Myanmar | research reports Yangon SERVICED APARTMENT MARKET REPORT H1 2019 Lower grade apartments offer strong potential Summary • Midtown continues to dominate serviced apartment market • Wide variations in Grade B pricing and quality • Emergence of aparthotels beginning in Yangon • One-bedroom units command significantly higher rental rates per square metre HISTORICAL SUPPLY OF SERVICED APARTMENT UNITS IN YANGON Source: Picon-Deed Research Note 2014 – The number of units on the market fell after the closure of Grand Mee Ya Hta in Downtown (500) - 500 1,000 1,500 2,000 2,500 3,000 2013 2014 2015 2016 2017 2018 2019 est 2020 est 2021 est Units Supply at start of year New supply

Transcript

Myanmar | research reports

Yangon SERVICED APARTMENT MARKET REPORT H1 2019

Lower grade apartments offer strong potential

Summary • Midtown continues to dominate serviced apartment market

• Wide variations in Grade B pricing and quality

• Emergence of aparthotels beginning in Yangon

• One-bedroom units command significantly higher rental rates per square metre

HISTORICAL SUPPLY OF SERVICED APARTMENT UNITS IN YANGON

Source: Picon-Deed Research

Note 2014 – The number of units on the market fell after the closure of Grand Mee Ya Hta in Downtown

(500)

-

500

1,000

1,500

2,000

2,500

3,000

2013 2014 2015 2016 2017 2018 2019 est 2020 est 2021 est

Units

Supply at start of year New supply

Yangon Serviced Apartment Market Report H1 2019

2

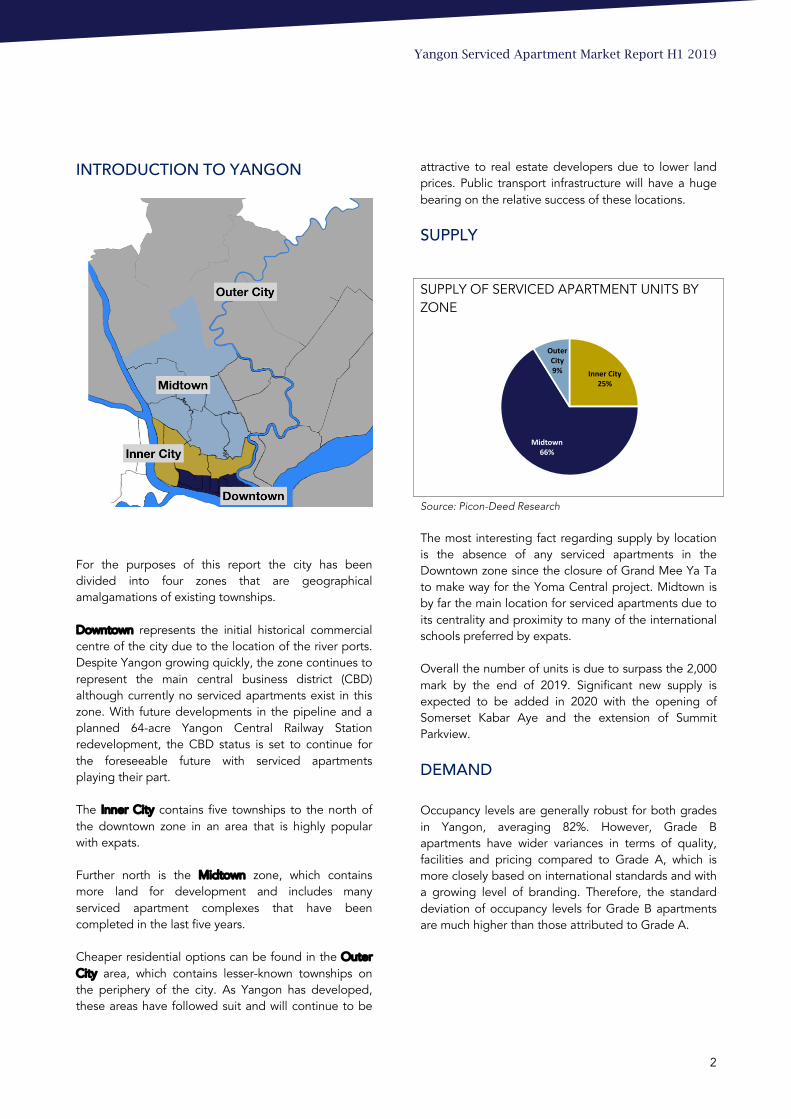

INTRODUCTION TO YANGON

For the purposes of this report the city has been divided into four zones that are geographical amalgamations of existing townships. Downtown represents the initial historical commercial centre of the city due to the location of the river ports. Despite Yangon growing quickly, the zone continues to represent the main central business district (CBD) although currently no serviced apartments exist in this zone. With future developments in the pipeline and a planned 64-acre Yangon Central Railway Station redevelopment, the CBD status is set to continue for the foreseeable future with serviced apartments playing their part. The Inner City contains five townships to the north of the downtown zone in an area that is highly popular with expats. Further north is the Midtown zone, which contains more land for development and includes many serviced apartment complexes that have been completed in the last five years. Cheaper residential options can be found in the Outer City area, which contains lesser-known townships on the periphery of the city. As Yangon has developed, these areas have followed suit and will continue to be

attractive to real estate developers due to lower land prices. Public transport infrastructure will have a huge bearing on the relative success of these locations.

SUPPLY

SUPPLY OF SERVICED APARTMENT UNITS BY ZONE

Source: Picon-Deed Research

The most interesting fact regarding supply by location is the absence of any serviced apartments in the Downtown zone since the closure of Grand Mee Ya Ta to make way for the Yoma Central project. Midtown is by far the main location for serviced apartments due to its centrality and proximity to many of the international schools preferred by expats. Overall the number of units is due to surpass the 2,000 mark by the end of 2019. Significant new supply is expected to be added in 2020 with the opening of Somerset Kabar Aye and the extension of Summit Parkview.

DEMAND Occupancy levels are generally robust for both grades in Yangon, averaging 82%. However, Grade B apartments have wider variances in terms of quality, facilities and pricing compared to Grade A, which is more closely based on international standards and with a growing level of branding. Therefore, the standard deviation of occupancy levels for Grade B apartments are much higher than those attributed to Grade A.

Inner City25%

Midtown66%

Outer City9%

Yangon Serviced Apartment Market Report H1 2019

3

OCCUPANCY AND STANDARD DEVIATION FOR SERVICED APARTMENTS BY GRADE

Source: Picon-Deed Research

Demand for Grade A apartments comes mainly from expats working at a senior level for multinational companies, embassies and NGOs. Due to the fact that such expats are likely to bring families; the need for larger sized units, often in the three-bedroom category, are in demand. As such, proximity to the high quality international schools is a main determinant of the popularity of 3-bedroom serviced apartments. The picture is more mixed for Grade B apartments, where tenants are more likely to be single and on a much lower housing budget more in line with smaller studios or one-bedroom units. Locations closer to shopping and entertainment are key considerations. A number of Grade B serviced apartments have high rental rates that are out of kilter to the wider market, where rates have been falling year-on-year for the past three years; as such those complexes have far lower occupancy rates.

RENTAL RATES

AVERAGE RENTAL RATES OF SERVICED APARTMENTS BY GRADE

Source: Picon-Deed Research

The general supply of larger three-bedroom units on the market for both serviced apartments and condominiums for rent means that rental rates per square metre are considerably lower than for smaller one and two-bedroom units. Grade A serviced apartments are considered to be of international quality with a more consistent level of quality, especially with the introduction of international brands. There is a greater variation in terms of quality for Grade B serviced apartments and rental rates also vary significantly.

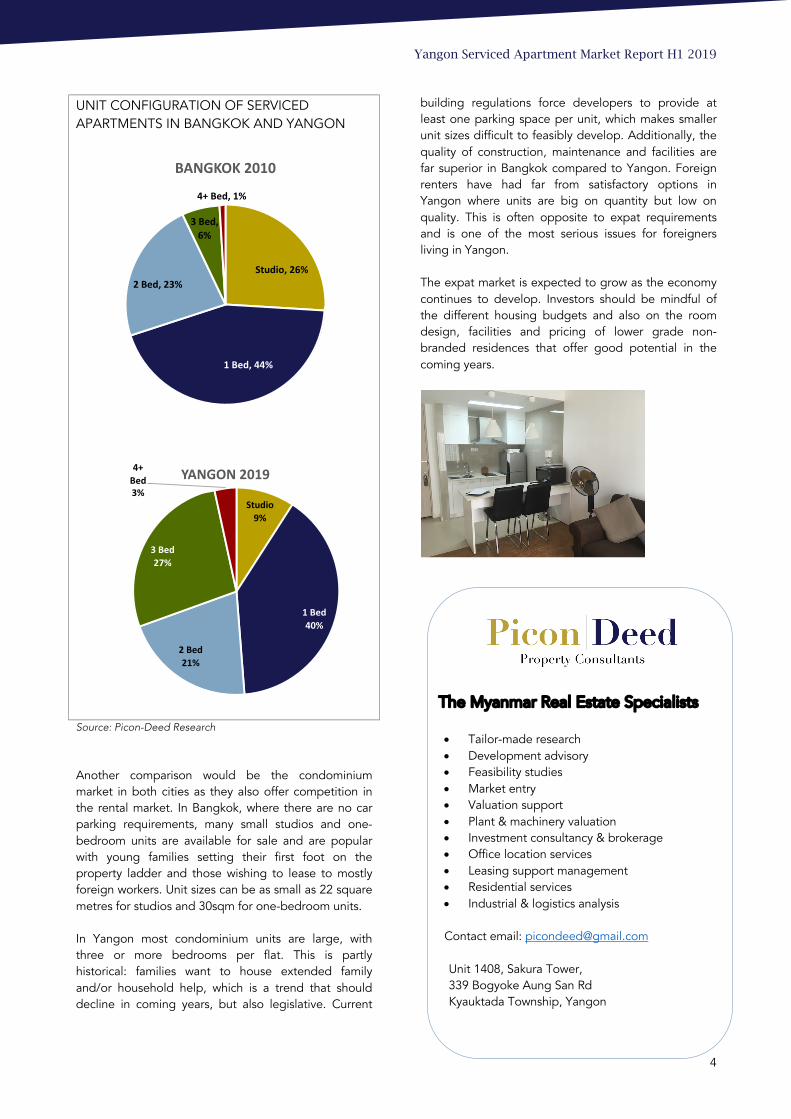

UNIT CONFIGURATIONS The market for studio and one-bedroom units is geared toward expats on lower housing budgets than is the case for three bedroom units in higher grade serviced apartments. Expat embassy staff, a significant number of NGOs and top executives of multinational companies have housing budgets starting from 5,000 USD and even single occupants in this category will take larger units fitting their generous budgets, rather than downgrade. A number of more affordable serviced apartments are refurbished older buildings, with unit configurations that are not fit for purpose, inefficient layouts and sub-optimal facilities. However, even new builds have not been developed with practical space allocation in mind. Although the trend is towards more minimalist design and sleeker furniture, just a small number of units can be categorized as truly space-saving. Only a limited number of units can be considered hybrid hotel design, although a number of future developments will focus on the aparthotel concept that is increasingly popular globally. The average unit configuration in Yangon has been repositioning away from the three-bedroom dominance that existed five years ago. Since then more mid-end apartments have been developed with a larger number of one-bedroom units; the recent extension of Sakura Residence added a significant number of one-bedroom units, with no three-bedroom units. However, compared to Bangkok the distribution of three-or-more-bedroom units is still high, making up 30% of supply in this category, compared to 7% in Bangkok. The other key difference is the proportion of studio units, which is far higher in Bangkok than Yangon.

0

5

10

15

20

25

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

90%

Grade A Grade B

Stan

dard

Dev

iatio

n

Aver

age

Occu

panc

y

Average Occupancy Occupancy Standard Deviation

USD 0 USD 10 USD 20 USD 30 USD 40 USD 50 USD 60

1 bedroom

2 bedroom

3 bedroom

Rent per sqm per month

Grade B Grade A

Yangon Serviced Apartment Market Report H1 2019

4

UNIT CONFIGURATION OF SERVICED APARTMENTS IN BANGKOK AND YANGON

Source: Picon-Deed Research

Another comparison would be the condominium market in both cities as they also offer competition in the rental market. In Bangkok, where there are no car parking requirements, many small studios and one-bedroom units are available for sale and are popular with young families setting their first foot on the property ladder and those wishing to lease to mostly foreign workers. Unit sizes can be as small as 22 square metres for studios and 30sqm for one-bedroom units. In Yangon most condominium units are large, with three or more bedrooms per flat. This is partly historical: families want to house extended family and/or household help, which is a trend that should decline in coming years, but also legislative. Current

building regulations force developers to provide at least one parking space per unit, which makes smaller unit sizes difficult to feasibly develop. Additionally, the quality of construction, maintenance and facilities are far superior in Bangkok compared to Yangon. Foreign renters have had far from satisfactory options in Yangon where units are big on quantity but low on quality. This is often opposite to expat requirements and is one of the most serious issues for foreigners living in Yangon. The expat market is expected to grow as the economy continues to develop. Investors should be mindful of the different housing budgets and also on the room design, facilities and pricing of lower grade non-branded residences that offer good potential in the coming years.