46

North American Steel Trade Committee Laredo, Texas November 2007 NAFTA Steel Industry ‘Pulse’

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | lucius-lancaster |

| View: | 37 times |

| Download: | 1 times |

North American Steel Trade Committee

Laredo, Texas

November 2007

NAFTA Steel Industry ‘Pulse’

2

Outline• Preamble

• Industry Developments

• Market & Trade Trends

• Intra-NAFTA Policy Issues

• Feature Topic: Trade and Manufacturing

• Key Policy Imperatives

3

Preamble

4

Putting Recent Performance In Context

• Earning the Cost of Capital Over Economic Cycles:– Over the past 25 years, the U.S. and Canadian industries’ after tax

returns have averaged 0.95% and 1.6%, respectively

• Volatility: – From 1950-2006, the coefficient of volatility for the U.S. steel

industry has been 266.7%, vs. 27.6% for all manufacturing

• Competitiveness:– Consolidation / restructuring– Operational efficiencies / technology– Cost structure dynamics– Location

5

No Immunity

• Conditions Leading to Past Crises Are Still in Place:– World Overcapacity

– Governmental Ownership / Interventions

– Non-Market Behaviour

– Special Case of China (and India)

• No Immunity From Longstanding and Ongoing Threats

6

Proper Role of Governments

• Defending The Free Market From Abuse:– Eliminating market interventions and distortions by all governments

– Enforcing compliance with trade agreements and competition law

– Maintaining and enforcing trade remedy laws

– Assisting trading partners with understanding / adopting best practices

• Recognizing And Fostering The Steel Industry’s Contribution To National Goals:– Economic Security

– National Security

– Staple of a Strong Manufacturing Sector

7

Industry Developments

8

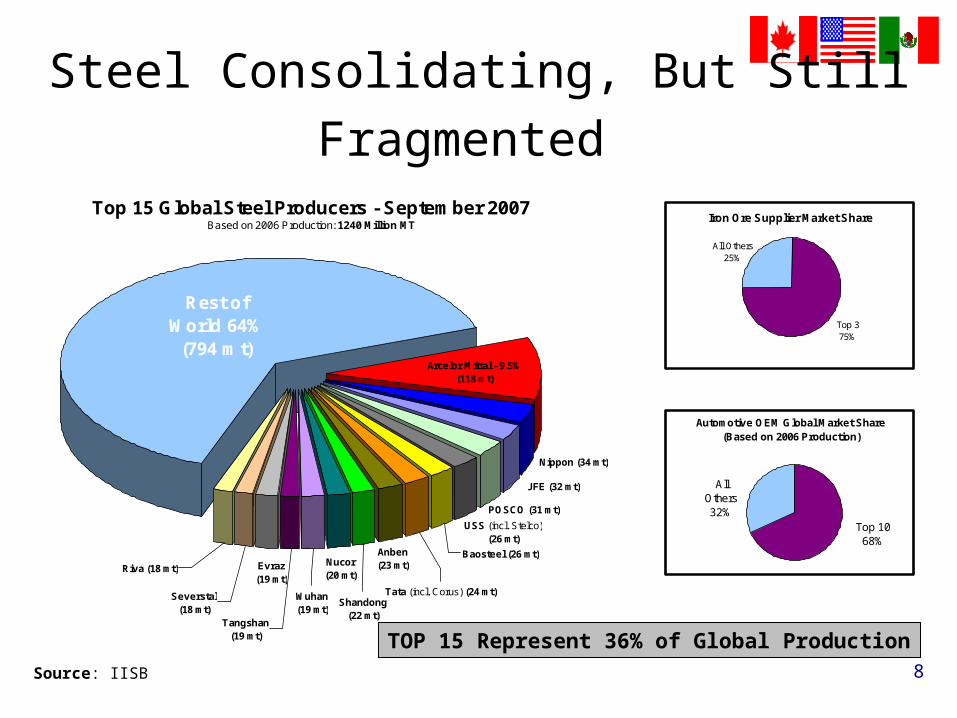

Steel Consolidating, But Still Fragmented

Top 15 Global Steel Producers - September 2007Based on 2006 Production: 1240 Million MT

Baosteel (26 mt)

Tata (incl. Corus) (24 mt)

USS (incl. Stelco) (26 mt)

POSCO (31 mt)

JFE (32 mt)

Anben (23 mt)

Shandong (22 mt)

Nucor (20 mt)

Wuhan (19 mt)

Tangshan (19 mt)

Evraz (19 mt)

Riva (18 mt)

Severstal (18 mt)

Nippon (34 mt)

Rest of World 64%

(794 mt)Arcelor Mittal - 9.5%

(118 mt)

Automotive OEM Global Market Share(Based on 2006 Production)

Top 1068%

All Others32%

Iron Ore Supplier Market Share

Top 375%

All Others25%

TOP 15 Represent 36% of Global Production

Source: IISB

9

Consolidation: China The Exception

Source: IISI *2006 Production in Million MT

Regional Top 5 Producer Market Share

% of T

otal P

rodu

ction

# of Facilities

10m+ 33 9

5-10m 19 12

2-5m 23 32

<2m 25 N/a

Total 100 N/a

2006 Chinese Steel Production By Facility Size

(in Million MT)

Source: CISA

ROW: Market-Driven China

67%

Total US / Canada 114 *

58%

Total Europe 173

47%

Total CIS 119

77%

Total Japan 116

23%

Total China 419

65%

Total Others Asia 113Total Latin America 63

72%

10

China: World’s No. 1 Is Government Directed

Privately OwnedGovernment Owned or

Controlled

191 million tonnes

19 million tonnes

Source: Money for Metal (2007)

Top 20 Chinese Steel Producers:Government Control Vs. Private Ownership

Top 20 Capacity: 210 Million Tons

-

100,000

200,000

300,000

400,000

500,000

600,000

China Asia other thanChina

European Union(25)

North America C.I.S. (6) South America Other Europe Africa Middle East Oceania

Metr

ic t

on

s p

rod

uced

(in

'000s)

Source: World crude production through 9/07 annualized; IISI

2007 Projected Global Production

Australian Government Predicting China Will Reach 1B Tons by 2015

91%

11

Active Consolidation Within NAFTA

• Recent Key NAFTA Announcements:– ArcelorMittal-Dofasco– USS-Stelco, USS-LoneStar– Gerdau-Chaparral– Ternium-Grupo Imsa– SSAB-IPSCO– Essar-Algoma, Essar-Minnesota

• Emerging Downstream Focus:– Nucor-Harris, Nucor-Barker, Gerdau-Enco

• Extending to Scrap:– Sims-Metal Management, Steel Dynamics-OmniSource

12

Consolidation: Opportunities & Risks

• Potential Benefits:– Access to Capital, Technology

– Deeper Customer Relationships

– Facility Optimization / Strategic Fit

– Industry Sustainability

• But Benefits Are Undermined By Prevailing Risks:– Global Overcapacity

– Subsidies and Other Trade and Market Distortions

13

New Capacity Outpaces Consumption Growth

Capacity – Multiple Sources; Nucor Analysis

Demand – IISI projections thru ’08; 6% increase “09 – ‘10

EU-251%

India23%

NAFTA2%Other Asia

15%

Other Europe3%

CIS6%

Africa & Middle East5%

Central & South America

12%

China33%

Announced Steel Capacity Increases By Region

(2006 – 2012)

Announced Steel Capacity Vs. Projected Consumption 2007 – 2010

(Million Metric Tonnes)

Compound Annual Growth Rates:Capacity: 6.83% Demand: 4.65%

14

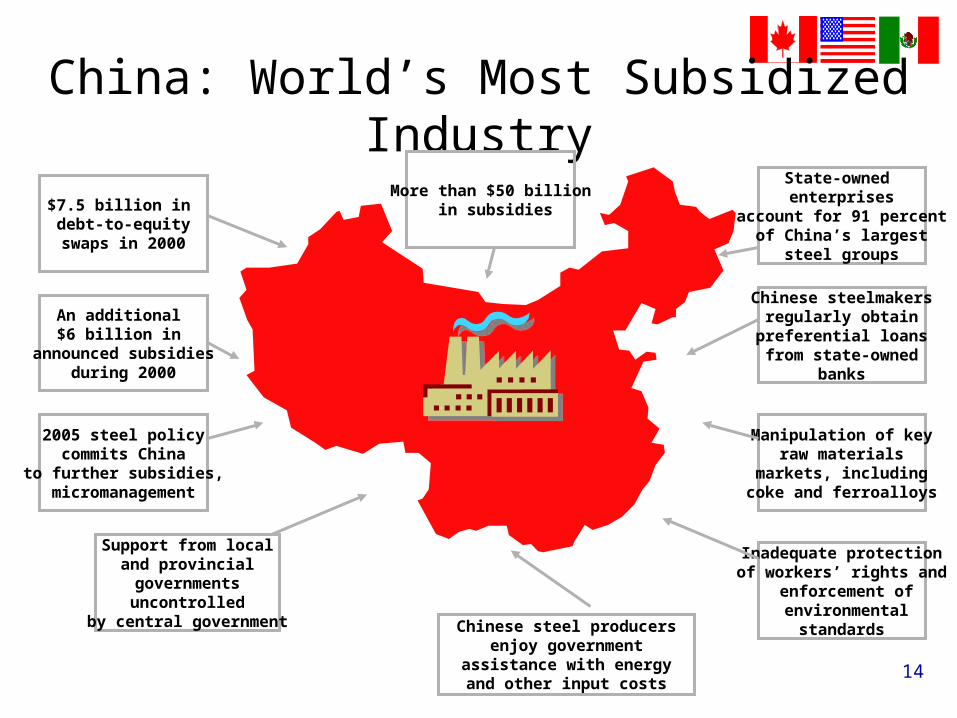

China: World’s Most Subsidized Industry

More than $50 billion in subsidies$7.5 billion in

debt-to-equityswaps in 2000

An additional $6 billion in

announced subsidiesduring 2000

2005 steel policycommits China

to further subsidies,micromanagement

Support from localand provincialgovernmentsuncontrolled

by central government Chinese steel producersenjoy government

assistance with energyand other input costs

Inadequate protectionof workers’ rights and

enforcement of environmental

standards

Manipulation of keyraw materials

markets, includingcoke and ferroalloys

Chinese steelmakersregularly obtain

preferential loansfrom state-owned

banks

State-owned enterprises

account for 91 percentof China’s largest

steel groups

15

Raw Materials: Governments Still Intervening

• Governments (e.g., China, India) Continue to Intervene in Key Raw Materials Markets For Steel:– Iron Ore– Coke– Ferroalloys– Refractory Materials

• Export Tax Manipulations / Restrictions

• Distortions Created; NAFTA Competitiveness Negatively Impacted

16

Consolidation: Key Takeaways

• Consolidation is Creating a Stronger Global Industry– NAFTA companies now competing for capital on a global basis– China, the dominant producer, not participating in the trend

• Level Playing Field Necessary to Ensure NAFTA Benefits from Market-Driven Consolidation– Continued overcapacity threat, led by China– Subsidies & government interventions driving export growth and

potential for continued trade distortions

• Successful Consolidation Outcomes Require:– Working to address effectively “root causes” of trade distortions– Ensuring NAFTA trade remedies are fair, accessible, enforceable and

able to respond effectively to market distortions as they occur

17

Market & Trade Trends

18

Global Growth, But Non-NAFTA

Global Crude Steel Production

2006 vs. 2007

Cou

ntry /

Region

2006 P

rodu

ction

2007* P

rodu

ction

% C

han

ge

NAFTA 132 132 -

EU 25 198 211 +6.6

CIS 120 124 +3.3

S. Amer. 45 47 +4.4

China 421 483 +14.7

Japan 116 119 +2.6

Other Asia 136 119 -12.5

World 1248 1308 +4.8Source: IISI *2007 Data Annualized From 9 Months

19

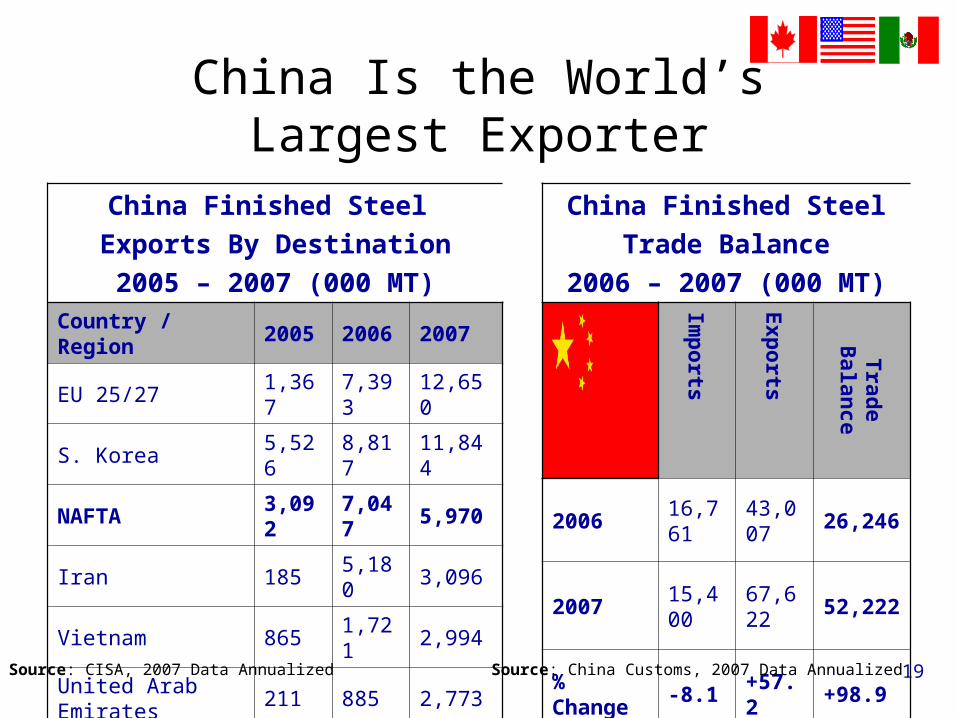

China Is the World’s Largest Exporter

China Finished Steel

Exports By Destination

2005 – 2007 (000 MT)Country / Region 2005 2006 2007

EU 25/27 1,367 7,393 12,650

S. Korea 5,526 8,817 11,844

NAFTA 3,092 7,047 5,970

Iran 185 5,180 3,096

Vietnam 865 1,721 2,994

United Arab Emirates 211 885 2,773

India 417 1,574 2,447

Others 8,861 15,052 25,848

TOTAL 20,524 43,007 67,622Source: CISA, 2007 Data Annualized

China Finished Steel

Trade Balance

2006 – 2007 (000 MT)Im

ports

Exp

orts

Trad

e B

alance

2006 16,761 43,007 26,246

2007 15,400 67,622 52,222

% Change -8.1 +57.2 +98.9

Source: China Customs, 2007 Data Annualized

20

World Market And Trade Flows Are Dynamic

• NAFTA Faces a Potential Significant Import Surge Risk

• Concerns about the Combined Effects of:– Unrelenting Chinese Export Expansion– Effect of Other Nations (e.g., EU) Taking Actions Against China

• No Immunity for the NAFTA Market Despite Industry Consolidation and Enhanced Competitiveness

• Need for NAFTA Governments to Counter Adverse Spillover Effects from Chinese Non-Market Behaviour

21

NAFTA Apparent Steel Demand Fell in 2007

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 20070

20

40

60

80

100

120

140

160

180

12%12%

15% 22% 17%18%

16% 16% 12%

17%

17%

21%17%

Domestic Shipments Imports

Mill metric tonnes

Sources: AISI, Statistics Canada, Canacero

22

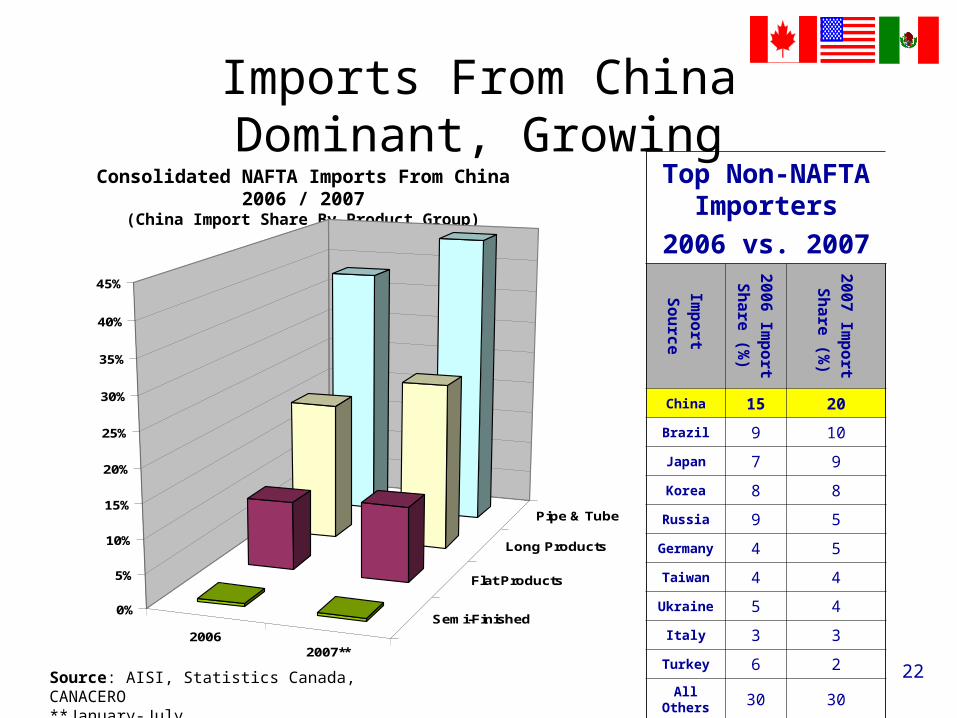

Imports From China Dominant, GrowingTop Non-NAFTA

Importers

2006 vs. 2007Im

port

Sou

rce

2006 Im

port

Sh

are (%)

2007 Im

port

Sh

are (%)

China 15 20

Brazil 9 10

Japan 7 9

Korea 8 8

Russia 9 5

Germany 4 5

Taiwan 4 4

Ukraine 5 4

Italy 3 3

Turkey 6 2

All Others 30 30

Consolidated NAFTA Imports From China 2006 / 2007(China Import Share By Product Group)

Source: AISI, Statistics Canada, CANACERO**January-July

20062007**

Semi-Finished

Flat Products

Long Products

Pipe & Tube

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

23

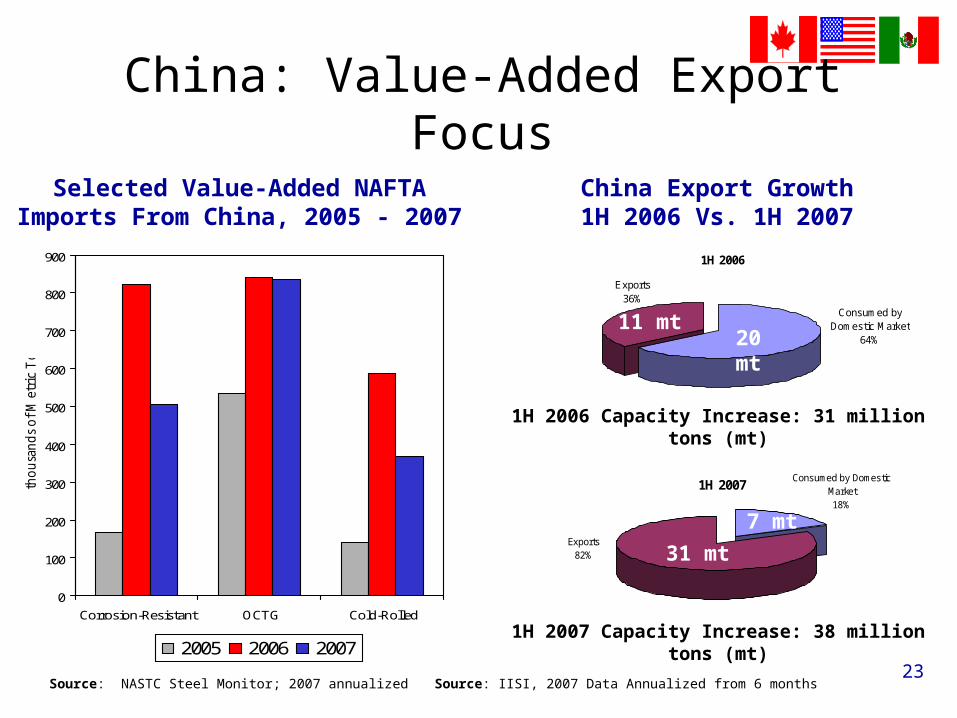

China: Value-Added Export Focus

1H 2006

Exports36%

Consumed by Domestic Market

64%

1H 2007

Exports82%

Consumed by Domestic Market18%

1H 2006 Capacity Increase: 31 million tons (mt)

1H 2007 Capacity Increase: 38 million tons (mt)

Source: IISI, 2007 Data Annualized from 6 months

0

100

200

300

400

500

600

700

800

900

Corrosion-Resistant OCTG Cold-Rolled

tho

usa

nd

s o

f M

etri

c T

on

s

2005 2006 2007

Source: NASTC Steel Monitor; 2007 annualized

11 mt20 mt

31 mt

7 mt

Selected Value-Added NAFTA Imports From China, 2005 - 2007

China Export Growth1H 2006 Vs. 1H 2007

24

China: Unfulfilled Commitments

“All the measures taken by the Chinese governments to curb exports have been without effect so far…If China wishes to avoid long-running trade conflicts, the rules of the market have to be obeyed.”

-Ekkehard D. Schulz, Chairman, ThyssenKrupp AG

September 30, 2007

25

China Central To Current NAFTA CasesKey NAFTA Steel Trade Cases (Ch. 72 & Ch. 73)

May–November 2007

Country New Cases Current Sunsets

Canada Seamless OCTG Plate

United States

Pipe x 2

Nails

Wire Hangers

Hot-Rolled*

Mexico

Plate

Seamless OCTG

Nails

Wire Hangers

Wire Mesh

*Finding renewed against China on October 10, 2007

26

Intra-NAFTA Policy Issues

27

Steel Remains a Strategic NAFTA Sector

• Recent Developments (August 2007):– Montebello SPP Leaders Summit– NAFTA Commission / Trade Ministers Meeting– North American Competitiveness Council

(NACC) Report

28

Context: NAFTA Economic Uncertainties

• Economic Concerns in All NAFTA Countries– U.S. Weakening– Mexico: Tracking U.S. Performance– Canada: Uneven Performance, Slowing Growth,

Currency Appreciation ($CDN > $USD)

• Rising Input Costs and Uncertainties (e.g., Energy)

• Potential Negative Impacts on Both Steel Producers and Customers

29

Effective Trade Policies Remain Essential

• WTO: NAFTA Governments’ Coordination– Subsidies Case– Rules Negotiations

• Expanding Focus from Doha to Bilaterals– US: Korea, Columbia, Peru, Panama– Canada: Korea, Columbia/Peru, EFTA– Mexico: Korea, Peru

• Key Industry Priorities on FTAs:– Remedies– Steel Customer Impacts / Incentives for Value-Added in North America

• NAFTA Policy Coordination– AD/CVD Applicability to NMEs– Need to Adopt Best Practices / Highest Level of Enforcement

30

Climate Change: Trade Impacts

• Emerging Legislative & Regulatory Issues in NAFTA:– U.S.: Congress Debating Cap & Trade, Border Adjustability– Canada: New Plan – Technical & Compliance Issues– Mexico: Government Open to Discussion of IISI / Sectoral Model

• The Pressure For Stringent Regulation Could Have Significant Trade Consequences– “Decoupling” / Production Loss and Migration– Increased Import Penetration– “Next Generation” Trade Policy: “Green Content”

• Bottom Line: Need to Avoid Creating Trade Distortions or Reducing NAFTA Competitiveness

31

Feature Topic: Trade and Manufacturing

32

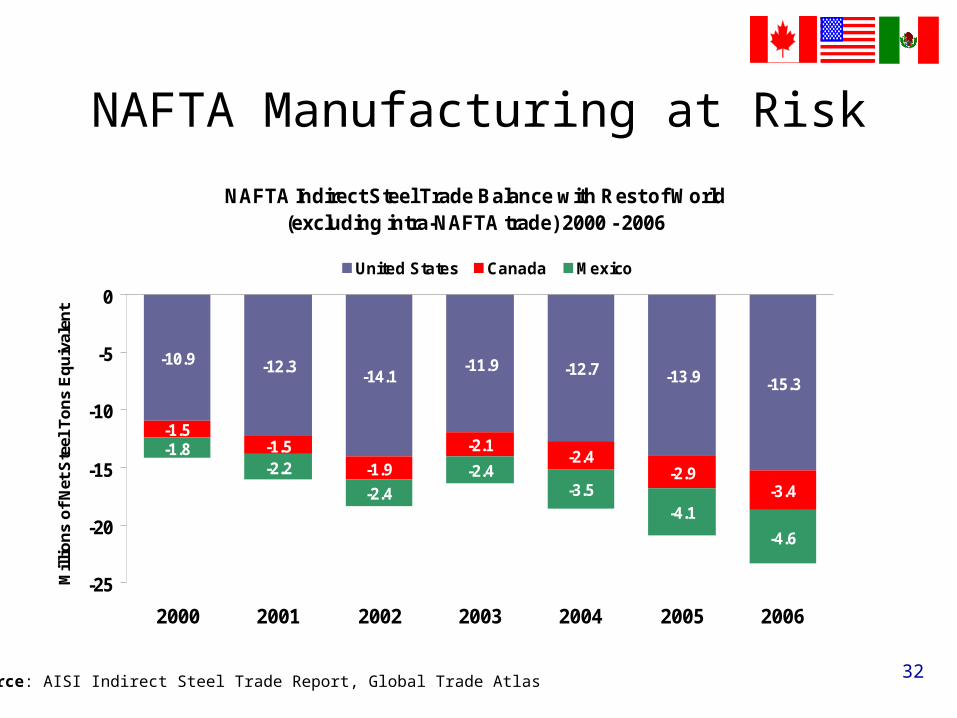

NAFTA Manufacturing at Risk

Source: AISI Indirect Steel Trade Report, Global Trade Atlas

NAFTA Indirect Steel Trade Balance with Rest of World(excluding intra-NAFTA trade) 2000 - 2006

-10.9 -12.3-14.1

-11.9 -12.7 -13.9 -15.3

-1.5-1.5

-1.9

-2.1-2.4

-2.9-3.4

-1.8-2.2

-2.4-2.4

-3.5-4.1

-4.6

-25

-20

-15

-10

-5

0

2000 2001 2002 2003 2004 2005 2006

Mil

lio

ns

of

Net

Ste

el T

on

s E

qu

ival

ent

United States Canada Mexico

33

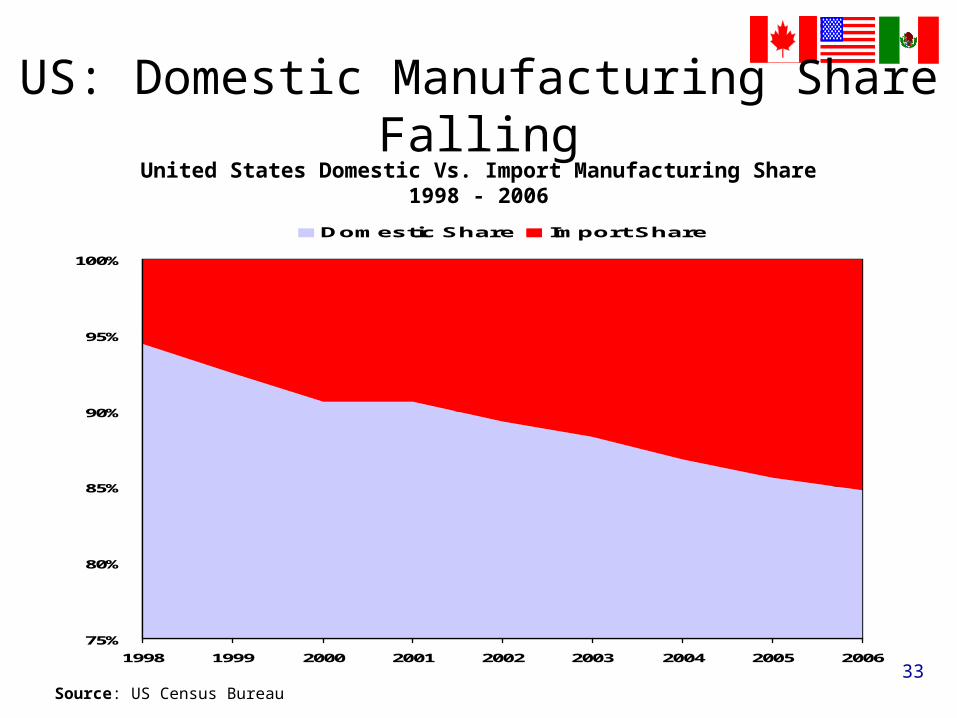

US: Domestic Manufacturing Share Falling

75%

80%

85%

90%

95%

100%

1998 1999 2000 2001 2002 2003 2004 2005 2006

Domestic Share Import Share

Source: US Census Bureau

United States Domestic Vs. Import Manufacturing Share1998 - 2006

34

US: 3m Jobs Lost; Trade Deficits GrowingU.S. Manufacturing Jobs vs. Trade Deficit

2000 - 2007

14,000

14,500

15,000

15,500

16,000

16,500

17,000

17,500

Ma

r-0

0

Sep

-00

Ma

r-0

1

Sep

-01

Ma

r-0

2

Sep

-02

Ma

r-0

3

Sep

-03

Ma

r-0

4

Sep

-04

Ma

r-0

5

Sep

-05

Ma

r-0

6

Sep

-06

Ma

r-0

7

U.S

. E

mp

loy

ees

in M

an

ufa

ctu

rin

g (

00

0's

)

250

350

450

550

650

750

850

950

U.S

. T

ra

de D

efi

cit

in

Bil

lio

ns

of

Do

lla

rs

(Ov

er P

rev

iou

s 4

Qu

arte

rs)

Manufacturing Jobs Trade Deficit

Sources: US Census Bureau (trade data), US Labor Dept. (employment data)

*Dr. Peter Morici, former Chief Economist of ITC (estimate of lost mfg. jobs due to China trade)

Estimated 1m Jobs Lost Due to

China Trade*

Trade Deficit: +123% Since 2000

35

US: China Drives Indirect Steel Trade Deficit

United States Indirect Steel Trade Balance with China2000 - 2006

-3.2

-3.2 -3.7

-4.6

-5.5

-2.1 -2.5

-6

-5

-4

-3

-2

-1

0

2000 2001 2002 2003 2004 2005 2006

Mill

ion

s o

f Net

ton

s E

qu

ival

ent

Source: AISI Indirect Steel Trade Report

36

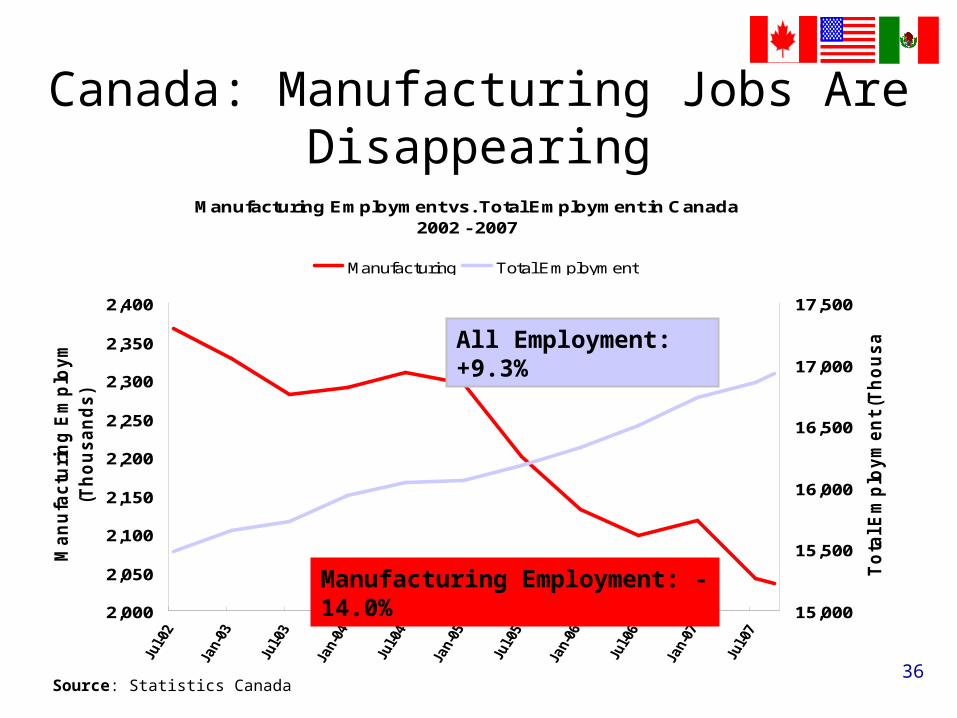

Canada: Manufacturing Jobs Are Disappearing

Manufacturing Employment vs. Total Employment in Canada 2002 - 2007

2,000

2,050

2,100

2,150

2,200

2,250

2,300

2,350

2,400

Ma

nu

fac

turi

ng

Em

plo

ym

en

t

(Th

ou

sa

nd

s)

15,000

15,500

16,000

16,500

17,000

17,500

To

tal E

mp

loy

me

nt

(Th

ou

sa

nd

s)

Manufacturing Total Employment

All Employment: +9.3%

Manufacturing Employment: -14.0%

Source: Statistics Canada

37

Canada's Steel and Steel-Containing Goods^ Trade Balance 1997-2007

-$30

-$25

-$20

-$15

-$10

-$5

$0

$5

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*

Va

lue

(B

illio

ns

of

CD

N$

)

China All Countries (incl. China)

Canada: Steel-Related Trade Deficit Persists

^Steel-containing goods includes all HS Sections for Base Metals and articles of Base Metals (Sec. XV), Machinery, Appliances and Equipment (Sec. XVI), and Vehicles, Aircraft, Vessels and Transportation Equipment (Sec. XVII).

Canada’s Projected 2007 Deficit With China Represents 71% of the Total

Source: Statistics Canada*2007 Data Annualized from January-July Actuals

38

Canada: China Growing Value, Market ShareAPPLIANCES

Source2005 Imports

(CDN$ Millions)

Import

Share(%)

2007 Imports

(CDN$ Millions)

Import

Share (%)

% Value Change

05 / 07

1. United States 1579.7 53.75 1560.9 48.6 -2.2

2. China 605.0 20.59 764.2 23.8 +26.3

3. Mexico 146.6 4.99 226.9 7.1 +54.7

CONSTRUCTION PRODUCTS / FURNISHINGS

Source2005 Imports

(CDN$ Millions)

Import

Share (%)

2007 Imports

(CDN$ Millions)

Import

Share (%)

% Value Change

05 / 07

1. United States 3677.93 65.12 3860.88 61.11 +5.0

2. China 509.04 9.01 776.47 12.29 +52.5

3. Mexico 212.0 3.75 212.78 3.37 +0.03

Source: World Trade Atlas / AISI.

DOMESTIC & COMMERCIAL EQUIPMENT

Source2005 Imports

(CDN$ Millions)

Import

Share (%)

2007 Imports

(CDN$ Millions)

Import

Share (%)

% Value Change

05 / 07

1. United States 1493.3 50.34 1467.1 45.49 -1.8

2. China 619.13 20.87 802.42 24.88 +29.6

3. Mexico 351.68 11.86 377.16 11.69 +7.24

39

Mexico Real Manufacturing GDP & Imports1994 - 2007

RealManufacturingGDP (LHS)

Manufacturing Imports (RHS)

Source: BIE – Mexico’s Economic Statistics Data Bank

40,000

90,000

140,000

190,000

240,000

1Q 1

994

3Q 1

994

1Q 1

995

3Q 1

995

1Q 1

996

3Q 1

996

1Q 1

997

3Q 1

997

1Q 1

998

3Q 1

998

1Q 1

999

3Q 1

999

1Q 2

000

3Q 2

000

1Q 2

001

3Q 2

001

1Q 2

002

3Q 2

002

1Q 2

003

3Q 2

003

1Q 2

004

3Q 2

004

1Q 2

005

3Q 2

005

1Q 2

006

3Q 2

006

1Q 2

007

30,000

50,000

70,000

90,000

110,000

130,000

Mil

lio

n U

SD

Mil

lio

n U

SD

Mil

lio

n

Mil

lio

n

US

DU

SD

Mexico: Imports Gaining Market Share

40

Mexico Real Manufacturing GDP & Employment1994 - 2007

Source: BIE – Mexico’s Economic Statistics Data Bank

Th

ou

san

ds

Th

ou

san

ds

Mil

lio

n U

SD

Mil

lio

n U

SD

Real ManufacturingGDP

ManufacturingEmployment

3,650

3,850

4,050

4,250

4,450

4,650

4,850

5,050

5,250

1Q 1

994

3Q 1

994

1Q 1

995

3Q 1

995

1Q 1

996

3Q 1

996

1Q 1

997

3Q 1

997

1Q 1

998

3Q 1

998

1Q 1

999

3Q 1

999

1Q 2

000

3Q 2

000

1Q 2

001

3Q 2

001

1Q 2

002

3Q 2

002

1Q 2

003

3Q 2

003

1Q 2

004

3Q 2

004

1Q 2

005

3Q 2

005

1Q 2

006

3Q 2

006

1Q 2

007

30,000

55,000

80,000

105,000

130,000

155,000

180,000

205,000

230,000

255,000

Mexico: Significant Employment Loss

41

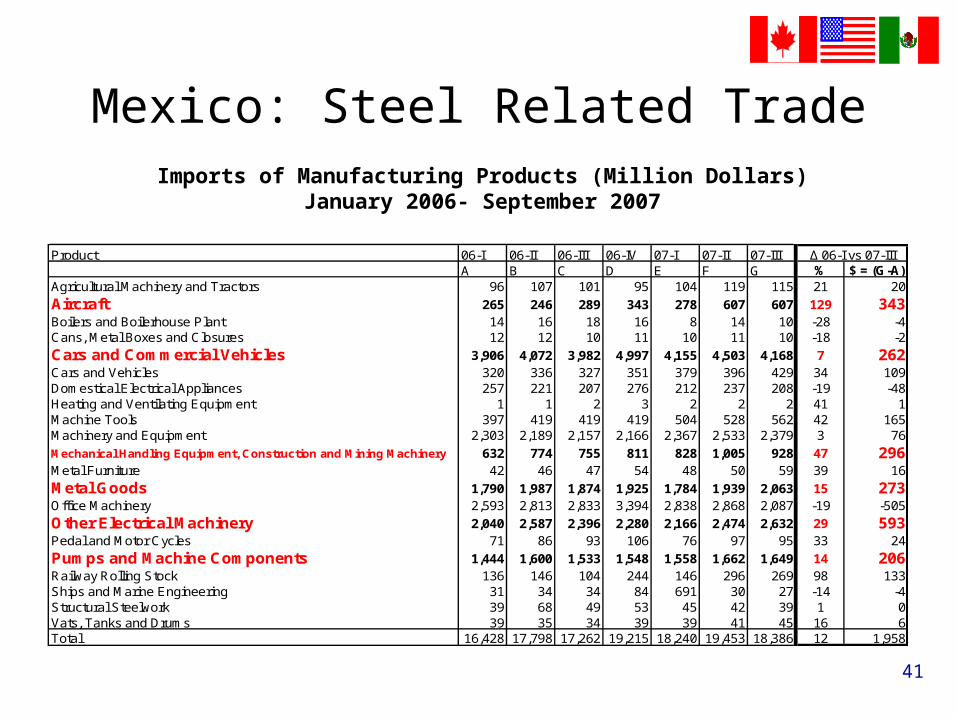

Imports of Manufacturing Products (Million Dollars)January 2006- September 2007

Product 06-I 06-II 06-III 06-IV 07-I 07-II 07-IIIA B C D E F G % $ = (G-A)

Agricultural Machinery and Tractors 96 107 101 95 104 119 115 21 20

Aircraft 265 246 289 343 278 607 607 129 343Boilers and Boilerhouse Plant 14 16 18 16 8 14 10 -28 -4Cans, Metal Boxes and Closures 12 12 10 11 10 11 10 -18 -2

Cars and Commercial Vehicles 3,906 4,072 3,982 4,997 4,155 4,503 4,168 7 262Cars and Vehicles 320 336 327 351 379 396 429 34 109Domestical Electrical Appliances 257 221 207 276 212 237 208 -19 -48Heating and Ventilating Equipment 1 1 2 3 2 2 2 41 1Machine Tools 397 419 419 419 504 528 562 42 165Machinery and Equipment 2,303 2,189 2,157 2,166 2,367 2,533 2,379 3 76

Mechanical Handling Equipment, Construction and Mining Machinery 632 774 755 811 828 1,005 928 47 296Metal Furniture 42 46 47 54 48 50 59 39 16

Metal Goods 1,790 1,987 1,874 1,925 1,784 1,939 2,063 15 273Office Machinery 2,593 2,813 2,833 3,394 2,838 2,868 2,087 -19 -505

Other Electrical Machinery 2,040 2,587 2,396 2,280 2,166 2,474 2,632 29 593Pedal and Motor Cycles 71 86 93 106 76 97 95 33 24

Pumps and Machine Components 1,444 1,600 1,533 1,548 1,558 1,662 1,649 14 206Railway Rolling Stock 136 146 104 244 146 296 269 98 133Ships and Marine Engineering 31 34 34 84 691 30 27 -14 -4Structural Steelwork 39 68 49 53 45 42 39 1 0Vats, Tanks and Drums 39 35 34 39 39 41 45 16 6Total 16,428 17,798 17,262 19,215 18,240 19,453 18,386 12 1,958

∆ 06-I vs 07-III

Mexico: Steel Related Trade

42

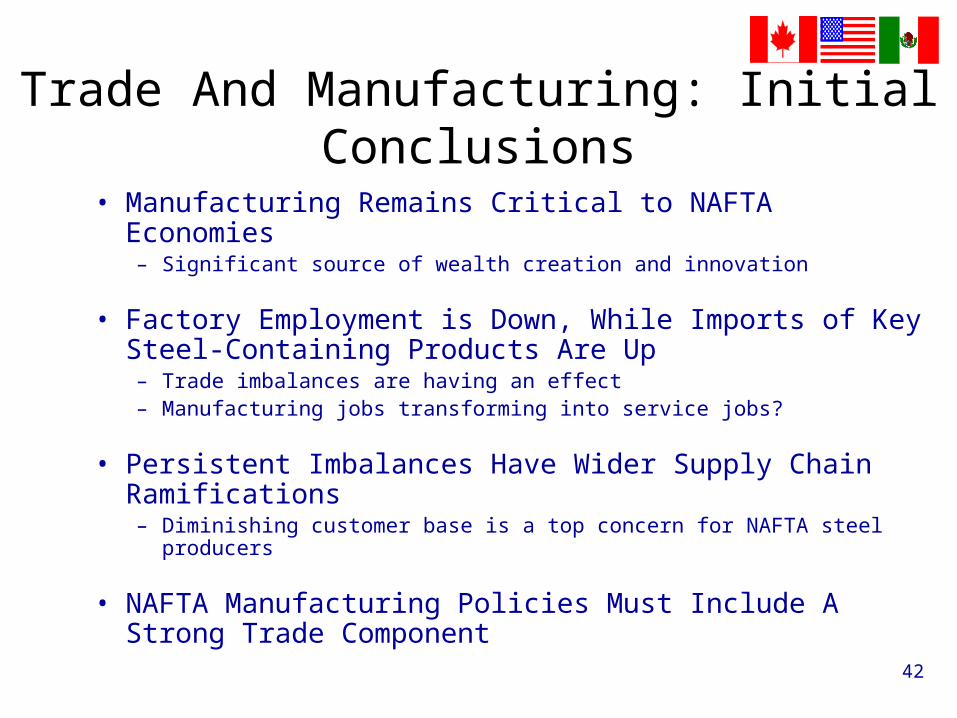

Trade And Manufacturing: Initial Conclusions

• Manufacturing Remains Critical to NAFTA Economies– Significant source of wealth creation and innovation

• Factory Employment is Down, While Imports of Key Steel-Containing Products Are Up– Trade imbalances are having an effect– Manufacturing jobs transforming into service jobs?

• Persistent Imbalances Have Wider Supply Chain Ramifications – Diminishing customer base is a top concern for NAFTA steel producers

• NAFTA Manufacturing Policies Must Include A Strong Trade Component

43

Overall Conclusions –NAFTA Policy Implications

44

Strategic Government Actions Required:

• Ensure Rules-Based Trade For Manufacturing Industries

• Achieve Highest Level Of AD/CVD Practice & Enforcement

• Prevent Market Distortions Before They Impact The NAFTA Region

• Strengthen Intra-NAFTA Trade Facilitation

45

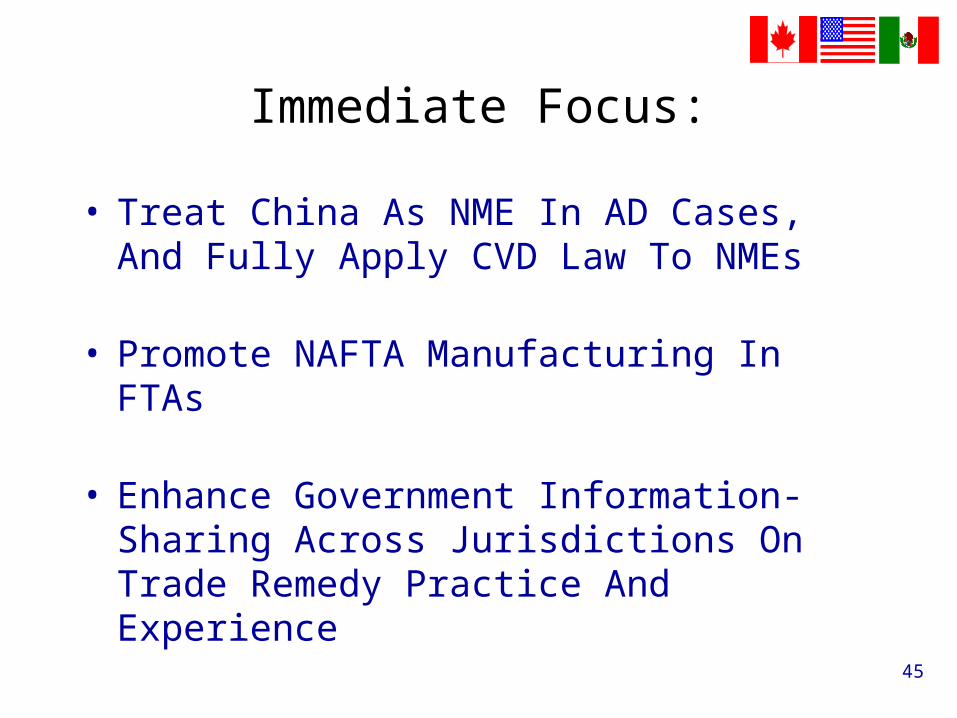

Immediate Focus:

• Treat China As NME In AD Cases, And Fully Apply CVD Law To NMEs

• Promote NAFTA Manufacturing In FTAs

• Enhance Government Information-Sharing Across Jurisdictions On Trade Remedy Practice And Experience

46

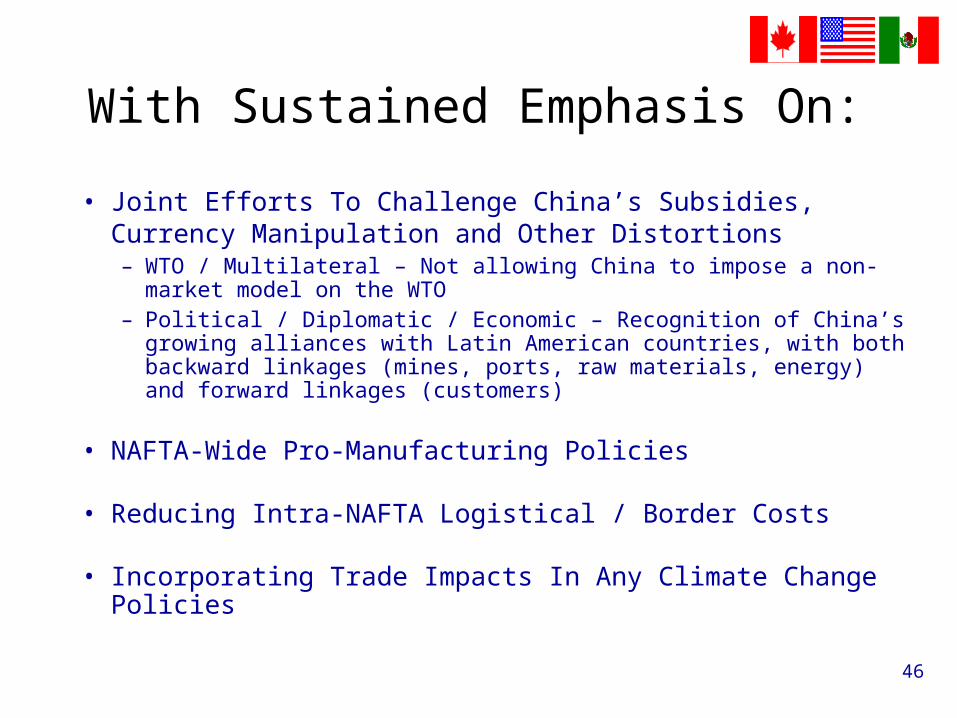

With Sustained Emphasis On:

• Joint Efforts To Challenge China’s Subsidies, Currency Manipulation and Other Distortions – WTO / Multilateral – Not allowing China to impose a non-market model on

the WTO– Political / Diplomatic / Economic – Recognition of China’s growing

alliances with Latin American countries, with both backward linkages (mines, ports, raw materials, energy) and forward linkages (customers)

• NAFTA-Wide Pro-Manufacturing Policies

• Reducing Intra-NAFTA Logistical / Border Costs

• Incorporating Trade Impacts In Any Climate Change Policies