investments?

1 to 3 years

4 to 6 years

7 to 10 years

10 years or more

2. How do you rate the risks associated with Mutual Funds?

Low

Moderate

High

3. Which among the following principles do you consider while selecting a Mutual Fund?

Enquiring about fund Managers

Finding about its Past Performance

Identifying your own objective

Other

4. Which end-scheme do you feel is good? *Open end type of mutual fund are those that

does not have restrictions on the amount of shares the fund will issue and Closed end

fund is a publicly traded investment company that raises a fixed amount of capital

through an initial public offering (IPO).

Open End

Close End

5. What is your annual income ?

Below Rs. 100000

100000 to 300000

300000 to 500000

Above 500000

6. What do you think which risks usually affects Mutual Funds? Systematic risk is the

risks inherent to the entire market segment as interest rates and unsystematic risks are

specific risks as NEWS that affects specific stock.

Systematic

Unsystematic

7. Which are the primary sources of your knowledge about Mutual Funds as an

investment option?

Television

Internet

Newspaper/Journals

Friends/Relatives

Sales

Representatives

15. While investing your money, how these factors affect your decision ? Corresponding to

your choices how would you rate their influence on your final Mutual Fund purchase

decision. Please rank them on a scale of 1-5 with 1 representing minimal influence and 5

representing Strong influence

1 2 3 4 5

Liquidity

High Return

Professional

Management

Diversification

Brand Image

Price

Risk

16. Which among the following is the safest Investment option?

Mutual Fund

Stock Market

Bank Deposit

Others

17. Which factors prevent you to invest in mutual fund?

Bitter Past Experience

Lack of Knowledge

Lack of Confidence in Service being provided

Difficulty in Selection of Schemes

Inefficient investment advisors

Other

18. Reason you make investment in mutual fund

Higher return

Tax benefit

Professional management

other

Anything you would like to add about mutual fund.

You are welcome

Data Analysis & Interpretation

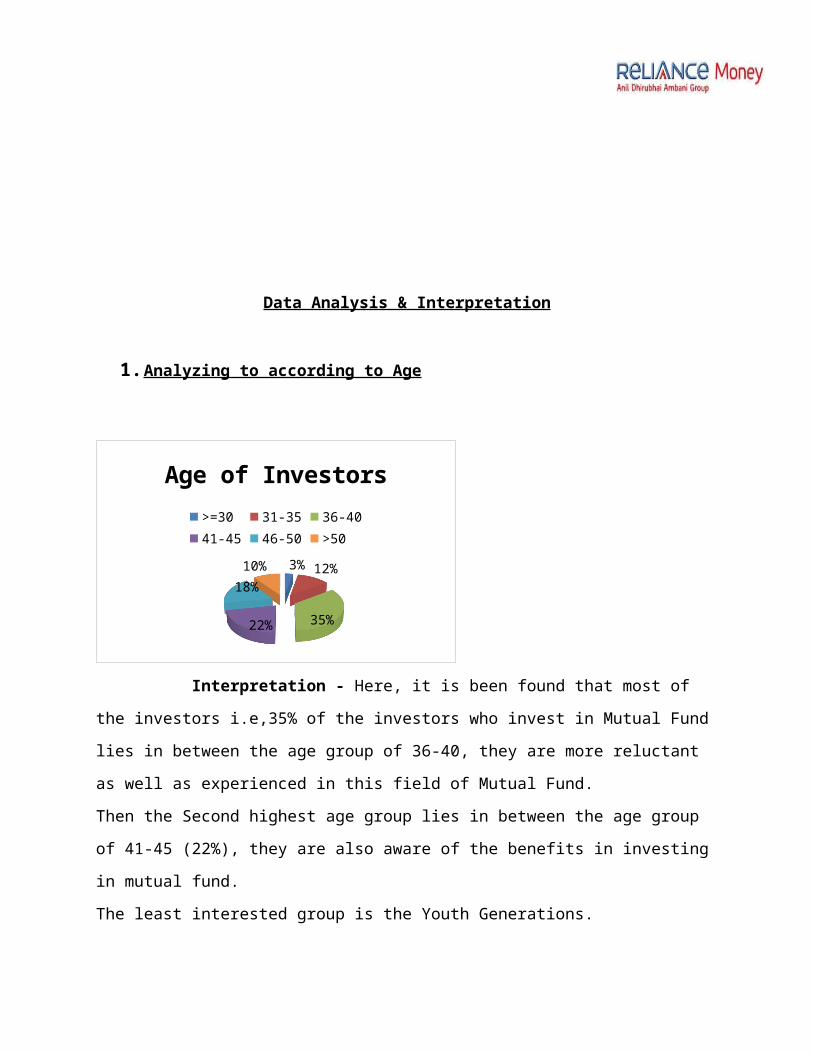

1. Analyzing to according to Age

3%12%

35%22%

18%

10%

Age of Investors>=30 31-35 36-40 41-45 46-50 >50

Interpretation - Here, it is been found that most of the investors i.e,35% of the investors

who invest in Mutual Fund lies in between the age group of 36-40, they are more reluctant as

well as experienced in this field of Mutual Fund.

Then the Second highest age group lies in between the age group of 41-45 (22%), they are also

aware of the benefits in investing in mutual fund.

The least interested group is the Youth Generations.

2. Analyzing according to Qualifiaction

Undergrad

uates

Grauad

tes

Post gra

duation

Others0

204060

Qualification of Investors

Qualification

No.

of I

nves

tors

Interpretation - Out of my survey of 100 people, 71% of the investors are Graduates and Post

Graduates and 16.67% are Under Graduates and Others, around 12.5%, which may include

persons who have passed their 10th standard or 12th standard invests in Mutual Funds.

3. Analyzing according to Occupation

Gov-ern-ment24%

Private46%

Business25%

Others5%

Investor's Proffession

Interpretation - Here it is amazed to see that around 46% of the investment is been invested by

the persons working in Private sectors, according to them investing in Mutual Funds is more

safer as well as more gainer.

Then we find that the businessmen of around 25%gives more preference in investing in mutual

funds, they think that investing in mutual fund is better than investing in shares as well as Post

office.

Next we see that the persons working in Government sectors of around 24% only invests in

Mutual Fund.

1. Analyzing according to Monthly Family Income

20%

25%

35%

20%

<30000030001-5000050001-100000<100000

Interpretation - Here , we find that HNI investors of around 35% with the monthly income of

Rs. 50001-100000 are the most likely to invest in Mutual fund , than followed by investors of

around 25% with monthly income of Rs 30001-50000 any other income group. And then 20% -

20 % by investors having monthly income of <30000and <100000

Analyzing investment in mutual fund on the basis of volatility in market

70%

30%

yesno

mutual fund as an invetment in volatile market

Interpretation- from the above pie chart it is clear that 70% of investors consider investment in

mutual fund as a destination in this highly volatile market where as 30% of investors consider

investment in mutual fund as a destination

Analysis on the basis of mutual fund plans investors consider

Blanced Equity plan Income plan Other0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

mutual fund plans

Interpretation- from the data collected through questionnaires I come to find that near

about 40% of investors invest in balanced funds ie.. in both equity and in debt fund keeping their

portfolio balanced .30% of the investors that were covered in the research finds equity plans

more beter than others and belive in taking more and more risk. 10% invest in income plans

which are also known as debt schemes. These schemes generally invest in fixed income

securities such as bonds and corporate debentures. Capital appreciation in such schemes may be

limited. and rest 20% invest in other plans such as tax saving plans, index plans etc

Analysis according to length of time to hold investment in mutual fund

20%

40%

35%

5%

time period of investing in mutual funds

1-3 years4-6years7-10 years 10 years or more

Interpretation- the above pie chart shows that most of the investors (40%) believe in investing

their in money in mutual funds for a period of 4-6 years, followed by 35% investors who do it

for 7-10 years ,20% investors invest in mutual funds for 1-3 years and only 5% do the same for

10 years

Analysis on the basis of risk associated with the mutual fund

low moderate high0%

10%

20%

30%

40%

50%

60%

70%

risk associated with mutual funds

responses

Interpretation- near about 65% of the investors stated that they consider mutual funds as a

moderate risk as these are linked to the equity market moreover this risk is minimized by the

professional expertise of fund manager and diversification.20 % of the investors consider it as a

less risky and near about 15 % consider it as more risky due to its ultimate investment in equity

market

Analysis according to the principles investors consider while selecting a Mutual Fund s

20%

47%

15%

18%

principal they consider while selecting mutual fun

Enquiring about fund ManagersFinding about its Past Per-formanceIdentifying your own objec-tiveother

Interpreation- from the above pie chart it is clear that 47 % of investors finds about the past

performance of the mutual funds before investing in to it. While 20 % of investors enquire about

the fund manager , 15% investors invest in mutual fund in accordance with their own objectives

which differ from person to person and near about 18% of investors consider other principals

than the above mentioned three principles

Analysis on the basis of end scheme thae the investor feel good

70%

30%

end schemes (open and closed )

Open EndClose End

Interepration- the above graph simply depicts that 70% of the investor consider open ended

mutual funds good as they can enter and exit at any time from these fundsand benefit of sip

where they can purchase more shares when the price of share is low.where as 30% of investors

consider closed ended funds better than open ended funds as they belive that its timein the that

akes difference not timing the market

A nalysis acording to the risk (systematic and unsystematic)that affect themutual fund more

80%

20%

risk that affect mtual fund

systematic riskunsystematic risk

Interpreation- near about 80% of investors feel that systematic risk ussauly affects the mutual

funds as these can not be diversified and for this reasion people condider it as a un-diversifiable

risk and so.me time market risk. Where as 20%of people also consider unsystematic risk who

deals in market for short time

Analysis on the basis of source of knowladge about mutual funds

Telev

ision

Internet

Newsp

aper/

Journals

Frien

ds/Rela

tives

Sales

Repres

entati

ves

0%5%

10%15%20%25%30%35%40%45%

primary source of knowladge

responses

Interpretation- among the 5 sources mentioned in the questioner most people(45%) get

knowladge about mutual fund through the sale representative , 20% through internet,near about

16% through newspaper and journals ,near about 14 percent through friends and relatives by

word of mouth and only 10 percent through television

(this may b because the research was conducted in chandigarh and for the HNI’s )

Analysis on the basis of the factors that affect investors decision While investing your

money

Liquidity

High Retu

rn

Profes

sional

Manag

emen

t

Diversi

fication

Brand Im

age

Price

Risk0%5%

10%15%20%25%30%35%

factors that affect the decesion

responses

Interpretation:30% of the people look for high returns while making the investment and rank it

as a number 1st in overall research where as 20% of people look for risk assosiated with the

mutual funds and it was ranked as 2nd factor in overall research.17 % of investor look for the

liquidity of the mutual funds and this factor was ranked 3rd in overall research .price of mutual

fund is also considered vital by 13% of people and was ranked 4th in over all research,8%,8% of

people considered professional management and diversification and ranked them as 5th and 6th

factor in overall research.and only 5% of people have cosidered brand image as important and it

is ranked 7th in over all research

Analysis on the basis of safest investment option

Mutual Fund Stock Market Bank Deposit Others0%

10%

20%

30%

40%

50%

60%

70%

safest Investment option

responses

Interpreation- the safest investment option that65% people consider is bank deposit and

thenfollowed by mutual fund where 25%people has mentioned it as safest and no one consider

stock market as safest.and 10 % of people feel that investment in gold, property etc is the most

safest

Analysis according to the factor that prevent investors to invest in mutual fund

23%

22%

23%

10%

20%

2%

factors that prevent investors to invest in mutual fund

Bitter Past ExperienceLack of KnowledgeLack of Confidence in Service being providedDifficulty in Selection of SchemesInefficient investment ad-visorsOther

Interpretation- from the above pie chart it is clear that 23%,23% of people avoid investing in

mutual funds beacause of bitter past experience and lack of confidence in service being provided,

22% of people don’t have the proper knowladge about the mutual funds and therefore don’t

invest in it. Where as 20% of the respondent feels that the tinvestment advisors are in

sufficient ,10% finds difficulty in selection of schemes and 2% have other reasion that prevents

them form making investment

Analysis on the basis of pourpose of investment in mutual funds