39

Nestlé India Limited Gurgaon, 5 th August 2008 14 th Financial Analysts’ Meet

Nestlé India Limited

Gurgaon, 5th August 2008

14th Financial Analysts’ Meet

Agenda

Opening Remarks Martial Rolland

Key Financials Shobinder Duggal

Questions & Answers All

Disclaimer

This presentation may contain statements which reflect Management’s current views and estimates and could be construed as forward looking statements. The future involves certain risks and uncertainties that could cause actual results to differ materially from the current views being expressed. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

Responses can only be given to questions, which are not price sensitive.

2008

RIG OGNet Sales

INR 21.3 Bio

INR 17.0 Bio

+ 24.9% + 60bp

18.8%

18.2%

Volumes

& Prices

22.6%26.0%

22.4%17.7%

EBIT

+ 29.6%

INR 4.0 Bio

INR 3.1 Bio

1st Half snap shot

All calculations are based on non-rounded figures

2007Economic

Profit

+ 30.8%

INR 2.3 Bio

INR 1.8 Bio

Includes Figures from Nestlé Internal Reporting Standards

+ INR 4.3 Bio

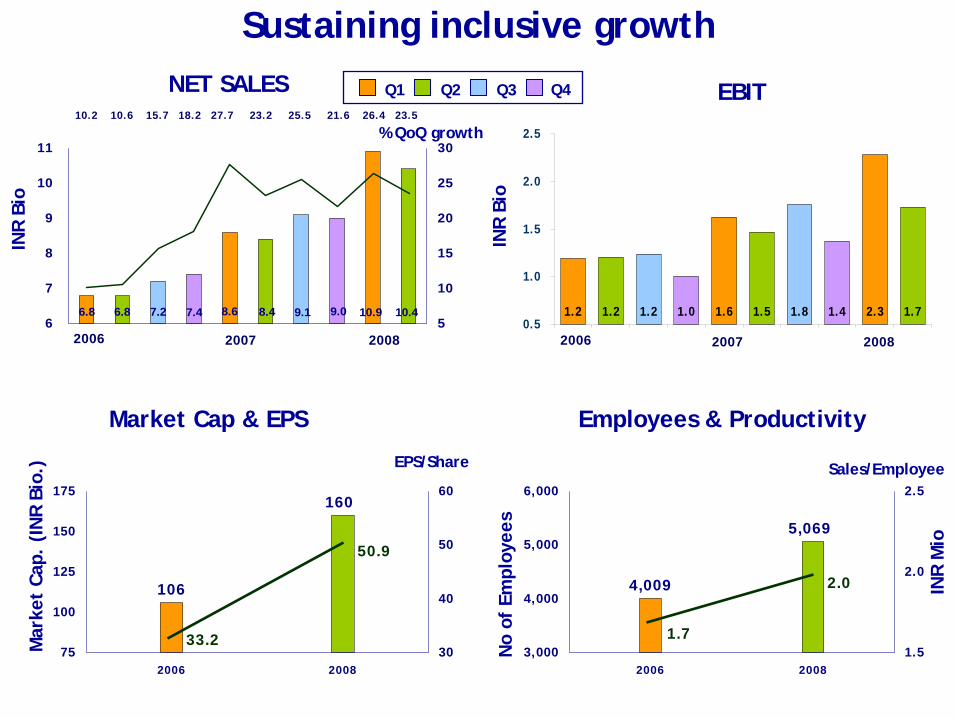

Sustaining inclusive growth

1.2 1.2 1.2 1.0 1.6 1.5 1.8 1.4 2.3 1.70.5

1.0

1.5

2.0

2.5

160

106

50.9

33.275

100

125

150

175

2006 200830

40

50

60

Q1 EBITQ2 Q3 Q4

INR

Bio

INR

Bio

Market Cap & EPS

5,069

4,009 2.0

1.73,000

4,000

5,000

6,000

2006 20081.5

2.0

2.5

Employees & Productivity

NET SALES

Mar

ket

Cap.

(IN

R Bi

o.)

No

of E

mpl

oyee

s

EPS/Share

2006 2007 2008 2006 2007 2008

10.9 10.49.09.17.4 8.66.86.8 7.2 8.46

7

8

9

10

11

5

10

15

20

25

30

10.2 10.6 15.7 18.2 27.7 23.2 25.5 21.6 26.4 23.5

Sales/Employee

INR

Mio

% QoQ growth

UNLEASHING 100% POTENTIAL6

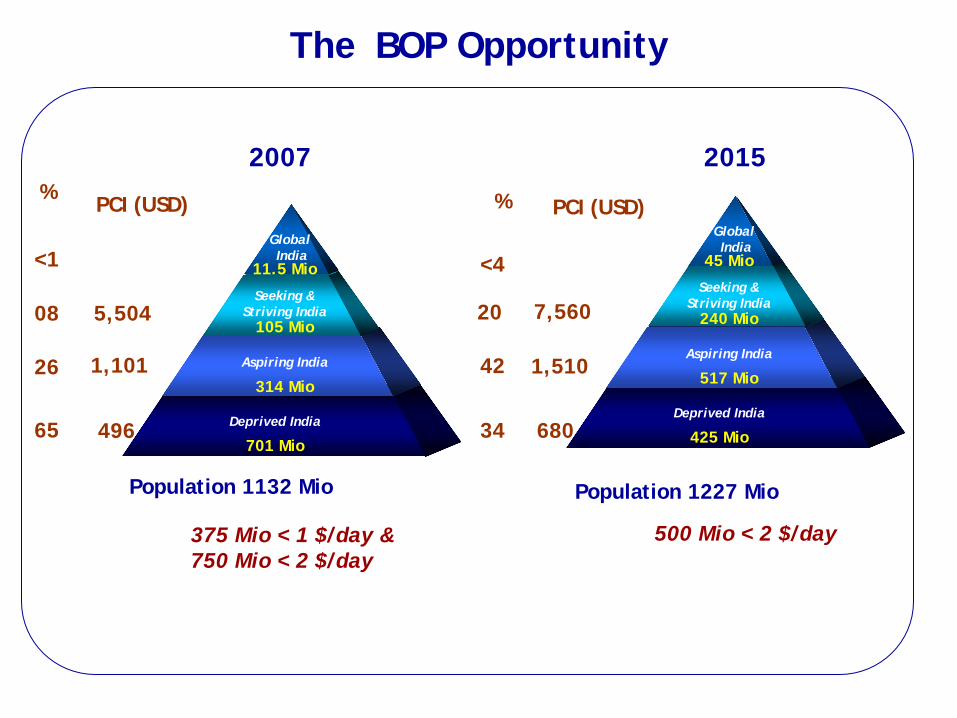

The BOP Opportunity

375 Mio < 1 $/day &750 Mio < 2 $/day

Population 1132 Mio

Deprived India

701 Mio

Aspiring India

314 Mio

Seeking & Striving India

105 Mio

GlobalIndia

11.5 Mio

65

26

08

<1

%

5,504

1,101

496

PCI (USD)

2007

Population 1227 Mio

Deprived India

425 Mio

Aspiring India

517 Mio

Seeking & Striving India

240 Mio

GlobalIndia

45 Mio

34

42

20

<4

%

2015

7,560

1,510

680

PCI (USD)

500 Mio < 2 $/day

BOP Consumers & PPP Products

Price Points &

affordabilit

y is key!

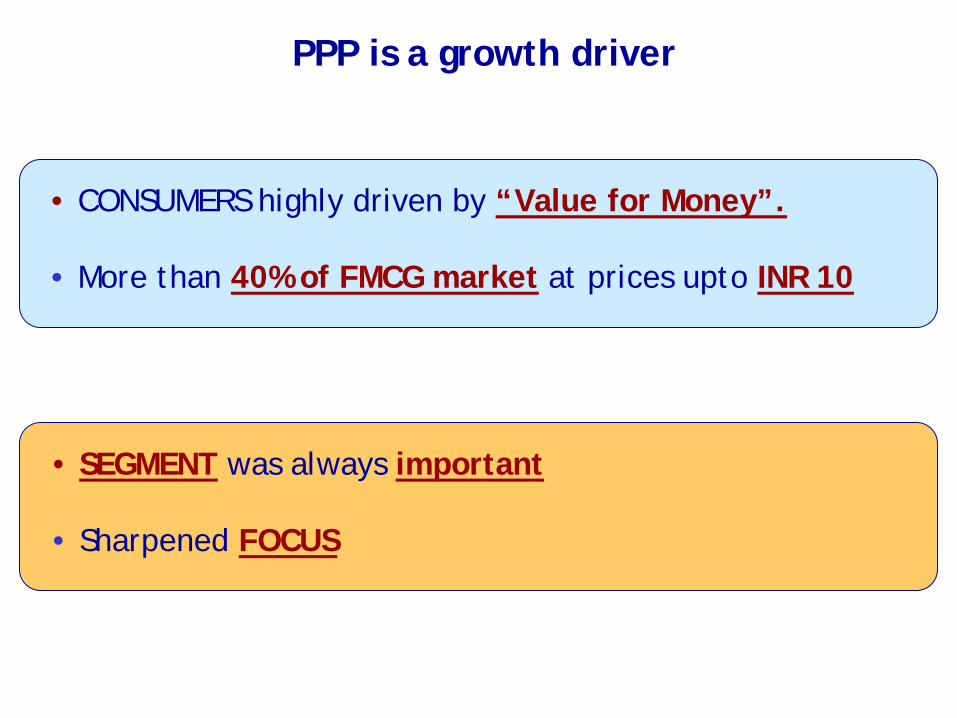

• CONSUMERS highly driven by “Value for Money”.

• More than 40% of FMCG market at prices upto INR 10

PPP is a growth driver

• SEGMENT was always important

• Sharpened FOCUS

UNLEASHING 100% POTENTIAL9

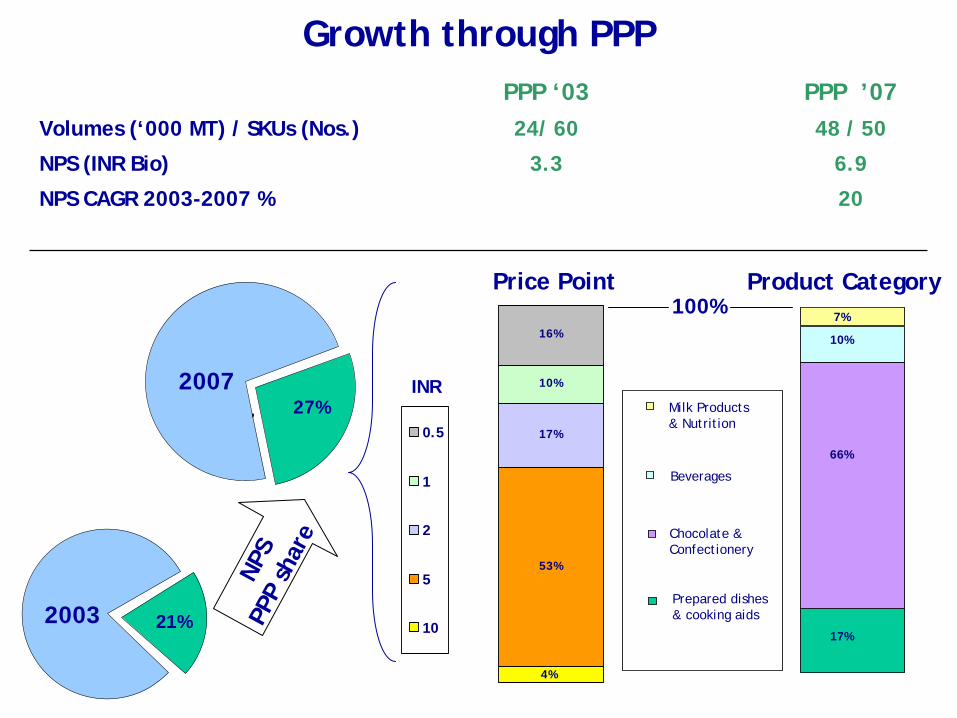

Growth through PPP PPP ‘03 PPP ’07

Volumes (‘000 MT) / SKUs (Nos.) 24/ 60 48 / 50

NPS (INR Bio) 3.3 6.9

NPS CAGR 2003-2007 % 20

53%

17%

10%

16%

4%

0.5

1

2

5

10

Price Point Product Category100%

INR

NPS

PPP

shar

e

2003

200727%

21%

2007

200317%

66%

10%

7%

Milk Products& Nutrition

Beverages

Chocolate & Confectionery

Prepared dishes& cooking aids

UNLEASHING 100% POTENTIAL10

Managing a PPP business demands a creative

‘mindset’ which challenges traditional thinking

and re-defines paradigms.

Conclusion

SALES GROWTH (1)

26.7 29.7 36.8 17.8 22.2

7.99.7

17.7

22.6

19.8

23.3

11.412.1

22.4

26.0

10.0

14.0

18.0

22.0

26.0

30.0

34.0

38.0

2005 2006 2007 H1 07 H1 080

7

14

21

28

Sales INR Bio Real Internal Growth (%) Organic Growth (%)

Sales Evolution

Basis Nestlé Internal Reporting Standards

Sale

s in

INR

bio

(%)

RIG

&O

G

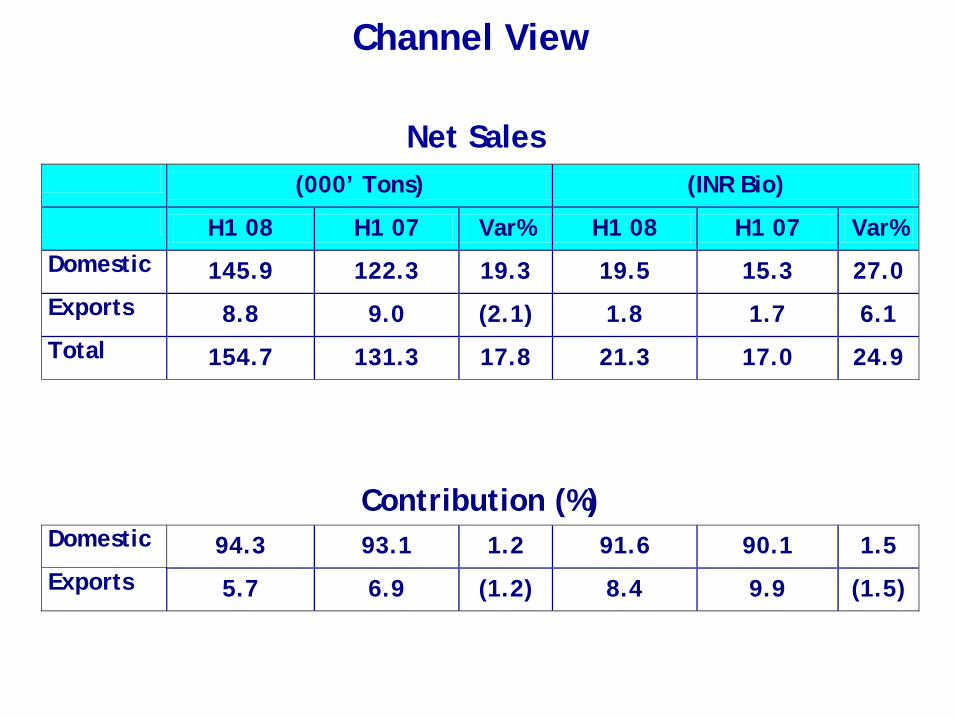

(000’ Tons) (INR Bio) H1 08 H1 07 Var% H1 08 H1 07 Var% Domestic 145.9 122.3 19.3 19.5 15.3 27.0 Exports 8.8 9.0 (2.1) 1.8 1.7 6.1 Total 154.7 131.3 17.8 21.3 17.0 24.9

Contribution (%) Domestic 94.3 93.1 1.2 91.6 90.1 1.5 Exports 5.7 6.9 (1.2) 8.4 9.9 (1.5)

Channel View

All calculations are based on non-rounded figures

Net Sales

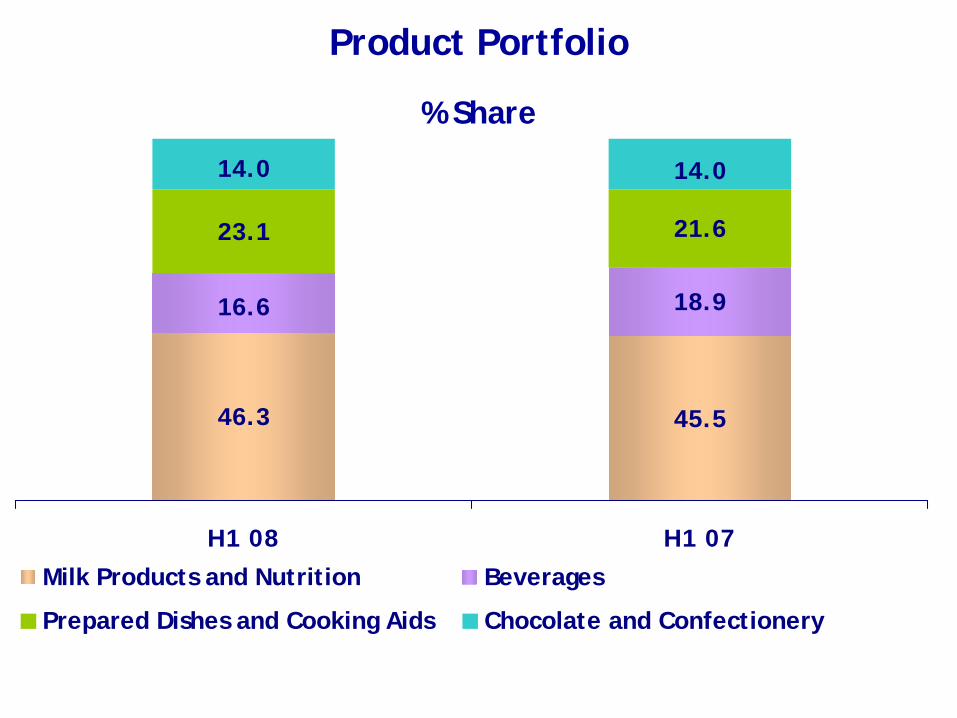

45.546.3

18.916.6

21.623.1

14.014.0

H1 08 H1 07Milk Products and Nutrition Beverages

Prepared Dishes and Cooking Aids Chocolate and Confectionery

% Share

Product Portfolio

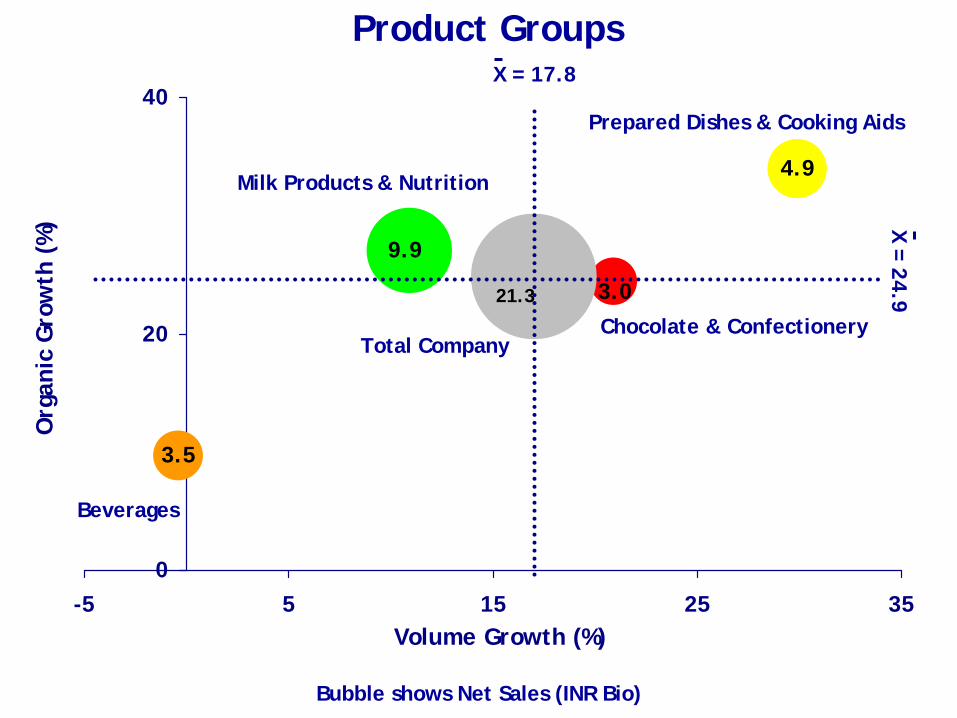

Product Groups

9.9

4.9

3.5

3.0 21.3

0

20

40

-5 5 15 25 35Volume Growth (%)

Org

anic

Gro

wth

(%

)

Chocolate & Confectionery

Milk Products & Nutrition

Beverages

Prepared Dishes & Cooking Aids

Bubble shows Net Sales (INR Bio)

X = 24.9X = 17.8

Total Company

55.3

61.3

45

53

61

H1 07 H1 08

7.7

9.9

7

8

9

10

H1 07 H1 08

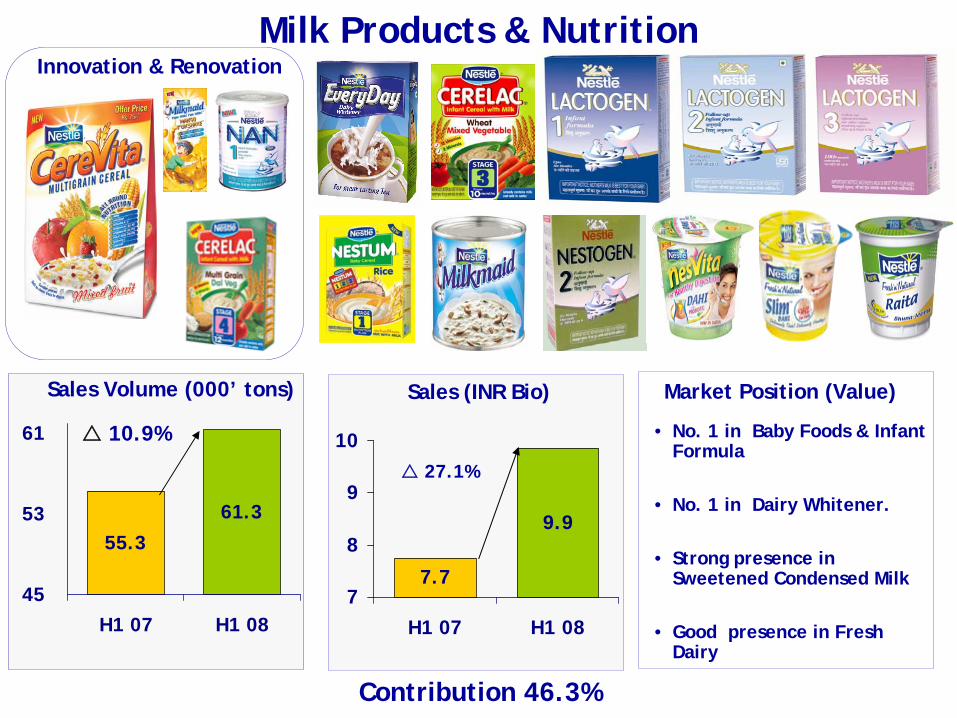

Milk Products & Nutrition

Sales Volume (000’ tons)

10.9%

Sales (INR Bio)

27.1%

• No. 1 in Baby Foods & Infant Formula

• No. 1 in Dairy Whitener.

• Strong presence in Sweetened Condensed Milk

• Good presence in Fresh Dairy

Innovation & Renovation

Contribution 46.3%

Market Position (Value)

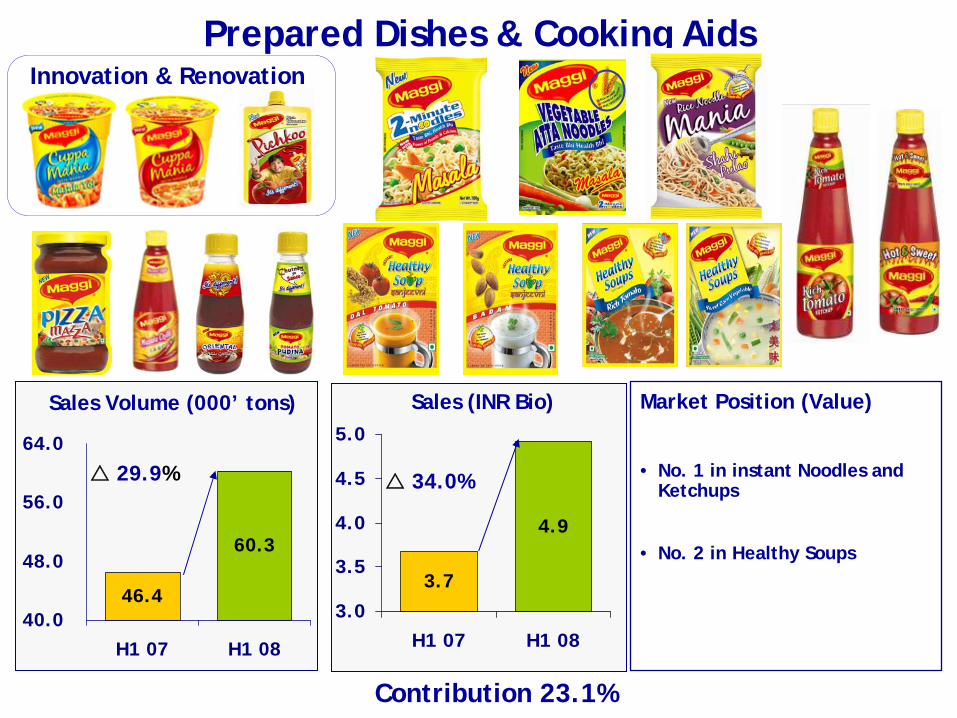

3.7

4.9

3.0

3.5

4.0

4.5

5.0

H1 07 H1 08

34.0%

46.4

60.3

40.0

48.0

56.0

64.0

H1 07 H1 08

Sales Volume (000’ tons)

Prepared Dishes & Cooking Aids

29.9%

Sales (INR Bio) Market Position (Value)

• No. 1 in instant Noodles and Ketchups

• No. 2 in Healthy Soups

Innovation & Renovation

Contribution 23.1%

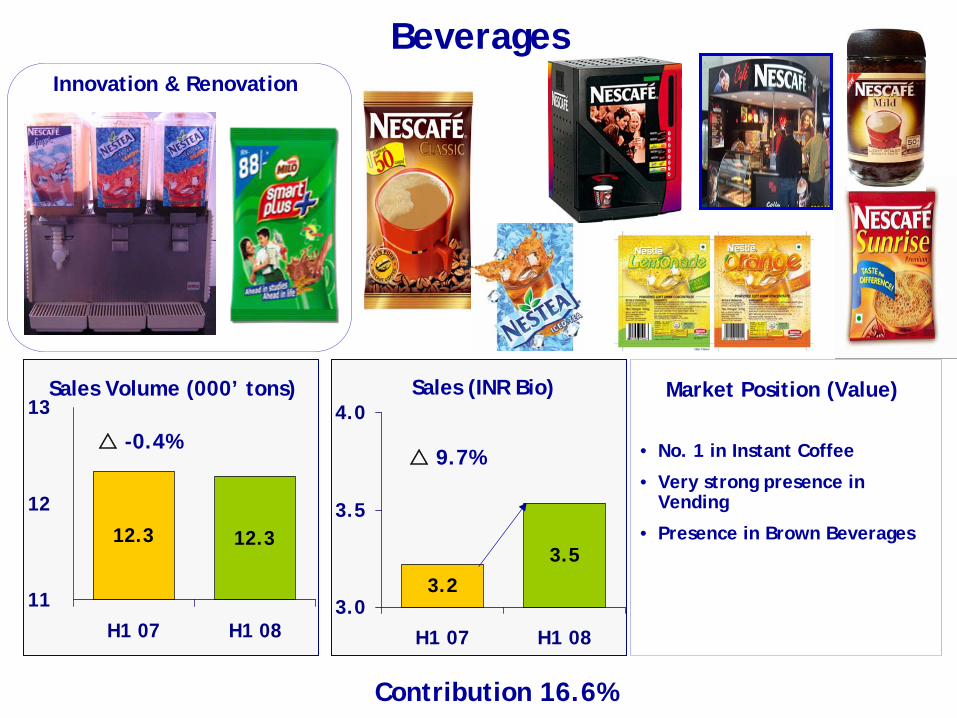

12.3 12.3

11

12

13

H1 07 H1 08

Sales (INR Bio)

3.23.5

3.0

3.5

4.0

H1 07 H1 08

9.7%-0.4%

Beverages

Sales Volume (000’ tons)

Innovation & Renovation

Market Position (Value)

• No. 1 in Instant Coffee

• Very strong presence in Vending

• Presence in Brown Beverages

Contribution 16.6%

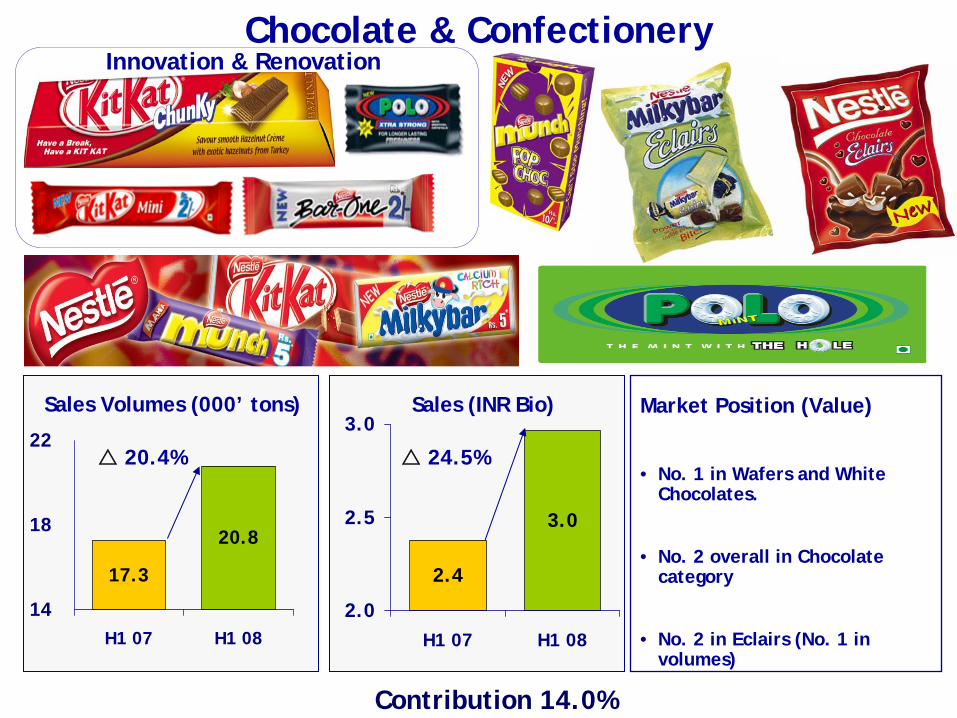

2.4

3.0

2.0

2.5

3.0

H1 07 H1 08

17.3

20.8

14

18

22

H1 07 H1 08

Chocolate & Confectionery

Sales Volumes (000’ tons)

20.4%

Sales (INR Bio)

24.5%

Market Position (Value)

• No. 1 in Wafers and White Chocolates.

• No. 2 overall in Chocolate category

• No. 2 in Eclairs (No. 1 in volumes)

Innovation & Renovation

Contribution 14.0%

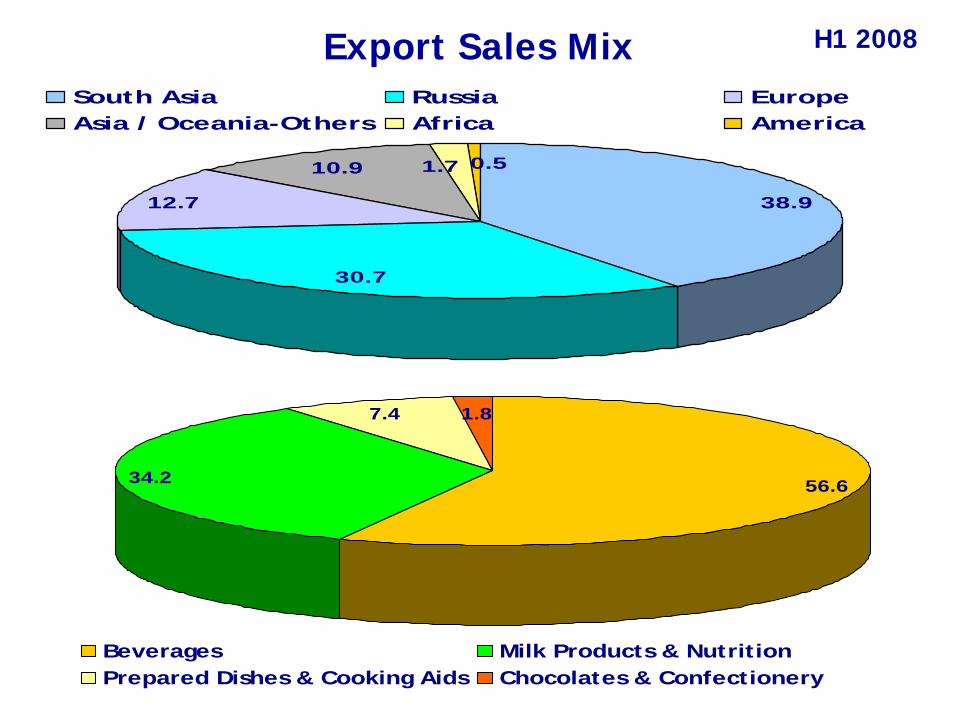

Export Sales Mix

38.9

30.7

12.7

10.9 1.7 0.5

South Asia Russia EuropeAsia / Oceania-Others Africa America

56.634.2

7.4 1.8

Beverages Milk Products & NutritionPrepared Dishes & Cooking Aids Chocolates & Confectionery

H1 2008

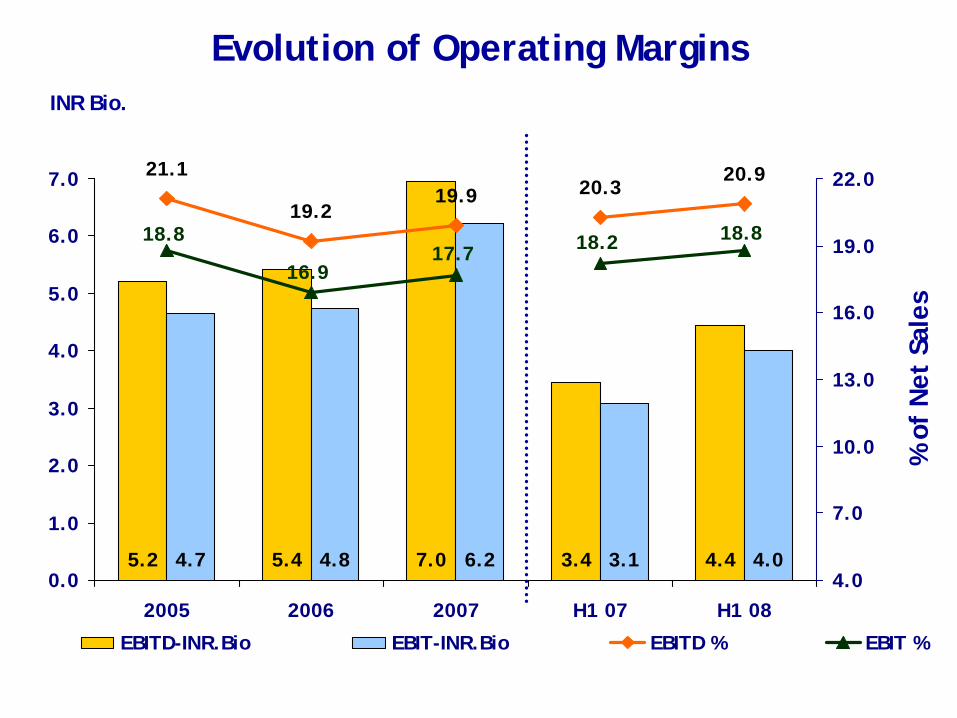

PROFIT MARGINS (2)

Evolution of Operating MarginsINR Bio.

5.2 7.0 4.05.4 4.43.44.7 3.16.24.8

20.920.319.9

19.2

21.1

18.8

16.917.7 18.2 18.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2005 2006 2007 H1 07 H1 084.0

7.0

10.0

13.0

16.0

19.0

22.0

EBITD-INR.Bio EBIT-INR.Bio EBITD % EBIT %

% o

f N

et S

ales

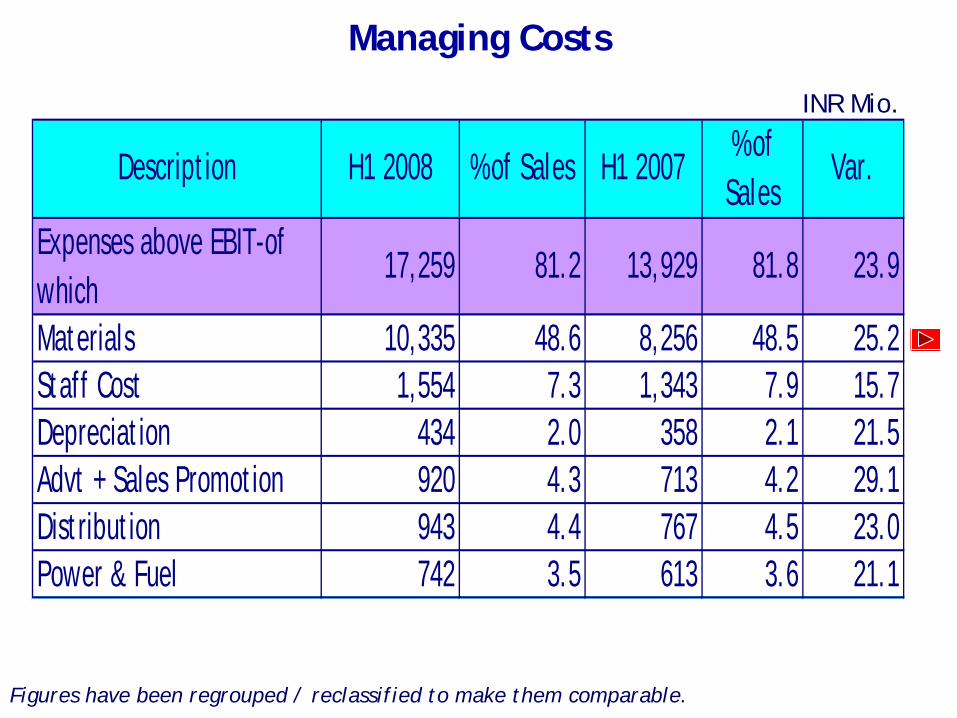

INR Mio.

Managing Costs

Figures have been regrouped / reclassified to make them comparable.

Description H1 2008 % of Sales H1 2007% of Sales

Var.

Expenses above EBIT-of which

17,259 81.2 13,929 81.8 23.9

Materials 10,335 48.6 8,256 48.5 25.2 Staff Cost 1,554 7.3 1,343 7.9 15.7 Depreciation 434 2.0 358 2.1 21.5 Advt + Sales Promotion 920 4.3 713 4.2 29.1 Distribution 943 4.4 767 4.5 23.0 Power & Fuel 742 3.5 613 3.6 21.1

Evolution of Net Profit Margins

INR Bio.

3.1 3.2 4.1 2.0 2.8

12.5

11.212.0

13.211.8

1

2

3

4

5

2005 2006 2007 H1 07 H1 085

10

15

Amount % of Net Sales

% of Net sales

WORKING CAPITAL INTENSITY (3)

Trade Net Working Capital (TNWC)

INR Mio

30th Jun 2008

30th Jun 2007

Receivables from Customers 731 629

Inventories 5,161 4,409

Less: Trade Payables * 2,594 1,998

TNWC 3,298 3,040

As % of Sales (12 rolling months ) 8.0 9.2

Basis Nestle Internal Reporting Standards and including affiliated customers and vendors

* Excludes payables for taxes, Staff Costs, Capex, provisions for contingencies etc.

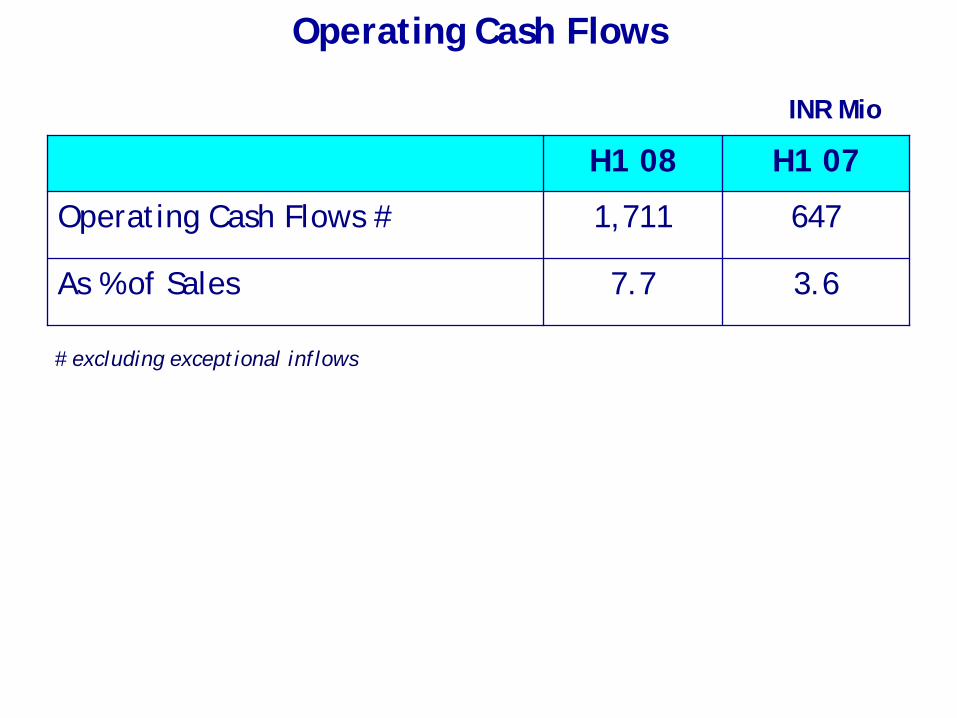

Operating Cash Flows

INR Mio

H1 08 H1 07

Operating Cash Flows # 1,711 647

As % of Sales 7.7 3.6

Basis Nestle Internal Reporting Standards

# excluding exceptional inflows

FIXED CAPITAL INTENSITY (4)

INR mio. % of Net sales

Investment in Fixed Assets

1,522 1,698 442 733781

4.8

2.6

3.4

5.4

3.2

300

800

1300

1800

2005 2006 2007 H1 07 H1 081.0

3.0

5.0

7.0

Amount % of Net sales

Depreciation 498 555 640 305 381

Excludes Intangibles

Rotation of Average Tangible Fixed AssetsTimes

Basis Nestlé Internal Reporting Standards

6.6

6.97.0

7.2

6.5

6.0

6.3

6.6

6.9

7.2

7.5

2005 2006 2007 H1 07 H1 08

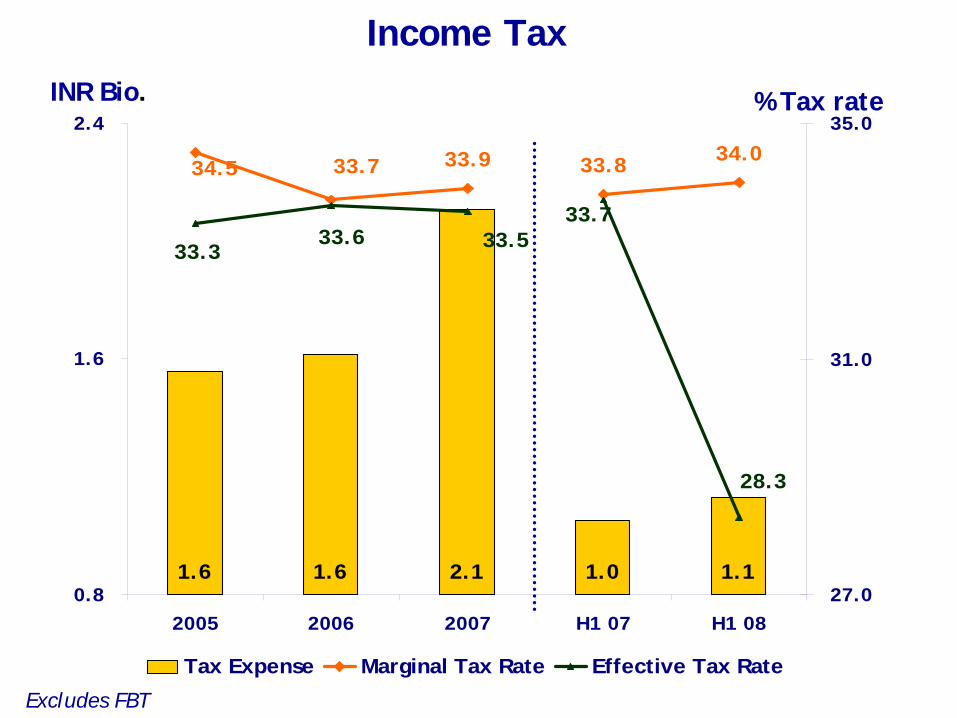

INCOME TAX RATE (5)

1.6 1.6 2.1 1.0 1.1

34.5 33.7 33.8 34.033.9

33.533.333.6

33.7

28.3

0.8

1.6

2.4

2005 2006 2007 H1 07 H1 0827.0

31.0

35.0

Tax Expense Marginal Tax Rate Effective Tax Rate

INR Bio. % Tax rate

Excludes FBT

Income Tax

COST OF CAPITAL (6)

Cost of Capital

Basis Nestlé Internal Reporting Standards

11.3 11.2

7.27.7 7.7

7.9

11.7

10.5

9.3

6.6

5.0

8.5

12.0

2005 2006 2007 H1 07 H1 08

Adjusted Cost of Capital (ACC) Risk Free Rate

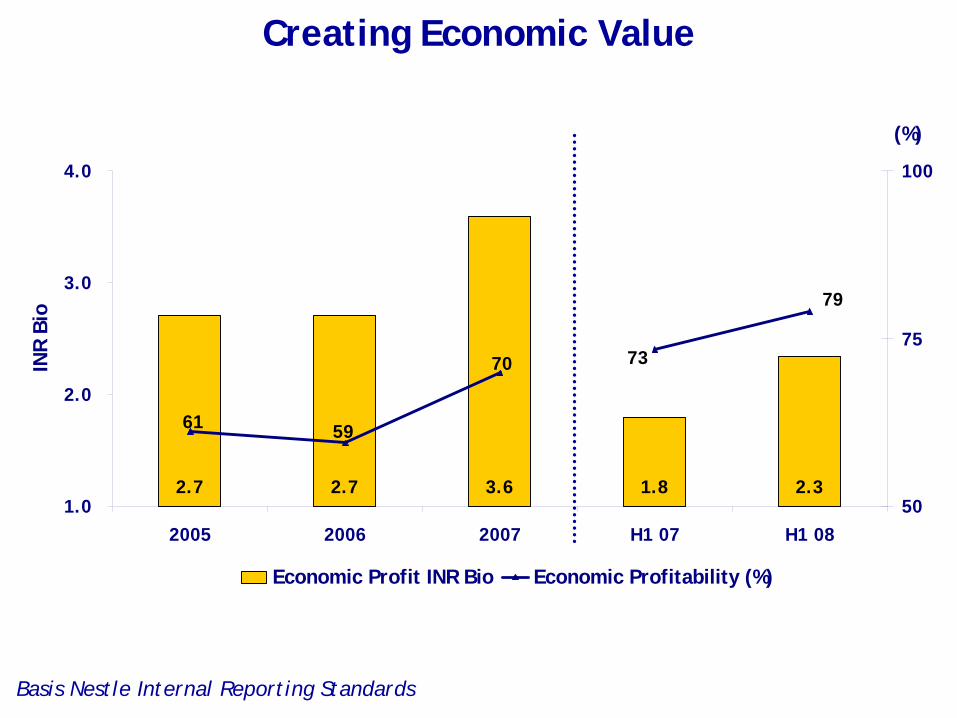

VALUE GROWTH DURATION (7)

2.7 2.7 3.6 1.8 2.3

70

61 59

73

79

1.0

2.0

3.0

4.0

2005 2006 2007 H1 07 H1 08

INR

Bio

50

75

100

(%)

Economic Profit INR Bio Economic Profitability (%)

Basis Nestle Internal Reporting Standards

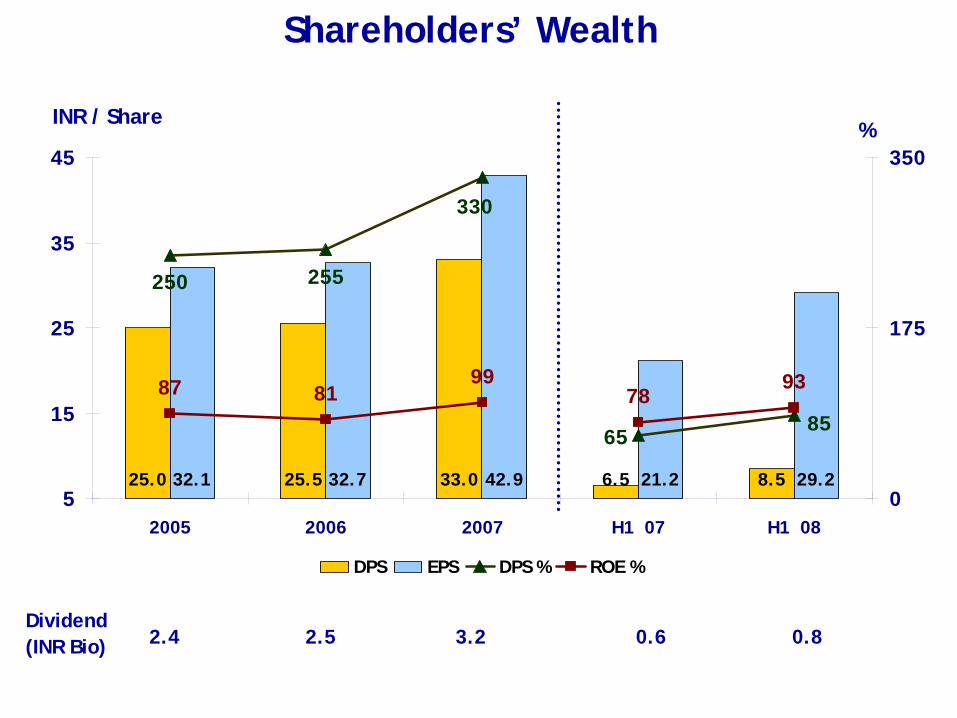

Creating Economic Value

25.0 25.5 33.0 6.5 8.532.1 32.7 42.9 21.2 29.2

87 8199

7893

250

65

255

330

85

5

15

25

35

45

2005 2006 2007 H1 07 H1 080

175

350

DPS EPS DPS % ROE %

INR / Share%

Shareholders’ Wealth

2.4 2.5 3.2 0.6 0.8Dividend(INR Bio)

THANK YOU

10.0

21.7

-1.6

5.4

23.5

-5

0

5

10

15

20

25

Inde

xed

cos

t in

crea

se %

Commodity Costs - Ongoing Challenge

H1 2007

Reference point - Jan-Jun 2007 prices

Green Coffee

Milk Solids

Wheat Flour

Oils

Sugar

H1 2008