Netting Technology for Small-scale Vegetable Growers in Sub-Saharan Africa: One-year pilot-project to assess the scalability of netting technology in Kenya Financial Services supporting BNA scale up November 2017

Transcript

Netting Technology for Small-scale Vegetable Growers in Sub-Saharan Africa:

One-year pilot-project to assess the scalability of netting technology in Kenya

Financial Services supporting BNA scale up

November 2017

Inception Report – Final draft

Financial Services to support BNA scale up

CONTENTS

Abbreviations and Acronyms ............................................................................................................................ 3

1 Purpose and Methodology ........................................................................................................................ 4

2 Agricultural lending in Kenya ..................................................................................................................... 5

2.1 Key features of financing agriculture ................................................................................................ 5

6.1.1 Strategy and way forward ....................................................................................................... 19

ABBREVIATIONS AND ACRONYMS

AFC Agriculture Finance Corporation

Afraca Africa Rural and Agricultural Association

AMFI Association of Microfinance Institutions

BNA Bio Net Agro

FICCF Finance Innovation for Climate Change Fund

FSP Financial Service Provider

KES Kenyan Shilling

KWFT Kenya Women Finance Trust

MFI Micro Finance Institution

MESPT Micro Enterprises Support Programme Trust

MoU Memorandum of Understanding

NDA Non-Disclosure Agreement

SACCO Savings and Credit Co-Operative

USAID Unites States Assistance for International Development

USD US Dollar

1 PURPOSE AND METHODOLOGY

This report is a tool to implement a pre-scale-up activity for the Net House Technology in Kenya. The goal is to provide critical information on if, how, and at which conditions access to financial services for farmers can be part of the scale-up process of Net Houses.

This report is the result of the activity carried out by Microfinanza from the 15th of April to 30th of November 2017, including two-field mission of the field Experts, Mr David Berno and Mr Marco Pasini, and desk strategic advice from Mr Giampietro Pizzo. Key activities:

Sharing feature of net house investments and needs of the scale-up strategy with BNA team: CIRAD, AtoZ, Icipe, UC Davies, and principal consultants and beneficiaries;

Scouting relevant stakeholders in agricultural finance, with a specific care in checking products and conditions for loans in agriculture;

Contacting about 25 banks and MFIs in Kenya, and meeting Rafiki Bank, KWFT, Eclof and Cooperative Bank;

Meeting networks and other stakeholders in Kenyan Agricultural Finance sector: AMFI, AFRACA, FICCF, KPMG, MESPT, Microfinanza Rating;

Organizing two focus groups with farmers on the topics of profitability of net houses and financial habits of farmers, plus one focus group on the functioning and profitability of greenhouses;

Preparing a questionnaire for farmers, government extension officers, agro-dealers and brokers to investigate preferences and needs regarding investments and financial service;

Analysing data from the survey;

Sharing results and data with partners (ICIPE; CIRAD, AtoZ), and financial institutions in Kenya;

The questionnaires designed by Microfinanza Srl with other partners' support, aimed to integrate data and information available for drafting the business plan regarding the scale-up stage of net house technology in Kenya. And at the same time, the survey also helped to identify the farmers' preferences in accessing financial services. The questionnaires have been administered by AtoZAgroZ/TGDL staff from July 24th to August the 15th 2017, and then data has been entered by the same team, on a pre-determined matrix, and made available at the end of September 2017. Overall 218 people have been interviewed: 26 extension officers, coming from 11 counties; 44 agro-dealers, coming from 16 counties, 21 brokers, coming from 8 counties, and 127 farmers, coming from 16 counties. 70 of these farmers had a greenhouse, 27 had a net-house, and 16 of them had both; 46 farmers grew their crops in open field. 70% of interviewed farmers were males and 30% females. The average size of plots was 6,88 acres, ranging from 0.25 to 400 acres, with 39% of such areas smaller than 2 acres, and 28% between 2 and 3 acres.

The sample of farmers has been random, but not randomized; therefore results cannot be inferred for general conclusions. Actually, because of the need to target greenhouse and net house owners, who are potential early adopters of the Net House, the sample is probably including farmers with better financial conditions and background than the average in the country.

The report covers the following aspects:

Agricultural lending and Kenya specificities

Savings and investment techniques of farmers

Partnerships with financial service providers: bottlenecks, opportunities and interested institutions

Essential conditions to make the Net House an appealing product or financial institutions

The final report integrates and completes the interim report, presented in July 2017,

2 AGRICULTURAL LENDING IN KENYA

2.1 Key features of financing agriculture

Agriculture is typically a challenging sector for the microfinance world for a series of reasons:

There's the need for a substantial investment in training of loan officers, and probably to dedicate some loan officers only to the agricultural portfolio;

Assessment and follow up are often more costly than ordinary loans, because of the technical competence that is needed to the loan officer, and because of distances to be made to meet all the farmer clients;

Loan cycles have to be adapted to crop cycles, making it almost impossible to have frequent instalments and, on the contrary, needing grace periods and often single instalment repayments;

Agricultural production is vulnerable to climate instability, and also to price fluctuation.

Therefore, coping with risk management and operational costs is a challenge and, at the same time, a necessity for agricultural finance.

Climate Change is representing a further challenge for agricultural production and, therefore, agricultural lending. Droughts, unpredictable rainy seasons and floods are becoming more and more frequent in rural areas, especially in low development contexts where national and international actors did not invest in the necessary infrastructure to mitigate Climate Change effects.

Smallholder farmers face higher vulnerability than large producers, as they are more vulnerable both to market instability and to climate. Because of that, smallholder farmers find it difficult to have access to credit and investment for their agricultural activity.

The key issue is risk management.

Financial institutions that finance the agricultural sector, primarily Microfinance Institutions, tend to concentrate their investments of low-risk productions and in low risk agrarian context, where, as an example, the Government has made some infrastructural interventions, like in irrigation, of where contract farming agreements are in force. That means that the more a farmer needs some investment to reinforce and stabilise its production, the less s/he is likely to find an institution that will provide the necessary loan.

Because of all these reasons, farmers and financial institutions find it difficult to communicate and understand each other. From the farmers' side, there is the feeling that their financial needs are not fully understood, as neither the related-opportunities are not well evaluated. On the other hand, the financiers perceive the operations supporting the farmers very costly and risky, too much exposed to external factors. Successful agricultural finance manages to match the parties' needs.

Providing capital when it is needed and planning reimbursement when it is possible, to maximise the revenue.

Minimizing the financial risk to lose the whole capital in case of any external or unexpected event.

2.2 Kenyan context

Kenya provides no exception. Financial service providers (Banks, Microfinance Banks, or Microfinance Institutions - credit only institutions) tend to concentrate their lending activities to the clients (urban small business and employees) able to repay with frequent and regular instalments and in a short period anon small business or trade. Agriculture is somehow a niche sector, being perceived as costly and risky by the financial institutions.

According to the 2014 Microfinance Sector Report, realised by AMFI (Association of Microfinance Institutions) and Microfinanza Rating, at the end of 2013 over 70% of the loan portfolio was for business related loans, while only 8.5% is dedicated to agriculture. Moreover, it is important to mention that this

figure is made almost only on investment from Microfinance institutions, whose agricultural portfolio was 21% of the overall portfolio, while banks lent 97% of their portfolio to business-related activities. Agriculture counts for 35% of GDP (WB data 2016), and employs 75% of the workforce (last available data 2006, from WB). Thus it appears clear that financial institutions underserve the sector and therefore there is room for growth in agricultural lending. Another relevant aspect to mention of Agri-lending is regarding the low percentage of Portfolio at Risk (late payments up to 30 days). From the report as mentioned above, such figure result equal to 3,6% compared to the 8.0% average of the whole microfinance sector.

Some Kenyan institutions have started focusing on agricultural lending. We noted some activism both from private companies (Juhudi Kilimo, Greenland Fedha, and many others), and government institutions (AFC – Agriculture Finance Corporation).

To date, the credit gap versus the smallholder farmers remains high, mainly for the reasons as mentioned earlier. Therefore, promoting the adoption of net house on debt with FSPs should keep in mind the described scenario.

3 SAVINGS AND INVESTMENT TECHNIQUES OF FARMERS

The analysis of clients’ preferences, based on focus group discussion; contact with selected MFIs, banks and networks, and the questionnaire administered to farmers, agro-dealer, brokers and extension officers, allows driving some general considerations.

3.1 How to finance and investment

Farmers tend to finance their investments by relying on their savings.

Borrowing is an option as soon savings, or other recourses collected within the family or peers, or via informal or semi-formal groups, are not enough. It can be used to top up savings to get to the necessary amount.

Relationship with financial institutions seems to be quite difficult, with few financial institutions understanding the need for grace periods adapting to crop cycles, or being ready to estimate the revenue on the main crop and not on other resources, making it possible to ask for monthly repayments.

According to our questionnaire, Banks are anyway the first provider of loans whenever necessary, with Equity Bank and KCB being the most used. SACCOs, and to a lower extent Chamas, are the other sources of financing when coming to loans. The same questionnaire confirms that the inappropriate financial products for agriculture are a more important barrier than mistrust or accessibility to financial institutions.

Farmers usually save in different ways. Most have a bank account, either at a bank or, frequently, at a SACCO (Saving and Credit Cooperative). Moreover, they invest in livestock, other assets, and are members of savings groups, like Chamas. There are individual cases of farmers that, being close to Nairobi, actually invest their savings in the stock exchange market. Such investment gives better returns than any blocked savings product or savings account, and in any case, money is available within a short time (while this might be a challenge in a savings group or a SACCO).

3.2 Informal or semi-formal tools

Chamas

Chamas are savings groups where people contribute with the same amount each month, and one person takes the whole amount each time, as soon as the cycle is concluded with all members’ benefit of the entire amount one time.

A large part of smallholder farmers is members of Chamas, either of their farmers' group or their Church, or their neighborhood. 60% of the farmers in the questionnaires were members of a saving group, in half of the cases a Chama. It is an appreciated saving method, comfortable because of its proximity. It is perceived as not risky, even though about one-quarter of interviewed farmers lost money at least once, while this is close to zero in the case of SACCOs. Probably people compare risk in Chamas with other informal savings option, rather than with formal ones.

The limit, often, is the amount that can be obtained when it’s each person’s turn, usually enough for minor investments. This amount can vary from 3,000 to 500,000 in our sample, but on average keeps below 100,000

Table banking

Table banking is a collective saving system, where all members save each month (different amount), and each month all the collected money is lent to some group members. Each person can borrow up to the double of what his/her contribution is, and has to pay back the double amount in 1-3 months (depending on the group). At the end of the year, people divide the overall capital collected in this way. The system is formalized, and those who do not pay back their loans can be brought to court.

This method can be useful to raise significant amounts in a relatively short time lapse. The figures at the end of the year undoubtedly allow people to buy a net house at the prices under consideration so far. However, even if the local police have the right to control the processes, there is a non-negligible risk of some members defaulting.

SACCOs

SACCOs are the preferred financial institutions among farmers. They tend to lend at about 12% flat interest rate per annum, which is considered acceptable by farmers1. Overall, according to the survey, farmers are familiar with the SACCOs' mechanism and usually trust them due to mainly their proximity. The limit, often, is the timing of the availability of loans, even though the amounts provided by this kind of institutions can be sufficient to buy the net-house. The research showed that 2 out of 3 farmers declare that they can borrow the amount that they need, at the convenient time, from SACCOs.

Another limit on the functioning of the SACCOs, according to the farmers, is about the savings' withdraw that can be quite difficult.

3.3 Financial institutions

As mentioned, access to formal financing is limited for farmers, even though most of them use either savings or other services from banks and MFIs. A bank is the first choice for farmers when it comes to savings, while Chamas and SACCOs are the second best options. Many farmers use mobile phone accounts for their savings, as well (M-Pesa; M-Shwari).

The primary constraints reported by the farmers are linked to the reimbursement conditions of loan disbursed by formal financial institutions. Such repayments are very often proposed as monthly repayments, with no grace period. Among farmers, there is also, to a smaller extent, a component of fear of the banks, mainly due to a weak knowledge of their functioning.

Difficult mutual comprehension is also perceived as a constraint "They would rather lend you money to buy a car of a motorbike rather than for investment in agriculture" one farmer remarked.

However, even with all these problems, most of the farmers in our sample, who took a loan for their

1. This nominal rate is lower the one provided by the banks (capped by the Central Bank at 14%). We suspect though

that many farmers do not have a clear understanding of the difference between flat and declining interest rate. Further evidence shows that the 20% interest rate proposed by MFI is not higher than the 12% offered by SACCOs

investment, did it through a formal financial institution, a bank in most cases, rather than with a semi/informal Institution. Therefore, reinforcing the offer of agricultural loans at banks and MFIs level is an essential aspect of making sure that potential Net-House customers have adequate access to the necessary resources. Informal institutions, like SACCOs and Chamas, are not sufficient, nor the best option, to cover this need.

4 PARTNERSHIPS

4.1 Provision of financial services associated with AgroZ net houses

The analysis has been conducted considering some models to deliver financial services associated with AgroZ bio-net houses

A) One-stop-shop model. The same organisation provides the net-House and its financing. This implies either AgroZ giving credit (actually, possibility to pay in instalments) to clients, or financial institutions directly selling the Net House Package.

B) Financial Institution partnering with AgroZ. AgroZ enters into a partnership with a local financial institution to sell the Net House Package. This model typically involves a financial institution providing credit to an end-user and managing the monitoring and repayment processes, while AgroZ offers the Net House, the installation and after-sales services. The customer might either receive money or directly the net house. In the latter case, the financial institution pays AgroZ the price for the Net House.

C) Group partnership model. AgroZ enters into partnership with some groups or intermediate bodies (ex. farmers cooperatives, credit unions, or other village‐based financial institutions). The group manages to collect the resources and either lends to some members, or works as the guarantee for a group member towards the financial institutions, or buy the Net House whose property will be shared by group members. The Group Organisation is the counterpart of AgroZ and/or the financial institutions and manages the monitoring and repayment processes of members when appropriate. This model can be associated with the partnership with a financial institution.

D) Brokering model. A third-party organisation or individual is paid by the finance provider and AgroZ to market Net Houses and assess customer’ suitability for financing. They will then bring viable customers forward to buy the Net Houses. The model can be formal, where the broker is hired or is and agro-dealer working in the area; or informal, where the relationships are with Net House users disseminating the technology among peers, or with brokers proposing it to their contracting farmers.

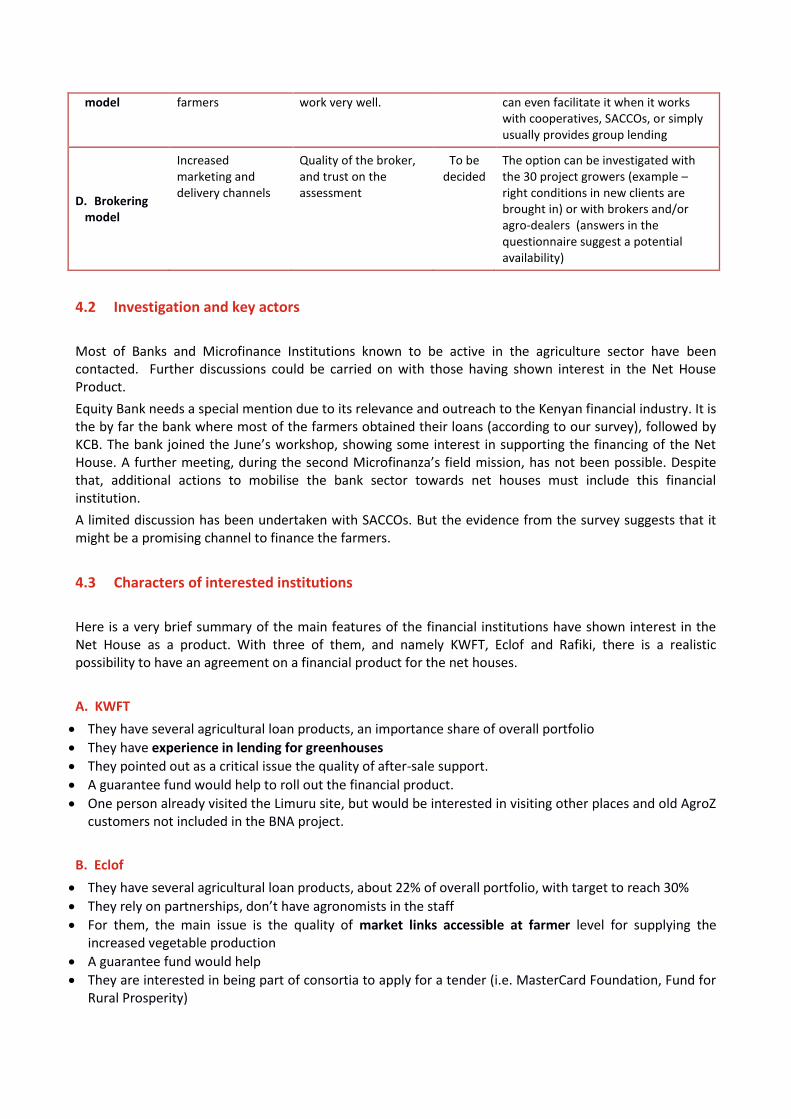

Business model Pros Cons Selected Comments

A. One stop shop model

The most comfortable solution for the customer, the most appreciated

AgroZ or the FI bear the whole risk, market and financial one.

No It might work only if AgroZ suppliers would accept to be paid in instalments, consistently with clients’ repayment to AgroZ, and this is pretty unlikely. In this way, AgroZ would pre-finance the suppliers, and this is not interesting.

B. Financial institution partnering with AgroZ

The financial institution bears the financial risk

The FSP might keep harsh conditions for clients, or be too conservative in delivering loans.

Yes FSP must buy the product and be supported in drafting an appropriate loan product for customers' needs.

A risk reduction tool for the FSP (like guarantee fund) helps mitigating loan conditions for customers

C. Group partnership

Delivery channels are closer to

Solidarity mechanisms inside the group must

To be decided

This solution can be explored on local, rather than national, basis. The FSP

model farmers work very well. can even facilitate it when it works with cooperatives, SACCOs, or simply usually provides group lending

D. Brokering model

Increased marketing and delivery channels

Quality of the broker, and trust on the assessment

To be decided

The option can be investigated with the 30 project growers (example – right conditions in new clients are brought in) or with brokers and/or agro-dealers (answers in the questionnaire suggest a potential availability)

4.2 Investigation and key actors

Most of Banks and Microfinance Institutions known to be active in the agriculture sector have been contacted. Further discussions could be carried on with those having shown interest in the Net House Product.

Equity Bank needs a special mention due to its relevance and outreach to the Kenyan financial industry. It is the by far the bank where most of the farmers obtained their loans (according to our survey), followed by KCB. The bank joined the June’s workshop, showing some interest in supporting the financing of the Net House. A further meeting, during the second Microfinanza’s field mission, has not been possible. Despite that, additional actions to mobilise the bank sector towards net houses must include this financial institution.

A limited discussion has been undertaken with SACCOs. But the evidence from the survey suggests that it might be a promising channel to finance the farmers.

4.3 Characters of interested institutions

Here is a very brief summary of the main features of the financial institutions have shown interest in the Net House as a product. With three of them, and namely KWFT, Eclof and Rafiki, there is a realistic possibility to have an agreement on a financial product for the net houses.

A. KWFT

They have several agricultural loan products, an importance share of overall portfolio

They have experience in lending for greenhouses

They pointed out as a critical issue the quality of after-sale support.

A guarantee fund would help to roll out the financial product.

One person already visited the Limuru site, but would be interested in visiting other places and old AgroZ customers not included in the BNA project.

B. Eclof

They have several agricultural loan products, about 22% of overall portfolio, with target to reach 30%

They rely on partnerships, don’t have agronomists in the staff

For them, the main issue is the quality of market links accessible at farmer level for supplying the increased vegetable production

A guarantee fund would help

They are interested in being part of consortia to apply for a tender (i.e. MasterCard Foundation, Fund for Rural Prosperity)

C. Rafiki Bank

They are recovering from Chase Bank's crisis that is the majority shareholder at Rafiki. During such crisis Rafiki's assets were frozen during the crisis. The issue seems being solved after March 2017.

They have only 3% agricultural portfolio, but the strategy plan sets a target at 30%: they showed significant interest for this opportunity.

They already worked in Climate Smart Agriculture projects, in the dairy sector.

They expect some Guarantee or similar support,

D. Cooperative bank

They work with most of SACCOs in the country

They also provide technical assistance to the creation of cooperatives

They are waiting for more information on ROI and the scale-up strategy to organise a further meeting.

The list as mentioned above is non-exhaustive of the potential partners that can be interested in providing loans to farmers in buying a Net House. It indicates the institutions that actively showed interest in the product. Annex 1 provides extensive and detailed information on all other financial institution that can either directly provide loans for the purchase of a net house, or be interested in developing dedicated financial products.

5 KEY CONDITIONS Partnerships with financial institutions could be included as one of the leading strategies for supporting those farmers financially not equipped with the necessary resources to purchase the net-house.

However, it is relevant to clarify what are the key conditions to make the net house investment appealing and affordable both for farmers and financial institutions.

5.1 Viability of the investment and ROI

Preliminary information of the Return of the Investment after the first cycle of crops, collected by ICIPE, allows an early analysis of the viability of the net house investment and the appropriate loan conditions that can be applied.

Following the hypothesis of rotation between tomato, French beans and cabbage in a plot in a one-year time, the research from ICIPE found the following difference in net margin between a net house and open field production:

YEARLY MARGIN (USD) mean min max

Net house 503 250 794

Open field 95 10 259

With this information, we can then estimate what is the added value of the net house investment by checking the additional margin generated using a net house compared to what would have been produced in open field

To check the viability of the investment, the first aspect to consider is a cost-opportunity of investing in a net house rather than using money in another way. We use the option of a fixed deposit of the same amount of money as a comparison. The Kenyan Central Bank has established a floor to fixed deposit

YEARLY MARGIN (USD) mean min max

Additionally margin net house vs open field

408 240 535

interest rate at 70% of the Central Bank’s Benchmark Rate, CBR, which has been 10% all along 2017.

We find here below the comparison of the two investments.

INVESTMENT year 1 year 2 year 3 year 4 year 5

Net house return – mean value 408,00 844,56

2 1.311,68 1.811,50 2.346,30

Net house return – maximum value 535,00 1.107,45 1.719,97 2.375,37 3.076,65

Fixed deposit at 7% 1.605,00 1.717,35 1.837,56 1.966,19 2.103,83

According to this estimate, the net house investment can overcome a standard fixed deposit investment in 4 to 6 years. Considering that the lifespan of a net house is 5 years for the net, and 10 years for the overall structure, the estimated return justifies the investment at current interest rates in Kenya.

5.2 Loan conditions

The preliminary figures on the return of investment we can estimate what financial conditions might be acceptable for the farmers. As an introduction, the following aspects are to be taken into consideration

Condition Discussion Farmers’ questionnaire and analysis

Interest rate

Famers tend to consider the 12% flat rate of SACCOs as appropriate, and the 20% declining rate of MFIs as too high. Actually, in real terms, the interest rates are almost the same so, in case of a partnership with MFIs, either communication strategies, or financial education activities for farmers, should be put in place.

Our internal analysis confirmed that farmers expect an interest rate between 10 and 15%, is not lower.

This does not necessarily mean that a standard MFI interest rate at about 20% would not be accepted (people used to borrow at MFIs know the interest rates), but some efforts either to reduce and/or explain the interest rate could be done.

Upfront payment

Microfinanza’s opinion is that an upfront payment should be asked to farmers, as it will increase farmer’s repayment attitude. Preliminary discussions seem to confirm that this is not a problem for farmers; on the contrary, it eases the burden of the loan.

Questionnaire to farmers confirmed the availability to provide an upfront payment.

Most farmers would appreciate a figure lower than 10%. However, figures up to 25% would not be a problem for about half of respondents, with the percentage rising among greenhouse and net house owners, who would be one or the primary targets of the promotion campaign

Repayment period

A grace period has to be included, allowing the farmer to start paying after the first harvest inside the net.

A grace period of at least 1-3 months, but better if up to the first harvest (3-5 months depending on the crop) would be a key element of attractiveness for the financial product

Given these conditions, we can estimate what kind of conditions are applicable, given the available information, for a financial product for net houses. It is to be kept in mind that if research on Return on the Investment provides different results, the following analysis can be integrated and modified accordingly.

2 The progression is calculated as follows: in each year the additional value from the revenue in the net house is

included, and the capital of the previous year is increased by the same 7% of the fixed deposit option

There are two ways to estimate the repayment schedule to be proposed:

1. The first is based on the added value of the investment as the sole source of funding to reimburse the loan,

2. The second is to consider the overall repayment capacity of the farmer, based on the additional revenue coming from the net house and the standard revenue that he/she is used to getting from agricultural activity.

For both options, we estimate three interest rates at an average market value: 14% declining for banks, 20% declining for Microfinance Institutions, and 12% flat for SACCOs

5.2.1 Net house added value - Repayment schedule

The analysis based on the added value of the net house is more rigorous to estimate the financial viability of the investment for a smallholder farmer, with limited resources, who does not generate important revenue from agricultural activity and wants to change this condition. This is a frequent condition among small horticulture farmers.

In this case, the repayment schedule needs to be at least three years to be paid back by the added value, in case of the maximum result, or four years, in case of the mean result.

The calculation is made in USD according to with the currency used in the ROI study and considering a 100KES=1USD exchange rate. The loan projection considers the following standard conditions

The choice to estimate a 25% upfront payment, which is higher than open field farmers’ expectation in the questionnaire, has been made in other to make the discussion on a potentially interesting, and then realistic, product for financial institutions. Moreover, this is a necessary arrangement to reduce the overall charges on loan.

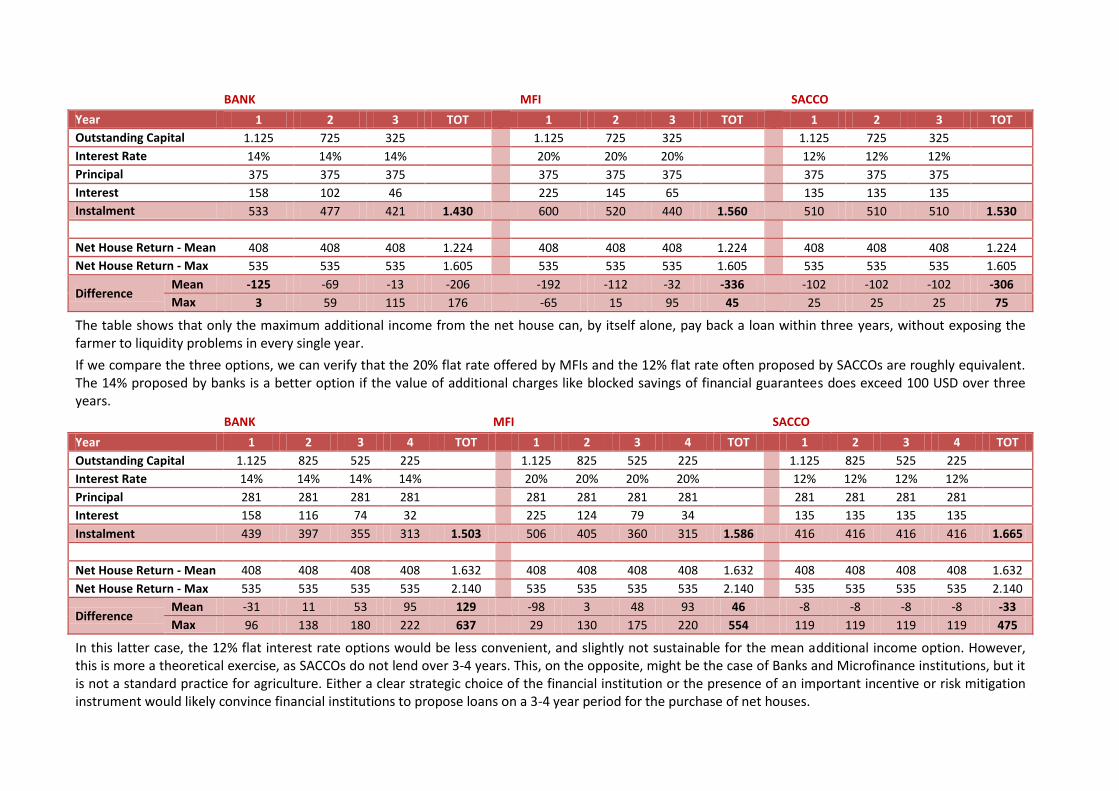

Results are summarised in the following tables:

BANK MFI SACCO

Year 1 2 3 TOT

1 2 3 TOT

1 2 3 TOT

Outstanding Capital 1.125 725 325

1.125 725 325

1.125 725 325

Interest Rate 14% 14% 14%

20% 20% 20%

12% 12% 12%

Principal 375 375 375

375 375 375

375 375 375

Interest 158 102 46

225 145 65

135 135 135

Instalment 533 477 421 1.430

600 520 440 1.560

510 510 510 1.530

Net House Return - Mean 408 408 408 1.224

408 408 408 1.224

408 408 408 1.224

Net House Return - Max 535 535 535 1.605

535 535 535 1.605

535 535 535 1.605

Difference Mean -125 -69 -13 -206

-192 -112 -32 -336

-102 -102 -102 -306

Max 3 59 115 176

-65 15 95 45

25 25 25 75

The table shows that only the maximum additional income from the net house can, by itself alone, pay back a loan within three years, without exposing the farmer to liquidity problems in every single year.

If we compare the three options, we can verify that the 20% flat rate offered by MFIs and the 12% flat rate often proposed by SACCOs are roughly equivalent. The 14% proposed by banks is a better option if the value of additional charges like blocked savings of financial guarantees does exceed 100 USD over three years.

BANK MFI SACCO

Year 1 2 3 4 TOT

1 2 3 4 TOT

1 2 3 4 TOT

Outstanding Capital 1.125 825 525 225

1.125 825 525 225

1.125 825 525 225

Interest Rate 14% 14% 14% 14%

20% 20% 20% 20%

12% 12% 12% 12%

Principal 281 281 281 281

281 281 281 281

281 281 281 281

Interest 158 116 74 32

225 124 79 34

135 135 135 135

Instalment 439 397 355 313 1.503

506 405 360 315 1.586

416 416 416 416 1.665

Net House Return - Mean 408 408 408 408 1.632

408 408 408 408 1.632

408 408 408 408 1.632

Net House Return - Max 535 535 535 535 2.140

535 535 535 535 2.140

535 535 535 535 2.140

Difference Mean -31 11 53 95 129

-98 3 48 93 46

-8 -8 -8 -8 -33

Max 96 138 180 222 637

29 130 175 220 554

119 119 119 119 475

In this latter case, the 12% flat interest rate options would be less convenient, and slightly not sustainable for the mean additional income option. However, this is more a theoretical exercise, as SACCOs do not lend over 3-4 years. This, on the opposite, might be the case of Banks and Microfinance institutions, but it is not a standard practice for agriculture. Either a clear strategic choice of the financial institution or the presence of an important incentive or risk mitigation instrument would likely convince financial institutions to propose loans on a 3-4 year period for the purchase of net houses.

5.2.2 Repayment capacity

According to the results in the questionnaire submitted to farmers and other stakeholders, farmers declare that they would be able to cover the investment of a net house, of roughly 150.000 KES, in a period within 12 and 18 months. This would be a far more attractive option for the financial institution, but we have already verified that the additional value generated by the net house investment is not enough, per se, to let farmers pay back the loan in such a time frame.

To check the viability of this option, we can compare the characteristics of a loan over 18 months at financial institutions with the savings capacity that farmers have declared in the questionnaire.

Since no reliable cost-expense calculation has been possible within the questionnaire, we chose to compare the result with the savings that farmers declared that they could generate at harvest time. It is reasonable to estimate that this figure represents the actual revenue of a farmer at harvest time, that is the part of the income still available once costs are deducted (at least production costs, while it is questionable whether other household costs are considered in this estimate).

Therefore, this exercise does not mean to check whether the additional value generated by horticulture in net houses can pay back the investment. It means to check whether Kenyan farmers, making also but not only horticulture, generally have the capacity, from their current activity, to sustain a loan to purchase a net house within 18 months, notwithstanding the additional income, and costs, generated by the net house itself.

As a term for comparison, we consider a loan of 18 months length, with monthly repayments and a grace period of 4 months, to let farmers start collecting the first harvest when payments begin. We estimated a 15%, rather than 25%, upfront payment. This latter choice is to make a product more in line with farmers' expectations. The estimate has been made in Kenyan Shillings since it is the currency that has been used in the questionnaire with farmers and other stakeholders. Loan conditions are summarised as follows

Investment 150.000 KES Upfront Payment 15% 22.500 KES Loan 127.500 KES

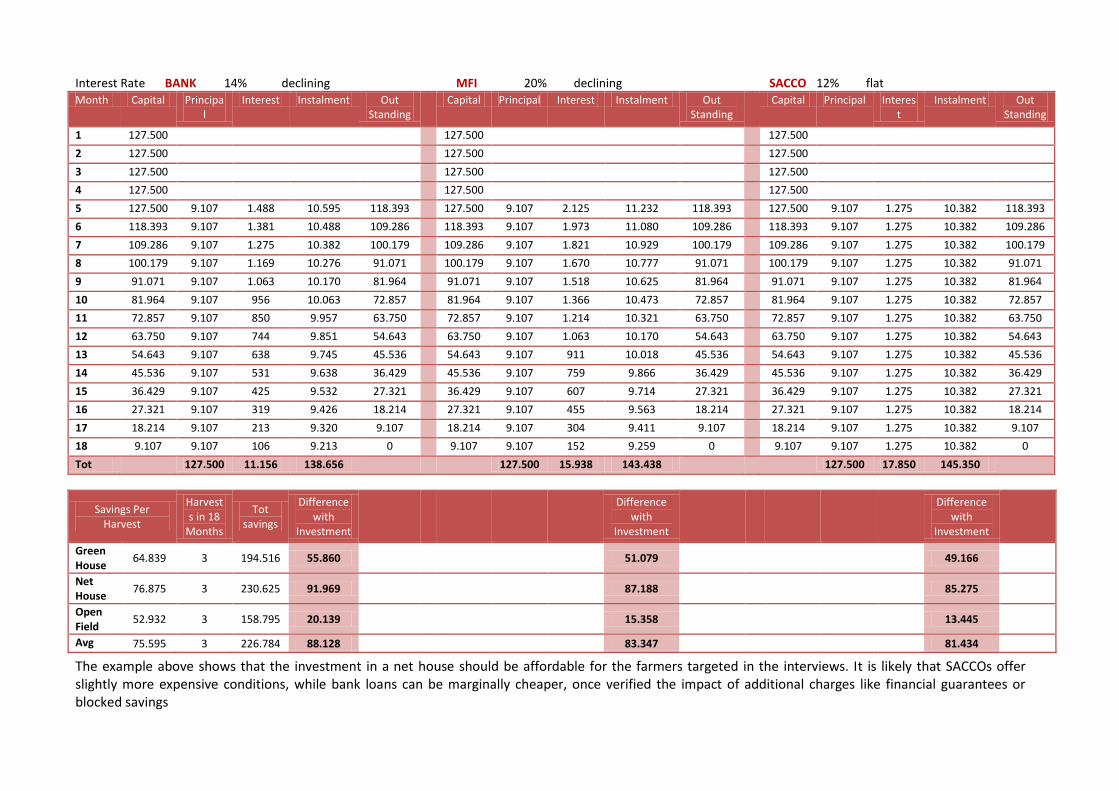

Interest Rate BANK 14% declining MFI 20% declining SACCO 12% flat Month Capital Principa

l Interest Instalment Out

Standing Capital Principal Interest Instalment Out

Tot 127.500 11.156 138.656 127.500 15.938 143.438 127.500 17.850 145.350

Savings Per Harvest

Harvests in 18

Months

Tot savings

Difference with

Investment

Difference with

Investment

Difference with

Investment

Green House

64.839 3 194.516 55.860

51.079

49.166

Net House

76.875 3 230.625 91.969

87.188

85.275

Open Field

52.932 3 158.795 20.139

15.358

13.445

Avg 75.595 3 226.784 88.128

83.347

81.434

The example above shows that the investment in a net house should be affordable for the farmers targeted in the interviews. It is likely that SACCOs offer slightly more expensive conditions, while bank loans can be marginally cheaper, once verified the impact of additional charges like financial guarantees or blocked savings

5.3 Risk reduction

Microfinanza’s experience shows that, with no risk sharing or risk reduction tool, even if an agreement is reached with the MFI, there is the clear risk that either the MFI will be too prudent to issue loans to farmers, or conditions will not be favourable for the farmers.

Moreover, the specific case of the simulation on the Kenyan context shows that an incentive is necessary for financial institutions to be able to propose financial products that match with preferences and/or necessities from the market, i.e. a repayment period over 3 years.

For risk-sharing tools, we imagine some financial instruments to cover part of the losses, or part of the costs, of the financial institutions.

5.3.1 Guarantee fund

The introduction of a guarantee fund could foster the disbursement of loans to farmers in getting the net house. This risk-mitigate tool should be established in a third party location (not at the FSPs nor AtoZ), and it would be accessible from the FSPs to mitigate their losses when some specific conditions have been respected (scope of the loan, loan conditions, follow up, etc.). In this way, the financial institution will be facilitated into absorbing the potentially higher losses that are physiologic in innovative products, and/or ensure looser loan conditions, because part of the losses do not need to be covered with income from the interest rate since the fund provides for that. Here are some key aspects of this option:

Cover part of the expected losses, not all. The MFI has to keep its share of the risk. For innovation products, we can imagine from 50% to 75% of the losses to be covered by the fund.

Farmers have to be unaware of its existence. The communication issue is a crucial aspect of the success of the fund, and a tricky issue when donors of NGOs are there. No press conferences to launch the fund!

It has to be placed in a separate place, not at the financial institution(s) issuing the loans. That means that the management of the fund has to be independent of the financial institutions granting the loans.

It can work on leverage, thus mobilising much more significant amounts. The positive aspect of the guarantee fund options is that it can provide a leverage effect of several times the size of the fund concerning lent capital.

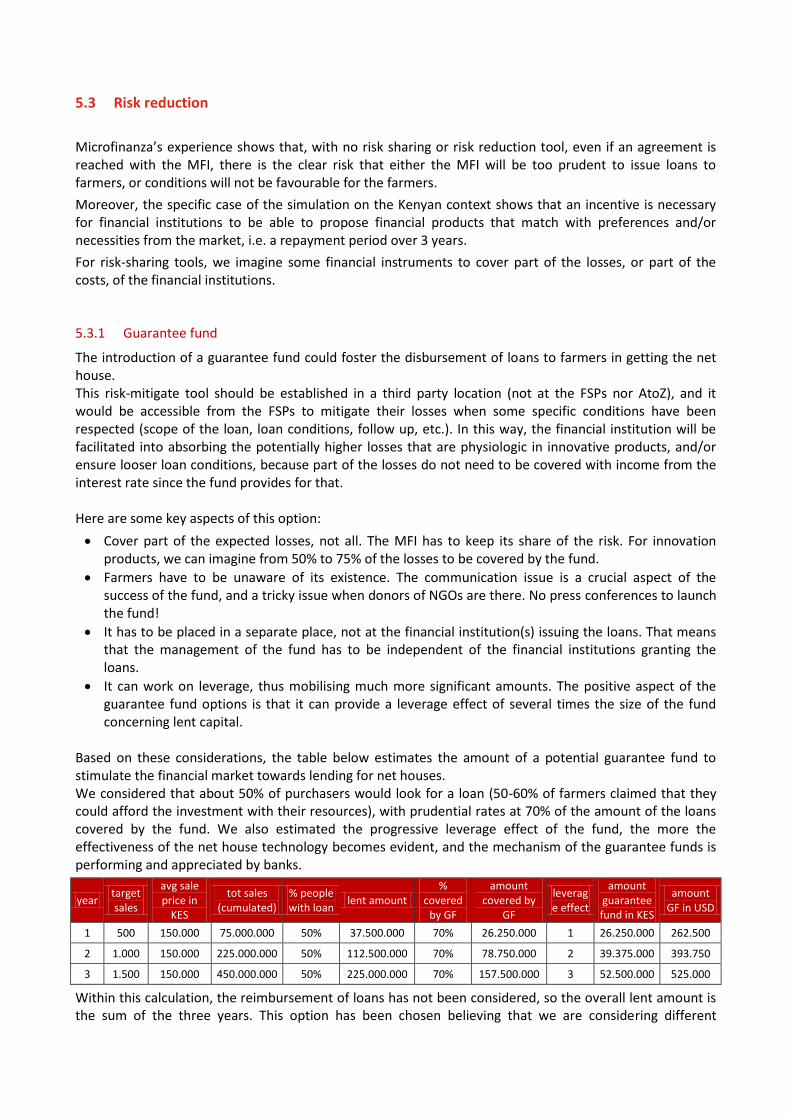

Based on these considerations, the table below estimates the amount of a potential guarantee fund to stimulate the financial market towards lending for net houses. We considered that about 50% of purchasers would look for a loan (50-60% of farmers claimed that they could afford the investment with their resources), with prudential rates at 70% of the amount of the loans covered by the fund. We also estimated the progressive leverage effect of the fund, the more the effectiveness of the net house technology becomes evident, and the mechanism of the guarantee funds is performing and appreciated by banks.

Within this calculation, the reimbursement of loans has not been considered, so the overall lent amount is the sum of the three years. This option has been chosen believing that we are considering different

potential types of loans, from 12-18 months to 3-4 years. From the fourth year, if sales are stabilised, the overall amount of the fund could be kept stable as well. In this case, the overall guarantee fund would be as big as 500-550,000 USD, generating about 2,250,000 loans, with a threefold leverage effect starting from the third year. The logic is to create a financial instrument that is sustainable over time, whose performance allows the capital to be maintained, if not even increased when proper functioning rules (eligibility criteria to the fund) and management activity (risk assessment and functioning fees) are in place.

The table does not deduct the upfront payment requested by farmers. As an example, in the event of a 10% upfront payment provided by farmers, the overall guarantee fund should be between 450.000 and 500,000 USD for the first three years

If AtoZ invests in it, even in a limited percentage, the credibility is much higher. In case of a 10% contribution from AtoZ, that would mean 45.000 to 55.000 USD to the fund. Such participation will be blocked by during the lifespan of the guarantee fund, and recollected, on a significant percentage if the management is proper, at the end of this period.

The Guarantee Fund mechanism needs some dedicated resources for the setup and its management. These additional costs should be considered in the proposal to USAID or any other donor, in addition to the overall amount of the fund.

As for above, Microfinanza can provide this service. The cost depends mainly on the number of operations that are expected each year (rather than of the size of the fund). If, part of these costs are covered by the guarantee fee applied to the banks, some additional resources should also be foreseen in a proposal for the constitution of the fund. We investigated the opportunity to increase existing funds rather than creating new ones, but so far this option does not appear possible. The latter option can reduce (partially) the cost of the operation, but mainly can be operational in a shorter time.

5.3.2 Credit lines of facilities

An alternative incentive for the financial institution can be the adoption of a credit line, or credit facility, for loans on BNA Net Houses. The credit line provides the necessary capital to issue the loans at a reduced, or no, cost. In this case, it would have a limited investment in the capital but would bear the risk of failures. At the moment, the only viable option identified it the credit line managed by MESPT. The remarkable point of the credit line is that it targets SACCOs, which are a strategic stakeholder in the project. However, more information about the functioning, size and performance of the credit line are needed to fully evaluate this option.

5.3.3 After sales and market conditions

Microfinance institutions, because of their core business, have experience and attitude on managing financial risk in the absence of real guarantee or collateral provided by their clients. Their methodology is driven by a detailed assessment, follow up, and thorough market and cash flow analysis. The financial institutions that have been involved have, anyway, mentioned some specific characteristic of the product and its market value as the most important aspect to be evaluated to invest in this product: After sales services Experience with greenhouse investment is that the reason of a significant part of the failures of this venture (KWFT had to write off 80% of greenhouse loans) was the lack of good after sale services for farmers adopting the technology. They have not, therefore, been able to benefit fully from the advantage of utilising the greenhouse and, on the contrary, suffered from the problems of the technology. For this reason, thorough technical support up to the first harvest is a key feature of the product package to be offered to farmers, both on the farmers’ and financial institutions’ interest.

This aspect is confirmed by the questionnaire to farmers, agro-dealers, brokers and extension officers: support services are a key factor of the success of the investment, and technical assistance up to the first harvest and a drip irrigation facility is the most important support services. To a lower extent, seedlings, pesticides and other products can contribute to the success of the investment. Further detail can be provided by ICIPE in its comparative study Available Market for vegetables Even taking for granted the benefit regarding quantity and quality of production with the Net House Technology, the business case for the financial institutions also includes a guarantee on the capacity to sell this vegetable production from farmers. The questionnaire provides mixed results. While farmers seem confident on the possibility to sell the additional produce in the internal Kenyan market, some farmers and other stakeholders point out the importance of diversifying delivery channels and making sure that increase production is available during the offseason to make sure that additional vegetables can be sold. The possibility to clarify, and quantify, the market for vegetables or, better, make partnerships with aggregators, buyer or exporters in the logic of contract farming will be a key aspect in easing the conditions from loans from financial institutions. From this point of view, partnerships with stakeholders like MESPT or, for some products, Illuminium Greenhouses, should be considered as a priority

6 CONCLUSIONS

Microfinanza’s understanding, based on available information, is that there are the conditions to create partnerships with financial institutions to support the scale-up of the Net House Technology.

Partnerships with financial institutions are to be preferred to an internal lending option offered directly by AtoZ for a series of reasons:

Financial institutions have a better experience in the financial assessment and the collection of reimbursement from clients;

Providing loan in a context which is different from a financial institution can hinder the repayment attitude of the clients, especially when project, donors or NGOs are somehow a part of the process and clients are aware of it;

Since the Net is less than 30% of the overall cost of the Net House Package, if AtoZ offers the financial product directly, it will pre-finance not only farmers, but also its subcontractors, and there is no economic reason for that.

Moreover, this opinion is supported by the ROI analysis, showing a clear increase in the income available to farmers adopting a net house, and also a comparative advantage of this choice rather than other financial investments.

However, it is clear that borrowing from a financial institution is one among several options that farmers have to gather resources to invest in a Net House. A scale-up strategy should take into account all farmers' strategies, being aware that access to formal finance in an actual constraint of a significant customer segment

50 to 60% of potential customers are likely to use their resources to invest in a net house, once they decide to do that. The preferred strategy is to gather resources by mobilising savings, maybe mutual savings of family members or peers, and dedicated, as an example, all the revenue of a crop to finance the investment. Such a technique can be done independently, or by using favourite informal financial tools like Chamas and Table banking. Our analysis shows that, on average, farmers can generate the necessary resources to buy a net house with 2 to 4 harvest. However, this proportion is higher among farmers already having a net house or a greenhouse.

The more the Net House Technology is scaled up to smallholder, open field, horticulture growers, the more

the possibility to accede to a loan will be critical to the success of the strategy.

When borrowing is necessary, SACCOs are the first options, and only to a second extent formal financial institution, mainly because of sophisticated communication and mutual understanding on lending conditions (especially regular repayment). However, for more substantial investment farmers tend to rely on formal financial institutions.

There’s an important aspect to be kept in mind. Microfinanza understanding is that, even though farmers can handle these multiple financial tools, there is sometimes an incomplete comprehension of the risk and advantages of all the tools, and therefore farmers can fail to compare the options and choose for the best ones. A clear example can be made on interest rate. Farmers tend to complain about high-interest rates from banks, and especially MFIs, while they believe that SACCOs' interest rates are acceptable. However, our examples show that there is no evident difference in the interest rate offered by SACCOs, but simply people fail to understand the impact of the flat rather than declining calculation method.

If activities like financial education or financial literacy are put in practice, there can be the possibility to reinforce the financial capacity of farmers, both regarding mobilisation of own resources, and of credibility towards any supporter or financial institution.

6.1.1 Strategy and way forward

Based on this considerations, Microfinanza proposes a strategy to include an effective financial component into the full scale-up strategy:

Finalize ROI analysis to verify and correct the conclusion drawn in this report. The goal is at arriving at a clear information of the necessary time to reimburse the investment thanks to the additional income generated by the Net House

Integrate the Business Plan for the Net House scale up with some agreements or arrangements of ensuring sales of the additional production with farmers. If tripartite agreements are possible (farmers, buyer and financial institution), these should be encouraged

Consider that about 50% of farmers would need a loan to adopt a Net House. This figure is likely to increase the more smallholder open field growers are targeted by the marketing strategy. On a first glance, there is the possibility to target an important proportion of farmers having the necessary resources to buy a net house

Include a guarantee fund, worth at least 500,000 USD, in the proposal to USAID for the full scale-up phase. This is critical especially for the second and third year, to make sure that selling figures can raise targeting farmers with fewer resources available. AtoZ should contribute with a 5-15% of the necessary capital to the Guarantee Fund, and the Fund should be put in place for at least 3 years’ time (better if 5 years). An additional amount between 100,000 and 150,000 USD should be considered as necessary resources for the setup and management of the guarantee fund by an external actor. It will be a matter of the consortium preparing the scale-up proposal to decide on the value for money of this option.

Based on the conditions as mentioned above and integrated information, contact financial institutions to open discussion for a real partnership. Actual numbers for the first scale-up phase do not represent a problematic investment for the financial institutions. ROI, repayment capacity, sales perspectives and existence of a guarantee fund are the key features of the strategy

Whenever possible if farmers can accede financial education activities, this can have a relevant influence on their capacity to afford the investment of a net house.

Microfinanza Srl is fully available to discuss the information included in this report and to integrate and modify the conclusions based on more accurate estimates of the ROI, sales prices and conditions, etc. Microfinanza Srl is also fully available to contribute to draw the proposal to USAID or other donors and participate in the scale-up phase of the Net House Technology by providing technical services like:

Product development for Financial Institutions

Technical Assistance with market and analysis and financial analysis

Design and Management of Guarantee Fund (if the option is considered an attractive added value to the strategy)

Financial Education

7 ANNEXES

1. Annex 1 – List of Financial Institutions with agricultural lending products in Kenya

2. Annex 2 – Market analysis questionnaire for farmers, extension officers, agro-dealers and brokers:

![.t.y.p.e.s..o.f..f.i.s.h.i.n.g. [ netting ] ( drift netting & gill netting ) [ seining ] ( purse seine and beach seine) [common in BC] ( trawling and.](https://static.documents.pub/doc/80x56/56649cbe5503460f94983eb9/typesoffishing-netting-drift-netting-gill-netting.jpg)