16

NEGOTIABLE INSTRUMENTS : CHEQUES

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | francis-watkins |

| View: | 228 times |

| Download: | 0 times |

NEGOTIABLE INSTRUMENTS :

CHEQUES

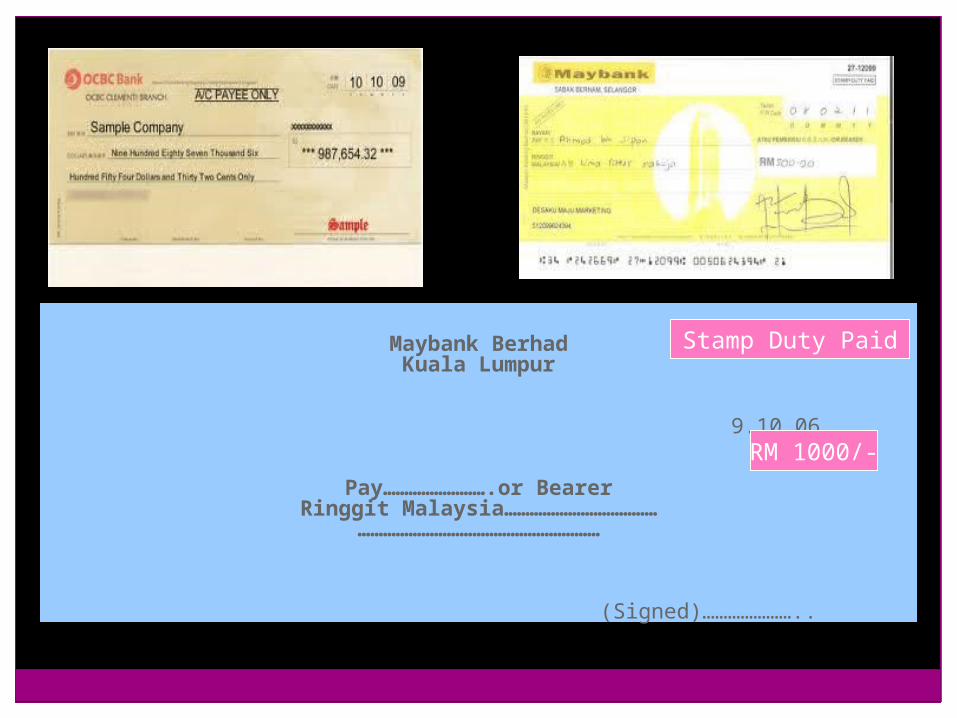

CHEQUE

• Def: S73 - a bill of exchange drawn on a banker & payable on demand.

• Characteristics:– Unconditional order in writing– It is signed by the drawer– It is drawn on the banker (drawee)– It orders the banker to pay sum certain in money on

demand– Drawn in favour of specified person (payee) or to his

order or in favour of a bearer

Maybank BerhadKuala Lumpur

9.10.06

Pay…………………….or BearerRinggit Malaysia………………………………

…………………………………………………

(Signed)…………………..

RM 1000/-

Stamp Duty Paid

Parties in a cheque

There are three parties to a bill; The drawer (who issued the bill) The drawee (who pays the bill / banker) The payee (who receives payment)

Person means a legal person and would include natural persons as well as firms and companies

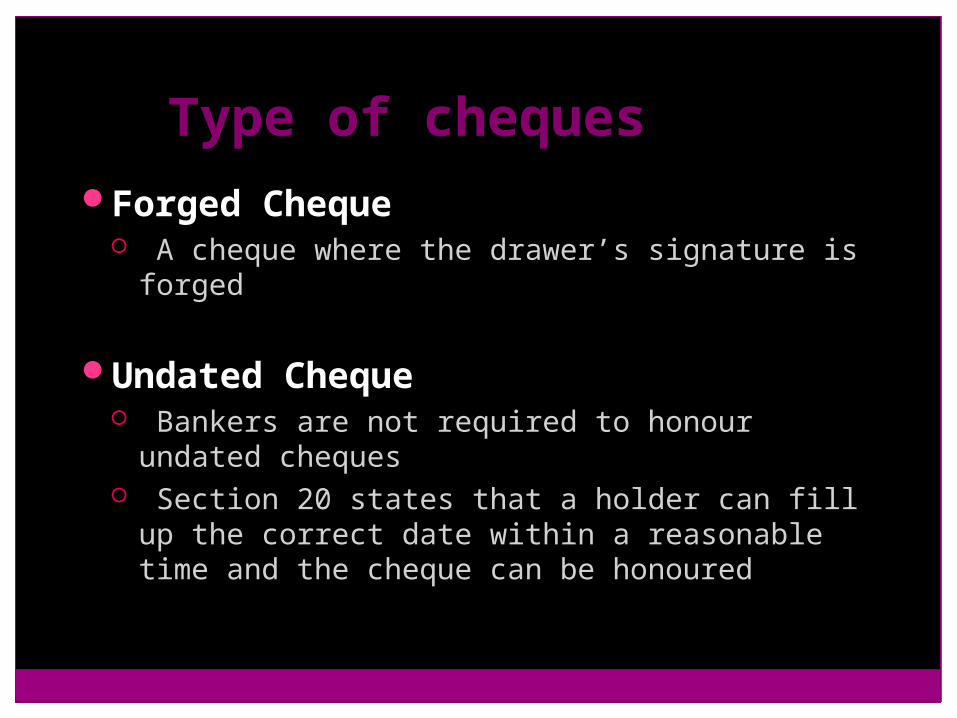

Type of chequesForged Cheque

A cheque where the drawer’s signature is forged

Undated Cheque Bankers are not required to honour undated

cheques Section 20 states that a holder can fill up the

correct date within a reasonable time and the cheque can be honoured

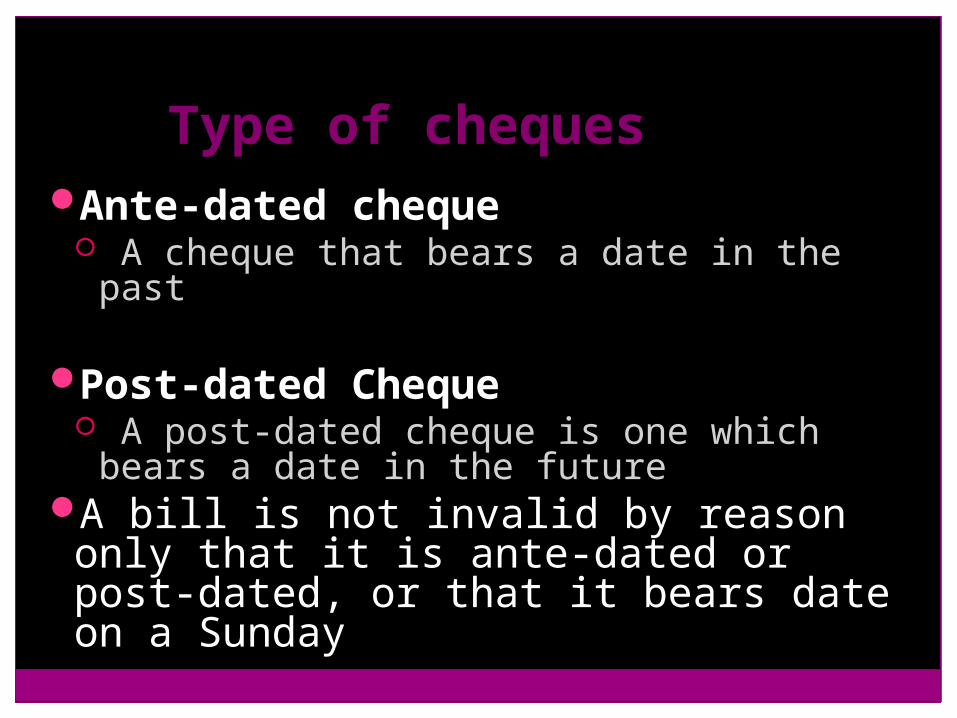

Type of chequesAnte-dated cheque

A cheque that bears a date in the past

Post-dated Cheque A post-dated cheque is one which

bears a date in the futureA bill is not invalid by reason only that it is ante-dated or post-dated, or that it bears date on a Sunday

Type of ChequesOverdue or Stale Cheque

An overdue cheque or stale cheque is one which has been in circulation for an unreasonable length of time

Section 36(3) Unreasonable length of time depends on the fact of

each case According to current banking practice in Malaysia,

a stale cheque is one which bears a date which is half a year old

i.e. six months or more have expired since the date of the cheque

CROSSING OF CHEQUETo make it difficult for an unauthorized person

such as a rogue to obtain payment across the counter.

A cross cheque can only be paid through bank.

TYPES OF CROSSINGS

GENERAL GENERAL CROSSINGSCROSSINGS

SPECIAL SPECIAL CROSSINGSCROSSINGS

General crossing….[S 76(1)]

It consists of two parallel lines drawn across the face of the cheque. Usually have words such as ‘Co.’ , ‘Not Negotiable’ or ‘A/C Payee’

• Effect of gen. crossings:

Loss character of negotiability

If the title of the transferor is defective, it will effect the title of the transferee even though he may not know the defect. Case: Wilson v Pickering

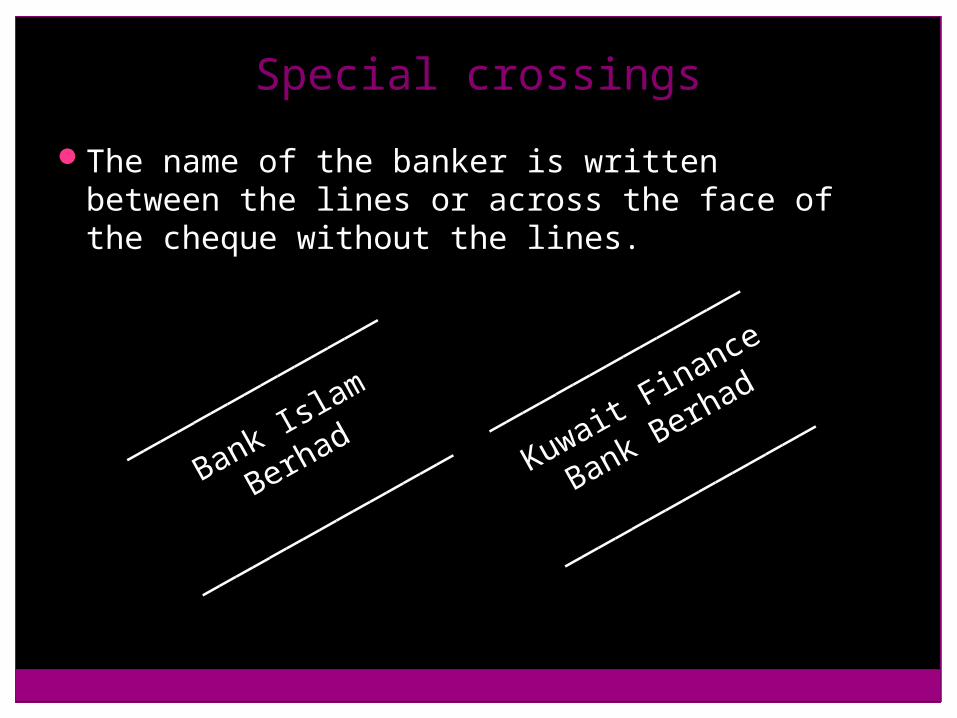

Special crossings

The name of the banker is written between the lines or across the face of the cheque without the lines.

_______________

_______________

Bank Islam Berhad

Bank Islam Berhad

_______________

_______________ _______________

_______________

Kuwait Finance

Kuwait Finance

Bank Berhad

Bank Berhad

_______________

_______________

Effect of special crossing

The paying banker must pay the amount of the cheque only to collecting banker named in the crossing.

The negotiability of the cheque is restricted, i.e. can only be negotiated to some person who is a customer of the bank to whom it is crossed.

Alteration on a cheque• Generally, a drawer will be discharged from

liability if the cheque has been altered without the drawer’s authority. If the bank pays on such cheque – the bank cannot debit the customer’s account.

• However - Customer’s duty of care against fraudulent alterations:– Customer must exercise due care in drawing

cheques to avoid fraud.• London Joint Stock Bank v Macmillan

A partner in a firm was negligent in drawing a cheque for $2 which was stated in figure but not in words.a clerk alter the figure to read $120 & wrote it in words before cashing the cheque at the bank. Held:the bank could debit the firm’s account with $120 due to negligent of the partner.

Protection of the paying banker

Paying banker = banker whereby a customer draws a cheque on him.

Duty = to pay the right person according to his customer’s mandate. If pay to wrong person, he must bear any loss.

S60 of BEA: the banker will not be liable if he can prove all the followings: Payment made after maturity of the bill, to the

holder in good faith without notice that his title to the cheque is defective.

– A paying banker is not protected if he pays a cheque drawn on him in which the drawer’s signature is forged coz he is expected to know his customers’ signature. However, he will be protected if it involved other persons who are not his customers.

– The banker is protected if he pays a cheque which is not indorsed or irregularly indorsed, in good faith and in the ordinary course of business.

– For crossed cheque, if paying banker pays to a person other than true owner, he will be protected if he had acted in good faith, without negligence and according to crossing.

Protection of the collecting bankers

Collecting banker = banker to whom a holder of cheque presents the cheque to be credited to holder’s account. The banker’s duty is to collect the amount form the drawer’s bank (paying banker)

S85 (1) BEA gives protection to collecting banker if he can prove that he acted for the customer in good faith and without negligence (had made proper enquiries) – he will not be liable to the true owner for wrongful conversion.

Distinction between a Cheque and a Bill of Exchange

• Cheque• 1.It is drawn only on

a banker. • 2.The amount is

always payable on demand or after a specified period.

• 3.It can be crossed to end its negotiability

• 4.Acceptance is not required.

Bill of Exchange1. It can be drawn on

any body including a banker.

2. The amount is payable on demand

3. It can not be crossed

4. Acceptance is a must.