20

Daniel M. Hofmann Senior Advisor Financial Stability The Geneva Association ISCM, Zurich, 15 September 2016 Nat Cat Protection Gaps in Emerging Market Economies

Daniel M. HofmannSenior Advisor Financial Stability

The Geneva Association

ISCM, Zurich, 15 September 2016

Nat Cat Protection Gapsin Emerging Market Economies

222

A FIRST INDICATOR – THE S-CURVECOUNTRIES BELOW THE CURVE ARE UNDERINSURED

Source: Swiss Re

Non-life insurance penetration; premium in percent of GDP/capita (2013)

333

A SECOND INDICATOR – THE GAP BETWEEN INSURED AND TOTAL LOSSESURBANISATION IN KNOWN RISK ZONES DRIVES GAP WIDENING

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

1976-1985 1986-1995 1996-2005 2006-2015

In p

erce

nt o

f GD

P

Total losses Insured losses

Source: Swiss Re

Insured and total economic losses in percent of gross domestic product (GDP)

△ = 40%

△ = 68%

△ = 73%

444

GLOBAL PROTECTION GAPS

Source: Swiss Re

High concentration of absolute property protection gaps

Annual expected natural catastrophe damage losses (USD bn, 2014)

USJapanChinaMexicoItalyTaiwanTurkeyPhilippinesIndonesiaGermanyCanadaIndiaChile

-5-10-15-20-25-30 5 10 15 20 25 30

Insured earthquakeUninsured earthquake

Insured floodUninsured flood

Insured windUninsured wind

INSURED UNINSURED

0

• Models estimate global uninsured Nat Cat losses at USD 153 bn annually

• Additional property under-insurance protection gap estimated at USD 68 bn

• Total annual/global NL protection gap USD 221 bn

• US Biggest uninsured: EQBiggest insured: Wind

• JapanBiggest uninsured: EQ

• ChinaBiggest uninsured: EQ and flood

• Global Life gap USD 86 trill

555

RELATIVE GAPS CONCENTRATED ON EMERGING MARKET ECONOMIES (EMEs)

0%

20%

40%

60%

80%

100%

120%

CHN COL JPN IDN IND TRK ESP AUS USA GBR CAN NZL

Nat Cat protection gap in percent of economic losses (1974-2013)(Selective sample only to illustrate predicament of EMEs)

Source: Swiss Re

• Urbanisation contributes to high property concentrations in known risk zones

666

JapanCalifornia

PROTECTION GAPS IN ADVANCED MARKET ECONOMIES (AMEs)THE SPECIAL CASES OF CALIFORNIA AND JAPAN

Last big event Northridge 1994

Economic loss USD 44 bn

Fatalities 61

Insured loss USD 24.5 bn (in 2015 prices)- 55.7% of total

HO policies in force 10% of total (was >70% on new homes 3 years after Northridge)

Commercial policies in force

55% of total but varying coverage

Reasons for gap • Anomalous industry reaction• Consumers’ inability to

comprehend low frequency risk• High premiums• 10% to 20% deductible; 15%

on CEA policies• Moral hazard (FEMA will pay)

Potential remedies • Compulsory EQ insurance• Federal reinsurance backstop• Cooperative reserve pool• Change tax rules on reserving

Last big event Fukushima 2011

Economic loss USD 210 bn

Fatalities 15,880

Insured loss USD 40.0 bn (in 2015 prices)- 19.0% of total

HO policies in force >74%

Commercial policies in force

11% of total

Reasons for gap • Focus on commercial cover but compensated by- Effective pre-disaster miti-

gation; good business conti-nuity (BCM) management

• Very high PML and • Little global reinsurance cover

Potential remedies • Make access to global reinsurance more attractive

CEA: California Earthquake Authority; FEMA: Federal Emergency Management Auhority

777

0

20

40

60

80

100

120

140

Perc

ent

Economic losses (USD bn)Haiti 8.0Chile 30.0NZ 20.0 (3 quakes total)

A TALE OF THREE EARTHQUAKES HAITI, CHILE, AND NEW ZEALAND (2010)

Haiti Chile NZ Haiti Chile NZ

Insured loss in percent of total Economic loss in percent of GDP

Haiti (Haiti) Chile (Maulé) New Zealand (Canterbury) Oct. 2010 – Feb. 2011

Magnitude 7.0 8.8 7.1

Buildings damaged 177,000 – 313,000 1,500,000 > 200,000

Fatalities 92,000 – 225,000 521 - 577 185

Source: CATDAT

3 quakes in total

3 quakes in total

888

CHILE, HAITI, AND NEW ZEALAND – FIVE YEARS LATER

80

90

100

110

120

130

09 10 11 12 13 14

Real GDP 2009=100

Chile – Uneven recovery Haiti – Still in shambles

80.0

90.0

100.0

110.0

120.0

130.0

09 10 11 12 13 14

Real GDP 2009=100

NZ – Steady recovery underway

80.0

90.0

100.0

110.0

120.0

130.0

09 10 11 12 13 14

Real GDP 2009=100

• In general, relative small structural damages due to strong building codes (withstand 9.0 magnitude)

• Steady reconstruction of private housing; <75% completed

• 85,000 people still housed in tent cities; many more in ramshackle temporary buildings

• Only small aid flows reached the country: of USD 2 bn in U.S. AID money only 0.7% reached Haiti; much of the remainder trickled down into Washington-based contractors

• Insurance industry paid out NZD 16.7bn; Earthquake Commission (EQC) paid NZD 9.0bn

• 4,500 claims yet to be settled

• Majority of 70,000 home repairs completed

• Surge in construction, yet parts of downtown Canterbury and Christ-church inhabitable due to many after-quakes

999

CAUSES OF UNDERINSURANCE IN EMERGING MARKET ECONOMIES (EMEs)

Cultural • Stigma on financial services (Takaful)• Lack of awareness and financial literacy

Economic development

• ”Backwardness”• Lack of affordability• Dominant state sector, weak private sector• Weak financial infrastructure• Weak institutional and governance frameworks in support

of private insurance market development• Inability to enforce contracts• Weak regulation; inadequate supervision

Insurance specific• Insufficient exposure data; weak cat modelling• Inability to implement appropriate risk-pricing• Broader limits to insurability

Source: The Geneva Association / DMH

101010

-2.0-1.5-1.0-0.50.00.51.01.52.0

GDP cumulative – 100% insured

t = years

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5GDP growth path – 100% insured

t = years

-4.0

-3.0

-2.0

-1.0

0.0

1.0GDP cumulative – uninsured

t = years

-1.5

-1.0

-0.5

0.0

0.5

1.0GDP growth path – uninsured

t = years

DOES INSURANCE WORK?POST-CATASTROPHE GDP DEVELOPMENT WITH AND WITHOUT INSURANCE SOLUTIONS

Source: v. Peter, v. Dahlen, Saxena, “Unmitigated disaster,” BIS WP No. 394, 2012

Based on a sample of 2,381 Nat Cats of category 4 or higher in 203 countries/jurisdictions, period 1960-2011

111111

Ø Potential to break the cycle between vulnerability and povertyØ 4 billion customers with unmet needs; accessible through new distribution channels (cell phones)Ø Impressive growth rates (although from low levels); but so far only a drop in the bucket

THE ROLE OF INNOVATION – 1MICRO-INSURANCE

Lives covered Micro-GWPUSD million

Micro-insurance GWPin % of total EME GWPmillion in % of total pop

Africa 44.4 4.4 550 0.9

Asia 170.4 4.3 830 0.2

Latin America 48.6 7.9 830 0.5

Total 263.4 2,210Source: Munich Re; Swiss Re

0% 2% 4% 6% 8%

LatamAsia

AfricaEMEsAMEsInsurance penetration rates (premiums / GDP) Premiums in USD million (2015)

AMEs

EMEs

Africa

Asia

Latam

3,704,063

849,723

64,123

524,211

158,146

121212

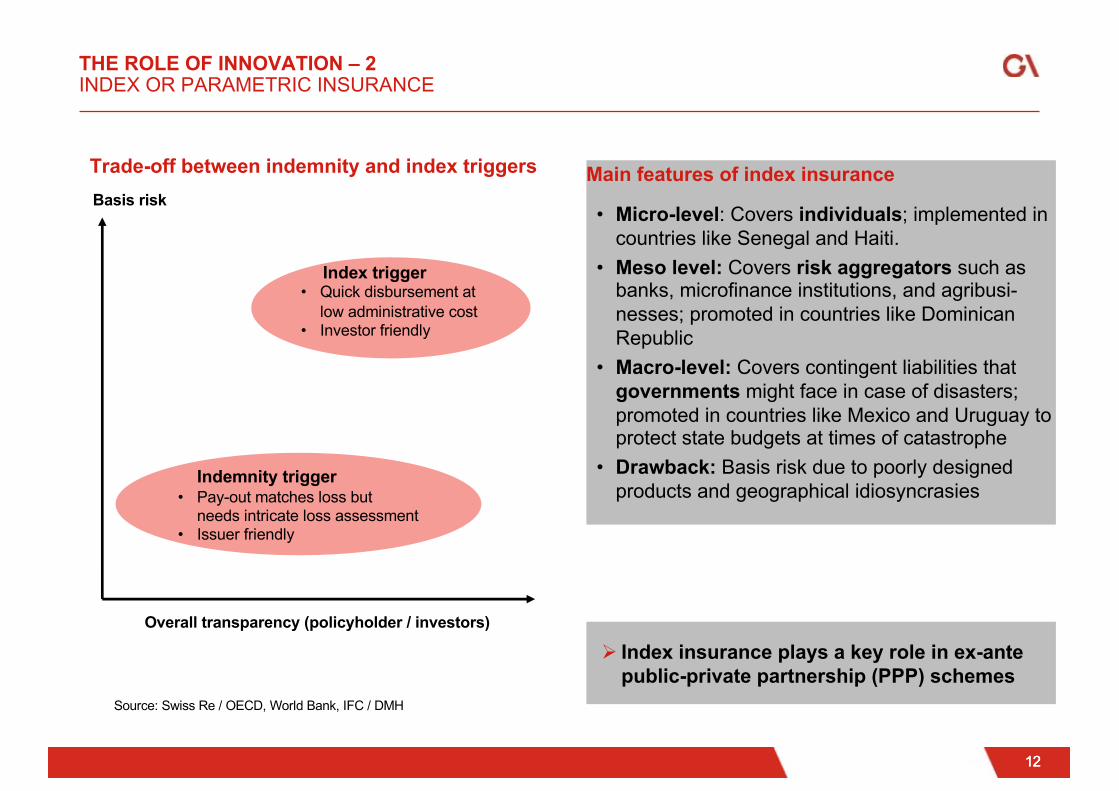

THE ROLE OF INNOVATION – 2INDEX OR PARAMETRIC INSURANCE

Basis risk

Overall transparency (policyholder / investors)

Source: Swiss Re / OECD, World Bank, IFC / DMH

Indemnity trigger• Pay-out matches loss but

needs intricate loss assessment• Issuer friendly

Index trigger• Quick disbursement at

low administrative cost• Investor friendly

Main features of index insurance

• Micro-level: Covers individuals; implemented in countries like Senegal and Haiti.

• Meso level: Covers risk aggregators such as banks, microfinance institutions, and agribusi-nesses; promoted in countries like Dominican Republic

• Macro-level: Covers contingent liabilities that governments might face in case of disasters; promoted in countries like Mexico and Uruguay to protect state budgets at times of catastrophe

• Drawback: Basis risk due to poorly designed products and geographical idiosyncrasies

Trade-off between indemnity and index triggers

Ø Index insurance plays a key role in ex-ante public-private partnership (PPP) schemes

131313

Three enabling factors• High PMLs and skewed loss distributions make for an

expensive Nat Cat capital allocation• Shrinking retro market after 2005 hurricane season;

also persistent regulatory pressure on retro market• Investors seek non-market correlated assets with high

Sharpe ratios

Innovative ART solutions• Insurance-linked securities (ILS) such as industry loss

warrants (ILWs), cat bonds and sidecars

Main challenges• For issuers and investors: design of triggers • For investors:

– Lack of transparency– Rating agency concerns– Liquidity

Potential solutions• Move from bespoke to standardised solutions• Allow for tranching to meet desired ratings and enable

bunching in tradeable derivatives

THE ROLE OF INNOVATION – 3PUSHING THE ART FRONTIER

51.3

37.0

25.1

2.7 3.0 1.60.1 0.9 0.10.0

10.0

20.0

30.0

40.0

50.0

60.0

EQ 6 events

Wind 27 events

Flood 18 events

USD

billi

on

High PMLs and skewed loss distributions

MaxMedianMin

Loss distribution of significant disasters over 50 years (U.S.)Source: Kunreuther and Michel-Kerjan (2009)

141414

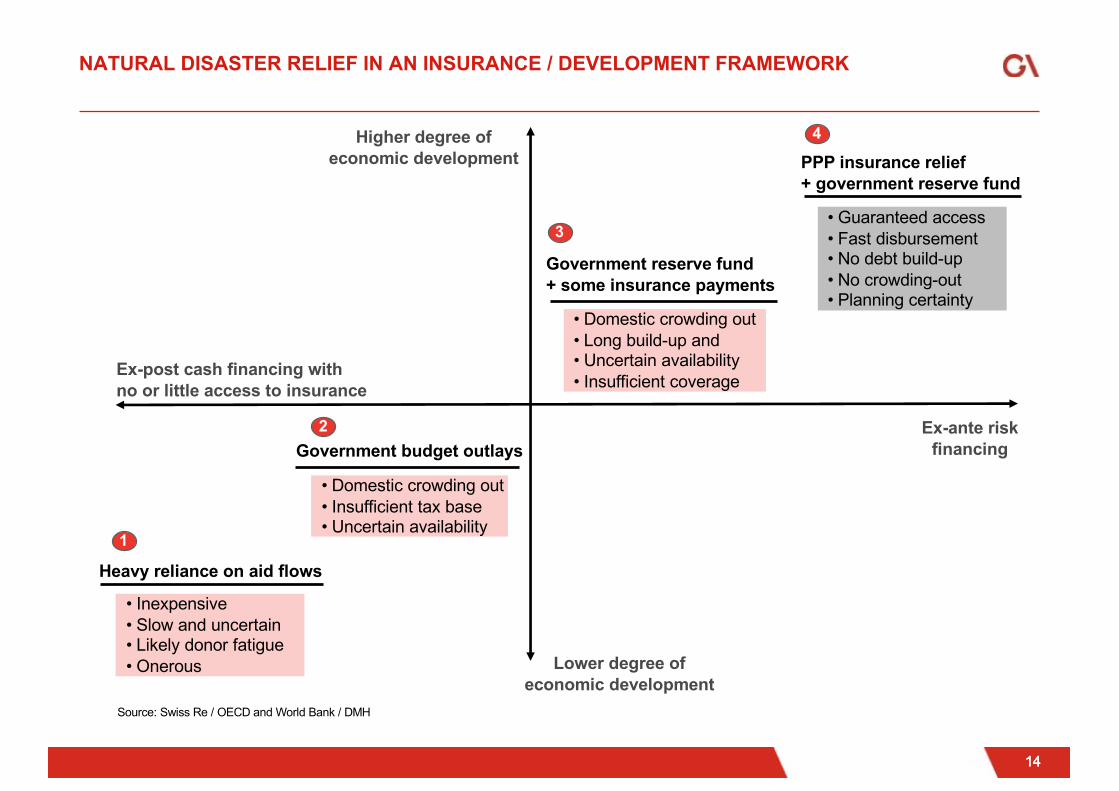

NATURAL DISASTER RELIEF IN AN INSURANCE / DEVELOPMENT FRAMEWORK

Higher degree ofeconomic development

Lower degree ofeconomic development

Ex-ante riskfinancing

Ex-post cash financing withno or little access to insurance

Heavy reliance on aid flows

Government budget outlays

Government reserve fund+ some insurance payments

PPP insurance relief+ government reserve fund

Source: Swiss Re / OECD and World Bank / DMH

• Inexpensive• Slow and uncertain• Likely donor fatigue• Onerous

• Domestic crowding out• Insufficient tax base• Uncertain availability

• Domestic crowding out• Long build-up and• Uncertain availability• Insufficient coverage

• Guaranteed access• Fast disbursement• No debt build-up• No crowding-out• Planning certainty

1

2

3

4

151515

CLOSING THE EME INSURANCE GAP REQUIRES A MULTI-STAKEHOLDER APPROACH

Cultural • Promote financial literacy and risk awareness

Economic development

• Strengthen financial infrastructure and market governance• Promote private sector development• Enforce contractual certainty• Enact regulation and strengthen supervision and establish

effective compulsory regimes

Insurance specific

• Promote risk prevention and risk mitigation• Encourage product innovation and new distribution channels• Reduce product complexity and improve product transparency• Promote micro-insurance• Deploy technology to enable more sophisticated u/w and risk

modelling• Promote collective data collection and data sharing to strengthen

cat / exposure modelling and improve loss estimates• Promote regional cat risk pooling• Build public-private partnerships (PPPs) • Promote financial innovation and tap into (global) capital markets

to enhance financial resilience in EMEs

Source: The Geneva Association / DMH

161616

Filling the protection gap is not a marketing slogan but a development need. However, in order to deliver, the industry needs to address a number of interrelated issues with respect to

• Products: 4 billion unmet customer needs require new solutions; micro-insurance will likely be part of the answer

• Distribution: The digital economy allows EMEs to leapfrog technological development stages; in designing new distribution models, insurers must harness digital solutions

• Risk / exposure modelling: Deploy technology (geo-spatial and big data) to improve underwriting and risk modelling capacity

• Capacity: Access to capital will increasingly be a limiting factor in providing Nat Cat cover; (re)insurers must continue to push the boundaries of ART solutions

• Regulation: – AMEs: Carefully consider capital standards for Nat Cat covers and ART solutions– EMEs: Priority to institutional capacity building and strengthening of domestic supervision

• Economic development: Insurance could play a vital role in catalysing economic development; PPPs sponsored by (re)insurers are likely to play a more prominent role

Ø An attitude problem: In an advanced market perspective insurance solutions for emerging market economies are often considered orphans and do not attract appropriate attention

WHAT NEXT?MEDIUM-TERM CHALLENGES TO MEET A REAL DEVELOPMENT NEED

171717

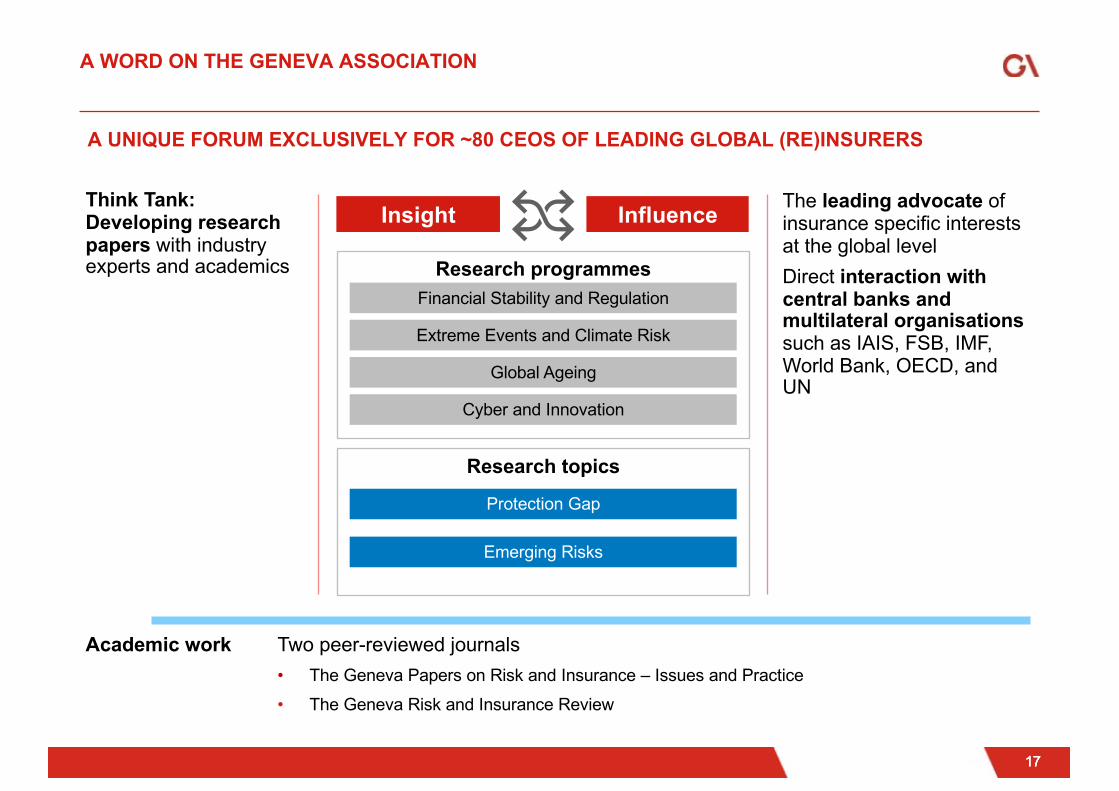

A WORD ON THE GENEVA ASSOCIATION

InfluenceInsight

Research programmesFinancial Stability and Regulation

Extreme Events and Climate Risk

Global Ageing

Cyber and Innovation

Research topics

Protection Gap

Emerging Risks

Think Tank: Developing research papers with industry experts and academics

The leading advocate of insurance specific interests at the global levelDirect interaction with central banks and multilateral organisationssuch as IAIS, FSB, IMF, World Bank, OECD, and UN

Academic work Two peer-reviewed journals • The Geneva Papers on Risk and Insurance – Issues and Practice • The Geneva Risk and Insurance Review

A UNIQUE FORUM EXCLUSIVELY FOR ~80 CEOS OF LEADING GLOBAL (RE)INSURERS

181818

EXAMPLE: OUR GLOBAL PROTECTION GAP RESEARCH ACTIVITIES

2014: The Global Insurance Protection Gap

Two major publications in 2014 / 2015

2015: Insuring Flood Riskin Asia’s High-Growth Markets

191919

• Structural features of today’s insurance markets: gauging the potential for digital• How digitisation impacts the economics and business models of insurance• Case studies (focus on emerging markets)• Stakeholder recommendations• Research complemented by more than 20 expert/executive interviews• To be published in Q4 2016

Upcoming GA study: Harnessing technology to narrow the protection gap

THE UNIVERSE OF PROTECTION GAPS IS WIDE AND GROWING

• Pensions / savings gap GA publication scheduled for Q4/2016 • Life protection and mortality gap

Other identified gaps