26

NATURAL GAS – SECURE ENERGY FOR THE FUTURE IEI EVENING LECTURE DENIS TWOMEY, COMMERCIAL OPERATIONS MANAGER, BORD GÁIS NETWORKS FEBUARY 21ST, 2006

NATURAL GAS – SECURE ENERGY FOR THE FUTURE

IEI EVENING LECTURE

DENIS TWOMEY, COMMERCIAL OPERATIONS MANAGER, BORD GÁIS NETWORKS

FEBUARY 21ST, 2006

CONTENTS

GLOBASLISED GAS MARKET

SECURITY OF SUPPLY• Infrastructure• Fuel Diversity

THE IRISH SITUATION

GAS PRICING• Transportation Tariffs• International Wholesale Gas Prices

ENVIRONMENT

SUMMARY

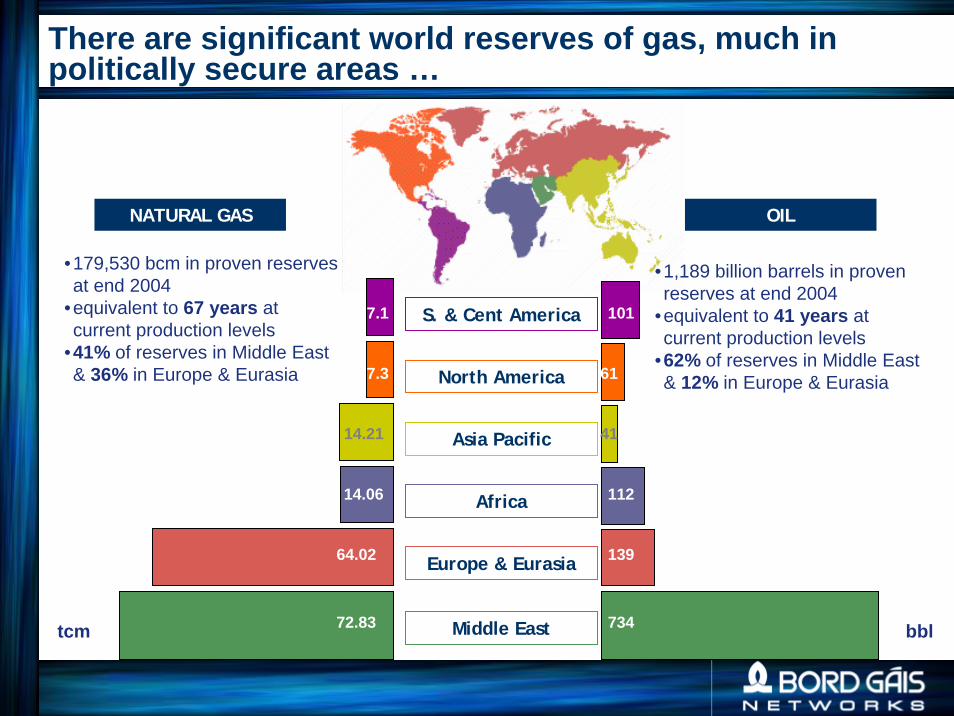

There are significant world reserves of gas, much in politically secure areas …

S. & Cent America

Europe & Eurasia

Middle East

Asia Pacific

North America

Africa

NATURAL GAS OIL

•179,530 bcm in proven reserves at end 2004

•equivalent to 67 years at current production levels

•41% of reserves in Middle East & 36% in Europe & Eurasia

•1,189 billion barrels in proven reserves at end 2004

•equivalent to 41 years at current production levels

•62% of reserves in Middle East & 12% in Europe & Eurasia

72.83tcm bbl

7.3

14.21

14.06

64.02

7.1

734

61

41

112

139

101

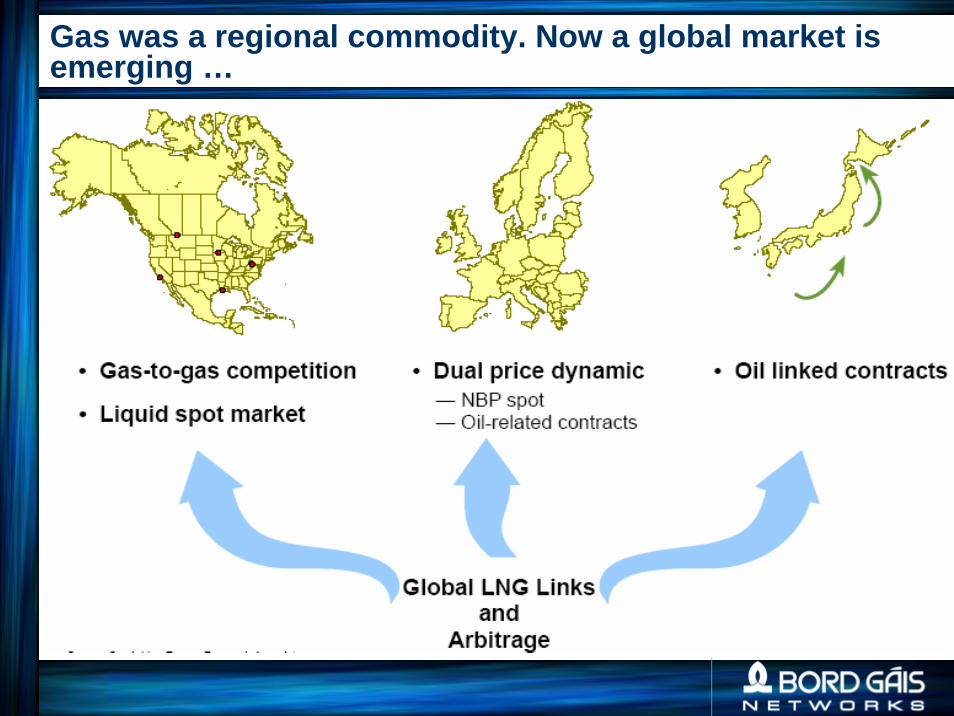

Gas was a regional commodity. Now a global market is emerging …

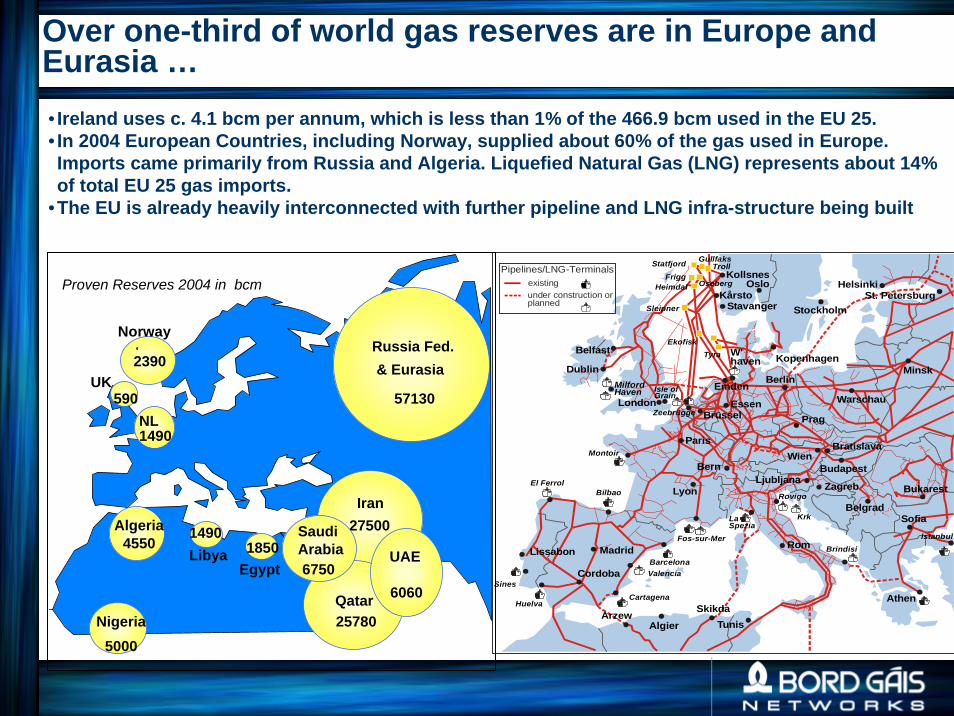

Over one-third of world gas reserves are in Europe and Eurasia …

ArzewSkikda

Cordoba

Lyon

St. Petersburg

Rom

Helsinki

Ljubljana

Oslo

StavangerKårsto

Kollsnes

Algier

Madrid

London

Kopenhagen

Prag

Berlin

BratislavaWien

Stockholm

Athen

Paris

Essen

Emden

Lissabon

Huelva

SinesCartagena

Barcelona

Fos-sur-Mer

Bilbao

Krk

Istanbul

La Spezia

Montoir

Zeebrügge

TyraEkofisk

TrollGullfaksStatfjord

HeimdalFrigg

Sleipner

Budapest

Tunis

Brüssel

Sofia

Bern

Belgrad

Dublin

Belfast

Warschau

Minsk

Bukarest

Oseberg

W'haven

ZagrebRovigo

El Ferrol

Valencia

Brindisi

Isle ofGrain

MilfordHaven

under construction orplanned

existingPipelines/LNG-Terminals

• Ireland uses c. 4.1 bcm per annum, which is less than 1% of the 466.9 bcm used in the EU 25.• In 2004 European Countries, including Norway, supplied about 60% of the gas used in Europe. Imports came primarily from Russia and Algeria. Liquefied Natural Gas (LNG) represents about 14% of total EU 25 gas imports.

•The EU is already heavily interconnected with further pipeline and LNG infra-structure being built

Proven Reserves 2004 in bcm

1490

590

Russia Fed. & Eurasia

57130

2390

5000Nigeria

Algeria

Norway

UK

NL

Iran27500

Qatar25780

UAE

6060

Libya1490

4550

Egypt1850

SaudiArabia6750

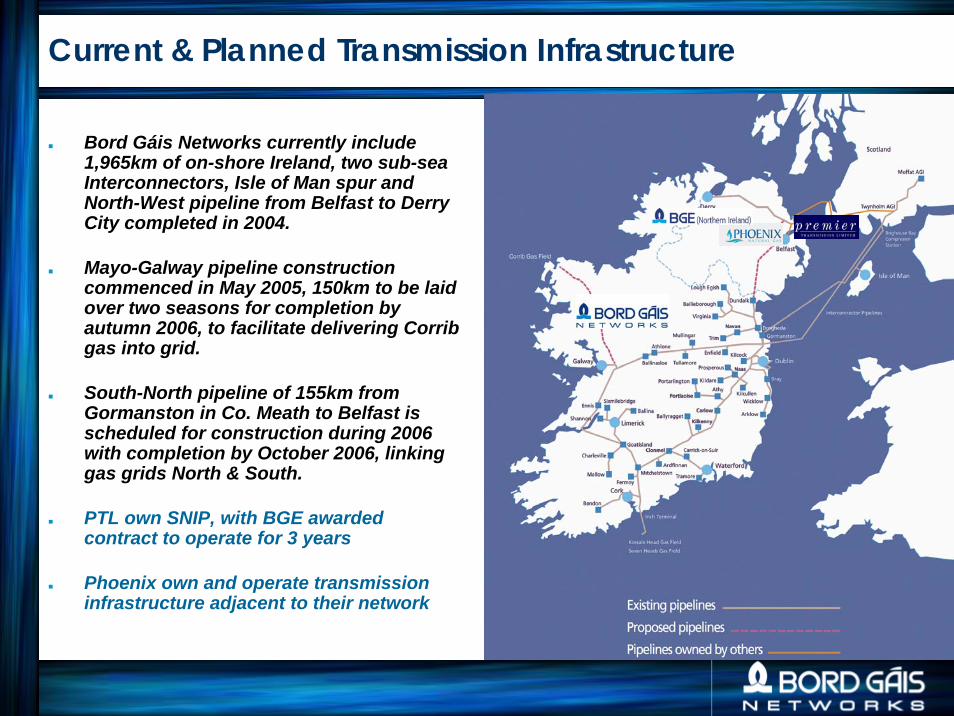

Current & Planned Transmission Infrastructure

Bord Gáis Networks currently include 1,965km of on-shore Ireland, two sub-sea Interconnectors, Isle of Man spur and North-West pipeline from Belfast to Derry City completed in 2004.

Mayo-Galway pipeline construction commenced in May 2005, 150km to be laid over two seasons for completion by autumn 2006, to facilitate delivering Corrib gas into grid.

South-North pipeline of 155km from Gormanston in Co. Meath to Belfast is scheduled for construction during 2006 with completion by October 2006, linking gas grids North & South.

PTL own SNIP, with BGE awarded contract to operate for 3 years

Phoenix own and operate transmission infrastructure adjacent to their network

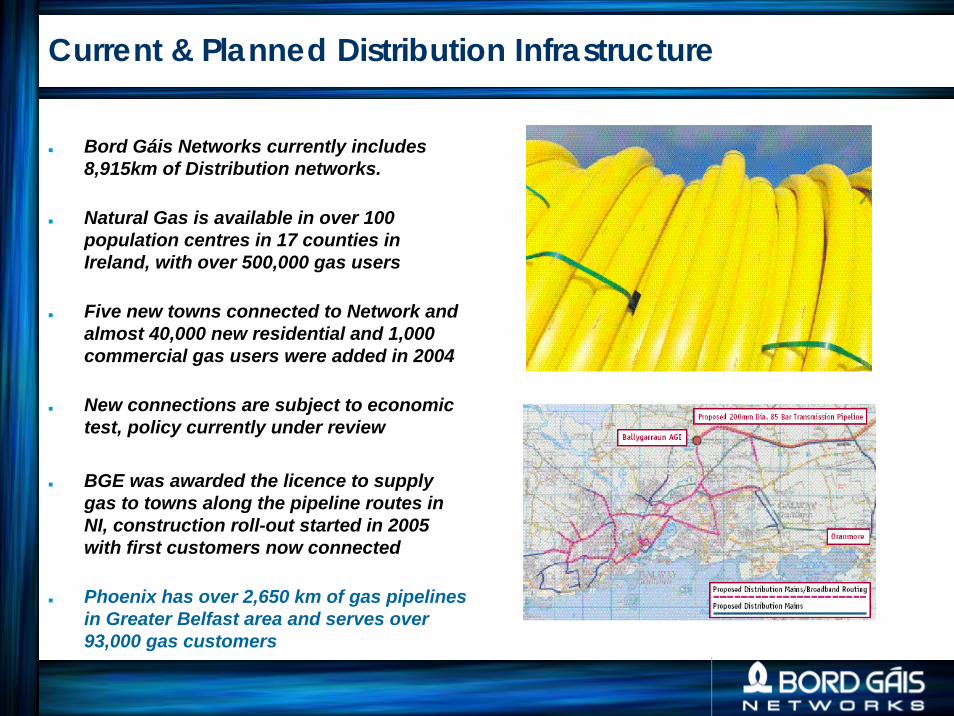

Current & Planned Distribution Infrastructure

Bord Gáis Networks currently includes 8,915km of Distribution networks.

Natural Gas is available in over 100 population centres in 17 counties in Ireland, with over 500,000 gas users

Five new towns connected to Network and almost 40,000 new residential and 1,000 commercial gas users were added in 2004

New connections are subject to economic test, policy currently under review

BGE was awarded the licence to supply gas to towns along the pipeline routes in NI, construction roll-out started in 2005 with first customers now connected

Phoenix has over 2,650 km of gas pipelines in Greater Belfast area and serves over 93,000 gas customers

The regimes in both jurisdictions have developed separately reflecting local market conditions. Significant recent developments include:

Northern Ireland– Introduction of Postalised Transmission Tariff in NI among three pipeline owners

• Required changes to contractual terms and licences, and new processes e.g. Common Fund• Facilitated gas to Coolkeeragh & towns along routes

– Mutualisation of SNIP• Required stronger regulatory underpinning of risk• Facilitated lower tariffs – lower capital returns, projected lower opex

– Market Developments• Market open to 75,000 therms level in Greater Belfast area• BGE bringing gas to ten new towns along routes of new pipelines

Republic of Ireland– Entry/Exit transportation regime

• More flexibility for shippers• Facilitates sale of gas at IBP

– Unified Code of Operations for Transmission & Distribution• Streamlined service to shippers, e.g. single code

– Market Developments• Market open to non-household level, plans developed for full market opening due mid 2006

Current Commercial & Operational regimes

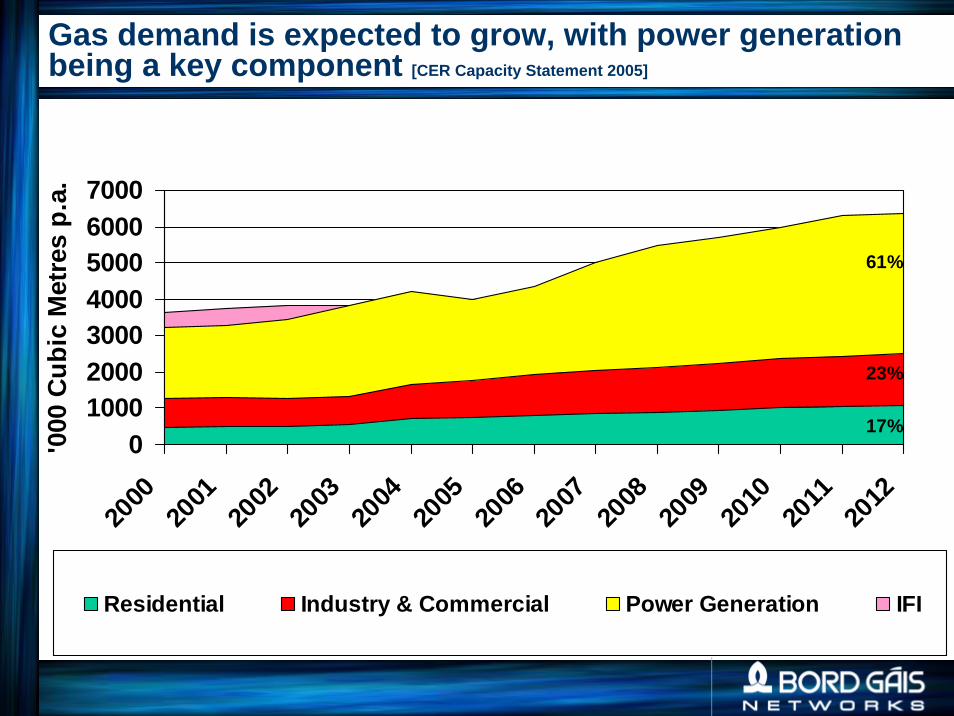

Gas demand is expected to grow, with power generation being a key component [CER Capacity Statement 2005]

01000200030004000500060007000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

'000

Cub

ic M

etre

s p.

a.

Residential Industry & Commercial Power Generation IFI

61%

23%

17%

0

5

10

15

20

25

30

35

40

45

50

NLHun

gary UKIta

lyLati

viaLith

uania

Slovakia

Belgium

Lithuan

iaIre

land

EU 25 av

erage

Austri

aDen

mark

German

yCze

ch R

ep.

Spain

France

Estonia

Portugal

Poland

Finalnd

Slovenia

Switzerl

and

Greec

eSwed

en

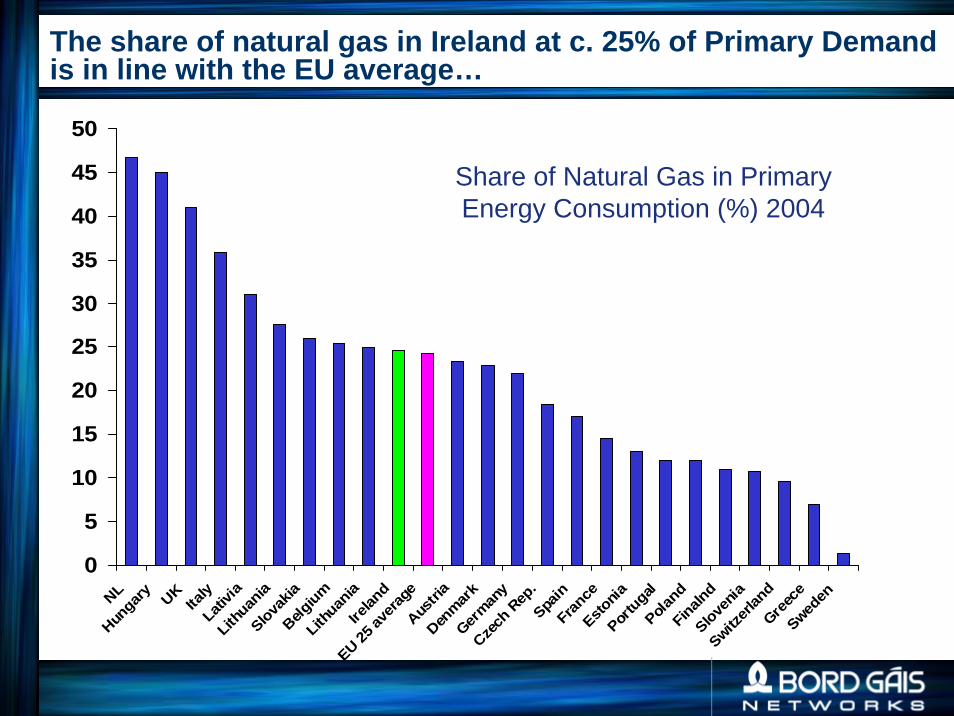

Share of Natural Gas in Primary Energy Consumption (%) 2004

The share of natural gas in Ireland at c. 25% of Primary Demand is in line with the EU average…

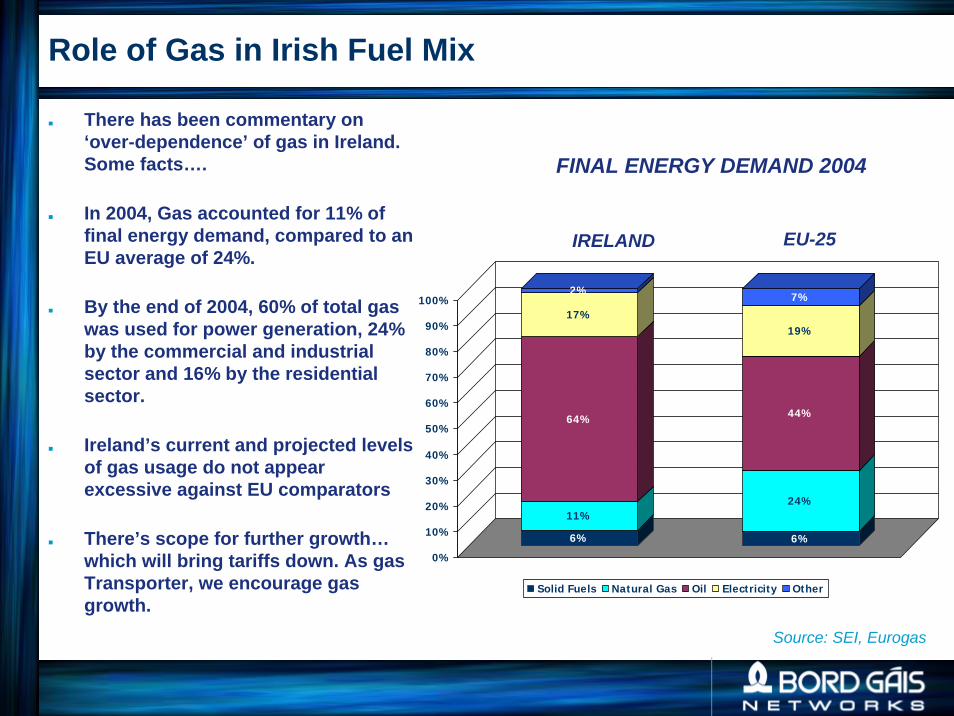

Role of Gas in Irish Fuel Mix

There has been commentary on ‘over-dependence’ of gas in Ireland. Some facts….

In 2004, Gas accounted for 11% of final energy demand, compared to an EU average of 24%.

By the end of 2004, 60% of total gas was used for power generation, 24% by the commercial and industrial sector and 16% by the residential sector.

Ireland’s current and projected levels of gas usage do not appear excessive against EU comparators

There’s scope for further growth…which will bring tariffs down. As gas Transporter, we encourage gas growth.

Source: SEI, Eurogas

6%

11%

64%

17%

2%

6%

24%

44%

19%

7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Solid Fuels Natural Gas Oil Electricity Other

IRELAND EU-25

FINAL ENERGY DEMAND 2004

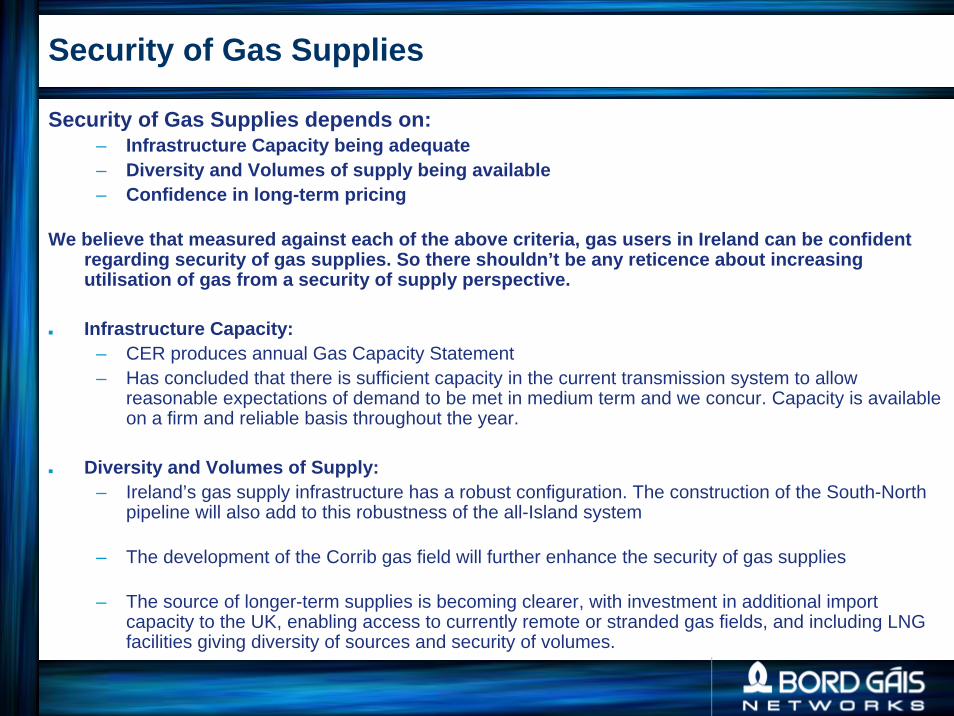

Security of Gas Supplies

Security of Gas Supplies depends on:– Infrastructure Capacity being adequate– Diversity and Volumes of supply being available– Confidence in long-term pricing

We believe that measured against each of the above criteria, gas users in Ireland can be confident regarding security of gas supplies. So there shouldn’t be any reticence about increasing utilisation of gas from a security of supply perspective.

Infrastructure Capacity:– CER produces annual Gas Capacity Statement– Has concluded that there is sufficient capacity in the current transmission system to allow

reasonable expectations of demand to be met in medium term and we concur. Capacity is available on a firm and reliable basis throughout the year.

Diversity and Volumes of Supply:– Ireland’s gas supply infrastructure has a robust configuration. The construction of the South-North

pipeline will also add to this robustness of the all-Island system

– The development of the Corrib gas field will further enhance the security of gas supplies

– The source of longer-term supplies is becoming clearer, with investment in additional import capacity to the UK, enabling access to currently remote or stranded gas fields, and including LNG facilities giving diversity of sources and security of volumes.

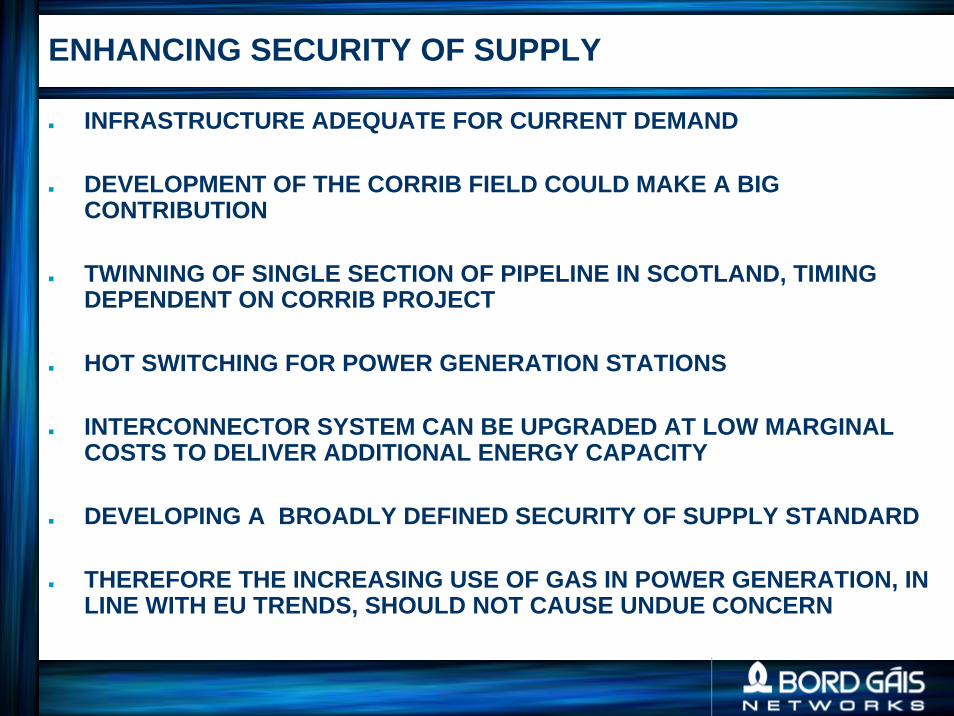

ENHANCING SECURITY OF SUPPLY

INFRASTRUCTURE ADEQUATE FOR CURRENT DEMAND

DEVELOPMENT OF THE CORRIB FIELD COULD MAKE A BIG CONTRIBUTION

TWINNING OF SINGLE SECTION OF PIPELINE IN SCOTLAND, TIMING DEPENDENT ON CORRIB PROJECT

HOT SWITCHING FOR POWER GENERATION STATIONS

INTERCONNECTOR SYSTEM CAN BE UPGRADED AT LOW MARGINAL COSTS TO DELIVER ADDITIONAL ENERGY CAPACITY

DEVELOPING A BROADLY DEFINED SECURITY OF SUPPLY STANDARD

THEREFORE THE INCREASING USE OF GAS IN POWER GENERATION, IN LINE WITH EU TRENDS, SHOULD NOT CAUSE UNDUE CONCERN

GAS PRICING

The final price of gas is made up of a transportation charge plus commodity …

0

5

10

15

20

25

30

35

00/01 2001/2 2002/3 2003/4 2004/5 2005/6

€ / M

Wh

Transportation Gas Forward Gas

14% 20% 22% 19% 13% 10%

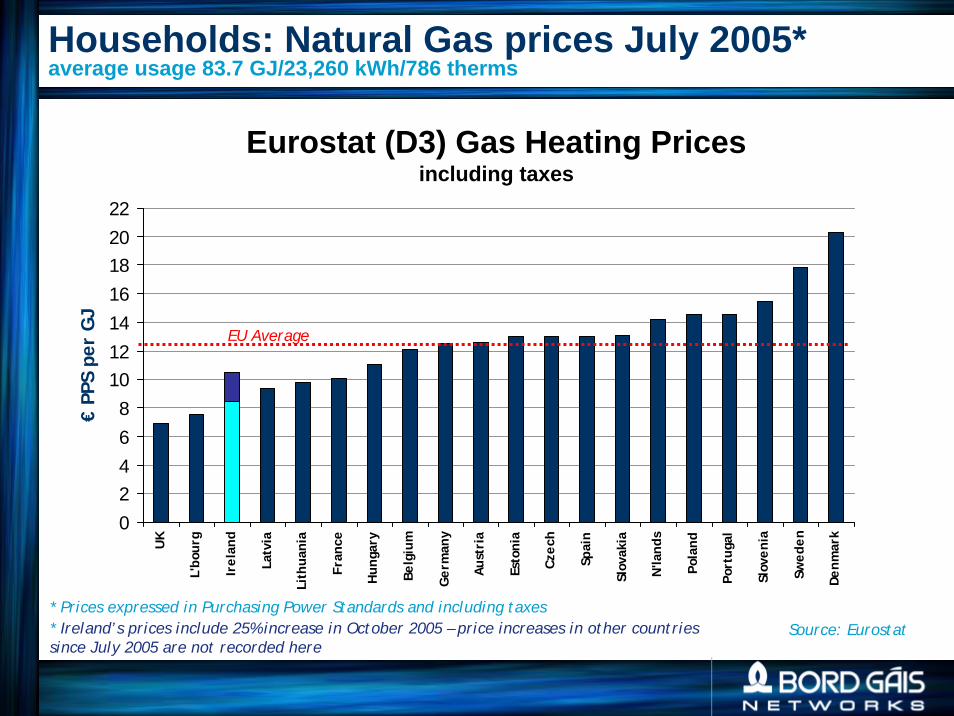

Households: Natural Gas prices July 2005*average usage 83.7 GJ/23,260 kWh/786 therms

* Prices expressed in Purchasing Power Standards and including taxes* Ireland’s prices include 25% increase in October 2005 – price increases in other countries since July 2005 are not recorded here

Source: Eurostat

02468

10121416182022

UK

L'bo

urg

Irel

and

Latv

ia

Lith

uani

a

Fran

ce

Hun

gary

Belg

ium

Ger

man

y

Aust

ria

Esto

nia

Czec

h

Spai

n

Slov

akia

N'la

nds

Pola

nd

Port

ugal

Slov

enia

Swed

en

Denm

ark

€ PP

S pe

r G

J

EU Average

Eurostat (D3) Gas Heating Pricesincluding taxes

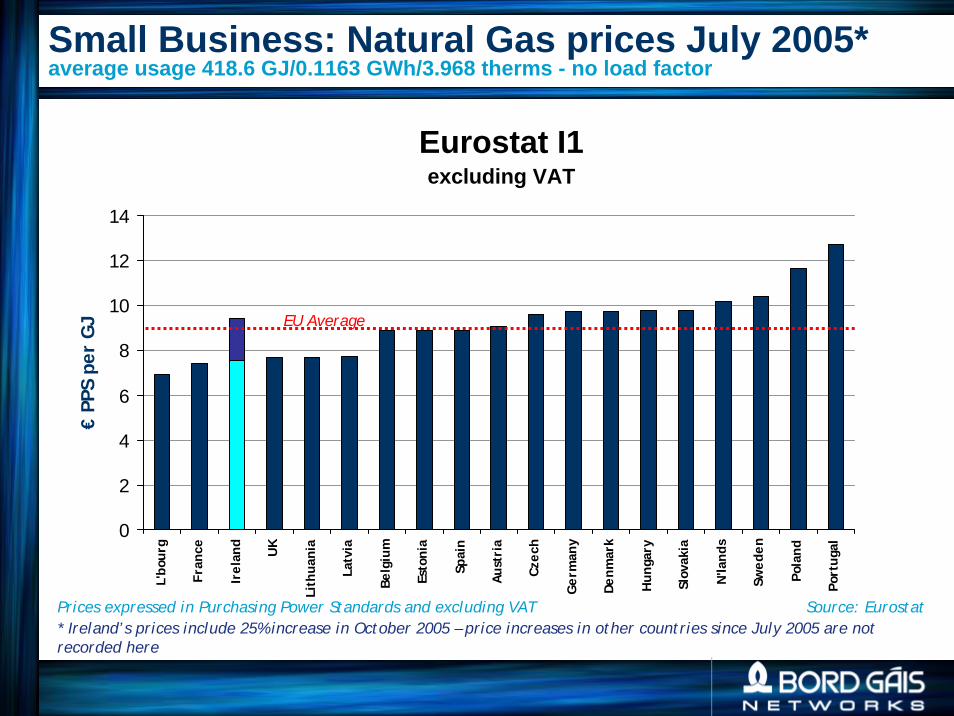

Small Business: Natural Gas prices July 2005*average usage 418.6 GJ/0.1163 GWh/3.968 therms - no load factor

Source: Eurostat

Eurostat I1excluding VAT

0

2

4

6

8

10

12

14

L'bo

urg

Fran

ce

Irel

and

UK

Lith

uani

a

Latv

ia

Belg

ium

Esto

nia

Spai

n

Aust

ria

Czec

h

Ger

man

y

Denm

ark

Hun

gary

Slov

akia

N'la

nds

Swed

en

Pola

nd

Port

ugal

€ PP

S pe

r G

J EU Average

Prices expressed in Purchasing Power Standards and excluding VAT* Ireland’s prices include 25% increase in October 2005 – price increases in other countries since July 2005 are not recorded here

Medium Business: Natural Gas prices July 2005*average usage 4,186 GJ/1.163 GWh/39,679 therms - 200 days modulation

Source: Eurostat

0

2

4

6

8

10

12

14

Spai

n

Esto

nia

Irel

and

Fran

ce

L'bo

urg

Belg

ium UK

Latv

ia

Lith

uani

a

Aust

ria

Denm

ark

N'la

nds

Slov

akia

Ger

man

y

Czec

h

Hun

gary

Port

ugal

Pola

nd

€ PP

S pe

r G

J

EU Average

Eurostat I2excluding tax

Prices expressed in Purchasing Power Standards and excluding VAT* Ireland’s prices include 25% increase in October 2005 – price increases in other countries since July 2005 are not recorded here

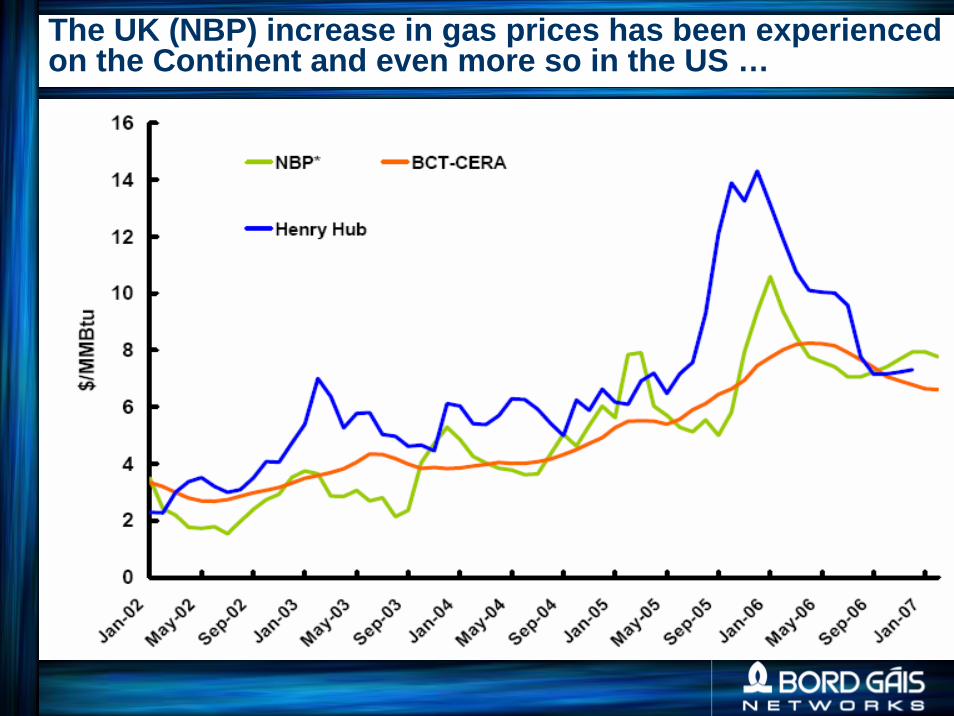

The UK (NBP) increase in gas prices has been experienced on the Continent and even more so in the US …

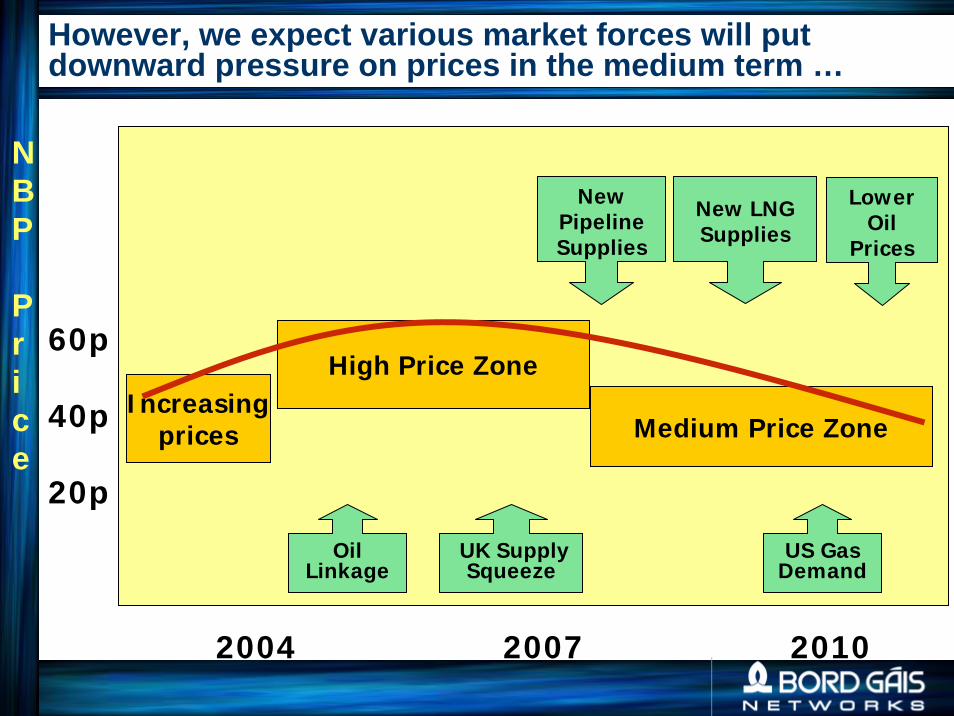

However, we expect various market forces will put downward pressure on prices in the medium term …

2004 2007 2010

60p

40p

20p

Increasingprices Medium Price Zone

OilLinkage

UK SupplySqueeze

US GasDemand

High Price Zone

NBP

Price

NewPipelineSupplies

New LNGSupplies

LowerOil

Prices

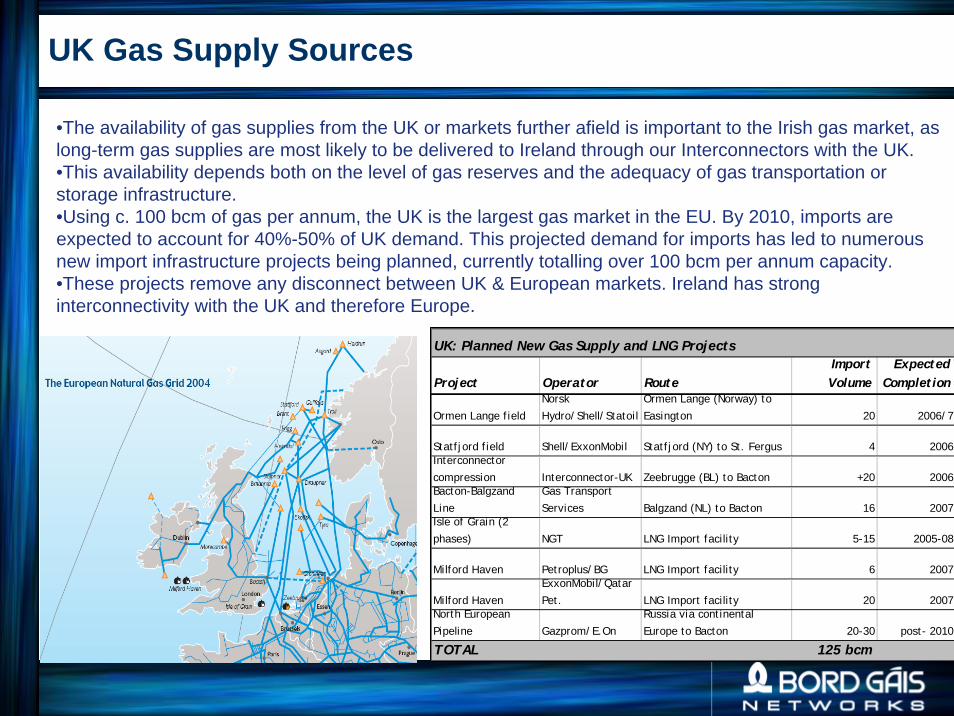

UK Gas Supply Sources

•The availability of gas supplies from the UK or markets further afield is important to the Irish gas market, as long-term gas supplies are most likely to be delivered to Ireland through our Interconnectors with the UK. •This availability depends both on the level of gas reserves and the adequacy of gas transportation or storage infrastructure.•Using c. 100 bcm of gas per annum, the UK is the largest gas market in the EU. By 2010, imports are expected to account for 40%-50% of UK demand. This projected demand for imports has led to numerous new import infrastructure projects being planned, currently totalling over 100 bcm per annum capacity.•These projects remove any disconnect between UK & European markets. Ireland has strong interconnectivity with the UK and therefore Europe.

UK: Planned New Gas Supply and LNG Projects

Project Operator Route Import Volume

Expected Completion

Ormen Lange field

Norsk

Hydro/Shell/Statoil

Ormen Lange (Norway) to

Easington 20 2006/7

Statfjord field Shell/ExxonMobil Statfjord (NY) to St. Fergus 4 2006Interconnector

compression Interconnector-UK Zeebrugge (BL) to Bacton +20 2006Bacton-Balgzand

Line

Gas Transport

Services Balgzand (NL) to Bacton 16 2007Isle of Grain (2

phases) NGT LNG Import facility 5-15 2005-08

Milford Haven Petroplus/BG LNG Import facility 6 2007

Milford Haven

ExxonMobil/Qatar

Pet. LNG Import facility 20 2007North European

Pipeline Gazprom/E.On

Russia via continental

Europe to Bacton 20-30 post- 2010

TOTAL 125 bcm

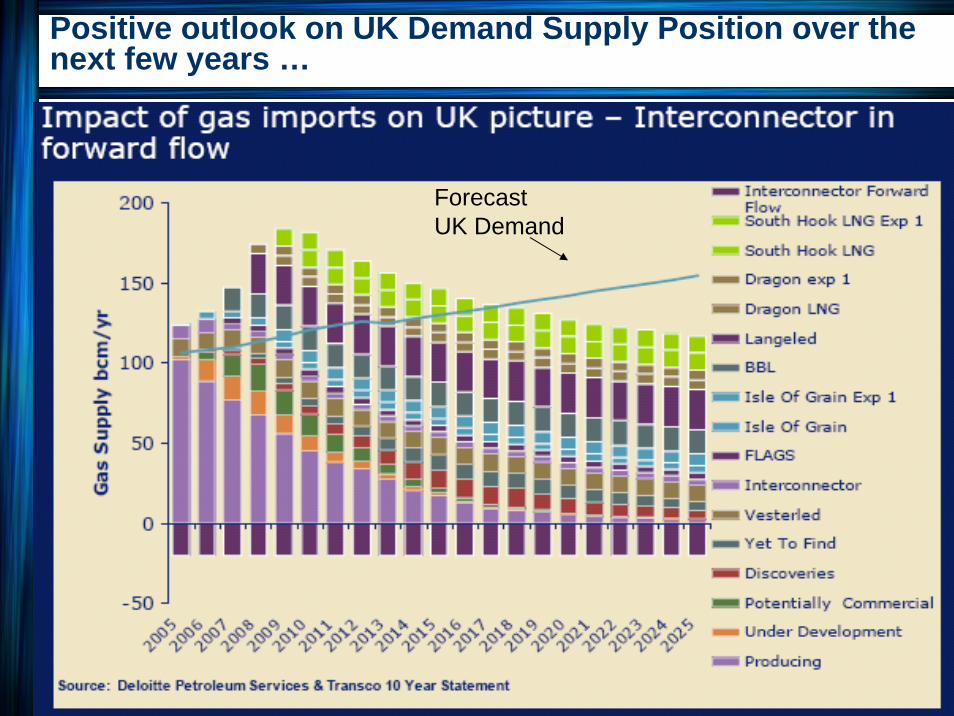

Positive outlook on UK Demand Supply Position over the next few years …

Forecast UK Demand

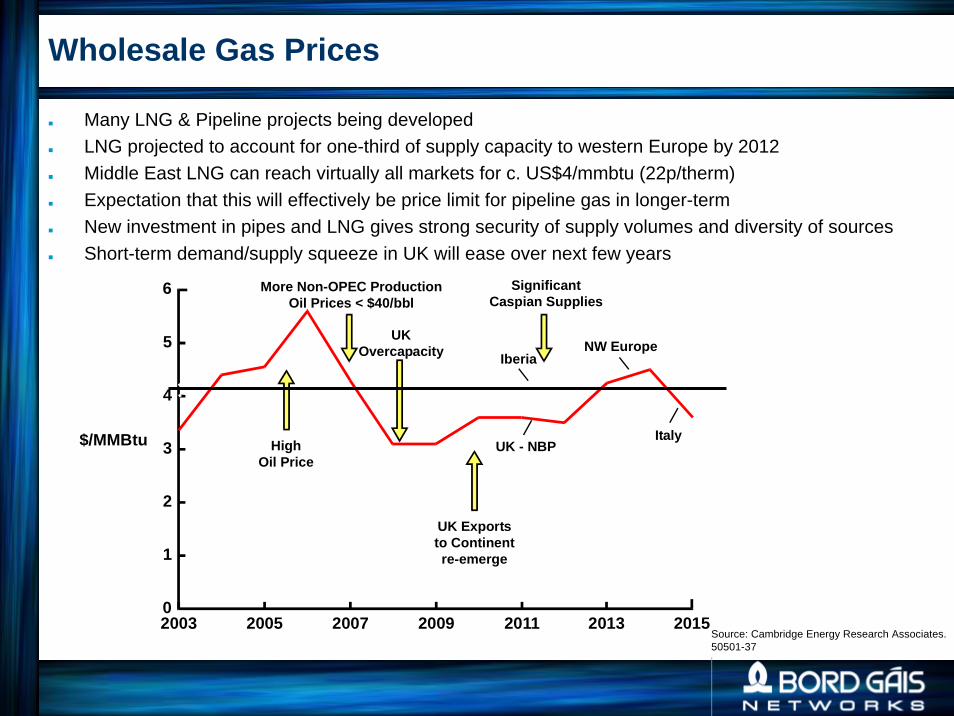

Wholesale Gas Prices

Many LNG & Pipeline projects being developedLNG projected to account for one-third of supply capacity to western Europe by 2012Middle East LNG can reach virtually all markets for c. US$4/mmbtu (22p/therm)Expectation that this will effectively be price limit for pipeline gas in longer-termNew investment in pipes and LNG gives strong security of supply volumes and diversity of sourcesShort-term demand/supply squeeze in UK will ease over next few years

6

$/MMBtu

2013 20150

5

4

3

2

1

ItalyUK - NBP

NW EuropeIberia

HighOil Price

UK Exportsto Continentre-emerge

UKOvercapacity

More Non-OPEC ProductionOil Prices < $40/bbl

20112009200720052003

SignificantCaspian Supplies

Source: Cambridge Energy Research Associates.50501-37

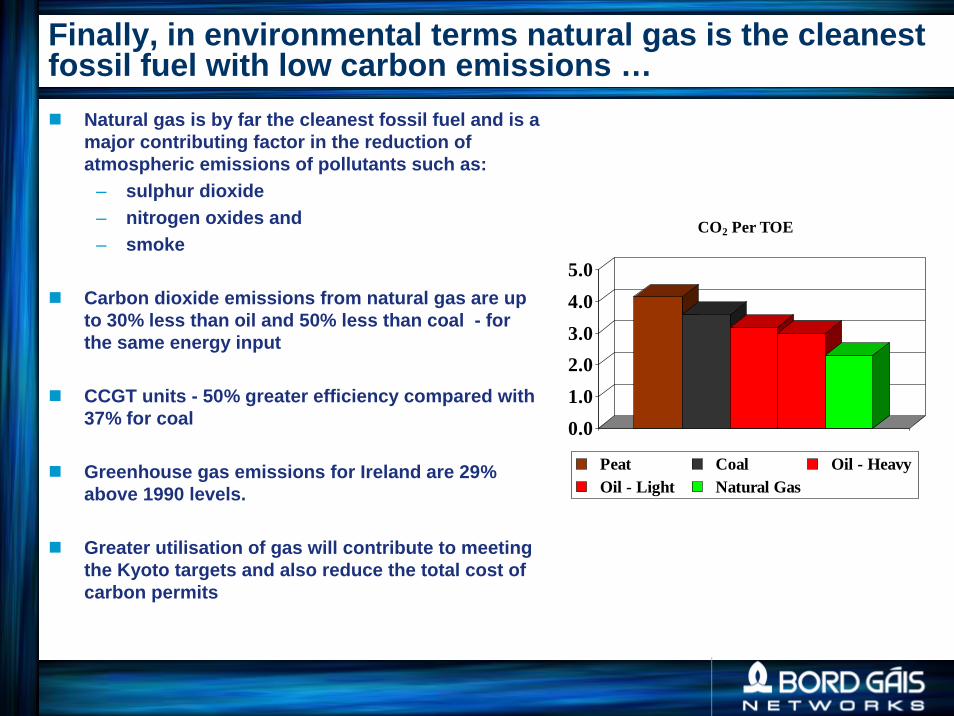

Finally, in environmental terms natural gas is the cleanest fossil fuel with low carbon emissions …

Natural gas is by far the cleanest fossil fuel and is a major contributing factor in the reduction of atmospheric emissions of pollutants such as:

– sulphur dioxide– nitrogen oxides and – smoke

Carbon dioxide emissions from natural gas are up to 30% less than oil and 50% less than coal - for the same energy input

CCGT units - 50% greater efficiency compared with 37% for coal

Greenhouse gas emissions for Ireland are 29% above 1990 levels.

Greater utilisation of gas will contribute to meeting the Kyoto targets and also reduce the total cost of carbon permits

0.01.02.03.04.05.0

CO2 Per TOE

Peat Coal Oil - Heavy Oil - Light Natural Gas

GOING FORWARD

SECURITY OF SUPPLYEU has economic access to significant long term sourcesIreland has adequate gas infrastructureIreland’s gas dependence in line with EU averageCorrib can make a big contributionComplete twinning of pipeline in Scotland, timing to depend on CorribGenerators to retain back-up fuel stocks as per licencesJoint approach to gas and electricity security and emergency planning

PRICESRemaining high near termProspects for reductions in the medium term due to developing pipeline and LNG infrastructure in the UK and wider EUGas prices will be a key influence on Irish and European power prices for the foreseeable future

ENVIRONMENTGreater gas utilisation contributes to energy efficiency and to the environment

Questions and Discussion