Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 1

1 SOCIO-ECONOMICS AND TOURISM

Introduction

1.1 This document presents the baseline data upon which an assessment of socio-economic and tourism impacts arising from the proposed Navitus Bay Wind Park project (hereafter referred to as the ‘project’) have been identified during its construction, operation and maintenance, and decommissioning phases.

1.2 This document also briefly reviews baseline data for the Commercial Fisheries and Shipping and Navigation impact assessments. Both of these are the subject of separate assessment, but linked to this work because of their role as economic activities.

Study Area

1.3 The study area for the socio-economic assessment takes in the counties of Dorset and Hampshire and the unitary authorities of Poole, Bournemouth, the Isle of Wight, Portsmouth and Southampton, and is detailed in Figure 1.1. These areas form the key areas of population and economic activity within which the proposed development site is located. It includes areas that may be involved in construction, operation and maintenance and decommissioning activities. Solely for the purpose of labour market analysis, a study area defined by 30, 45 and 60 minute drive time catchments from the ports has been adopted in relation to the offshore components of the project.

1.4 The tourism study area is also defined in Figure 1.1. This includes a 20 km zone which has as its midpoint, the coastline, stretching from the Purbeck Peninsula to the east of the Isle of Wight. It includes parts of the counties of Dorset and Hampshire and the unitary authorities of Poole, Bournemouth and the Isle of Wight. The principal towns and settlements in the surrounding area, including Bournemouth, Poole and Swanage are included. This area was considered appropriate in response to consultation, consideration of the approach adopted in other assessments of offshore wind proposals, and professional judgement.

1.5 For the onshore components of the project the study area is a 2 km zone around the cable route and substation. For the labour market analysis, a study area defined by 30, 45 and 60 minute drive time catchments from the substation has been adopted for the onshore components of the project..

1.6 The study area for the Commercial Fisheries assessment broadly includes the area of open sea from St. Catherine’s Point on the Isle of Wight in the east to St. Alban’s Head in Dorset in the west. This area includes all inshore waters and extends to the most southerly extent of the offshore development site.

1.7 The study area for the Shipping assessment is based on a 10 NM buffer around the proposed Offshore Development Area. This distance has been used as it presents a

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 2

sufficient area to capture the relevant issues for the wind farm in terms of vessel movements. In addition, the baseline includes a brief review of the available information about the economic role of the key ports within the socio-economic study area.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 3

Figure 1-1 Study Area

Source PBA RTP Baseline Assessment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 4

1.8 This baseline review is supplemented by a survey of local tourism businesses which may be affected by the project as well as two quantitative and one qualitative pieces of visitor research. The findings of this research, which are reported separately, provide additional detail on the profile of visitors and visits, key characteristics of the area, business trends and prospects, rates, levels of turnover and the perceived potential impact of the project on businesses.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 5

2 DATA SOURCES 2.1 This assessment has been informed by data and documents related to the study area for

the project, i.e. the administrative areas of Poole and Bournemouth Borough Councils, Southampton and Portsmouth City Councils, the counties of Dorset, Hampshire and the Isle of Wight and the South East and South West regions.

2.2 Information sources and relevant documents used in the compilation of the socio-economic and tourism baseline are listed in Table 2-1 below.

Table 2-1 Key Data Sources

Scale Source

Regional

Socio-Economics Office for National Statistics (via NOMIS)

Census data (2001and 2011)

Mid-year population estimates (2011)

Claimant Count (March 2013)

Annual Business Inquiry (2008)

Annual Population Survey (Jan 2012 – Dec 2012)

Regional GVA Figures (2011)

BERR – VAT registrations/ de-registrations by industry (2007)

Tourism

South West and South East Top 10 Paid and Unpaid Visitor Attractions (2011)

South West of England Regional Summary (VisitEngland) (2010)

South East of England Regional Summary (VisitEngland) (2010)

Great Britain Tourism Survey Analysis (2007-2011) (VisitEngland)

Overseas Tourism in UK Countries/Regions (2011) (VisitBritain)

Office for National Statistics. International Passenger Survey (2011)

Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

The Economic Impact of Tourism: New Forest (Tourism South East, 2008)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 6

Scale Source

Christchurch and East Dorset Core Strategy Pre-Submission (2012)

Building a more Competitive Economy in Bournemouth Dorset and Poole (2005-2016)

Isle of Wight Economic Development Plan (2011/12 – 2013/14)

Economic Strategy for New Forest District (2006)

Dorset Local Economic Partnership Prospectus (2012)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 7

3 EDUCATION AND TRAINING INFRASTRUCTURE 3.1 An assessment of education providers offering courses in the renewable energy market has

been prepared. The relevant courses in the area will help to train people to get a job in the renewables sector. Access to relevant courses will help to strengthen the areas skills within the renewables market.

3.2 In those areas with the potential to be impacted by the project (i.e. Bournemouth, Poole, Swanage, Southampton and Portsmouth), there are some training programmes and university/college courses specifically designed to cater for the renewable energy market. A summary of relevant academic courses and training programmes is provided below:

Southampton University

Environmental Engineering – Students learn about sustainable energy resources and there are specific modules with elements related to offshore wind. Examples include modules on Coastal and Maritime Engineering and Energy and Energy Resources and Engineering.

Sustainable Energy Technologies – Students are taught the advanced knowledge and practical skills needed for a professional career in the renewable energy industry amongst others. One of the compulsory modules of the course (Renewable Energy from the Environment) teaches students the theoretical understanding required to design suitable energy conversion devices suitable for exploiting wind, both on and offshore. At the end of the course students should have an understanding of how devices are sited and the considerations required for installation, maintenance, operational control and eventual decommissioning.

Maritime Engineering and Ship Science – Offshore structures and wind/water energy harvesting structures are examples of engineering systems considered on the course.

Warsash Maritime Academy

There is a training course titled Renewable UK Marine Survival Training (MST) which addresses the most significant health, safety and emergency response training issues as they relate to vessel transit and transfer. The course provides training for a number of modules including Offshore environment and hazards, Organisation for safety when transiting and transferring to and from offshore wind farms, offshore operations and emergencies and first aid.

Apprenticeship Training Ltd (ATL)

A training organisation in Southampton which offers a two day course on Renewables awareness.

3.3 As a result of a recent successful European Funding Bid, Southampton City Council and its UK/French partners have secured £1.7m for a project entitled BEEMS (Building European Environmental Maritime Skills). The project is envisaged to help stimulate the development and growth of environmental and maritime skills within the marine renewable energy industry. It should enable people to have the skills to work in the offshore renewables industry in a range of vocations such as welding to fire safety.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 8

3.4 There are also indirect courses which provide some of the skills to work in the offshore industry. At Bournemouth and Poole College there is a course in electronics and Corporate Safety Management (CSM) in Poole. This college offers a range of health and safety courses. Bournemouth and Poole College also offers construction courses relevant to the onshore project, as well as other providers such as Eastleigh College, A Plus Safety & Training Services in Bournemouth and Poole, Highbury College in Portsmouth and City College, Southampton.

3.5 Bournemouth University provides a variety of engineering degree courses as well as a Higher National Certificate (HNC) in Electrical Technology. Southampton University provides degree and post graduate courses in electrical engineering and Portsmouth University also offers engineering degree courses.

3.6 Across the wider South West and South East regions there are a greater number and range of education, training and skills providers which could help deliver a skilled labour market to develop the region’s energy industry.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 9

4 SOCIO-ECONOMIC PROFILE 4.1 This section outlines the socio-economic characteristics of the areas with the potential to be

impacted by the project. These are the areas of Bournemouth, Poole, the Isle of Wight, Southampton, Portsmouth, Dorset and Hampshire. For the purposes of this assessment these areas will be referred to as the ‘study area’. Study area characteristics are compared to the national socio-economic profile.

Population Structure and Projections

4.2 Since 2001 all areas within the study area have seen population growth, with the Isle of Wight, Southampton and Portsmouth experiencing growth in excess of the national average (Table 4-1). The average for the study area as whole is just below the GB average.

4.3 The areas of Poole, Isle of Wight, Dorset and Hampshire all have a relatively low proportion of working age population and a high dependency ratio1, compared to the study area and national averages. Whereas Bournemouth, Southampton and Portsmouth have a notably low dependency ratio and a higher number of working age population. These statistics are to be expected given that these are the three main cities in the study area, which are more likely to draw people looking for work. Since 2001 the age structure, in these three areas has strengthened (i.e. the proportion of working age people has increased) at a much higher rate compared to the wider socio-economic study area and national averages.

1 The dependency ratio (or proportion of working age people) is significant as it measures the relationship between the productive element of a population and the economically dependent.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

% change from 2001 7% 2% 0% 3% 4% -1% -1% -2% 1% *working age defined as anyone aged 16-64

**Total figure of Bournemouth, Poole, Isle of Wight, Southampton, Portsmouth, Dorset and Hampshire.

***GB data includes Scotland, England, and Wales.

Source: NOMIS 2013

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 11

4.4 Compared to the national average, the study area has higher economic activity rates2 and lower unemployment and claimant rates (Table 4-2). The study area also has a higher proportion of the workforce as employees and a well-represented self-employed labour force. A high proportion of self-employed workers is a good indicator of entrepreneurship and a dynamic labour market.

4.5 At a local authority level all these areas exhibit economic activity rates which are relatively close to the national average. The Isle of Wight is characterised by a higher unemployment and JSA Claimant rate3. Hampshire and Dorset by contrast have a well-balanced economically active labour force with relatively low unemployment rates.

2 The economic activity rate measures the percentage of the population who are in employment or unemployed. The economic activity rate is therefore a useful measure of the labour market opportunities available to the people. 3 A high proportion of economically active unemployed people represents and underutilised workforce that could contribute to the area’s economic performance.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 12

Table 4-2 Economic Activity (Jan 2012 - Dec 2012)

Bourne-mouth

Poole Isle of Wight

South-ampton

Ports-mouth

Dorset Hamp-shire

Study Area

GB

Economically active

84,700 (74.8%)

70,400 (78.7%)

63,000 (75.1%)

129,700 (73.7%)

115,500 (78.1%)

194,000 (80.7%)

678,600 (80.9%)

1,335,900 (81.3%) 76.9%

In employment

79,700 (70.3%)

66,700 (74.4%)

57,900 (69.0%)

120,300 (68.3%)

106,800 (72.3%)

183,800 (76.6%)

646,000 (76.9%)

1,261,200 (76.8%) 70.7%

Employees 67,000 (59.6%)

56,700 (63.7%)

47,400 (57.5%)

106,200 (60.7%)

93,900 (63.6%)

144,700 (62.4%)

548,100 (66.3%)

1,064,000 (64.8%) 60.6%

Self employed 12,300 (10.5%)

9,800 (10.4%)

10,300 (11.3%)

13,100 (7.1%)

12,100 (8.1%)

36,100 (13.6%)

94,000 (10.2%)

187,700 (11.4%) 9.6%

Unemployed 5,800 (6.7%)

3,700 (5.3%)

5,100 (8.1%)

10,100 (7.7%)

8,800 (7.6%)

10,200 (5.2%)

32,600 (4.8%)

76,300 (5.7%) 7.9%

JSA (2013) 4,033 (3.3%)

2,003 (2.2%)

3,852 (4.7%)

5,723 (3.5%)

5,294 (3.8%)

4,028 (1.7%)

16,291 (2.0%)

41,224 (2.5%) 3.8%

Economically inactive

27,700 (25.2%)

18,500 (21.3%)

20,100 (24.9%)

45,400 (26.3%)

31,900 (21.9%)

43,200 (19.3%)

153,100 (19.1%)

339,900 (20.7%) 23.1%

Wanting a job 5,800 (5.3%)

3,500 (4.1%)

4,300 (5.3%)

11,500 (6.7%)

10,600 (7.3%)

11,000 (4.9%)

40,800 (5.1%)

87,500 (5.3%) 5.8%

Not wanting a job

21,900 (19.9%)

14,900 (17.2%)

15,800 (19.6%)

33,800 (19.6%)

21,300 (14.6%)

32,300 (14.4%)

112,300 (14.0%)

252,300 (15.4%) 17.3%

Source: NOMIS 2013

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 13

Business Structure

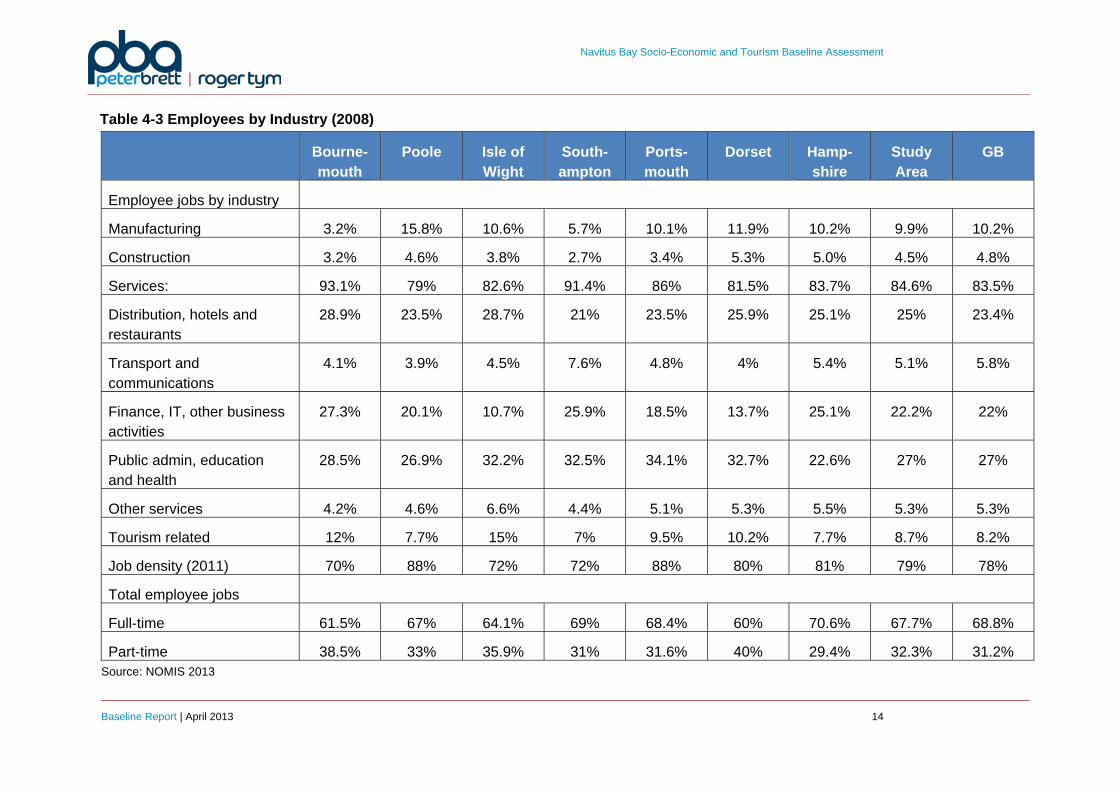

4.6 Table 4-3 illustrates employee jobs in industry type4. Poole has a strong manufacturing base with a significantly higher proportion of employee jobs in this sector compared to the study area as a whole and the national average. The proportion of those employed in manufacturing and construction across the study area is generally consistent with the national average.

4.7 Bournemouth has a particularly high concentration of service sector jobs, especially within the hotel and restaurant sector. This is unsurprising given its popularity as a tourism destination. Southampton also has a high proportion of service-related jobs, with particular concentrations around finance, IT, general business and the public sector. As a whole the study area has a greater proportion of service jobs compared to GB average.

4.8 Tourism is important to Bournemouth, the Isle of Wight, Portsmouth and Dorset, as each of these areas has a greater proportion of tourism-related employment compared to the study area as whole and the national average. Therefore, it is unsurprising that these same areas have a greater proportion of part-time jobs than the national average, given that tourism-related employment can be temporary and seasonal.

4.9 The job density5 figure in Poole and Portsmouth is high compared to the national average, indicating that employment opportunities are good in these areas. This also applies to the areas of Dorset and Hampshire. However, the number of jobs per resident aged 16-64 in Bournemouth, the Isle of Wight and Southampton is lower than the national average.

4 Note this data excludes self-employed, government supported trainees and HM Forces (source NOMIS 2012) 5 Job density measures the number of jobs (per resident aged 16-64) for every resident (also aged 16-64).

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 15

Employment Structure

4.10 The study area as a whole has a similar level of highly skilled workers as the national average. Both Hampshire and Dorset are characterised by a higher than average proportion of highly skilled workers. Whereas the Isle of Wight has a notably lower level of highly skilled workers compared to the rest of the study area.

4.11 In terms of skilled workers, every area, apart from Southampton and Hampshire, has a higher proportion than the national average. In particular, the areas of Bournemouth and the Isle of Wight have a high proportion of skilled trades people.

4.12 Southampton has a particularly high level of unskilled workers compared to the rest of the study area and Great Britain.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 16

Table 4-4 Employment Structure by Occupational Group (Jan 2012- Dec 2012)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 17

Qualifications and Skills

4.13 The proportion of people achieving the highest level of qualifications (HND, Degree and Higher Degree level qualifications) across the study area is slightly below the GB average, apart from Dorset and Hampshire which is above. Table 4-5 shows that Poole and the Isle of Wight have particularly low levels of those obtaining the highest qualifications. However, the proportion of people achieving some sort of qualification is relatively high across the study area, with low levels of people holding no qualifications compared to the national average.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 18

Table 4-5 Skills and Qualifications (Jan 2012 – Dec 2012)

Bournemouth Poole Isle of Wight

Southampton Portsmouth Dorset Hampshire Study Area

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 19

Gross Value Added (GVA) Output and Productivity

4.14 Table 4-6 shows that within the study area Hampshire has shown the greatest GVA growth (+60%) over the period 2001-2011, with the lowest growth in the period occurring in Southampton (+30%).

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 20

Table 4-6 GVA Total by Area – 2001- 2011 (£ million at current basic prices)

Bournemouth and Poole

Isle of Wight Southampton Portsmouth Dorset Hampshire Study Area UK*

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 21

Earnings

4.15 Average gross weekly pay for residents and full time (FT) workers in the study area are slightly lower relative to the national average (Table 4-7). The areas with the lowest gross weekly pay are the Isle of Wight and Southampton. These comparatively low wage rates are influenced by the lower than average proportion of highly paid, highly skilled occupations in each of these areas. Earnings in the Hampshire region exceed the study area and national averages.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 22

Table 4-7 Average Weekly Earnings by Place of Residence 2012

Bournemouth Poole Isle of Wight Southampton Portsmouth Dorset Hampshire Study Area

GB

Earnings by workplace FT workers £482.1 £485.6 £457 £466.3 £479.1 £480 £532.9 £483.29 £508

% of Study Area 100% 100% 95% 96% 99% 99% 110% 100% 105%

Source: NOMIS 2013

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 23

Business Health

4.16 VAT registrations and de-registrations offer a useful guide to the pattern of business start-ups and closures in an area, and are a useful indicator of the level of entrepreneurship and health of a business population.

4.17 The study area as a whole has shown strong growth in the number of VAT registered businesses since 2001, particularly in Poole. VAT registrations also surpassed de-registrations for the latest available data period for each of the authorities in the study area (Table 4-8).

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 24

Table 4-8 Business Health of VAT Registered Business (2007)

Bournemouth Poole Isle of Wight

Southampton Portsmouth Dorset Hampshire Study Area

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 27

Table 4-10 Drive time catchment data - substation

Mannington Substation

Drive time 30 Mins 45 Mins 60 Mins

Economically active (16-74 yrs) 238,791 572,965 851,783

Potentially available labour pool 11,517 25,726 35,726

Manufacturing and construction related workforce

35,035 84,328 131,620

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 28

Figure 4-1 Southampton Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 29

Figure 4-2 Portsmouth Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 30

Figure 4-3 Portland Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 31

Figure 4-4 Poole Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 32

Figure 4-5 Yarmouth Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 33

Figure 4-6 Mannington Substation Drive Time Catchment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 34

Summary

4.19 Bournemouth has an increasing population with a strong working age structure. It has an economic activity rate comparable to the national average. Service and tourism related employment is important in the area. The area is characterised with good educational attainment levels. However, average earnings in the area are below the national average.

4.20 The area around Poole has an economic activity rate which is above the national average and has a strong manufacturing base. Its employment structure is characterised as having an above average proportion of skilled labour. The area has relatively low levels of people achieving the highest levels of qualifications and its average wages are comparatively low.

4.21 The Isle of Wight is characterised by a low working age population, a below average economic activity rate and fairly low level of educational attainment. The service sector is an important employment sector in the area. There are an above average number of unskilled workers in the area. Average weekly pay in the area is low.

4.22 Southampton has a strong working age population with an economic activity rate lower than the national average. Service related employment makes up the majority of the jobs in the area particularly in the public sector. It has an above average proportion of unskilled workers. Educational attainment levels are comparatively low compared to national averages. GVA growth in the area has been relatively low.

4.23 Portsmouth has an increasing population with a good economic activity rate. Tourism related employment is important in the area. The area has an above average proportion unskilled workers. The area is characterised by a low proportion of people achieving the highest levels of qualifications. GVA growth between 2001 and 2011 has been at a rate greater than the UK average.

4.24 Dorset has a strong working age population with an above average economic activity rate. The job density rate in the area is also higher than the UK average. There are an above proportion of highly skilled and skilled workers in the area. Educational attainment levels are also relatively high. Average earnings however are below average.

4.25 Hampshire has an increasing population with a high economic activity rate. The job density rate in the area is high indicating that job opportunities are good. There is a higher than average proportion of highly skilled workers in the area. There are also high proportions of people achieving the highest levels of qualifications. GVA growth in the area is also high with workers receiving above average weekly wages.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 35

5 TOURISM BASELINE 5.1 The area with the potential to be impacted by the project includes parts of two sub-national

divisional areas, the most eastern part of the South West region and the most western part of the South East region. This section presents a tourism baseline profile of both regions. Where possible, local level data is used, focusing on the areas generally perceived to have the greatest potential for impact (beneficial and adverse). This includes the County Authority (CA) areas of Dorset, Hampshire; and the local authority (LA) areas of the Isle of Wight and Bournemouth and Poole. The baseline provides a thorough understanding of the tourism context in which the project is set.

5.2 This section provides an overview which details the volume and value of tourism, identifies significant tourism attractions, accommodation provision and sets out the tourism business density of the areas most likely to be affected (if at all) by the proposed wind farm and the presence of grid connections, including underground cable routing and associated substation infrastructure.

Regional Overview

South West

5.3 The South West of England has a diverse tourism profile with a range of activities and visitor attractions. The region covers about 9,200 square miles with a varied landscape, including rocky coastline and high moorland in the west to flat clay vales and chalk and limestone downland in the east.

5.4 Within the area there are two National Parks – Exmoor and Dartmoor, as well as four World Heritage Sites.6 There also 13 Areas of Outstanding Natural Beauty (AONB) including Dorset, the Cotswolds and the Quantock Hills. There are 50 National Nature Reserves across seven counties in the region, as well as six Registered Historic Battlefields including the Battle of Braddock Down.

5.5 The coastline of the South West totals 700 miles. Much of its coastline is protected. Such designations include World Heritage and Heritage Coast status. The region as a whole has high levels of legal coastal access in England.

5.6 There are a number of beaches in the South West region, with 25 having Blue Flag status (as of September 2012) offering visitors the chance to enjoy sandy beaches and access to clean and safe swimming waters. There are a number of key seaside destinations in the area including Bournemouth and Poole.

5.7 The area also has a significant amount of architectural attractions and traditions and includes a number of historic cities and towns.

6 Stonehenge, Avebury and Associated Sites, City of Bath, Cornwall and West Devon Mining Landscape and Dorset and East Devon Coast.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 36

South East

5.8 As with the South West, the South East region also has a varied mix of tourism activities and attractions, ranging from numerous historical buildings and natural features to theme parks and zoos. The region itself covers 7,373 square miles with over 990 miles of coastline, 45 miles of which is designated as heritage coast.

5.9 The area has numerous heritage sites, including two National Parks – The New Forest and the South Downs and two World Heritage sites7. It also has six Registered Historic Battlefields including the site of the Battle of Hastings and nineteen Protected Historic Wreck Sites including the 16th century warship of King Henry VIII's feet, The Mary Rose, which is located in the Solent near Portsmouth.

5.10 Some of the major attractions in the area include historic environment visitor attractions such as Canterbury Cathedral and Windsor Castle. There are also a number of theme parks including Thorpe Park (Chertsey) and Legoland (Windsor).

5.11 There are 18 Blue Flag beaches in the South East region including two on the Isle of Wight and 3 around Portsmouth.

Key Visitor Attractions and Activities

Regional Area

5.12 VisitEngland carries out a regular survey to determine the most popular visitor attractions in various regions across the country. Table 5.1 shows the top 10 paid and unpaid attractions in the South West and South East of England. The most popular attractions are the Moors Valley Country Park and Stonehenge in the South West and the flagship garden of the Royal Horticultural Society, RHS Garden Wisley, and Canterbury Cathedral in the South East.

5.13 The closest county authorities to the proposed wind farm are Dorset (located in the South West region) and Hampshire (South East region). One top ten paid attraction and two unpaid attractions in the South East are the located in Hampshire; none of which are within the 10 km coastal study area. None of the top ten paid or unpaid attractions in the South West are within the 10 km coastal study area around the project site. However, one attraction, the Moors Valley Country Park, is within close proximity (approximately 2.5 km) to the proposed cable route, although outside of the study area.

7 Blenheim Palace in Oxfordshire and a strip of sites in Canterbury (the Cathedral, St Augustine's Abbey and St Martin's Church.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 37

Table 5-1 Top 10 Paid and Unpaid Regional Attractions (Hampshire and Dorset Highlighted) (2011)

6. Grand Pier 350,000 6. Pitt Rivers Museum 245,773

7. Gloucester Cathedral 275,862 7. Brighton Museum and Art Gallery 235,894

8. Salisbury Cathedral 253,474 8. Royal Victoria Country Park 234,500

9. New Brewery Arts 253,000 9. Rochester Cathedral 234,371

10. Durlston Country Park National Nature Reserve

250,000

10. Itchen Valley Country Park (Southampton, Hampshire) 183,783

Source: South West and South East Top 10 Paid and Unpaid Visitor Attractions (2011)

Study Area

5.14 There is a wide variety of tourism attractions and activities in Bournemouth, Poole, Swanage, Christchurch, Isle of Wight, Wareham and the New Forest National Park and their surrounding areas.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 38

Bournemouth

5.15 There are 7 miles of beaches at Bournemouth including Durley Chine and Alum Chine. Four beaches in the area have Blue Flag status. These beaches all have access to safe clean bathing waters. Visitors are able to participate in watersports, go on boat trips, play volleyball and walk along one of the area’s numerous piers, the most famous being Bournemouth Pier, which has a theatre, a restaurant and a gift shop. Visitors can travel up and down cliffs at the beaches using the West and East Cliff lifts. People are able to move around the various beaches using the Land Train which runs along the promenade.

5.16 Bournemouth is also home to a number of other attractions. These include the Oceanarium, which is an award-winning aquarium that has a variety of marine life. Bournemouth has three gardens which play host to events and attractions during the summer months. Within the Lower Gardens, there is the Bournemouth Balloon, which offers riders a panoramic view of the English Channel and the surrounding area for up to 20 miles from the highest public observation point in Bournemouth. Tourists can visit built heritage in the area such as the historic Grade 1 listed Civic Church, St Peter’s. Bournemouth is also home to a variety of concerts and shows, with popular venues including the Bournemouth International Centre and Bournemouth Pavilion. There are also sightseeing tours and museums including the Russell Cotes Art Gallery and Museum.

Poole

5.17 Poole provides a number of tourist attractions and destinations, primarily focused around its coast (self-proclaimed as the ‘Coast with the Most’). It has the world’s second largest natural harbour and Poole Quay offers views of its miles of beaches. As with Bournemouth, there are four beaches with Blue Flag status and ample opportunities for watersports such as surfing and sailing. There are also numerous boat trips and charters including the Poole Sea Safari and Sea Events (Boat Charter). Activities ashore include, visiting museums such as the Poole Museum and the Poole Old Lifeboat Museum and Shop. There are theme park attractions such as the water theme park Splashdown and located just outside the town is Farmer Palmer’s Farm Park, which caters for the under 8’s. Other attractions in Poole include Ginger Pop, an attraction focused around the works of Enid Blyton. Located just outside Poole is Upton Country Park, where visitors can go on guided walks around the grounds. Another popular visitor attraction nearby Poole is Brownsea Island, where there is a nature reserve and a castle. It is also the birthplace of the Scouting and Guiding movement and there is a Baden-Powell Outdoor Centre. There are opportunities for visitors to the island to take in views of the Purbeck Hills.

Swanage

5.18 Outside Poole and Bournemouth, there are other important visitor attractions. At Swanage there are two nature reserves and a heritage centre. The Purbeck coast path also passes through it. Swanage Pier is another key attraction, where there are steamer sailings. There is also the Swanage Railway, which allows visitors to travel in heritage steam engine locomotives. Situated just outside Swanage, is the Durlston Country Park and nature reserve. It is part of the Jurassic Coast World Heritage Site, and provides scenic views, numerous walking trails and a wide variety of habitat including cliffs, downs and woodland.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 39

It is also home to the historic Anvil Point Lighthouse and one of the largest stone spheres in the world, The Great Globe.

Christchurch

5.19 At Christchurch, attractions include visiting the remains of Christchurch Castle, and a number of museums including the Museum of Electricity. There is also the Adventure Wonderland theme park.

Isle of Wight

5.20 Needles Park provides various attractions including rides, a chairlift to the beach, glassmaking crafts, a sweet factory, kid’s activities and shopping and eating outlets. There are also a number of historical attractions and museums such as the Brighstone Village Museum, The Heritage Attractions, Tennyson Monument. Children’s activities include The Dinosaur Isle, Britain's first purpose built dinosaur museum and visitor attraction.

Wareham

5.21 In Wareham, one of the major attractions is the thousand year old Corfe Castle. It offers visitors the chance to enjoy views across Purbeck. There are walks around the castle as well as a model village which depicts the Castle and village as it was in 1646. Other attractions in Wareham include the Tank Museum and the Purbeck Information and Heritage Centre.

New Forest National Park

5.22 Another key attraction is the New Forest National Park where there a multitude of attractions and activities8. Within the park are museums such as the Beaulieu National Motor Museum. There are a number of parks and gardens, including Exbury Gardens where there is a steam railway. Visitors can visit historic buildings such as Beaulieu Abbey as well as look at wildlife and nature at locations such as the Liberty's Owl Raptor and Reptile Centre and The New Forest Wildlife Park. Paultons Family Theme Park is situated close to the eastern edge of the New Forest National Park. This includes Peppa Pig World which opened in recent years and is specifically aimed at younger children.

5.23 Within the New Forest District lies the Port of Lymington, which is well known for sailing. It hosts a number of world famous regattas such as the Royal Lymington Cup and the Source Regatta. The town also holds a number of major keelboat and dinghy events.

5.24 On the southern edge of the New Forest District there are a number of small seaside villages such as Barton on Sea and Milford on Sea, which offer picturesque views across to the Isle of Wight.

Accommodation Stock

5.25 In 2010 VisitEngland carried out an accommodation stock audit in both the South West and South East of England. The audit determines the number of serviced establishments

8 It should be noted that sections to the north of National Park in Wiltshire are not included in study area and are therefore not included in this assessment

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 40

versus the number of non-serviced establishments in the area and also specifies the number of bed spaces contained within these establishments.

South West

5.26 The majority of serviced accommodation provision is located within Dorset and Somerset. However, in general there is a fairly even split across the South West areas. In terms of non-serviced establishments, over two-thirds are found in Cornwall, the Isles of Scilly and Devon. A fifth is found in Dorset and Somerset, whilst only small proportion is found in the Gloucestershire, Wiltshire and Bristol/Bath area.

5.27 Table 5-2 shows that in terms of the number of serviced bed spaces, nearly a third of the stock (31%) is found in Dorset and Somerset. Whilst for non-serviced bed spaces the majority is found in Cornwall and the Isles of Scilly (36%).

5.28 Dorset and Somerset are well represented with serviced and non-serviced accommodation providers and bed spaces, indicating their popularity and importance as a tourist destination.

Table 5-2 Serviced and Non-Serviced Accommodation Bed Space Provision in South West of England 2010

Dorset and Somerset

Gloucestershire, Wiltshire and

Bristol/Bath area

Cornwall and Isles of Scilly Devon

South West

Number of Serviced establishments

2,348 1,423 1,551 1,716 7,038

% of South West Total

33% 20% 22% 24%

Number of serviced bed spaces

57,899 51,351 30,677 27,352 187,085

% of South West Total

31% 27% 16% 25% -

Number of non-serviced establishments

2,575 862 4,478 4,691 12,606

% of South West Total

20% 7% 36% 37% -

Number of non-serviced bedspaces

193,659 53,476 236,004 127,994 635,356

% of South West Total

30% 8% 37% 24% -

Source: South West of England Regional Summary (VisitEngland, 2010)

South East

5.29 Approximately a quarter (27%) of the serviced accommodation provision is located within Hampshire and the Isle of Wight, with the majority being found in Surrey, East and West Sussex. However, in terms of non-serviced accommodation, Hampshire and the Isle of Wight have a far greater share (42%) than the other counties. This suggests that self-catering type accommodation is popular in these areas.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 41

5.30 Table 5-3 shows that in terms of serviced bed spaces, 25% of the region’s stock is found in Hampshire and the Isle of Wight. These areas also have the largest share of non-serviced bed spaces at just over a third (36%).

Table 5-3 Serviced and Non-Serviced Accommodation Bed Space Provision in South East of England 2010

Hampshire and Isle of

Wight

Berkshire, Buckinghamshire and Oxfordshire

Surrey, East and

West Sussex Kent

South East

Number of Serviced establishments

1,776 1,614 2,010 1,141 6,541

% of South East Total

27% 25% 31% 17% -

Number of serviced bed spaces

54,560 61,706 72,365 33,139 221,770

% of South East Total

25% 28% 33% 15% -

Number of non-serviced establishments

1,728 366 1,175 871 4,140

% of South East Total

42% 9% 28% 21% -

Number of non-serviced bed spaces

87,756 32,198 78,838 43,138 241,930

% of South East Total

36% 13% 33% 18% -

Source: South East of England Regional Summary (VisitEngland, 2010)

Tourism Volume and Value

Domestic Trips, Nights and Spend

5.31 The volume and value of domestic tourism in the South West is far greater than that of the South East (Table 5-4). Overall both regions have not seen any major changes in their domestic tourism figures between 2007 and 2011. This shows the relative popularity of both these regions, to perform consistently in the current economic climate. The recession and the advent of more people choosing to holiday in the UK may have helped these regions.

5.32 Dorset accounts for just over 16% of the South West of England region’s domestic tourism and value9. Domestic tourism in Dorset has remained generally stable. There have been small reductions in average annual trips (-2%), nights (-4%) and spend (-2%) between the 2007 to 2009 and 2009 to 2011 periods.

9 The South West region is made up of the following sub-regions: Cornwall, Devon, Dorset, Somerset, Bristol, Gloucestershire and Wiltshire.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 42

5.33 Hampshire makes up approximately 20% of the South East region’s domestic tourism and value10. As with Dorset, the area’s performance has remained relatively consistent, with small percentage decreases recorded in average trips, nights and spend between the reporting periods of 2007-09 and 2009-11.

5.34 The Isle of Wight performance has also seen modest increases in these areas over the same time period. The average annual spend in the Isle of Wight is relatively high given its size, as it accounts for nearly 10% of the South East’s total spend.

5.35 At a local level, Poole, Purbeck and Bournemouth make up approximately 5-10% of the South West’s tourism and value. Whereas these areas account for nearly 50% of Dorset’s tourism and value. Bournemouth is the most popular destination in Dorset for domestic tourism, with 30% of Dorset’s annual trips and spend coming from the seaside town. Despite its popularity, between the reporting periods of 2007-09 and 2009-11, Bournemouth has seen a fall in its number of trips (-2%) and nights (-4%). Over the same time period, Poole has also seen its tourism and value figures reduced. Purbeck has experienced a distinct reduction in its number of trips (-17%), nights (-23%) and spend (-11%).

10 The South East region is made up of the following sub-regions: Berkshire, Buckinghamshire, East Sussex, Hampshire, Isle of Wight, Kent, Oxfordshire, Surrey and West Sussex

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 43

Table 5-5-4 Tourism – Domestic Trips, Nights and Spend (3- Year Averages)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 44

Overseas Visitor Trips

Number of Trips

5.36 Figure 5-1 shows that in terms of overseas tourism trips, Hampshire destinations are more popular relative to Dorset and the Isle of Wight. In relation to the South East of England, Hampshire accounted for 15% of trips in 2011, whilst the Isle of Wight contributed 1%.16% of overseas trips to the South West were to Dorset.

5.37 Between 2003 and 2011, overseas trips to Hampshire have fluctuated, from a low of 500,000 trips in 2005 to a high of 670,000 trips in 2006. Recent trends have shown an increase in trips to the area, whereas figures for Dorset and the Isle of Wight for the same period have remained fairly stable and consistent.

Figure 5-1 Overseas Trips (000’s)

Source: Overseas Tourism in UK Countries/Regions 2011 (VisitBritain, 2011)

Purpose of Visit

5.38 Trip purpose is detailed in Table 5-5, with the majority of overseas visits from those either on holiday or visiting friends or relatives.

Table 5-5 Purpose of Overseas Visits (000’s) (2011)

Holiday VFR* Business Other Study Dorset 164 (49%) 103 (31%) 41 (12%) 8 (2%) 19 (6%) Hampshire 204 (33%) 254 (41%) 133 (21%) 24 (4%) 11 (2%) Isle of Wight 27 (44%) 28 (46%) 4 (7%) 0 (0%) 2 (3%) South West 880 (42%) 739 (35%) 347 (17%) 71 (3%) 52 (2%) South East 1,422 (33%) 1,590 (37%) 933 (22%) 246 (6%) 112 (3%)

Source: Office for National Statistics. International Passenger Survey 2011

*VFR – Visiting friends and relatives

0

100

200

300

400

500

600

700

800

2003 2004 2005 2006 2007 2008 2009 2010 2011

Dorset

Hampshire

Isle of Wight

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 45

Overseas Visitor Nights

Number of Nights

5.39 In terms of overseas nights, as with trips, Hampshire counted for the majority in comparison with Dorset and the Isle of Wight. However, in 2011 Hampshire only accounted for 14% of the South East’s overseas nights. Whilst Dorset accounted for 17% of the South West figure.

5.40 Both Hampshire and Dorset have experienced fluctuations in overseas nights between 2003 and 2011 (Figure 5-2). The biggest change was noted in Dorset which saw a 65% increase from 2.6 million nights in 2005 to 4.3 million nights in 2006. This correlates to the 12% increase in overseas trips seen during the same time period. Hampshire also saw a large increase (43%) from 3.9 million nights in 2005 to 5.6 million trips in 2006. However, both these areas have seen reductions in overseas nights spent between 2009 and 2010 (Dorset -22%, Hampshire -17%) which can be explained by the current financial situation, with people having less disposable income for overseas trips. However, both Dorset and Hampshire have increased since 2010.

5.41 The Isle of Wight, however, has appeared to be relatively unaffected by the current financial climate in terms of overseas nights spent, as its figures have remained fairly consistent between 2003 -10.

Figure 5-2 Overseas Nights (Millions) (2011)

Source: Overseas Tourism in UK Counties/Regions 2011 (VisitBritain)

Accommodation Used

5.42 Table 5-7 shows that the majority of these nights, as with visits, were spent free at friends’ or relatives’ accommodation. A significant number of nights were also spent in hotel accommodation, for all the areas concerned. These trends are generally consistent with those seen at the wider England level.

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2003 2004 2005 2006 2007 2008 2009 2010 2011

Dorset

Hampshire

Isle of Wight

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 46

Table 5-6 Accommodation Used for Overseas Nights (000’s) (2011)

Dorset Hampshire

Isle of Wight

South West

South East

England

Free guest with relatives or friends 1,200 (41%) 2,504 (53%) 386 (62%)

8,380 (48%)

15,903 (48%)

53,739 (26%)

Hotel/guest house 223 (8%) 709 (15%) 96 (15%)

2,512 (14%)

5,251 (16%)

98,257 (47%)

Paying guest family or friends house 71 (2%) 93 (2%) 10 (2%)

Source: Office for National Statistics. International Passenger Survey 2011

Overseas Visitor Spend

Amount Spent

5.43 Figure 5-3 details the value of overseas tourism 2003-2011 in the region. As to be expected, given the greater number of visits and nights spent, Hampshire has secured a significant amount of spend across the study area. In 2011 across the South East region Hampshire accounted for 13% of its overseas spend. Whilst the Isle of Wight made up only 1.7%. Nearly a fifth of overseas spend in the South West in 2011 was taken from Dorset. This highlights the importance of Dorset a key tourist destination in the South West.

5.44 Dorset, Hampshire and the Isle of Wight have seen recent increases in overseas spend. Between 2010 and 2011 overseas spend in Hampshire increased by 30%. Overseas spend in Isle of Wight has doubled between 2010 and 2011, indicating that it is becoming an increasingly popular destination for overseas tourists.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Source: Overseas Tourism in UK Counties/Regions 2011 (VisitBritain)

Where Money is Spent

5.45 Table 5-8 illustrates the origin of spend by type of accommodation. The majority of spend for all areas originates from either visitors staying free with friends or relatives or those staying in hotels. These figures are not surprising given the similar trends recorded for overseas visits and nights spend. Again these figures are broadly similar to the total all England figures, where nearly 80% of revenue has come from those residing free with friends or relatives or from people staying in hotels.

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2003 2004 2005 2006 2007 2008 2009 2010 2011

Dorset

Hampshire

Isle of Wight

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 48

Table 5-7 Full Year Accommodation Usage Figures for 2011 – Spend (£ million) – Staying Visitors

Source: Office for National Statistics. International Passenger Survey 2011

Overseas Activities

5.46 The International Passenger Survey (ONS, 2011b) is carried out annually and in it visitors to the UK are asked what activities they undertake whilst visiting. The top three most popular things to do in the South West of England were ‘eating in restaurants’, ‘going to a pub’ and ‘shopping for clothes and accessories’. Visiting the countryside was one area that makes the South West stand out from other regions, with over of third of respondents enjoying this activity. Built heritage was also a key draw for visitors, with a third going to see famous buildings or monuments. Less prominent activities include golf, researching ancestry and visiting spa/beauty centres.

5.47 Similar results were found in the South East of England, where again ‘eating in restaurants’ was the most popular activity. After this shopping for clothes/accessories was the second most popular choice of activity. ‘Going to the Pub’ and ‘Socialising with the locals’ were also common activities for many. As with the South West, visiting built heritage and going to the countryside were other popular draws.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 49

6 COASTAL TOURISM PROFILES 6.1 The preceding chapter outlined visitor statistics for the region and sub-region acquired from

VisitEngland and VisitBritain. The following section refers to bespoke visitor profiles for the coastal area. These profiles also provide estimates of volume and value which can be overlaid with the VisitEngland and VisitBritain data and provide useful visitor profile information.

Isle of Wight

6.2 The Isle of Wight, situated 2.5 miles off the coast of Hampshire, is England’s largest island spanning some 150 square miles. The island has been a popular visitor destination since the Victorian era and regularly attracts around 2.5 million visitors each year.

6.3 The tourism industry employs around 15% of the island’s workforce and is one of the island’s main industries. A number of music festivals such as the Isle of Wight International Jazz Festival and the Isle of Wight (rock music) Festival add to the island’s visitor appeal. The Isle of Wight Walking Festival also attracts approximately 24,000 participants over a 2 week period in May making it one of the largest walking festivals in the UK. The island also has an extensive cycle path network and coastal paths to capitalise on the island’s attractive natural environment.

6.4 The Isle of Wight Tourism Activity Monitor report provides insight on the Isle of Wight’s tourism industry during 2010-2011.

Volume and Value

6.5 Table 6-1 shows that total tourist visits per annum fell slightly in 2010/11 (4%). However they have remained relatively stable over the last 4 years at around 2.5million per annum. Domestic visits account for around 9 out of 10 tourist visits (95%). Overall domestic visits fell recently (2%) as did overseas visitor numbers which notably decreased (-31%).

Overseas visitors p.a. 122 176 123 120 122 Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.6 Overall visitor expenditure slightly reduced in 2010/11 by 0.3% compared to 2009-10. The domestic staying visitor market accounts for over three quarters (83%) of the total value of the Isle of Wight’s visitor market. Day trippers and overseas visitors account for around 10% each.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 50

Table 6-2 Value of Tourism (£million)

2010/11 2009/2010 % change

Day trip £35m £41m Domestic staying trip £336m £317m Overseas staying £30m £45m Total £402m £403m -0.3%

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.7 The preferred method of travel on the island is by private car, as visitors are more likely to travel with their car to the island and use it to travel around (Table 6-3). The proportion of people choosing to walk on foot has increased by over 10% since 2009/10.

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.8 Nearly half (43%) of domestic visitors surveyed were visiting the island for holiday. The majority of which were additional holidays to their main holidays (37%). The domestic business day trips to the island accounted for over a tenth of total domestic trips.

6.9 In terms of overseas trips nearly a third were visiting on holiday. Moreover, a relatively high proportion (30%) visited friends or relatives. Over a quarter of overseas trips were day trips whilst on holiday.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 51

Table 6-4 Purpose of Trip 2010/11

Domestic Trips % Overseas Trips %

Overnight Main holiday 6% 6% Other holiday/leisure 37% 25% Visiting friends and relatives (overnight) 16% 30% Business (overnight) 3% 4% Leisure and business (overnight) 0% 1% Other (overnight) 1% 1% Day Day from home 12% 5% Day on holiday 4% 26% Visiting friends and relatives (day) 7% 4% Business (day) 13% 1% Other (day) 2% 0%

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.10 Staying at the home of a friend or a relative is the most popular type of accommodation used by overnight visitors (37%). This may be related to the current recession with visitors trying to find more cost-effective forms of accommodation. Staying in hotel accommodation is the second most popular accommodation (Table 6-5). Staying in self-catering accommodation or static caravan/ chalets account for around a fifth of all accommodation. The island also has a notable proportion of visitors visiting their second home on the island (6%).

Table 6-5 Type of Accommodation used by Overnight Visitors (2010/11)

Accommodation Type

% Home of a friend or relative 37% Hotel 23% Rented Self-catering 10% Static caravan or chalet 4% Touring caravan or tent 11% Guest House or bed and breakfast 6% Second home 6% On-board a yacht/ boat 1% Other type of accommodation 1%

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.11 Germany, France and the U.S.A account for the majority of overseas visitors to the island. Visitors from Spain have increased in recent years while the number of visitors from the Netherlands has declined.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 52

Table 6-6 Origin of Overseas Visitors

2010/11 2009/10

Germany 13% 10%

France 10% 15%

U.S.A 10% 9%

Spain 9% 4%

Australia 7% 8%

Belgium 7% 1%

Rep. of Ireland 5% 1%

Netherlands 5% 8%

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.12 Over half (53%) of domestic day visitors come from Hampshire which is unsurprising given its relatively close proximity. Nearby Dorset to the west and West Sussex; Surrey and London to the east account for around 5% each.

Table 6-7 Origin of Domestic Day Visitors

2010/11 2009/10

Hampshire 53% 52%

Dorset 7% 6%

West Sussex 5% 5%

Surrey 5% 5%

London 4% 5%

East Sussex 2% 2%

Wiltshire 2% 2%

Kent 2% 2% Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.13 The domestic staying visitor market is more fragmented attracting a greater proportion of visitors from further afield. Visitors from Hampshire still account for the majority of staying visitors however visitors from London and Surrey are also well represented.

Table 6-8 Origin of Domestic Staying Visitors

2010/11 2009/10

Hampshire 19% 18%

London 14% 13%

Surrey 9% 9%

West Sussex 5% 4%

Kent 4% 4%

Essex 4% 4% East Sussex 3% 3% Dorset 3% 3%

Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 53

6.14 There has been a decline in the proportion of tourists visiting a tourist attraction during their stay. 40% reported visiting a tourist attraction during their time on the island which is 11% lower than the previous year.

Table 6-9 Visits to Attractions

2010/11 2009/10 2008/09

% of all tourists visiting attractions

40% 51% 44%

Free 12% 15% 13%

Paid for 28% 36% 31% Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

6.15 The Isle of Wight has a high level of repeat visits particularly from visitors who returned within the last 12 months. This suggests a high level of satisfaction with the area’s tourism offer.

Table 6-10 Repeat Visitors 2010/2011

%

First visit 12%

Visited in last 12 months 62%

Visited 2-5 years ago 17%

Visited 5+ years ago 9% Source: Isle of Wight Tourism Activity Monitor Visitor statistics for tourism year (2010/2011)

New Forest

6.16 The New Forest District Council area sits between the Solent and east Dorset, and contains the majority of the New Forest National Park – which primarily covers areas in Hampshire but also extends north into Wiltshire; with a mix of forest, heathland and unenclosed pasture land. Villages and small towns are spread throughout the park boundary.

6.17 The New Forest was awarded National Park status in 2005 to conserve and enhance the area’s outstanding natural beauty, wildlife and cultural heritage. The Park covers 220 square miles and lies between the conurbations of Bournemouth and Southampton. It is bounded by the River Avon to the west and The Solent to the south.

6.18 The 2008 Economic Impact of Tourism in the New Forest (Tourism South East, 2008) outlines the tourism volume and value of the district council area.

Volume and Value

6.19 7.2 million day trips were made to the New Forest in 2008, which represented a slight rise (2.9%) in visitor numbers since 2006. Associated visitor expenditure marginally increased (2.4%) and now stands at around £278 million.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 54

Table 6-11 Tourism Day Trips and Spend

Trips Spend

Total 2008 7,175,000 £277,755,000

Total 2006 6,975,000 £271,231,000

% change 2.9% 2.4% Source: The Economic Impact of Tourism New Forest (Tourism South East, 2008)

6.20 Almost 900,000 overnight trips were made in 2008 the vast majority (92%) from domestic tourists. However overseas visitors account for 17% of total overnight expenditure despite only accounting for 8% of total overnight visitors.

Table 6-12 Tourism Overnight Trips and Spend

Overseas

Trips

Spend

Domestic

Trips

Spend

Total 2008 801,800 £135,093,000 69,300 £27,286,000

Total 2006 823,000 £127,109,000 70,000 £26,887,000

% change -2.6% 6.3% -1% 1.5% Source: The Economic Impact of Tourism New Forest (Tourism South East, 2008)

6.21 The majority of domestic visitors stay in serviced accommodation (26%) such as hotels while around a quarter of visitors (24%) stay with friends or relatives. Touring caravans/ tents (22%) and static caravans/ tents (19%) also make up a sizable proportion of domestic tourists’ visitor accommodation.

6.22 A larger share of overseas tourists stay with friends and relatives (33%) and self-catering accommodation (9%) relative to domestic visitors. Serviced accommodation still accounts for around 1 in 4 accommodation types favoured by overseas tourists. Caravan and tent accommodation is also less favoured by overseas visitors.

Table 6-13 Accommodation type used (2008)

UK Overseas Total

Serviced 26% 25% 26%

Self-catering 5% 9% 6%

Touring caravans/ tents 22% 13% 21%

Static caravans 19% 12% 18%

Group. Campus 0% 0% 0%

Second homes 1% 3% 1%

Boat moorings 2% 0% 1%

Other 1% 4% 1%

Paying guests 0% 0% 0%

Staying with friends and relatives 24% 33% 25% Source: The Economic Impact of Tourism New Forest (Tourism South East, 2008)

6.23 Day visitors spend most of their expenditure on food and drink (42%) and shopping (25%). Domestic overnight and overseas overnight visitors’ expenditure is spread more evenly between accommodation, shopping and food and drink.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 55

6.24 The day visitor market is worth almost two thirds (63%) of the New Forest’s overall visitor market; overnight domestic market is worth around a third (31%). The overnight overseas tourism market is worth 6% in total.

Table 6-14 Sector Breakdown of Visitor Expenditure (2008)

UK touristsOverseas tourists

Sub-Total Tourist

day visits

Total

£m Accommodation £41.0 £7.4 £48.4 £0.0 £48.4

Shopping £25.3 £8.0 £33.2 £69.8 £103.0

Food and drink £29.8 £6.0 £35.8 £117.1 £152.9 Attractions/ entertainment

Source: The Economic Impact of Tourism New Forest (Tourism South East, 2008)

Dorset

6.25 Dorset is located in South West England and covers an area of 1,000 square miles bordering Hampshire to the east, Wiltshire to the north-east, Somerset to the north-east and Devon to the south-west. Bournemouth-Poole accounts for almost half of Dorset’s population. The area beyond this is primarily rural and has a low population density.

6.26 Tourism is a key employer and major driver of Dorset’s economy, especially in the coastal areas. The Dorset Visitor Study (2009) provides detailed information on the profile of tourists visiting Dorset; their main motivation for visiting the area and their origin and expenditure patterns.

Domestic

6.27 Over half (57%) of domestic visitors are from the immediate South East and South West area. London and the West Midlands account for around 10% (9% and 8% respectively). Visitors from Wales, Scotland and Northern Ireland only account for 6% of all domestic visits.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 56

Table 6-15 UK Visitor Origins (2009)

% South East 29% South West 28% London 9% West Midlands 8% North West 6% East Midlands 6% North East 6% Wales 3% East Anglia 2% Scotland 2% Northern Ireland 1%

6.28 Germany and Holland make up the largest share of the area’s overseas visitors market (19% and 18% respectively). Ireland also accounts for a notable share (9%).

Table 6-16 Overseas Visitor Origin (2009)

% Germany 19% Holland 18% Ireland 9% USA 6% Italy 6% France 6% Poland 5% Guernsey 5% Canada 5% Australia 5% Spain 4% Belgium 4% Switzerland 3% Jersey 3% Rest of World 6%

6.29 Bournemouth is the most popular destination in Dorset accounting for 1 in 4 trips (25%). The Weymouth and Portland area was the second most popular destination (16%). The coastal areas of Christchurch and Poole were two of the least popular destinations in Dorset (8% and 4% respectively).

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 57

Table 6-17 Visitor Destinations (2009)

% Bournemouth 25% Weymouth and Portland

16%

West Dorset 13% Purbeck 12% Outside Dorset 12% East Dorset 10% Christchurch 8% Poole 4% North Dorset 2%

6.30 The majority of visitors to Dorset travel a significant distance to visit the region. Over half (56%) travel at least 100 miles which indicates the area has a strong appeal and is a good tourism product.

Table 6-18 Distance Travelled (2009)

% 200 miles + 27% 100-190 miles 38% 50-90 miles 16% 25-49 miles 14% 1-24 miles 5%

6.32 Visiting the seaside, beaches and coastal area was the main motivation for domestic trips to Dorset (22%). Visiting friends and relatives was also a common reason for visiting (19%).

6.33 Over a third (35%) of overseas visitors were visiting friends and relatives in the area, while around a quarter (24%) wanted to visit somewhere they had not been before.

Table 6-20 Main Motivation for Visiting the Area (2009)

UK Overseas

Visited the area before 20% 10%

Visiting friends and relatives 19% 35% Wanted to go somewhere they had not been before

10% 24%

Seaside, beaches, coast 22% 6%

Scenery and countryside 5% 1%

Recommended by friends 4% 7%

Local visitor attractions 4% 9%

Easy to get to 2% 1%

Peace and quiet 1% 1%

Good shopping facilities 0% 0%

Cultural heritage 2% 6%

Sporting activities 4% 0%

An event of festival 8% 4%

Trying local food 0% 0%

World heritage site 4% 3% Source: Dorset Visitor Survey 2009 (Bournemouth, University, 2010)

6.34 Over 90% of visitors rated the availability, quality, standard and service in Dorset accommodation to be either good or very good.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

6.35 The average number of visitor nights spent in Dorset has steadily declined since 2007. In 2009 on average visitors spent around 6.7 nights in Dorset compared to 7.7 nights in 2006. People spend the least number of nights in Bournemouth (5.7 nights) and stay the most number of nights in East Dorset (7.3 nights).

6.36 Around a third (32%) of visitors stay in hotel accommodation. A further 22% stay in mobile accommodation such as a campervan; tent or touring caravan.

Table 6-23 Accommodation (2009)

%

Hotel 32%

Guest House/ bed and breakfast 8%

Self-catering 11%

Static caravan 6%

Campervan/ mobile 7%

Holiday park 3%

Touring caravan/ tent 15%

Home of a friend 13%

Second home 1%

Other 4%

Navitus Bay Socio-Economic and Tourism Baseline Assessment

6.38 The language school market in Bournemouth and Poole is estimated to generate 36,000 trips, 1.3million bed nights and an overall spend of £130m11.

6.39 Conferences in Bournemouth and Poole are estimated to generate 353,000 trips, 371,000 nights, generating an estimated spend of £123.8m12.

Coastal Tourism Summary

6.40 Bournemouth, Poole, Christchurch, Swanage and parts of the Isle of Wight and New Forest have high concentrations of tourism related businesses, while all of the coastal authorities (with the exception of Poole) have above average tourism related employment.

Isle of Wight

6.41 The Isle of Wight has a relatively steady number of visitors each year (c.2.5m). Its visitor market is heavily reliant on domestic staying visitors. Almost half (43%) of domestic visitors were on holiday trips. The day trip market is mainly locally based with over half of visitors’ travelling from neighbouring Hampshire. The domestic overnight market attracts visitors from a wider geographic area. The Isle of Wight is also characterised by a high level of repeat visitors with over a third of all visitors visiting a paid or unpaid attraction.

New Forest

6.42 The New Forest National Park is growing in popularity and now attracts around 8 million visitors per annum. Day trips account for the majority of visits however overseas visitors are also extremely valuable. Overseas tourists, while only accounting for 8% of total overnight visitors, accounts for 6.3% spend.

Dorset

6.43 Dorset (including Bournemouth; Poole and Christchurch) has a strong visitor appeal with the majority of visitors travelling over 100 miles. According to visitors Dorset also offers a

11 Team, 2008, Bournemouth and Poole Tourism Strategic Framework; based on 2005 data 12 Team, 2008, Bournemouth and Poole Tourism Strategic Framework; based on 2005 data

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 61

high level of accommodation. However the average number of nights has steadily fallen since 2007. The immediate South East and South West area make up the majority of the domestic visitor market. Visiting the beaches and staying with friends and relatives was the main visitor incentive for domestic and overseas tourists respectively. Conference and language school markets are important parts of the Bournemouth and Poole tourism market.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 63

7 ONSHORE CABLE ROUTE AND SUBSTATION 7.1 Site visits have been used to establish the tourism businesses and destinations alongside

the route of the onshore cable and around the substation at Mannington, within the 2 km zone around the cable route and substation. In addition to the potential impacts common to other tourism businesses across the study area, these locations may be affected by additional impacts from the construction and decommissioning phases, such as obstruction, or other effects such as noise or traffic.

7.2 Figure 7-1 notes the businesses identified and their location.

7.3 The cable route comes onshore between Barton-on-Sea and Milford on Sea. The underground cable route goes past Hordle, around New Milton, and passes Hinton, Sopley and Avon before heading through West Moors to the substation site in Three Legged Cross. The first half of the cable route is located underground in Hampshire and the second half is within Dorset.

7.4 Tourist attractions in proximity to the proposed cable route include Snowtrax Ski Centre and Matchams Karting Centre. The route also runs nearby various walking and cycling route including a number of rights of way and National Cycling Route 2.

7.5 It is also noted that the cable route runs through a number of small towns or villages without tourist attractions.

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 64

Figure 7-7-1 Tourism Businesses and Destinations along the Cable Route and Substation

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 65

8 TOURISM BUSINESS DENSITY BY AREA 8.1 Table 8-1 shows the number of tourism related businesses13 located along a 5 km and

10 km coastal strip and within 15 km of the proposed substation (see Figure 8-1 overleaf).

8.2 The proportional split between tourism business types is broadly similar across each of the three geographic areas. Restaurants account for approximately half of all tourism related businesses. Hotels account for between 13 and 17%, while sporting activities account for between 14 and 18%.Three quarters (76%) of tourism related businesses within the 10 km strip of the coastal are located within the core 5 km coastal strip.

Table 8-1 Tourism Business Density (200814) Geographic area

Hotels Camping sites and other

provision of short-stay

accommodation

Restaurants Sporting activities

Other recreational

activities

TOTAL

5 km coastal area

192 90 617 159 105 1,163

10 km coastal area

249 141 764 248 135 1,537

15 km from substation

164 74 659 214 109 1,220

% OF TOTAL

5 km coastal area

17% 8% 53% 14% 9% 100%

10 km coastal area

16% 9% 50% 16% 9% 100%

15 km from substation

13% 6% 54% 18% 9% 100%

Source: ONS ABI (2012)

8.3 Figure 8-1 shows the concentration of tourism related businesses in the study area. Bournemouth, Poole, Christchurch, Swanage, and parts of the Isle of Wight and New Forest have notably high tourism business densities which is unsurprising given their role as visitor destinations and tourism centres.

13 By broad classification type 14 Latest data available

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 66

Figure 8-1 Tourism Business Density Map (2008)

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 67

Tourism Businesses by Area

8.4 Using data received from Experian, the make-up of tourism businesses located in key towns within proximity of the project can be identified.

Bournemouth

8.5 In Bournemouth there are an estimated 664 tourism-related businesses. The majority (45%) are either restaurants or cafes. Over a fifth are hotels or similar accommodation providers. There are also a number of pubs and bars as well as a variety of businesses which provide sporting activities such as sailing and leisure centres. Other activities include paintballing and ten-pin bowling.

Figure 8-2 Tourism Businesses in Bournemouth

Source: Experian

Poole

8.6 Out of the estimated 294 tourism businesses in Poole, nearly half are restaurants and cafes. There are also over 60 pubs and bars as well as accommodation providers such as holiday parks, bed and breakfast establishments (B&Bs) and guesthouses. There are a number of maritime related businesses such as those which provide boat trips and jet ski experiences.

0

50

100

150

200

250

300

350

Hotels and similar

accommodation

Other Accommodation

Restaurants and Cafes

Pubs and Bars Sporting Acivities

Other Activities

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 68

Figure 8-3 Tourism Businesses in Poole

Source: Experian

Christchurch

8.7 The historic town of Christchurch, which lies between Bournemouth and the New Forest, accommodates around 135 tourism businesses, the majority of which are restaurants and cafes. The area has a wide range of accommodation providers, from traditional hotels to camping parks. Pubs and bars are also well represented. Other attractions include historic Grade I listed buildings and children’s theme parks.

Figure 8-4 Tourism Businesses in Christchurch

Source: Experian

0

20

40

60

80

100

120

140

160Numberof Businesses

0

10

20

30

40

50

60

Number of Business

Navitus Bay Socio-Economic and Tourism Baseline Assessment

Baseline Report | April 2013 69

Swanage

8.8 Just over a third of Swanage’s 99 tourism businesses are made up of a range of accommodation providers including holiday and caravan parks, B&Bs and guesthouses. There are over 25 restaurants and cafes. Other activities include amusements, a country park and museums.

Figure 8-5 Tourism Businesses in Swanage

Source: Experian

Tourism Employment

8.9 Table 8-2 below shows the number of tourism related jobs and their proportional share of overall jobs for each of the coastal local authorities in the study area and the wider Dorset, Hampshire and South West and South East study area.

8.10 Tourism related employment in the South East LPAs Isle of Wight and New Forest has increased in recent years whereas tourism related employment in the South West local authorities has either remained broadly constant (Christchurch and Purbeck) or declined (Bournemouth, Poole and Weymouth and Portland). This South West/ South East trend is also event at the wider County Council level and regional level.

8.11 Tourism related employment accounts for an above average proportion of all employment in each local authority (with the notable exception of Poole). Tourism related employment in the southern west LPAs Purbeck and Portland account for a particularly high share of all employment. The Isle of Wight and New Forest also have a high proportion of tourism related jobs compared to the regional average.

0

5

10

15

20

25

30

35

40

Number of Businesses

Navitus Bay Socio-Economic and Tourism Baseline Assessment