New Jersey Defined Contribution Retirement Plan Stan Rovinski, Prudential Retirement Counselor For Institutional Plan Sponsor Use Only

Transcript

Your Future in Focus 1 of 37 0236362-00001-00 Ed.12/2012

New Jersey Defined Contribution Retirement Plan Stan Rovinski, Prudential Retirement Counselor

For Institutional Plan Sponsor Use Only

Your Future in Focus 2 of 37

Plan Overview

Plan Contributions

Available Investment Options

Asset Allocation & Diversification

GoalMaker ® asset allocation program

Submitting Contributions

Available Resources

Table of Content

Page 3

Page 4

Page 5

Page 6

Pages 7 - 8

Page 9

Paged 10-11

For Institutional Plan Sponsor Use Only

Your Future in Focus 3 of 37

Defined Contribution Retirement Plan: Retirement benefit Group Life Insurance Long-term Disability Insurance

Eligible employees include:

Elected and appointed officials Employees earning salary in excess of “maximum

compensation” limits Part-time employees earning at least $5,000 annually

Plan Overview

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

The New Jersey Defined Contribution Retirement Plan (NJDCRP) is a retirement plan for a variety of public employees, including those who hold an elected or appointed public office. The DCRP, established July 1, 2007, provides retirement benefits for eligible employees and their beneficiaries. The Plan is a tax-qualified defined contribution money purchase pension plan under Internal Revenue Code (IRC) § 401(a) et seq., and is a “governmental plan” within the meaning of IRC § 414(d). In addition to a tax-deferred defined contribution retirement benefit, the DCRP provides eligible members with employer-provided group life insurance and group long-term disability benefits. Group Life Insurance: DCRP members are covered by employer-paid life insurance, payable to their designated beneficiaries in the amount of 1½ times the annual base salary on which DCRP contributions were based. Long Term Disability Coverage: Members are eligible for employer-paid long-term disability insurance coverage after one year of participation in the DCRP. The DCRP is administered through the Division of Pensions and Benefits and Prudential Retirement is the Plan’s recordkeeper. A Defined Contribution Retirement Program Board has also been established to oversee the program. Employees eligible to participate in the DCRP include: State or Local Officials who are elected or appointed on or after July 1, 2007; Employees enrolled in the Public Employees Retirement System (PERS) or Teachers Pension and Annuity Fund (TPAF) on or after July 1, 2007, who earn salary in excess of established “maximum compensation” limits; Employees enrolled in the Police and Firemen’s Retirement System (PFRS) or State Police Retirement System (SPRS) after May 21, 2010, who earn salary in excess of established “maximum compensation” limits; Employees otherwise eligible to enroll in the PERS or TPAF on or after November 2, 2008, who do not earn the minimum annual salary for PERS or TPAF Tier 3 enrollment ($8,100 in 2014, subject to adjustment in future years) but who earn salary of at least $5,000 annually; and Employees otherwise eligible to enroll in the PERS or TPAF after May 21, 2010, who do not work the minimum number of hours per week required for PERS or TPAF Tier 4 or Tier 5 enrollment (35 hours per week for State employees or 32 hours per week for local government or local education employees) but who earn salary of at least $5,000 annually.

Your Future in Focus 4 of 37

Employer Contributions 3.0% of base salary

Member Contributions 5.5% of base salary

Allocation of Contributions

Participants choose allocations If no choice is made, invested in default fund

Plan Contributions

You are immediately vested in your own contributions. Employer contributions are vested after 12 months of service.

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

Employer Contributions The DCRP employer contribution rate has been set at three percent of base salary.* Base salary means the annual compensation of a member, plus the value of maintenance, if applicable, in accordance with contracts, ordinances, resolutions or other established salary policies of the member's employer for all employees in the same position, or all employees covered by the same collective bargaining agreement, which is paid in regular, periodic installments in accordance with the payroll cycle of the employer. Overtime, bonuses, and lump sum payments for longevity, holiday pay, vacation, compensatory time, or accumulated sick leave are NOT included as base salary. Member Contributions Each employer picks up employee contributions for all base salary paid with respect to enrolled participants. The employee contributions so picked up are treated as employer contributions pursuant to IRC § 414(h)(2).The employer pays the picked up contributions directly to the DCRP, instead of paying such amounts to the participants, and such contributions are paid from the same funds that are used in paying salaries to participants. Such contributions, although designated as employee contributions, are paid by the employer in lieu of contributions by participants. Participants may not elect to receive such contributions directly instead of having them paid by the employer to the DCRP. Employee contributions so picked up are treated for all purposes of the DCRP and State law, other than federal tax law, in the same manner as employer contributions made without a pick up. By law (Chapter 103, P.L. 2007), the DCRP member contribution rate is set at 5.5 percent. The employer deducts member contributions from the applicable salary. These contributions, along with the employer contributions, are put into the DCRP participant's tax-deferred investment account established with the DCRP's administrative services provider, Prudential Retirement. Participants are allowed to allocate their contributions and the contributions of their employer into the investment choices determined by the DCRP Board. If a participant does not select an investment allocation, their contributions will be invested in the default as defined by the Plan.

Your Future in Focus 5 of 37

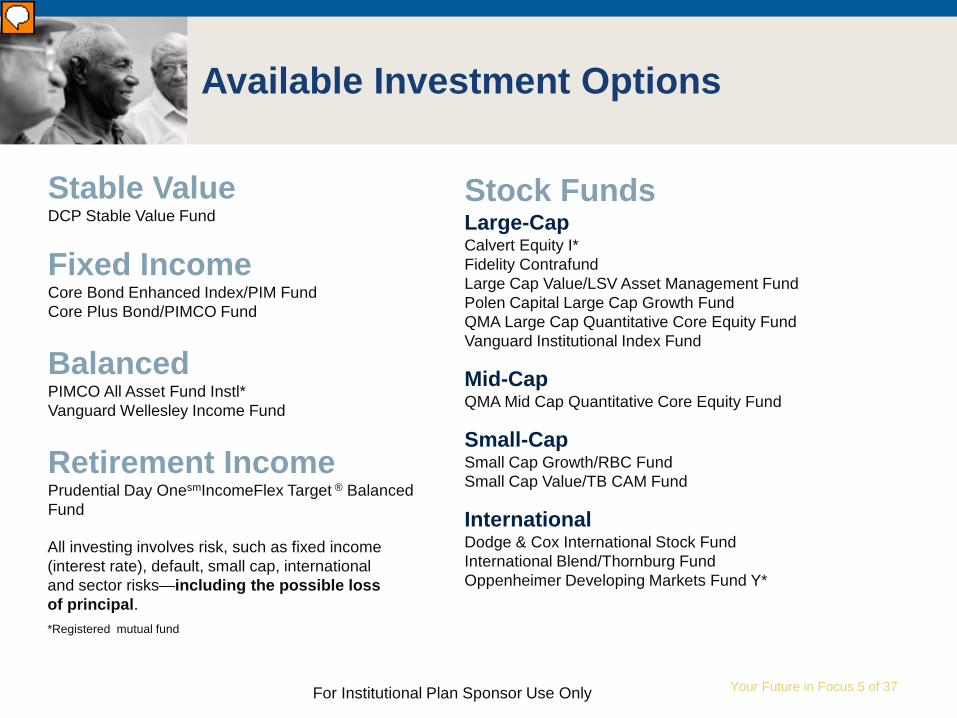

Available Investment Options

Stock Funds Large-Cap Calvert Equity I* Fidelity Contrafund Large Cap Value/LSV Asset Management Fund Polen Capital Large Cap Growth Fund QMA Large Cap Quantitative Core Equity Fund Vanguard Institutional Index Fund

Mid-Cap QMA Mid Cap Quantitative Core Equity Fund

Small-Cap Small Cap Growth/RBC Fund Small Cap Value/TB CAM Fund

International Dodge & Cox International Stock Fund International Blend/Thornburg Fund Oppenheimer Developing Markets Fund Y*

Stable Value DCP Stable Value Fund

Fixed Income Core Bond Enhanced Index/PIM Fund Core Plus Bond/PIMCO Fund

Balanced PIMCO All Asset Fund Instl* Vanguard Wellesley Income Fund

Retirement Income Prudential Day OnesmIncomeFlex Target ® Balanced Fund

All investing involves risk, such as fixed income (interest rate), default, small cap, international and sector risks—including the possible loss of principal. *Registered mutual fund

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

The investment options available in the DCRP are shown here. Remember: participants are allowed to allocate their contributions and the contributions of their employer into these investment choices. If a participant does not select an investment allocation, their contributions will be invested in the default as defined by the Plan—which is the DCP Stable Value Fund. This is an important point, because participants are automatically enrolled in the DCRP. This means that many of them fail to select an investment allocation. This is something that the Division of Pensions and Benefits and Prudential try to address by reaching out to participants on an ongoing basis.

Your Future in Focus 6 of 37

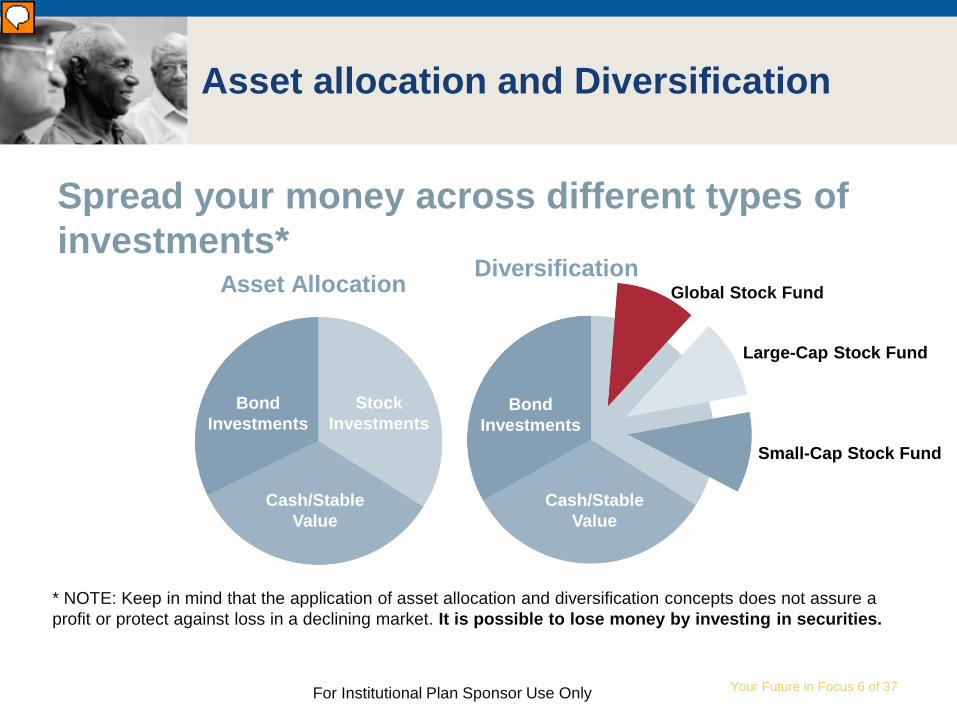

Spread your money across different types of investments*

Diversification Asset Allocation

Bond Investments

Stock Investments

Cash/Stable Value

Bond Investments

Cash/Stable Value

Global Stock Fund

Large-Cap Stock Fund

Small-Cap Stock Fund

* NOTE: Keep in mind that the application of asset allocation and diversification concepts does not assure a profit or protect against loss in a declining market. It is possible to lose money by investing in securities.

Asset allocation and Diversification

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

An important concept when it comes to managing investment risk is called asset allocation. Asset allocation is simply the process of spreading your money across different types of asset classes—stock, fixed income and stable value investments. By dividing your portfolio among a variety of investment classes, you minimize your reliance on any one investment and help manage your investment risk. Historically, the markets move in cycles—generally, when one kind of investment is performing well, another may not be performing as well. Changing economic and financial market conditions affect asset classes differently. And, since you don’t know which asset class will perform well next year or the year after, having a variety of asset classes in your portfolio may help you to better weather the rough spots in the market.

Your Future in Focus 7 of 37

Participants provide… • Their expected retirement age • Their investor style • Desire for income protection

Participants get… • Automatic asset allocation • Automatic rebalancing • Automatic age adjustment • Automatic income protection

Introducing GoalMaker

Keep in mind that application of asset allocation and diversification concepts does not assure a profit or protect against loss in a declining market. It is possible to lose money by investing in securities.

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

Because asset allocation is so important, the DCRP offers a tool that participants can use to help them select an investment allocation. It’s called GoalMaker, and it’s an optional asset allocation program available at no additional cost. GoalMaker is designed to help participants make investment selections quickly and easily. GoalMaker uses two simple pieces of information: the participant’s expected retirement age and their investor style—conservative, moderate, or aggressive—to guide them, for their consideration, to a professionally designed model portfolio made up of investments available in the plan. Once the participant selects their model portfolio, GoalMaker will automatically rebalance their investment mix and shift it over time as they near retirement. And, if the participant wants lifetime retirement income, GoalMaker with IncomeFlex Target can help with that, too.

Your Future in Focus 8 of 37

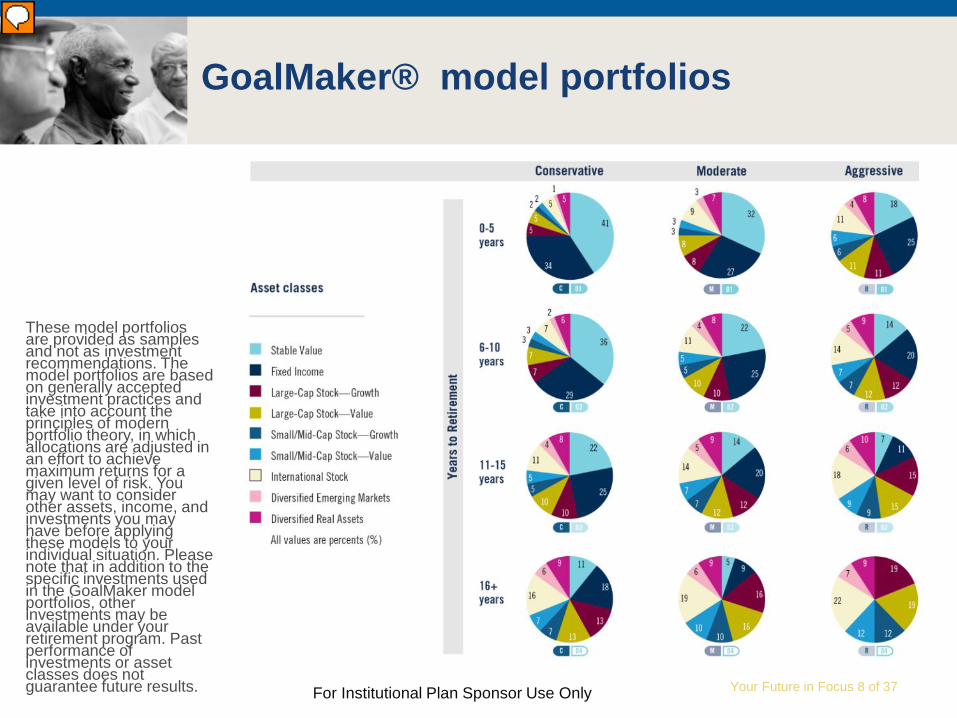

GoalMaker® model portfolios

These model portfolios are provided as samples and not as investment recommendations. The model portfolios are based on generally accepted investment practices and take into account the principles of modern portfolio theory, in which allocations are adjusted in an effort to achieve maximum returns for a given level of risk. You may want to consider other assets, income, and investments you may have before applying these models to your individual situation. Please note that in addition to the specific investments used in the GoalMaker model portfolios, other investments may be available under your retirement program. Past performance of investments or asset classes does not guarantee future results. For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

The sample portfolios on this slide show the percentage of stable value, fixed income (bonds), and stock/equity investments that correspond to certain investor styles and years to retirement. Participants can use the information from the sample portfolios to help determine a mix of investments from among those options in the DCRP. GoalMaker’s Automatic Rebalancing feature will automatically adjust a participant’s portfolio on a regular basis to match their chosen target portfolio. And, through an optional feature called automatic age adjustment, GoalMaker will adjust investments over time. As a participant approaches retirement, their GoalMaker portfolio automatically adjusts to become more conservative. That’s important because the closer they are to retirement, the more conservative they may choose to be as their priorities may shift and focus more on preserving the money they’ve saved over the years.

Your Future in Focus 9 of 37

Submitting Contributions

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

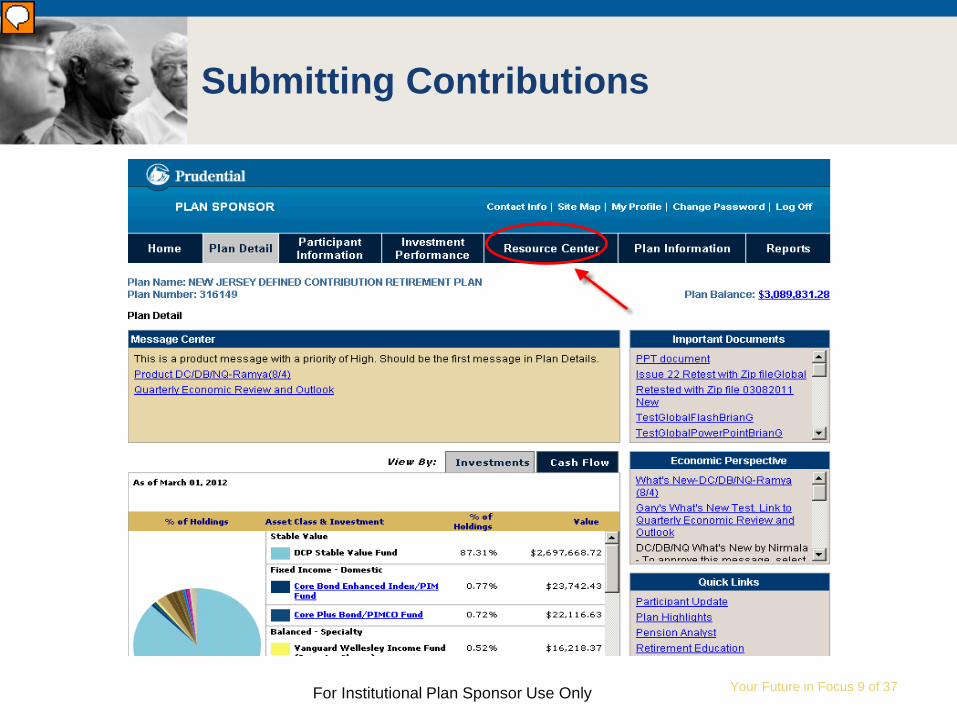

Employers must submit contributions using Prudential's Online Retirement Center for Plan Sponsors. The procedure for submitting contributions in this manner is outlined in a presentation available online. You see an image of the Plan Sponsor website here. The process involves these steps: Log on to the Plan Sponsor Website at www.prudential.com/sponsor Create a new batch Input data Verify totals Transmit batch to Prudential Confirm file was sent

Your Future in Focus 10 of 37

Division of Pensions and Benefits website www/state.nj.us/treasury/pensions

Fact Sheet #79, DCRP for PERS, TPAF, PFRS and SPRS Members

Fact Sheet #80, DCRP for Elected and Appointed Officials Fact Sheet #82, DCRP if ineligible for PERS or TPAF

Prudential Retirement 1-800-932-0432. Enter DCRP Plan # 316149.

Press #1 for Jeff Beilman or #2 for Linda Mangan.

Available Resources for Employers

For Institutional Plan Sponsor Use Only

Presenter

Presentation Notes

Additional resources are available regarding the DCRP. The Division of Pensions and Benefits provides information about the DCRP online at www.state.nj.us/treasury/pensions: Fact Sheet #79, Defined Contribution Retirement Program (DCRP) for PERS,TPAF, PFRS, and SPRS Members Fact Sheet #80, Defined Contribution Retirement Program (DCRP) for Elected and Appointed Officials Fact Sheet 82, Defined Contribution Retirement Program (DCRP) if Ineligible for PERS or TPAF For questions regarding contribution remittance or administrative issues, you may contact Prudential Retirement at 1-800-932-0432. If participants would like a consultation, please have them contact me, Stan Rovinski, at 609-218-3601.

Your Future in Focus 11 of 37

Prudential Retirement 1-866-NJDCRP1 (1-866-653-2771) www.prudential.com/njdcrp Stan Rovinski (609) 218-3601 or [email protected]

Available Resources for Participants

For Institutional Plan Sponsor Use Only

Your Future in Focus 12 of 37

Questions? [ ]

For Institutional Plan Sponsor Use Only

Your Future in Focus 13 of 37

Investors should consider the fund's investment objectives, risks, charges and expenses before investing. The prospectus, and if available the summary prospectus, contain complete information about the investment options available through your plan. Please call 1-866-657-3327 for a free prospectus and if available, a summary prospectus that contain this and other information about our mutual funds. You should read the prospectus and the summary prospectus, if available carefully before investing. It is possible to lose money when investing in securities.

Shares of the registered mutual funds are offered by Prudential Investment Management Services LLC (PIMS), Three Gateway Center, 14th Floor, Newark, NJ 07102-4077. PIMS is a Prudential Financial company. Stan Rovinski, Linda Mangan and Jeff Beilman are are registered representatives of PIMS. The Prudential IncomeFlex Target Fund is a separate account under a group variable annuity contract issued by Prudential Retirement Insurance and Annuity Company (PRIAC), Hartford, CT.PRIAC does not guarantee the investment performance or return on contributions to the separate account. You should consider the objectives, risks, charges, and expenses of the Fund and guarantee features before purchasing this product. Like all variable investments, this fund may lose value. Availability and terms may vary by jurisdiction; subject to regulatory approvals. For this and other information, please visit www.prudential.com/njsedcp or call 1-866-NJSEDCP (1-866- 657-3327) for a copy of the Prudential IncomeFlex Target® Important Considerations before investing.

Guarantees are based on the claims-paying ability of the insurance company and are subject to certain limitations, terms, and conditions. Annuity contracts contain exclusions, limitations, reductions of benefits and terms for keeping them in force. Contract form #GA-2020-TGWB4-0805-NJ. PRIAC is solely responsible for its financial condition and contractual obligations.