34

Standing for trust and integrity NASBA International Forum Professional Accounting Challenges in the EU Philip Johnson, FEE President Orlando, Florida October 31 ‒ November 1, 2012

Standing for trust and integrity

NASBA International Forum

Professional Accounting Challenges in the EU

Philip Johnson, FEE President Orlando, Florida

October 31 ‒ November 1, 2012

Standing for trust and integrity

What is FEE and who does it represent?

Standing for trust and integrity 279

Federating the European Profession

Ø 45 professional institutes of accountants

Ø 33 European countries, including all 27 European Union (EU) Member States

Ø 700,000 professionals incl. all sections of the profession: large, medium, small practices, business, public sector

Standing for trust and integrity 280

Engaging with stakeholders

Catalyst in Europe

Standing for trust and integrity 281

Active FEE Working Groups

Ethics

Direct Tax

Indirect Tax

Qualification and Market

Access

SMP Forum Corporate Reporting

Policy Group Auditing

IAASB EDs Subgroup

Company Law and Corporate Governance

Anti-Money Laundering

Insurance

Accounting

Capital Markets

Banks

Public Sector Committee

Sustainability

Standing for trust and integrity 282

The EU legislative process How does it work?

Standing for trust and integrity 283

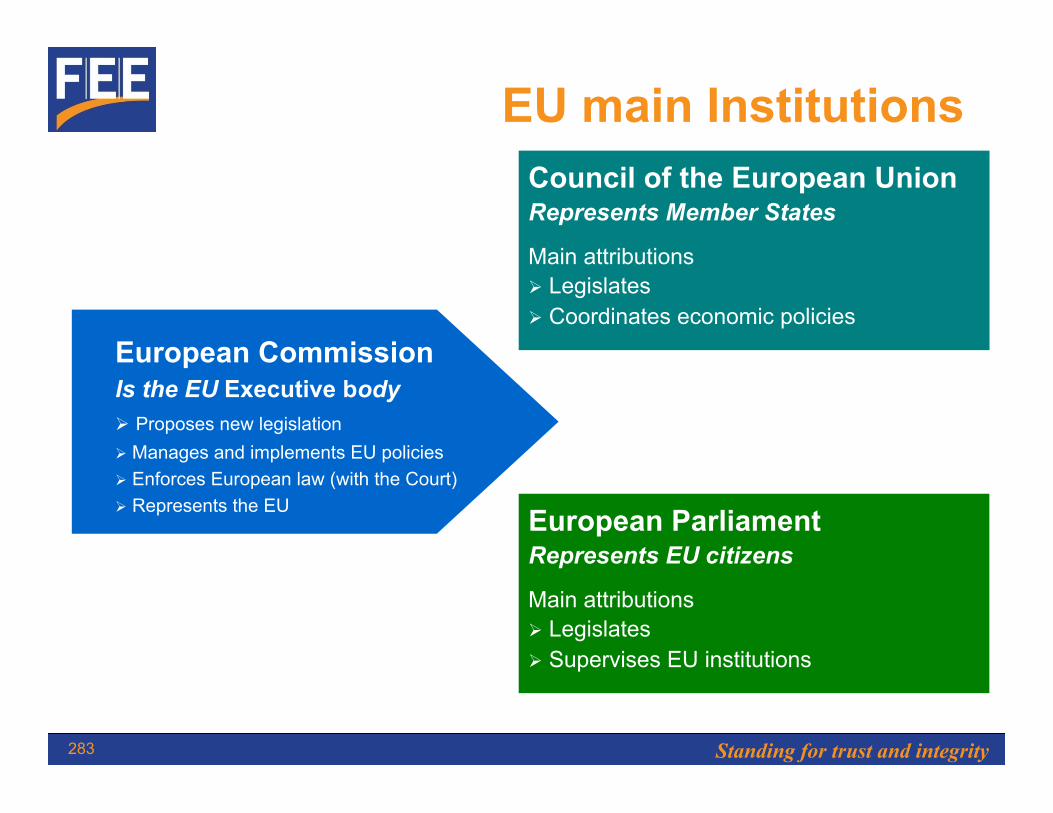

EU main Institutions Council of the European Union Represents Member States

Main attributions Ø Legislates Ø Coordinates economic policies

European Parliament Represents EU citizens

Main attributions Ø Legislates Ø Supervises EU institutions

European Commission Is the EU Executive body Ø Proposes new legislation Ø Manages and implements EU policies Ø Enforces European law (with the Court) Ø Represents the EU

Standing for trust and integrity 284

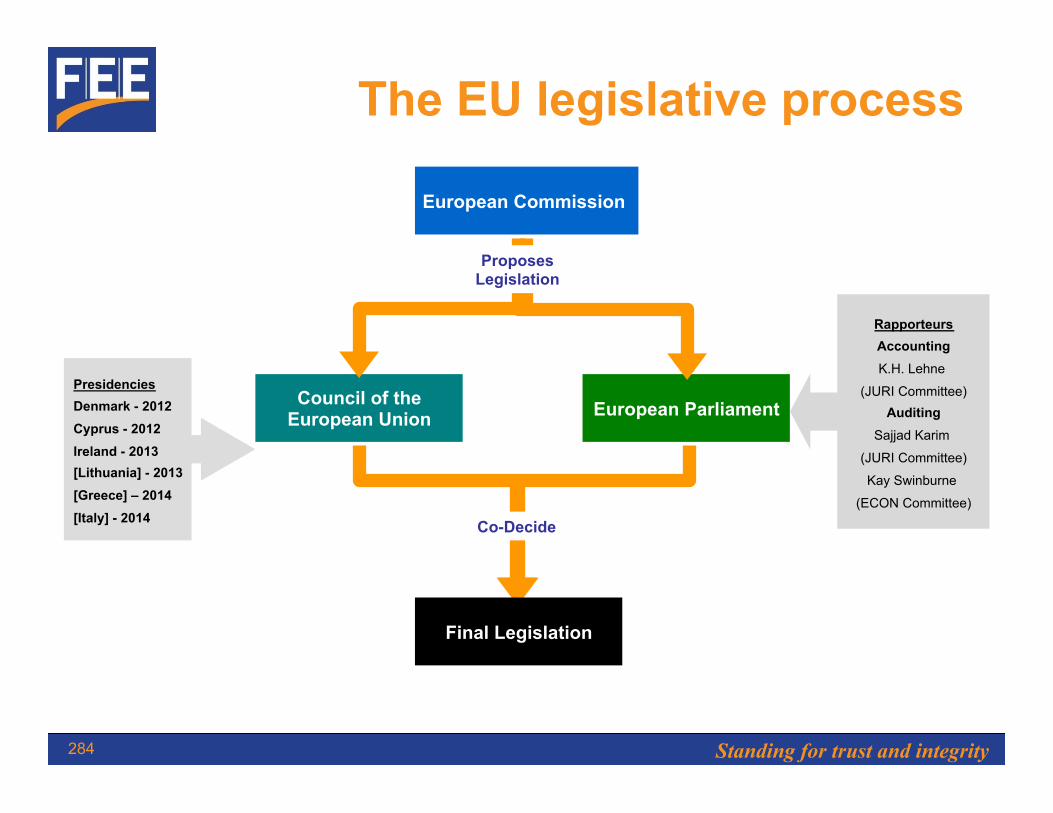

The EU legislative process

European Commission

Council of the European Union European Parliament

Proposes Legislation

Co-Decide

Rapporteurs Accounting K.H. Lehne

(JURI Committee) Auditing

Sajjad Karim

(JURI Committee)

Kay Swinburne

(ECON Committee)

Final Legislation

Presidencies Denmark - 2012 Cyprus - 2012 Ireland - 2013 [Lithuania] - 2013 [Greece] – 2014 [Italy] - 2014

Standing for trust and integrity 285

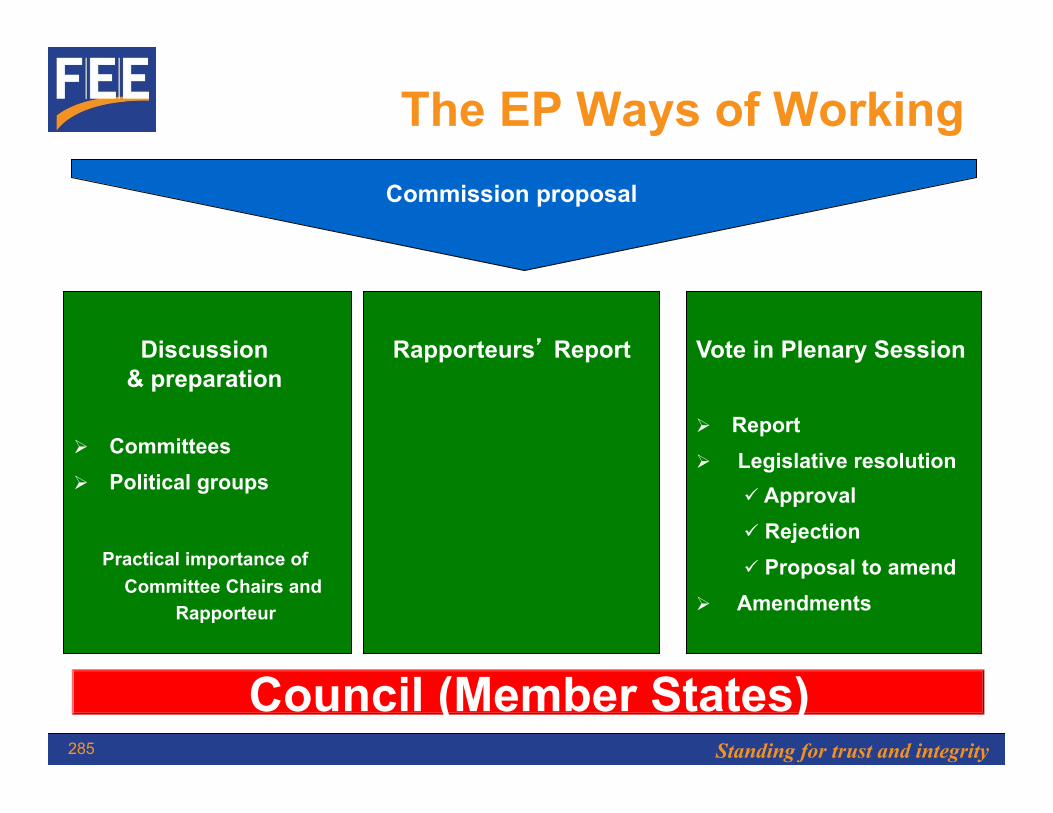

The EP Ways of Working Commission proposal

Discussion

& preparation

Ø Committees Ø Political groups

Practical importance of Committee Chairs and

Rapporteur

Rapporteurs’ Report

Vote in Plenary Session

Ø Report Ø Legislative resolution

ü Approval ü Rejection ü Proposal to amend

Ø Amendments

Council (Member States)

Standing for trust and integrity 286

Proposals to amend EU Accounting Directives

Standing for trust and integrity 287

EC Accounting Reform Proposals of 25 October 2011

Combining and amending the existing 4th and 7th Accounting Directives

Standing for trust and integrity 288

EC Proposals (1/4) Ø “Think small first approach”

Ä New size category: “micro” entities (Member State option to exempt)

Ä Bottom up approach for reporting and disclosures (small, medium, large companies and Public Interest Entities (PIEs))

Ä Limited disclosure requirements for “small” companies Ø Fully harmonised EU size criteria for financial reporting (27

countries) Ø Size criteria for audit requirement

Ä Mandatory audit at EU level for medium and large companies and PIEs

Ä No EU level audit requirement for small companies Ä BUT Member State option to require audit of some or all small

companies allowed (“opt-in” option)

Standing for trust and integrity 289

Proposed accounting and auditing threshold criteria* (2/4)

* Entity or Group, if not exceeding 2 of the 3 criteria

In millions EUR Micro Small Medium Large

Agreed Current Proposed Current Proposed Current Proposed

Balance Sheet <0.35 <4.4 <5 <17.5 <20 >17.5 >20

Net Turnover <0.7 <8.8 <10 <35 <40 >35 >40 Average # of employees <10 <50 <50 <250 <250 >250 >250

Standing for trust and integrity 290

EC Proposals (3/4)

Ø IAS 2005 Regulation requiring use of IFRS (EU) for listed entities remains in place (all listed entities to adopt IFRS)

Ø Full adoption of IFRS for SMEs is not pursued

Ø Relatively minor accounting obstacles

Ä Presentation of unpaid subscribed share capital (Directive: recognised as asset vs. IFRS for SMEs: not recognised)

Ä Amortisation periods for goodwill where expected useful life cannot be reliably estimated (Directive: 5 years vs. IFRS for SMEs:10 years)

Standing for trust and integrity 291

EC Proposals (4/4) Ø Country by Country Reporting (CbyC) on payments made

to governments by the extractive industries and forestry companies

Ø Comparable to the US Dodd-Frank Act (July 2010) requiring SEC registered extractive industry companies to report on payments to governments

Ø To improve accountability in resource - rich emerging economies

Ø No specific threshold proposed for reporting

Ø Difficulty getting agreement by Member States

Standing for trust and integrity 292

Draft European Parliament (EP) & Council Positions (1/2)

Ø Accounting and auditing thresholds for small undertakings Ä EP and Council

q Member State option for the thresholds ranging from § Balance sheet total: EUR 4 million to EUR 6 million § Net turnover: EUR 8 million to EUR 12 million

q Average number of employees: 50

Ø Limited disclosure requirements for small companies Ä EP

q Further limitation to disclosure requirements by removing § off-balance sheet transactions § post balance sheet items § related party transactions

Ä Council q Member State option to require the above three disclosure

requirements

Standing for trust and integrity 293

Draft EP & Council Positions (2/2) Ø Audit requirement for small companies

Ä Council • Explicitly stating: Member States are not prevented from imposing an

audit on small companies Ø The use IFRS for SMEs

Ä EP and Council • The restriction to write off goodwill removed by a Member State

option to determine write off period between 5 - 10 years • Other obstacle retained

Ø Country By Country reporting Ä EP

• Threshold for disclosure per total payment of EUR 80,000 • The scope extension to large companies and PIEs active in banking,

construction or telecommunication industries Ä Council

• Threshold for disclosure per total payment of EUR 500,000 • No scope extension proposed to other industries

Standing for trust and integrity 294

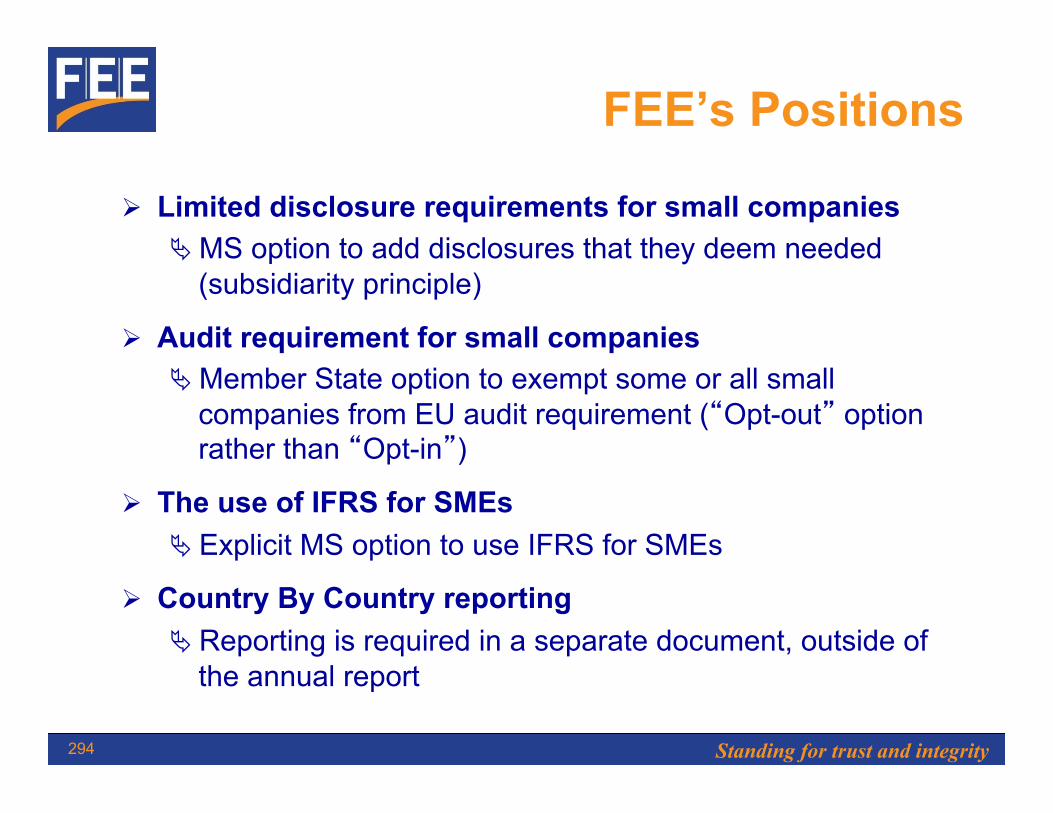

FEE’s Positions

Ø Limited disclosure requirements for small companies Ä MS option to add disclosures that they deem needed

(subsidiarity principle)

Ø Audit requirement for small companies Ä Member State option to exempt some or all small

companies from EU audit requirement (“Opt-out” option rather than “Opt-in”)

Ø The use of IFRS for SMEs Ä Explicit MS option to use IFRS for SMEs

Ø Country By Country reporting Ä Reporting is required in a separate document, outside of

the annual report

Standing for trust and integrity 295

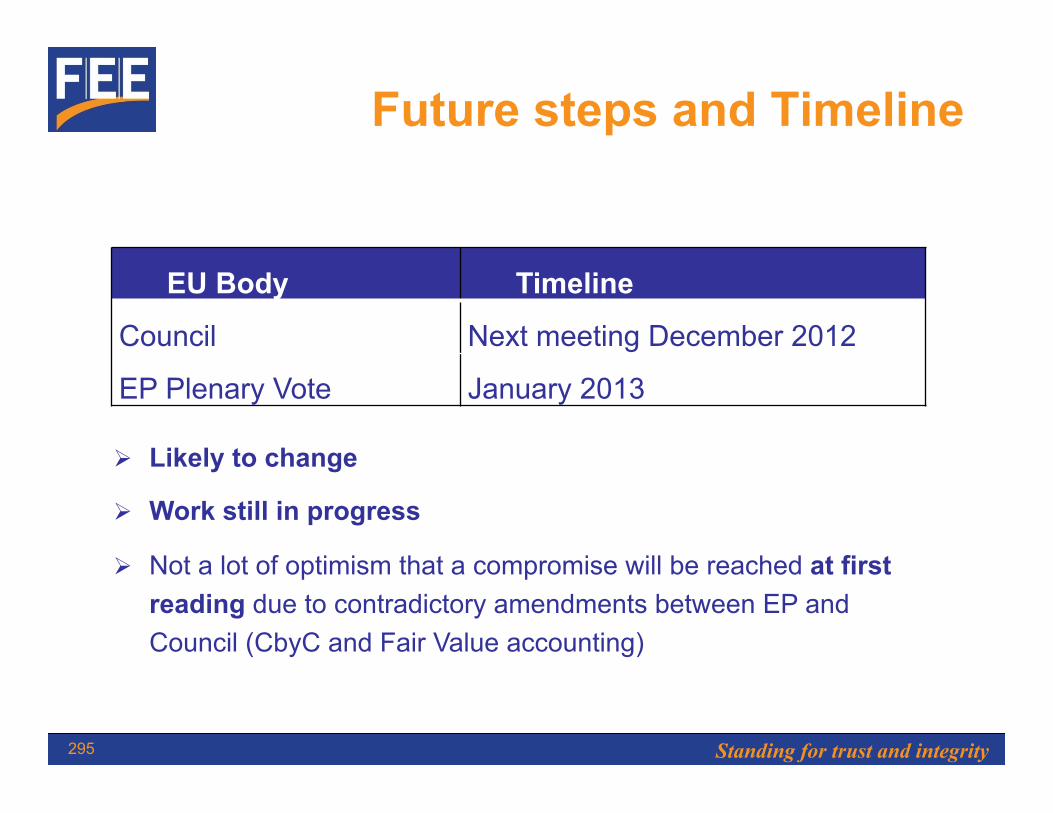

Future steps and Timeline

EU Body Timeline

Council Next meeting December 2012

EP Plenary Vote January 2013

Ø Likely to change

Ø Work still in progress

Ø Not a lot of optimism that a compromise will be reached at first reading due to contradictory amendments between EP and Council (CbyC and Fair Value accounting)

Standing for trust and integrity 296

Proposals to revise EU Audit Policy

Standing for trust and integrity 297

«Business as usual is not an option…»

How this started

Standing for trust and integrity 298

Ø EC Green Paper Consultation, Oct. 2010 Ä Role of the Auditor Ä Communication by auditors to stakeholders Ä International Standards on Auditing (ISAs) Ä Governance and Independence of Audit Firms Ä Supervision (public oversight) Ä Market structure and concentration Ä Creation of a European internal market for

auditing Ä Simplification: SMEs & SMPs Ä International cooperation

« No subject should be taboo »

Standing for trust and integrity 299

EC Audit Reform Proposals of 30 November 2011

Amending current 2006 Statutory Audit Directive for all statutory audits

Proposing new Regulation for audits of Public Interest Entities (PIEs)

Standing for trust and integrity 300

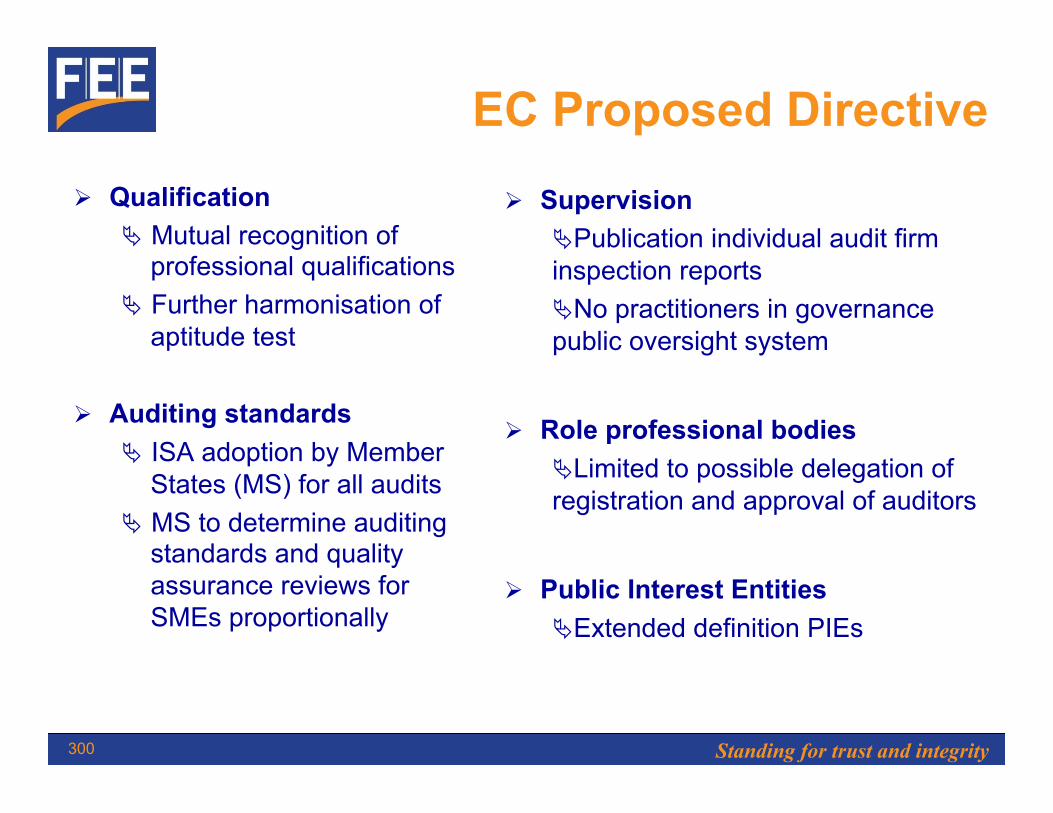

EC Proposed Directive Ø Qualification

Ä Mutual recognition of professional qualifications

Ä Further harmonisation of aptitude test

Ø Auditing standards Ä ISA adoption by Member

States (MS) for all audits Ä MS to determine auditing

standards and quality assurance reviews for SMEs proportionally

Ø Supervision Ä Publication individual audit firm inspection reports Ä No practitioners in governance public oversight system

Ø Role professional bodies Ä Limited to possible delegation of registration and approval of auditors

Ø Public Interest Entities Ä Extended definition PIEs

Standing for trust and integrity 301

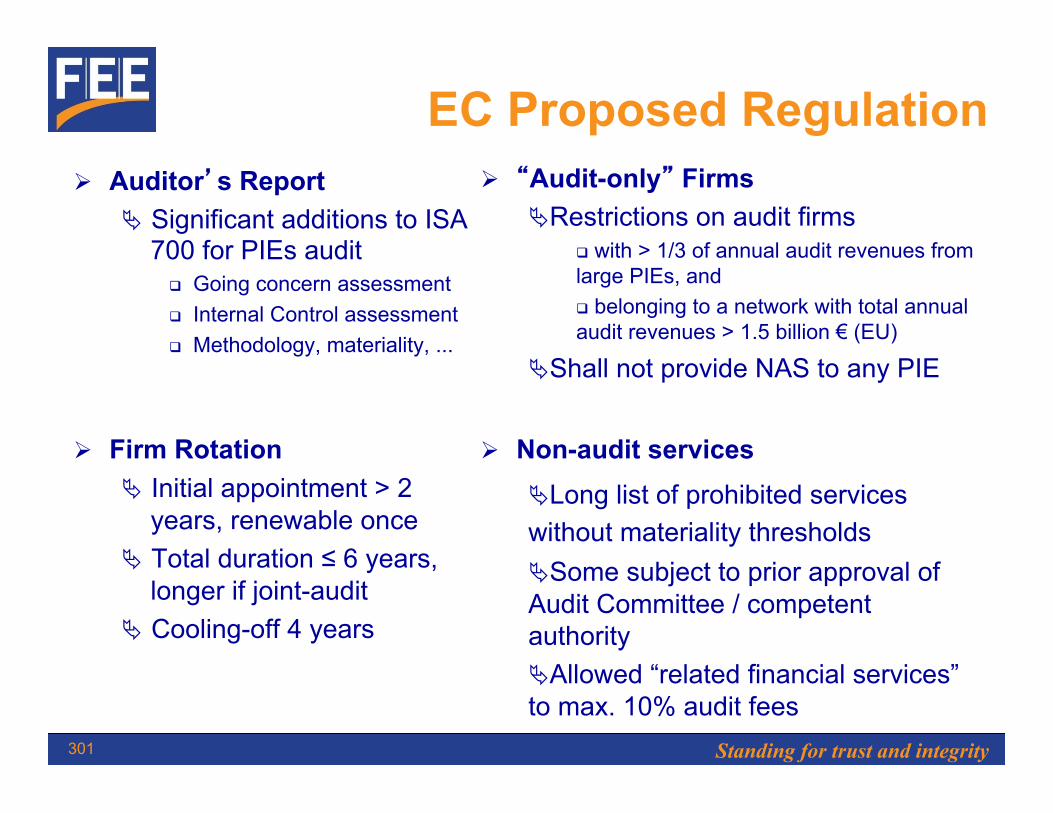

EC Proposed Regulation Ø Auditor’s Report

Ä Significant additions to ISA 700 for PIEs audit

q Going concern assessment q Internal Control assessment q Methodology, materiality, ...

Ø Firm Rotation Ä Initial appointment > 2

years, renewable once Ä Total duration ≤ 6 years,

longer if joint-audit Ä Cooling-off 4 years

Ø “Audit-only” Firms Ä Restrictions on audit firms

q with > 1/3 of annual audit revenues from large PIEs, and q belonging to a network with total annual audit revenues > 1.5 billion € (EU)

Ä Shall not provide NAS to any PIE

Ø Non-audit services Ä Long list of prohibited services without materiality thresholds Ä Some subject to prior approval of Audit Committee / competent authority Ä Allowed “related financial services” to max. 10% audit fees

Standing for trust and integrity 302

European Parliament Draft Opinions (1/3)

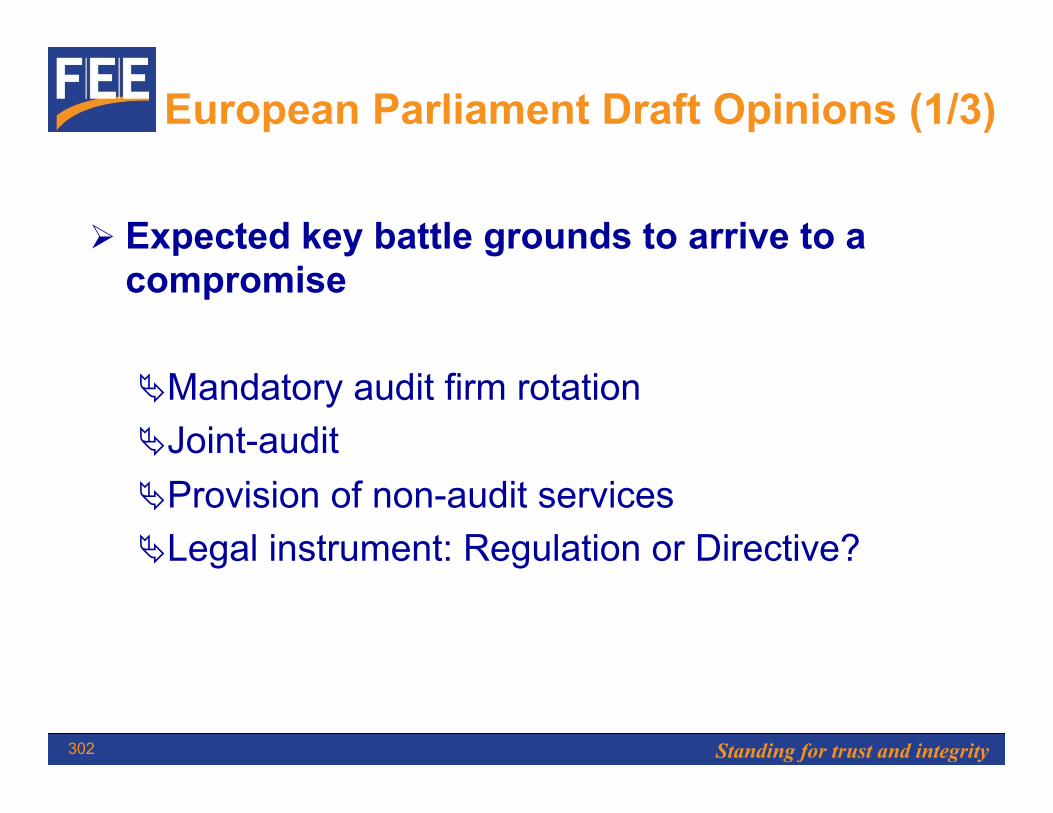

Ø Expected key battle grounds to arrive to a compromise

Ä Mandatory audit firm rotation Ä Joint-audit Ä Provision of non-audit services Ä Legal instrument: Regulation or Directive?

Standing for trust and integrity 303

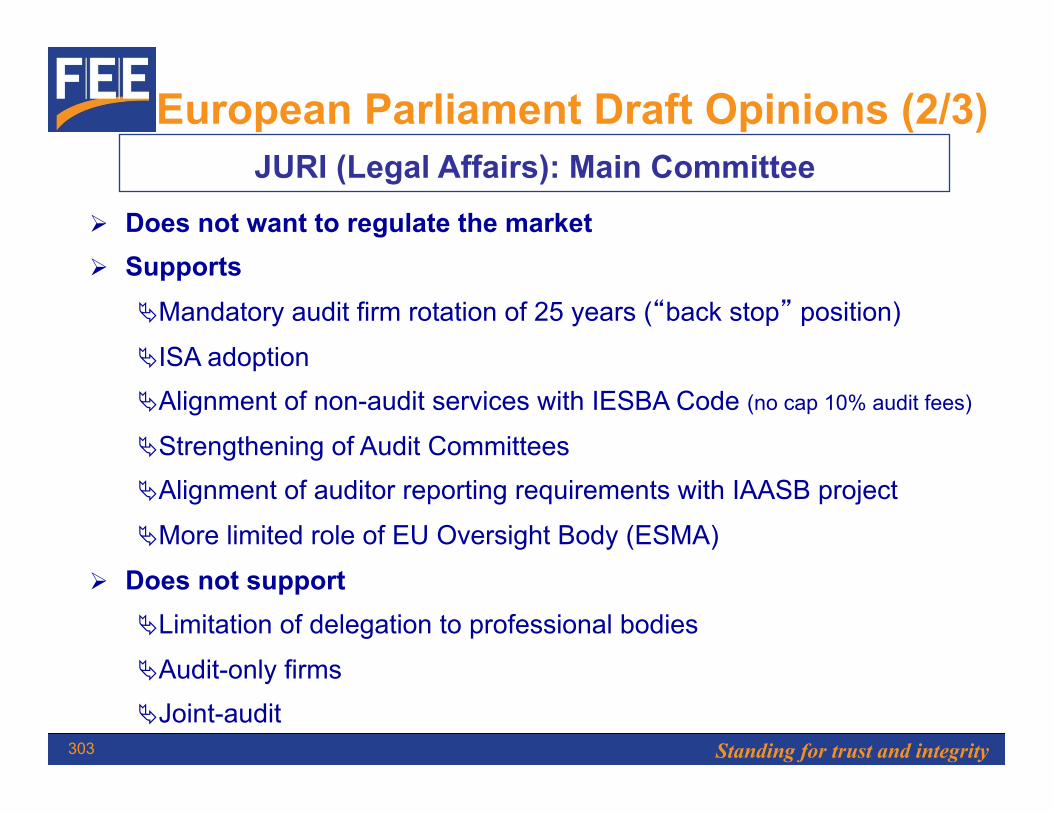

European Parliament Draft Opinions (2/3) JURI (Legal Affairs): Main Committee

Ø Does not want to regulate the market Ø Supports

Ä Mandatory audit firm rotation of 25 years (“back stop” position)

Ä ISA adoption Ä Alignment of non-audit services with IESBA Code (no cap 10% audit fees)

Ä Strengthening of Audit Committees Ä Alignment of auditor reporting requirements with IAASB project

Ä More limited role of EU Oversight Body (ESMA)

Ø Does not support Ä Limitation of delegation to professional bodies

Ä Audit-only firms Ä Joint-audit

Standing for trust and integrity 304

European Parliament Draft Opinions (3/3)

ECON (Economic & Monetary affairs): Secondary Committee

Ø Supports Ä Limitation of delegation to professional bodies Ä Alignment of non audit services with IESBA Code with 10% audit

fee cap Ä Tendering for non audit services Ä Strengthening of Audit Committees Ä Mandatory tendering for audit every 7 years

Ø Does not support Ä Audit-only firms

Ä Mandatory audit firm rotation Ä Joint-audit

Ä EU oversight role for ESMA

Standing for trust and integrity 305

Draft Council Opinions

Ø Different views being expressed by Member States, which want to stay much closer to 2006 Statutory Audit Directive

Ø Appropriateness of legal instrument Ä Audit report: better to wait for IAASB proposals? Ä Non-audit services: safeguards vs clear list of

prohibitions Ä Opposition to 10% cap on fees of financial audit services Ä Concerns about pure-audit firm proposal Ä No consensus on mandatory audit firm rotation Ä Questions on role of ESMA

Ø Compromise text being drafted by Cypriot Presidency

Standing for trust and integrity 306

Positions of the Accountancy Profession in Europe & FEE

Ø Delegation to professional bodies should be possible Ø PIE definition: no EU extension Ø ISA Adoption Ø Auditor reporting in line with IAASB proposals Ø Provision of non-audit services in line with IESBA Code Ø No cap (10%) of audit fees for provision of other services Ø No pure-audit firms Ø Strengthening role of Audit Committees Ø Audit market structure? Mandatory rotation of firms Ø Strengthening EU audit oversight

Standing for trust and integrity 307

Future steps and timeline

EU Body Timeline

EP Committees Vote Early 2013

EP Plenary Vote Spring 2013

Council Vote Under Irish Presidency H1 2013

Ø Likely to change

Ø Work still in progress

Standing for trust and integrity 308

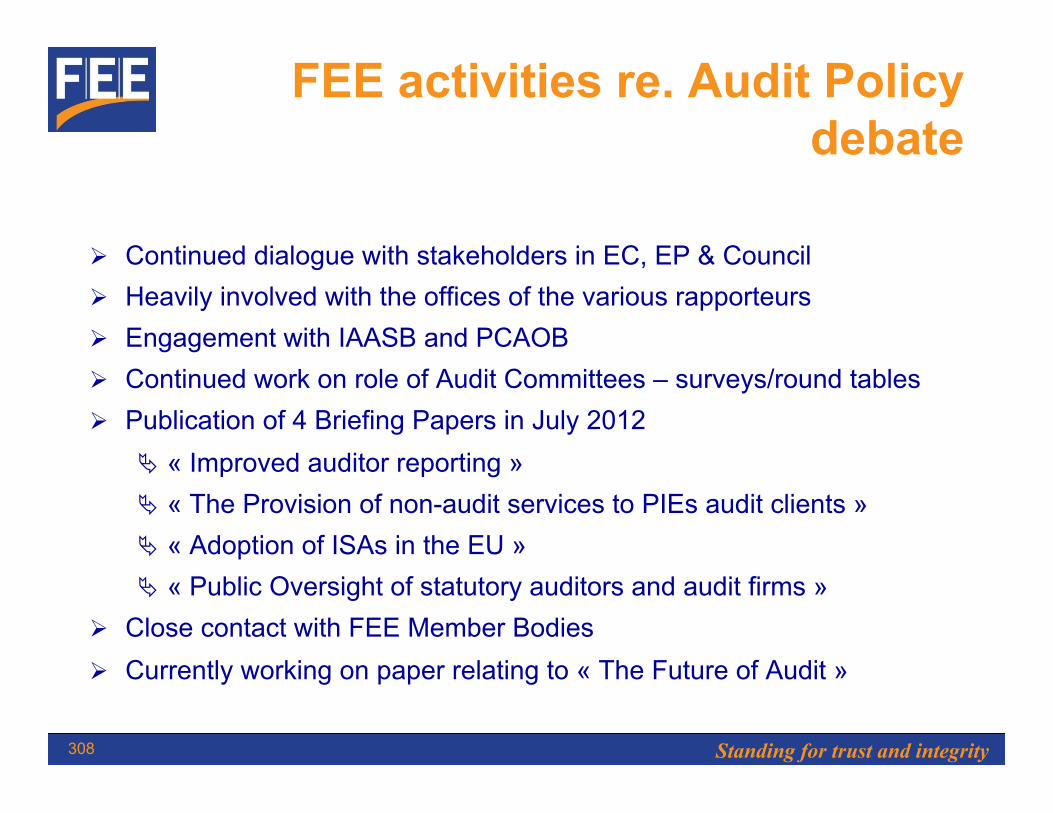

FEE activities re. Audit Policy debate

Ø Continued dialogue with stakeholders in EC, EP & Council Ø Heavily involved with the offices of the various rapporteurs Ø Engagement with IAASB and PCAOB Ø Continued work on role of Audit Committees – surveys/round tables Ø Publication of 4 Briefing Papers in July 2012

Ä « Improved auditor reporting » Ä « The Provision of non-audit services to PIEs audit clients » Ä « Adoption of ISAs in the EU » Ä « Public Oversight of statutory auditors and audit firms »

Ø Close contact with FEE Member Bodies Ø Currently working on paper relating to « The Future of Audit »

Standing for trust and integrity 309

Questions

Standing for trust and integrity 310

Standing for trust and integrity

Visit us @ www.fee.be