43

Navios Maritime Holdings Inc. 5th Annual Shipping, Logistics & Offshore Services Conference New York City September 16, 2008

Navios Maritime Holdings Inc.

5th Annual Shipping, Logistics & Offshore Services Conference

New York City

September 16, 2008

DisclosuresStatements in this presentation which are not statements of historical fact are “forward-looking statements” (as such term is defined in Section 21E of the Securities Exchange Act of 1934, as amended). These forward-looking statements are based on the information available to, and the expectations and assumptions deemed reasonable by, the Company at the time this presentation was made. Although the Company believes that the assumptions underlying such statements are reasonable, it can give no assurance that they will be attained. The Company undertakes no obligation to update any forward-looking statements, whether as a result of new information or future events, unless it is required to do so under the securities laws. The Company makes no prediction or statement about the performance of its common units.

For the selected financial data presented herein, Navios compiled consolidated statement of operations for the three-month and six month periods ended June 30, 2008 and June 30, 2007.

EBITDA represents net income plus interest and finance costs plus depreciation and amortization and income taxes, if any. EBITDA is included because it is used by certain investors to measure a company's financial performance. EBITDA is a “non-GAAP financial measure” and should not be considered a substitute for net income, cash flow from operating activities and other operations or cash flow statement data prepared in accordance with accounting principles generally accepted in the United States or as a measure of profitability or liquidity. EBITDA is presented to provide additional information with respect to the Company's ability to satisfy its obligations including debt service, capital expenditures, working capital requirements and determination of dividends. While EBITDA is frequently used as a measure of operating results and the ability to meet debt service requirements, the definition of EBITDA used here may not be comparable to that used by other companies due to differences in methods of calculation.

3

Agenda

• Navios Business Model Overview• Q2 2008 and Recent Developments• Vessel Operations• Navios Maritime Partners• Navios South American Logistics• Industry Overview• Financial Highlights – Q2 and H1 2008• Appendix

4

Navios Business Model Overview

555

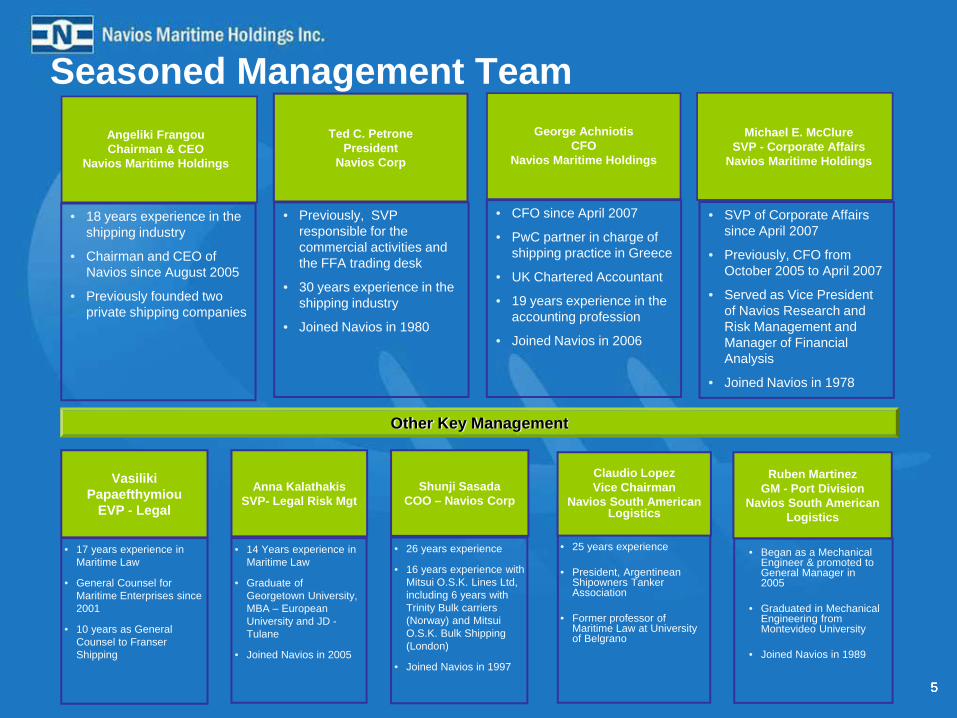

Seasoned Management Team

• 18 years experience in the shipping industry

• Chairman and CEO of Navios since August 2005

• Previously founded two private shipping companies

Shunji SasadaCOO – Navios Corp

• 26 years experience

• 16 years experience with Mitsui O.S.K. Lines Ltd, including 6 years with Trinity Bulk carriers (Norway) and Mitsui O.S.K. Bulk Shipping (London)

• Joined Navios in 1997

Other Key Management

• SVP of Corporate Affairs since April 2007

• Previously, CFO from October 2005 to April 2007

• Served as Vice President of Navios Research and Risk Management and Manager of Financial Analysis

• Joined Navios in 1978

Angeliki FrangouChairman & CEO

Navios Maritime Holdings

• CFO since April 2007

• PwC partner in charge of shipping practice in Greece

• UK Chartered Accountant

• 19 years experience in the accounting profession

• Joined Navios in 2006

George AchniotisCFO

Navios Maritime Holdings

Michael E. McClureSVP - Corporate Affairs

Navios Maritime Holdings

Vasiliki Papaefthymiou

EVP - Legal

• 17 years experience in Maritime Law

• General Counsel for Maritime Enterprises since 2001

• 10 years as General Counsel to Franser Shipping

Anna KalathakisSVP- Legal Risk Mgt

• 14 Years experience in Maritime Law

• Graduate of Georgetown University, MBA – European University and JD -Tulane

• Joined Navios in 2005

• Previously, SVP responsible for the commercial activities and the FFA trading desk

• 30 years experience in the shipping industry

• Joined Navios in 1980

Ted C. PetronePresident

Navios Corp

Claudio LopezVice Chairman

Navios South American Logistics

• 25 years experience

• President, Argentinean Shipowners Tanker Association

• Former professor of Maritime Law at University of Belgrano

Ruben MartinezGM - Port Division

Navios South American Logistics

• Began as a Mechanical Engineer & promoted to General Manager in 2005

• Graduated in Mechanical Engineering from Montevideo University

• Joined Navios in 1989

66

Company Overview• NYSE listing (“NM”)

• 50+ year operating history

• Among world’s largest vertically integrated dry bulk shipping companies

– Young fleet of 64 owned & chartered-in vessels (6.2 million dwt)

– In-house technical & commercial management

– Purchase options on 20 vessels significantly below fair market value

• Flexible Business Model

• Significant Contracted Revenue

• Low-cost Operator

• Strong Brand with Established Long-term Relationships

Capesize

Ultra-Handymax

Panamax

(1) Fleet Growth statistics shown represent change from September 1, 2005 to September 12, 2008. Fleet calculation includes controlled fleet of Navios Group. Fleet of 21 vessels at September 1, 2005 and 62 controlled vessels at September 12, 2008. EBITDA represents CAGR for 2005-2007. Includes Obeliks (95% owned) sold in Q2 2008

EBITDA: 55%Fleet: 205%

Significant Growth (1)

Analyst Coverage• Cantor Fitzgerald• Dahlman Rose & Co.• Fearnley Fonds• JP Morgan• Lazard Capital Markets• Merrill Lynch• Jefferies• Goldman Sachs• Bank of America• DnB NOR

777

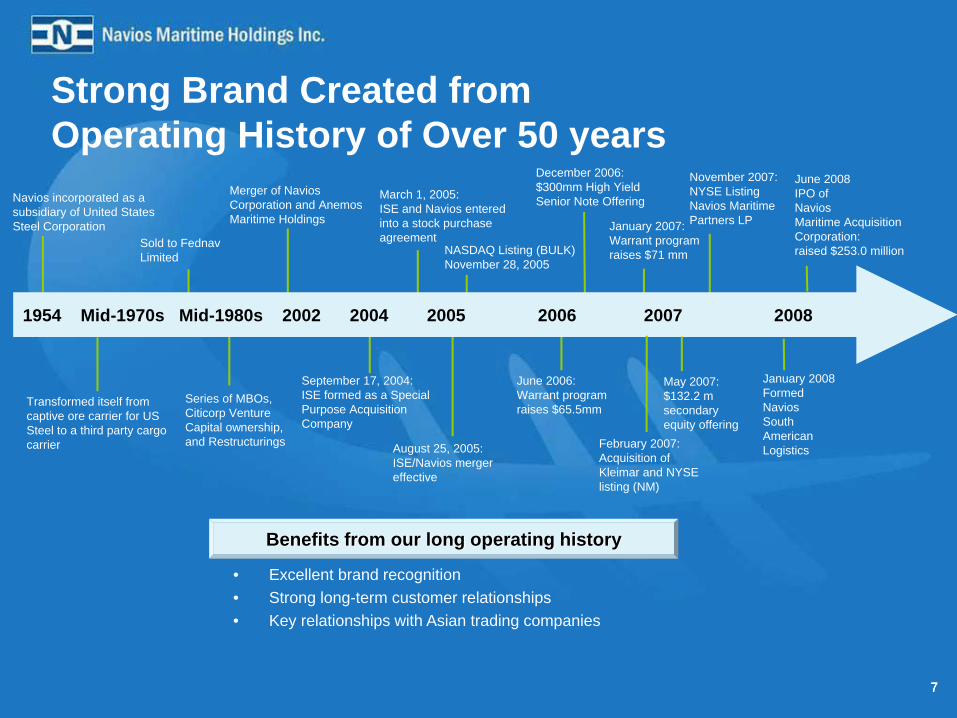

Strong Brand Created from Operating History of Over 50 years

December 2006:$300mm High YieldSenior Note OfferingNavios incorporated as a

subsidiary of United States Steel Corporation

Sold to Fednav Limited

Merger of Navios Corporation and Anemos Maritime Holdings

Transformed itself from captive ore carrier for US Steel to a third party cargo carrier

Series of MBOs, Citicorp Venture Capital ownership, and Restructurings

September 17, 2004:ISE formed as a Special Purpose Acquisition Company

August 25, 2005: ISE/Navios merger effective

March 1, 2005:ISE and Navios entered into a stock purchase agreement

1954 Mid-1970s Mid-1980s 2002 2004 2005 2006 2007 2008

NASDAQ Listing (BULK)November 28, 2005

• Excellent brand recognition• Strong long-term customer relationships• Key relationships with Asian trading companies

Benefits from our long operating history

June 2006:Warrant program raises $65.5mm

January 2007:Warrant program raises $71 mm

February 2007: Acquisition of Kleimar and NYSE listing (NM)

May 2007:$132.2 m secondary equity offering

November 2007:NYSE Listing Navios Maritime Partners LP

January 2008FormedNaviosSouthAmericanLogistics

June 2008IPO ofNaviosMaritime Acquisition Corporation:raised $253.0 million

88

NM Flexible Business ModelSecured Cash Flow + Risk Management + Investment Opportunities

Core Fleet (Owned and Long-Term Chartered-in Fleet)

Capitalize on real-time Market Intelligence in making strategic fleet management decisionsContracts of Affreightment (“COA”)Short-Term ChartersForward Freight Agreements (“FFA”)

Risk Management

63.8% ownership stakeBarge operations in the Hidrovia region and Port Terminal facilities (grain and liquid)Emerging markets commoditiesSignificant growth potential

Navios South American Logistics

Navios Maritime Partners L.P.(NYSE:NMM)

51.6% ownership stake 2.0% General Partner Interest Significant Incentive Distribution RightsHigh dividend distribution modelSignificant growth potentialNAV per NM share: $1.24*

Navios Maritime Acquisition Corp.(NYSE:NNA.U)

19% ownership stake for NM $253.0 million Gross IPO Proceeds$7.6 million NM investment Favorable marine transportation dynamicsNAV subject to successful business combination

NM TotalEBITDA

Includes both owned and long term chartered-in vesselsEmployed in long-term charter-out contracts (>12 months) Significant spreads over vessel operating expenses and charter-in rates

* As of September 8, 2008

9

Q2 2008 and Recent Developments

10

Recent Fleet Chartering Activity– Renewal of charters at 80% premium to current rates – Newbuildings chartered-out well ahead of availability

(1) Net time charter-out rate per day (net of commissions)

(2) Charter agreements include a redelivery time range of two to four months

(3) Estimated commencement date of new charter assuming midpoint redelivery by charterers

Vessel Type DWT Current charter-out daily rate (1)

New charter-out daily rate (1)

Period (2) Charter-out date (3)

Navios Orion

Panamax 76,602 $27,312 $49,400 3.5 years 4/1/2009

Navios Achilles

Ultra-Handymax

52,063 $21,138 $38,009 3 years 2/23/2009

Navios TBN

Capesize 172,000 n/a $41,325 10 years Q4 2009

Navios TBN

Capesize 172,000 n/a $57,000 5 years Q1 2010

11

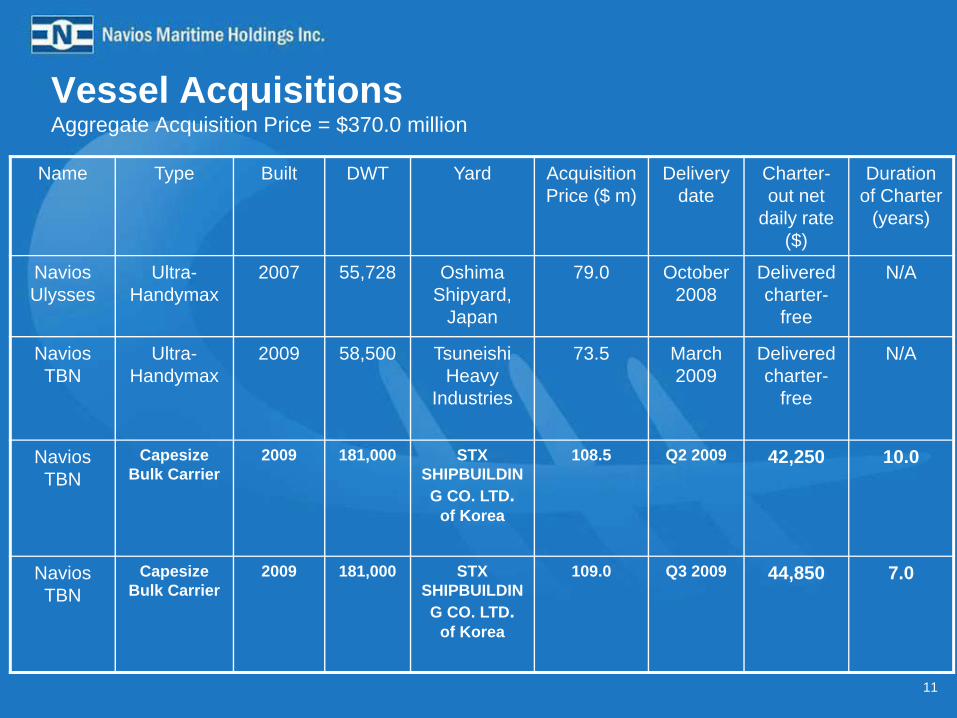

Vessel AcquisitionsAggregate Acquisition Price = $370.0 million

Name Type Built DWT Yard Acquisition Price ($ m)

Delivery date

Charter-out net

daily rate ($)

Duration of Charter

(years)

Navios Ulysses

Ultra-Handymax

2007 55,728 Oshima Shipyard,

Japan

79.0 October 2008

Delivered charter-

free

N/A

Navios TBN

Ultra-Handymax

2009 58,500 Tsuneishi Heavy

Industries

73.5 March 2009

Delivered charter-

free

N/A

Navios TBN

Capesize Bulk Carrier

2009 181,000 STX SHIPBUILDING CO. LTD.

of Korea

108.5 Q2 2009 42,250 10.0

Navios TBN

Capesize Bulk Carrier

2009 181,000 STX SHIPBUILDING CO. LTD.

of Korea

109.0 Q3 2009 44,850 7.0

12

Navios Maritime Acquisition Corporation

• Priced on June 25, 2008

• Closed on July 1, 2008

• Gross Proceeds of $253.0 million

• Units trading on NYSE (NYSE: NNA.U)– Common shares trade on NYSE under the symbol NNA– Warrants trade on NYSE under the symbol NNA WS

• 19% ownership position for NM

• Potential to NM – $7.6 million initial investment– Significant upside potential

Vessel Operations

1414

Navios Holdings – 64 vessels & 6.2 million DWT

(1) Includes Product tanker Vanessa, excludes Navios Logistics’ Fleet(2) Navios Group is composed of Navios Holdings (NM) and Navios Partners (NMM)

22 Panamax

• 17 vessels (1.35 million dwt)

17 Ultra-Handymax

• 5 vessels (0.27 million dwt)

• 3 vessels (0.17 million dwt)

36 Long-term Chartered-in 3.40 million dwt

20 Purchase Options

28 Owned Vessels2.79 million dwt

Controls 64(1) Vessels (6.2 million dwt)33 Currently Operating (2.6 million dwt)

Average Age = 4.5 years

Charter-in strategy allows fleet expansion with zero capital outlay& future ownership option via purchase options

Navios Group(2) controls 74 vessels and 7.2 million DWT

19 Capesize

• 10 vessels (1.75 million dwt)

• 9 vessels (1.61 million dwt)

• 3 vessels (0.54 million dwt)

One of the largest fleet among US-listed dry bulk carriers

6 Handysize

• 5 vessels (0.17 million dwt)

• 5 vessels (0.17 million dwt)

• 1 vessel (1)

(0.02 million dwt)• 5 vessels

(0.38 million dwt)• 12 vessels

(0.64 million dwt)

• 9 vessels (0.72 million dwt)

15

Fleet Growth Strategy

9,555

13,410

16,138

8,899

4,000

8,000

12,000

16,000

20,000

2008 2009 2010 2011

Available Days (1)

(1) Excludes COAs, Kleimar controlled Fleet and Navios Logistics’ Fleet

Equivalent Vessels (1)

26.5

37.3

44.8

24.7

20

25

30

35

40

45

50

2008 2009 2010 2011

1616

Attractive Charter-Out Rates with Creditworthy Parties

Top Ten Charter PartiesCharterer % of Total Charter-Out Revenue (2)

Cosco Bulk Carriers 20.4% Mitsui O.S.K. Lines Ltd. 15.4% Korea Line Corp 12.9% Daiichi Chuo Kisen Kaisha 6.3% Sanko 5.3% STX Pan Ocean Co. Ltd. 3.9% Emirates Trading Agency 3.5% Shinwa 3.2% Samsun Logix 3.0% Sangamon Trans Grp 2.9%

Total: 76.8%

Contracted Revenue(1)

2008: $217.3 million2009: $223.0 million2010: $245.2 million2011: $218.3 million

Average Daily Charter Rate

$24,760

$33,277$36,578 $37,929

$21,479

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

2007 2008 2009 2010 2011

Average Daily Charter-out Rate

High utilization ratesEarnings visibilitySteady cash flowDownside protection in challenging markets

Time Charter Strategy

(1) Excludes COAs, Kleimar controlled Fleet and Navios Logistics’ Fleet

% Days Contracted

36%

50%

70%

99%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011

% Days Contracted

AA insurance on all charters-out

(2) Years 2008 through 2010

1717

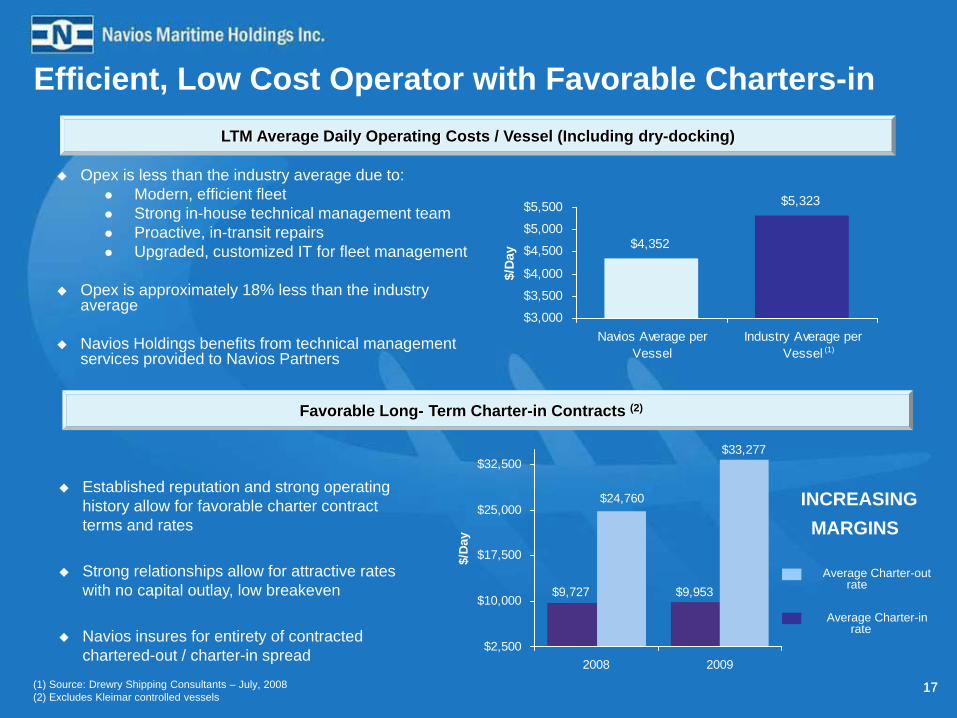

Efficient, Low Cost Operator with Favorable Charters-in

Opex is less than the industry average due to:Modern, efficient fleetStrong in-house technical management team Proactive, in-transit repairs Upgraded, customized IT for fleet management

Opex is approximately 18% less than the industry average

Navios Holdings benefits from technical management services provided to Navios Partners

LTM Average Daily Operating Costs / Vessel (Including dry-docking)

$4,352

$5,323

$3,000

$3,500

$4,000

$4,500

$5,000

$5,500

Navios Average perVessel

Industry Average perVessel

$/Da

y

(1)

(1) Source: Drewry Shipping Consultants – July, 2008(2) Excludes Kleimar controlled vessels

Favorable Long- Term Charter-in Contracts (2)

Established reputation and strong operating history allow for favorable charter contract terms and rates

Strong relationships allow for attractive rates with no capital outlay, low breakeven

Navios insures for entirety of contracted chartered-out / charter-in spread

$9,727 $9,953

$33,277

$24,760

$2,500

$10,000

$17,500

$25,000

$32,500

2008 2009

$/D

ay

Average Charter-out rate

Average Charter-in rate

INCREASINGMARGINS

Navios Maritime Partners

19

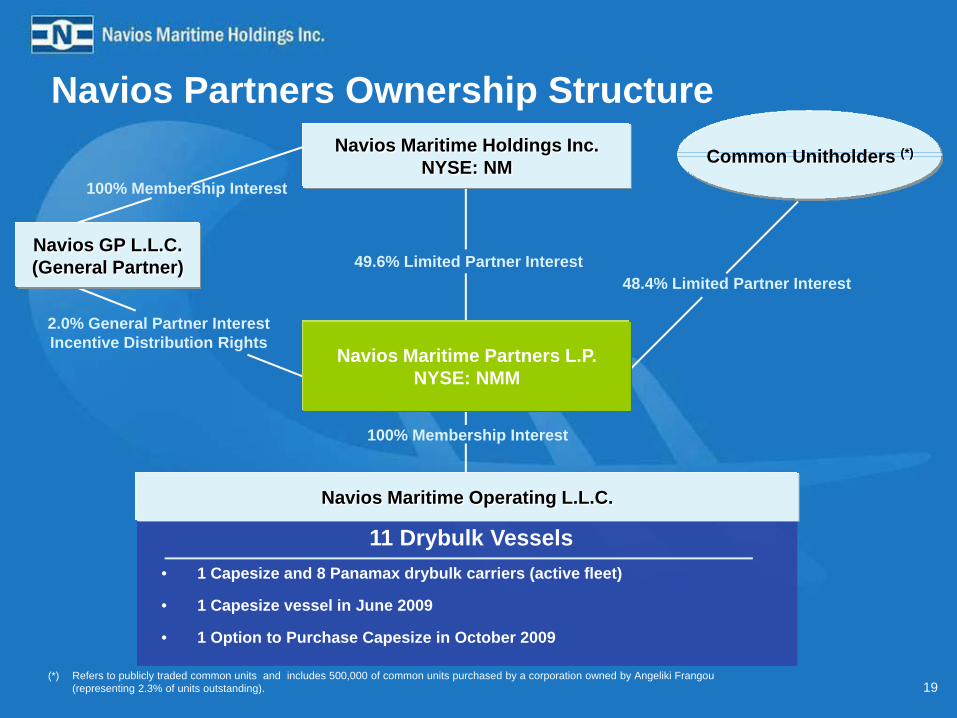

Navios Partners Ownership Structure

100% Membership Interest

2.0% General Partner InterestIncentive Distribution Rights

48.4% Limited Partner Interest49.6% Limited Partner Interest

11 Drybulk Vessels• 1 Capesize and 8 Panamax drybulk carriers (active fleet)

• 1 Capesize vessel in June 2009

100% Membership Interest

Navios GP L.L.C.(General Partner)

Navios Maritime Partners L.P.NYSE: NMM

Navios Maritime Operating L.L.C.

Common Unitholders (*)Navios Maritime Holdings Inc.NYSE: NM

(*) Refers to publicly traded common units and includes 500,000 of common units purchased by a corporation owned by Angeliki Frangou (representing 2.3% of units outstanding).

• 1 Option to Purchase Capesize in October 2009

20

NMM: Transactional and Strategic Overview• NMM’s Strategy

– Create durable cash flow for investors• Replacement reserve from operating cash for asset renewals

– Business Model • Panamax and Capesize vessels w/ target charter period of > 3 years • Pursue growth strategy – multiple avenues for growth• Excludes FFA / Short term chartering / COA • Excludes technical and commercial management

• NMM benefits from NM relationship– Proven source of new assets to grow the MLP– Proven network of strong relationships– Seasoned management providing:

• technical management• commercial management• administrative services

• Omnibus Agreement – Governs relationship between NM and NMM for future vessel acquisitions, etc.

Navios South American Logistics

22

Creation of Navios South American Logistics

• Acquired 51% interest in Horamar for $112.2 million cash• Horamar is a South American operator of barges and upriver port terminal with 30+

years operating history• Combined Navios’ port terminal business with Horamar’s barge and upriver port• Navios owns 63.8% of Navios Logistics (Lopez family own the remaining 36.2%)• Transaction Rationale:

– Critical mass for South American logistics business • Complementary business• Eventual Spin off

– Assets complementary to Navios Port Terminal– Strong presence in inland waterway transportation in the Hidrovia region of

Argentina, Bolivia, Brazil, Paraguay and Uruguay– Create platform capitalizing on region’s growing agricultural and mineral exports– Attractive valuation for consideration paid : 8.4x -9.3x 2008F EBITDA– Attractive valuation for Navios Port Terminal (15x 2007E EBITDA)

23

Navios South American LogisticsGroup Structure

23

Navios South American Logistics Inc(Marshall Islands)

100%

Horamar S.A

• 240 wet and dry barges• 1 Port - Paraguay• Fleet employed in Argentine cabotage business

(four product oil tankers):- Malva H delivered on January 13, 2008 - Estefania H delivered on July 25, 2008 - Makenita: expected delivery in Q4 2008- Sara H: expected delivery in Q4 2009

Corporación Navios S.A.

Port Terminal – Nueva Palmira –Uruguay (tax free zone)

2424

Navios Logistics Fleet Expansion• Fleet expansion:

– Acquisition of six convoys at approximately $72.0 million– Financing: $70.0 million Loan Facility– Secured Long-Term Cash Flow:

• 3 & 5 year agreements with two major commodity producers • Starting operations in Q4 2008

• Fleet employed in Argentine cabotage business:– Malva H delivered on January 13, 2008

• Product Oil Tanker, built in 2007, dwt 9,947• Employed as of February 2, 2008• Chartered for minimum four years (plus charterer’s option to extend for two years)

– Estefania H delivered on July 25, 2008• Product Oil Tanker, built in 2008, dwt 12,000• Employed as of August 2, 2008

– Makenita: expected delivery in Q4 2008• Product Oil Tanker, dwt 17,000

– Sara H: expected delivery in Q4 2009• Product Oil Tanker, dwt 9,000

• Navios Logistics will control a fleet of 240 barges and vessels transporting wet and dry cargo

25

Industry Overview

BDI Index 2006 - 2008Forward expectations remain strong …

0

2000

4000

6000

8000

10000

12000

14000

JAN

JAN

JAN

FEB

FEB

FEB

MARMAR

APR

APR

APR

MAYMAYJUN

JUN

JUN

JUL

JUL

JUL

AUG

AUG

AUGSEP

SEP

OCT

OCTOCTNOVNOVNOVDEC

DECin

dex

poin

BDI 2006

BDI 2007

BDI 2008

Forward Curve Q4

Forward Curve SEP

….. despite continuing worldwide credit and equity concerns

Source: The Baltic Exchange

27272727

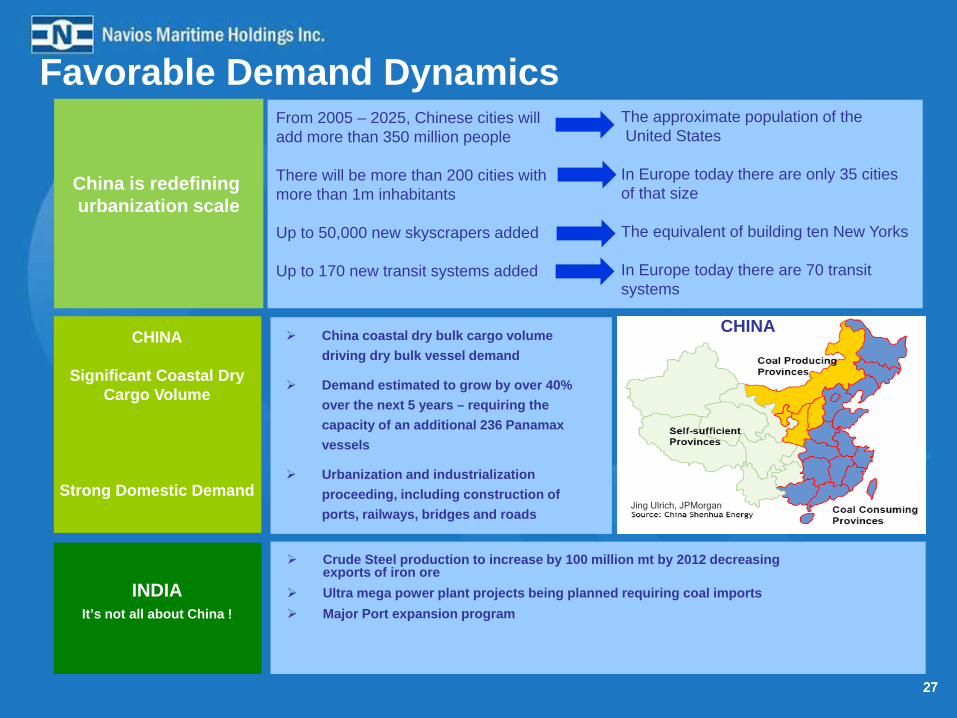

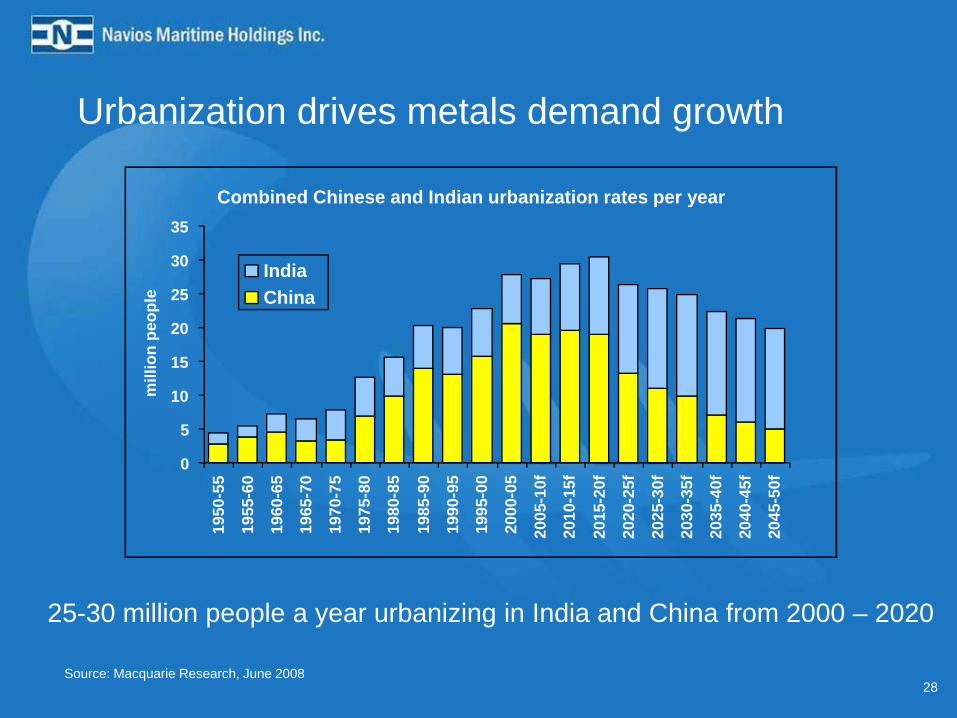

Favorable Demand Dynamics

CHINA

Significant Coastal Dry Cargo Volume

Strong Domestic Demand

China coastal dry bulk cargo volume driving dry bulk vessel demand

Demand estimated to grow by over 40% over the next 5 years – requiring the capacity of an additional 236 Panamax vessels

Urbanization and industrialization proceeding, including construction of ports, railways, bridges and roads

CHINA

Jing Ulrich, JPMorgan

INDIAIt’s not all about China !

Crude Steel production to increase by 100 million mt by 2012 decreasingexports of iron ore Ultra mega power plant projects being planned requiring coal importsMajor Port expansion program

China is redefining urbanization scale

From 2005 – 2025, Chinese cities will add more than 350 million people

There will be more than 200 cities with more than 1m inhabitants

Up to 50,000 new skyscrapers added

Up to 170 new transit systems added

The approximate population of theUnited States

In Europe today there are only 35 cities of that size

The equivalent of building ten New Yorks

In Europe today there are 70 transit systems

28

25-30 million people a year urbanizing in India and China from 2000 – 2020

Combined Chinese and Indian urbanization rates per year

0

5

10

15

20

25

30

3519

50-5

5

1955

-60

1960

-65

1965

-70

1970

-75

1975

-80

1980

-85

1985

-90

1990

-95

1995

-00

2000

-05

2005

-10f

2010

-15f

2015

-20f

2020

-25f

2025

-30f

2030

-35f

2035

-40f

2040

-45f

2045

-50f

mill

ion

peop

le

IndiaChina

Urbanization drives metals demand growth

Source: Macquarie Research, June 2008

29

Trade growth mainly China and mainly iron ore

29

Annual Changes in Seaborne Demand

-30-20-10

0102030405060708090

100110120

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

f20

09f

2010

f20

11f

2012

f

m to

nnes

cha

nge

Outside ChinaChina

China’s future role is even greaterSource: Macquarie Research, June 2008

30

Drybulk Vessels – Supply vs. Aging Fleet• Order book includes 181.1 mdwt (44.5% of fleet) of scheduled deliveries through 2010(1)

– New vessels ordered today will not be delivered until 2011– Substantial greenfield (red) and inexperienced (gray) shipyard risk– Capesize orderbook to be built at 31 yards – only 13 of them have built Capes before (2)

– Slippage of newbuilding deliveries has occurred

(1) Source: Drewry Shipping Consultants, Ltd. (August 2008)(2) Source: Howe Robinson (January 2008)(3) Source: SSY’s Dry Bulk Forecaster (August 2008)(4) Source: SSY (July 2008)

29%

16%

0%

10%

20%

30%

40%

50%

Total Drybulk Fleet Total Drybulk Fleet

Over 20 Years Old Over 25 Years Old

Drybulk Industry Age Profile (% dwt) (3)

0102030405060708090

100

Handy Handymax Panamax Cape

%

Established New Entrant (size) New Entrant (Type)

Given strong market conditions, older vessels are not being actively scrapped

Dry Bulk Orderbook by Type of Builder: Share of 2009/2010 Orders (4)

31

Financial Highlights: Q2 2008 and H1 2008

32

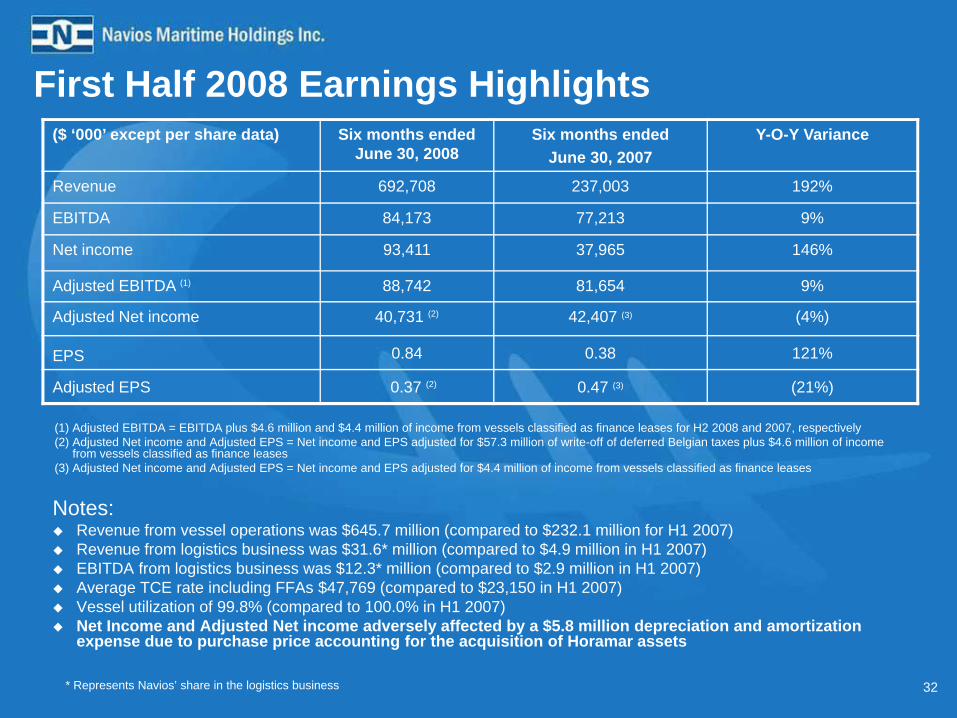

First Half 2008 Earnings Highlights

Notes: Revenue from vessel operations was $645.7 million (compared to $232.1 million for H1 2007)Revenue from logistics business was $31.6* million (compared to $4.9 million in H1 2007)EBITDA from logistics business was $12.3* million (compared to $2.9 million in H1 2007)Average TCE rate including FFAs $47,769 (compared to $23,150 in H1 2007)Vessel utilization of 99.8% (compared to 100.0% in H1 2007)Net Income and Adjusted Net income adversely affected by a $5.8 million depreciation and amortization expense due to purchase price accounting for the acquisition of Horamar assets

($ ‘000’ except per share data) Six months ended June 30, 2008

Six months ended June 30, 2007

Y-O-Y Variance

Revenue 692,708 237,003 192%

EBITDA 84,173 77,213 9%

Net income 93,411 37,965 146%

Adjusted EBITDA (1) 88,742 81,654 9%

Adjusted Net income 40,731 (2) 42,407 (3) (4%)

EPS 0.84 0.38 121%

Adjusted EPS 0.37 (2) 0.47 (3) (21%)

* Represents Navios’ share in the logistics business

(1) Adjusted EBITDA = EBITDA plus $4.6 million and $4.4 million of income from vessels classified as finance leases for H2 2008 and 2007, respectively(2) Adjusted Net income and Adjusted EPS = Net income and EPS adjusted for $57.3 million of write-off of deferred Belgian taxes plus $4.6 million of income

from vessels classified as finance leases (3) Adjusted Net income and Adjusted EPS = Net income and EPS adjusted for $4.4 million of income from vessels classified as finance leases

33

Second Quarter 2008 Earnings Highlights

Notes: Revenue from vessel operations was $328.9 million (compared to $132.5 million for Q2 2007)Revenue from logistics business was $17.1* million (compared to $3.4 million in Q2 2007) EBITDA from logistics business was $6.9* million (compared to $2.3 million in Q2 2007)Average TCE rate including FFAs $48,390 (compared to $23,909 in Q2 2007)Vessel utilization of 99.7% (compared to 100.0% in Q2 2007)Net Income and Adjusted Net income adversely affected by a $2.8 million depreciation and amortization expense due to purchaseprice accounting for the acquisition of Horamar assets

($ ‘000’ except per share data) Three months ended June 30, 2008

Three months ended June 30, 2007

Y-O-Y Variance

Revenue 354,432 135,865 161%

EBITDA 46,175 42,641 8%

Net income 79,166 23,182 241%

Adjusted EBITDA(1) 48,217 45,578 6%

Adjusted Net income 23,960 (2) 26,119 (3) (8%)

EPS 0.72 0.24 200%

Adjusted EPS 0.22 (2) 0.27 (3) (19%)

(1) Adjusted EBITDA = EBITDA plus $2.0 million and $2.9 million of income from vessels classified as finance leases for Q2 2008 and 2007, respectively(2) Adjusted Net income and Adjusted EPS = Net income and EPS adjusted for $57.3 million of write-off of deferred Belgian taxes plus $2.0 million of income

from vessels classified as finance leases (3) Adjusted Net income and Adjusted EPS = Net income and EPS adjusted for $2.9 million of income from vessels classified as finance leases

* Represents Navios’ share in the logistics business

34

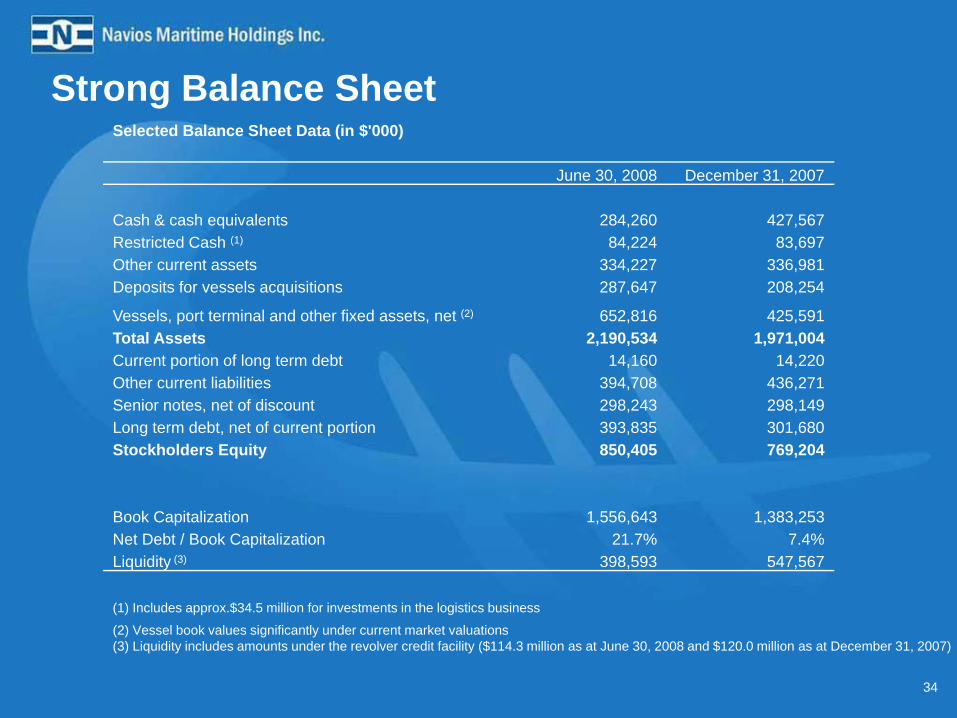

Strong Balance Sheet Selected Balance Sheet Data (in $'000)

June 30, 2008 December 31, 2007

Cash & cash equivalents 284,260 427,567Restricted Cash (1) 84,224 83,697Other current assets 334,227 336,981Deposits for vessels acquisitions 287,647 208,254

Vessels, port terminal and other fixed assets, net (2) 652,816 425,591Total Assets 2,190,534 1,971,004Current portion of long term debt 14,160 14,220Other current liabilities 394,708 436,271Senior notes, net of discount 298,243 298,149Long term debt, net of current portion 393,835 301,680Stockholders Equity 850,405 769,204

Book Capitalization 1,556,643 1,383,253Net Debt / Book Capitalization 21.7% 7.4%Liquidity (3) 398,593 547,567

(1) Includes approx.$34.5 million for investments in the logistics business

(2) Vessel book values significantly under current market valuations(3) Liquidity includes amounts under the revolver credit facility ($114.3 million as at June 30, 2008 and $120.0 million as at December 31, 2007)

35

New Bank Facility

• NM entered into a new Term Loan Facility with DnB Nor Bank ASA for $133.0 million on June 24, 2008

• The proceeds will be used to finance two new-building Capesize vessels delivering in March & June 2010

• 8 year loan (18 year amortization profile)

• Interest rate: LIBOR + 100 bp

• Principal repayments commence only upon the delivery of the vessels

• Principal repayments over 16 equal semiannual installments of $1.85 million each– Annual repayment $3.7 million each (total $7.4 million)– Balloon payment of $36.9 million each (total $73.8 million)

36

Dividend Distribution for Q2 2008

– Proposed dividend distribution for Q2 2008 of $0.09 per share outstanding

– Record Date: September 2, 2008– Payment Date: September 12, 2008– Shares outstanding (NYSE: NM): 104,159,215 (1) (2)

– Warrants outstanding (NYSE: NM WS): 6,903,930 (1)

Buyback Program Update (1)

– Number of shares bought: 3,164,440

(1) As of August 18, 2008

(2) Excludes shares repurchased

37

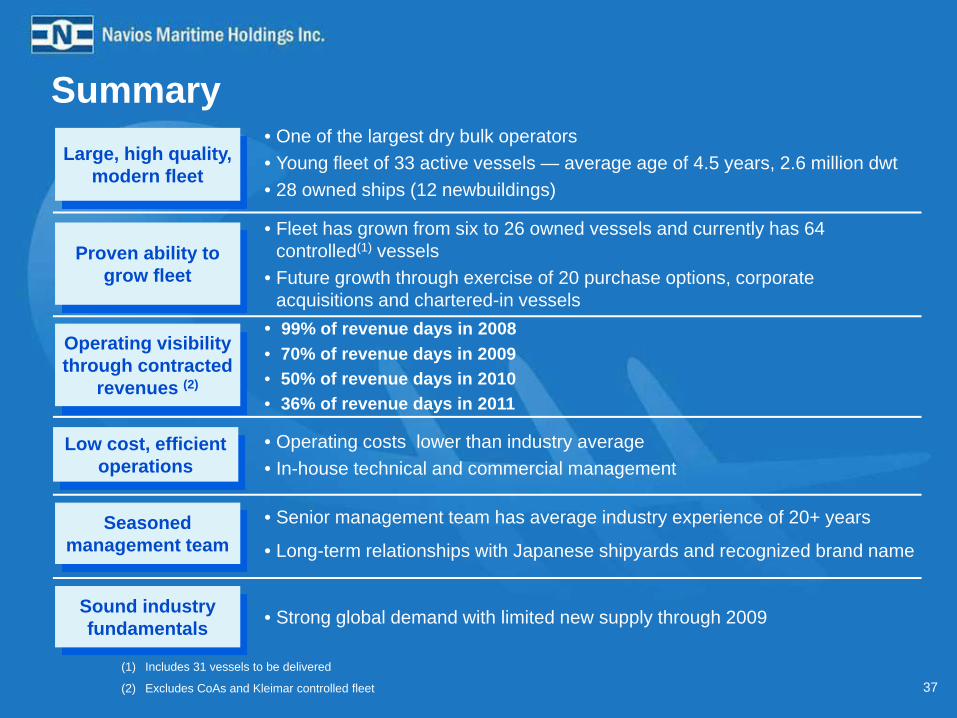

Summary

• Senior management team has average industry experience of 20+ years

• Long-term relationships with Japanese shipyards and recognized brand name

• Operating costs lower than industry average• In-house technical and commercial management

• 99% of revenue days in 2008• 70% of revenue days in 2009 • 50% of revenue days in 2010• 36% of revenue days in 2011

• Fleet has grown from six to 26 owned vessels and currently has 64 controlled(1) vessels

• Future growth through exercise of 20 purchase options, corporate acquisitions and chartered-in vessels

• One of the largest dry bulk operators• Young fleet of 33 active vessels — average age of 4.5 years, 2.6 million dwt• 28 owned ships (12 newbuildings)

Large, high quality, modern fleet

Proven ability to grow fleet

Seasoned management team

Low cost, efficient operations

Operating visibility through contracted

revenues (2)

(1) Includes 31 vessels to be delivered

(2) Excludes CoAs and Kleimar controlled fleet

• Strong global demand with limited new supply through 2009Sound industry fundamentals

Appendix

404040

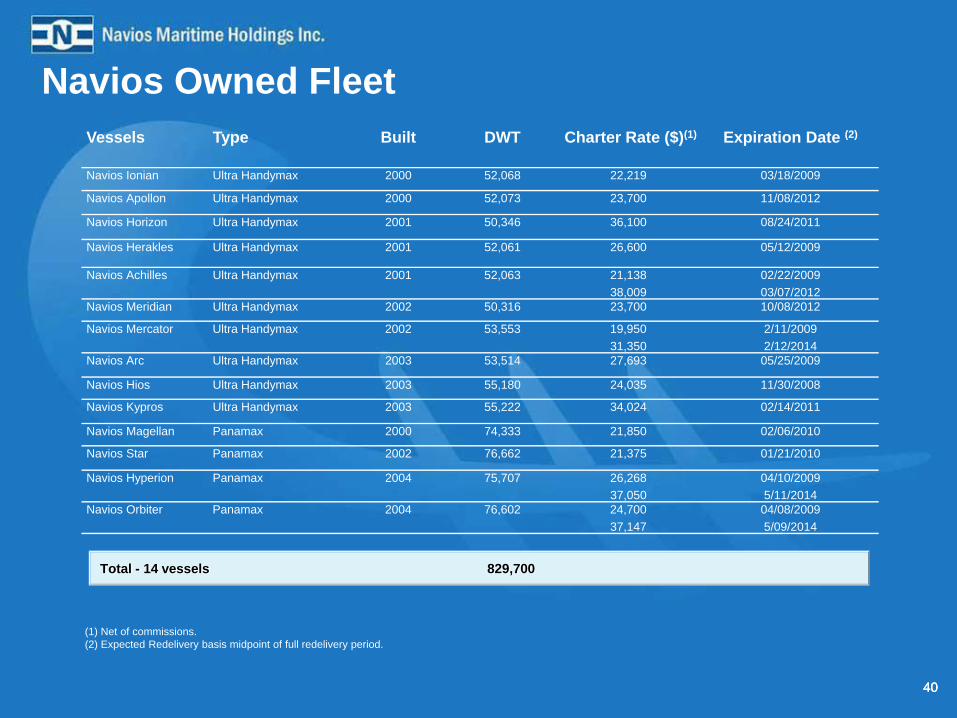

Navios Owned FleetVessels Type Built DWT Charter Rate ($)(1) Expiration Date (2)

Navios Ionian Ultra Handymax 2000 52,068 22,219 03/18/2009

Navios Apollon Ultra Handymax 2000 52,073 23,700 11/08/2012

Navios Horizon Ultra Handymax 2001 50,346 36,100 08/24/2011

Navios Herakles Ultra Handymax 2001 52,061 26,600 05/12/2009

Navios Achilles Ultra Handymax 2001 52,063 21,13838,009

02/22/200903/07/2012

Navios Meridian Ultra Handymax 2002 50,316 23,700 10/08/2012

Navios Mercator Ultra Handymax 2002 53,553 19,95031,350

2/11/20092/12/2014

Navios Arc Ultra Handymax 2003 53,514 27,693 05/25/2009

Navios Hios Ultra Handymax 2003 55,180 24,035 11/30/2008

Navios Kypros Ultra Handymax 2003 55,222 34,024 02/14/2011

Navios Magellan Panamax 2000 74,333 21,850 02/06/2010

Navios Star Panamax 2002 76,662 21,375 01/21/2010

Navios Hyperion Panamax 2004 75,707 26,26837,050

04/10/20095/11/2014

Navios Orbiter Panamax 2004 76,602 24,70037,147

04/08/20095/09/2014

Total - 14 vessels 829,700

(1) Net of commissions. (2) Expected Redelivery basis midpoint of full redelivery period.

414141

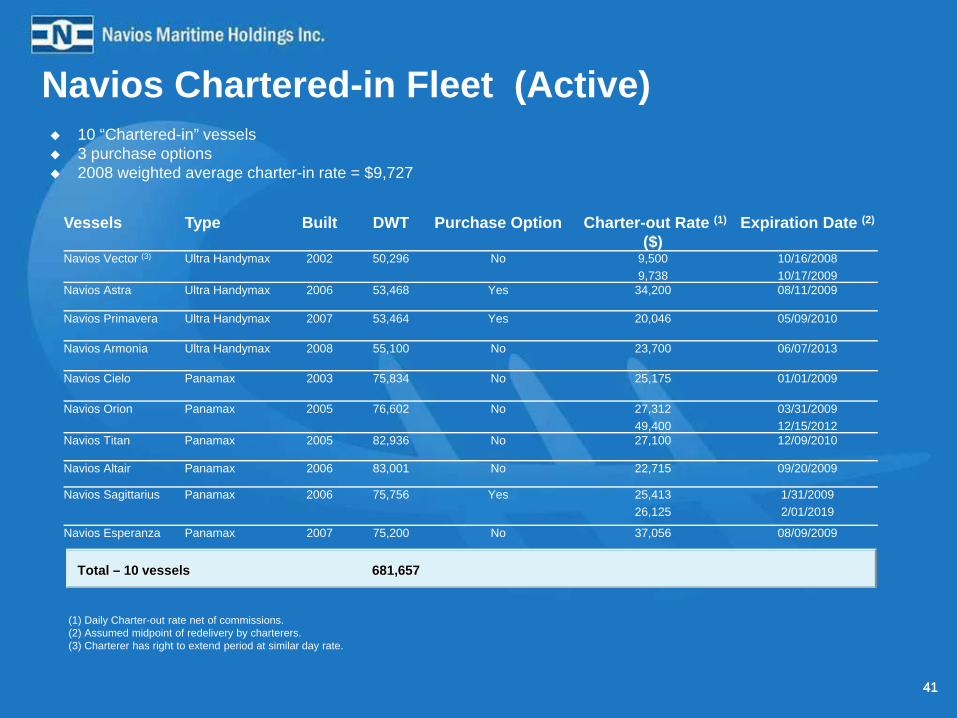

Navios Chartered-in Fleet (Active)

Vessels Type Built DWT Purchase Option Charter-out Rate (1)

($)Expiration Date (2)

Navios Vector (3) Ultra Handymax 2002 50,296 No 9,5009,738

10/16/200810/17/2009

Navios Astra Ultra Handymax 2006 53,468 Yes 34,200 08/11/2009

Navios Primavera Ultra Handymax 2007 53,464 Yes 20,046 05/09/2010

Navios Armonia Ultra Handymax 2008 55,100 No 23,700 06/07/2013

Navios Cielo Panamax 2003 75,834 No 25,175 01/01/2009

Navios Orion Panamax 2005 76,602 No 27,31249,400

03/31/200912/15/2012

Navios Titan Panamax 2005 82,936 No 27,100 12/09/2010

Navios Altair Panamax 2006 83,001 No 22,715 09/20/2009

Navios Sagittarius Panamax 2006 75,756 Yes 25,41326,125

1/31/20092/01/2019

Navios Esperanza Panamax 2007 75,200 No 37,056 08/09/2009

10 “Chartered-in” vessels 3 purchase options2008 weighted average charter-in rate = $9,727

Total – 10 vessels 681,657

(1) Daily Charter-out rate net of commissions.(2) Assumed midpoint of redelivery by charterers.(3) Charterer has right to extend period at similar day rate.

424242

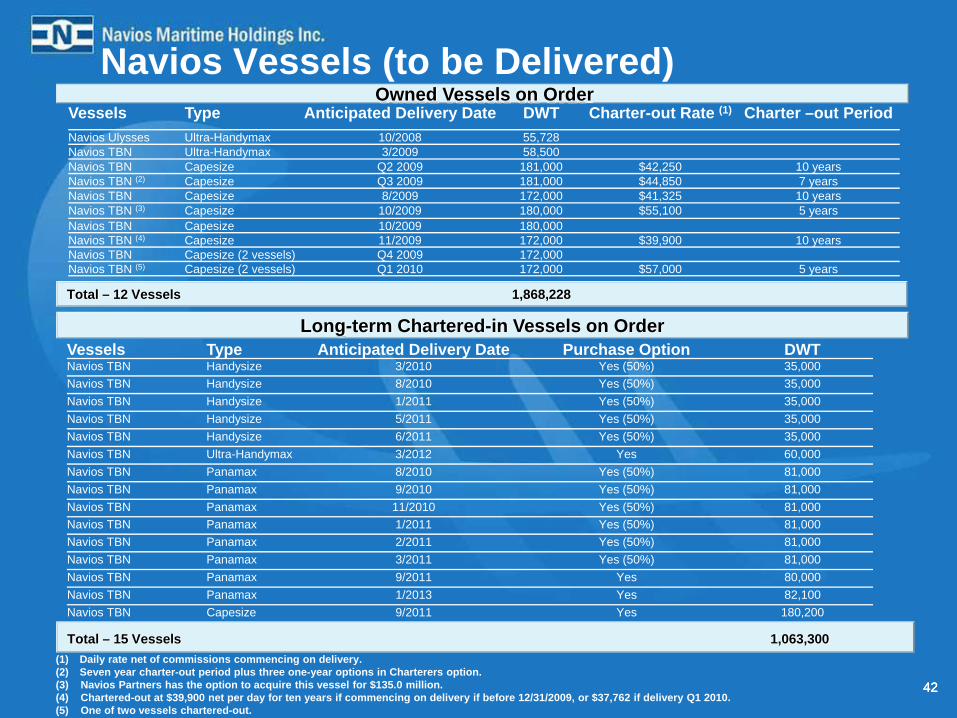

Navios Vessels (to be Delivered)

Vessels Type Anticipated Delivery Date Purchase Option DWTNavios TBN Handysize 3/2010 Yes (50%) 35,000Navios TBN Handysize 8/2010 Yes (50%) 35,000Navios TBN Handysize 1/2011 Yes (50%) 35,000Navios TBN Handysize 5/2011 Yes (50%) 35,000Navios TBN Handysize 6/2011 Yes (50%) 35,000Navios TBN Ultra-Handymax 3/2012 Yes 60,000Navios TBN Panamax 8/2010 Yes (50%) 81,000Navios TBN Panamax 9/2010 Yes (50%) 81,000Navios TBN Panamax 11/2010 Yes (50%) 81,000Navios TBN Panamax 1/2011 Yes (50%) 81,000Navios TBN Panamax 2/2011 Yes (50%) 81,000Navios TBN Panamax 3/2011 Yes (50%) 81,000Navios TBN Panamax 9/2011 Yes 80,000Navios TBN Panamax 1/2013 Yes 82,100Navios TBN Capesize 9/2011 Yes 180,200

Long-term Chartered-in Vessels on Order

Total – 15 Vessels 1,063,300

Owned Vessels on OrderVessels Type Anticipated Delivery Date DWT Charter-out Rate (1) Charter –out PeriodNavios Ulysses Ultra-Handymax 10/2008 55,728Navios TBN Ultra-Handymax 3/2009 58,500Navios TBN Capesize Q2 2009 181,000 $42,250 10 yearsNavios TBN (2) Capesize Q3 2009 181,000 $44,850 7 yearsNavios TBN Capesize 8/2009 172,000 $41,325 10 yearsNavios TBN (3) Capesize 10/2009 180,000 $55,100 5 yearsNavios TBN Capesize 10/2009 180,000Navios TBN (4) Capesize 11/2009 172,000 $39,900 10 yearsNavios TBN Capesize (2 vessels) Q4 2009 172,000Navios TBN (5) Capesize (2 vessels) Q1 2010 172,000 $57,000 5 years

Total – 12 Vessels 1,868,228

(1) Daily rate net of commissions commencing on delivery.(2) Seven year charter-out period plus three one-year options in Charterers option.(3) Navios Partners has the option to acquire this vessel for $135.0 million.(4) Chartered-out at $39,900 net per day for ten years if commencing on delivery if before 12/31/2009, or $37,762 if delivery Q1 2010.(5) One of two vessels chartered-out.

434343

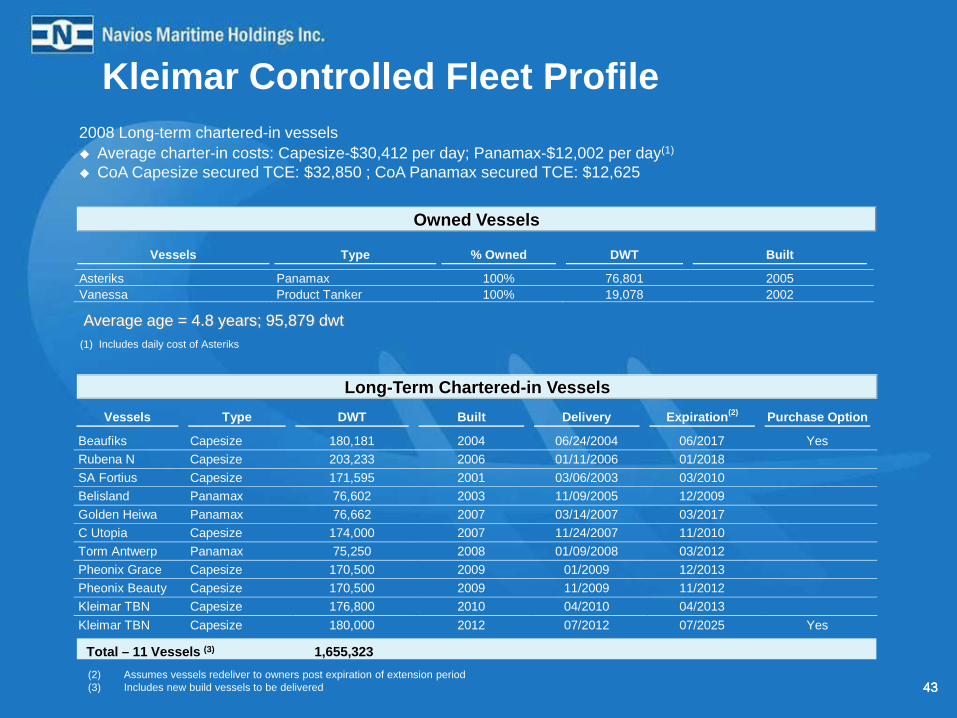

Kleimar Controlled Fleet Profile2008 Long-term chartered-in vessels

Average charter-in costs: Capesize-$30,412 per day; Panamax-$12,002 per day(1)

CoA Capesize secured TCE: $32,850 ; CoA Panamax secured TCE: $12,625

(2) Assumes vessels redeliver to owners post expiration of extension period(3) Includes new build vessels to be delivered

Long-Term Chartered-in Vessels

Vessels Type % Owned DWT Built

Asteriks Panamax 100% 76,801 2005 Vanessa Product Tanker 100% 19,078 2002

Owned Vessels

Vessels Type DWT Built Delivery Expiration(2) Purchase Option

Beaufiks Capesize 180,181 2004 06/24/2004 06/2017 Yes Rubena N Capesize 203,233 2006 01/11/2006 01/2018 SA Fortius Capesize 171,595 2001 03/06/2003 03/2010 Belisland Panamax 76,602 2003 11/09/2005 12/2009 Golden Heiwa Panamax 76,662 2007 03/14/2007 03/2017 C Utopia Capesize 174,000 2007 11/24/2007 11/2010 Torm Antwerp Panamax 75,250 2008 01/09/2008 03/2012 Pheonix Grace Capesize 170,500 2009 01/2009 12/2013 Pheonix Beauty Capesize 170,500 2009 11/2009 11/2012 Kleimar TBN Capesize 176,800 2010 04/2010 04/2013 Kleimar TBN Capesize 180,000 2012 07/2012 07/2025 Yes

(1) Includes daily cost of Asteriks

Total – 11 Vessels (3) 1,655,323

Average age = 4.8 years; 95,879 dwt