30

New Administrators Orientation Budget and Business Processes Lori McMahon Associate Provost for Academic Budget and Personnel July 9, 2015

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | osborne-murphy |

| View: | 221 times |

| Download: | 3 times |

New Administrators OrientationBudget and Business Processes

Lori McMahon

Associate Provost for Academic Budget and Personnel

July 9, 2015

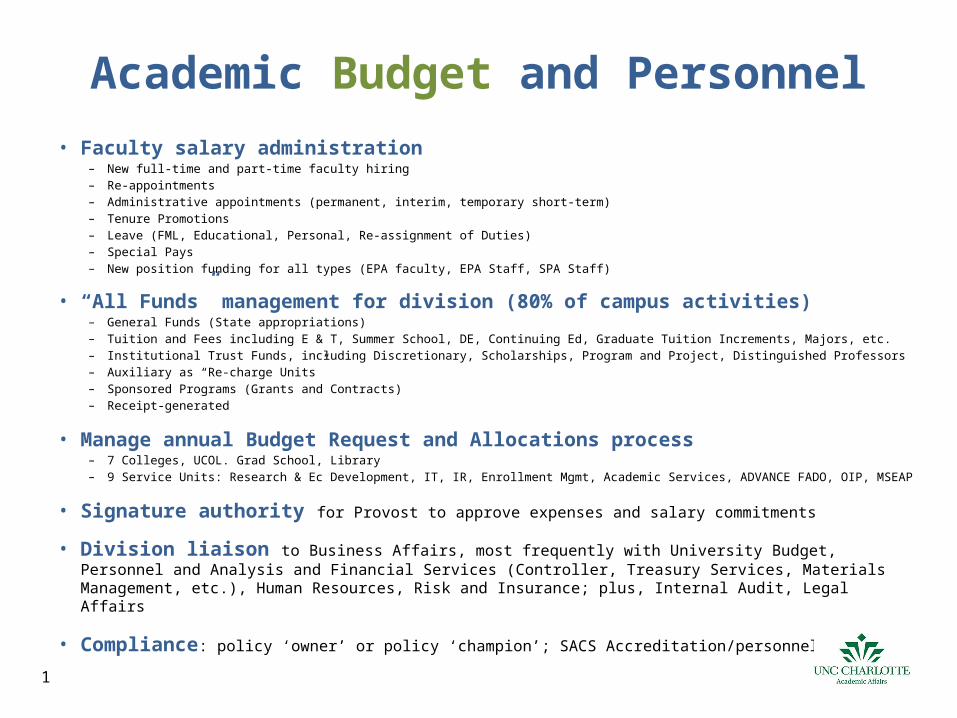

Academic Budget and Personnel• Faculty salary administration

– New full-time and part-time faculty hiring– Re-appointments– Administrative appointments (permanent, interim, temporary short-term)– Tenure Promotions– Leave (FML, Educational, Personal, Re-assignment of Duties)– Special Pays– New position funding for all types (EPA faculty, EPA Staff, SPA Staff)

• “All Funds” management for division (80% of campus activities)– General Funds (State appropriations)– Tuition and Fees including E & T, Summer School, DE, Continuing Ed, Graduate Tuition Increments, Majors, etc.– Institutional Trust Funds, including Discretionary, Scholarships, Program and Project, Distinguished Professors– Auxiliary as “Re-charge Units”– Sponsored Programs (Grants and Contracts)– Receipt-generated

• Manage annual Budget Request and Allocations process– 7 Colleges, UCOL. Grad School, Library– 9 Service Units: Research & Ec Development, IT, IR, Enrollment Mgmt, Academic Services, ADVANCE FADO, OIP, MSEAP

• Signature authority for Provost to approve expenses and salary commitments

• Division liaison to Business Affairs, most frequently with University Budget, Personnel and Analysis and Financial Services (Controller, Treasury Services, Materials Management, etc.), Human Resources, Risk and Insurance; plus, Internal Audit, Legal Affairs

• Compliance: policy ‘owner’ or policy ‘champion’; SACS Accreditation/personnel only1

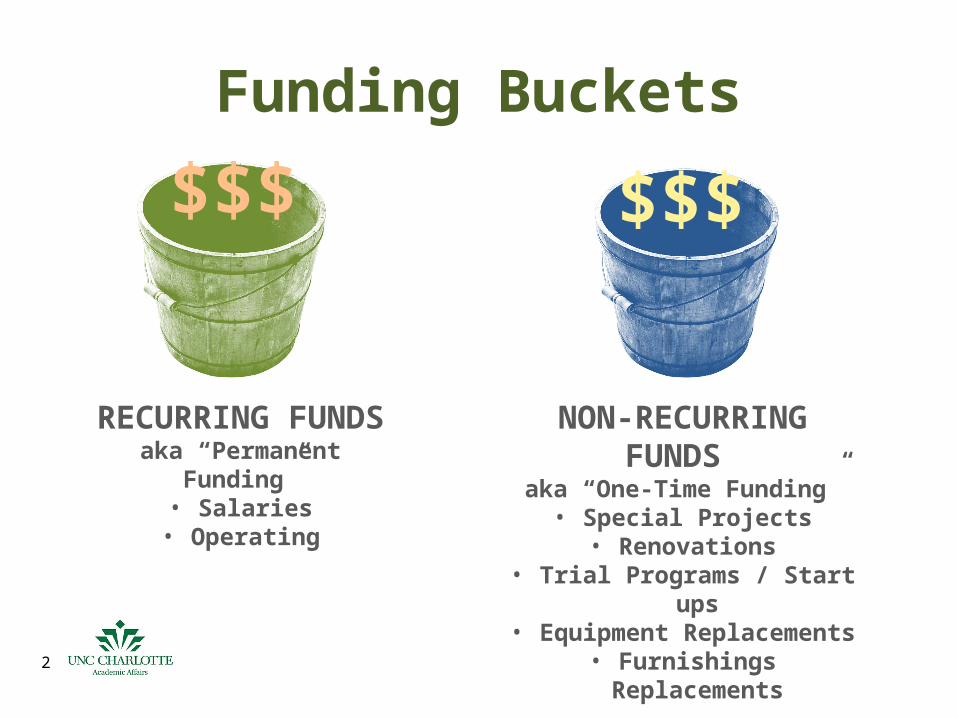

Funding Buckets

$$$ $$$

RECURRING FUNDS

aka “Permanent Funding”• Salaries

• Operating

NON-RECURRING FUNDS

aka “One-Time Funding”• Special Projects

• Renovations• Trial Programs / Start ups• Equipment Replacements

• Furnishings Replacements2

The Many Colors of Money

• Determined when money comes INTO the University.

• Cannot be changed by anyone within the University.

• Drives many accounting decisions (fund accounting) with compliance and audit implications.

3

Unrestricted Funds

• State General Funds • The total $ amount as appropriated funds to the campus • Chancellor (campus) decides how/where to further allocate and spend

• Tuition and Fee Revenue

$6,532 NC Res/UG/12+ Credit Hours• Fees are an increasing proportion of campus resources; Fee rates finalized each mid-July• Fees represent 45%(+) of what a fully enrolled in-state UG student pays for FY16• Education and Technology (E&T) Fee• Graduate Tuition Increments• Special Fees (Majors, College, Course, International Student, etc.)• General Fees (Athletics, Health Services, Debt Service)• Other Fees: ID, Food Services Facilities, Campus Security,

Transportation, Matriculation, UNC System Student Assoc• Distance Education and Summer Fees

4

Unrestricted Funds cont’d

• Institutional Trust Funds (ITF) – a mix of resources that will need to intentionally and proportionally grow to offset

pricing constraints with tuition and fees

• Unrestricted gifts– Endowment income (unrestricted endowments)– Contract/Grant residuals– Certain Conference residuals– F&A Funds (Overhead Receipts, 54.95% Faculty/Staff Regular

Research On Campus)– Sales and Services (Recharge Units, Conf. & Event fees)– Student Auxiliary funds– Student Fees

5

Restricted Funds

• Must be determined by external parties

• Institutional Trust Funds:– Grants and contracts (except exchange transactions)

– Restricted Gifts• Restricted by donor for the college or department• Can be further restricted as to how one spends the funds

(e.g. scholarships only)• Income generated from restricted endowments

• Restricted Appropriations6

Discretionary Funds

• Can be Restricted or Unrestricted

• Restricted Funds: if the outside party did not restrict funds to certain account codes (books, scholarships), funds can usually be labeled as discretionary– Must still have a business purpose and follow all the

expenditures policies and procedures of the University

• Identification of Discretionary Funds– Moving forward…New funds will be marked when newly created

as discretionary (if applicable)– Older existing funds will be reviewed at department’s request to

see if they qualify for discretionary spending7

Other Types of Funds

• Endowment funds

• Agency funds (eg. Student associations)

• Capital funds

• Debt Service funds

• Annuity and Life Income funds

• Loan funds8

Endowment Funds• True Endowment Funds

– Only created due to contribution of an outside party– Must be held in perpetuity– Only the income can be spent (interest generated from principle earnings; i.e., spending

policy)

• Quasi Endowment Funds– Restricted if formed with restricted sources– Unrestricted if formed with unrestricted sources– Function like endowments– Management/Board decision to treat funds as endowment– Generally, only income is spent, but principal can be divested upon management

decision

• Term Endowment Funds

• Treasury Services: Jane Johansen, Director, x754329

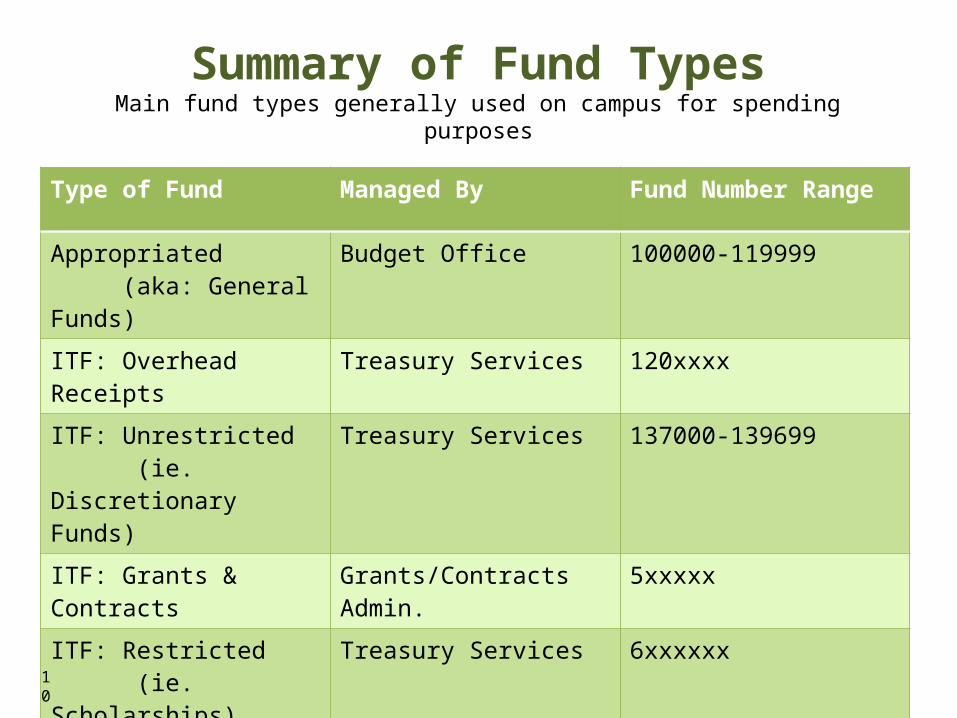

Summary of Fund TypesMain fund types generally used on campus for spending purposes

Type of Fund Managed By Fund Number Range

Appropriated (aka: General Funds)

Budget Office 100000-119999

ITF: Overhead Receipts Treasury Services 120xxxx

ITF: Unrestricted (ie. Discretionary Funds)

Treasury Services 137000-139699

ITF: Grants & Contracts Grants/Contracts Admin. 5xxxxx

ITF: Restricted (ie. Scholarships)

Treasury Services 6xxxxxx

Agency Treasury Services 83xxxx

Foundation Treasury Services N/A for Chart 1

10

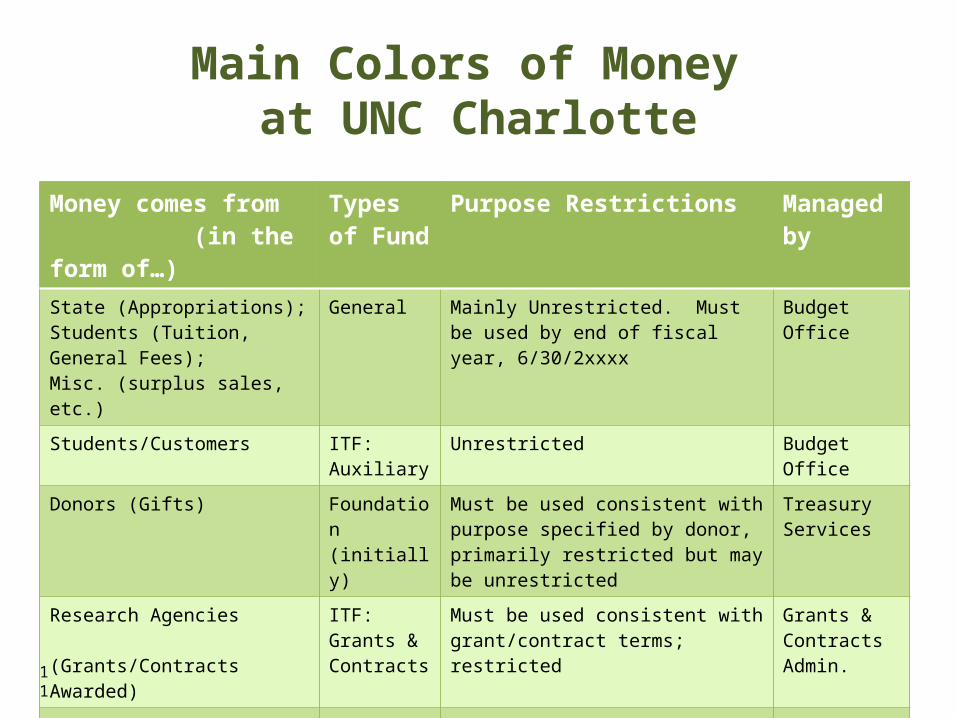

Main Colors of Money at UNC Charlotte

Money comes from (in the form of…)

Types of Fund

Purpose Restrictions Managed by

State (Appropriations);Students (Tuition, General Fees);Misc. (surplus sales, etc.)

General Mainly Unrestricted. Must be used by end of fiscal year, 6/30/2xxxx

Budget Office

Students/Customers ITF: Auxiliary Unrestricted Budget Office

Donors (Gifts) Foundation (initially)

Must be used consistent with purpose specified by donor, primarily restricted but may be unrestricted

Treasury Services

Research Agencies (Grants/Contracts Awarded)

ITF: Grants & Contracts

Must be used consistent with grant/contract terms; restricted

Grants & ContractsAdmin.

Designated Student Fees(e.g. Debt Proceeds paid from student fees)

Capital Restricted to designation Budget Office

Other ITF Depends Treasury Serv.

11

Takeaways• University Funds have different ‘use’ restrictions depending upon the

source of funds

• Discretionary Funds have the most flexibility in terms of use (e.g., food/beverages, allowable gifts or awards, gross-up honorarium payments to presenters in which department pays the individual’s taxes)

• Policy 601.8 provides spending restrictions on certain funds

• Expenditures can generally be lumped into 3 categories of allowable transactions:

1. Ordinary business expenditures

2. Unallowable/nonoperational expenditures (eg. $$ discretionary)

3. Expenditures requiring documentation (e.g., via FB&A form)

12

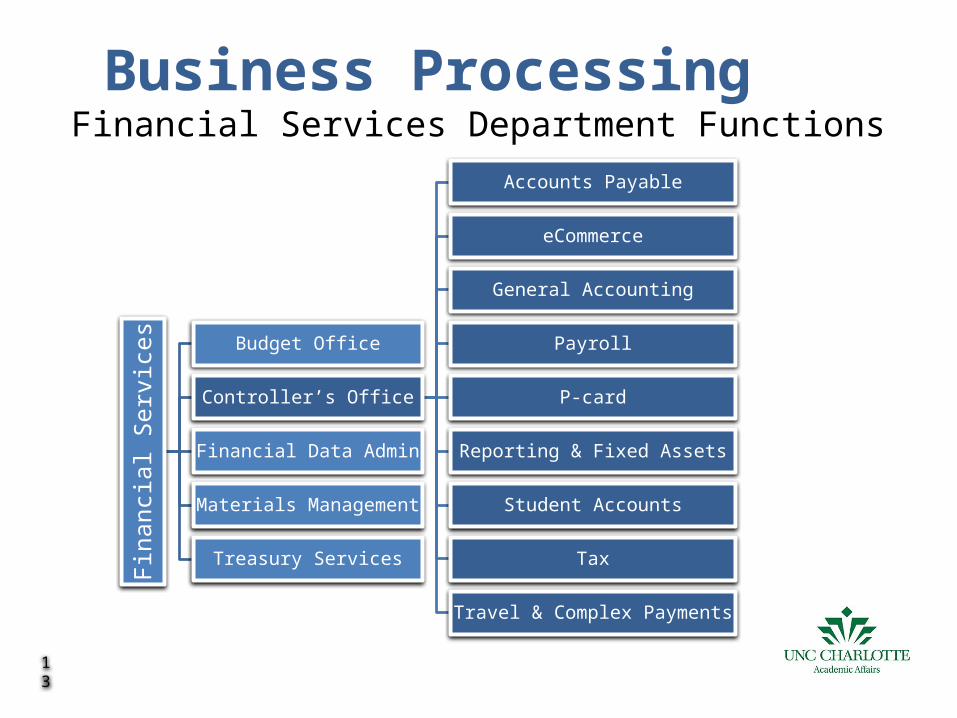

Business Processing Financial Services Department Functions

Fina

ncia

l Ser

vice

s

Budget Office

Controller’s Office

Accounts Payable

eCommerce

General Accounting

Payroll

P-card

Reporting & Fixed Assets

Student Accounts

Tax

Travel & Complex Payments

Financial Data Admin

Materials Management

Treasury Services

13

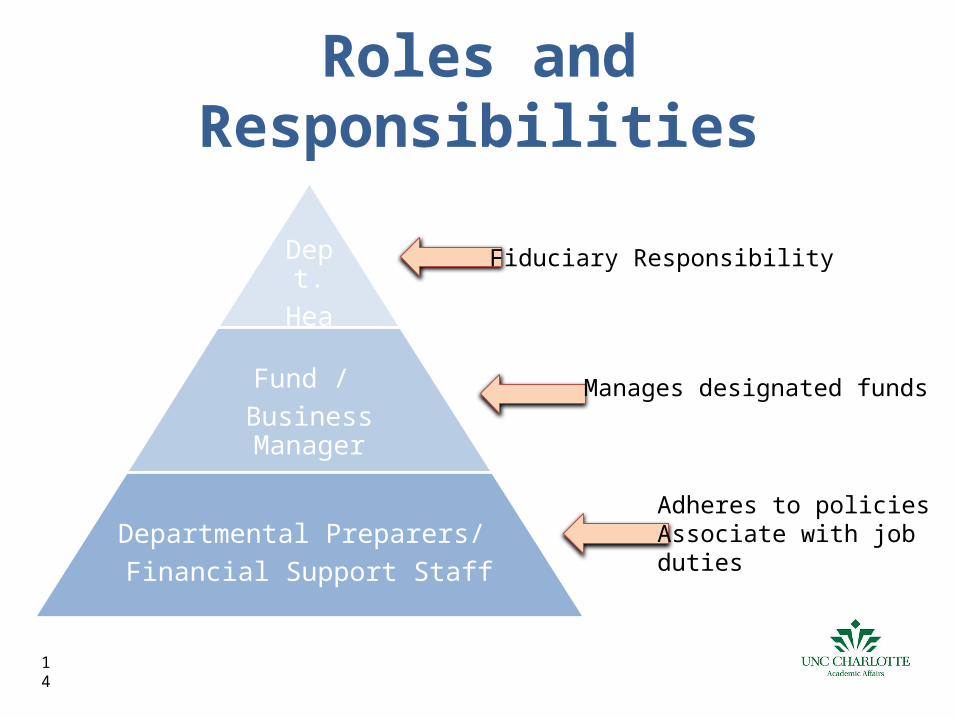

Roles and Responsibilities

Dept.Head

Fund / Business Manager

Departmental Preparers/ Financial Support Staff

Fiduciary Responsibility

Manages designated funds

Adheres to policiesAssociate with jobduties

14

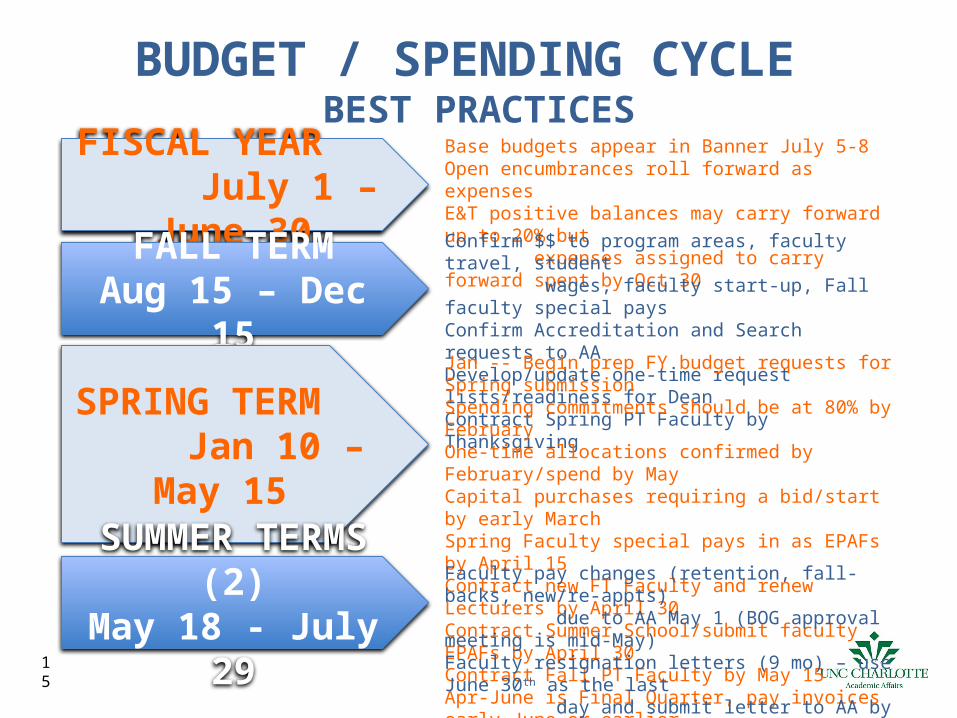

BUDGET / SPENDING CYCLE BEST PRACTICES

FISCAL YEAR July 1 – June 30

Base budgets appear in Banner July 5-8Open encumbrances roll forward as expensesE&T positive balances may carry forward up to 20% but expenses assigned to carry forward spent by Oct 30

FALL TERMAug 15 – Dec 15

SPRING TERM Jan 10 – May 15

SUMMER TERMS (2)May 18 - July 29

Confirm $$ to program areas, faculty travel, student wages, faculty start-up, Fall faculty special paysConfirm Accreditation and Search requests to AA Develop/update one-time request lists/readiness for DeanContract Spring PT Faculty by Thanksgiving

Jan -- Begin prep FY budget requests for Spring submissionSpending commitments should be at 80% by FebruaryOne-time allocations confirmed by February/spend by MayCapital purchases requiring a bid/start by early MarchSpring Faculty special pays in as EPAFs by April 15Contract new FT Faculty and renew Lecturers by April 30Contract Summer School/submit faculty EPAFs by April 30Contract Fall PT Faculty by May 15 Apr-June is Final Quarter, pay invoices early June or earlier

Faculty pay changes (retention, fall-backs, new/re-appts) due to AA May 1 (BOG approval meeting is mid-May)Faculty resignation letters (9 mo) – use June 30th as the last day and submit letter to AA by June 15th

15

Grace Murray Hopper, Ph.D.Rear Admiral, US Naval Reserve and Research Fellow in Engineering and Applied Physics at Harvard’s

Computation Laboratory. B.A Mathematics/Physics from Vassar, 1928; M.A and Ph.D. Mathematics from Yale University 1930/1934.

“It’s easier to beg

forgiveness than to get

permission.”

16

…sorry Grace, not so much in a State institution.

Faculty Special PaysUniversity Policy 101.15 -- Use appropriate fund source

“Special Pays” use lapse salary $$ from vacant faculty lines as a funding source. EPAFs should be submitted by April 30th to ensure lapse funding reports are accurate for May.

• Faculty can be paid for work not a part of their standard duties

• Short duration (pay dates match the work period)

• Conducting seminars, workshops and training in other than their home department

• Teaching continuing education or summer school courses

• Dual employment from other state agencies

• Internal grant stipends from the Office of the Provost

• University sanctioned awards

• Sponsored payments during summer term (9 or 11 mo. only)

• Other interim and temporary assignments one year or less17

Fiscal Year End Timing “Traps”

• Travel expenses incurred in May and June, reimbursements submitted after June 10

• Temp wages paid to students in June will not be paid until July of the next fiscal year

• Pcard spending must be completed by early May so expenses hit early June for payout. Pcard transactions completed in June = expenses will not pay out until next fiscal year.

• Fourth-quarter Special Pays to faculty submitted as EPAFs after May 15 wont show in a lapse report until June 8-10…this is very, very late for the college business manager to pull/spend the $$, receive goods, and close out invoicing by June 25th. $$ on the table.

• Capital equipment ($5K and over) purchasing requires a bid process that can take 12 weeks or more to complete (write bid requirements, submit to purchasing, bid is posted, vendors respond to bids, bids are reviewed/rated, vendor selected, purchase made, goods delivered, goods ‘received’ in 49er Mart, invoice submitted by vendor, invoice paid).

• “Open encumbrances” as invoices not-yet-paid need to be actively monitored. A vendor may need to be contacted directly to ensure the invoice is accurate/submitted so it can be paid by June 25th. Invoices/expenses not paid by June 30th will pay out next FY.

18

Delegation Criteria

Department Heads (Deans, Associate Provosts) who delegate financial responsibilities to a Business Manager must:

Prior to delegation --• Consider the circumstances: condition of funds, competence of potential fund

managers, and degree of supervision that will be required.• Communicate reporting and reconciliation expectations clearly and completely.• Verify the delegate’s understanding of responsibilities and capacity to execute

them.

During delegation --• Retain fiduciary responsibility for accuracy and compliance and retain

management-level decision making.• Retain open communication with delegate.• Regularly monitor and assess each delegate’s performance.

19

Financial Activity Guidelines

1) Planning– Evaluate financial consequences of activities– Evaluate anticipated costs and benefits– Re-allocate budgets where needed (strategic priorities)

2) Executing Transactions– Comply with policies, regulations, grant terms, etc.– Recorded accurately and timely– Reconciled monthly, at minimum & increasingly more frequently as 4th quarter (APRIL -

JUNE) progresses

3) Reporting

4) Training and Competence (Technical, Behavioral)

5) Corrective Actions– Timely, Clear, Specific, Documented (if needed)– If frequent, or repeated, assess need for preventive controls, additional training,

and/or sanctions20

Fund Management

Departments are responsible for managing their funds as follows:

1. Accurate financial reporting

2. Prudent, planned spending aligned with University goals and policies

3. Safeguard assets

4. Safeguard confidential and sensitive information

5. Manage finances effectively (commit 80% by February)

6. Avoid financial penalties or added costs

7. Avoid fraud

21

Accurate Financial Reporting & Analysis

Department level financial management and analysis must be completed at least monthly for the following reasons:

• Banner output is used as the basis for management decisions.

• Accounting must be accurate and timely in order for management to evaluate the status of budgets, funds, cash flow, etc.

• Budgeted labor and expenditure balances by fund and account must remain in a positive position to ensure that reporting and certifications are submitted on time to the state and budgeted cash flow is not disrupted.

• Cash flow problems may have a negative impact on vendor relationships and create complications that affect multiple departments.

• Monthly analysis and validation enable more efficient month-end and year-end close processes since corrections and other entries are made timely.

22

Accurate Financial Reporting & Analysis

Corrective Actions:If reporting exceptions continue to occur, control procedures must be implemented to correct the situation.

Examples of corrective actions include:– Revise plan or budget to reflect changed circumstances,– Change or eliminate activities,– Obtain additional funding,– Modify goals or objectives,– Correct transaction errors,– Alter future budget assumptions,– Implement new control procedures, – Document managerial decisions that depart from the budget.

Document any corrective actions taken.23

Spend Money Wisely

All purchases and payments must be:1. Prudent and in compliance with University spending policies, and 2. Within budgetary constraints3. Well planned and paced throughout the year (commit 80% by February)

UNIVERSITY POLICY 601.8, APPROPRIATE USE OF UNIVERSITY FUNDS Staff and leaders should make a thorough review of this policy to ensure that costs are allowable and charged appropriately (i.e. Food and Beverage Expense Form/attachments)

Other documents to reference requirements include: • University PURCHASING MANUAL (49erMart, Direct Payments, P-Card)• University TRAVEL PROCEDURES MANUAL (Pre-Authorization, Reimbursement)• UNC Charlotte PURCHASING CARD MANUAL• Any documents governing grant and contract terms

24

Safeguarding University Assets

Cash Handling• All cash, checks, and cash equivalents in excess of $250 are to be

deposited by noon of the next day in accordance with the North Carolina Daily Deposit Act (NC G.S. 147-77). Exceptions to this requirement are rare.– If a department receives cash and/or equivalents that cannot be readily

identified for a purpose, the department needs to contact General Accounting for direction immediately. These funds are still subject to the Daily Deposit Act.

• All petty cash and change funds must be authorized by the Controller’s Office. All cash shortages and excesses must be promptly reported to a supervisor, who must investigate them immediately. See the Petty Cash and Change Fund Procedures

25

Safeguarding University Assets

Physical Assets• A physical inventory of all equipment must be conducted on an

annual basis. All discrepancies must be promptly reported and investigated. See the Fixed Asset Guidebook.

• All thefts of University assets, including cash, must be reported to the police immediately.

Financial Records• Adjustments to asset records must be documented and approved.• Access to any forms or online resources that can be used to alter

financial balances must be restricted to only those employees requiring such access to perform their University duties.

26

Safeguarding Sensitive Information

Policy 311, Data and Information Access and Security. When dealing with University financial information, proper safeguards must be in place

to ensure the security of confidential and sensitive data

Assess Your RisksDepartment heads should assess and address risks in all

areas of their operation. Simple steps include:• Determining what information is being collected and stored, and whether there is

a business need to do so and ensuring any sensitive information is stored securely.• Limiting access• Ensuring proper information security awareness and training, especially with

credit card transactions – PCI DSS Compliance (Payment Card Industry Data Security Standards)

• Regularly reminding employees of security policies• Knowing how to handle a breach. See Policy 311.5

See SANS Security Awareness training information at:

http://itservices.uncc.edu/security/security-awareness27

Avoiding Financial Penalties & Fraud

Special Responsibility Constituent Institution” (SRCI) under G.S. 116-30.1

The University has been granted additional financial and administrative authority. If we were found to be negligent or non-compliant with how we spend funds, we would lose this critical designation.

Shared responsibilities to keep this designation:– Maintain appropriate administrative staffing, procedures and internal controls

– Resolve significant audit findings within 3 months

– Support the ability to carry out BOG-defined educational mission with our General Fund budget

– Obtain BOG approval to establish new academic, research, public service or financial aid programs sourced by the General Fund

– Measure impact on student learning and development

– Submit monthly General Fund budget reports to governing agencies28

Contacts – “ABC & T”• Academic Affairs:

Lori McMahon, Associate Provost for Academic Budget and Personnel, 7-5774 Niki Moseley, Budget Manager/General Funds (State Appropriations), 7-5772 Liezl Breitwise, Budget Manager & Analyst/Non-State Funds, 7-5521

• Budget: Budget Office website: http://finance.uncc.edu/budget-office Vacant, Assistant Budget Director, 7-5599 Carrie Smith, Budget Analyst, 7-5003

• Controller: General Accounting website: http://finance.uncc.edu/controllers-office/general-accounting Laura Williams, Controller, 7-5756 Ron Sanders, Assistant Controller, 7-5786

• Treasury Services: Treasury Services website: http://finance.uncc.edu/about-us/treasury-services Jane Johansen, Director, 7-5432 Sonja Austin, Financial Reporting and Outreach, 7-581129