40

“Navigating The Future” Midlands Group Conference 8 th June 2016

“Navigating The Future” Midlands Group Conference

8th June 2016

Chairperson’s Introduction

Andy Greig

Chairperson

Hot Topic Panel Discussion Hosted by John Kempster, Trustee Solutions

Emma King, Eversheds Robin Ellison, Pinsent Masons LLP

Mike Roberts, PAN Governance

In or Out: A Dog’s Brexit for UK Pensions?

Pensions Management Institute

Birmingham 8 June 2016

5 squirepattonboggs.com

In or Out: A Dog’s Brexit for UK Pensions?

6 squirepattonboggs.com

In or Out: A Dog’s Brexit for UK Pensions?

Basic State Pension

IN – triple lock and OBR forecasts: ↑ £169 (2017/18)

OUT – shock / severe shock: ↓ £137 – 142 (2017 /18)

Annuities

ABI: 6m annuities, mainly non-indexed

Treasury: ↓ £50 – 190 (2017 /18)

DB pensions

Inflation

Non-pension assets (house prices / investments)

Shock (2017/18): £170 bn

Severe shock (2017/18): £300 bn

Treasury Report: 26 May 2016

7 squirepattonboggs.com

In or Out: A Dog’s Brexit for UK Pensions?

DC assets of today’s 50 year olds

Shock (2030): £450m (£223 pa)

Severe shock (2030): £700m (£335 pa)

The Out view

Iain Duncan Smith: “utterly outrageous” “cynical”

Matthew Elliot: “[economy] will become even stronger once we leave”

“[Treasury’s figures] literally made up”

Treasury Report: 26 May 2016 (continued)

8 squirepattonboggs.com

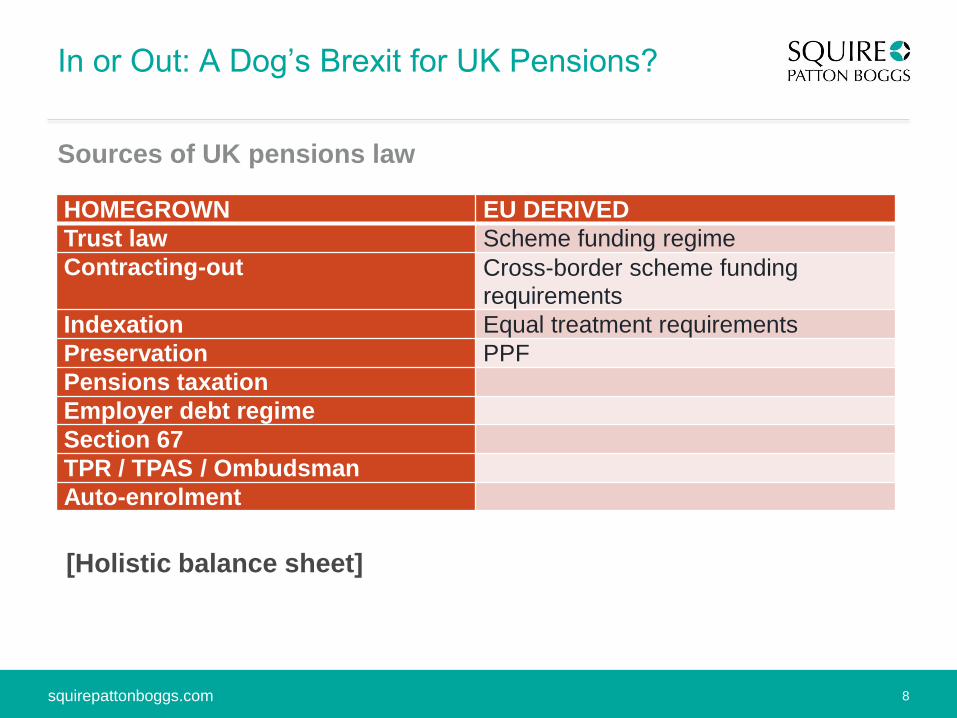

In or Out: A Dog’s Brexit for UK Pensions?

Sources of UK pensions law

HOMEGROWN EU DERIVED Trust law Scheme funding regime Contracting-out Cross-border scheme funding

requirements Indexation Equal treatment requirements Preservation PPF Pensions taxation Employer debt regime Section 67 TPR / TPAS / Ombudsman Auto-enrolment

[Holistic balance sheet]

9 squirepattonboggs.com

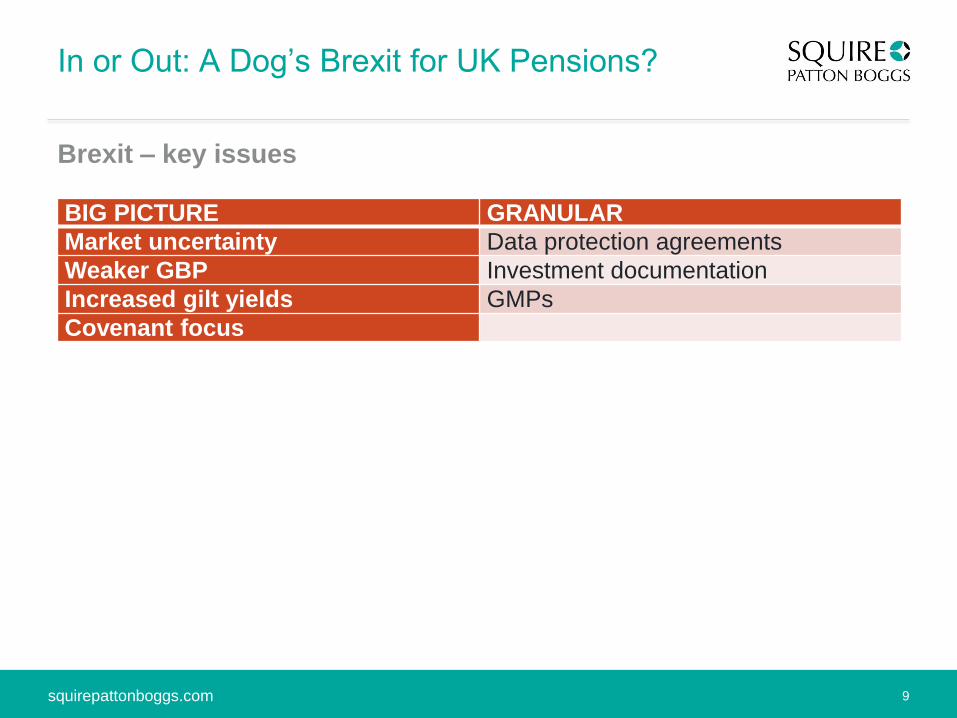

In or Out: A Dog’s Brexit for UK Pensions?

Brexit – key issues

BIG PICTURE GRANULAR Market uncertainty Data protection agreements Weaker GBP Investment documentation Increased gilt yields GMPs Covenant focus

10 squirepattonboggs.com

In or Out: A Dog’s Brexit for UK Pensions?

No change: AE, DC Governance / Charges, Public Sector

Unlikely: DB funding

Likely: Moral hazard / enforcement (tPR / PPF)

Insolvency Regulation: COMI, applicable law, mandatory recognition across EU

Recast Insolvency Regulation: greater focus on restructuring, not liquidation;

increased efficiency of cross-border insolvencies; public register

Brussels Regulation on Enforcement of Judgments

Regulatory impact

11 squirepattonboggs.com

In or Out: A Dog’s Brexit for UK Pensions?

QUESTIONS

12 squirepattonboggs.com

Abu Dhabi

Beijing

Berlin

Birmingham

Böblingen

Bratislava

Brussels

Budapest

Cincinnati

Cleveland

Columbus

Dallas

Denver

Doha

Dubai

Frankfurt

Hong Kong

Houston

Kyiv

Leeds

London

Los Angeles

Madrid

Manchester

Miami

Moscow

Newark

New York

Northern Virginia

Palo Alto

Paris

Perth

Phoenix

Prague

Riyadh

San Francisco

Santo Domingo

Seoul

Shanghai

Singapore

Sydney

Tampa

Tokyo

Warsaw

Washington DC

West Palm Beach

Israel

Mexico

Panamá

Peru

Turkey

Venezuela

Global Coverage

Africa

Argentina

Brazil

Chile

Colombia

Cuba

India

Office locations

Regional desks and strategic alliances

Pensions Management Institute

PMI – Navigating The Future

Gareth Tancred Chief Executive

8th June 2016

Predictions about the year 2000

Predicting The Future

Freedom & choice

Auto enrolment

TPAS/MAS merger

Tax reform - LISA

Macro Changes

Accommodation

Processes & governance

Development

Growth

Changes at PMI

Relationships between company boards & trustees

PMI Career Development Survey

DPT consultation

Member Guidance qualification

Media

Societal Impact

How can we help people?

Systems of the future

All people are unique

How do we develop systems? Roboadvice

Dashboards

How do we protect against fraud, cybercrime, scams, etc?

PMI of the future

Relevant

Authoritative voice

Learning & education

Impact

UK - Actuarial Advisory Firm of the Year

UK - Pensions Advisor of the Year

23 June 2016

DB funding in a low

yield environment

Mark Da Silva, Partner – Barnett Waddingham LLP

24

Agenda

2016 valuations

scheme demographics

asset returns: 2013-2016

liability changes: 2013-2016

Impact on Recovery Plans (RPs)

longevity update

conclusions

Scheme GB: demographics Source: the purple book 2015

• 5,945 schemes (2014: 6,057)

• 11.0 members (2014: 11.1m)

• £1.30tr assets (2014: £1.14tr)

• £2.10tr buyout liabs (2014: £1.69tr)

25

Scheme GB: asset allocation

26

20%

20%

20%

20%

20% 23%

14%

13%

21%

29% Overseas equities

UK equities

DGF/Property/Other

Index-linked gilts

Gilts and corporate

bonds

Investment returns 2013-2016

27

Market volatility:

“Markets have been particularly volatile which may impact schemes’ reporting funding positions.

Schemes should focus on the longer-term view for risk/rewards.”

TPR key messages

Real forward gilt curves 2013-2016

28

Average duration

c. 18 years

“Lower for longer?”

Longer term

gilt yields

29

Investment returns:

“We expect schemes to set strategies based on lower than expected

investment returns from most asset classes.

Schemes which relied on gilt yield reversion at last valuation should consider

whether they need to implement any of the contingencies they have in place.

Trustees should review their assumptions with regard to yield reversion.”

TPR key messages

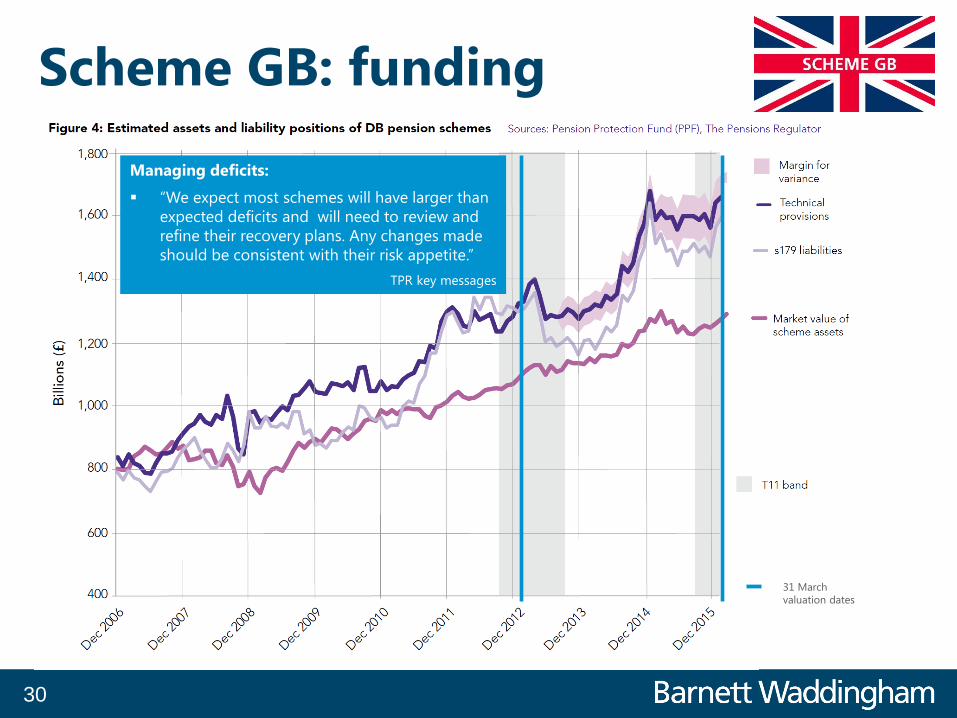

Scheme GB: funding

30

31 March

valuation dates

Managing deficits:

“We expect most schemes will have larger than

expected deficits and will need to review and

refine their recovery plans. Any changes made

should be consistent with their risk appetite.”

TPR key messages

Scheme GB: reconciliation Note: £bn figures below are approximate Barnett Waddingham estimates

31

£39bn

£324bn

375bn

£275bn

£63bn

£85bn

£115bn

Managing risk

32

Managing risk:

“Trustees need to be aware

of impending cashflow and

liquidity issues and start to

plan for them.

Trustees should use an IRM

framework to decide how

much and when to hedge

against risks, and be aware

of the implications of un-

hedged risks.”

TPR key messages

Longevity

33

CMI comment:

“At this stage it is difficult

to say whether mortality

improvements may

return to levels more in

line with prior years’

experience or whether we

are at the start of a

period of prolonged

lower improvements.”

|

|

Mortality assumptions:

“We would consider it reasonable for

trustees to update their mortality

assumptions to CMI2015 which will

produce lower life expectancies than the

2014 model.

However, they should consider what the

impact would be if this reduction was

reversed and, at present, there is very

little evidence that this is indicative of

changes to long-term trends.”

TPR key messages

Impact on Recovery Plan (RP)

34

Recovery Plans:

“From our analysis, many schemes

may have the capacity for the

employer to increase their

contributions without affecting their

plans for growth.

We expect trustees to seek higher

contributions where there is sufficient

affordability for the employer.

Where this is not the case, we expect

trustees and employers to discuss

this issue openly and also to consider

what alternative options exist.

Employers should ensure they treat

the pension scheme fairly.”

TPR key messages

Conclusions - “The art of the possible”

Funding

• RP options

• fixed vs flexible deficit-repair

contributions (DRCs)

• Memorandum of Understanding (MoU)

Covenant

• affordability of DRCs

• strength of technical provisions (TPs)

• solvency: improvements in security

• appropriate ongoing of monitoring

Investment

• Value-at-Risk (VaR) analysis

• self-sufficiency journey planning

35

TPR key conclusions:

“An Integrated Risk Management

(IRM) approach is key, along with a

clear assessment and understanding

of the employer covenant.

Assessing risk : trustees should

measure the risks impacting scheme

assets and liabilities and join this up

with the trustees’ views on the

employer covenant.

There is no need to eliminate all risk

but an IRM approach makes sure the

level of risk is appropriate for the

scheme and employer.

Open and collaborative working

between trustees, employers and

advisers is vital as all parties need to

be comfortable with the level of risk

the scheme is exposed to and any

mitigation measures put in place.”

TPR key messages

Questions

36

Regulatory Information • The information in this presentation is based on our understanding of

current taxation law, proposed legislation and HM Revenue & Customs practice, which may be subject to future variation.

• This presentation is not intended to provide and must not be construed as regulated investment advice. Returns are not guaranteed and the value of investments may go down as well as up.

• Barnett Waddingham LLP is a limited liability partnership registered in England and Wales.

• Registered Number OC307678.

• Registered Office: Cheapside House, 138 Cheapside, London, EC2V 6BW

• Barnett Waddingham LLP is authorised and regulated by the Financial Conduct Authority and is licensed by the Institute and Faculty of Actuaries for a range of investment business activities.

37

Investments: Navigating a Diverging World

Glyn Owen

Momentum Global Investment Management

Thank you for attending the PMI Midlands Conference entitled “Navigating The Future”

Your views are very important to us and will help us in planning any future events we hold.

You will shortly be receiving an email with a link to a brief survey and we would be very

grateful if you could take a few moments to complete it.

A copy of today’s slides will be available on the PMI Midlands section of The Pensions

Management Institute website.

Thank you

Andy Greig

Chairperson – PMI Midlands