Navigating the SBA 7(a) Loan Closing to Protect your Guaranty A Guided Tour through the Due Diligence Process, SBA Loan Documentation and Potential Pitfalls Presented by Kerry M. Southerland, Shareholder

Transcript

Navigating the SBA 7(a)Loan Closing to Protect your Guaranty

A Guided Tour through the Due Diligence Process, SBA Loan Documentation and Potential Pitfalls

Presented by Kerry M. Southerland, Shareholder

Reasonable and Prudent Lending Practices

• SBA lenders must analyze each application in acommercially reasonable manner, consistent withprudent lending standards.

• Service and liquidate SBA portfolio just like yourconventional loans.

• Understand your internal loan requirements and those ofSBA to avoid potential servicing problems orrepairs/denials should the loan default.

• Be proactive vs. reactive.

Loan Authorization: Your Roadmap

• The lender sets the terms andconditions for extending creditto the borrower.

• SBA establishes the terms andconditions for its loanguaranty (SBA Form 750 and750B).

• The Authorization is SBA'swritten agreement betweenthe SBA and the lenderproviding the terms andconditions under which SBAwill guarantee the commercialloan.

National 7(a) Authorization Boilerplate

SBA establishes the mandatory wording for allstandard 7(a), CLP and PLP conditions in theBoilerplate.

• SOP controls – references to regulations and SOPprovisions therein.

• Export Working Capital Program

• CAPLines

• SBA Express and Export

Express (Boilerplate or abbreviated version

allowed)

The Wizard

Technical tool to help you create the Authorization based on the Boilerplate.

• The party responsible for drafting the Authorization isdetermined by the program under which the loan isprocessed:

– Standard 7(a), non-PLP 7(a) Small Loans and CAPLines –SBA drafts and signs.

– Standard EWCP – SBA drafts and signs.

– CLP Lender drafts, SBA finalizes/approves and signs.

– PLP Loans – Lender drafts and signs on SBA’s behalf.

Modifications to the Authorization

• For 7(a), CLP, 7(a) Small Loan (non-PLP) and CAPLines (non-PLP), Lender may request modifications to the terms and conditions of the Authorization at any time after approval.

• All modification requests through final disbursement must be approved by the LGPC.

• For PLP Loans, Lender isresponsible for modifying theauthorization under its delegatedauthority and must document itsfile with a written explanationthat includes justification for thechange and any supportingdocumentation.

• Make certain your approval andauthorization MATCH.

• Confirm credit analysis iscomplete per SOP requirements.

Unilateral Action Matrix

•The two servicing centers, NGPC, and HQwork together to keep the Unilateral ActionMatrix current.

•It is designed to assist lenders inunderstanding if actions require SBAapproval, SBA notification, or are unilateral.

•As long as the actions you take aredocumented, prudent, are within yourunilateral authority, and don’t cause harm tothe Agency, the Center will generally not beconcerned with them at the time ofpurchase.

•Important to document your file withdetails and justification for unilateral activity.

Follow the Roadmap

• Identify Obligors – EPC/OC? Guarantors?

• Collateral Requirements?

• Insurance Requirements?

• Cash Injection?

• Franchise?

• Standby Notes?

• Occupancy Requirements?

Circulate a Closing Checklist

• Determine which items are necessary forclosing.

• Determine which items you have vs. whichitems can be collected from Borrower, titlecompany, seller, etc.

• Address any issue that could impair repaymentability or constitute an adverse change.

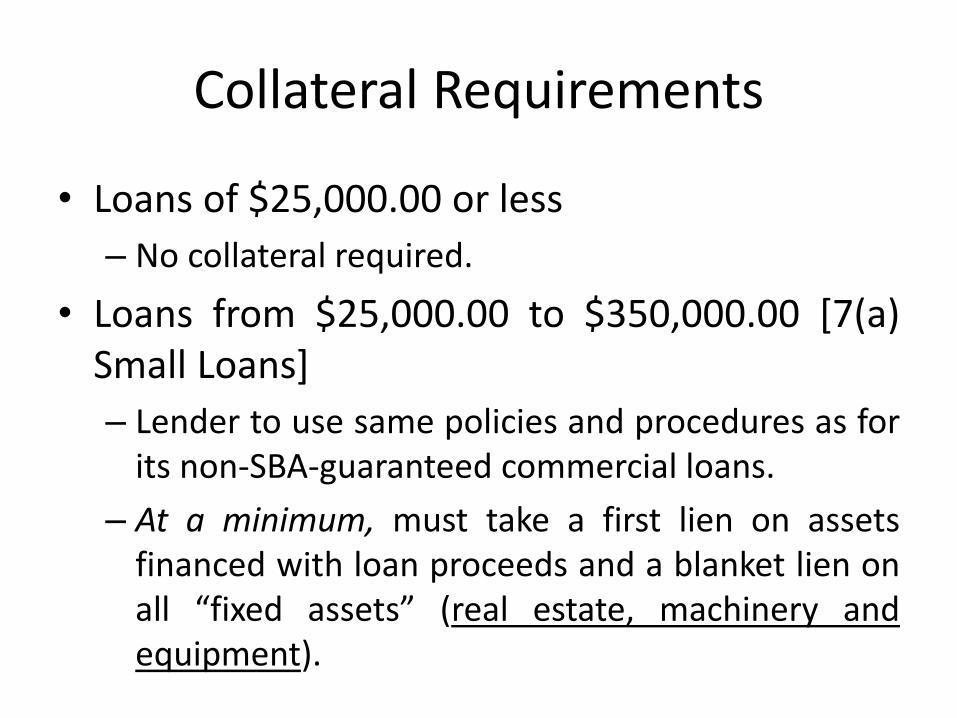

Collateral Requirements

• Loans of $25,000.00 or less

– No collateral required.

• Loans from $25,000.00 to $350,000.00 [7(a)Small Loans]

– Lender to use same policies and procedures as forits non-SBA-guaranteed commercial loans.

– At a minimum, must take a first lien on assetsfinanced with loan proceeds and a blanket lien onall “fixed assets” (real estate, machinery andequipment).

Collateral Requirements

• Loans over $350,000.00

– Lender must collateralize the loan “to themaximum extent possible up to the loan amount”.

– SBA considers a loan as “fully secured” if thelender has taken security interests in all availablefixed assets with a combined “Net Book Value” asadjusted up to the loan amount.

– “Net Book Value” is defined as an asset’s originalprice minus depreciation and amortization.

Collateral Requirements

• For collateral purposes, adjusted Net Book Value isdetermined as follows:

– New machinery and equipment may be valued at75% of Net Book Value or 80% with an OrderlyLiquidation Appraisal minus any prior liens;

– Used or existing machinery and equipment may bevalued at 50% of Net Book Value or 80% with anOrderly Liquidation Appraisal, minus any prior liens;and

– Improved real estate may be valued at 85% of theappraised value and unimproved at 50% ofappraised value.

Collateral Requirements

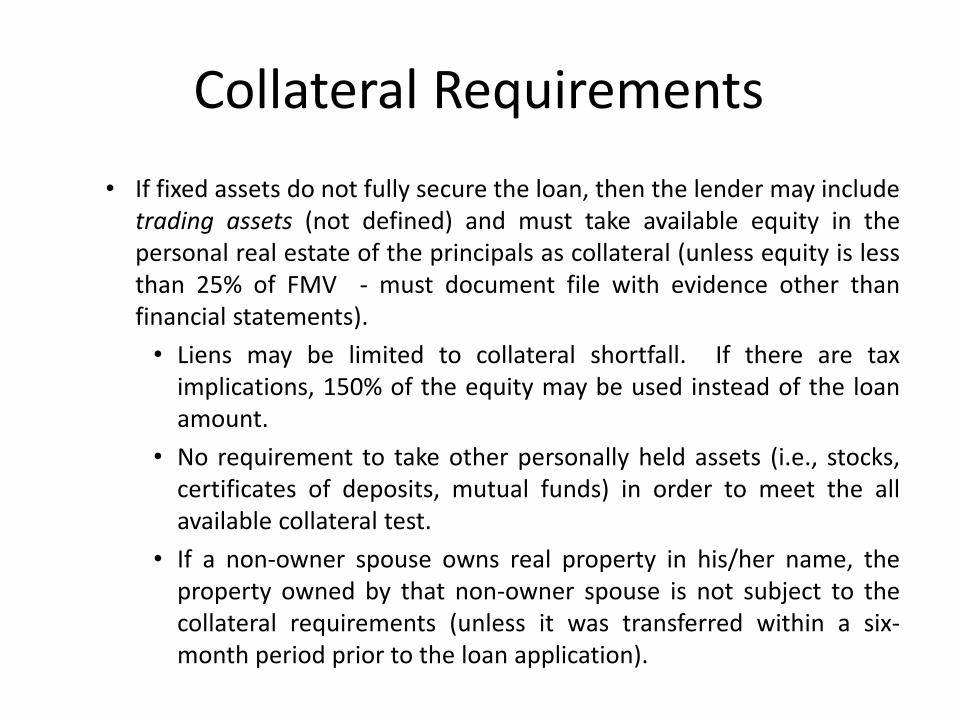

• If fixed assets do not fully secure the loan, then the lender may includetrading assets (not defined) and must take available equity in thepersonal real estate of the principals as collateral (unless equity is lessthan 25% of FMV - must document file with evidence other thanfinancial statements).

• Liens may be limited to collateral shortfall. If there are taximplications, 150% of the equity may be used instead of the loanamount.

• No requirement to take other personally held assets (i.e., stocks,certificates of deposits, mutual funds) in order to meet the allavailable collateral test.

• If a non-owner spouse owns real property in his/her name, theproperty owned by that non-owner spouse is not subject to thecollateral requirements (unless it was transferred within a six-month period prior to the loan application).

Real Property Collateral

• Obtain required lien position.

– Confirm release and/or subordination of any

prior liens.

• Obtain a survey acceptable to the title company to remove surveyexceptions and obtain T-19 endorsement .

• Review title commitment and approve Schedule B exceptions.

• Review restrictive covenants (e.g. use restrictions) affecting the property.Focus on limitations that could potentially decrease value!

• Obtain necessary endorsements to protect Lender and SBA.

• Ensure all taxes are paid current.

• Ensure assessment liens (payable to POA) are subordinated.

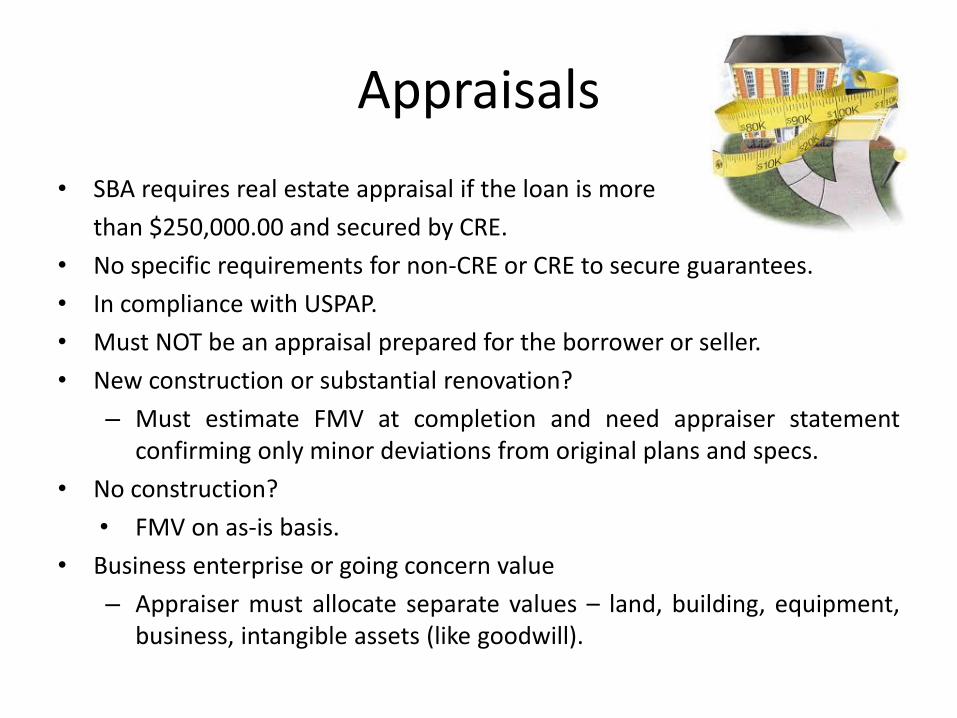

Appraisals

• SBA requires real estate appraisal if the loan is more

than $250,000.00 and secured by CRE.

• No specific requirements for non-CRE or CRE to secure guarantees.

• In compliance with USPAP.

• Must NOT be an appraisal prepared for the borrower or seller.

• New construction or substantial renovation?

– Must estimate FMV at completion and need appraiser statementconfirming only minor deviations from original plans and specs.

• No construction?

• FMV on as-is basis.

• Business enterprise or going concern value

– Appraiser must allocate separate values – land, building, equipment,business, intangible assets (like goodwill).

Flood Certifications

• Purchase if required by National Flood Insurance Program(NFIP).

• Based on Standard Flood Hazard Determination (FEMA Form)

• If any real property is in a flood zone, Lender must requireflood insurance for real property AND personal propertycollateral located within the flood zone.

• If any personal property is in a building that is NOT collateralin a flood zone, Lender can waive.

– Paper your file to justify your decision.

– Based on prudent lending standards.

Environmental Issues

• SBA requires environmental investigation for all CRE collateral.

• Type and depth depends on loan amount and risks of contamination.

• Starts with Environmental Questionnaire and Records Search with Risk Assessmentor Transaction Screen to Phase II ESA

– Goal is to determine risk of contamination, submit to SBA for concurrence thatno further investigation is warranted.

– If further investigation is warranted:

• Phase I ESA

• Phase II ESA

• Proceed as Recommended by EP

• Submit to SBA for recommendations and concurrence.

– Contamination revealed? EP must document the file re: remediation, estimateof costs and schedule to complete remediation.

– May disburse loan once risks are sufficiently minimized and no further actionis required.

Personal Property Collateral

• Itemized list of all equipment

– Serial numbers for any item valued at or over$5,000.00

• Invoices and/or purchase orders for equipment/inventoryto be purchased with loan proceeds

• CD to be assigned

• Certificates of Title for vehicles

• Stock Certificates

• Evidence of brokerage account – uncertificated securities

• USPTO search – patents, trademarks, IP

UCC-1 Financing Statements

• Properly file to be effective.

• Identify the debtor.

• Identify the proper location of debtor.

• Attach any exhibits/addendums.

• Pay the filing fees.

UCC-1’s: Debtor’s Name

• Identify the debtor – based on currently filedpublic organic record.

– Articles of Incorporation/Certificate of Formation

– Drivers’ License or State-Issued I.D. Card

– Avoid trade names or dba’s.

UCC-1’s: Debtor’s Location

• Identify the proper location and file in the correct central filing records.

– Registered business = state of organization.

– Individuals = state of principal residence.

UCC-1’s: Pre- and Post-Filing

• Practice of Pre-Filing

– Encouraged.

– Prevent intervening liens.

• Conduct Post-Filing Search

– Confirm lien priority and compliance withcollateral conditions.

– Required for purchase requests.

• File Continuations Statements

– UCC-1 lapses 5 years from filing date.

Change of Ownership

• Stock Purchase

– Includes stock redemption.

• Asset Purchase

– If Borrower is purchasing all or substantially all of seller’sassets or is otherwise continuing seller’s business.

Change of Ownership: Between Existing Owners

• Existing owner purchases interests of otherowners resulting in 100% ownership bypurchasing owner.

– Small Business and purchasing owner must be co-borrowers.

• Small Business redeems ownership of anowner resulting in 100% ownership byremaining owners.

– Small Business must be borrower and remainingowners may be co-borrowers or guarantors.

Change of Ownership: Resulting in New Owner

• Small business purchases 100% interest of another smallbusiness

– Acquiring entity may be borrower or both small businessesmay be co-borrowers.

• Non-owner purchases 100% interest of a small business

– New individual owner and small business must be co-borrowers.

• A small business is acquiring 100% interest in another smallbusiness through an asset purchase

– Acquiring entity may be borrower or both small businessesmay be co-borrowers.

Change of Ownership/Business Acquisitions

• Seller cannot remain as an officer, director, stockholder or keyemployee except as a consultant for 12-month transitionalperiod.

• Lender’s file must contain the following:

– Current Business Valuation (excluding real estate)

– Site Visit

– Real Estate Appraisal

– Analysis confirming promotion of sound developmentand/or preservation of existence of business.

Purchase of Existing Business

• Purchase and Sale Agreement

– Non-Compete Agreement

– Non-Solicitation Agreement

• “Purchase Price” includes all assets being acquired.

• Licenses and Permits

• Seller Note – confirm standby terms – seller debtmust be on full standby for full loan term to count asequity injection.

Insurance Requirements

• Hazard Insurance

• Flood Insurance

• Life Insurance

• General Liability

• Dram Shop/Liquor Liability

• Malpractice

• Disability

• Worker’s Compensation

Hazard Insurance

• Must insure ALL real and personal property collateral.

• Coverage must be in the amount of the full replacement cost.– If unavailable, obtain for maximum insurable value.

– Must contain mortgagee clause or lender’s loss payable clause (or substantial equivalent) in favor of lender.

– Policy must provide for at least 10 days prior written notice to lender of policy cancellation.

Life Insurance

• For standard 7(a) loans over $350,000.00, lenderscan follow their internal policy except

• If loan is not fully-secured, life insurance is required forprincipals of sole props, single member LLC’s or businessesotherwise dependent on owner’s active participation.

• Delays are standard – start the process early.

• Obtain a copy of the actual policy and acknowledgedassignment from the insurance company.

– Confirm whether insurance company has required form.

IRS Tax Transcripts

• Before submission of application or first disbursement, Lendermust submit IRS Form 4506-T to the IRS.

• Confirm applicant filed tax returns and confirm financialstatements submitted with application agree.

– Obtain tax information on the borrower and/or OC for thelast 3 years.

– Exception for startup businesses

IRS Tax Transcripts

• Borrower must resolve any discrepancies tolender’s satisfaction – similar to “no adversechange” determination.

• If PLP lender does not receive a response ortax transcript within 10 business days ofsubmission, lender can proceed to close anddisburse.

• Be sure to follow up and resolve discrepanciespost-closing.

Standby Debt and Agreements

• SBA Form 155 or Equivalent

• Don’t forget to attach the note.

• Must subordinate all lien rights in collateral.

• Take no action against borrower without Lender’s consent.

• Standby debt counts as equity only if on full standby for the term of the loan.

Leases

• When loan proceeds are to be used for leaseholdimprovements or collateral consists of leaseholdimprovements and/or fixtures, lender shouldobtain (for all locations where all personalproperty collateral is located):

• Assignment of lease w/ term including renewal optionsthat equals or exceeds loan term;

• Requirement that lessor provide 60-day written noticeof default to lender with option to cure; and

Landlord’s Waiver

• Subordinates the landlord’s interest.

• Provides written notice of default with reasonable opportunity to cure.

• Allows the right to take possession and dispose/remove collateral.

EPC/OC Structure

• Eligible Passive Company (EPC) must lease 100% of the property to Operating Company (OC)

• Make sure no loan proceeds are used to finance improvements occupied by 3rd party tenants.

• Ensure you obtain Subordination and Non-Disturbance Agreements (SNDA’s) from all tenants.

– Subordination: Tenant agrees to allow its interest to be junior to lender; gives the lender the option to terminate the lease after foreclosure.

– Non-Disturbance: Allows tenant to continue to occupy leased premises after foreclosure so long as there’s no default.

– Attornment: Tenant recognizes lender as new landlord.

Leasehold Estates

If loan proceeds will finance existing or new improvements on a leaseholdinterest, the ground lease must include the following:

– Consent to Encumbrance - tenant’s right to encumber leaseholdestate

– No modification or cancellation of lease without lender’s approval

– Lender’s rights to

o Acquire the leasehold at foreclosure

o Sublease

o Hazard insurance proceeds resulting from damage toimprovements

o Share in condemnation proceeds

– Clarify lender’s rights upon default of tenant or termination.

o 60-day written notice of default from lessor

Construction

• For new construction or addition to existing building:

– soils report

– building permit

– evidence of availability of utilities – on or brought to property

– zoning letter

– budget and schedule

– AIA Qualification statement (only if required by Lender)

– Architect/Engineer’s Letter regarding compliance with laws (Texas Accessibility Standards and ADA)

Evidence of compliance with National Earthquake Hazards Reduction Program (NEHRP)

• Earthquake Certification - certificate from architect,engineer or similar professional or letter from state orlocal government agency

– Line up someone early.

– Required for any permanent leasehold improvements

– Can request modification from Authorization if only

temporary leasehold improvements.

Construction: Loans over $350,000.00

• Survey – locate easements and prevent surprises!

• Completed SBA Form 601 Agreement of Compliance

• Need this at a minimum for construction costs over $10,000.00.

• Evidence that contractor has furnished 100% payment andperformance bond

• Filed of record with contract attached

• Unless engage a 3rd party construction management service thatcontrols disbursement of proceeds and monitors project

• Builder’s risk and worker’s comp insurance

• Satisfied equity injection – if borrower injecting funds into theproject

• Plans and specs

Construction: Loans over $350,000.00

• Construction contract in approved amount

• Statutory Retainage

– Texas requires owner to retain 10% of contract priceuntil 30 days after completion of work

– Section 53.101 of Texas Property Code

– 10% deducted from each draw

• Borrower’s Agreement re: no material changes withoutlender’s consent

• Evidence of borrower’s ability to pay cost overruns

• Lender to make interim and final inspections

Post Construction: Loans over $350,000.00

• Obtain lien waivers and/or releases from all contractorsand subs

– Final lien waiver from GC required to releaseretainage

• Document that construction completed in conformancewith plans and specs

• Certificate of Occupancy

• Evidencing that all zoning, applicable licensing andpermit requirements met

Post Construction: Loans over $350,000.00

• Affidavit of Completion

– Filed in real property records

– Certifies that all material men, contractors andsubcontractors have been paid.

• As-Built Survey (ground up)

– If required by lender.

• Recertification of Appraisal

– If required by lender.

• Make copies of all draw requests and other evidence ofproject costs.

Do-It Yourself Construction

• Generally proven to be “unsatisfactory” per SOP.

• Borrower is its own contractor

• Allowed if borrower/contractor is experienced in the type ofconstruction and licensed.

• Borrower will not earn a profit

• Cost is the same as, or less than, what an unaffiliatedcontractor would charge

– Based on 2 bids on the work

Franchises

• Question of Eligibility: affiliation and control

• Ineligible if imposes unacceptable control resulting inaffiliation.

• Affiliation can exist through common ownership, management, excessive restrictions, control by franchisor preventing profits/loss as part of standard ownership

• Includes jobber, dealer and similar agreements.

• SBA adopts the Federal Trade Commission’s (FTC) definition of “franchise.”

Franchise Directory

• SBA has taken out the guesswork and lenders can rely on the Franchise Directory (the “Directory”): https://www.sba.gov/document/support-sba-franchise-directory

• If the applicant’s brand meets the FTC’s definition of “Franchise”, it must be in the Directory.

• If not on the Directory, Lenders can apply for the same to be added after SBA makes an affiliation/eligibility determination.

• Check the Directory for the Franchise Identifier Code and to determine whether the SBA Addendum or SBA Negotiated Addendum is required prior to submission.

• Start-Up Businesses – minimum of 10% of total project cost.

• Change of Ownership (between existing owners or “partnerbuyout”) – minimum of 10% of the purchase price (per thePSA) of the business IF the following cannot be documented:– Existing owners have been active participants of the borrower and have

maintained same ownership for past 24 months.

– Borrower’s business balance sheets for previous year and current quarterreflect debt-to-worth ratio of no greater than 9:1 prior to the change ofownership.

• Complete Change of Ownership (resulting in a new owner) –minimum of 10% of total project cost.– Seller Debt can only count if on full standby for the full loan term and does not

exceed half of the required total injection.

Equity Injection - Sources

• Cash that is not borrowed.

• Cash from a personal loan to a borrower’sowner that does not come from borrower oraffect cashflow.

• Assets other than cash – Lender must“carefully evaluate” this option and documentyour file.

• Standby debt on full standby for the full loanterm.

Verification of Equity Injection

▪ Lenders can verify the injection with:

▪ Credit card receipts indicating items purchased for the business.

▪ Paid invoices with vendor receipts or cancelled checks.

▪ Copies of processed checks payable to the business and business

bank statement showing the funds deposited.

▪ Borrower bank statement that shows beginning and ending

balances prior to loan disbursement, dated within 2 months of

disbursement.

▪ Settlement Sheet or closing agent’s settlement statement dated

and signed by borrower and closing agent.

▪ If a Standby Agreement was required as part of the injection, provide

the Agreement and any resulting Notes.

Equity Injection - Verification

• A promissory note, “gift letter” or financial statement is notsufficient evidence of cash injection without corroboratingevidence.

• If the equity injection will come from any form of borrowed funds,such as a HELOC or seller financing in excess of the minimumBorrower injection requirements outlined above, Lender mustaddress the proposed repayment terms as well as any Standby orSubordination terms that will be in place in its credit analysis.

• For SBA Express, Export Express, and 7(a) Small Loans, if a Lenderrequires an equity injection and, as part of its standard processesfor similarly-sized, non-SBA guaranteed loans verifies the equityinjection, it must do so for its SBA Express, Export Express, and 7(a)Small Loans.

BEWARE of Tab 7 – Early Default

•“Early Default” means any of the following events of default that occurred either:

•(a) within 18 months of the initial disbursement of the loan, or; •(b) within 18 months of the final disbursement of the loan if the final disbursement occurred more than 6 months after the initial disbursement

•Unless the Borrower cured the default and made the scheduled loan payments for 12 months following the 18 month period. (No longer consecutive.)

Tab 7 – Early Default Requirements: Equity Injection

• You must verify proper asset/equity injection, if required.

• The source requirements vary based on when the loan was

originated. SBA commonly sees issues with sourcing.

• Injection should occur prior to disbursement.

• If it occurs on or after disbursement the lender must clearly

show that the injection did not come from loan proceeds.

• Rebuttable presumption that early default is due to failure of

Lender to properly verify and/or source equity injection.

Tab 7 - Early Default Requirements:IRS Verification and Credit Memo

▪ IRS Income Tax Verification

▪ The lender must provide copies of the IRS tax transcripts and the financial

statements and/or other financial information that was compared to the tax

transcripts in the credit analysis during the loan origination process.

▪ If the business is a start-up, this is not required.

▪ If you don’t have evidence that IRS transcripts were verified against financial

statements, provide an explanation as to what was used to verify the income

of the borrower.

▪ Copy of the Lender’s Internal Credit Approval

▪ SBA reviews the credit memo and supporting documents to ensure that the

lender has acted prudently.

▪ Pay attention to the credit elsewhere requirements in the credit memo.

▪ Cash flow/repayment ability will be examined in the credit memo to ensure

that the risk involved in making the loan was fully considered.

▪ Again - confirm your credit memo matches the loan authorization.

Avoid Tab 7 and Early Defaults!

• Higher scrutiny level

• Consider forbearance agreements, if prudent, in an effort to work with the borrower to cure any defaults. (More on this topic in a few slides.)

And……..

• Guaranty Fee

• Payoffs

• Homestead issues and waivers

• Sales Contract/Purchase and Sale Agreement

• Warranty Deed/Bill of Sale

• Receipt and approval of financial statements within 90 days of closing

• State-specific requirements

What if the loan defaults?* *Don’t worry.

• Avoid certain issues with protective provisions in loan documents.

• Include Effective Waivers

– Uniform Commercial Code

• Provides general guidance during the collection process.

• Check which provisions of UCC have been adopted by subject state.

• Different states have different versions.

Forbearance Agreements

• A formalized way of recognizing that there is a problem in the financial relationship and attempting to solve it.

Clean up the loan documents.

Post-Default Review

• Important to conduct due

diligence to cure or clean up

loan documents and lien

perfection flaws.

• Opportunity to correct any

deficiencies in the existing

terms, documentation

or collateral.

Problems?

• If any problems exist that could warrant repair/denial, analyze the possibility of obtaining additional collateral and/or executing additional documents.

Shameless Plug

• Communication is key.

• Advise all parties of process, necessary paperwork/information and deadlines.

• Delegate and assign tasks.

• Set realistic expectations and engage counsel if you have questions or issues.