98

RESULTS NEDBANK GROUP LIMITED 2017 ANNUAL ar FOR THE YEAR ENDED 31 DECEMBER

RESULTS

NEDBANK GROUP LIMITED

2017

ANNUALar

FOR THE YEAR ENDED 31 DECEMBER

2NEDBANK GROUP LIMITED – Annual Results '17ar

Solid performance during a

difficult and volatile year

OVERVIEW

MIKE BROWN

3NEDBANK GROUP LIMITED – Annual Results '17ar

Overview of our 2017 performance

Solid financial performance – headline earnings +2.8% (H1 2017: -2.9%)

Good performance from managed operations – headline earnings +7.8% (H1 2017: +6.7%)

− Unresolved structural challenges in SA economy compounded by political & policy uncertainty

− Cyclical economic downturn in SA

− Multiple event risks resulted in high levels of volatility – Nedbank navigated these well

− Business & consumer confidence at multiyear lows – slowdown in asset growth & transactional

activity, particularly evident in CIB & Wealth

− Selective loan origination & quality advances book with high levels of resolutions of historically

problematic accounts

− Expenses well managed

ETI loss from Q4 2016 impacted Nedbank’s H1 2017 result – returned to profitability in the

9 months to 30 September 2017, boosting Nedbank Group's H2 growth rates

Accelerated digital delivery to enhance client experience & improve efficiency

Delivering value to all our stakeholders – ongoing focus on governance & sustainability

4NEDBANK GROUP LIMITED – Annual Results '17ar

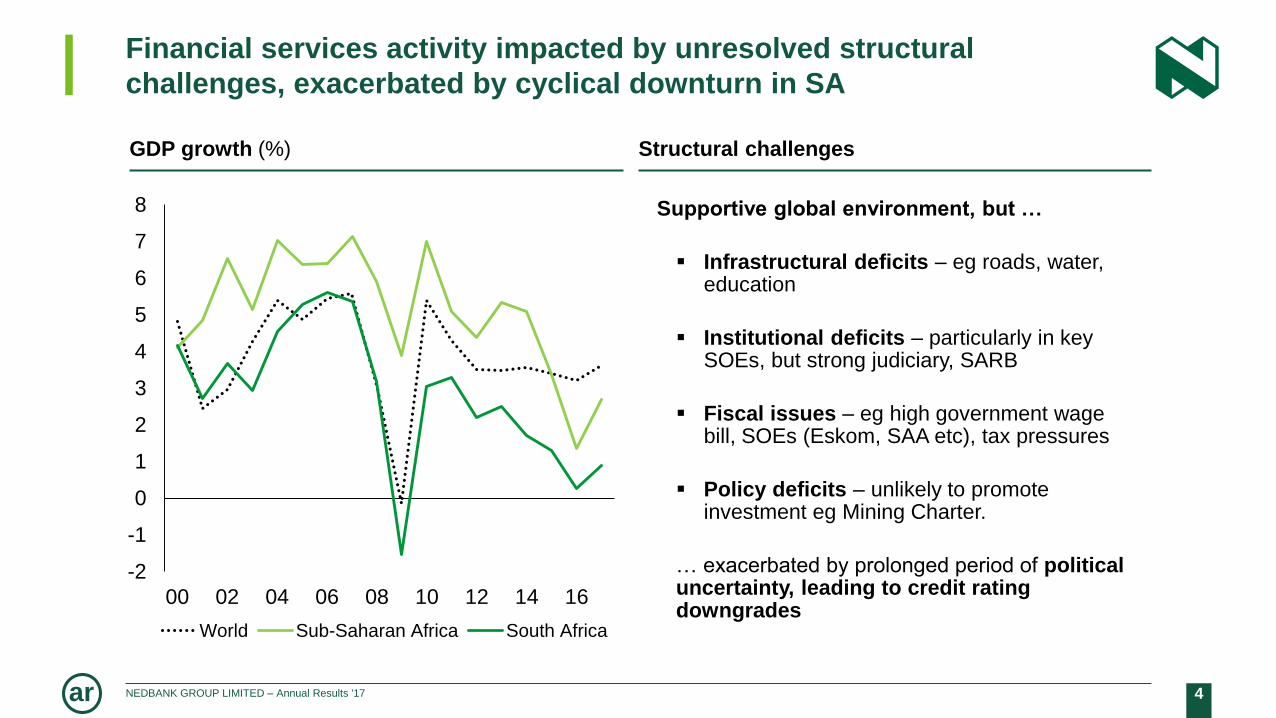

Financial services activity impacted by unresolved structural

challenges, exacerbated by cyclical downturn in SA

GDP growth (%)

-2

-1

0

1

2

3

4

5

6

7

8

00 02 04 06 08 10 12 14 16

World Sub-Saharan Africa South Africa

Structural challenges

Supportive global environment, but …

Infrastructural deficits – eg roads, water, education

Institutional deficits – particularly in key SOEs, but strong judiciary, SARB

Fiscal issues – eg high government wage bill, SOEs (Eskom, SAA etc), tax pressures

Policy deficits – unlikely to promote investment eg Mining Charter.

… exacerbated by prolonged period of political uncertainty, leading to credit rating downgrades

5NEDBANK GROUP LIMITED – Annual Results '17ar

Multiple event risks resulted in high levels of volatility – Nedbank

navigated these well

USD/ZAR JSE top 40

SA 10 year government bond yield (%) 5-year CDS spreads (%)

Pravingate

Fitch downgrade

Surprise rate cut

S&P downgrade

ANC elective conference

11

12

13

14

15

Jan 17 Mar 17 May 17 Jul 17 Sep 17 Nov 17

8

9

10

Jan 17 Mar 17 May 17 Jul 17 Sep 17 Nov 17

Pravingate

Fitch downgrade

Surprise rate cut

S&P downgrade

ANC elective conference

40 000

45 000

50 000

55 000

60 000

Jan 17 Mar 17 May 17 Jul 17 Sep 17 Nov 17

150

200

250

Jan 17 Mar 17 May 17 Jul 17 Sep 17 Nov 17

Steinhoff

Steinhoff

6NEDBANK GROUP LIMITED – Annual Results '17ar

Business & consumer confidence at multiyear lows – slight

improvement in last quarter

BER business confidence index BER consumer confidence index

0

10

20

30

40

50

60

70

80

90

100

94 96 98 00 02 04 06 08 10 12 14 16

-25

-20

-15

-10

-5

0

5

10

15

20

25

94 96 98 00 02 04 06 08 10 12 14 16

7NEDBANK GROUP LIMITED – Annual Results '17ar

Credit demand muted – decline more pronounced in wholesale given

political & policy uncertainty

Industry credit growth (%)

-10

0

10

20

30

40

00 02 04 06 08 10 12 14 16

Households (yoy%) Companies (yoy%)

81 8964 54

2323

2020

5458

6166

915

1713

14 15 16 17

CIB BB Retail Other

Nedbank new loan payouts (Rbn)

167185

153162

8NEDBANK GROUP LIMITED – Annual Results '17ar

149176

123143

Home loans Net client cashflows

16 17

Volumes also at lower levels

Retail credit application volumes (000)

1 271

1 403

1 286

1 381

Personal loans Vehicle finance

CIB trading revenues (2017, indexed from Q1)

91

100

58

6765

Q1 Q2 Q3 Q4

Nedbank JP Morgan FICC & equities

CITI FICC & equities BAML FICC & equities

+1%

(2%)

(17%)

SA industry NCCF1 (Rbn)

(19%)

1 Source: ASISA

9NEDBANK GROUP LIMITED – Annual Results '17ar

Delivering value to shareholders

13

14

3

14

39

5

15

685

15

83

0

16

99

0

13 14 15 16 17

895

1028

1107

1200

1285

13 14 15 16 17

17.2 17.2 17.0

16.5 16.4

13.013.5

13.0

14.2 14.0

16.8

18.1 18.1

13 14 15 16 17

ROE (excl GW)

COE

ROE (excl GW & ETI)

+7.3% +7.1%

NAV per share (cents) ROE & cost of equity (%) Dividend per share (cents)

CAGR: +6.6% CAGR: +9.5%

10NEDBANK GROUP LIMITED – Annual Results '17ar

Our role in society – contributing by delivering value to all our stakeholders

STAFF

CLIENTS

SHAREHOLDERS

REGULATORS

SOCIETY

Paid R16.5bn in salaries & benefits to support our 31 887 staffmembers & their families

Facilitated transfer of R3.7bn payroll taxes on behalf of staff to government

Implemented a leadership & culture change programme supporting strategy, incl New Ways of Work

Transforming our workforce towards SA demographics (> 78% black employees)

R153bn new loan payouts to enable clients to finance their homes, vehicles, education & grow their businesses

Enhanced client convenience – 234 new Intelligent Depositors, 55% reformatted digitally focused branches & new innovative apps & CVPs

Safeguarded R772bn deposits at competitive interest rates

Voted top SA asset manager – managing our clients’ investments

NAV per share up 7.3% to 169 90 cents

Paid R6.1bn dividends to shareholders who represent pension funds & investments of all South Africans (incl GEPF, a 6.8% shareholder in Nedbank)

Supportive outcomes at 50th AGM – all resolutions passed with > 90% votes of approval

Maintained a strong balance sheet to support a safe & stable banking system

Paid R9.8bn direct, indirect & other taxes

Invested more than R100bn in government & public sector bonds to support the funding needs of government

Procured 75% of our goods & services locally

Contributed R168m to socioeconomic development (50% spent on education)

Active participant in the CEO Initiative

Overall winner at the 2017 Independent Top Empowered Companies Awards. Remained a Level 2 BBBEE contributor, now measured under the Amended FSC

TO BE THE MOST ADMIRED

FINANCIAL SERVICES PROVIDER IN AFRICA

BY OUR STAKEHOLDERS

Our purpose - to use our financial expertise to do good for individuals, families, businesses & society

11NEDBANK GROUP LIMITED – Annual Results '17ar

Good performance from

managed operations in a

challenging macroeconomic

environment

FINANCIAL

OVERVIEW

RAISIBE MORATHI

12NEDBANK GROUP LIMITED – Annual Results '17ar

Key performance indicators – good performance from managed operations

2017 2016 2017¹ 2016¹

Headline earnings (Rm) 2.8% 11 787 11 465 7.8% 12 762 11 839

ROE (excl goodwill) 16.4% 16.5% 18.1% 18.1%

Diluted HEPS growth 2.4% 4.8% 7.3% 15.1%

Preprovisioning operating profit growth (3.2%) 4.4% (0.3%) 10.0%

Net interest margin2 3.62% 3.54%

Credit loss ratio 0.49% 0.68%

CET1 CAR 12.6% 12.1%

Dividend per share (cents) 7.1% 1 285 1 200

Managed operations

1 Excluding ETI associate income/losses, as well as ETI-related funding costs. Managed operations reporting provided to assist in analysis of group performance during the

period of ETI Q4 2015/16 losses, but we will revert to blended results in 2019. 2 2016 rebased.

13NEDBANK GROUP LIMITED – Annual Results '17ar

Headline earnings – good performance from managed operations

11 465 11 787

1 198 560

1 250 (1 446)

(733)

(507)

2016 NII NIR Impairments Expenses Associateincome

Direct tax& other

2017

+4.5% (27.4%)+2.4% +5.1% (> 100.0%)

2.8

7.8

Group Managedoperations

16.418.1

Group Managedoperations

Headline earnings (Rm) HE growth (%)

ROE excl GW (%)

14NEDBANK GROUP LIMITED – Annual Results '17ar

Headline earnings – improved H2 2017 performance from both managed

operations & ETI

H1 2017 vs H2 2017 (Rm)

13

028

13

398

13

548

14

076

H1 H2

NII

11

357

12

146

11

730

12

333

H1 H2

NIR

22

11

2343

1594

1710

H1 H2

Impairments

13

686

14

680

14

369

15

443

H1 H2

Expenses

6030

5809

6433

6329

H1 H2

HE managed operations

(43

1) 32

6

(1 0

53

)

215

H1 H2

Associate income

+4.0% +5.1%

+3.3%+1.5%

(27.9%) (27.0%)

+5.0% +5.2%

+6.7% +9.0%

(144%) (34%)

16 17 ETI: (446) (1061) 321 317

15NEDBANK GROUP LIMITED – Annual Results '17ar

Net interest margin – driven by endowment & asset mix

Net interest margin (bps)

Average interest-earning banking assets1: +2.2%

341 354

362

135

8 (2) (2) (2) 1

2016 Removal oftrading LAP

2016rebased

Endowmentimpact

Assetmix

Assetpricing

Liabilitypricing& mix

Prime-JIBARimpact

Other 2017

1 Rebased NIM for twelve months ended 31 December 2016 would have been 354 bps & AIEBA of R745bn, had HQLA been removed from the banking book & included in the

trading book from 1 January 2016.

16NEDBANK GROUP LIMITED – Annual Results '17ar

2

(3)

(10)

(3)(2)

13 14 15 16 17

(2)

10

5

18

5

(5)

(2)

0

13 14 15 16 17

3

(12) (12)

(4)

8

Net interest margin – driven by endowment & asset mix

change

Asset mix change (bps) Endowment (bps)

BOOKLET SLIDE

Liability mix & pricing (bps) HQLA (bps)

17NEDBANK GROUP LIMITED – Annual Results '17ar

Funding

sources

Funding

base mix

Local currency

downgrade

(what we expected1)

Local currency

downgrade

(what actually happened2)

Further local currency

downgrade

(what we expect3)

Households 21.5%Limited impact – closed

domestic market Limited impact – closed

domestic market

Limited impact – Closed

domestic marketCommercial 28.0%

Cost of new term funding:

+5 bps

Wholesale 37.6%Cost of new term funding:

+10 bps

Cost of new term funding:

+5−8 bps

Cost of new term funding:

+5−10 bps

Capital markets 6.8%Cost of new capital markets

funding: +25 bps

Reprice on new issuances,

however, capital market

spreads have decreased

given demand for good credit

Reprice on new issuances:

+25−35 bps

Foreign – asset matched 5.1%Matched to US$ lending – no

material impact

Matched to US$ lending

No material impact

Matched to US$ lending

No material impact

Foreign – general funding

pool1.0%

Cost of new foreign funding:

+25−50 bps (1 year)

Reprice on contractual

repricing date, however,

funding costs have

decreased on the back of

risk-on foreign appetite

Cost of new foreign funding:

+15−25 bps (1 year)

Volume-weighted total 100% circa +5 bps 0 bps circa +4 bps

Net interest margin – impact of sovereign-credit-ratings

downgrades on funding costs not materialBOOKLET SLIDE

Total funding (deposits + long-term debt) at 31 December 2017: R823bn.1 From June 2017 year-end presentation | 2 On 24 November 2017 S&P downgraded the sovereign long-term local currency rating from BBB- to BB+ while Moody’s placed SA on Review | 3

Moody's is expected to announce the outcome of their credit rating review in March 2018. Assuming they decrease SA’s sovereign long-term local currency rating from Baa3 to Ba1 (sub-

investment grade), SA would be excluded from the WGBI. The potential impact is expected to have reduced substantially given that foreign investors have had time to pro-actively pre-position

their portfolios for this potential event. Following the ANC elective conference, SA 2018 budget announcement & Presidential & Ministerial changes, markets appear to be pointing to a lower

probability of a sovereign-credit ratings downgrade. Assuming a rating downgrade, continued risk-on EM demand is likely to dampen the potential impact..

18NEDBANK GROUP LIMITED – Annual Results '17ar

152

162

121

145

106 1

9

15

162

148

11

4

150

11

2 20

16

Commercialproperty

Termloans

Otherloans

Homeloans

Vehiclefinance

Personalloans

Card

Dec 16 Dec 17

21

Selective origination

& unique positioning

Gross advances (Rbn)

Mostly

ST &

volatile

Wholesale

Advances up 0.5% – solid growth & market share gains across retail

portfolios offset by early repayments in CIB

BA900 market share3 (%)

+6.5%+3.2%

(8.3%)

(5.2%)+6.3%

+4.1% +6.3%

Leveraging

relationships &

pipeline

Retail

1 Terms loans & other longer-dated loans. | 2 Other loans include overdrafts, overnight loans, preference shares, deposits placed under reverse repurchase agreements & other smaller

corporate loans. | 3 BA900 – Dec 2017 (Compared to Dec 2016). | 4 Core corporate loans comprise commercial mortgages, corporate overdrafts, corporate credit cards, corporate instalment

credit, foreign sector loans, public sector loans, preference shares, factoring accounts & other corporate loans (other loans and advances excluding household personal loans). | 5 VAF per

BA 900 comprises total lease & Instalment sales.

Share Trend

Commercial

property40.5 (0.3)

Core corporate4 21.0 (1.3)

Home loans 14.5 0.0

Vehicle finance5 28.1 +0.4

Personal loans 10.3 +0.1

Card 14.0 +0.3

19NEDBANK GROUP LIMITED – Annual Results '17ar

BA900 market share1Deposits (Rbn)

Deposits up 1.3% – good household deposit growth, particularly in RBB,

up 8.5%, evident in ongoing market share gains

Share Trend

Wholesale 21.2 (1.1)

Corporate

(non-financial)16.5 +0.2

Household 18.9 +0.2

Foreign

currency 12.8 +0.2

1 BA900 – Dec 2017 (Compared to Dec 2016).

761

772

23

2 1 (4)

(11)

2016 RBB Wealth Rest ofAfrica

CIB CentralMgnt

2017

+8.5% +4.8% +4.2% (1,3%) (13,3%)

Basel III + Basel III -

20NEDBANK GROUP LIMITED – Annual Results '17ar

17 355

3 900

1 566

708

534

Commission& fees

Tradingincome

Insuranceincome

Privateequity

Other¹

Non-interest revenue up 2.4% – resilient underlying performance, offset by high

base, the impact of a challenging economic environment & weak insurance result

NIR growth per cluster (%)Non-interest revenue (Rm)

1 Represents sundry income, investment income & fair-value adjustments. | 2 C&F 72% of NIR.

Rest of Africa & Centre excluded as not material.

CIB RBB Wealth

16 17 16 17 16 17

14.5 (3.9) 6.9 5.0 (5.1) (0.6)

▲2.3

▼(24.1)

▼(4.5)

▼(10.0)

▲18.9

▲3.1

▲16.4

▼(4.3)

▲7.1

▲5.32

21NEDBANK GROUP LIMITED – Annual Results '17ar

Credit loss ratio – improvement underpinned by a quality portfolio &

proactive risk management

47.3% 45.5% 4.3% 2.9%Banking

advances

106

79 77

68

49

13 14 15 16 17

34

112

8

98

6

106

9

102

CIB RBB Wealth RoA

16 17

1

Group CLR1 (bps) Cluster CLR (bps)

1 Nedbank through-the-cycle target range: 60–100 bps.

22NEDBANK GROUP LIMITED – Annual Results '17ar

Defaulted advances flat & maintained healthy coverage levels

16 17

1 157 1 224 654 350

500150

16 17

RBB Centre

Specific coverage (%) Portfolio coverage (%)

Overlays & central

provision (Rm)

Defaulted advances (Rbn, %)

37.4 36.2

16 17

0.69 0.70

16 17

19.6 19.6 16.2 15.4

2.7 2.7

2.32.1

0

1

2

3

0

10

20

30

16 17 16 17

Defaulted advances Defaulted advances as % of book

+0.0%

(4.9)%Postwriteoff

recoveries (Rm)

Defaulted advances Defaulted advances

(excl performing

defaults)1

1 Performing defaults is defined as Retail advances held in default for longer due to regulatory requirements, but are otherwise performing.

23NEDBANK GROUP LIMITED – Annual Results '17ar

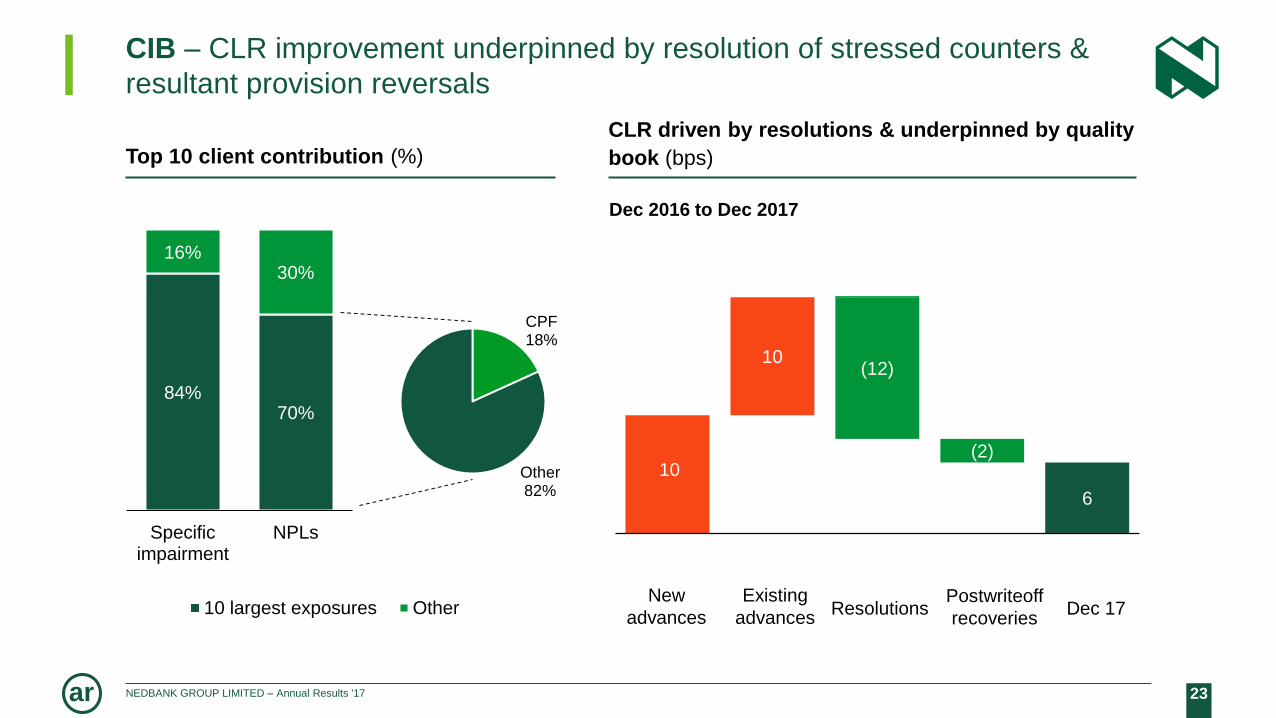

84%70%

16%30%

Specificimpairment

NPLs

10 largest exposures Other

CPF18%

Other82%

CIB – CLR improvement underpinned by resolution of stressed counters &

resultant provision reversals

Top 10 client contribution (%)

CLR driven by resolutions & underpinned by quality

book (bps)

6

10

10(12)

(2)

Dec 17ResolutionsNew

advances

Existing

advances

Dec 2016 to Dec 2017

Postwriteoff

recoveries

24NEDBANK GROUP LIMITED – Annual Results '17ar

RBB – CLR underpinned by quality origination

Nedbank Competitors1 Source: Experian Delphi Score2 Source: Lightstone Risk Quality Grade3 Source: Experian

HL new business – low risk clients proportion1 (%)

HL new business – low risk properties proportion² (%)

0%

10%

20%

30%

40%

09 10 11 12 13 14 15 16 17

0%

10%

20%

30%

40%

09 10 11 12 13 14 15 16 17

PL market share of new business by risk band3 (%)

0%

5%

10%

15%

20%

14 15 16 17

Low Risk * Low-Medium Risk Medium Risk High risk

Nedbank Tier 1 ** Tier 2 **

0%

20%

40%

60%

80%

14 15 16 170%

20%

40%

60%

80%

1714 15 16

Vehicle finance 3 months+ arrears benchmarking3

0%

1%

2%

3%

4%

5%

6%

13 14 15 16 17

* Low risk (Bureau score ≥ 658); Low−medium risk (Bureau score 644−657); Medium risk (Bureau score 626−643); High risk (Bureau score ≤ 625)

** Tier 1 refers to traditional 4 banks excluding Nedbank while tier 2 refers to remaining material providers of unsecured personal loans

25NEDBANK GROUP LIMITED – Annual Results '17ar

0

20

40

60

80

100

120

Group CIB Home loans Vehicle finance Personal loans Card

Nedbank (Dec 17) Nedbank (Dec 16) Bank A Bank B Bank C

Specific coverage – reflecting wholesale & retail asset

mix profile

Big 4 banks’ specific coverage ratios1 (%)

1 Peer information from last reported financials (June 2017).

Wholesale advances contribution

Selective origination

since 2010 & high-

quality book

CPF 40% of CIB book (higher levels of

security) & coverage in CIB individually

determined

Total retail coverage 39.5 42.8 43.0 35.5

59% 39% 32% 38%

BOOKLET SLIDE

26NEDBANK GROUP LIMITED – Annual Results '17ar

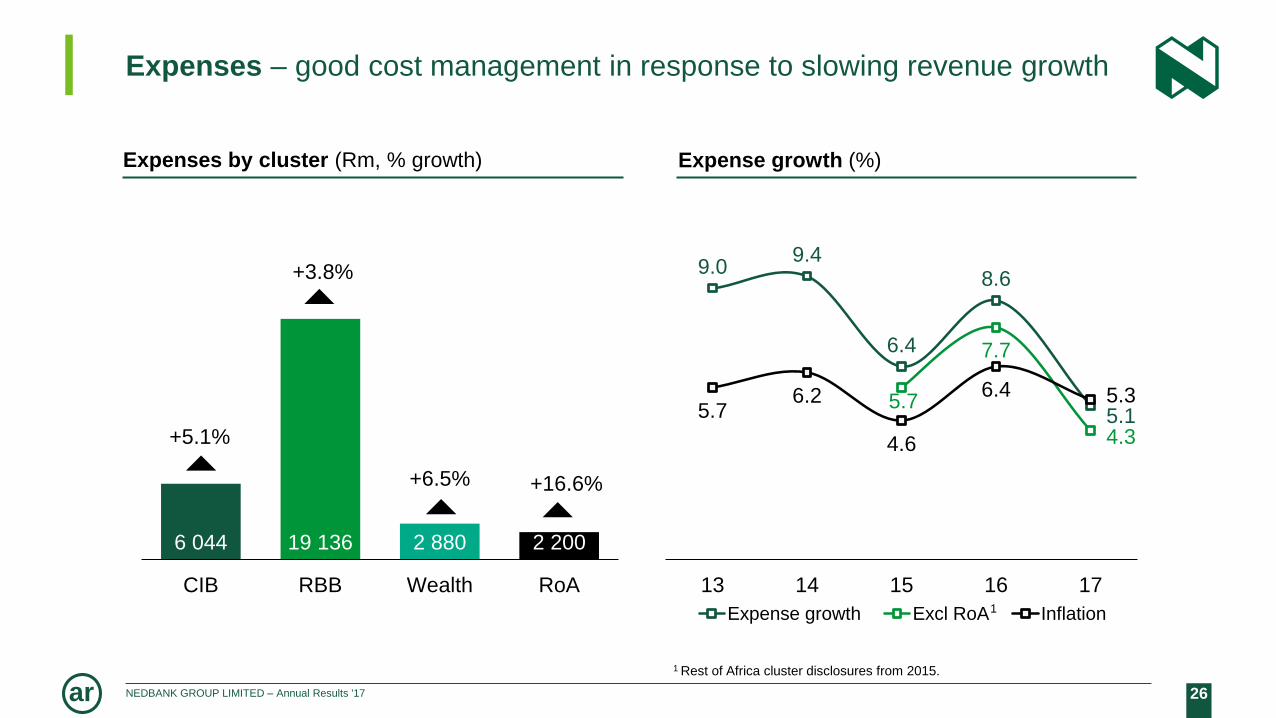

Expenses – good cost management in response to slowing revenue growth

Expense growth (%)

9.09.4

6.4

8.6

5.15.7

7.7

4.3

5.76.2

4.6

6.4 5.3

13 14 15 16 17

Expense growth Excl RoA Inflation

Expenses by cluster (Rm, % growth)

6 044 19 136 2 880 2 200

CIB RBB Wealth RoA

+5.1%

+3.8%

+16.6%+6.5%

1

1 Rest of Africa cluster disclosures from 2015.

27NEDBANK GROUP LIMITED – Annual Results '17ar

28 366 28 850

29 812

1 105 (621) 617 107 238

2016 BAUgrowth

Efficiencies BAUgrowth

Investments Regulatory BancoÚnico

2017

Expenses – good cost management in response to slowing revenue

growth

Expenses (Rm)

1 R621m includes TOM, OM synergies & other cost savings. R444m accrues to RBB2 Investments, including IT projects, branch reformatting costs, etc.

+1.7% +3.4%

21

28NEDBANK GROUP LIMITED – Annual Results '17ar

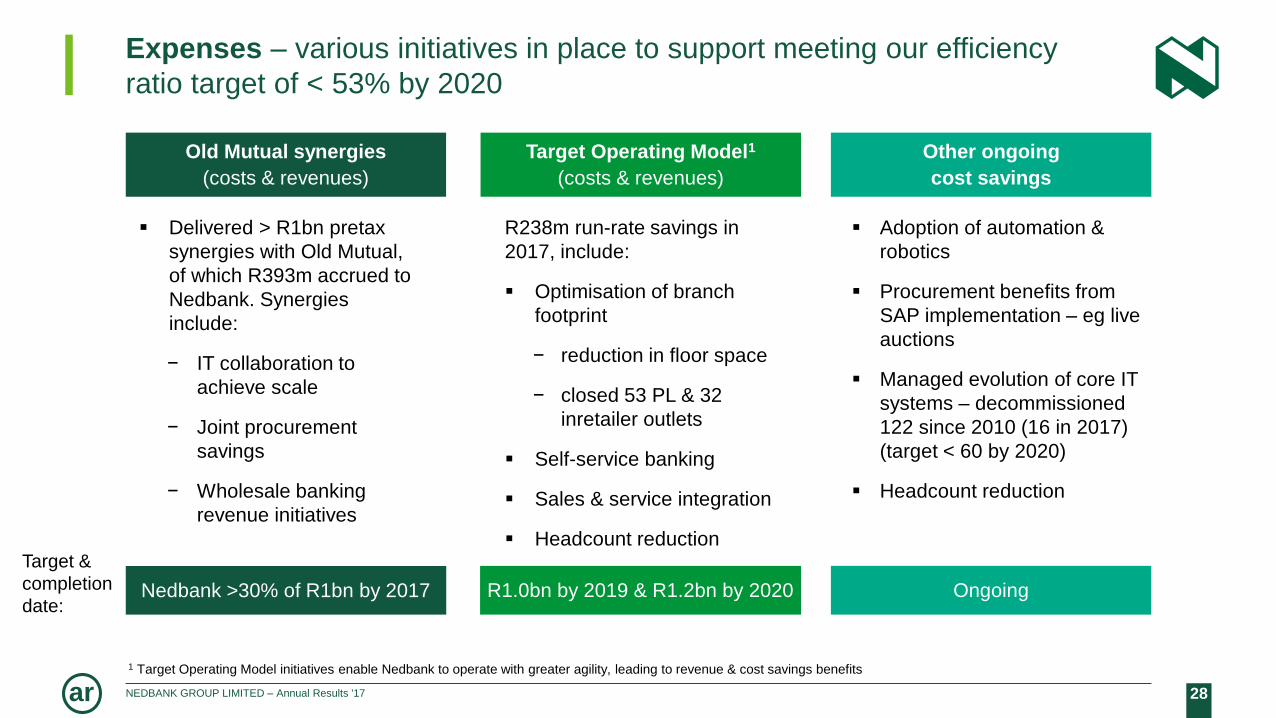

R238m run-rate savings in

2017, include:

Optimisation of branch

footprint

− reduction in floor space

− closed 53 PL & 32

inretailer outlets

Self-service banking

Sales & service integration

Headcount reduction

Expenses – various initiatives in place to support meeting our efficiency

ratio target of < 53% by 2020

Adoption of automation &

robotics

Procurement benefits from

SAP implementation – eg live

auctions

Managed evolution of core IT

systems – decommissioned

122 since 2010 (16 in 2017)

(target < 60 by 2020)

Headcount reduction

1 Target Operating Model initiatives enable Nedbank to operate with greater agility, leading to revenue & cost savings benefits

Old Mutual synergies

(costs & revenues)

Nedbank >30% of R1bn by 2017

Target &

completion

date:

Target Operating Model1

(costs & revenues)

R1.0bn by 2019 & R1.2bn by 2020

Other ongoing

cost savings

Ongoing

Delivered > R1bn pretax

synergies with Old Mutual,

of which R393m accrued to

Nedbank. Synergies

include:

− IT collaboration to

achieve scale

− Joint procurement

savings

− Wholesale banking

revenue initiatives

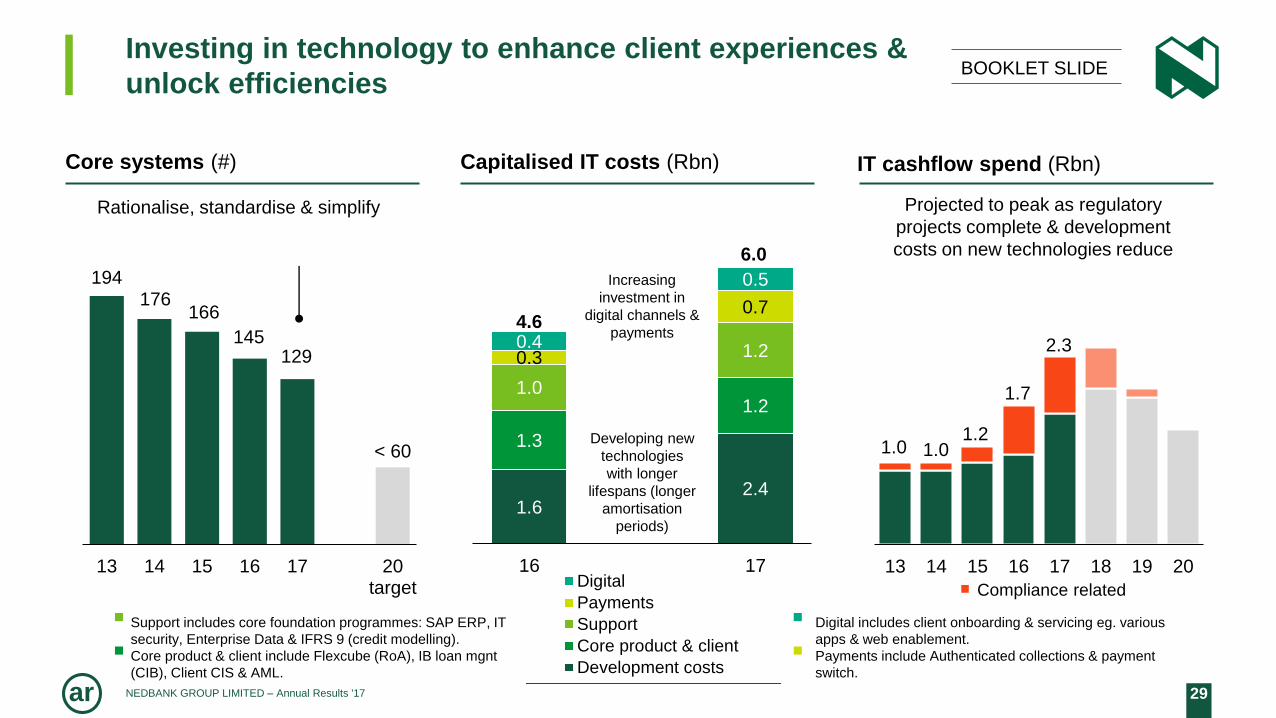

29NEDBANK GROUP LIMITED – Annual Results '17ar

1.0 1.01.2

1.7

2.3

13 14 15 16 17 18 19 20

IT cashflow spend (Rbn)

Investing in technology to enhance client experiences &

unlock efficiencies

Capitalised IT costs (Rbn)

Projected to peak as regulatory

projects complete & development

costs on new technologies reduce

1.62.4

1.3

1.21.0

1.20.3

0.7

0.4

0.5

16 17Digital

Payments

Support

Core product & client

Development costs

4.6

6.0

Developing new

technologies

with longer

lifespans (longer

amortisation

periods)

Increasing

investment in

digital channels &

payments

BOOKLET SLIDE

194176

166

145129

< 60

13 14 15 16 17 20target

Core systems (#)

Rationalise, standardise & simplify

Digital includes client onboarding & servicing eg. various

apps & web enablement.

Payments include Authenticated collections & payment

switch.

Support includes core foundation programmes: SAP ERP, IT

security, Enterprise Data & IFRS 9 (credit modelling).

Core product & client include Flexcube (RoA), IB loan mgnt

(CIB), Client CIS & AML.

Compliance related

30NEDBANK GROUP LIMITED – Annual Results '17ar

148278 292

152

(676)

230 171 150

(1 203)

142 152 165

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Associate income – ETI performance reflective of tough but improving

environment, particularly in Nigeria

Associate income from ETI1 (Rm)

870 (125) (744)

1 ETI accounted for one quarter in arrear. | 2 Source: ETI disclosures. ETI reported COE at ~ 17%.

ETI H1 2017

results

audited

15 16 17

ETI medium-to-long

term guidance2

ROTE target: COE + 5%

(H1 2017: 15.3%)

Efficiency ratio: 50−55%

(H1 2017: 60.6%)

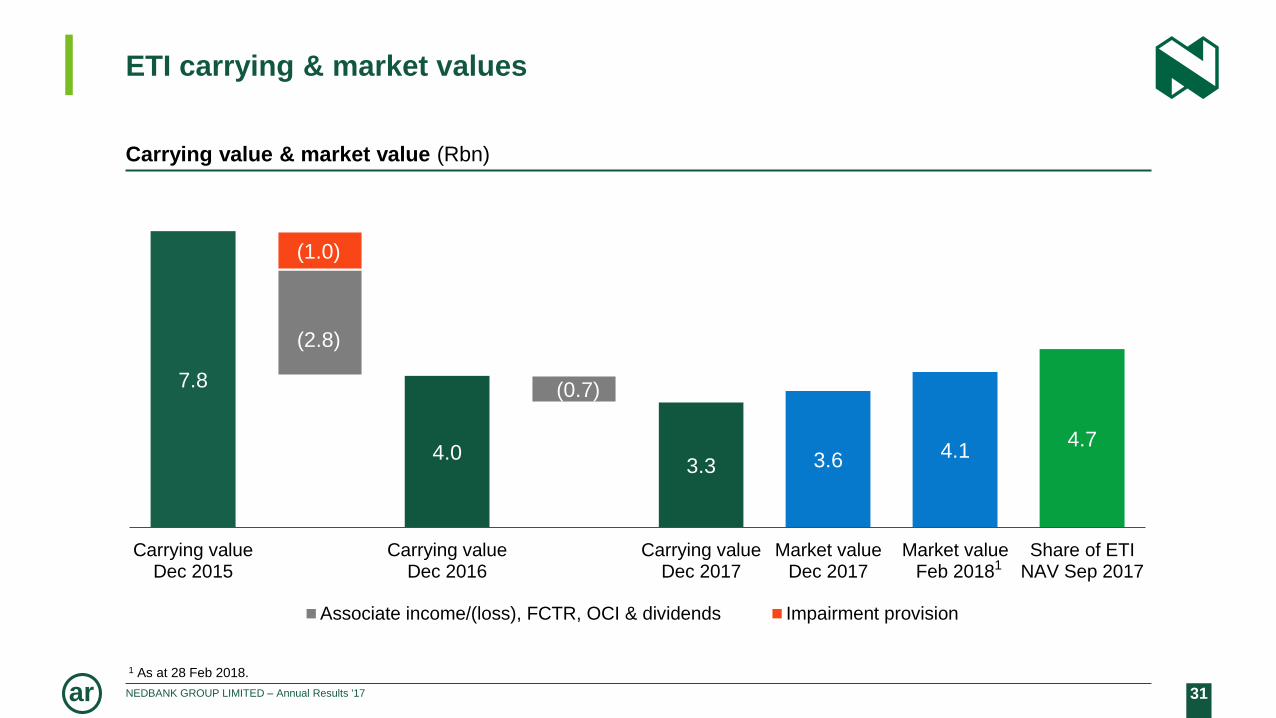

31NEDBANK GROUP LIMITED – Annual Results '17ar

ETI carrying & market values

Carrying value & market value (Rbn)

7.8

4.03.3 3.6 4.1

4.7

(2.8)

(0.7)

(1.0)

Carrying valueDec 2015

Carrying valueDec 2016

Carrying valueDec 2017

Market valueDec 2017

Market valueFeb 2018

Share of ETINAV Sep 2017

Associate income/(loss), FCTR, OCI & dividends Impairment provision

1 As at 28 Feb 2018.

1

32NEDBANK GROUP LIMITED – Annual Results '17ar

12.1

13.0 12.6

12.6

2.1(1.2) (0.4)

Dec2016

Organicprofits

Dividendspaid

RWA increases

Dec2017

Capital – CET1 above the top end of our target range

CET1 capital ratio (%)

CET1: 10.5–12.5%

SARB minimum CET1: 7.25%

Fully loss-absorbent capital adequacy ratios (%)

Jun 17 Dec 2017

16.714.9 14.7 15.2 15.2

14.3 13.7 13.912.8 13.1

Bank A Bank B Bank C Nedbank Nedbank

Tier 1 Tier 2

16.2

14.9 14.715.2 15.4

33NEDBANK GROUP LIMITED – Annual Results '17ar

IFRS 9 & 15 accounting standard day 1 impact1 – strengthened balance

sheet coverage with immaterial impact on CET1

66.4~ 65.7

~ 3.2

2.0~ 0.9 ~ 0.2 ~ 0.2

31 Dec 2017 IFRS 9Impairments

Excess ofdownturn ECLover provisions

Tax effect

IFRS 9Classification &measurement

IFRS 15Revenue

1 Jan 2018proforma

Common equity tier 1 (Rbn)

Portfolio coverage:

CET1:

0.70% ~1.05%

12.6% >12.4%< 0.1%

~ 0.35%

2

< 0.1%

1 These estimates are based on accounting policies, assumptions, judgements & estimation techniques that will be regularly reviewed & assessed during 2018. | 2 Excess downturn expected

credit loss over provisions reversed due to increase in IFRS provisions. | Excludes ETI IFRS 9 impacts to be announced in H1 2018.

34NEDBANK GROUP LIMITED – Annual Results '17ar

Key drivers of IAS 39 to IFRS 9 transition

Balance sheet impairments (Rbn, illustration)

Mix of the lending book

− Nedbank more wholesale than retail

compared with industry (impact from

lengthening of emergence period under

IFRS 9 greater on retail portfolio provisions

than wholesale portfolio provisions)

− Nedbank has relatively large CPF book –

appreciating assets mitigate lifetime ECL

impacts

Relative proportion of book on AIRB

− AIRB book already includes downturn EL

deduction from capital, thereby partially

offsetting impact of IFRS9 on CET1 in AIRB

portfolios

− Nedbank proportion of book on AIRB at 94%

(peer average at ~ 80%)

Cash tax implications

− Depends on individual banks’ tax practices −

Nedbank historically conservative

IFRS 9 drivers

12.0

~15.2

IAS 39 Stage 1 Stage 2 Stage 3 IFRS 9

Removal of

emergence periods

& replacing with

12-month ECL on all

exposures

Retail more

impacted than

wholesale

Inclusion of off-

balance sheet

exposures

Lifetime ECL on

exposures that have

a significant

increase in credit

risk

Minor impact as

default definition

remains unchanged

BOOKLET SLIDE

35NEDBANK GROUP LIMITED – Annual Results '17ar

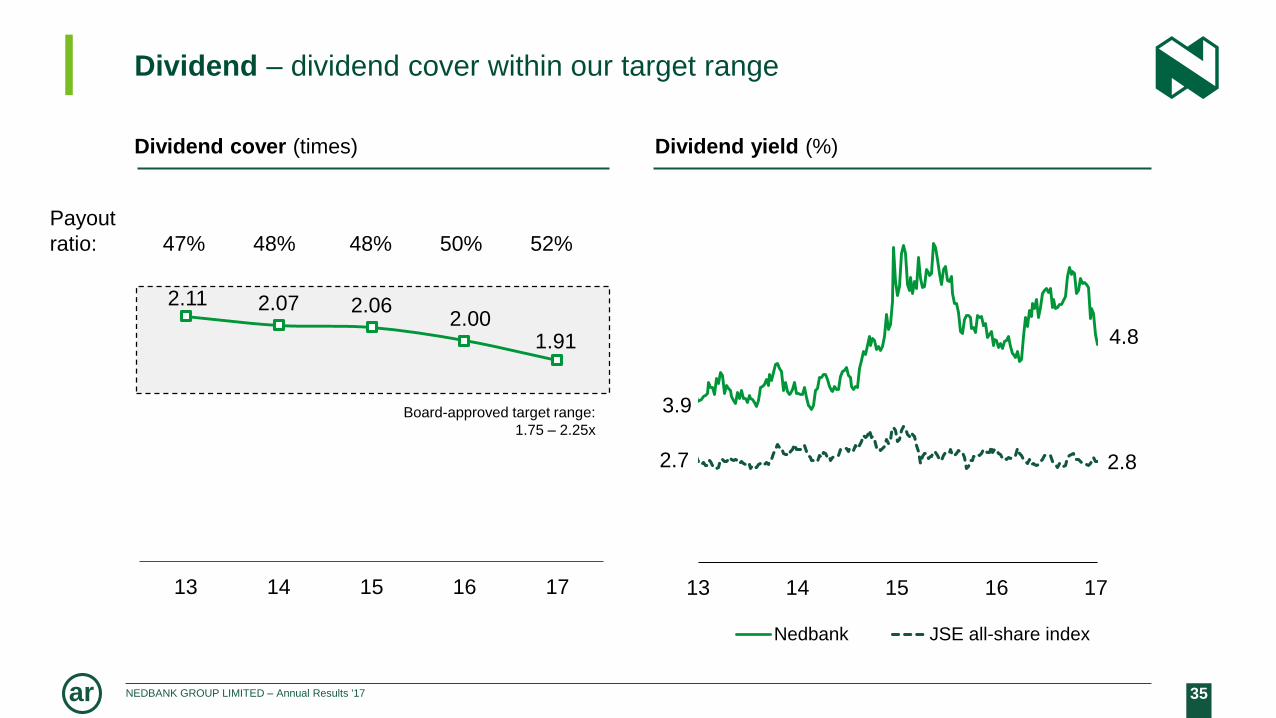

Dividend – dividend cover within our target range

2.11 2.07 2.062.00

1.91

13 14 15 16 17

Board-approved target range:

1.75 – 2.25x

Dividend cover (times) Dividend yield (%)

Payout

ratio: 47% 48% 48% 50% 52%

3.9

4.8

2.7 2.8

13 14 15 16 17

Nedbank JSE all-share index

36NEDBANK GROUP LIMITED – Annual Results '17ar

Good performance from our managed operations – group headline

earnings up 2.8%

60

14

49

60

11

92

(287)

(414)

63

15

53

02

10

68

(810)

(88)

CIB RBB Wealth Rest ofAfrica

Centre

16 17

+5.0%

+6.9%

(10.4%)

Earnings contribution (Rm)Headline earnings (Rm)

54%

45%

9%

1%

(8%) (1%)

CIB RBB

Wealth Rest of Africa

ETI Centre

37NEDBANK GROUP LIMITED – Annual Results '17ar

Strong risk management in a

difficult and volatile

environment

NEDBANK CORPORATE

AND INVESTMENT

BANKING

BRIAN KENNEDY

38NEDBANK GROUP LIMITED – Annual Results '17ar

39

71

47

27

52

08

60

14

63

15

27.6 27.0

22.621.1 20.7

- 2.0

3.0

8.0

13.0

18.0

23.0

28.0

-

2 000

4 000

6 000

8 000

10 000

12 000

13 14 15 16 17

Headline earnings (Rm) ROE (%)

Strong risk management in a difficult & volatile environment

Operating Income +3.9%: Lack of business

confidence translating to lower advances &

revenue

CIB integration providing significant client

penetration & cross-sell opportunities

CLR 6 bps: Strong risk management,

collections & high-quality portfolio

Expenses +5.1%: Efficient franchise

Strong franchise providing good returns

(ROE > 20%)

Key messagesHeadline earnings, ROE

+5%

Network

39NEDBANK GROUP LIMITED – Annual Results '17ar

54%

46%

Headline earnings

50%50%

Assets

Nedbank CIB Other clustersYear ended % change FY 2017 FY 2016

Headline earnings (Rm) 5.0 6 315 6 014

Operating income (Rm) 3.9 14 187 13 649

PPOP (Rm) (7.9) 8 173 8 878

Net interest margin (%) 2.12 1.97

NIR-to-expense ratio (%) 118.5 129.6

Efficiency ratio (%) 42.3 39.0

Credit loss ratio (%) 0.06 0.34

Average banking advances (Rm) 0.7 327 695 325 428

Average deposits (Rm) 0.1 337 052 336 878

Headline economic profit 1 (Rm) 3.5 2 039 1 970

Allocated capital (Rm) 6.9 30 437 28 462

ROE (%) 20.7 21.1

Corporate & Investment Banking – financial highlights

1 Cost of equity 2016: 14.2%. | 2017: 14.0%.

BOOKLET SLIDE

40NEDBANK GROUP LIMITED – Annual Results '17ar

CIB business unit – financial highlights BOOKLET SLIDE

3 035

4 012 4 584

3 1103 056 3 551

4 703

3 070

Property Finance Investment Banking Markets Short-term &Transactional

16 17

Property

FinanceRest of CIB

16 17 16 17

HE (Rm) 1 540 1 560 4 474 4 755

ROE (%) 21.6% 20.6%

CLR (%) 0.04% (0.05%)

GOI by business unit (Rm)

41NEDBANK GROUP LIMITED – Annual Results '17ar

138187 182

85

128 1387

11 8

13 16 17

Other Property finance Banking

Average advances growth affected by early repayments, although

pipeline remains steady

Average banking advances (Rbn)

1 Banking defined as Investment Banking & Client Coverage combined. | 2 NIM restated for prior years for the removal of the liquid-asset portfolio out of interest-earning banking assets.

(3%)

8%

+7%

+13%

+4%

CAGR

+9%

230

325 328

Investment grade & NIM

71% 73% 74%

1.89%1.97%

2.10%2.14% 2.12%

1.00%

1.50%

2.00%

2.50%

0%

20%

40%

60%

80%

100%

13 16 17

Investment grade exposure Reported NIM (RHS)

Restated NIM (RHS)

1%

1

2

42NEDBANK GROUP LIMITED – Annual Results '17ar

36.0%

1.2%

4.4%

3.7%

2.0%

4.4%

32.5%

1.0%

3.8%

4.0%

1.3%

4.2%

PropertyFinance

Construction

Equity

Mining

Retailers

StateOwnedEntities

16 17

Proactive risk management in prior periods yielding results

CLR (%)

Coverage ratios (%)

23.627.7

17.1

26.3

21.0

0.21 0.24 0.29 0.290.45

13 14 15 16 17

Portfolio Specific

CIB selected sector exposures (%)

Migration

riskDown-

side risk

Change

H

H

M

L

M

L

H

-

-

-

H M -

M M -

M ▲

1 State Owned Entities restated to exclude direct Government related entities

1

[ ] Risk decrease [ ] No change [ ] Risk increase

Change on prior period:

▼ - ▲

0.30

0.19

0.40 0.34

0.06

13 14 15 16 17

43NEDBANK GROUP LIMITED – Annual Results '17ar

47% 46% 47% 45%42%

13 14 15 16 17

Quality commercial property book

Diversified book by property type (%)

Low average loan-to-value (LTV) (%)

22

22

12

11

5

9

2

34

10

Offices

Retailers

Warehouse

Multiple portfolios

Manufacturing

Residential

Vacant land

Hotel & BB

Other mortgages

Other loans

Key drivers

Strong client base supported by an experienced team

Lending access to existing collateral pools

Vacant land < 3% & Residential < 10% of portfolio

Retail centre developments funded on > 70% pre-lets

One third of book lending into listed property funds

Primary lending operation supplemented by private equity arm

CLR (%)

BOOKLET SLIDE

: LTVs >90%119.4% 4.6% 3.0% 2.5%17.5%

0.27

0.21

0.08 0.04

(0.05)

13 14 15 16 171 Excludes unsecured loans to listed REITS – by regulation these REITS have gearing ratios of less than 60%.

44NEDBANK GROUP LIMITED – Annual Results '17ar

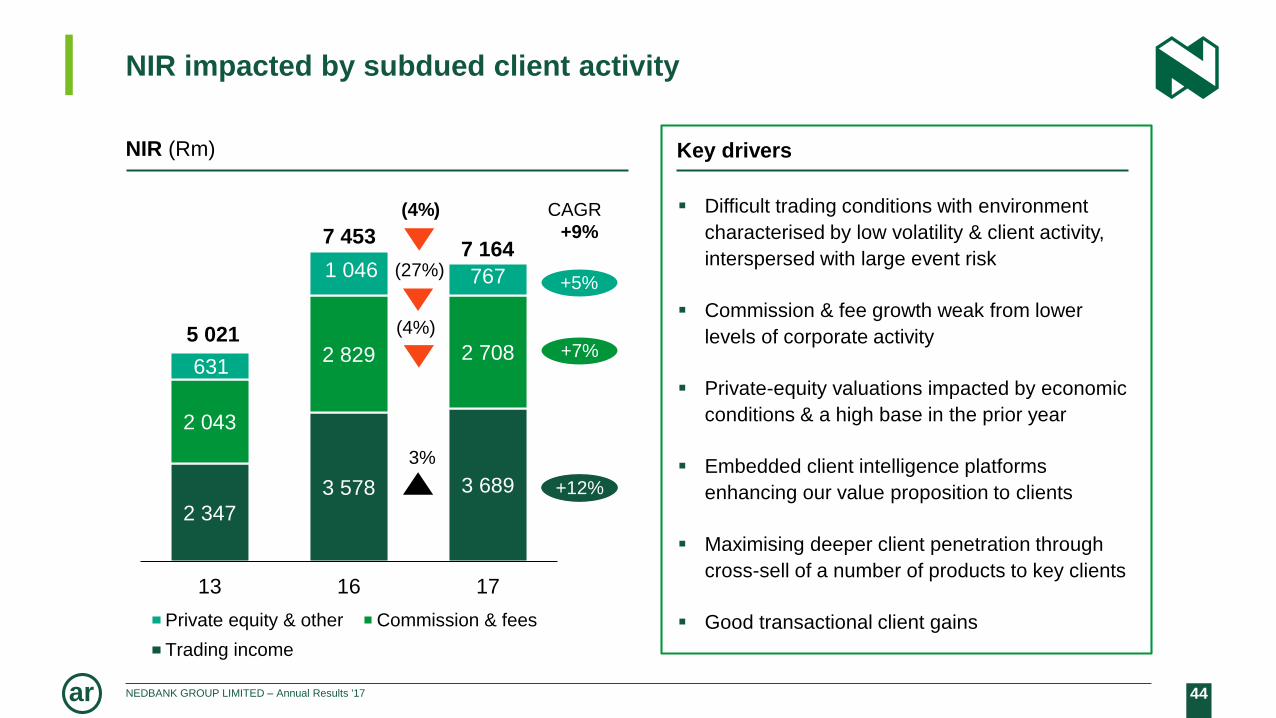

NIR impacted by subdued client activity

Key drivers

Difficult trading conditions with environment

characterised by low volatility & client activity,

interspersed with large event risk

Commission & fee growth weak from lower

levels of corporate activity

Private-equity valuations impacted by economic

conditions & a high base in the prior year

Embedded client intelligence platforms

enhancing our value proposition to clients

Maximising deeper client penetration through

cross-sell of a number of products to key clients

Good transactional client gains

NIR (Rm)

2 347

3 578 3 689

2 043

2 829 2 708631

1 046 767

13 16 17

Private equity & other Commission & fees

Trading income

(4%)

3%

+12%

+7%

+5%

CAGR

+9%

5 021

7 4537 164

(27%)

(4%)

45NEDBANK GROUP LIMITED – Annual Results '17ar

25

5

10

11

2

7

22 21 22

2

3

13 14 15 16 17

Tier 4 Tier 3 Tier 2

Tier 1 Target

Growing our transactional banking franchise faster than the

market – ongoing new primary client wins in CIB

Primary client wins (#) Selected primary transactional account wins

Target = 25 p.a. 26

39

46NEDBANK GROUP LIMITED – Annual Results '17ar

Client solutions leading to significant wins

2017

2017

2017

2017

2017

Jointly acted as bookrunner in the placement of 19.1m shares into the market as part of its empowerment

entity’s BEE structure unwind

Appointed as co-MLA & coordinator to refinance and upsize its existing

US $250m revolving credit facility

Jointly mandated to lead MTN’s first local bond issuance in four years raising R2.5bn Capital raising of R1bn through the debt

capital market

Appointed as joint lead bookrunner for the second consecutive year for the National

Treasury’s dollar-denominated bond issuance in the international debt capital

markets

Appointed as the primary banker to the Parliament of RSA for a second

consecutive 5−year term

Successfully raised R500m Tier 2 subordinated debt for Old Mutual Insure

Appointed as the primary banker to the Sedibeng District Municipality for a

5−year term

2017

20172017

BOOKLET SLIDE

2017

Re-appointed as the primary banker to the Western Cape Government (WCG) for a

third consecutive five-year term

47NEDBANK GROUP LIMITED – Annual Results '17ar

Delivering innovative market-leading client experiences

Executive EySightTM

Real-time client & management

information insight

Robotics Process Automation

Improve efficiencies, accuracy

& quality of work

Technology

Enhancing client experiences

Client

Intelligence

Platform

Executive

EySightTM

First implementations delivering benefits Implementations | Pilots

Cross-sell & client servicing benefits

135 processes identified

Potential cost-savings in man hours

Insight into client cross-or up-sell

opportunities

Continuous enhancements leading to

management insights & predictive

analytics

Implementation of systems to enhance client experience

Continuous testing of disruptive technologies to improve the way we do business

48NEDBANK GROUP LIMITED – Annual Results '17ar

Prospects for Corporate & Investment Banking

A powerful wholesale business focused on its clients

Renewed optimism in the country hopefully leading to an increase in SA corporate investment

Good pipeline that is expected to convert as business confidence improves

Leveraging off strategic partners to benefit clients on the continent & globally

Continued focus on people with a shift towards ‘digital’ talent

2018: Headline earnings growth in line with nominal GDP growth

2020 targets:

ROE ≥ 20% − maintain strong returns

Cost to income ≤ 40% − leverage technology to retain industry-leading efficiency ratio

49NEDBANK GROUP LIMITED – Annual Results '17ar

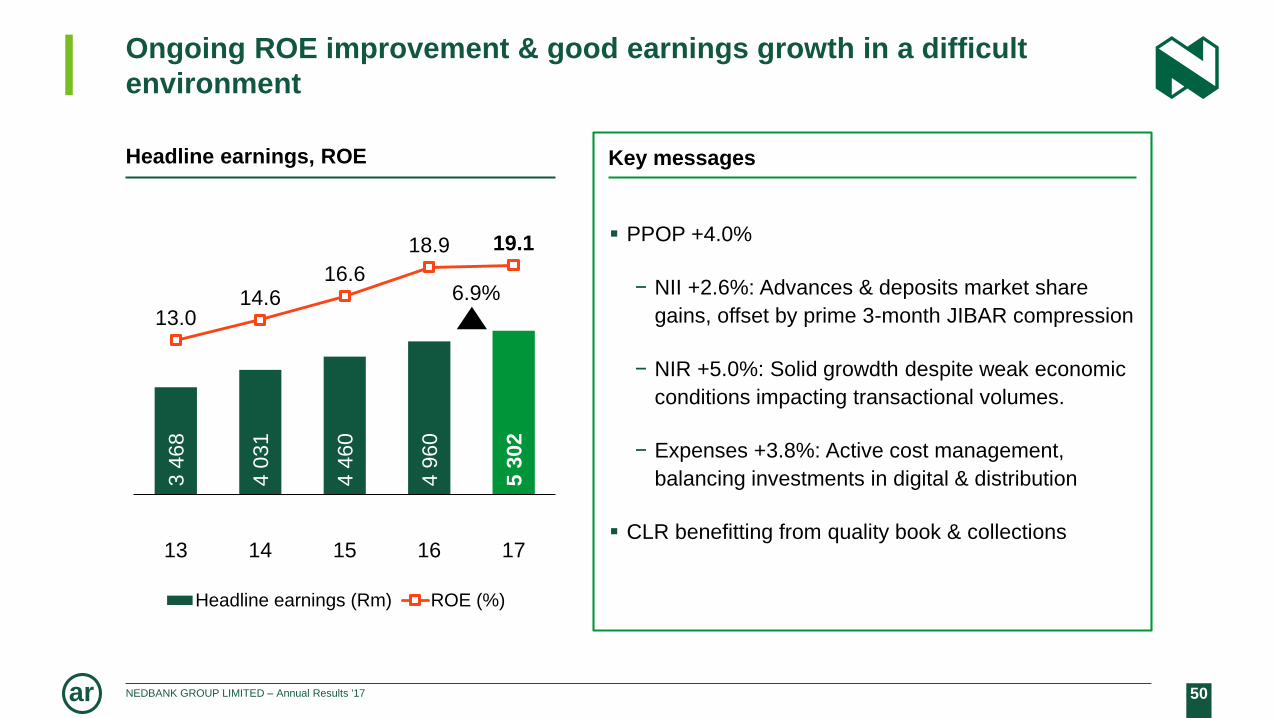

Ongoing ROE improvement

and good earnings growth

in a difficult environment

NEDBANK RETAIL

& BUSINESS

BANKING

CIKO THOMAS

50NEDBANK GROUP LIMITED – Annual Results '17ar

3468

40

31

44

60

49

60

53

02

13.014.6

16.6

18.9 19.1

-2.0

3.0

8.0

13.0

18.0

23.0

28.0

(1 000)

1 000

3 000

5 000

7 000

9 000

11 000

13 14 15 16 17

Headline earnings (Rm) ROE (%)

Ongoing ROE improvement & good earnings growth in a difficult

environment

Key messages

PPOP +4.0%

− NII +2.6%: Advances & deposits market share

gains, offset by prime 3-month JIBAR compression

− NIR +5.0%: Solid growdth despite weak economic

conditions impacting transactional volumes.

− Expenses +3.8%: Active cost management,

balancing investments in digital & distribution

CLR benefitting from quality book & collections

Headline earnings, ROE

6.9%

51NEDBANK GROUP LIMITED – Annual Results '17ar

45%55%

Headline earnings

33%

67%

Assets

Nedbank RBB Other clustersYear ended % change 2017 2016

Headline earnings (Rm) 6.9 5 302 4 960

Operating income (Rm) 4.1 26 880 25 810

PPOP (Rm) 4.0 10 606 10 199

Net interest margin (%) 5.81 6.08

NIR-to-expense ratio (%) 64.3 63.6

Efficiency ratio (%) 63.6 63.4

Credit loss ratio (%) 1.06 1.12

Average banking advances (Rm) 4.2 294 930 282 992

Average deposits (Rm) 9.2 281 779 257 968

Headline economic profit 1 (Rm) 13.3 1 394 1 230

Allocated capital (Rm) 5.9 27 812 26 254

ROE (%) 19.1 18.9

Retail & Business Banking – financial highlights BOOKLET SLIDE

1 Cost of equity 2016: 14.2%. | 2017: 14.0%.

52NEDBANK GROUP LIMITED – Annual Results '17ar

3 713 4 019 4 184

1 385 1 430 1 616

4 223 4 566

4 737

15 16 17

Retail transactional NIR growth ahead of client growth – deeper

client penetration

Total retail client base (#000) Retail NIR (Rm)

4 377 4 633 4 755

2 703 2 784 2 783

15 16 17

Retail excl

main-

banked

Total7 5387 417

7 080

+4.8%

+3.0%

0.0%

Main-

banked

+1.6%

Transactional

Other

Total

10 0159 321

+5.2%

+7.4%

+6.0%

+6.9%

10 537

Consumer

card issuing

53NEDBANK GROUP LIMITED – Annual Results '17ar

Client-centred strategy intact but measure impacted by the

macro environment

Main-banked, # 000K

ids &

yo

uth

Entr

y le

ve

lM

idd

le

Pro

fessio

na

lS

ma

ll B

usin

ess

Bu

sin

ess

Ba

nkin

g1

1 Client groups with gross operating income contributions in excess of R500 pm.

Note: Non-resident, non-individual segment not shown.

15 16 17

739 786 797

+6% +1%

1615

107

17

101 113

+6% +6%

7066 68

+4% +3%

382407 410

+1% (7%)

22,2 22,3 22,4

0% +1%

1 404 1 4111 381

+2% +1%

54NEDBANK GROUP LIMITED – Annual Results '17ar

Good progress in growing main-banked market share

9.0% 9.5% 9.4%8.8%

9.6%10.1%

12.7%

1210 11 13 1714 1615

Nedbank main-banked market share (%)

AMPS

Consulta

Same question asked:

‘Which ONE bank do you regard as your main bank for personal banking?’

AMPS

discontinued

55NEDBANK GROUP LIMITED – Annual Results '17ar

Good growth in consistently active main banked clients

Total retail

clients

Transactional

clients1

Active

clients2

Main-banked

clients

Retail client base breakdown (#000)

Consistently active

clients3

2 7832 784

6 026

7 417 7 538

5 925

3 7463 870

1 723 1 795

16 17

YOY% Growth

+1.6%

+1.7%

(3.2%)

0.0%

+4.2%

1 Clients with a transactional product. | 2 Active clients within the last 6 months. | 3 Main-banked for each of the past 12 months.

Definition of main-banked clients: Youth & ELB ≥ 3 debits, 1 credit ; Middle market ≥ 6 debits, 1 credit ; Professionals ≥ 12 debits, 1 credit ; SBS ≥ 25 debits ; All over 3-month period.

56NEDBANK GROUP LIMITED – Annual Results '17ar

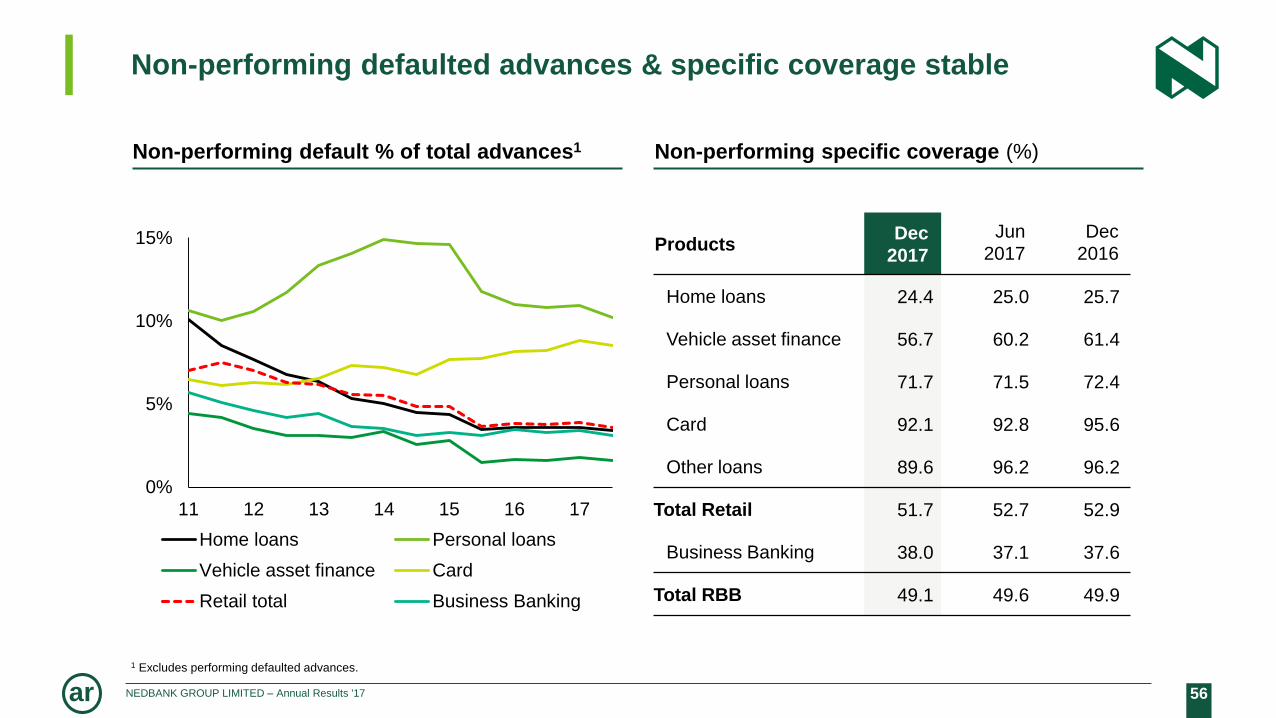

Non-performing defaulted advances & specific coverage stable

ProductsDec

2017

Jun

2017

Dec

2016

Home loans 24.4 25.0 25.7

Vehicle asset finance 56.7 60.2 61.4

Personal loans 71.7 71.5 72.4

Card 92.1 92.8 95.6

Other loans 89.6 96.2 96.2

Total Retail 51.7 52.7 52.9

Business Banking 38.0 37.1 37.6

Total RBB 49.1 49.6 49.9

0%

5%

10%

15%

11 12 13 14 15 16 17

Home loans Personal loans

Vehicle asset finance Card

Retail total Business Banking

Non-performing default % of total advances1 Non-performing specific coverage (%)

1 Excludes performing defaulted advances.

57NEDBANK GROUP LIMITED – Annual Results '17ar

Personal loans well positioned from a credit risk & regulatory

perspective

Product & policy

summaryNedbank Market1

Maximum term

(months)60 84

Minimum term

(months)12 1

Maximum loan

amount250k 350k

Restructuring policy

Debt

counselling

only

Yes

Readvances to

clients in arrearsNo Unknown

Nedbank practices

Recent growth primarily in low & low-to-medium

risk categories

Current term offering more conservative than the

industry (no pay-day loans)

Maximum loan below industry, but increased to

R250k for best-risk customers only

Do not restructure accounts other than those

accounts in debt counselling (DC)

Do not settle internal loans in arrears or who

have previously been restructured with a re-

advance

1 Based on market information as available; includes traditional four banks & material providers of personal loans. It reflects the maximum or minimum available from 1 or more market competitors

58NEDBANK GROUP LIMITED – Annual Results '17ar

Accelerated digitisation of technology & operations

Change in 2017Deposit volumes (# 000)

48%

2015

23%

2017

34%

2016

27 81829 594 29 256

+3%

Traditional deposits Self-service deposits

>100%

(5%)

30%

Launched 2017

21%

38%

18%

(13%)

130k

39%

Digital clients1 (# 000)

5 784

Enabled

5 3442

3 354

+31%

Dec’15 Dec’17Dec’16

891

Active

788852

+6%

Devices

Intelligent Depositors

ATMs

Video bankers

Self-service kiosks

Interactive tellers

Volumes

Digital volumes

Total App usage

Money App registrations

ID deposits

Teller activity

1 Digitally enabled & active clients have been restated to include all digital channels & to allow for only last 90 days of recent activity.2 Growth largely as a result of the Digital Activation Programme run in Q4 2016.

59NEDBANK GROUP LIMITED – Annual Results '17ar

Floor space saved

(m2)

639 593

453391

277

171

255304

336

10 14 15 16 17

Traditional New-image

Integrated channels – efficient use of space & staff,

optimising branch footprint

10 14 15 16 17

Outlets format mix

(#)

Total & new-image outlets

(#)

13 695

18 743

764708 695

7 273

Cumulative target >30 000 m2

by 2020

639

452 500 504 507 512

4371 55 40 0

144

193149 148

101

10 14 15 16 17

Branches Personal Loans

Inretailers

764708 695

63924 485613 613

BOOKLET SLIDE

60NEDBANK GROUP LIMITED – Annual Results '17ar

Cost initiatives – contributor to ongoing efficiencies & savings

313 Initiatives

Credit

Evolved distribution

Organisation

simplification

Procurement

Operational excellence

Branch optimisation – slowdown in new rollouts, closure

of 53 inretailers & 32 personal-loan outlets & 10

branches

Sales & service integration & reducing layers of

management – headcount reduction of 267

Self-service initiatives – 46 new video bankers, 234 new

Intelligent Depositors, 249 self-service kiosk & 200k

statements processed on IDs monthly

Credit function simplification in BB & operational

improvements in NRR & Debt Collections

Adoption of robotic automation (33 robots deployed)

Support function optimisation, eg finance, human

resources & risk

Rationalise vendor list

PET (Professional fees, entertainment & technology

spend) savings achieved

RBB initiatives Total RBB employees (#)

Efficiencies (Rm)

21 305 20 243

16 17

358444

16 17

61NEDBANK GROUP LIMITED – Annual Results '17ar

Delivering innovative market-leading client experiences

UNLOCKED.ME

Innovative lifestyle e-commerce platform

Banking’s first

UNLOCKED.ME brings together three pillars, It is a

platform which will allow you to unlock your lifestyle,

your potential and your money.

It is full of unique experiences, sure to thrill our youth

target audience. It is our first lifestyle market place,

designed with our clients in mind.

Payment solutions

Winning in digital

Worldclass banking apps

The Nedbank Money app features user-centred

design for basic banking with self service

capabilities.

The Karri App is an integrated, mobile payment

solution, to reduce the handling of cash at

schools

Digital branch

SA’s first digital branch

– entirely self-service

Leading in digital outlets

Launched at Gautrain Sandton Station (Sept ‘17)

Technology available: Intelligent Depositor, video

banking, quick-chat banking, self service kiosk,

virtual reality, grab-and-learn wall, interactive demo

station, facial recognition

62NEDBANK GROUP LIMITED – Annual Results '17ar

Prospects for Retail & Business Banking

Building sustainable, profitable businesses through the cycle

Grow transactional clients faster than the market through focus on acquisition, retention & cross-sell, enabled by:

− Digital First, First in Digital – accelerate digitisation of key client journeys & services to make it simple & easy for

clients to transact with us

− Disruptive CVPs – accelerate financial inclusivity of our banking propositions & to find ways to reduce transacting

costs for our clients, & tapping into ecosystem-based propositions

− Sales & service excellence – continue to innovate & rollout digital branches to enable clients to migrate to digital

channels, & empower our staff with digital tools to serve clients

− Loyalty & rewards – deliver new differentiated loyalty & reward programme

2018: Headline earnings growth in line with nominal GDP (H1 2018 growth likely to be slower than H2 2018)

2020 targets:

ROE ≥ 20% − ongoing improvement, underpinned by lower cost-to-income ratio & relative CLR outperformance

through the cycle

Cost to income ≤ 58% − enabled by improved client experience, transactional market share gains, continued quality

origination & operational efficiencies

63NEDBANK GROUP LIMITED – Annual Results '17ar

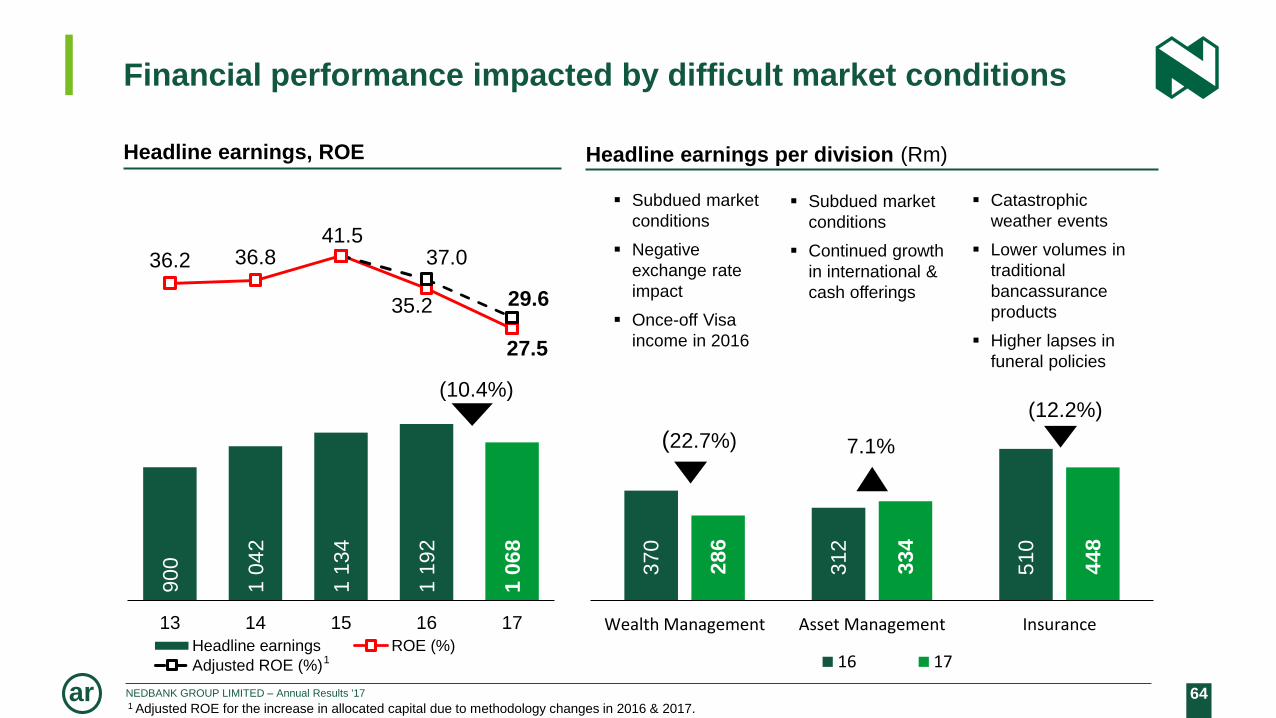

A challenging year

NEDBANK

WEALTH

IOLANDA RUGGIERO

64NEDBANK GROUP LIMITED – Annual Results '17ar

90

0

10

42

11

34

11

92

10

68

36.2 36.841.5

35.2

27.5

37.0

29.6

13 14 15 16 17

Headline earnings ROE (%)

Adjusted ROE (%)

Financial performance impacted by difficult market conditions

Headline earnings, ROE

(10.4%)

Headline earnings per division (Rm)

370

31

2

51

0

28

6

33

4

44

8

Wealth Management Asset Management Insurance

16 17

Catastrophic

weather events

Lower volumes in

traditional

bancassurance

products

Higher lapses in

funeral policies

Subdued market

conditions

Continued growth

in international &

cash offerings

Subdued market

conditions

Negative

exchange rate

impact

Once-off Visa

income in 2016

1 Adjusted ROE for the increase in allocated capital due to methodology changes in 2016 & 2017.

1

(22.7%) 7.1%

(12.2%)

65NEDBANK GROUP LIMITED – Annual Results '17ar

Year ended % change 2017 2016

Headline earnings (Rm) (10.4) 1 068 1 192

Operating income (Rm) 0.1 4 367 4 362

PPOP (Rm) (11.2) 1 396 1 572

Net interest margin (%) 2.15 2.15

NIR-to-expense ratio (%) 117.7 126.1

Efficiency ratio (%) 65.6 61.7

CLR (%) 0.09 0.08

Assets under management (Rbn) 14.3 312 313 273 327

Life embedded value (Rm) 0.2 2 745 2 740

Life value of new business (Rm) (12.5) 349 399

Headline economic profit 1 (Rm) (26.6) 522 711

Allocated capital (Rm) 14.7 3 885 3 387

ROE (%) 27.5 35.2

BOOKLET SLIDE

9%

91%

Headline earnings

Wealth Other clusters

Net inflows R28.5bn

Life APE (7.9%)

Non-life GWP +2.3%

Wealth – financial highlights

1 Cost of equity 2016: 14.2%. | 2017: 14.0%.

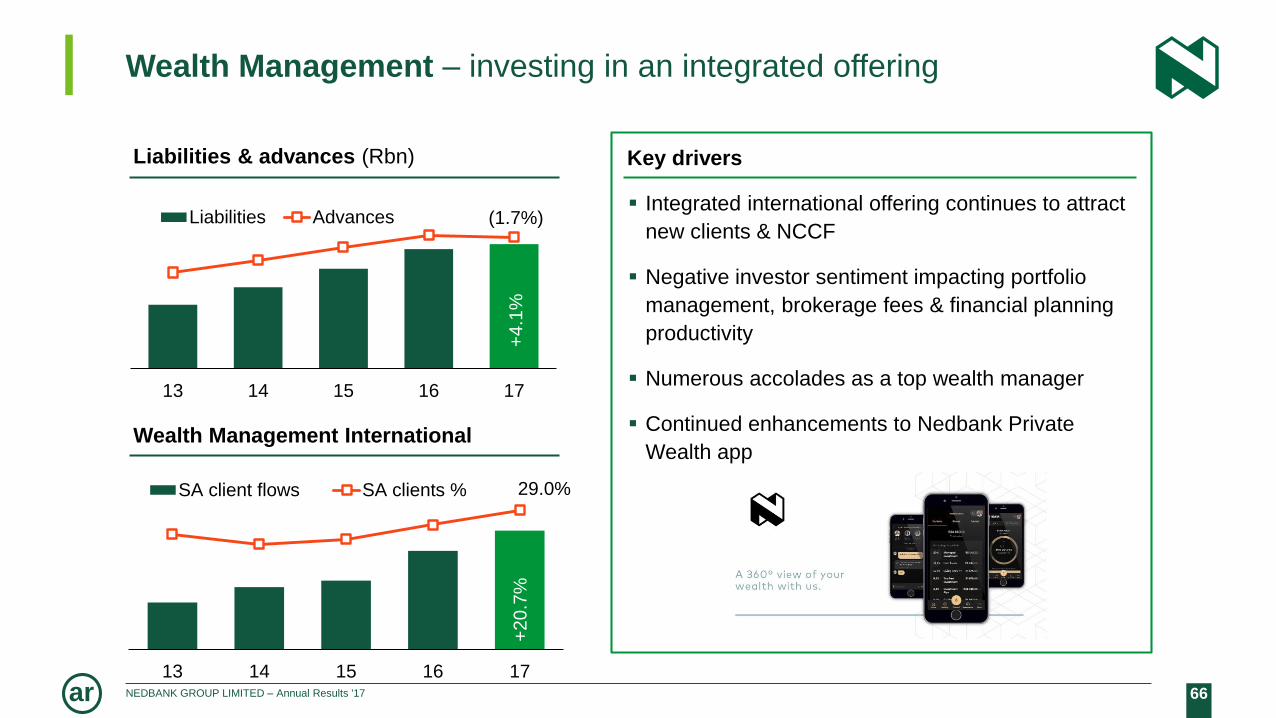

66NEDBANK GROUP LIMITED – Annual Results '17ar

+4.1

%

(1.7%)

13 14 15 16 17

Liabilities Advances

Wealth Management – investing in an integrated offering

Key drivers

Integrated international offering continues to attract

new clients & NCCF

Negative investor sentiment impacting portfolio

management, brokerage fees & financial planning

productivity

Numerous accolades as a top wealth manager

Continued enhancements to Nedbank Private

Wealth app

Liabilities & advances (Rbn)

Wealth Management International

+2

0.7

%

29.0%

13 14 15 16 17

SA client flows SA clients %

67NEDBANK GROUP LIMITED – Annual Results '17ar

190212

257273

312

13 14 15 16 17

Local International

Asset Management – a solid performance

Key drivers

4th-largest UT manager & 3rd-largest offshore

manager in SA

Maintained position as top offshore manager in SA

for third consecutive year

Leading net flows of R28.5bn

Digitisation of business processes & development

of innovative solutions such as chatbot & robo-

advisor

Assets under management (Rbn)

Market share1 (%)

14.3%

1 Source: ASISA

09 10 11 12 13 14 15 16 17

SA unit trust FSB approved offshore unit trust

8%

11%

5%

1%

68NEDBANK GROUP LIMITED – Annual Results '17ar

399

349

-

50

100

150

200

250

13 14 15 16 17

Insurance – a tough year

Key drivers

Earnings impacted by catastrophic weather events

resulting in higher claims & lower volumes in

traditional bancassurance products, partially offset

by a release of reserves

Decline in VNB driven by lower single-premium

investment policies, an increase in lapses & funeral

acquisition costs as well as pressure on margins

Digital solutions launched, including chatbot &

geyser telemetry

Life value of new business (Rm)

Non-life gross written premiums (Rm)

(12.5%)

1 1

18

1 1

44

13 14 15 16 17

2.3%

69NEDBANK GROUP LIMITED – Annual Results '17ar

Delivering innovative market-leading client experiences

Chatbot, robo-advisor &

geyser telemetry

Developing innovative solutions

Systems & processes

Digitising business processes

Unique in marketStraight through

processing

Nedbank Private Wealth app

Best-in-class client experience

& full financial suite of digital services

Rated one of the best HNW apps globally

1 Rated 6th out of 34 apps globally in the Mobile Apps for Wealth Management 2017 survey

Reduced

paperworkSame-day

processing

Safe &

secure

Market-leading robo-advisor

Chatbot, NIC, a pioneering digital insurance assistant.

First in market in the African insurance industry

Chatbot, EVA, allows simple transactions 24/7.

First in market in the SA asset management industry

Geyser telemetry, innovative connected home solution.

First in the SA banking market

Focus on digitising processes in asset management

Enhancing client onboarding experience in wealth &

asset management

Single-policy administration system for life & non-life

insurance

Independently rated a top SA high-net-worth banking

app & 6th-best globally1

App provides international & local consolidated view

of assets & liabilities

70NEDBANK GROUP LIMITED – Annual Results '17ar

Prospects for Nedbank Wealth

Building client-centred businesses

Enhanced client value propositions through accelerated digital innovation, investment in systems &

brand positioning

Delivering long-term investment performance & driving market share growth

Exploring new opportunities for growth & deepening group collaboration

2018: HE growth in line with nominal GDP, benefiting from expected improvement in market &

investor sentiment

2020 targets:

ROE ≥ 30% − benefiting from high EP businesses

Cost to income ≤ 60%

71NEDBANK GROUP LIMITED – Annual Results '17ar

SADC – investing for growth

and driving client value

ETI – steady progress,

outlook improving

REST OF AFRICA

MFUNDO NKUHLU

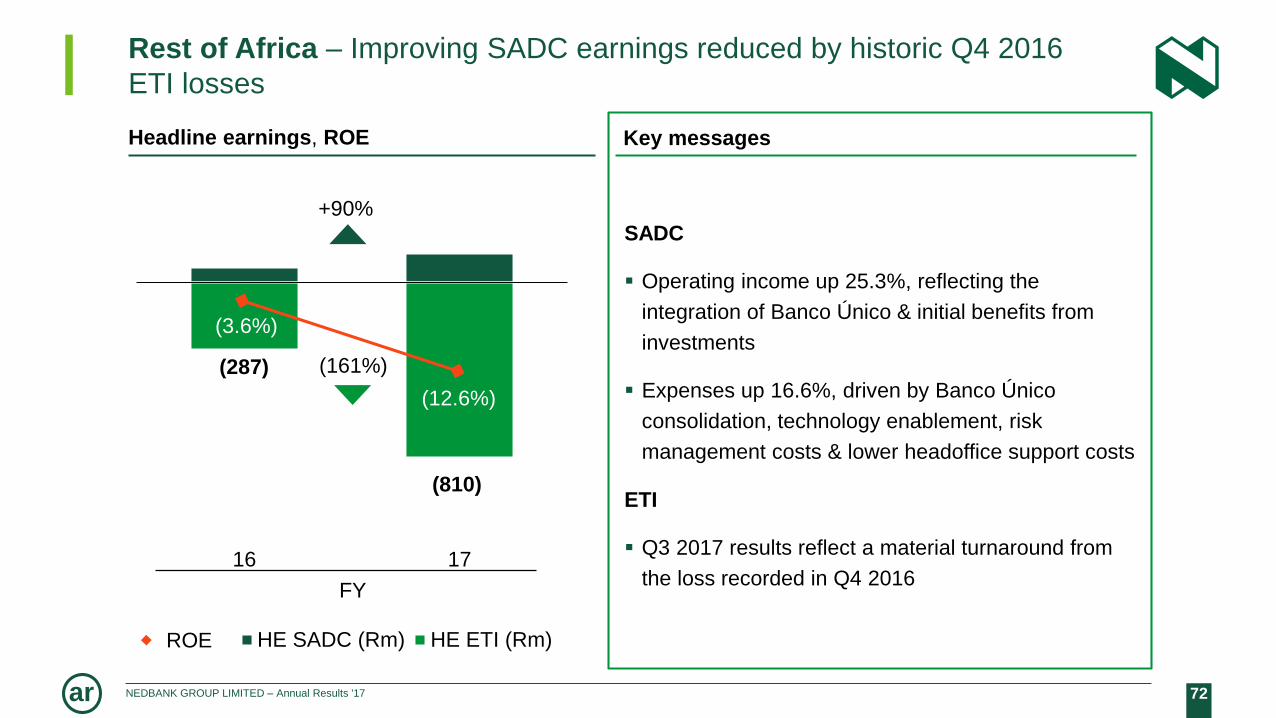

72NEDBANK GROUP LIMITED – Annual Results '17ar

-15

-10

-5

0

5

10

-1400.0

-1200.0

-1000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

16 17

HE SADC (Rm) HE ETI (Rm)

Rest of Africa – Improving SADC earnings reduced by historic Q4 2016

ETI losses

Headline earnings, ROE

+90%

(287)

(810)

FY

(161%)

Key messages

SADC

Operating income up 25.3%, reflecting the

integration of Banco Único & initial benefits from

investments

Expenses up 16.6%, driven by Banco Único

consolidation, technology enablement, risk

management costs & lower headoffice support costs

ETI

Q3 2017 results reflect a material turnaround from

the loss recorded in Q4 2016

(3.6%)

(12.6%)

ROE

73NEDBANK GROUP LIMITED – Annual Results '17ar

4%

96%

Assets

Rest of Africa Other clusters

Rest of Africa – financial highlights

NEDBANK GROUP LIMITED – ANNUAL RESULTS ‘17

Year ended % change 2017 2016

SADC

Headline earnings (Rm) 89.7 165 87

Operating income (Rm) 25.3 2 579 2 058

PPOP (Rm) 67.5 449 268

Net interest margin (%) 7.14 6.69

NIR-to-expense ratio (%) 45.3 46.5

Efficiency ratio (%) 78.8 82.9

Credit loss ratio (%) 1.02 0.98

Average banking advances (Rm) 14.9 20 366 17 724

Average deposits (Rm) 19.4 28 061 23 492

Headline economic profit 1 (Rm) (8.8) (534) (491)

Allocated capital (Rm) 22.2 4 981 4 076

ROE (%) 3.3 2.1

ETI investment

Headline earnings (Rm) (>100) (975) (374)

Total headline earnings (>100) (810) (287)

(7%)

107%

Headline earnings

BOOKLET SLIDE

1 Cost of equity 2016: 14.2%. | 2017: 14.0%.

74NEDBANK GROUP LIMITED – Annual Results '17ar

156

68

178

73

28

19

30

20

SADC – Enhanced client value propositions to drive growth

Clients (# 000)

Branches & ATMs

Other subsidiariesBanco Único

Investments made

… with the following key outcomes

Enhanced digital channel access

Deeper client relationships

Improved client value propositions

Improved service

Improved risk management capabilities

Banking app (#000)

Online activations (#000)

18

462

4

+148%

29 36

910

+22%

4638

50

20

274 314

2122

+14%

336

1716

295

Core banking systems Mobile platforms

Risk management

Payment solutionsCard offering

BranchATM BranchATM

184

87

208

93

1716

1716 1716

75NEDBANK GROUP LIMITED – Annual Results '17ar

SADC – Delivering innovative market-leading client experiences

Transactional

Online product application &

debit order switching

Insurance

Life & funeral cover offering

Improved value propositions

Build bancassurancebusiness

Digital

A unique mobile banking solution

for business

Leading in digital

Banco Único Mozambique MBCA1Nedbank Namibia 1 To be rebranded Nedbank Zimbabwe in H1 2018

76NEDBANK GROUP LIMITED – Annual Results '17ar

ETI – Steady progress on a recovery path for 2017

Macroeconomic environment improving Progress in strategic turnaround led by ETI board

Changes to the board composition & MIS representation on various board subcommittees

Strengthened ETI management team

Conclusion of the US $400m convertible bond issue in September 2017

Financial turnaround, as reflected by:

− Audited H1 2017 results

− Solid Q3 2017 performance

− ETI management guidance for FY 2017

Increasing levels of collaboration between Nedbank & ETI

1 IMF forecasts

7.7

3.5

(1.6)

6.7 6.8

0.8

6.67.7

2.2

Côte d'Ivoire Ghana Nigeria

GDP growth forecasts1

17 18

Key ETI markets

16

77NEDBANK GROUP LIMITED – Annual Results '17ar

Nedbank – Ecobank collaboration – integrated crossborder transfer

solution (initially outbound only)

African migrants

2.7m

Market size: Remittance

value SA – Rest of Africa

R14−19bn

Through mobile/digital

channels internationally

25%

Through international cash

transfers

60%

Through traditional banking

channels internationally

5%

Access & distributionOpportunity Differentiation 1

Lowest cost to client in the

industry (no third parties)

Cheap

Instant cross border transfer

– subject to regulatory &

compliance checks (other

solutions 10 min to 2 days)

Quick

Usage across all channels

– initially account to account,

mobile app & website.

Moving to wallet, USSD,

ATM, branches, etc

Available in 33 countries

24 hours – initially business

operating hours, moving to

24/7

Easy

1 Key competing products include Mukuru, hello (PAISA), Western Union (BGA), MoneyGram (FNB & Standard Bank)

78NEDBANK GROUP LIMITED – Annual Results '17ar

Prospects for Rest of Africa

SADC

Create shared value with clients from investments made & reposition the business for the digital age

through improved client experience, improved data analytics, work with partners to accelerate digital

capabilities, implement regional talent management programme & enhanced risk management.

ETI

Shareholders are supportive of the strategic agenda

Leveraging the investment in ETI by:

− capitalising on improved growth prospects across the region, especially West Africa

− exploiting opportunities for greater collaboration

2018: From a headline earning loss in 2017 to a profit in 2018 – expect to be the largest contributor to the

Nedbank Group’s earnings growth rate in the year ahead

2020 targets:

ROE ≥ cost of equity1

Cost-to-income ≤ 60% − creating scale from investments & cost optimisation

1 COE approximately 16%

79NEDBANK GROUP LIMITED – Annual Results '17ar

Ongoing delivery into 2018,

supported by recovery in ETI, laying

the foundation for 2020 targets

STRATEGY & 2018

GUIDANCE

MIKE BROWN

80NEDBANK GROUP LIMITED – Annual Results '17ar

Looking forward

2018 has started with renewed optimism & the structural challenges remaining will be tackled.

Improving business & consumer confidence should lead to cyclical economic upturn off a low base

Momentum in delivering on our strategic focus areas – enhancing client experiences & improving

levels of efficiency through digital innovation is key focus for 2018

Old Mutual managed separation to be materially complete in 2018 – for Nedbank this provides

increased shareholder certainty with free float benefits & for clients & staff it remains business as usual

2018 guidance – stronger earnings growth than in 2017

– Revenue growth recovery off low base

– Ongoing focus on expense optimisation & risk management

– ETI turnaround is a key driver

2020 targets – pathway to ongoing & sustainable improvements in key metrics that support

shareholder value creation

81NEDBANK GROUP LIMITED – Annual Results '17ar

Cyclical economic upturn off a low base

Prospects

Clients

– Increasing levels of consumer & business

confidence. Initial benefits likely in CIB & Wealth

Balance sheet

– Stronger wholesale & retail advances growth

– Liquidity metrics & capital levels to remain

strong

Income statement

– Revenue growth in 2018 higher than 2017

– Impairments to increase cyclically; & IFRS 9

impact

– Expenses continue to be well managed

Assets under management

– Good growth, particularly in cash & offshore

2017 2018 2019 2020

GDP SA 0.9% 1.6% 1.8% 2.4%

GDP SSA 2.4% 3.2% 3.5% 3.5%

Inflation (CPI) 5.3% 5.1% 5.5% 5.5%

Industry credit

growth5.0% 6.5% 7.9% 10.1%

Average prime

interest rate10.4% 10.3% 10.3% 10.7%

Macroeconomic drivers1 (%)

1 Assuming no local currency downgrade | All Nedbank economic unit forecasts as

at 15 February 2018 | GDP SSA as per World Bank.

82NEDBANK GROUP LIMITED – Annual Results '17ar

Strategic focus areas – enhancing client experiences & efficiency through

digital innovation is a key focus for 2018

Delivering innovative market-leading client experiences

Growing our transactional

banking franchise faster

than the market

Being

operationally excellent

in all we do

Managing scarce resources

to optimise economic

outcomes

Providing our clients with

access to the best financial

services network in Africa

Delivered in 2017 … … launching in 2018

Managed Evolution – rationalise, simplify & standardise

core systems (reduced by 122, < 60 by 2020)

Digital Fast Lane & New Ways of Work – more client-

focused, competitive, digital & agile

New apps – Nedbank Private Wealth (rated 6th globally),

Nedbank Money, Karri (school payments)

Channels – NZone (self-service digital branch), Solar

Turtle (deep-rural solar-powered branch), Intelligent

Depositors, video banking

Business optimisation – Executive EySightTM, Robotic

Process Automation (50 software robots)

Pilots – Chatbots, robo-advisors, Blockchain

Platforms – UNLOCKED.ME (millennial market place),

Refreshed Nedbank internet banking platform

Simplified client onboarding – convenient, FICA-

compliant account opening from your couch

Ability to sell an unsecured loan bundled with a

transactional account

New Loyalty & reward programme

Geyser telemetry – reduce electricity usage

Stokvel – a community savings solution

Further rollout of software robots, artificial intelligence,

robo-advisors, chatbots

Integration with ETI remittance app to reach 2.7m people

83NEDBANK GROUP LIMITED – Annual Results '17ar

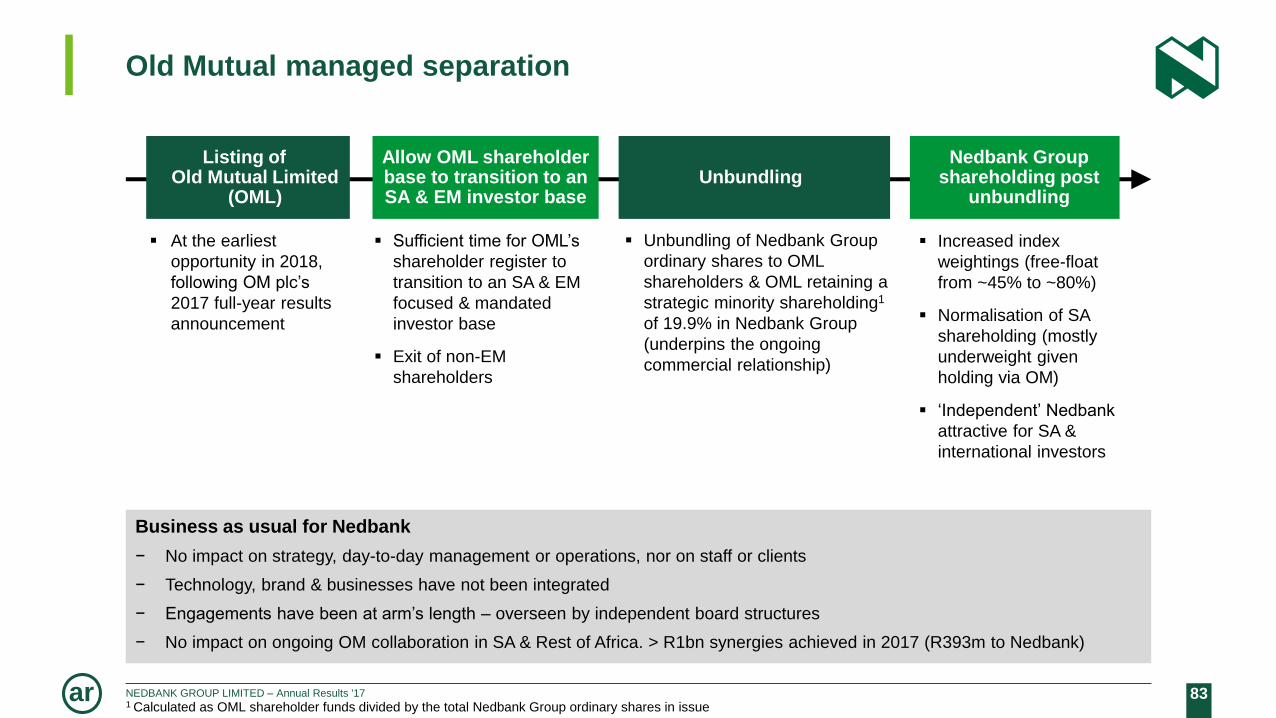

Listing of Old Mutual Limited

(OML)

Old Mutual managed separation

Business as usual for Nedbank

− No impact on strategy, day-to-day management or operations, nor on staff or clients

− Technology, brand & businesses have not been integrated

− Engagements have been at arm’s length – overseen by independent board structures

− No impact on ongoing OM collaboration in SA & Rest of Africa. > R1bn synergies achieved in 2017 (R393m to Nedbank)

UnbundlingAllow OML shareholder base to transition to an SA & EM investor base

At the earliest

opportunity in 2018,

following OM plc’s

2017 full-year results

announcement

Unbundling of Nedbank Group

ordinary shares to OML

shareholders & OML retaining a

strategic minority shareholding1

of 19.9% in Nedbank Group

(underpins the ongoing

commercial relationship)

Sufficient time for OML’s

shareholder register to

transition to an SA & EM

focused & mandated

investor base

Exit of non-EM

shareholders

Nedbank Group shareholding post

unbundling

Increased index

weightings (free-float

from ~45% to ~80%)

Normalisation of SA

shareholding (mostly

underweight given

holding via OM)

‘Independent’ Nedbank

attractive for SA &

international investors

1 Calculated as OML shareholder funds divided by the total Nedbank Group ordinary shares in issue

84NEDBANK GROUP LIMITED – Annual Results '17ar

2018 guidance

Growth in DHEPS for full-year 2018 more than or equal to growth in nominal GDP +5%, supported by ETI recovery

Average interest-earning banking asset1 growth to increase in line with nominal GDP

growth

NIM slightly above the 2017 level of 3.62%

NII

To increase to within the bottom half of our target range of 60–100 bps (under IFRS 9)

Above mid-single-digit growth

Mid-single-digit growth

CLR

NIR

Expenses

To be positive (ETI associate income reported quarterly in arrear)Associate

income

85NEDBANK GROUP LIMITED – Annual Results '17ar

2020 & medium-to-long-term targets

Metric 2017 vs MLT

Medium-to-long-term

target (MLT) 2018 outlook 1 vs 2017

ROE (excl goodwill) 16.4% ▼5% above COE 3

(≥ 18% by 2020)Increase, but remain below MLT

Diluted HEPS growth 2.4% ▼ ≥ CPI + GDP growth + 5%Grow in line with MLT,

supported by ETI recovery

Credit loss ratio 49 bps ► 60–100 bpsIncrease to within the bottom half

of MLT (under IFRS 9)

NIR-to-expenses ratio 80.7% ▼ > 85%Increase, but

remain below MLT

Efficiency ratio 2 58.6% ▲50–53%

(≤ 53% by 2020)

Decrease, but

remain above MLT

CET 1 CAR

Tier 1 CAR

Total CAR

12.6%

13.4%

15.5%

▲

▲

▲

Basel III basis:

10.5–12.5%

> 12%

> 14%

Within

target range

Dividend cover 1.91 x ► 1.75 to 2.25 timesWithin

target range

1 2018 outlook based on current economic forecasts. | 2 Efficiency ratio includes associate income. | 3 Target to be revised should Nedbank make future acquisitions that

increase goodwill

▲

▲

▲

▲

▲

▲▲

86NEDBANK GROUP LIMITED – Annual Results '17ar

Nedbank Group – an attractive investment

An improving macroeconomic environment

Supportive global environment

Cyclical improvement in SA growth as confidence

levels improve with structural changes now more likely

Rest of Africa growth ahead of SA

Strong & growing franchises

CIB – strong wholesale franchise (ROE ≥ 20%)

benefiting as business confidence improves

RBB – ongoing revenue growth momentum, CLR

outperformance & efficiencies/ digital to drive

C:I ≤ 58% & ROE ≥ 20% by 2020

Wealth – attractive ROE business (≥ 30% by 2020)

leveraging Nedbank distribution

Rest of Africa

− ETI turnaround underway - share price up 65% in

2017

− Investments made to unlock scale in SADC

subsidiaries

KPIs that support shareholder value creation

2018 DHEPS growth ≥ nominal GDP growth + 5%

ROE (excluding goodwill) ≥ 18% by 2020

Cost to income ≤ 53% by 2020

Strong governance & enterprise wide risk management

Attractive valuation metrics

SA & EM flows likely to continue

Nedbank price to book at the lower end of SA peer

group

Nedbank dividend yield at the higher end of SA peer

group

Improved free-float post unbundling, with any overhang

reduced during transition of OML shareholder base

post OML listing & prior to Nedbank unbundling

Building a more digital, agile & competitive Nedbank

THANK YOU

88NEDBANK GROUP LIMITED – Annual Results '17ar

Nedbank Group – attractive relative valuation

Price : earnings1,2 (x)

12.210.8

16.0

13.9

21.7

9.6

NED BGA FSR SBK CPI EMbanks

Price : book1,2 (x) Dividend yield1,2 (%)

Source: 1 I-Net consensus as at 22 Feb 2018. | 2 EM banks include Brazil, Russia, Turkey & SA (Data from JP Morgan). | All data based on 1-year forward forecasts.

1.7 1.6

3.5

2.2

5.6

1.7

NED BGA FSR SBK CPI EMbanks

4.4

5.2

3.5

4.1

1.7

4.3

NED BGA FSR SBK CPI EMbanks

‘3 year forecast

EPS growth1

(CAGR %)7.4 6.3 9.8 10.2 20.0 10.4

BOOKLET SLIDE

89NEDBANK GROUP LIMITED – Annual Results '17ar

2020 targets – strategy in place to improve financial metrics in

RBB & RoA, while maintaining good returns in CIB & Wealth

Efficiency ratio Return on equity1

Nedbank

2017

Peer

average2

Nedbank

2020 target

Nedbank

2017

Peer

average2

Nedbank

2020 target

Nedbank Group 58.6% 54% ≤ 53% 16.4% 18% ≥ 18%

Corporate &

Investment Banking42.3% 48% ≤ 40% 20.7% 21% ≥ 20%

Retail & Business

Banking63.6% 56% ≤ 58% 19.1% 27% ≥ 20%

Wealth 65.6% 64% ≤ 60% 27.5% 24% ≥ 30%

Rest of Africa3 127.1% 54% ≤ 60% (12.6%) 19% ≥ COE

1 Nedbank ROE target at group excluding goodwill for comparability purposes. | 2 Peer averages based on Dec 2016 for BGA & SBK, June 2017 for FSR | CIB – BGA CIB,

RMB & SBK CIB | RBB – BGA SA RBB, FNB & Wesbank, SBK SA PBB, Wealth – BGA WIMI, RoA – BGA RoA (Barclays Africa acquisition), SBK RoA Legal 3 Rest of Africa includes ETI. COE estimated at >16%.

BOOKLET SLIDE

90NEDBANK GROUP LIMITED – Annual Results '17ar

59

21

57

65

42

77

11

46

5

11

78

7

06 07 08 09 10 11 12 13 14 15 16 17

Nedbank Group in a strong position

16.3

4.5

20.1

5.4

06–08 14–17Wholesale Retail

481584

1 363

08 09 17

(28%)

Global

financial

crisis

Headline earnings (Rm) Loan growth (CAGR %)

NII sensitivity for 1% change in

interest rates (Rm)

BOOKLET SLIDE

CAGR

13.4%

91NEDBANK GROUP LIMITED – Annual Results '17ar

0.45 0.470.70

08 09 H1 17

32.0 33.9 36.2

08 09 17

1 Core equity tier 1.

Nedbank Group in a strong position

Number of clients (m) NIR income contribution (%) Defaulted advances (%)

CET 1 ratio (%) Funding tenor (%) Coverage (%)

4.4 4.2

7.9

08 09 17

39.8

42.2

46.6

08 09 17

3.9

5.9

2.7

08 09 17

8.21

9.91

12.6

08 09 17

88% 4.4% (3.2)

BOOKLET SLIDE

2.7%

Sp

ecific

Po

rtfo

lio

60.9 57.9 51.2

19.9 21.021.8

19.2 21.1 27.0

08 09 17

ST

MT

LT

92NEDBANK GROUP LIMITED – Annual Results '17ar

3.0

3.1

3.2

3.3

3.4

3.5

3.6

Jan '16 Mar '16 May '16 Jul '16 Sep '16 Nov '16 Jan '17 Mar '17 May '17 Jul '17 Sep '17 Nov '17

Net interest margin – narrowing of prime−JIBAR spread in 2016 & 2017

Prime – 3-month average JIBAR spread (bps)

H2 2016

Ave: 345 bps Ave: 320 bps Ave: 320 bps

Narrowing of the prime−JIBAR

spreads 2017 vs 2016, continued

volatility due to political uncertainty &

prospects of sovereign-credit-rating

downgrades.

H2 2017

Ave: 317 bps

H1 2016

20172016Ave: 332 bps

NII: R77m

Ave: 318 bps

NII: (R151m)

H1 2017

BOOKLET SLIDE

93NEDBANK GROUP LIMITED – Annual Results '17ar

23

(2) (1)

1

(9)

Nedbank Retail & Business BankingNIM decline mainly due to the compressed spread between prime & the

3-month Jibar linked cost of funding

Funding cost impact (bps) Liability (bps)Endowment impact (bps)

Mix & volume change

impact (bps)

Asset pricing impact (bps)Net interest margin (bps)

559 497 582 608 581

32 6 3

(16)

(5)18

9

28

(0)

13 14 15 16 17

(5) (6)

6 5

(3)

13 14 15 16 17

(0) (1)

(13) (12)

1

13 14 15 16 17

BOOKLET SLIDE

94NEDBANK GROUP LIMITED – Annual Results '17ar

289

189

33247

14 13

(179) (18)

588

Trans-actional

Card Securedlending

Priceincreases

Other Cardmargin

Mix &activity

Personalloans

YOY NIRgrowth

1

Nedbank Retail & Business BankingNIR growth support by good volume growth, but muted by strategic choices & other factors

NIR growth (Rm)

2016 NIR growth (Rm)

Volume–related

+217 +332 +47 +176 +86 (97) +23 (31) +753

BOOKLET SLIDE

1 Includes average price increase of 4.6% implemented on 1 January 2017.