36

The world leader in serving science Tom Sellig Senior VP, Global Sales Nov. 12, 2017 New Business Models for Pharma & CDMO’s

The world leader in serving science

Tom Sellig

Senior VP, Global Sales

Nov. 12, 2017

New Business Models for Pharma & CDMO’s

22 |

• CDMO Industry Defined

• Key Trends and Implications

• Impact of Mergers & Acquisitions

• New Business Models

• Pharma Market Trends and Implications

• Executive Research Results

• Surviving Inaccurate Forecasts

• Delivering Flexible & Complex Manufacturing Solution

• The Condominium Model

• Summary

Agenda

33 |

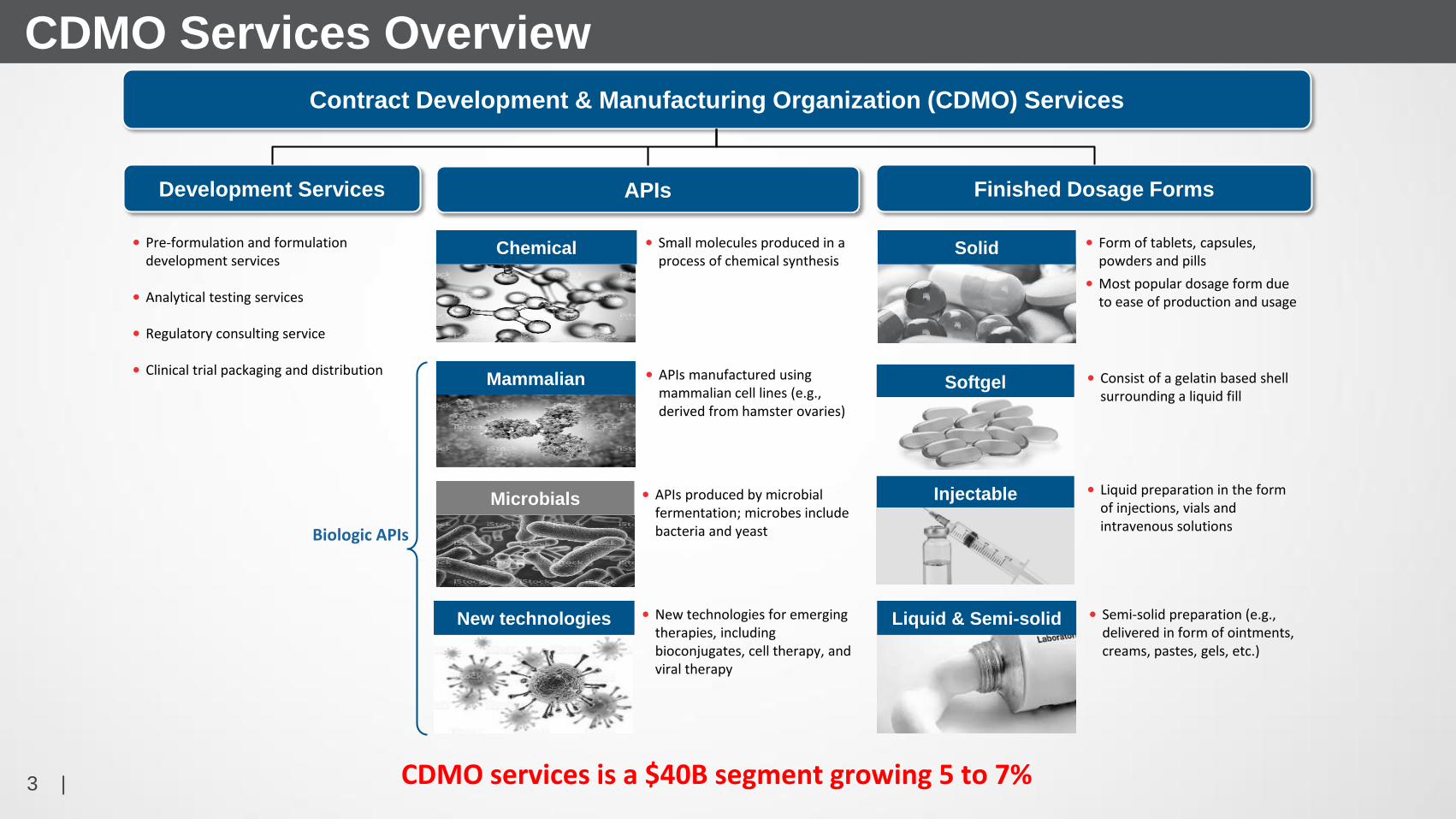

CDMO Services Overview

Contract Development & Manufacturing Organization (CDMO) Services

Development Services Finished Dosage FormsAPIs

• Form of tablets, capsules, powders and pills

• Most popular dosage form due to ease of production and usage

Liquid & Semi-solid • Semi-solid preparation (e.g., delivered in form of ointments, creams, pastes, gels, etc.)

Injectable • Liquid preparation in the form of injections, vials and intravenous solutions

Chemical • Small molecules produced in a process of chemical synthesis

Microbials • APIs produced by microbial fermentation; microbes include bacteria and yeast

New technologies • New technologies for emerging therapies, including bioconjugates, cell therapy, and viral therapy

Mammalian • APIs manufactured using mammalian cell lines (e.g., derived from hamster ovaries)

• Pre-formulation and formulation development services

• Analytical testing services

• Regulatory consulting service

• Clinical trial packaging and distribution

Biologic APIs

CDMO services is a $40B segment growing 5 to 7%

Solid

Softgel • Consist of a gelatin based shell surrounding a liquid fill

44 |

CDMO Segment Overview

Pharmaceutical Development

Services

API Manufacturing

Finished Dosage Forms

Chemical(Small Molecule)

Biologics(Large Molecule)

Description

Process development: advanced

formulation and production from

research to clinical / pilot scale

Development and manufacturing of APIs

under current Good Manufacturing

Practices (cGMP)

Commercial scale

manufacturing of small

molecule and biologic drugs

Addressable

Segment Size$2B $20B $4B $15B

Long-term Segment

Growth Rate7 to 8% 6 to 8% 10 to 11% 3 to 4%

55 |

Key trends and strategies - Emerging CMO segmentation

Global Innovators Niche Specialists Capacity-Driven

Revenues $500+ M $100+ M $10-1000 M

Market scope Global (US, EU, Japan) Home region,

some global spillover

Home region

Strategy High value, complex products;

innovative business models

New delivery of late lifecycle

and generic drugs

Fill commodity capacity

Pharmaceutics

capabilities

Broad development tool box,

range of primary dose forms,

preformulation

Specialized formulation and

delivery

Tech transfer and simple

formulation

Regulatory

capabilities

Global registrations and

QA

Global registrations and QA Regional registrations and

QA

Approvals/ portfolio NMEs, new forms

Few generics

New forms, generics, a few

NMEs

Generics, OTC

Examples Patheon

Catalent

Vetter

Fareva

Unither

Lohmann

Famar

Delpharm

Bushu

66 |

Geographic Reach of CDMO’s

77 |

CDMO Services Select PlayersPharmaceutical

Development

Services

API ManufacturingFinished Dosage

FormsChemical(Small Molecule)

Biologics(Large Molecule)

( )

( )

A HEALTHIER WORLD. DELIVERED A HEALTHIER WORLD. DELIVERED A HEALTHIER WORLD. DELIVERED A HEALTHIER WORLD. DELIVERED

( )

88 |

CDMO Segment Growth Drivers (1/2)

R&D / Technology Demographics

• Growth of new drugs in development (5% long term historical growth rate)

• Growth of companies with active drug pipelines (7% long term historical growth rate)

• 4,000+ small molecule drugs in trials with increasing demand for HPAPI and complex formulations

• Innovation in dosage forms and delivery methods (e.g., injectables)

• Growth in elderly population with an estimated 1B 60+ year-old people expected to drive $1 trillion in prescription drug sales by 2021

• Continued expansion of middle class and insured population globally

• Increasing incidence of chronic disease

Underlying Drug Demand

Strong fundamentals to support future growth

99 |

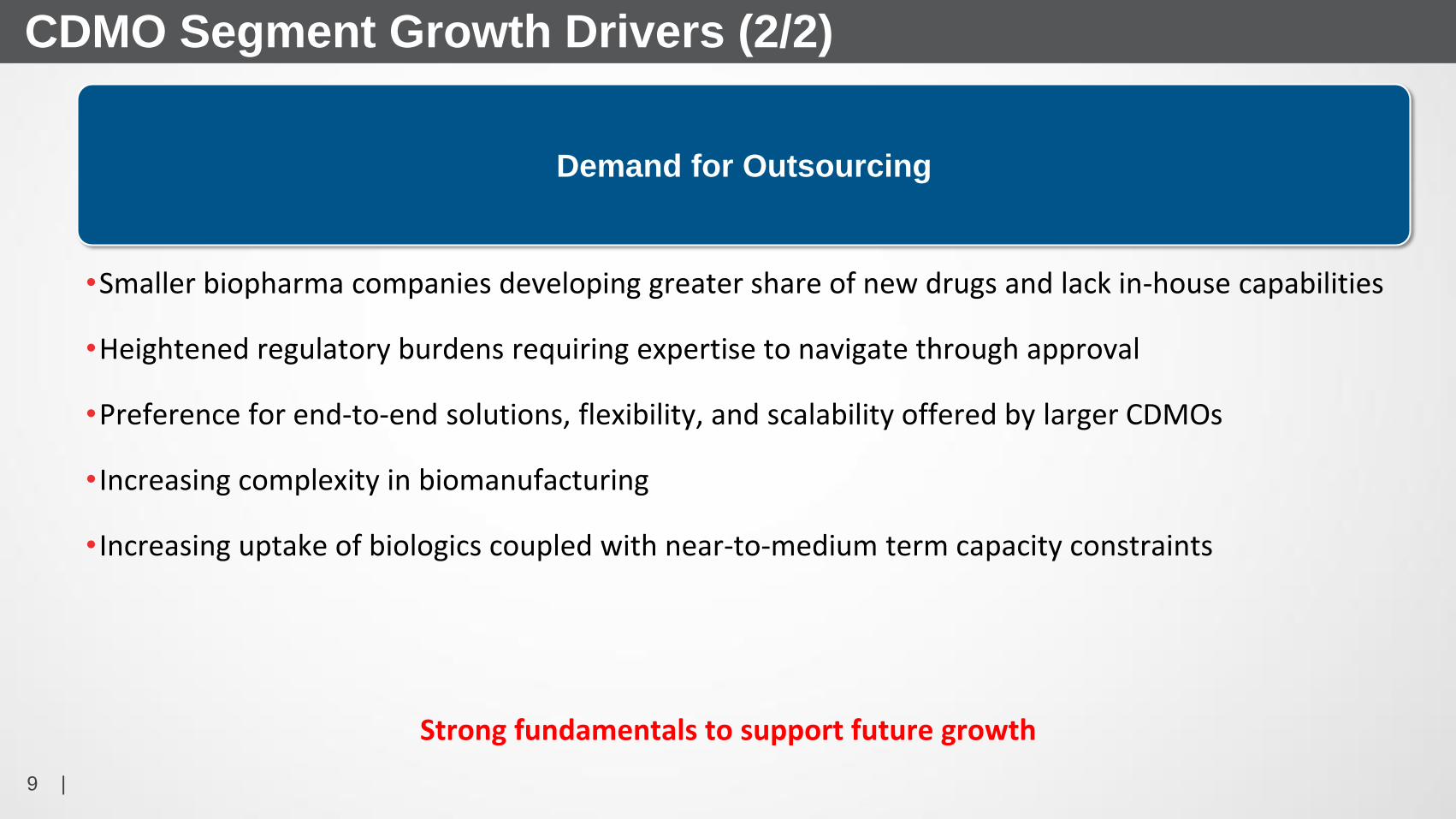

CDMO Segment Growth Drivers (2/2)

Demand for Outsourcing

•Smaller biopharma companies developing greater share of new drugs and lack in-house capabilities

•Heightened regulatory burdens requiring expertise to navigate through approval

•Preference for end-to-end solutions, flexibility, and scalability offered by larger CDMOs

• Increasing complexity in biomanufacturing

• Increasing uptake of biologics coupled with near-to-medium term capacity constraints

Strong fundamentals to support future growth

1010 |

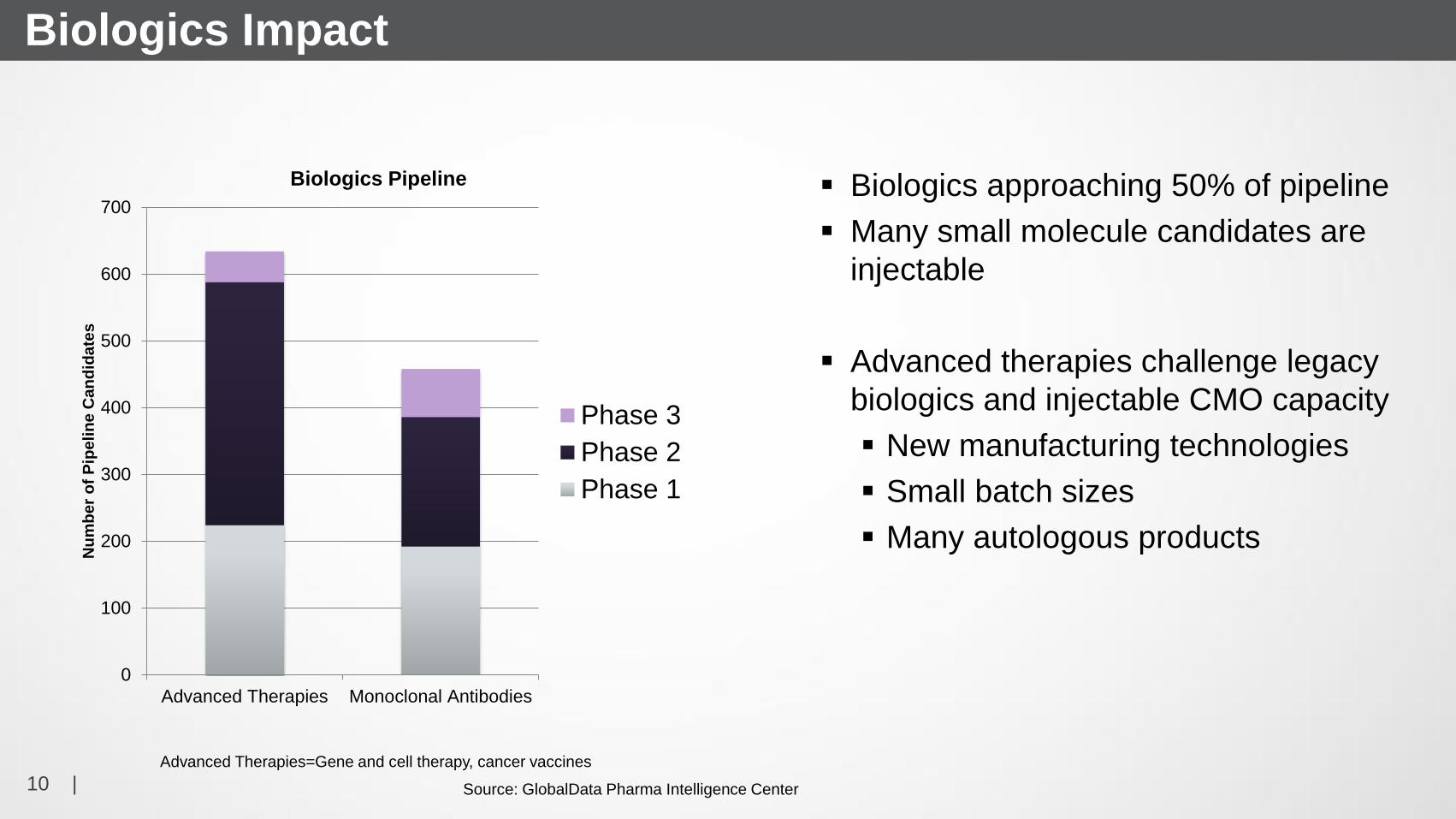

Biologics Impact

0

100

200

300

400

500

600

700

Advanced Therapies Monoclonal Antibodies

Nu

mb

er

of

Pip

eli

ne

Ca

nd

ida

tes

Biologics Pipeline

Phase 3

Phase 2

Phase 1

Biologics approaching 50% of pipeline

Many small molecule candidates are

injectable

Advanced therapies challenge legacy

biologics and injectable CMO capacity

New manufacturing technologies

Small batch sizes

Many autologous products

Advanced Therapies=Gene and cell therapy, cancer vaccines

Source: GlobalData Pharma Intelligence Center

1111 |

Outsourced FDA approvals 2012 - 2017

39

28

4148

2733

48

52

58

69

71

35

0

20

40

60

80

100

120

140

2012 2013 2014 2015 2016 2017 - 6months

NDA/BLA Approvals 2012-2017

NME Non-NME

15 16

2 1

13

19

0

5

10

15

20

25

30

35

40

NME Non-NME

Nu

mb

er

of

Ap

pro

va

ls

Dose Manufacturing of 2017 NDA/BLA Approvals

Through July

In-house Only

In & Out

Outsourced Only

57%

Out

47%

Out

Source: PharmSource STRATEGIC ADVANTAGE

1212 |

Outsourced Dosage Form Approvals

Patheon14

Vetter9

Baxter4

Pfizer3Recipharm

2

BI2

Single11

Outsourced Injectable NME Approvals 2012-2017

Patheon30

Catalent12

Fareva3

Aenova3

PCI3

Singles10

Outsourced Solid Dose NME Approvals 2012-2017

Source: PharmSource STRATEGIC ADVANTAGE

1313 |

M&A re-shaping CMC services industry

0 10 20 30 40

Multi-service

Packaging

Analytical/Formulation

BioAPI

Small API

Dose

CMC Acquisitions 2014-2017

The world leader in serving science

New Business Models to support the need of the Pharma Industry

1515 |

Demand forecasts influence manufacturing decisions for new product

launches more than all other factors.

Managing the more predictable manufacturing variables is imperative for building a strong

foundation for accurate forecasting.

Some of the more

predictable

variables in

demand forecasting

for new product

launches include:

“The manufacturing cost incurred during the whole process is the most predictable one and one

can expect to have the least amount of variance here. But as you know, it’s a very complex thing

and we don’t have sole control over it, so sometimes it becomes uncontrollable.”

–Assoc Director, Global Business Development, Large Pharma Co, US

Ingredients & raw

materials costs

Manufacturing

costs

Pricing structure

of the product

Formulation

process

1616 |

Reimbursement

rates are another

variable that is

difficult to forecast.

Actual market demand is challenging to predict and incorporate into a

new product’s demand forecast.

Market uptake and competitor strategies are highly volatile.

“You’d expect a certain type of doctor to use a product,

but you find out in the end that doctors don’t want to

prescribe it because they’re committed to using the

alternate drug. We launched an injectable that replaces

surgery. Upon launch, we found that the surgeons didn’t

want a simple, 15-minute procedure when they were

trained all their lives as surgeons - they wanted to do

surgery. Companies can do a lot of research, but sometimes there’s an unknown.”

–Sr Director of API Manufacturing, Mid-Size Pharma Co, US

Market UptakeCompetitorStrategies

In order to realistically predict market share for a new

product, companies must be cognizant of not only the

willingness of the market to adopt the product, but

also of what their competitors are doing

Physicians and consumers can respond to new

product launches in different ways that can be

difficult to predict, especially because of the lack of

structure in today’s variable pricing

ReimbursementRates

1717 |

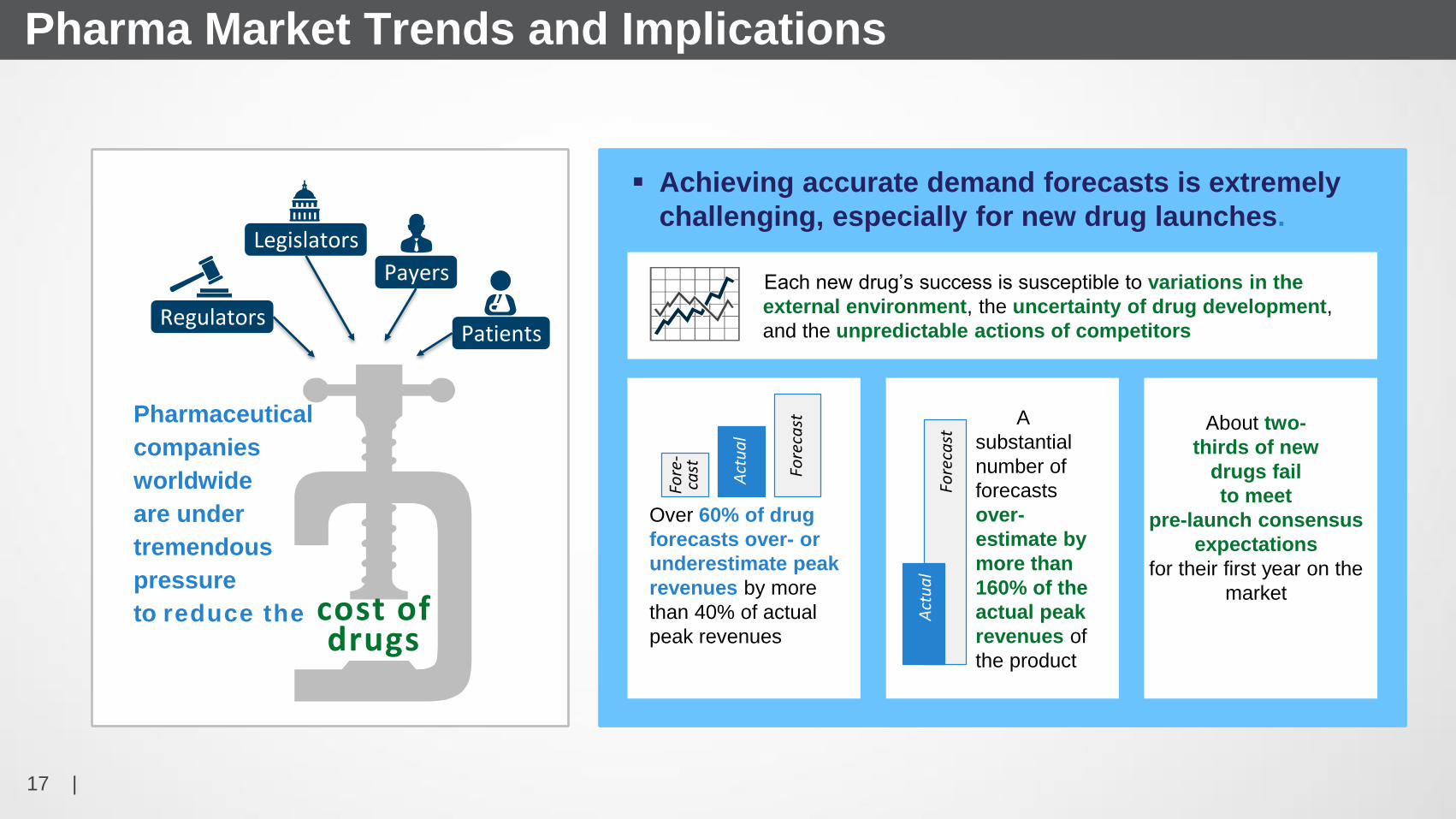

Pharma Market Trends and Implications

Pharmaceutical

companies

worldwide

are under

tremendous

pressure

to reduce the cost of drugs

Regulators

Legislators

Payers

Patients

Achieving accurate demand forecasts is extremely

challenging, especially for new drug launches.

Over 60% of drug

forecasts over- or

underestimate peak

revenues by more

than 40% of actual

peak revenues

A

substantial

number of

forecasts

over-

estimate by

more than

160% of the

actual peak

revenues of

the product

Forecast

Actual

Forecast

Actual

Fore-

cast

Each new drug’s success is susceptible to variations in the

external environment, the uncertainty of drug development,

and the unpredictable actions of competitors

About two-

thirds of new

drugs fail

to meet

pre-launch consensus

expectations

for their first year on the

market

1818 |

Implications of Forecast Uncertainty

Incorrect forecasts have serious consequences for

both operational efficiency and the bottom line.

It is estimated

that a delay in

launch costs an

average of $15

million per drug,

per day

When a

company is unable to

meet demand, the

lack of inventory can

result in…

loss of

sales

product

risk

overworked

employees

Overestimating

demand forces

manufacturers to

mark down the

price of the product

which can, in

some cases, lead to

plant closures and

employee layoffs

$15M per day

Co

sts

Inaccuracies in

demand

forecasting

increases in

complex manufac-

turing processes

combined

with

are driving a

need for more

choices in

manufacturing

solutions

1919 |

Yesterday’s approach no longer fits the new drug development landscape

30 - 40%

On new

indication for

rare or

orphan

diseases

60-90%

Of all new

compounds entering

development will

need specialized

manufacturing

High-volume, Uniform

Manufacturing Needs

TIME

PAST

Generic Generic

New Blockbuster New Blockbuster New Blockbuster

New BlockbusterNew BlockbusterNew Blockbuster

Generic GenericBiosimilar

Generic Generic Biosimilar

New Blockbuster New Blockbuster New Blockbuster

New Blockbuster New Blockbuster New Blockbuster

2014

Rare

Smaller Volumes,

Novel Manufacturing

approaches

EKG monitor

watch

EEG headset Orphan Niche Niche

2020 |

Choosing the right partner is more crucial than ever

COST TO DEVELOP

$1.188

B

2010

$1.576

B

2015

33%

SALES

$816M

2010

$416M

2015

50%

Are you certain your partner can overcome today’s barriers?

TECHNOLOGY

TRANSFER

REGULATORY MANUFACTURING

CHALLENGES

SIMPLIFYING

THE SUPPLY

CHAIN

Trends in costs and returns are upside down

2121 |

Flexible Manufacturing Business Models Deliver Value

TRADITIONAL MODEL

DEDICATED FACILITY

FRACTIONAL OWNERSHIP

GLOBAL NETWORK ACCESS

CONDOMINIUM

Fixed capacity

Flexibility in dose

form, manufacturing

process design,

continuous

manufacturing

options, etc.

Single facility for

one client total

flexibility around

capacity and use.

Suitable for multi-

product launches.

Can mix portfolio

within change part

range.

Single facility built for

2-3 clients. Flexible

capacity within defined

bands. Suitable for

clients with single or

double product launches.

Can mix product portfolio

within change part range.

Full access to capacity

within an agreed upon

notice. Ideal for clients with

uncertain manufacturing

schedules and market

demands. Facilities

pre-exist in

global network.

New facility designed

specifically to client

needs. Ideal for complex

formulations or

challenging delivery

systems. Manufacturing

runway from development

to commercial.

ENTERPRISE

For companies that own

facilities in need of

operational improvements.

Patheon can manage

these facilities while

allowing companies

to focus on their

core competencies.

2222 |

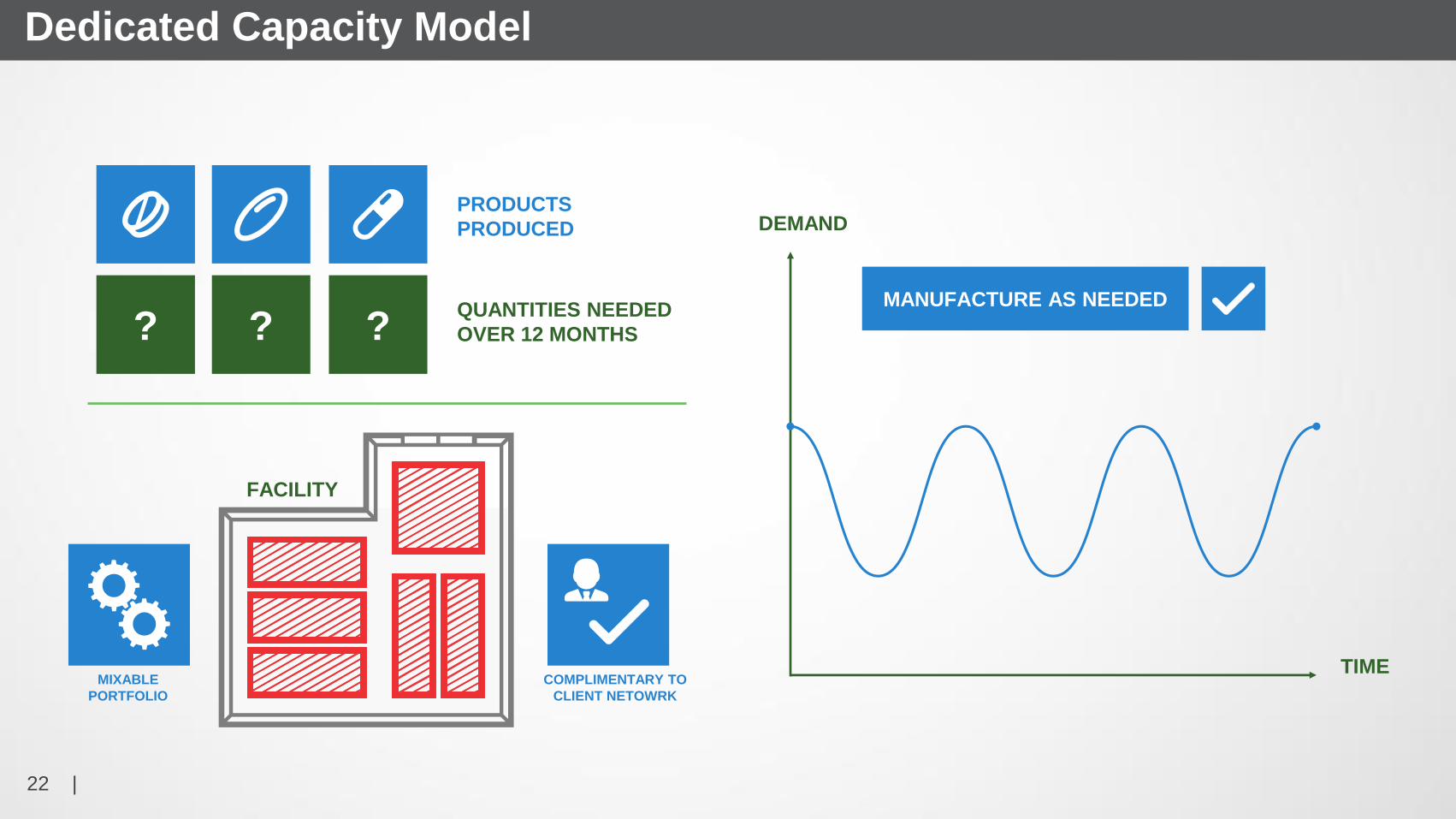

Dedicated Capacity Model

DEMAND

TIME

MANUFACTURE AS NEEDED

?QUANTITIES NEEDED

OVER 12 MONTHS? ?

PRODUCTS

PRODUCED

FACILITY

MIXABLE

PORTFOLIO

COMPLIMENTARY TO

CLIENT NETOWRK

2323 |

Fractional Ownership Model

MIXABLE

PORTFOLIO

COMPLIMENTARY T

O CLIENT NETOWRK

UNCERTAIN

QUANTITIES NEEDED

18 MONTHS

FACILITY

SECTIONS ALLOTTED

OTHER CLIENTS

DEMAND

TIME

Flexibility

2424 |

Global Network Access Model

TOTAL

PATHEON

CAPACITY

I WILL NEED THIS CAPACITY

SOMETIME SOON

RESERVED FOR YOU

APPROVAL

2525 |

Enterprise Solutions

DEMAND

TIME

MANUFACTURE AS NEEDED

?OPTIMIZE OPERATIONS

OR CLOSE FACILITIES?? ?

UNDERUTILIZED

CLIENT FACILITIES

CLIENT OWNED

FACILITIES

CLIENT FOCUSES ON

CORE COMPETENCIES

INSTEAD OF

MANUFACTURING

OPERATIONS

OPTIMIZE OPERATIONS

REFACTOR NEW LINES

CLOSE LINES

2626 |

Condominium Model

DEVELOPMENT COMMERCIAL

REQUIRES UNIQUE

PROCESS

FACILITY

SECTIONS ALLOTTED

DEMAND

TIME

FLEX PURCHASE

WITHIN BAND

CONFIDENTIAL ©2015 PATHEON®CONFIDENTIAL ©2015 PATHEON®

Patheon’s Approach to Condominium Model

2828 |

The Condominium Model

To focus on specialty products in dedicated suites in partnership with our clients, the

approach differs from the conventional CMO offering at Patheon to one known as the

CONDOMINIUM MODEL:

• Fully serviced GMP tailored facilities

• Management of novel dosage forms in conjunction with clients

• Facility design and build expertise

• Extensive complex Technology Transfer experience

• Global expert support

• Welcoming client ‘person in plant’ operation

2929 |

Possible Condo Business Models to Suit Your Strategy

• Flexible business models to match Client clinical and commercialization plans

Dedicated: Client to pay for the facility design and construction and then utilizes as

needed to meet its needs. Patheon operates and staffs the unit and supplies

product. Annual minimum revenues would be needed to support the facility

Multi-client: Client to pay for the facility and either license others or grant Patheon

license to produce products. Clients would pay a license or usage fee to Client in

addition to normal CMO charges. CMO revenues offset the minimum overall

suite revenues.

3030 |

Staged Approach to Investment / Deal

Four distinct phases:

• Construction: Suite construction, equipment ordering and IQ,OQ, PQ

• Capital and project management fees. Limited suite revenue expectations. Some dedicated resource

staffing to be covered.

• Development and Registration: Suite operation at low usage and staffing to transfer projects,

optimize, file and wait for approval

• Interim level suite fees aligned to staffing and usage. Growth of dedicated resources toward approval

• Commercial: Product validation and launch. Commercial supply and ongoing pipeline

management.

• Full suite fees apply and full staffing for microsphere suite

• Traditional CMO project development and commercial revenues for non dedicated downstream processing

• Termination: End of term or project failure. Removal of equipment

• Return suite to normal use and capability. Return all IP and dedicated equipment

3131 |

Does your CDMO offer all that you need?

Truly flexible

business

models

Unmatched

technical

capabilities

Proven excellence in technology

transferGlobal network of

locationsIndustry-leading client services

organization

3232 |

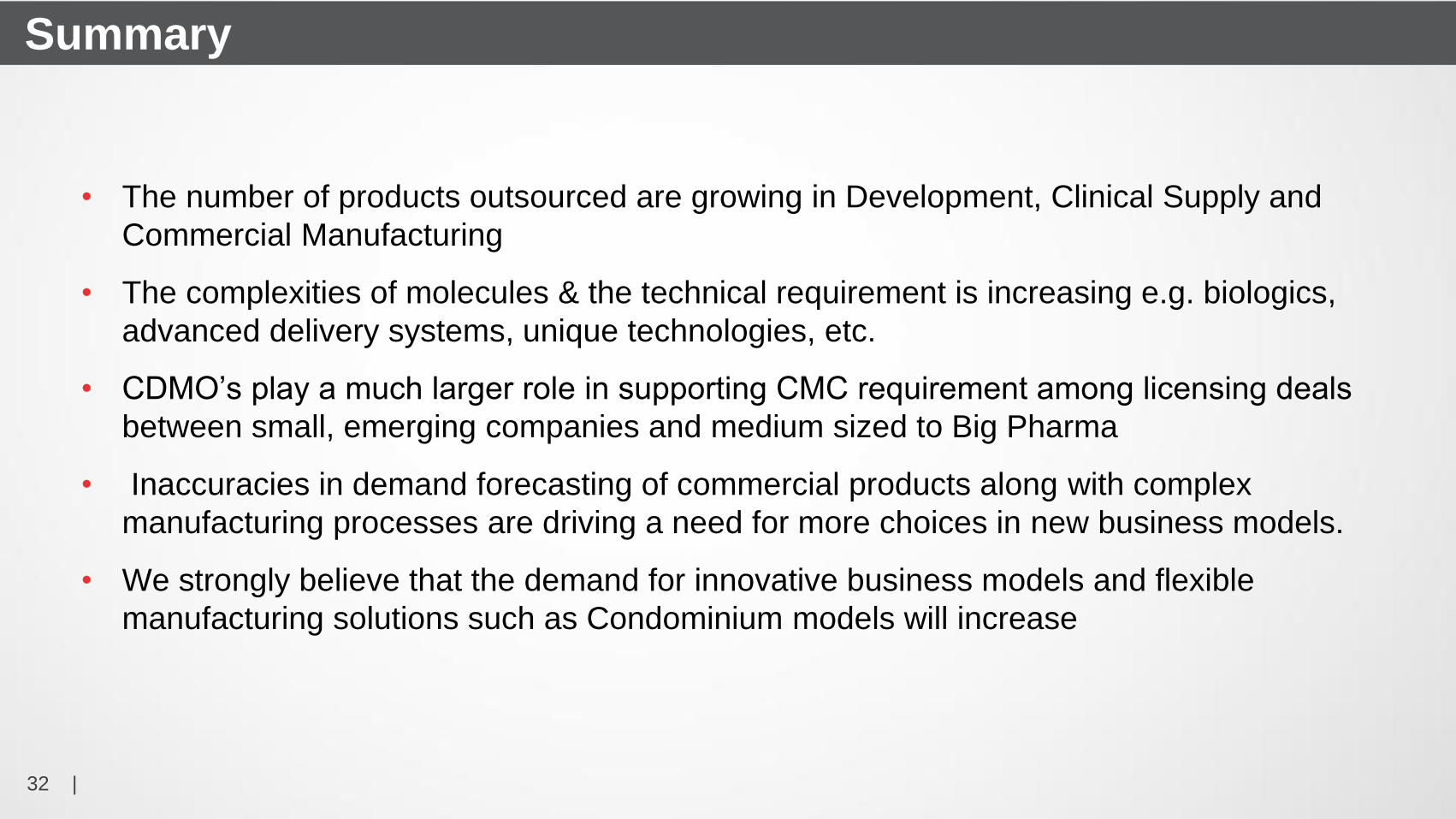

• The number of products outsourced are growing in Development, Clinical Supply and

Commercial Manufacturing

• The complexities of molecules & the technical requirement is increasing e.g. biologics,

advanced delivery systems, unique technologies, etc.

• CDMO’s play a much larger role in supporting CMC requirement among licensing deals

between small, emerging companies and medium sized to Big Pharma

• Inaccuracies in demand forecasting of commercial products along with complex

manufacturing processes are driving a need for more choices in new business models.

• We strongly believe that the demand for innovative business models and flexible

manufacturing solutions such as Condominium models will increase

Summary

3333 |

Questions

Thank You

PRESENTATION TITLE

3434 |

Thank you!

3535 |

Independent Research Results

Demand Forecast

Manufacturing Costs

Reimbursement Rates

Market Demand

Competitor Products

Raw Materials Costs

Supply of API

* Research completed by ORC International, March 2016

3636 |

Independent Research Results

The majority of companies recognize a significant

need to improve demand forecasts – they are

looking to third parties for assistance and establishing

secondary production lines as a back-up.

Almost all companies are more likely to outsource

if there is a high degree of forecast uncertainty.

The majority of companies indicated that they are

very likely to consider at least one of the new outsourced manufacturing

models, including dedicated capacity, fractional ownership, condo model,

and network options.

* Research completed by ORC International, March 2016