32

Place and crop your image here and send to back Neste Q2 2021 Peter Vanacker | President and CEO| 27 Jul 2021

Place and crop your

image here and send to back

Neste Q2 2021

Peter Vanacker | President and CEO| 27 Jul 2021

Place and crop your

image here

Contents

1. Q2 2021 review

2. Group financials

3. Segment reviews

4. Current topics

5. Appendix

2

Disclaimer

The following information contains, or may be deemed to contain, “forward-looking statements”. These statements relate

to future events or our future financial performance, including, but not limited to, strategic plans, potential growth,

planned operational changes, expected capital expenditures, future cash sources and requirements, liquidity and cost

savings that involve known and unknown risks, uncertainties and other factors that may cause Neste Corporation’s or its

businesses’ actual results, levels of activity, performance or achievements to be materially different from those

expressed or implied by any forward-looking statements. In some cases, such forward-looking statements can be

identified by terminology such as “may”, “will”, “could”, “would”, “should”, “expect”, “plan”, “anticipate”, “intend”, “believe”,

“estimate”, “predict”, “potential”, or “continue”, or the negative of those terms or other comparable terminology. By their

nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on

circumstances that may or may not occur in the future. Future results may vary from the results expressed in, or implied

by, the following forward-looking statements, possibly to a material degree. All forward-looking statements made in this

presentation are based on information presently available to management and Neste Corporation assumes no obligation

to update any forward-looking statements. Nothing in this presentation constitutes investment advice and this

presentation shall not constitute an offer to sell or the solicitation of an offer to buy any securities or otherwise to engage

in any investment activity.

3

Place and crop your

image here

Solid performance in Renewable Products – Porvoo refinery major turnaround completed

• Group comparable EBIT 241 MEUR in Q2

• Renewable Products with healthy margin as a result

of high sales performance

• Oil Products’ quarter mainly characterized by the

Porvoo refinery major turnaround

• Marketing & Services performed very well

• Focus on strategy execution

4

Solid financial position

ROACE, rolling 12 months, % Leverage, %

5

15.6%

0

5

10

15

20

25

30

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

Target 15%

-10

0

10

20

30

40

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

7.7%

Target below 40%

Place and crop your

image here and send to back

Q2 2021Group financials

6

Group financials Q2/21

7

MEUR Q2/21 Q2/20 H1/21 H1/20 2020

Revenue 3,022 2,572 6,155 5,842 11,751

EBITDA 599 333 1,184 659 1,508

Comparable operating profit 241 255 542 663 1,416

Renewable Products 287 314 580 644 1,334

Oil Products -58 -60 -66 14 50

Marketing & Services 18 19 35 27 68

Others (incl. eliminations) -7 -18 -7 -21 -36

Operating profit 463 208 920 405 828

Cash flow before financing activities 261 -246 -384 -366 1,019

Comparable earnings per share, EUR 0.31 0.26 0.62 0.76 1.60

Resilient Renewables and Porvoo refinery major turnaround

8

Group comparable EBIT by segments Q2/21 vs. Q2/20, MEUR

Q2/20 Renewable Products Oil Products Marketing & Services Others (incl.eliminations)

Q2/21

255

+2

-28+12 241

0

Q2/20 Volumes Sales margin Fx changes Fixed costs Other items Q2/21

+13+19

Higher sales margin compensated lower volumes

9

Group comparable EBIT Q2/21 vs. Q2/20, MEUR

255 -72 -45241

+71

H1/20 Volumes Sales margin Fx changes Fixed costs Other items H1/21

+43+41

Half-year result impacted by scheduled Porvoo turnaround and weak USD

10

Group comparable EBIT H1/21 vs. H1/20, MEUR

663 -105

-101 542+1

Place and crop your

image here and send to back

Q2 2021Segment reviews

11

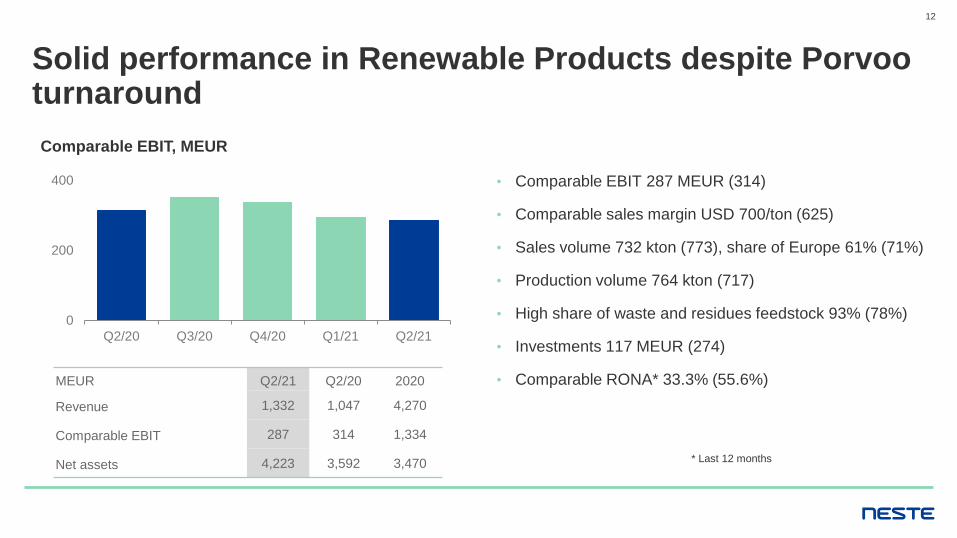

Solid performance in Renewable Products despite Porvooturnaround

• Comparable EBIT 287 MEUR (314)

• Comparable sales margin USD 700/ton (625)

• Sales volume 732 kton (773), share of Europe 61% (71%)

• Production volume 764 kton (717)

• High share of waste and residues feedstock 93% (78%)

• Investments 117 MEUR (274)

• Comparable RONA* 33.3% (55.6%)

12

0

200

400

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

MEUR Q2/21 Q2/20 2020

Revenue 1,332 1,047 4,270

Comparable EBIT 287 314 1,334

Net assets 4,223 3,592 3,470

Comparable EBIT, MEUR

* Last 12 months

Q2/20 Volumes Sales margin Fx changes Fixed costs Other items Q2/21

Healthy sales margin and stable volumes

13

Comparable EBIT Q2/21 vs. Q2/20, MEUR

314-37

287

+48-24 -4 -11

Feedstock market continued to be tight

14

Vegetable oil and animal fat prices*, USD/ton

*Quotations in NWE, source: Oil World, The Jacobsen

400

600

800

1,000

1,200

1,400

1,600

1,800

Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Soybean Rapeseed Palm oil Animal fat

High RIN and stable LCFS prices supported US margins

15

California Low Carbon Fuel Standard, LCFS credit price, USD/ton RIN prices, US cent /gal

0

30

60

90

120

150

180

210

240

Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

0

40

80

120

160

200

Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Biomass-based diesel (D4) Conventional renewable fuel (D6)

Strong sales performance and volume allocation supported sales margin

• Comparable sales margin USD 700/ton (625)

• California LCFS credit USD 185/ton (201)

• D4 RIN USD 1.70/gal (0.52)

• Sales of 100% Neste MY diesel 28% (27%)

• Utilization rate 96% (90%)

Comparable sales margin, USD/ton

16

0

200

400

600

800

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

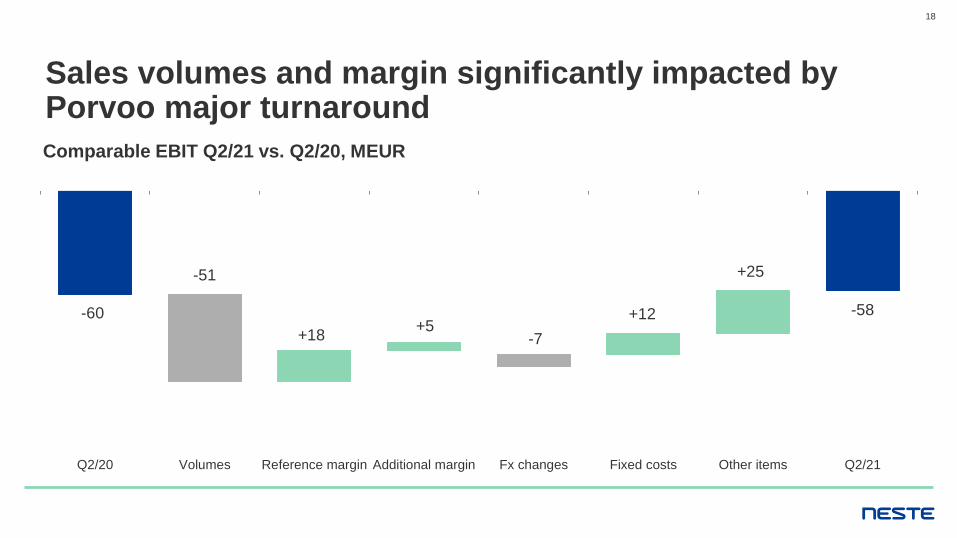

Oil Products’ major turnaround in Porvoo completed

• Comparable EBIT -58 MEUR (-60)

• Sales volume 1.2 Mton (3.1)

• Refinery average utilization rate 20% (67%)

• Urals’ share of feed 70% (67%)

• Investments 115 MEUR (58)

• Comparable RONA* -1.3% (9.6%)

17

MEUR Q2/21 Q2/20 2020

Revenue 1,331 1,218 6,063

Comparable EBIT -58 -60 50

Net assets 2,321 2,579 1,848

Comparable EBIT, MEUR

* Last 12 months

-60

0

60

120

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

Q2/20 Volumes Reference margin Additional margin Fx changes Fixed costs Other items Q2/21

Sales volumes and margin significantly impacted by Porvoo major turnaround

18

Comparable EBIT Q2/21 vs. Q2/20, MEUR

-60

-51

-7

-58+5

+18

+12

+25

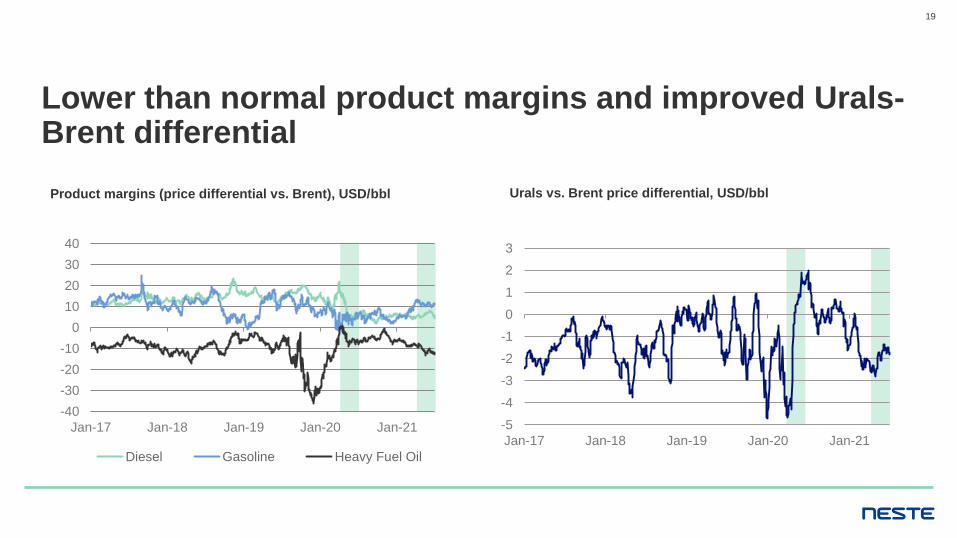

Lower than normal product margins and improved Urals-Brent differential

19

Product margins (price differential vs. Brent), USD/bbl Urals vs. Brent price differential, USD/bbl

-40

-30

-20

-10

0

10

20

30

40

Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Diesel Gasoline Heavy Fuel Oil

-5

-4

-3

-2

-1

0

1

2

3

Jan-17 Jan-18 Jan-19 Jan-20 Jan-21

Additional margin supported by currency hedging

• Total refining margin USD 9.7/bbl (4.8)

• Reference margin USD 2.2/bbl (-0.3)

• Additional margin USD 7.5/bbl (5.1)

• Exceptionally high refinery production costs USD

21.5/bbl (5.6) mainly due to maintenance

Total refining margin, USD/bbl

20

-2

0

2

4

6

8

10

12

14

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

Reference margin Additional margin

Marketing & Services performed very well

• Comparable EBIT 18 MEUR (19)

• Normalized unit margins

• Slightly higher sales volumes, aviation and marine still

impacted by COVID-19

• Successful fixed cost management

• Investments 3 MEUR (4)

• Comparable RONA* 37.8% (24.7%)

21

MEUR Q2/21 Q2/20 2020

Revenue 886 664 3,055

Comparable EBIT 18 19 68

Net assets 185 206 192

Comparable EBIT, MEUR

* Last 12 months

0

10

20

30

Q2/20 Q3/20 Q4/20 Q1/21 Q2/21

Place and crop your

image here and send to backCurrent topics

22

Place and crop your

image here and send to

back

Place and crop your

image here and send to

back

Place and crop your

image here and send to

back

Focusing on strategy implementation

Progress during Q2

• Singapore expansion project proceeding

according to schedule

• Rotterdam 500 kton SAF optionality

project moving ahead

• Definition phase in preparation for possible

next renewable products refinery in

Rotterdam, aim at investment decision

readiness late this year or early 2022

• Several commercial agreements and

partnerships in Renewable Aviation and

Renewable Polymers & Chemicals

Progress during Q2

• IPCEI (Important Projects of Common

European Interest) status for Porvoo

clean hydrogen related projects being

applied for

• Business Finland Circular Economy

investment aid received for chemical

recycling related site and laboratory

investments

• Promising purification concepts found

for challenging waste and residues

Scale up faster and bolder Increase innovations

Progress during Q2

• Porvoo refinery major turnaround

completed

• Short-term cost reduction measures

successfully continued

Drive efficiency in operations

23

Place and crop your

image here and send to back

Segment outlook for Q3/2021

• Sales volumes of renewable diesel

expected to be lower than in previous

quarter due to Singapore turnaround

• Waste and residue markets anticipated

to remain tight

• Sales margin expected to remain healthy

but be lower than in Q2

• Utilization rates forecast to remain high,

except for scheduled seven-week

maintenance turnaround at the

Singapore refinery, with estimated -90

MEUR impact on comp. EBIT

• Sales volumes and unit margins are

expected to follow previous years'

seasonality pattern

• Some negative impact anticipated on

demand and sales volumes due to

COVID-19 pandemic

Renewable Products Marketing & Services

• Market demand will continue to be

depressed as a result of COVID-19

pandemic

• Reference margin expected to remain

low and volatile

• Approx. 20 MEUR of the negative

result impact of Porvoo refinery major

turnaround is expected to materialize

in Q3

Oil Products

24

Place and crop your

image here and send to back

Other 2021 topics

• Cash-out capital expenditure in 2021

estimated to be approx. 1.2 BEUR,

excluding M&A

Group CAPEX

• Scheduled 4-week catalyst change at

Rotterdam refinery in Q4, which is

estimated to have negative impact of

approx. 50 MEUR on comp. EBIT

Renewable Products

25

Place and crop your

image here

Capital Markets Day 2021

• Neste will host Virtual Capital

Markets Day as webcast on

Thursday 23 September

• More information from IR to

follow

26

Place and crop your

image here and send to backAppendix

27

Renewable Products comparable EBIT calculation

28

Q2/20 Q3/20 Q4/20 2020 Q1/21 Q2/21

Sales volume, kton 773 730 732 2,966 743 732

Comparable sales margin, USD/ton 625 744 760 703 699 700

Comparable sales margin, MEUR 439 464 466 1,824 432 425

Fixed costs, MEUR -82 -66 -79 -307 -88 -86

Depreciations, MEUR -43 -47 -50 -184 -51 -54

Comparable EBIT, MEUR 314 352 338 1,334 294 287

Oil Products’ refinery production costs

29

Q2/20 Q3/20 Q4/20 2020 Q1/21 Q2/21

Refined products Million barrels 23.0 26.7 23.8 103.3 22.8 5.8

Exchange rate EUR/USD 1.10 1.17 1.19 1.14 1.21 1.21

Utilities costsMEUR 41.3 48.7 45.8 185.4 61.0 38.6

USD/bbl 2.0 2.1 2.3 2.1 3.2 8.1

Fixed costsMEUR 76.6 48.4 53.2 241.4 45.8 64.7

USD/bbl 3.7 2.1 2.7 2.7 2.4 13.5

External cost salesMEUR -0.3 -0.3 -0.3 -1.3 -0.3 -0.2

USD/bbl 0.0 0.0 0.0 0.0 0.0 0.0

TotalMEUR 117.6 96.8 98.6 425.5 106.4 103.1

USD/bbl 5.6 4.2 4.9 4.7 5.6 21.5

Cash flow

30

MEUR Q2/21 Q2/20 Q1/21 H1/21 H1/20 2020

EBITDA 599 333 585 1,184 659 1,508

Capital gains/losses 0 0 -1 -1 0 -1

Other adjustments -48 219 98 49 99 277

Change in net working capital 75 -432 -801 -726 -395 460

Net finance costs -18 -19 -6 -24 -19 -54

Income taxes paid -41 -40 -27 -68 -90 -133

Net cash generated from operating activities 567 61 -153 413 254 2,057

Capital expenditure -239 -348 -417 -657 -546 -972

Other investing activities -67 41 -74 -141 -74 -67

Cash flow before financing activities 261 -246 -645 -384 -366 1,019

Liquidity & maturity profile

• Group’s liquidity EUR 2,667 million at end of June 2021

• Liquid funds EUR 1,317 million

• Unused committed credit facilities EUR 1,350

million

• Average interest rate for interest-bearing liabilities was

1.5% and maturity 3.6 years at end of June 2021

• No financial covenants in Group companies’ existing

loan agreements

31

0

200

400

600

2021 2022 2023 2024 2025 2026 2027 2028 2029

Short-term Long-term

MEUR