28

Myanmar’s Model Oil and Gas PSC 10 December 2012 Edwin Vanderbruggen Partner, VDB‐Loi Yangon

Myanmar’s Model Oil and Gas PSC

10 December 2012

Edwin Vanderbruggen Partner, VDB‐Loi Yangon

2

At a Glance

Transactions Investment M&AResourcesReal estate Energy

Half Law, Half TaxWe sell results, not time.

Our Commitment

More than 60Professional Advisers

Laos

Cambodia

Singapore

Vietnam

Indonesia

6 countriesMyanmar

Taxation StructuringInternationalComplianceCustoms Controversy

3

Key People on the Ground in MyanmarU Myo Nyunt is an advocate to the Supreme Courtof Myanmar and one of Myanmar’s mostdistinguished senior lawyers. He is the formerDirector of the Supreme Court and AppellateJudge, and a noted author on Myanmar law. He isa member of the Bar Council, and a member of theboard of editors of the Myanmar Law Review.

Marla is an American of Burmese descent with adegree in law from the College of Law of Englandand Wales and a bachelor’s degree from FordhamUniversity in New York. She advises on investmentand M&A transactions. She has seven years ofexperience with the United Nations and law firmsin New York. Marla lives in Yangon.

Cynthia qualified as a Chartered Accountant withErnst & Young in London. She is a member of theInstitute of Chartered Accountants of Scotland.She also holds a Master’s in engineering withbusiness finance (University College London, UK).She advises on investment projects and taxoptimization for mining, oil & gas, energy and realestate. Cynthia lives full‐time in Yangon.

Jean LoiManaging Partner

Jean Loi is widely recognized as one of the region’smost experienced professional advisers with a CPAbackground. She was formerly a partner withPricewaterhouseCoopers in Southeast Asia. As themanaging partner of VDB Loi, Jean has extensiveexperience with licensing energy, power, propertyand consumer product projects. Her Myanmar taxexperience is unsurpassed. She lives in Yangon.

Edwin VanderbruggenPartner, Yangon

Edwin was formerly with Loyens & Loeff and apartner at DFDL. He has 21 years of experience asa lawyer, academic and government advisor,including five years of experience on Myanmar taxand investment issues. Edwin has advised oilcompanies, distributors, property funds, andprivate equity funds on making investments inMyanmar. He lives full‐time in Yangon.

May May KyiDirector, Yangon

May directs our licensing team, focusing primarilyon investment permits, operating licenses andimport/export licensing. In addition, her practiceareas include customs duties, customs valuation,compliance and company establishment. She holdsa bachelor’s degree in Commerce from theInstitute of Economics, University of Yangon.

Paul Nikitopoulos Senior Counsel, Yangon

Paul is a US attorney with 15 years of experience,and was formerly with Clifford Chance andO’Melveny & Myers. He holds an MBA fromCambridge University and a J.D. from DukeUniversity. He has extensive experience inproviding integrated solutions for M&A and privateequity transactions. He lives full time in Yangon.

Kyi Naing is a Myanmar‐qualified lawyer withseven years of experience, most recently withDFDL in Myanmar. Experienced in cross‐borderlegal issues, he has assisted international clientswith their investment projects in Myanmar, andadvised on a wide range of corporate andcommercial issues.

U Myo NyuntSenior Counsel, Yangon

Marla BuAssociate, Yangon

Cynthia HermanTax Manager, Yangon

Kyi NaingAssociate, Yangon

4

Our Offices in Myanmar

YangonLevel 8 Centrepoint Towers

No. 65 Sule Pagoda Rd & Merchant StKyauktada Township

Nay Pyi TawNo. 2, Thittsar (2) Street,

Pobathiri Township

Contact: edwin@vdb‐loi.comTel. No.: +95 942 112 9769

5

Contents

Upcoming Tender Update

Impact of the New Foreign Investment Law

Fiscal Regime Misgivings

Accounting Obligations

Domestic Market Obligation

Farm‐in’s in Myanmar

Financing: Local Issues

Suitable International Structure

6

Selection of Shortlisted Bidders

Select Contractor and Draft PSC

Access to Data

Individual Negotiations

Upcoming Tender Update Onshore and offshore

Expression of Interest (EoI)

Supporting Documentation

What information is in the Tender Format?

Government Evaluates EoI’s

7

EXISTING PSCs

Tax holiday ‐ 3 years or 5 years? Customs duty exemption ‐ 3 years only or also during approved expansion?

NEW PSCs

Tax holiday ‐ 5 years from productionCustoms duty exemption ‐ 3 years plus any approved expansion

Art. 45 FIL 2012 Persons that have invested under the 1988 FIL are deemed

to have invested under this [new] law

Art. 52 FIL 2012Persons with existing investment contracts will continue to receive the benefits as provided under those contracts as

prescribed

Impact of the New Foreign Investment LawTax holiday of existing v new PSCs?

8

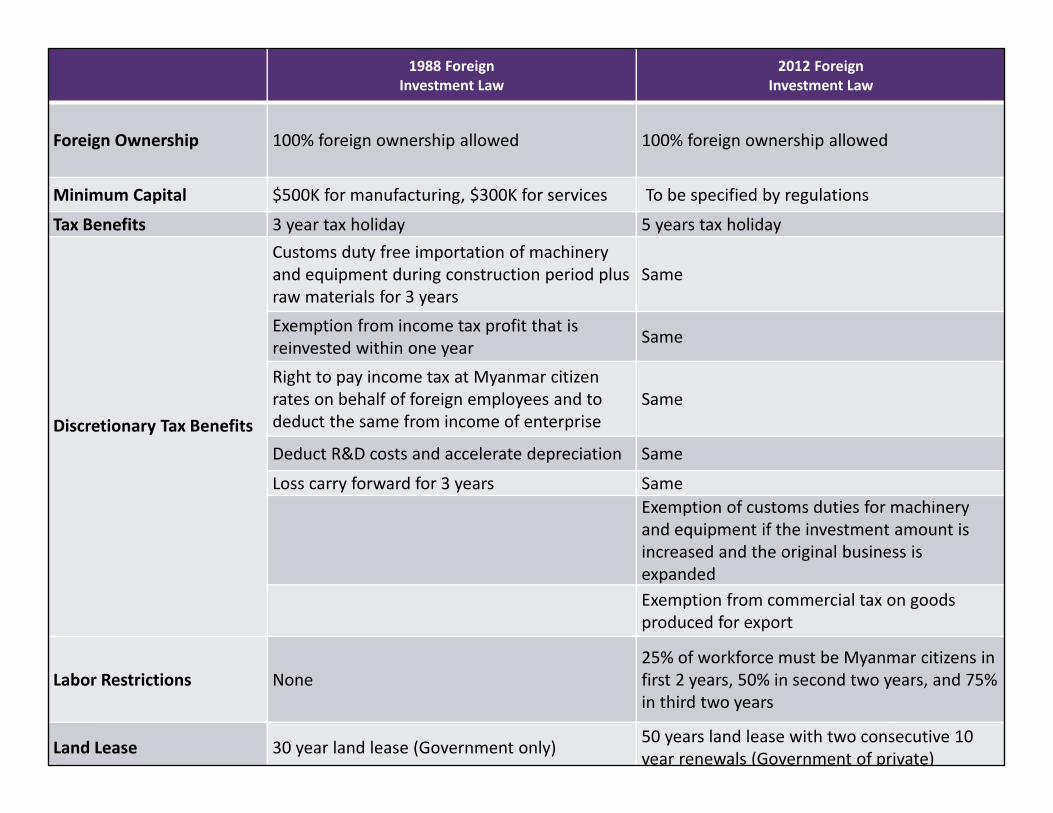

Impact of the New Foreign Investment LawComparison

1988 ForeignInvestment Law

2012 Foreign Investment Law

Foreign Ownership 100% foreign ownership allowed 100% foreign ownership allowed

Minimum Capital $500K for manufacturing, $300K for services To be specified by regulations

Tax Benefits 3 year tax holiday 5 years tax holiday

Discretionary Tax Benefits

Customs duty free importation of machinery and equipment during construction period plus raw materials for 3 years

Same

Exemption from income tax profit that is reinvested within one year Same

Right to pay income tax at Myanmar citizen rates on behalf of foreign employees and to deduct the same from income of enterprise

Same

Deduct R&D costs and accelerate depreciation Same

Loss carry forward for 3 years SameExemption of customs duties for machinery and equipment if the investment amount is increased and the original business is expandedExemption from commercial tax on goods produced for export

Labor Restrictions None25% of workforce must be Myanmar citizens in first 2 years, 50% in second two years, and 75% in third two years

Land Lease 30 year land lease (Government only) 50 years land lease with two consecutive 10 year renewals (Government of private)

9

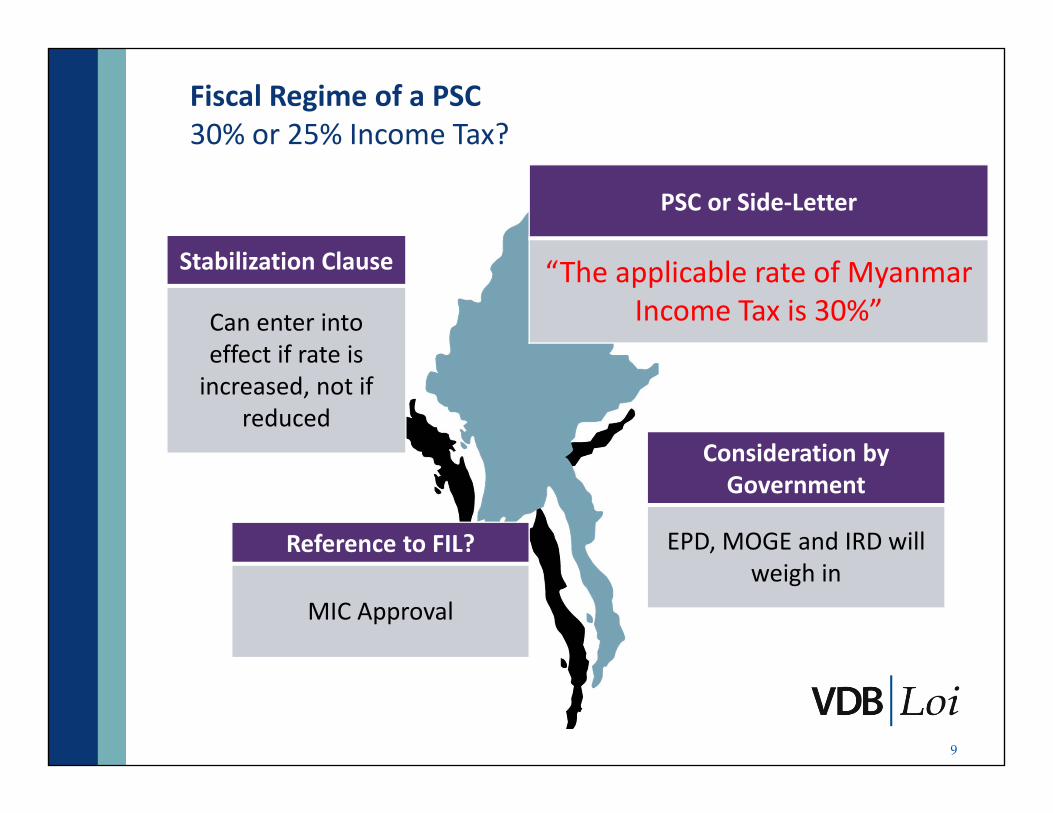

PSC or Side‐Letter

“The applicable rate of Myanmar Income Tax is 30%”

Consideration by Government

EPD, MOGE and IRD will weigh in

Reference to FIL?

MIC Approval

Stabilization Clause

Can enter into effect if rate is increased, not if

reduced

Fiscal Regime of a PSC30% or 25% Income Tax?

10

PSC Time vs Fiscal Regime

Exploration

3 Year

Development and Production

1 Year

1 Year

Signature BonusData Fee

Work Commitment Withholding Tax obligations

Training Fee

Study

6 Months

20 Year (from completion of development)

Production BonusRoyalty

MOGE’s Petroleum ShareIncome Taxes

Withholding Tax obligationsTraining Fee and R&D Fund

Drill 1 well, evaluation

Remote sensing, modeling

Drill 2 wells

Drill 1 well

Development Plan + bonus

Gas Sale Agreement

11

Fiscal Regime of a PSC

Profit Petroleum Income Taxation

Available Petroleum(produced not used in operations)

MOGE

Royalty (in cash or in kind)

Cost Petroleum (Recoverable)capped at 50% or 60% of Available

Petroleum per quarter

Profit Petroleum Shared between Company and

Government (40‐60%)

IRD

12

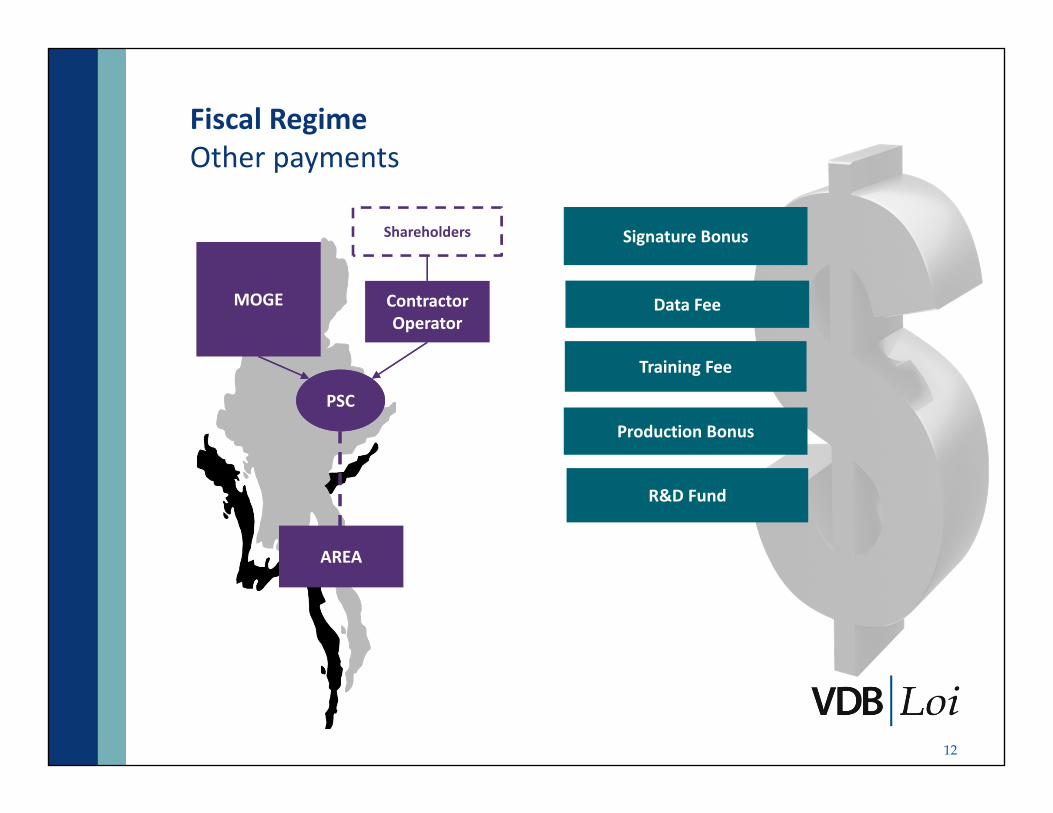

Fiscal RegimeOther payments

MOGE

Shareholders

Contractor Operator

PSCPSC

AREA

Signature Bonus

Production Bonus

Training Fee

R&D Fund

Data Fee

13

Fiscal RegimeTop 5 common misunderstandings

1.Loss carry forward (!)

2.Miscalculation of royalties in the Income Taxfinancial model (!)

3.Capital gains implications of farm‐in or carry

4.Misunderstanding of tax complianceobligations of non‐operator Contractors

5.Cost recovery and Income Tax calculation incase of multiple PSCs

14

Accounting RegimeCost Recovery

Item Issue

Operating costs When are operating costs deducted?

Capital expenditure What is the rate of amortization?

Capital expenditure for certainequipment

What if the Contractor uses equipment in multiple areas?

Employee costsAre benefits and taxes also recoverable?Do employees need to work in Myanmar

to trigger cost recovery?

15

Accounting RegimeCost Recovery

Item Issue

Training fees paid to theGovernment

Is this cost recoverable?

Materials supplied by theContractor

Cost recoverable at FMV or cost price?

Legal fees Which portion is cost recoverable?

General administrative andexecutive expenses

Are general expenses allocated from the head office cost recoverable, or tax

deductible?

16

Domestic Market ObligationPSC provisions

Specified in Section 16 of the PSC

•How much is the DMO?

• Crude Oil (proportion or 20%)

• Natural Gas (proportion or 25%)

•Selling price equals 90% of FMV

•Price applicable for Government purchases inexcess of the DMO

•Currency and remittance of purchase price?

17

Farm‐ins in Myanmar Myanmar Capital Gains Tax

Tax on Capital GainsResidents 10%

Non‐residents 40%

Oil & gas sector

40% for gains up to US$100M

45% for gains between US$100M and US$150M

50% for gains above US$150M

Income Tax LawCapital Assets

includeAssets of enterprise

Land

Shares

Compliance: tax return is due within 1 month following execution of the transfer or the date of delivery of the asset, whichever is earlier.

18

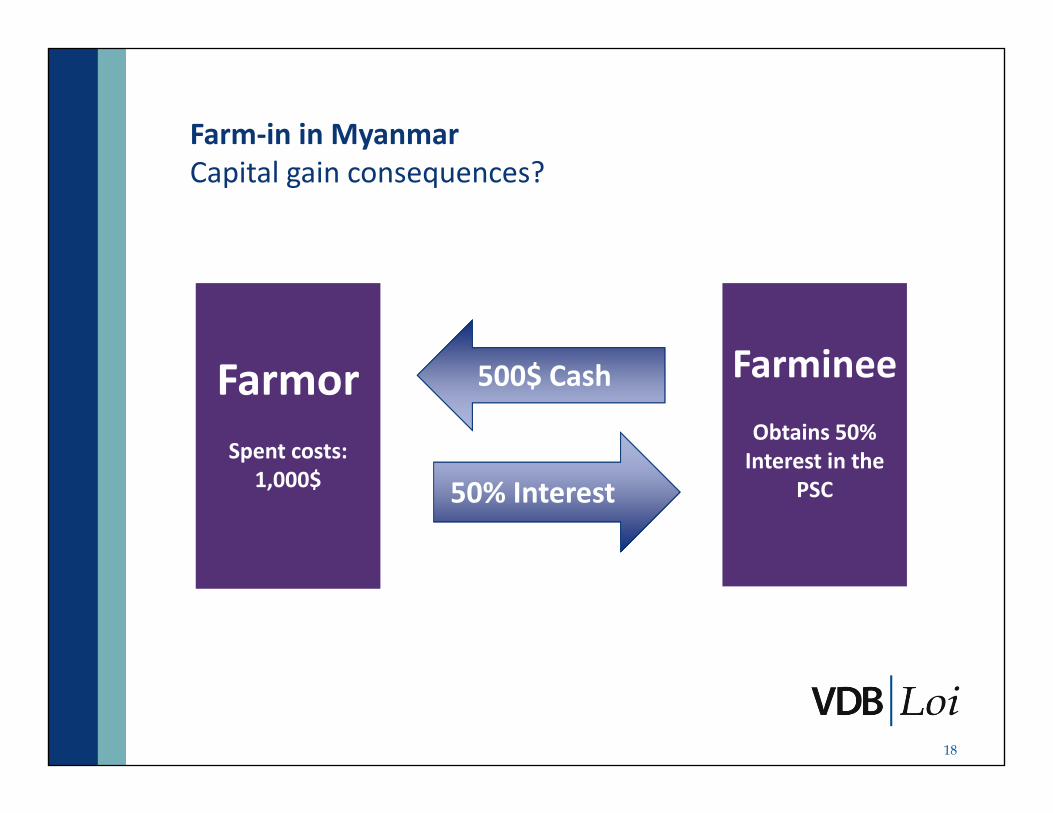

Farm‐in in MyanmarCapital gain consequences?

FarmorSpent costs:

1,000$

500$ Cash FarmineeObtains 50% Interest in the

PSC50% Interest

19

Farm‐in in MyanmarCapital gain consequences?

FarmorSpent costs:

1,000$

Commitment to pay 500$ forward costs Farminee

Obtains 50% Interest in the

PSC50% Interest

20

Farm‐in in MyanmarCapital gain consequences?

FarmorSpent costs:

1,000$

1000$ Cash FarmineeObtains 50% Interest in the

PSC50% Interest

21

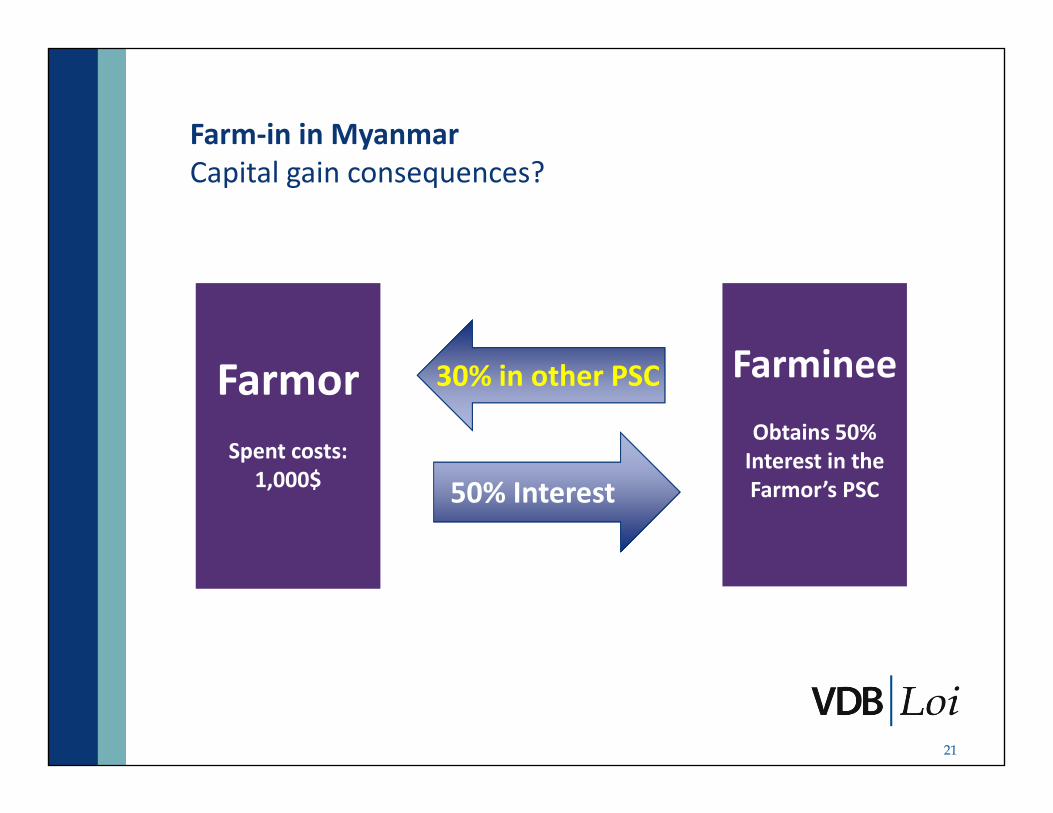

Farm‐in in MyanmarCapital gain consequences?

FarmorSpent costs:

1,000$

30% in other PSC FarmineeObtains 50% Interest in the Farmor’s PSC50% Interest

22

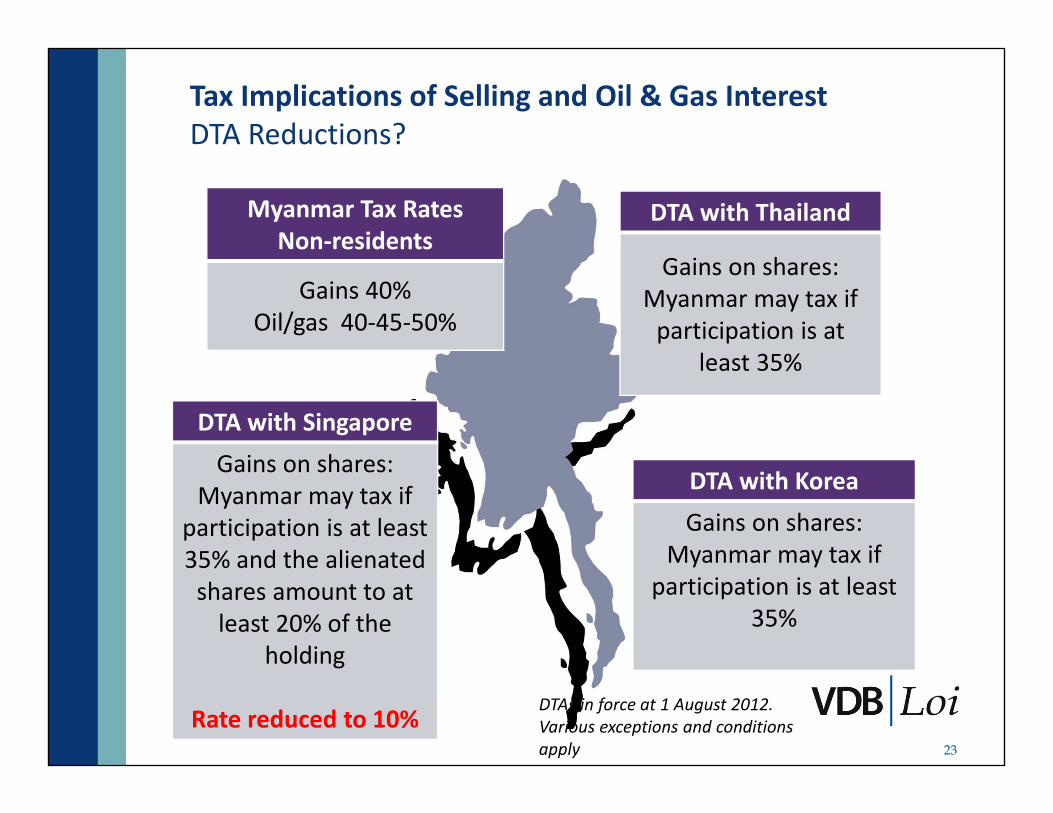

Myanmar Tax RatesNon‐residents

Gains 40%Oil/gas 40‐45‐50%

DTA with Vietnam

Gains on shares: Myanmar may tax

DTA with MalaysiaGains on shares:

Myanmar may tax if participation is at least

35%

DTA with UK

No article on capital gains

DTA with India

Gains on shares: Myanmar may tax

Tax Implications of Selling and Oil & Gas Interest DTA Reductions?

DTAs in force at 1 August 2012. Various exceptions and conditions apply

23

Myanmar Tax RatesNon‐residents

Gains 40%Oil/gas 40‐45‐50%

DTA with Thailand

Gains on shares: Myanmar may tax if participation is at

least 35%

DTA with KoreaGains on shares:

Myanmar may tax if participation is at least

35%

DTA with Singapore

Gains on shares: Myanmar may tax if

participation is at least 35% and the alienated shares amount to at least 20% of the

holding

Rate reduced to 10%

Tax Implications of Selling and Oil & Gas Interest DTA Reductions?

DTAs in force at 1 August 2012. Various exceptions and conditions apply

24

Financing Petroleum Operations Cost recovery and income tax deduction

ExplorationPhase

DevelopmentPhase

ProductionPhase

Recoverable?

Income Tax?

Recoverable?

Income Tax?

Recoverable?

Income Tax?

25

Will you be financing a branch or a subsidiary?

Withholding Tax on Interest

No DTA (US, Caymans, France, China, Russia, Australia, etc)

15%

UK No rule

India 10%

Korea 10%

Malaysia 10%

Thailand 10%

Vietnam 10%

Singapore 10% or 8%

Financing Petroleum Operations Withholding tax

26

Parent Company

Project CoSingapore

SubsidiaryMyanmar

No dividend withholding tax on payments to non‐resident

shareholders

No Income Tax on dividends received from Project Co

(conditions)No Capital Gains Tax

0‐10% Myanmar tax on capital gains instead of 40% or more

(conditions)

No dividend withholding tax under Myanmar tax law

Suitable International Structure? DTA Reductions

Financing10%WHT instead of

15%

27

Parent Company

Project CoSingapore

No dividend withholding tax on payments to non‐resident

shareholders

Credit (and Tax Sparing) for income received from Branch

(conditions)No Capital Gains Tax

10% Myanmar tax on capital gains instead of 40% or more

(conditions)

No branch remittance withholding tax under Myanmar tax law

Suitable International Structure? DTA Reductions

Financing15%‐10%WHT

Branch Myanmar

28

Thank You!

Edwin@vdb‐loi.com