Page 1

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 1/13

HIGHLIGHTSNORTH AMERICA

www.COllIERs.COM

Q3 2011 | IndustrIal

ROss J. MOORE Chief Economist | USA

The U.S. industrial market racked up another good quarter marked by rising occupancies and a dec

edly lower vacancy rate. Vacancies dropped in the majority of markets, and—with the exception of

Northeast—every region reported a lower vacancy rate for the quarter. Despite another considera

gain in occupancies, warehouse rents registered a further decrease, continuing an almost four-ye

trend.

With the economy registering modest growth in the third quarter, and similar expansion anticipated

the coming quarters, demand for warehouse space is expected to remain at currently levels. T

continued health of the manufacturing sector and a corresponding growth in exports remain key d

mand driver the nation’s industrial markets. As demonstrated by the Institute for Supply Managem

(ISM) index, manufacturing is o from the highs experienced in the spring, but remains in expans

territory. For October the ISM manufacturing index registered 50.8 (50 indicating expansion), wit

few sub-indexes such as new orders increasing signicantly from the previous month. Over the n

few quarters, the industrial market is expected to continue its slow crawl back to a more even balan

between supply and demand but no sharp snap back is anticipated.

With the latest slowdown in the global economy, a true rebound in the warehouse market is unlikely

occur before well into 2012. Warehouse construction, however, will remain at very low levels, so a

incremental increase in occupancies will immediately translate into lower vacancies. The rent pict

is unlikely to change soon, with vacancies still too high to give landlords any form of pricing pow

Look for the U.S.

industrial market to

surprise on the upsid

– the demand for qua

warehouse space is

quickly pushing

availabilities lower an

talk of speculative

construction is

beginning to be heard

select markets.

MARkET INdICATORsRelative to prior period

U.s. INdUsTRIAl MARkETsUMMARy sTATIsTICs, Q3 2011

U.S. Industrial Markets Showing MoreSigns of Strength

Q32011

Q42011*

VACANCy

NET ABsORPTION

CONsTRUCTION

RENTAl RATE

*Projected

U.s. INdUsTRIAl MARkET Q3 2009 – Q3 2011

Vacancy Rate: 9.99%Change from Q2 2011: -0.30%

Absorption:

36. Million Square Feet

New Construction:

1.4 Million Square Feet

Under Construction:

2. Million Square Feet

Asking Rents Per Square Foot

Average Warehouse/

Distribution Center: $4.3Change from Q2 2011: -2.7%

continued on pag

Absorption Completions Vacancy

Q3 2010Q2 2010Q1 2010Q4 2009Q3 2009

M i l l i o n S q u a r e F e e t

V a c a n c y ( % )

-50

-40

-30

-20

-10

0

10

20

30

40

50

8%

10%

12%

Q3 2011Q2 2011Q1 2011Q4 2010

10.50

10.90 11.10 11.00 11.00

10.8010.56

10.299.99

4%

6%

Page 2

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 2/13P. 2 | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

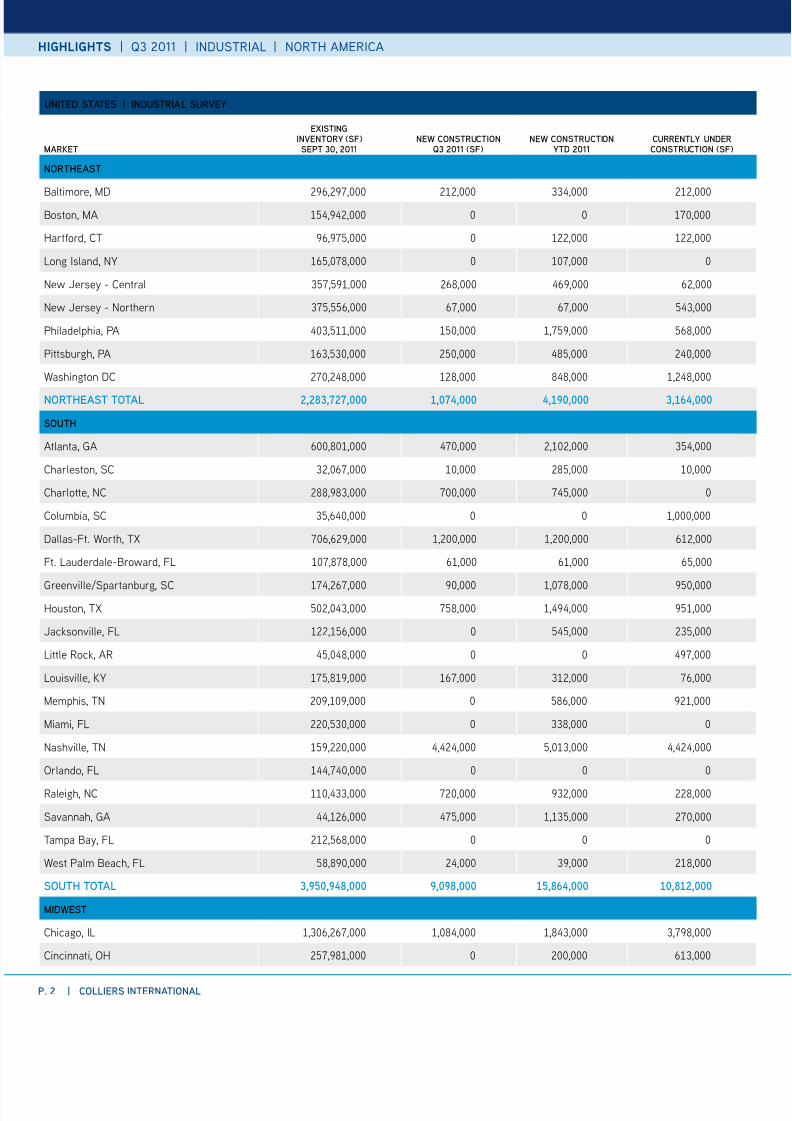

UNITEd sTATEs | INdUsTRIAl sURVEy

MARkET

EXIsTINGINVENTORy (sF)sEPT 30, 2011

NEw CONsTRUCTIONQ3 2011 (sF)

NEw CONsTRUCTIONyTd 2011

CURRENTly UNdERCONsTRUCTION (sF)

NORTHEAsT

Baltimore, MD 9,97, , 334, ,Boston, MA 4,94, 7,

Hartford, CT 9,97, , ,

Long Island, NY ,7, 7,

New Jersey - Central 37,9, , 49, ,

New Jersey - Northern 37,, 7, 7, 43,

Philadelphia, PA 43,, , ,79, ,

Pittsburgh, PA 3,3, , 4, 4,

Washington DC 7,4, , 4, ,4,

NORTHEAsT TOTAl ,8,, ,, ,, ,,

sOUTH

Atlanta, GA ,, 47, ,, 34,

Charleston, SC 3,7, , , ,

Charlotte, NC ,93, 7, 74,

Columbia, SC 3,4, ,,

Dallas-Ft. Worth, TX 7,9, ,, ,, ,

Ft. Lauderdale-Broward, FL 7,7, , , ,

Greenville/Spartanburg, SC 74,7, 9, ,7, 9,Houston, TX ,43, 7, ,494, 9,

Jacksonville, FL ,, 4, 3,

Little Rock, AR 4,4, 497,

Louisville, KY 7,9, 7, 3, 7,

Memphis, TN 9,9, , 9,

Miami, FL ,3, 33,

Nashville, TN 9,, 4,44, ,3, 4,44,

Orlando, FL 44,74,

Raleigh, NC ,433, 7, 93, ,

Savannah, GA 44,, 47, ,3, 7,

Tampa Bay, FL ,,

West Palm Beach, FL ,9, 4, 39, ,

sOUTH TOTAl ,5,8, ,8, 5,8, ,8,

MIdwEsT

Chicago, IL ,3,7, ,4, ,43, 3,79,

Cincinnati, OH 7,9, , 3,

Page 3

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 3/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRI

COllIERs INTERNATIONAl | P

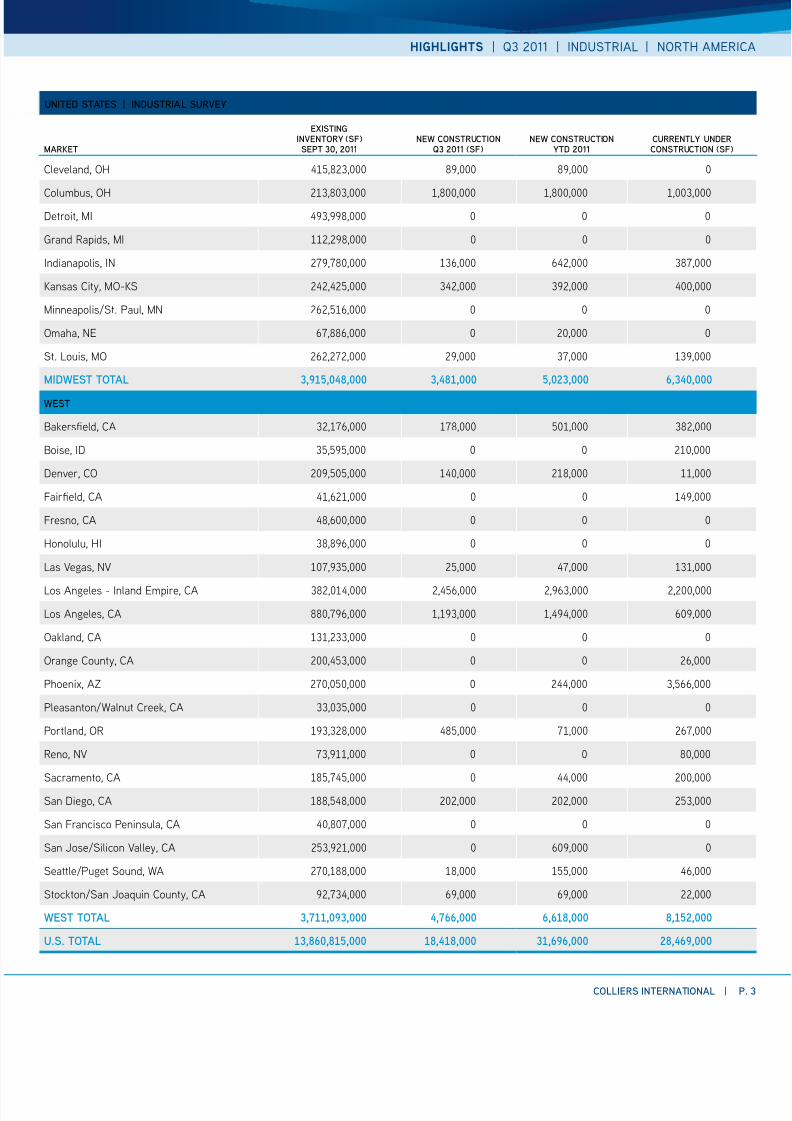

UNITEd sTATEs | INdUsTRIAl sURVEy

MARkET

EXIsTINGINVENTORy (sF)sEPT 30, 2011

NEw CONsTRUCTIONQ3 2011 (sF)

NEw CONsTRUCTIONyTd 2011

CURRENTly UNdERCONsTRUCTION (sF)

Cleveland, OH 4,3, 9, 9,

Columbus, OH 3,3, ,, ,, ,3,

Detroit, MI 493,99,

Grand Rapids, MI ,9,

Indianapolis, IN 79,7, 3, 4, 37,

Kansas City, MO-KS 4,4, 34, 39, 4,

Minneapolis/St. Paul, MN ,,

Omaha, NE 7,, ,

St. Louis, MO ,7, 9, 37, 39,

MIdwEsT TOTAl ,5,8, ,8, 5,, ,,

wEsT

Bakerseld, CA 3,7, 7, , 3,

Boise, ID 3,9, ,

Denver, CO 9,, 4, , ,

Faireld, CA 4,, 49,

Fresno, CA 4,,

Honolulu, HI 3,9,

Las Vegas, NV 7,93, , 47, 3,

Los Angeles - Inland Empire, CA 3,4, ,4, ,93, ,,

Los Angeles, CA ,79, ,93, ,494, 9,

Oakland, CA 3,33,

Orange County, CA ,43, ,

Phoenix, AZ 7,, 44, 3,,

Pleasanton/Walnut Creek, CA 33,3,

Portland, OR 93,3, 4, 7, 7,

Reno, NV 73,9, ,

Sacramento, CA ,74, 44, ,

San Diego, CA ,4, , , 3,

San Francisco Peninsula, CA 4,7,

San Jose/Silicon Valley, CA 3,9, 9,

Seattle/Puget Sound, WA 7,, , , 4,

Stockton/San Joaquin County, CA 9,734, 9, 9, ,

wEsT TOTAl ,,, ,, ,8, 8,5,

U.s. TOTAl ,8,85, 8,8, ,, 8,,

Page 4

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 4/13P. 4 | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

UNITEd sTATEs | INdUsTRIAl sURVEy

MARkETABsORPTIONQ3 2011 (sF)

ABsORPTIONyTd 2011

VACANCy RATEJUNE 30, 2011 (%)

VACANCy RATEsEPT. 30, 2011 (%)

NORTHEAsT

Baltimore, MD 34, 43, .4 .9

Boston, MA (4,) , . .7

Hartford, CT , 7, 9. 9.

Long Island, NY 93, (4,) .7 .

New Jersey - Central (,,) ,94, 9.79 .9

New Jersey - Northern (,,) (3,7,) . .7

Philadelphia, PA ,4, 3,74, 9. 9.3

Pittsburgh, PA (,) 99, .97 7.37

Washington DC 4, ,33, .9 .7

NORTHEAsT TOTAl (,,) ,85, . .5

sOUTH

Atlanta, GA 3,4, ,9, 4.4 3.3

Charleston, SC , ,37, .3 .4

Charlotte, NC ,4, 4,33, 3. .79

Columbia, SC , (9,) 7. .9

Dallas-Ft. Worth, TX ,3, ,7, .44 .3

Ft. Lauderdale-Broward, FL , (4,) 9.4 9.

Greenville/Spartanburg, SC ,, ,3, . 9.

Houston, TX 9, 3,3, .7 .7

Jacksonville, FL , 99, .97 .

Little Rock, AR 9, (9,) 4. 4.

Louisville, KY 34, ,947, .9 .

Memphis, TN (3,) ,, .9 .39

Miami, FL 47, ,3, .3 .47

Nashville, TN , 774, 4.4 .9

Orlando, FL 4, 999, .4 .3

Raleigh, NC ,3, ,3, .3 .4

Savannah, GA 3, ,99, . 4.

Tampa Bay, FL 43, ,7, .73 .43

West Palm Beach, FL , 44, 9. 9.4

sOUTH TOTAl ,, ,5, . .8

MIdwEsT

Chicago, IL 4,93, ,4, .7 .

Cincinnati, OH (39,) ,4, .77 .9

Page 5

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 5/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRI

COllIERs INTERNATIONAl | P

UNITEd sTATEs | INdUsTRIAl sURVEy

MARkETABsORPTIONQ3 2011 (sF)

ABsORPTIONyTd 2011

VACANCy RATEJUNE 30, 2011 (%)

VACANCy RATEsEPT. 30, 2011 (%)

Cleveland, OH (49,) (4,) 9. 9.

Columbus, OH ,, 3,3, . .

Detroit, MI ,39, ,3, 3.73 3.4

Grand Rapids, MI 9, 34, .9 .

Indianapolis, IN 477, ,7, . .4

Kansas City, MO-KS ,, 9, 7.9 .

Minneapolis/St. Paul, MN 44, 49, .7 .

Omaha, NE , 447, . .

St. Louis, MO (,4,) (,,) .49 .3

MIdwEsT TOTAl ,85, ,, . .

wEsT

Bakerseld, CA , 4, 9. 9.44

Boise, ID , (7,) .4 9.9

Denver, CO 7, , 7.9 7.

Faireld, CA , 3.33 .

Fresno, CA 3, 7, . .73

Honolulu, HI 9, (,) 4.73 4.7

Las Vegas, NV (3,) 3, .9 .3

Los Angeles - Inland Empire, CA 4,, 3,374, 9.4 7.

Los Angeles, CA ,, ,4, .3 .

Oakland, CA (7,) 3, .7 9.

Orange County, CA 37, ,7, .4 4.7

Phoenix, AZ ,, 3,, . 4.

Pleasanton/Walnut Creek, CA (37,) (497,) .33 .4

Portland, OR 99, ,79, 9. .

Reno, NV , 3, .4 4.94

Sacramento, CA 4, 93, 3. .77

San Diego, CA 33, , .44 .

San Francisco Peninsula, CA (,) 3, .94 9.4

San Jose/Silicon Valley, CA (3,) 4, 3.4 .

Seattle/Puget Sound, WA ,33, 3,7, 7.4 7.

Stockton/San Joaquin County, CA 34, ,7, . .3

wEsT TOTAl ,85, ,5, . 8.

U.s. TOTAl ,5, ,, . .

Page 6

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 6/13P. 6 | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

UNITEd sTATEs | INdUsTRIAl sURVEy | sAlEs PRICE ANd CAP RATE As OF sEPTEMBER 2011

MARkETsAlEs PRICE

(Usd PsF)CAP RATE

(%)VACANCy FORECAsT

(3 MONTHs)ABsORPTION FORECAsT

(3 MONTHs)RENT FORECAsT

3 MONTHs

NORTHEAsT

Baltimore, MD .3 7.9 Same Same Bottoming

Boston, MA Same Same Bottoming

Hartford, CT 3. . Up Same Declining

Long Island, NY . .4 Same Same Declining

New Jersey - Central .9 7.9 Up Down Bottoming

New Jersey - Northern .4 Up Down Bottoming

Philadelphia, PA .3 . Down Up No clear direction

Pittsburgh, PA . 7.7 Same Up Increasing

Washington DC 9. . Down Up No clear direction

NORTHEAsT AVERAGE .5 . – – –

sOUTH

Atlanta, GA 37.4 .7 Down Down Same

Charleston, SC 4. 7.7 Down Same Up

Columbia, SC Down Up Up

Dallas-Ft. Worth, TX . 7. Down Same Same

Ft. Lauderdale-Broward, FL 3.7 .7 Same Up Same

Greenville/Spartanburg, SC .7 9. Down Up Up

Houston, TX 4. 7.9 Down Up Up

Jacksonville, FL . Down Down Same

Little Rock, AR .4 9. Same Same Same

Memphis, TN 3. .9 Down Up Same

Miami, FL 7.93 Same Up Up

Nashville, TN 4. . Down Down Up

Orlando, FL . Down Same Same

Raleigh, NC 4. .4 Down Up Same

Savannah, GA 37. . Same Same Same

Tampa Bay, FL 39.7 . Down Up Same

West Palm Beach, FL 3.7 Same Up Down

sOUTH AVERAGE . 8. – – –

MIdwEsT

Chicago, IL 49. .7 Same Down Same

Cincinnati, OH 3. . Same Same Same

Columbus, OH . Down Up Same

Page 7

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 7/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRI

COllIERs INTERNATIONAl | P

UNITEd sTATEs | INdUsTRIAl sURVEy | sAlEs PRICE ANd CAP RATE As OF sEPTEMBER 2011

MARkETsAlEs PRICE

(Usd PsF)CAP RATE

(%)VACANCy FORECAsT

(3 MONTHs)ABsORPTION FORECAsT

(3 MONTHs)RENT FORECAsT

3 MONTHs

Detroit, MI . Same Same Down

Grand Rapids, MI . 3. Down Up Up

Indianapolis, IN 44. . Down Up Up

Kansas City, MO-KS .7 Same Same Same

Minneapolis/St. Paul, MN 3.97 . Down Same Same

Omaha, NE 4. 9. Down Up Same

MIdwEsT AVERAGE .8 . – – –

wEsT

Bakerseld, CA 3. . Same Same Same

Boise, ID 4. Same Same Same

Denver, CO . . Down Up Same

Faireld, CA Same Same Down

Fresno, CA 3. 9. Same Same Same

Honolulu, HI Up Down Same

Las Vegas, NV 33.9 Up Up Down

Los Angeles - Inland Empire, CA . . Down Up Up

Los Angeles, CA . . Same Same Same

Oakland, CA .97 . Down Up Up

Orange County, CA 94. . Same Same Same

Phoenix, AZ 49. . Down Same Same

Pleasanton/Walnut Creek, CA 9. . Same Same Same

Portland, OR 3.4 Same Same Same

Reno, NV Down Same Same

Sacramento, CA 44. .7 Same Same Same

San Diego, CA 79.97 . Down Same Same

San Francisco Peninsula, CA . . Same Same Same

San Jose/Silicon Valley, CA Up Same Same

Seattle/Puget Sound, WA 7.4 .44 Down Up Same

Stockton/San Joaquin County, CA . 7. Down Up Same

wEsT AVERAGE .5 .5 – – –

U.s. AVERAGE 55. 8.5 – – –

Page 8

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 8/13P. | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

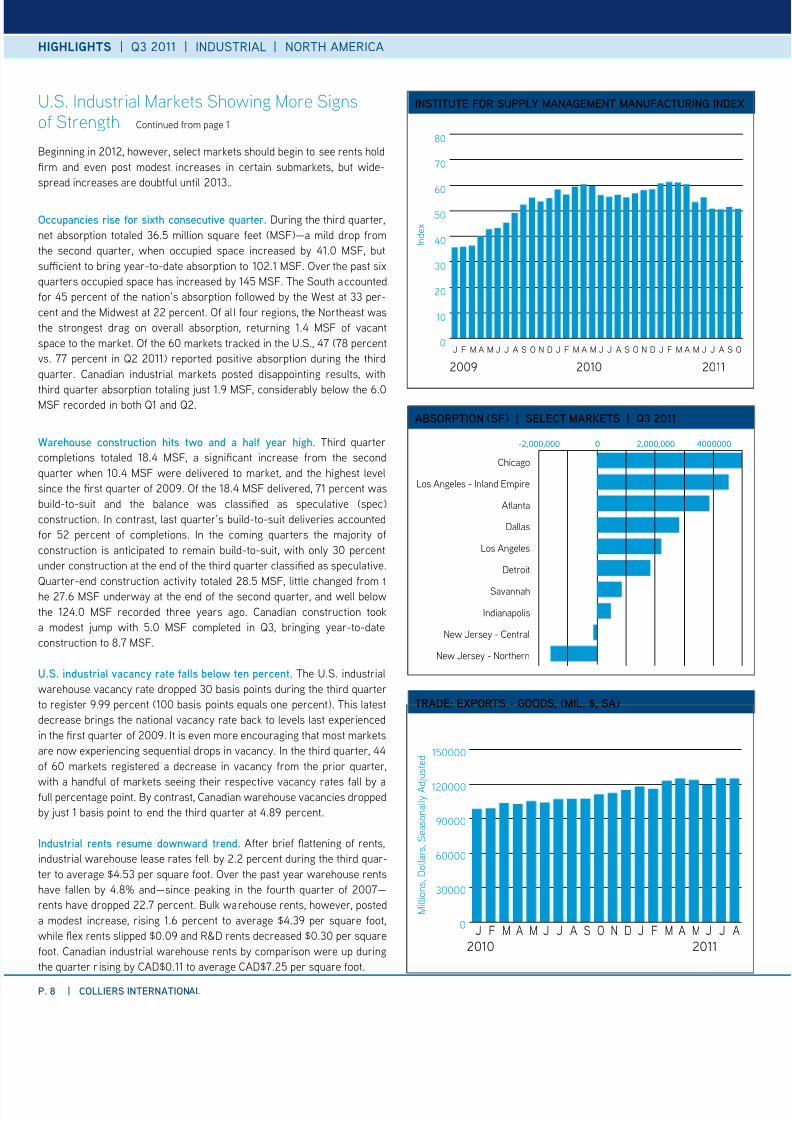

Beginning in 2012, however, select markets should begin to see rents hold

rm and even post modest increases in certain submarkets, but wide-

spread increases are doubtful until 2013..

Occupancie rie for ixth conecutive quarter. During the third quarter,

net absorption totaled 6.5 million square feet (MSF)—a mild drop from

the second quarter, when occupied space increased by 1.0 MSF, but

sucient to bring year-to-date absorption to 102.1 MSF. Over the past six

quarters occupied space has increased by 15 MSF. The South accounted

for 5 percent of the nation’s absorption followed by the West at per-

cent and the Midwest at 22 percent. Of al l four regions, the Northeast was

the strongest drag on overall absorption, returning 1. MSF of vacant

space to the market. Of the 60 markets tracked in the U.S., (8 percent

vs. percent in Q2 2011) reported positive absorption during the third

quarter. Canadian industrial markets posted disappointing results, with

third quarter absorption totaling just 1. MSF, considerably below the 6.0MSF recorded in both Q1 and Q2.

warehoue contruction hit to an a haf ear high. Third quarter

completions totaled 18. MSF, a signicant increase from the second

quarter when 10. MSF were delivered to market, and the highest level

since the rst quarter of 200. Of the 18. MSF delivered, 1 percent was

build-to-suit and the balance was classied as speculative (spec)

construction. In contrast, last quarter’s build-to-suit deliveries accounted

for 52 percent of completions. In the coming quarters the majority of

construction is anticipated to remain build-to-suit, with only 0 percent

under construction at the end of the third quarter classied as speculative.

Quarter-end construction activity totaled 28.5 MSF, little changed from t

he 2.6 MSF underway at the end of the second quarter, and well below

the 12.0 MSF recorded three years ago. Canadian construction took

a modest jump with 5.0 MSF completed in Q, bringing year-to-date

construction to 8. MSF.

U.s. inutria vacanc rate fa beo ten percent. The U.S. industrial

warehouse vacancy rate dropped 0 basis points during the third quarter

to register . percent (100 basis points equals one percent). This latest

decrease brings the national vacancy rate back to levels last experienced

in the rst quarter of 200. It is even more encouraging that most markets

are now experiencing sequential drops in vacancy. In the third quarter,

of 60 markets registered a decrease in vacancy from the prior quarter,

with a handful of markets seeing their respective vacancy rates fall by afull percentage point. By contrast, Canadian warehouse vacancies dropped

by just 1 basis point to end the third quarter at .8 percent.

Inutria rent reume onar tren. After brief attening of rents,

industrial warehouse lease rates fell by 2.2 percent during the third quar-

ter to average $.5 per square foot. Over the past year warehouse rents

have fallen by .8% and—since peaking in the fourth quarter of 200—

rents have dropped 22. percent. Bulk warehouse rents, however, posted

a modest increase, rising 1.6 percent to average $. per square foot,

while ex rents slipped $0.0 and R&D rents decreased $0.0 per square

foot. Canadian industrial warehouse rents by comparison were up during

the quarter rising by CAD$0.11 to average CAD$.25 per square foot.

U.S. Industrial Markets Showing More Signsof Strength

I n d e x

0

10

20

30

40

50

60

70

80

2009 2010 2011

OSAJJMAMFJDNOSAJJMAMFJDNOSAJJMAMFJ

INsTITUTE FOR sUPPly MANAGEMENT MANUFACTURING INdEX

-2,000,000 0 2,000,000 4000000

New Jersey - Northern

New Jersey - Central

Indianapolis

Savannah

Detroit

Los Angeles

Dallas

Atlanta

Los Angeles - Inland Empire

Chicago

ABsORPTION (sF) | sElECT MARkETs | Q3 2011

0

30000

60000

90000

120000

150000

2010 2011

M i l l i o n s ,

D o l l a r s ,

S e a s o n a l l y A d

j u s t e d

AJJMAMFJDNOSAJJMAMFJ

TRAdE: EXPORTs - GOOds, (MIl. $, sA)

Continued from page 1

Page 9

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 9/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRI

COllIERs INTERNATIONAl | P

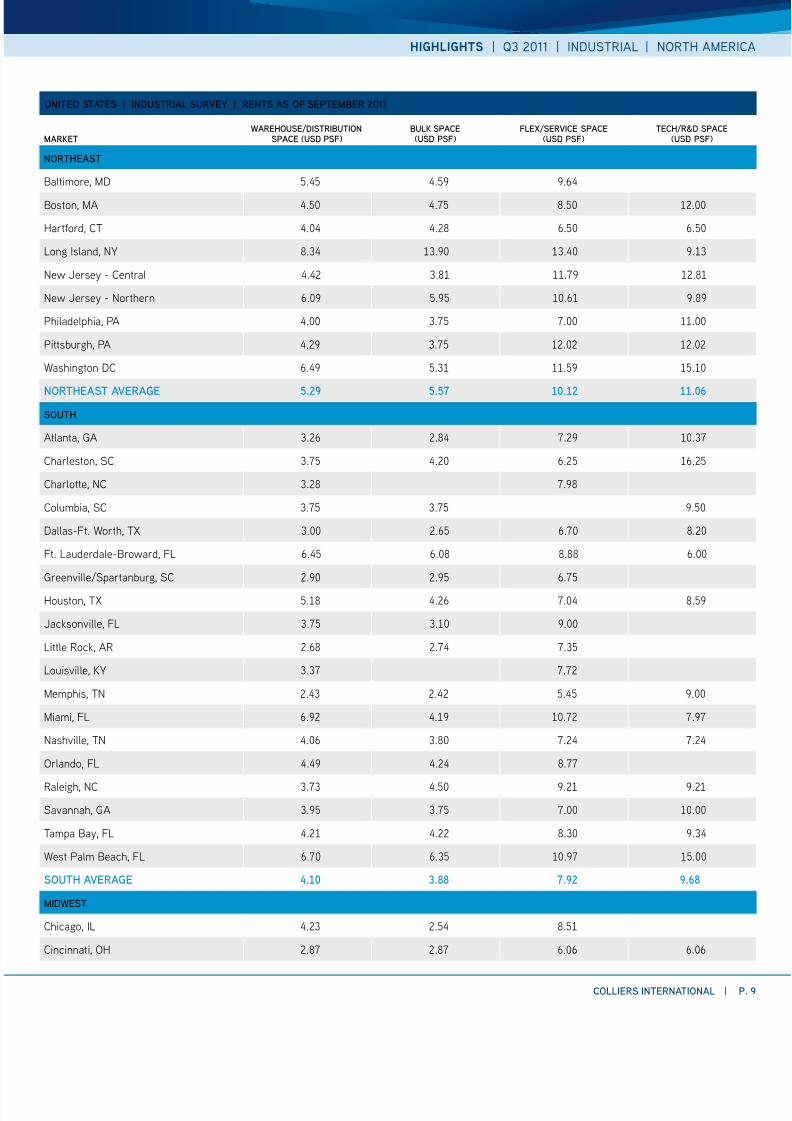

UNITEd sTATEs | INdUsTRIAl sURVEy | RENTs As OF sEPTEMBER 2011

MARkETwAREHOUsE/dIsTRIBUTION

sPACE (Usd PsF)BUlk sPACE(Usd PsF)

FlEX/sERVICE sPACE(Usd PsF)

TECH/R&d sPACE(Usd PsF)

NORTHEAsT

Baltimore, MD .4 4.9 9.4

Boston, MA 4. 4.7 . .

Hartford, CT 4.4 4. . .

Long Island, NY .34 3.9 3.4 9.3

New Jersey - Central 4.4 3. .79 .

New Jersey - Northern .9 .9 . 9.9

Philadelphia, PA 4. 3.7 7. .

Pittsburgh, PA 4.9 3.7 . .

Washington DC .49 .3 .9 .

NORTHEAsT AVERAGE 5. 5.5 . .

sOUTH

Atlanta, GA 3. .4 7.9 .37

Charleston, SC 3.7 4. . .

Charlotte, NC 3. 7.9

Columbia, SC 3.7 3.7 9.

Dallas-Ft. Worth, TX 3. . .7 .

Ft. Lauderdale-Broward, FL .4 . . .

Greenville/Spartanburg, SC .9 .9 .7

Houston, TX . 4. 7.4 .9

Jacksonville, FL 3.7 3. 9.

Little Rock, AR . .74 7.3

Louisville, KY 3.37 7.7

Memphis, TN .43 .4 .4 9.

Miami, FL .9 4.9 .7 7.97

Nashville, TN 4. 3. 7.4 7.4

Orlando, FL 4.49 4.4 .77

Raleigh, NC 3.73 4. 9. 9.

Savannah, GA 3.9 3.7 7. .

Tampa Bay, FL 4. 4. .3 9.34

West Palm Beach, FL .7 .3 .97 .

sOUTH AVERAGE . .88 . .8

MIdwEsT

Chicago, IL 4.3 .4 .

Cincinnati, OH .7 .7 . .

Page 10

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 10/13P. 10 | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

UNITEd sTATEs | INdUsTRIAl sURVEy | RENTs As OF sEPTEMBER 2011

MARkETwAREHOUsE/dIsTRIBUTION

sPACE (Usd PsF)BUlk sPACE(Usd PsF)

FlEX/sERVICE sPACE(Usd PsF)

TECH/R&d sPACE(Usd PsF)

Cleveland, OH 3.37 .

Columbus, OH .7 . 4. 4.

Detroit, MI 3.7 3. 7.9

Grand Rapids, MI 3. 3. 4. .

Indianapolis, IN 3. 3. 7.

Kansas City, MO-KS 3. 3. 7. .

Minneapolis/St. Paul, MN 4.7 4. 4.7

Omaha, NE .7 .9 .73 3.7

St. Louis, MO 3. .9

MIdwEsT AVERAGE . . . 5.5

wEsT

Bakerseld, CA 4. 3.4 .

Boise, ID 4. 4. . .3

Denver, CO 3. 3. . 9.

Faireld, CA .4 .3 .4 .7

Fresno, CA .4 . 4. .

Las Vegas, NV 4. 4. .4 9.

Los Angeles - Inland Empire, CA 3.9 3.79 .7 7.7

Los Angeles, CA .74 . 9.7 .

Oakland, CA 4.37 4. 4. 7.7

Orange County, CA .73 .3 . 3.9

Phoenix, AZ . 4. .3 .

Pleasanton/Walnut Creek, CA .4 4. .3 .3

Portland, OR . 4.7 9.44 9.9

Reno, NV 3.4 4. .4 .4

Sacramento, CA 4.9 3.7 .3 .7

San Diego, CA .4 7.44 . 4.4

San Francisco Peninsula, CA 9.4 9.4 . .

San Jose/Silicon Valley, CA .3 . .4 3.

Seattle/Puget Sound, WA .9 . .

Stockton/San Joaquin County, CA 3.4 3. .44 7.44

wEsT AVERAGE 5.8 . 8.88 .

Us AVERAGE .5 . 8. .

U.s. QUARTERly CHANGE -.% .% -.% -.%

Page 11

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 11/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRI

COllIERs INTERNATIONAl | P

CANAdA | INdUsTRIAl sURVEy

MARkET

EXIsTINGINVENTORy (sF)sEPT 30, 2011

NEw CONsTRUCTIONQ3 2011 (sF)

NEw CONsTRUCTIONyTd 2011

CURRENTly UNdERCONsTRUCTION (sF)

Calgary, AB 4,4, ,7, ,7, ,7,

Edmonton, AB 77,4, 3, 9,

Guelph, ON 9,94, , , 9,

Halifax, NS 7,7, , ,

Montreal, QC 347,77, ,

Ottawa, ON ,7,

Regina, SK ,9, 3, 99,

Saskatoon, SK ,, , 4, 4,

Toronto, ON 7,9, 77, ,7, ,9,

Vancouver, BC 79,3, ,, ,, ,,

Victoria, BC ,9, 43, ,

Waterloo Region, ON ,7, 9, 9, ,

CANAdA TOTAl ,5,8, ,, ,, 8,8,

CANAdA | INdUsTRIAl sURVEy

MARkETABsORPTIONQ3 2011 (sF)

ABsORPTIONyTd 2011

VACANCy RATEJUNE 30, 2011 (%)

VACANCy RATEsEPT. 30, 2011 (%)

Calgary, AB ,, ,4, .3 4.3

Edmonton, AB 7, , 3.4 3.4

Guelph, ON 9, , 3. 3.

Halifax, NS 7, (97,) .93 .3

Montreal, QC (,7,) (77,) .4 .

Ottawa, ON 9, (,) 7. .4

Regina, SK (4,) , .9 .

Saskatoon, SK 4, 3, .7 3.7

Toronto, ON ,34, 9,7, 4.97 4.9

Vancouver, BC , ,3, 4. 4.9

Victoria, BC , 3.37 3.37

Waterloo Region, ON (,) (44,) . .3

CANAdA TOTAl ,8, ,, . .8

Page 12

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 12/13P. 12 | COllIERs INTERNATIONAl

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

CANAdA | INdUsTRIAl sURVEy | sAlEs PRICE ANd CAP RATE As OF sEPTEMBER 2011

MARkETsAlEs PRICE

(CAd PsF)CAP RATE

(%)VACANCy FORECAsT

(3 MONTHs)ABsORPTION FORECAsT

(3 MONTHs)RENT FORECAsT

3 MONTHs

Calgary, AB . .7 Down Up Increasing

Edmonton, AB .4 7.44 Up Down Bottoming

Guelph, ON 4. . Same Same No clear direction

Halifax, NS 9. 7.7 Down Up Increasing

Montreal, QC . . Same Same No clear direction

Ottawa, ON . . Down Up No clear direction

Regina, SK 3. 7. Same Same Peaking

Saskatoon, SK 3. 7. Same Same Peaking

Toronto, ON 7. .7 Down Up Bottoming

Vancouver, BC . . Same Same Bottoming

Victoria, BC 7. .7 Down Up Bottoming

Waterloo Region, ON 3. . Same Same No clear direction

CANAdA AVERAGE . .5 – – –

CANAdA | INdUsTRIAl sURVEy | RENTs As OF sEPTEMBER 2011

MARkETwAREHOUsE/dIsTRIBUTION

sPACE (CAd PsF)BUlk sPACE(CAd PsF)

FlEX/sERVICE sPACE(CAd PsF)

TECH/R&d sPACE(CAd PsF)

Calgary, AB . . . .

Edmonton, AB 7.7 . 9. .

Guelph, ON 4.4 4.4 7.7 7.7

Halifax, NS 7.7 . . .

Montreal, QC 4.7 4. . .

Ottawa, ON 7. 7. . .Regina, SK 9. 7. . 4.

Saskatoon, SK 9. . . 3.

Toronto, ON 4.9 4.4 7.4 7.

Vancouver, BC 7.44 7. . 9.

Victoria, BC . . 3. 3.

Waterloo Region, ON 4.3 3.4 . .

CANAdA AVERAGE .5 . . .5

CANAdA QUARTERly CHANGE .% .5% -.% .%

GlossaryAborption – Net change in leased space over agiven period of time.

Bu space – 100,000 square feet or more with upto 10 percent oce space, the balance being generalwarehouse space with 20 to 6 foot ceiling heights.All loading is dock-height.

Fex space – Single-story buildings having 10- to18-foot ceilings with both oor-height and dock-height loading. Includes wide variation in ocespace utilization, ranging from retail and personalservice through distribution, light industrial andoccasional heavy industrial use.

Inventor – Includes all existing multi or single

tenant leased and owner-occupied industrialwarehouse, light manufacturing, ex and R&Dproperties greater than or equal to 10,000square feet.

Ne Contruction – Includes completed speculativeand build-to-suit construction. New constructionquoted on a net basis after any demolitions orconversions.

service space – Single story (or mezzanine) with10- to 16-foot ceilings with frontage treatment onone side and dock-height loading or grade levelroll-up doors on the other. Less than 15% oce.

Tech/R&d – One- and two- story, 10- to 15-footceiling heights with up to 50% oce/dry lab space

(remainder in wet lab, workshop, storage and othe

support), with dock-height and oor-height loadinTripe Net Rent – Includes rent payable to thelandlord and does not include additional expensessuch as taxes, insurance, maintenance, janitorial autilities. All industrial and high-tech/R&D rents inthis report are quoted on an annual, triple net persquare foot basis in U.S. dollars.

Vacanc Rate – Percentage of total inventoryavailable (both vacant and occupied) as at the surdate including direct vacant and sublease space.

warehoue – 50,000 square feet or more with up15 percent oce space, the balance being generalwarehouse space with 18- to 0- foot ceilingheights. All loading is dock-height.

Page 13

8/3/2019 NA Industrial Highlights - 3Q 2011

http://slidepdf.com/reader/full/na-industrial-highlights-3q-2011 13/13

hIghlIghts | Q3 2011 | INDUSTRIAL | NRTh AmeRIcA

COllIERs INTERNATIONAl

601 Union Street, Suite 800

Seattle, WA 8101

TEl +1 206 65 200

FOR MORE INFORMATION

Ross J. Moore

Chief Economist | USA

TEl +1 61 22 0221

EMAIl [email protected]

512 oces in61 countries on6 continentsUnited States: 125Canada: 8

Latin America: 18

Asia Pacic: 21EMEA: 11

• $1.5 billion in annual rvnu

• 979 illion squar ft undr

anagnt

• vr 12,000 profssionals

Copyright © 2011 Colliers International.

The information contained herein has been obtainedfrom sources deemed reliable. While every reasonable

eort has been made to ensure its accuracy, we cann

guarantee it. No responsibility is assumed for any

inaccuracies. Readers are encouraged to consult their

professional advisors prior to acting on any of the

material contained in this report.

Accelerating success

INdUsTRIAl VACANCy RATE RANkINGs

MARkET | UNITEd sTATEsVACANCy RATE

sEPT. 30, 2011 (%)

Honolulu, HI 4.7

Orange County, CA 4.7

Los Angeles, CA .

Houston, TX .7Long Island, NY .

Omaha, NE .

Indianapolis, IN .4

Kansas City, MO-KS .

Seattle/Puget Sound, WA 7.

Los Angeles - Inland Empire, CA 7.

Pittsburgh, PA 7.37

Denver, CO 7.

Columbia, SC .9

Miami, FL .47

Minneapolis/St. Paul, MN .

Portland, OR .

New Jersey - Northern .7

Grand Rapids, MI .

St. Louis, MO .3

Cincinnati, OH .9

Hartford, CT 9.

Ft. Lauderdale-Broward, FL 9.

San Francisco Peninsula, CA 9.4

Oakland, CA 9.

Philadelphia, PA 9.3

Bakerseld, CA 9.44

West Palm Beach, FL 9.4

Greenville/Spartanburg, SC 9.

Cleveland, OH 9.

Boise, ID 9.9

New Jersey - Central .9

Charleston, SC .4

Tampa Bay, FL .43

Jacksonville, Fl .

Louisville, KY .

Baltimore, MD .9

Dallas-Ft. Worth, TX .3

Chicago, IL .

San Diego, CA .

Columbus, OH .

Fresno, California .73

Washington DC .7

Orlando, FL .3

Raleigh, NC .4

San Jose/Silicon Valley, CA .

Memphis, TN .39

Pleasanton/Walnut Creek, CA .4

Sacramento, CA .77

Charlotte, NC .79Faireld, CA .

Nashville, TN .9

Detroit, MI 3.4

Atlanta, GA 3.3

Little Rock, AR 4.

Savannah, GA 4.

Phoenix, AZ 4.

Reno, NV 4.94

Stockton/San Joaquin County, CA .3

Las Vegas, NV .3

Boston, MA .7

INdUsTRIAl VACANCy RATE RANkINGs

MARkET | CANAdAVACANCy RATE

sEPT. 30, 2011 (%)

Regina, SK .

Saskatoon, SK 3.7

Victoria, BC 3.37

Edmonton, AB 3.4Guelph, ON 3.

Vancouver, BC 4.9

Calgary, AB 4.3

Toronto, ON 4.9

Montreal, QC .

Halifax, NS .3

Waterloo Region, ON .3

Ottawa, ON .4