New Business Models (Gas Pricing & Financing) in the New Era of Gas Presented at The 7 th International Indonesia Gas Conference and Exhibition 1 Conference and Exhibition Presented by Dr. Fereidun Fesharaki Chairman, FGE January 27, 2015 This presentation material contains confidential and privileged information. The dissemination, distribution, or copying by any means whatsoever without FGE’s prior written consent is strictly prohibited.

Transcript

New Business Models (Gas Pricing &

Financing) in the New Era of GasPresented at

The 7th International Indonesia Gas

Conference and Exhibition

1

The 7 International Indonesia Gas

Conference and Exhibition Presented by

Dr. Fereidun Fesharaki

Chairman, FGE

January 27, 2015

This presentation material contains confidential and privileged information.

The dissemination, distribution, or copying by any means whatsoever without FGE’s prior written consent is strictly prohibited.

Who is FGE?� For over 30 years, FGE has delivered strategic advice on the oil and gas markets to clients around the

world. The company was the first consulting firm to specialize in the downstream oil and gas markets with

a focus on the East of Suez region.

� Over the past decades, FGE has provided studies and advisory services to national governments, national

oil and gas companies, major oil and gas companies, independent oil and gas companies, financial

institutions, international and intergovernmental organizations, utilities, consultancies, and engineering

design firms.

� FGE’s global presence enables us to service clients around the world.

Over 270 Clients Around the Globe

2

Please visit our website,

www. FGEnergy.com for more information.

Beijing

SingaporeHonolulu

Dubai

London

Main Offices

Rep/Branch Offices

Global/Asian Headquarters

TokyoCalifornia

Melbourne

Mumbai

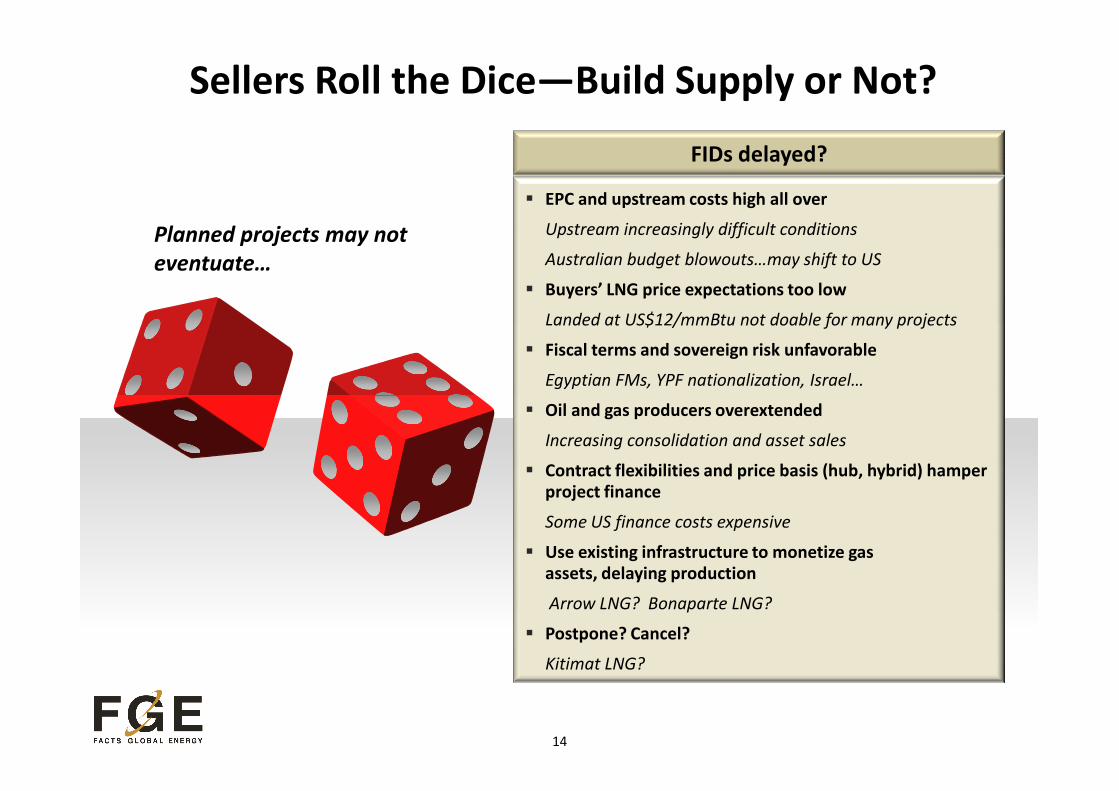

� Need for consistent integrated oil and gas policy in the era of volatile oil

prices.

� Since many new gas projects are high cost offshore gas, huge challenges

are faced by the industry to proceed forward. Incentives need to be

provided.

� Imported LNG is inevitable. Pricing of LNG imports will be much lower

New Paradigm for Indonesia

3

than expected in the past. A consistent relationship between domestic

and international prices needs to be established.

� Project financing will become more challenging in the era of lower oil

prices. There is a role for the State in facilitating and incentivizing

innovative project financing.

� There is a need to develop institutions along with policies to ensure

proper implementation, free of political wrangling.

�OPEC size addition to oil production New

� Largest producer of condensates in the world (now) New

�Amongst top 3 LNG exporters in the world (by 2020/22) New

�Top LPG exporter in the world (by 2015/16) New

The US as an Energy Superpower

4

Top LPG exporter in the world (by 2015/16) New

� Largest exporter of refined products in the world (now) New

�Emerging major petrochemical exporter (by 2020) New

�Emerging ethane exporter New

�Major coal exporter

$70

$80

$90

$100

$110

$120

$130

US$/bbl Brent (2005-2020)

Long-Term Oil Price: Finding A New Balance

5

$-

$10

$20

$30

$40

$50

$60

52005–2014: actual, forecast in $2014 thereafter

$40

$60

$80

$100

$120

US$/bbl Brent (Jan 2014-Dec 2015)

Massive Supplies Planned Post-2017…

…But Buyers Need to Commit!

500

600

700

800

900

mm

t

World Liquefaction Capacity and LNG Demand

Speculative

Planned

Under Construction

In Operation

6

0

100

200

300

400

500

mm

t

World LNG Demand

250

300

350

mm

t

Likely East Africa Exports to Asia*

Likely Canada Exports to Asia

Likely US Exports to Asia

Likely East of Suez Supply Capacity

Targeting Asia Pacific

Asia+ME Demand

2014: Supply required

from West of Suez

East of Suez LNG Market Pressure PointsEast of Suez Liquefaction Supply and LNG Demand